AI In Pharmacovigilance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.98 Billion |

| Market Size (2031) | USD 2.70 Billion |

| Growth Rate (2026 - 2031) | 22.50% CAGR |

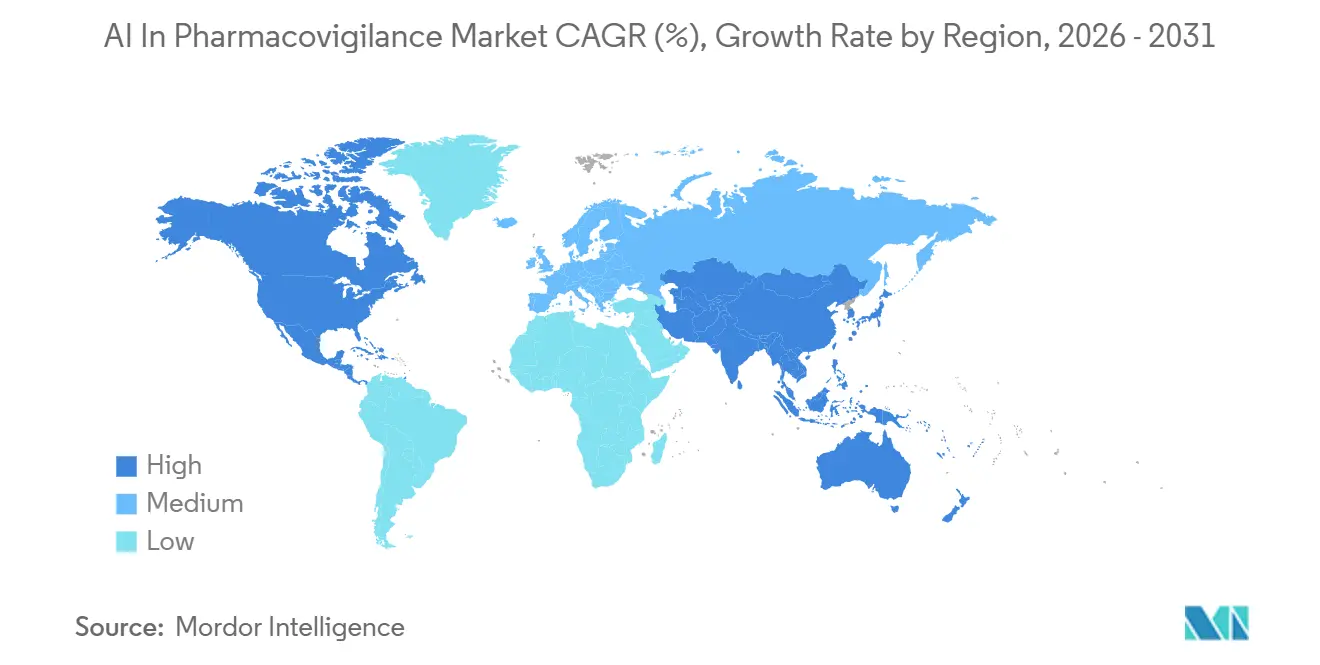

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Pharmacovigilance Market Analysis by Mordor Intelligence

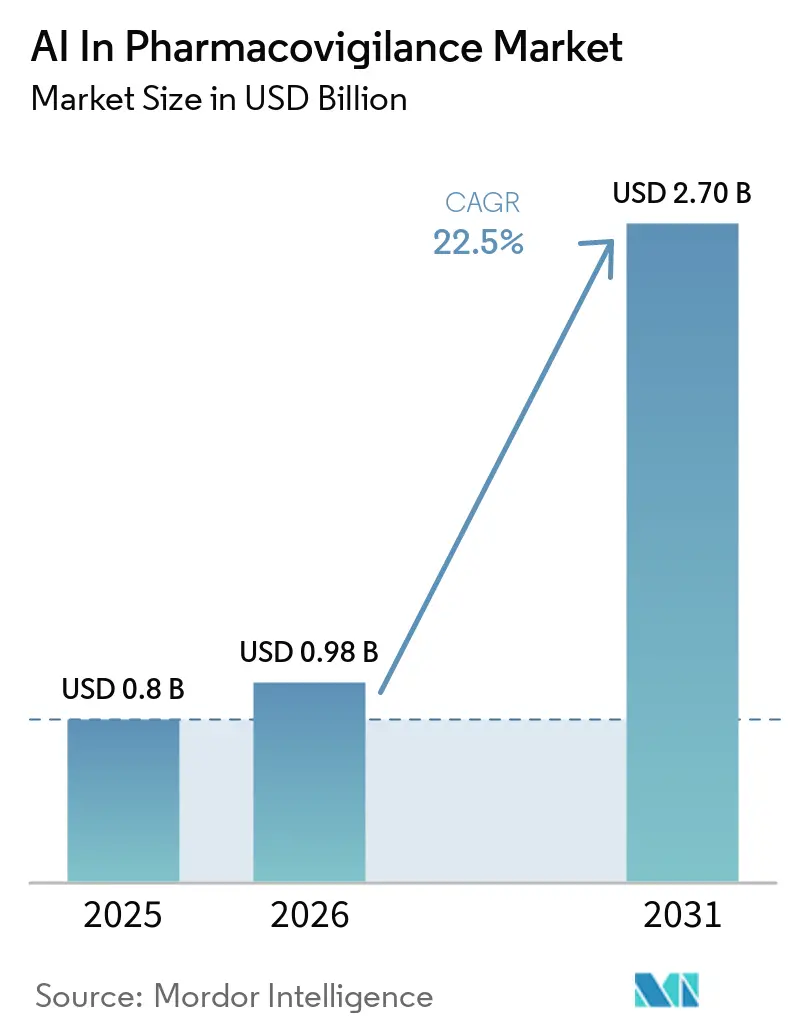

The AI In Pharmacovigilance Market size is expected to increase from USD 0.8 billion in 2025 to USD 0.98 billion in 2026 and reach USD 2.70 billion by 2031, growing at a CAGR of 22.5% over 2026-2031.

Drug-safety teams are increasingly transitioning to analytics-driven, predictive surveillance, moving away from traditional manual case processing. Advancements in natural language processing and large language models have streamlined repetitive tasks, reducing the median handling time for Individual Case Safety Reports (ICSR) from 22 minutes to under 17 minutes. Cloud delivery has emerged as the preferred option for most new installations, enabling seamless updates from MedDRA and ICH without causing customer downtime. Additionally, managed services are experiencing faster growth compared to platforms, as mid-tier biotechs increasingly outsource validation and tuning. Regulatory bodies are significantly driving this transformation. The FDA's Emerging Drug Safety Technology Program requires quarterly AI progress updates, while the EMA's ERATO system has achieved a notable reduction of over 400 monitoring hours within its first three months of operation.

Key Report Takeaways

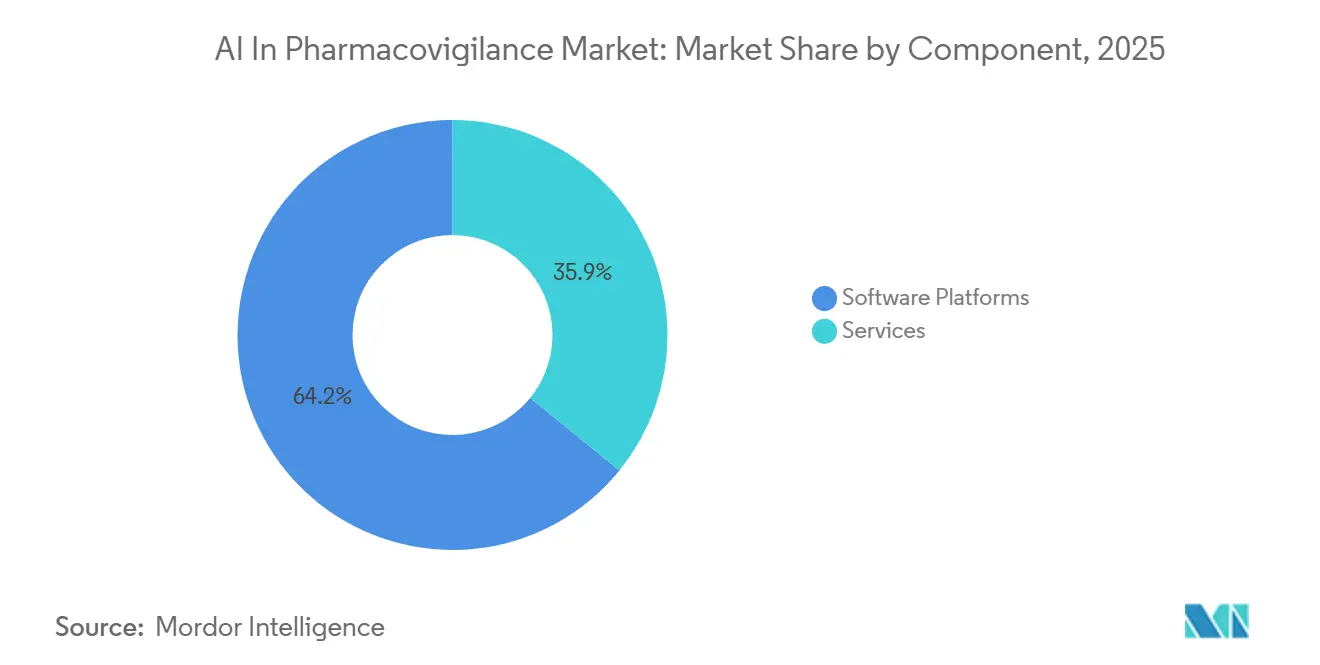

- By component, software platforms captured 64.15% revenue share in 2025, while services are projected to advance at a 23.45% CAGR to 2031.

- By deployment model, cloud-based delivery held 71.15% of the AI in Pharmacovigilance market share in 2025 and is forecasted to grow at a 23.85% CAGR through 2031.

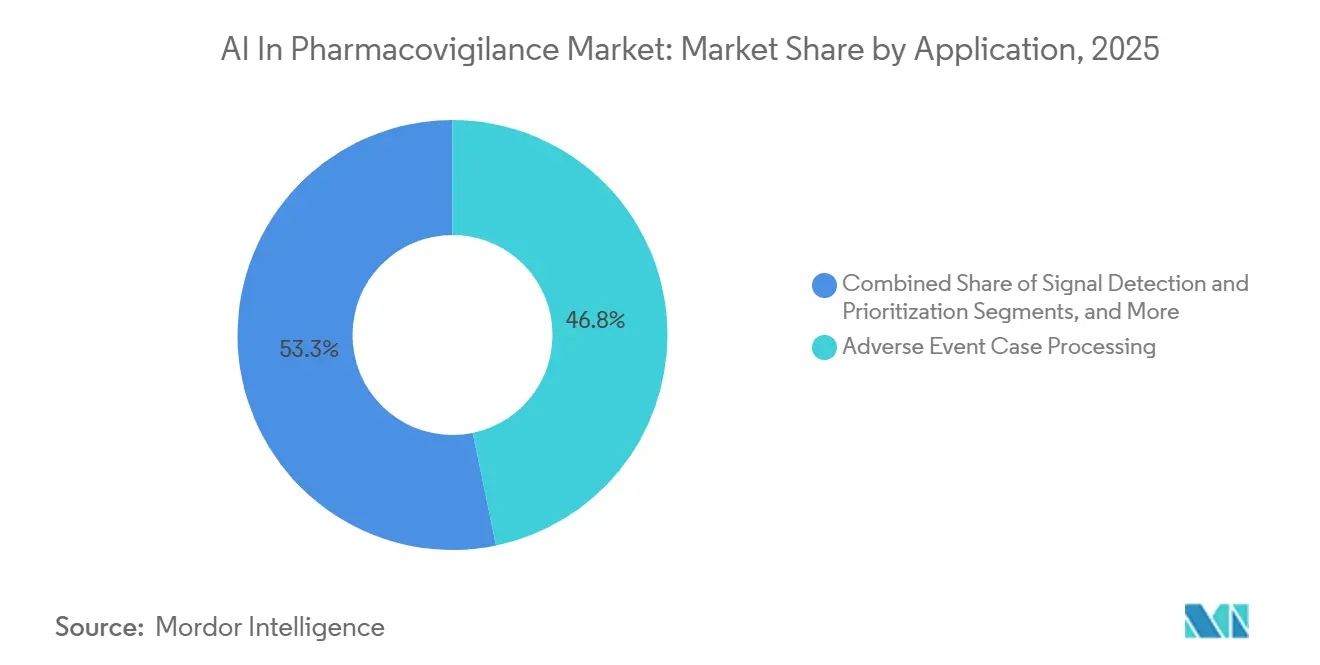

- By application, adverse-event case processing commanded 46.75% of the AI in Pharmacovigilance market size in 2025, yet signal detection and prioritization is expected to expand at a 24.54% CAGR to 2031.

- By end-user, pharmaceutical and biotech companies controlled 58.34% share in 2025, whereas regulatory authorities are expected to grow at a 24.75% CAGR to 2031.

- By geography, North America led with 41.56% revenue share in 2025, while Asia-Pacific is expected to be 23.35% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Pharmacovigilance Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising volume and complexity of safety data | +6.2% | Global | Short term (≤ 2 years) |

| Regulatory push for real-time monitoring | +5.8% | North America & EU | Medium term (2-4 years) |

| Cost pressure to automate case processing | +4.1% | Global | Short term (≤ 2 years) |

| Foundation models for rare-disease signal detection | +3.7% | North America, APAC | Long term (≥ 4 years) |

| Social-listening NLP for patient-reported outcomes | +5.8% | North America & EU | Medium term (2-4 years) |

| Federated learning agreements with EHR exchanges | +4.1% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Volume and Complexity of Safety Data

Annual ICSR submissions to FAERS topped 1.9 million in 2024, and EudraVigilance received 1.7 million ADRs in the same year, straining manual triage workflows.[1]Merck Healthcare KGaA & d-fine, “LLM-Based ICSR Extraction Pipeline,” merckgroup.com Social-media posts, EHR extracts, and wearable-device feeds enlarge data lakes that classical keyword filters cannot parse. AI pipelines now achieve 85-100% entity-match rates for structured clinical reports and reduce human correction to just 3.5% of data points. With every extra data stream, the AI in pharmacovigilance market becomes more indispensable to sponsors that must keep pace with twenty-four-hour regulatory reporting clocks.

Regulatory Push for Real-Time Monitoring

The FDA’s EDSTP, initiated in 2024, schedules quarterly sponsor meetings to evaluate AI systems, moving policy from retrospective submissions toward concurrent oversight.[2]U.S. Food and Drug Administration, “Emerging Drug Safety Technology Program,” fda.gov Across the Atlantic, revised EU rules obligate marketing authorization holders to monitor digital channels for unsolicited ADRs and submit serious unexpected cases within 15 days. Daily social-media output approaches 500 million posts, and roughly 0.02% reference medicines or side effects, a scale only AI can screen promptly, driving recurring investment in the AI in Pharmacovigilance market.

Cost Pressure to Automate Case Processing

Pharmacovigilance teams face mounting costs due to the sheer volume of adverse event reports that must be processed to meet regulatory requirements. Manual case handling is resource-intensive, requiring skilled staff to review, code, and submit data within strict timelines. AI-driven case processing automation helps reduce this burden by streamlining repetitive tasks such as data entry, triage, and narrative generation. This not only lowers operational expenses but also improves speed and accuracy, enabling companies to remain compliant while scaling up to handle growing data volumes without proportional increases in workforce size.

Social-Listening NLP for Patient-Reported Outcomes

Beyond formal clinical reports, patients increasingly share experiences on social media, forums, and health communities. These unstructured data sources provide valuable insights into real-world drug safety and effectiveness. AI-powered social listening NLP tools can detect, classify, and analyze patient-reported outcomes from these platforms, identifying emerging safety signals earlier than traditional reporting channels. By capturing authentic patient voices, companies gain a richer understanding of drug impact, uncover hidden adverse events, and strengthen post-market surveillance. This approach enhances pharmacovigilance by complementing structured regulatory data with real-world evidence.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Data privacy and cross-border transfer rules | -2.3% | EU, APAC core | Short term (≤ 2 years) |

| Algorithmic opacity and regulatory defensibility | -1.8% | Global | Medium term (2-4 years) |

| Scarcity of labeled safety datasets | -2.4% | EU, APAC core | Short term (≤ 2 years) |

| High compute cost of genAI inference | -1.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Cross-Border Transfer Rules

Multinational pharmaceutical companies are facing challenges due to regulations such as GDPR, China's PIPL, and Japan's APPI, which limit the offshore storage of health data. Consequently, these companies must either isolate datasets or implement regional cloud solutions. Additionally, there is a significant risk of LLMs re-identifying patients, as public-data pre-training can unintentionally embed personal information. A 2025 study revealed an 83% hallucination rate in clinical vignettes. Compliance costs are further slowing some deployments, restricting short-term growth in the AI in Pharmacovigilance market.

Algorithmic Opacity and Regulatory Defensibility

Neural networks, often criticized for their lack of transparency, are now required to meet the FDA's stringent seven-step credibility test, which prioritizes external validation and bias mitigation. As of 2024, only 14% of published AI models in Pharmacovigilance had undergone real-world validation. This has driven vendors to integrate explainability layers and detailed model-risk documentation, which are now essential for gaining sponsor approval. These requirements are tempering the near-term growth of the AI in Pharmacovigilance industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platforms Anchor Spending, Services Accelerate on Validation Work

In 2025, platforms accounted for 64.15% of the revenue, driven by Oracle Argus Safety, ArisGlobal LifeSphere, and Veeva Vault Safety suites. These platforms integrate intake, MedDRA coding, and E2B(R3) submissions into a single validated environment, minimizing audit risks. This unified change control feature is particularly appealing to top-20 pharmaceutical firms, each handling over 500,000 cases annually. Meanwhile, services, which make up the remaining portion of the AI in Pharmacovigilance market, are witnessing robust growth at a 23.45% CAGR. This surge is largely due to mid-tier biotech firms, lacking in-house validation teams, opting for turnkey outsourcing solutions. The EU AI Act mandates continuous AI model monitoring, periodic retraining, and explainability assessments, transforming consulting hours into a consistent revenue stream.

By Deployment Model: Cloud Gains Through Compliance Velocity and TCO Edge

In 2025, cloud models dominated the AI in Pharmacovigilance market with a 71.15% share and are projected to grow at a 23.85% CAGR, outpacing on-premise solutions. SaaS platforms offer versionless compliance, allowing vendors to implement overnight changes in ICH, MedDRA, and FDA forms. This capability eliminates downtime cycles associated with IQ/OQ/PQ. With pay-per-user pricing starting around USD 600 annually per user, organizations can shift from capital expenditures (CapEx) to operational expenditures (OpEx), avoiding server decommissioning costs. This results in IT maintenance bills that are 40% lower than those of on-premise setups.

By Application: Signal Detection Surges on Predictive Analytics

In 2025, adverse-event case processing generated 46.75% of the revenue, as each Individual Case Safety Report (ICSR) underwent intake, de-duplication, MedDRA coding, and E2B formatting. However, signal detection and prioritization are experiencing a faster growth rate of 24.54%. This acceleration is driven by advancements like real-time disproportionality algorithms, Bayesian change-point analysis, and transformer-based text mining, which have shortened discovery timelines from months to mere days. Continuous dashboards now notify safety scientists of emerging drug-event pairs, enabling timely labeling changes before case counts surge, addressing both patient safety and business risk concerns. Vendors are now integrating features like automated narrative summarization, IC disproportionality metrics, and anomaly flags into a unified interface.

By End-User: Industry Dominates, Regulators Accelerate

In 2025, pharmaceutical and biotech companies accounted for 58.34% of the AI PV revenue, underscoring their obligation to collect and submit global ICSRs promptly. Many leading firms are piloting AI initiatives for tasks like narrative extraction and triage, with several expanding these efforts company-wide. However, regulatory authorities are emerging as the fastest-growing segment, boasting a 24.75% CAGR. This growth is fueled by the FDA's introduction of the Elsa assistant in 2025, which saw an upgrade to version 4.0 in 2026 and is now utilized by 70% of pertinent staff. Furthermore, agencies from Canada to Singapore are assessing similar AI copilots. Such procurements create a ripple effect, compelling the industry to align with the analytics frameworks adopted by these regulatory reviewers, further propelling the AI in Pharmacovigilance market.

Geography Analysis

North America generated 41.56% of 2025 revenue, driven by the United States’ USD 600 billion pharmaceutical economy and the extensive 800 million-patient database of the Sentinel Initiative. The region demonstrates the highest cloud adoption, with 85% of drug-safety executives planning to increase AI budgets in 2026, reinforcing North America’s leadership in the AI in Pharmacovigilance market.

Asia-Pacific, however, is projected to grow at a 23.35% CAGR, supported by China, India, Japan, and South Korea, which collectively host more than one-third of global clinical trials, creating proportional safety workloads. Regulatory harmonization, including PMDA’s ICH E2B(R3) activation in 2025 and NMPA’s alignment roadmap, enables cross-border data flow within standardized message structures, encouraging SaaS adoption. The expansion of cloud availability zones across India and Southeast Asia allows CROs to store patient data locally while utilizing hyperscale GPU clusters, enhancing regional AI deployments and contributing to the growth of the AI in the Pharmacovigilance market size.

South America and the Middle East & Africa remain smaller but show targeted progress. Brazil’s regulator has introduced a sandbox for AI-enabled vigilance, and the African Medicines Agency, recognized as a WHO-Listed Authority since 2024, is coordinating regional post-market surveillance, necessitating tools beyond manual spreadsheets. These developments sustain vendor pipelines and highlight the long-term potential of the AI in Pharmacovigilance market as broadband and cloud infrastructure continue to advance.

Competitive Landscape

In the AI-driven pharmacovigilance landscape, major players, including platform giants, CRO service firms, and dedicated AI firms, are increasingly targeting the same clientele. Vendors are now focusing on three key differentiators. Firstly, pre-validated SaaS architectures are streamlining customer audits. For example, Veeva's efficient 10-month migration of 3.1 million legacy cases for a global client demonstrates a speed advantage that on-premise competitors cannot match. Secondly, explainable AI engines, such as ArisGlobal's NavaX and IQVIA's Vigilance Detect, are setting new standards. By displaying field-level confidence scores, these tools enable reviewers to adjust uncertain extractions, aligning with FDA's credibility benchmarks. Lastly, the emergence of "agentic AI" is transforming processes. This orchestration seamlessly integrates intake, coding, narrative drafting, and E2B auto-submission, all without rigid rules. Early adopters report a significant 30-40% boost in productivity.

Start-ups are carving out specialized niches. In 2025, Graph AI secured USD 3 million to expedite social-media signal detection for device manufacturers, claiming a 90% faster reporting time. Meanwhile, Sable Bio, with a USD 3.75 million seed round in 2026, is focusing on causal inference for safety profiling before product launches. These emerging players are pressuring established firms to accelerate feature releases, especially as AI email extraction approaches 95% accuracy, threatening to commoditize the market and reduce margins.

AI In Pharmacovigilance Industry Leaders

Oracle

ArisGlobal

Genpact

Cognizant

IQVIA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: AstraZeneca expanded its AI partnership with Immunai in a deal worth up to USD 37.5 million to accelerate oncology biomarker discovery and dose optimization.

- April 2026: ThinkTrends’ agentic Document AI platform went live within a U.S. federal health agency, processing 6-7 million adverse-event reports annually across multiple product classes.

- February 2026: Sable Bio secured USD 3.75 million in seed funding led by MMC Ventures to scale causal-inference safety analytics.

- January 2026: The FDA and EMA jointly issued “Guiding Principles of Good AI Practice in Drug Development,” setting a 10-point reliability framework for regulatory submissions.

Global AI In Pharmacovigilance Market Report Scope

As per the scope of the report, the AI in Pharmacovigilance (PV) market is experiencing rapid growth, driven by the need to manage rising safety case volumes, enhance drug safety detection, and improve regulatory compliance. Key applications include machine learning (ML) and natural language processing (NLP) for automating adverse event case processing, literature review, and signal detection.

The AI in Pharmacovigilance Market is segmented by component, deployment model, application, end-user, and geography. By component, the market includes software platforms and services. By deployment model, the market is segmented into cloud-based and on-premise. By application, the market is categorized into adverse event case processing, signal detection & prioritization, risk management & mitigation, and regulatory reporting & submissions. By end-user, the market is segmented into pharmaceutical & biotech companies, contract research organizations (CROs), medical device manufacturers, and regulatory authorities. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Software Platforms |

| Services |

| Cloud-Based |

| On-Premise |

| Adverse Event Case Processing |

| Signal Detection & Prioritisation |

| Risk Management & Mitigation |

| Regulatory Reporting & Submissions |

| Pharmaceutical & Biotech Companies |

| Contract Research Organizations (CROs) |

| Medical Device Manufacturers |

| Regulatory Authorities |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software Platforms | |

| Services | ||

| By Deployment Model | Cloud-Based | |

| On-Premise | ||

| By Application | Adverse Event Case Processing | |

| Signal Detection & Prioritisation | ||

| Risk Management & Mitigation | ||

| Regulatory Reporting & Submissions | ||

| By End User | Pharmaceutical & Biotech Companies | |

| Contract Research Organizations (CROs) | ||

| Medical Device Manufacturers | ||

| Regulatory Authorities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the size of the AI in Pharmacovigilance market today and where is it headed by 2031?

The market stands at USD 0.98 billion in 2026 and is projected to reach USD 2.70 billion by 2031, reflecting a 22.5% CAGR.

How fast is the cloud-based deployment model growing compared with on-premise setups?

Cloud delivery is expanding at a 23.85% CAGR through 2031, far outpacing the on-premise segment and already accounts for 71.15% of 2025 revenue.

Which application area will record the strongest growth over the forecast period?

Signal detection and prioritization is forecast to grow at 24.54% CAGR, overtaking routine case processing in relative momentum.

Which region is expected to deliver the highest growth rate?

Asia-Pacific is set to advance at a 23.35% CAGR to 2031, driven by dense clinical-trial activity and rapid cloud adoption among CROs.

Why are services gaining share even though platforms still dominate revenue?

Sponsors, especially mid-tier biotechs, are outsourcing validation, model-tuning, and migration work, pushing the services segment to a 23.45% CAGR.

Page last updated on: