AI In Cosmetic Formulation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.49 Billion |

| Market Size (2031) | USD 1.41 Billion |

| Growth Rate (2026 - 2031) | 23.44% CAGR |

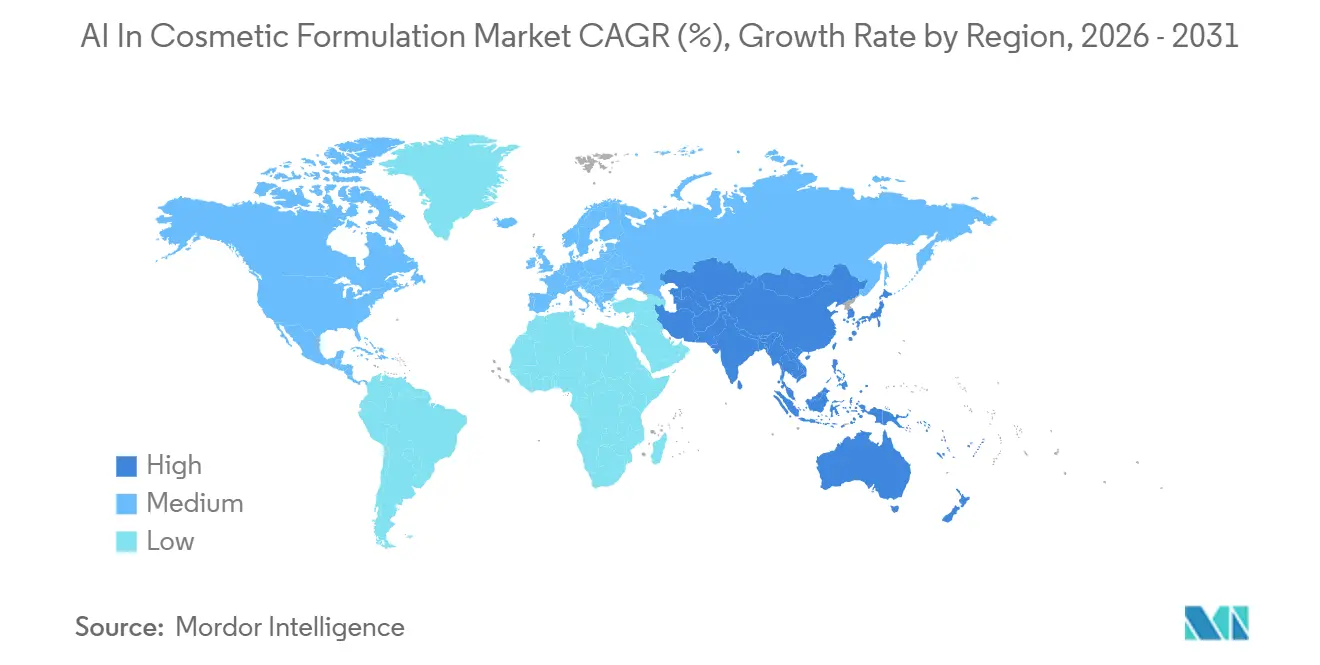

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

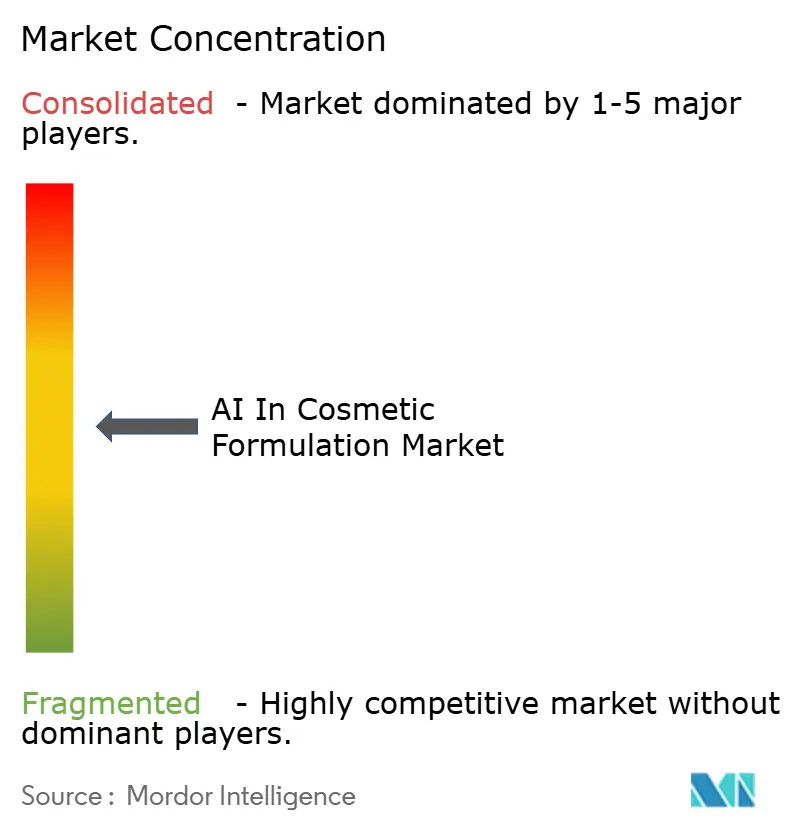

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Cosmetic Formulation Market Analysis by Mordor Intelligence

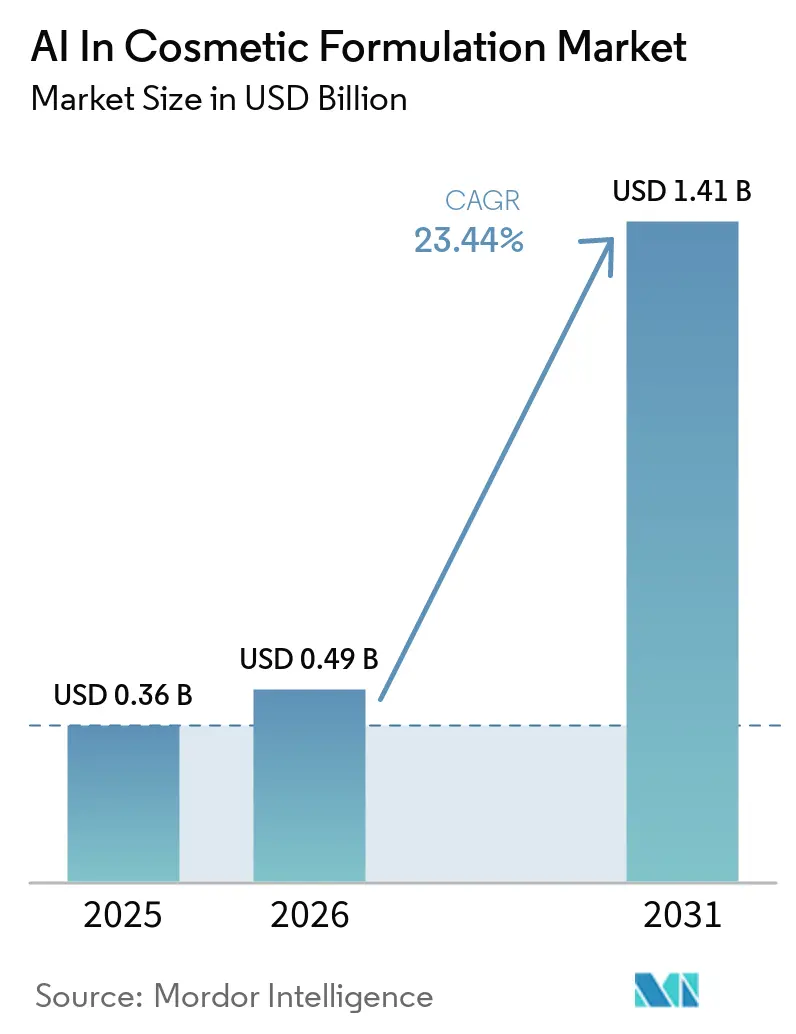

The AI In Cosmetic Formulation Market size is expected to increase from USD 0.36 billion in 2025 to USD 0.49 billion in 2026 and reach USD 1.41 billion by 2031, growing at a CAGR of 23.44% over 2026-2031.

The AI in cosmetic formulation market is moving from a supporting digital tool into a central layer of formulation R&D, where teams use it to shorten discovery cycles, improve ingredient selection, and prepare formulas for regulatory review earlier in development. The growth also indicates that digital infrastructure is capturing a larger share of value creation than conventional beauty growth patterns would suggest, because brands now depend on faster experimentation and more reliable screening to keep launch pipelines active. The AI in cosmetic formulation market is also benefiting from the push toward compliance-by-design, since brands need systems that can link ingredient science, documentation, and jurisdiction-specific checks inside one workflow. Competitive activity remains open rather than consolidated, with software specialists, ingredient suppliers, and beauty groups all building positions through partnerships, proprietary models, and workflow integration. Even with strong momentum, the AI in cosmetic formulation market still faces pressure from privacy controls and physical validation timelines, which means future adoption will favor hybrid workflows that combine algorithmic speed with human and lab-based verification.

Key Report Takeaways

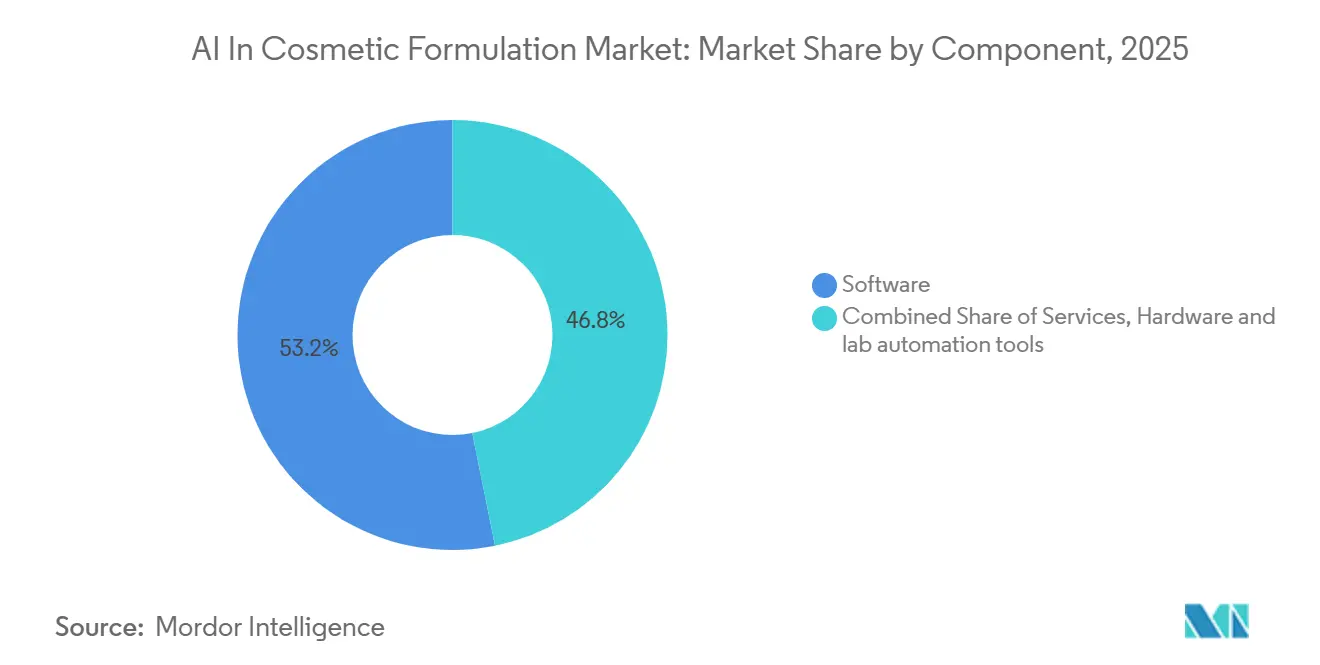

- By component, software held 53.16% of revenue in 2025, while services recorded the highest forecast growth at 24.88% CAGR through 2031.

- By deployment mode, cloud represented 61.17% of revenue in 2025 and also posted the fastest growth at 30.12% CAGR through 2031.

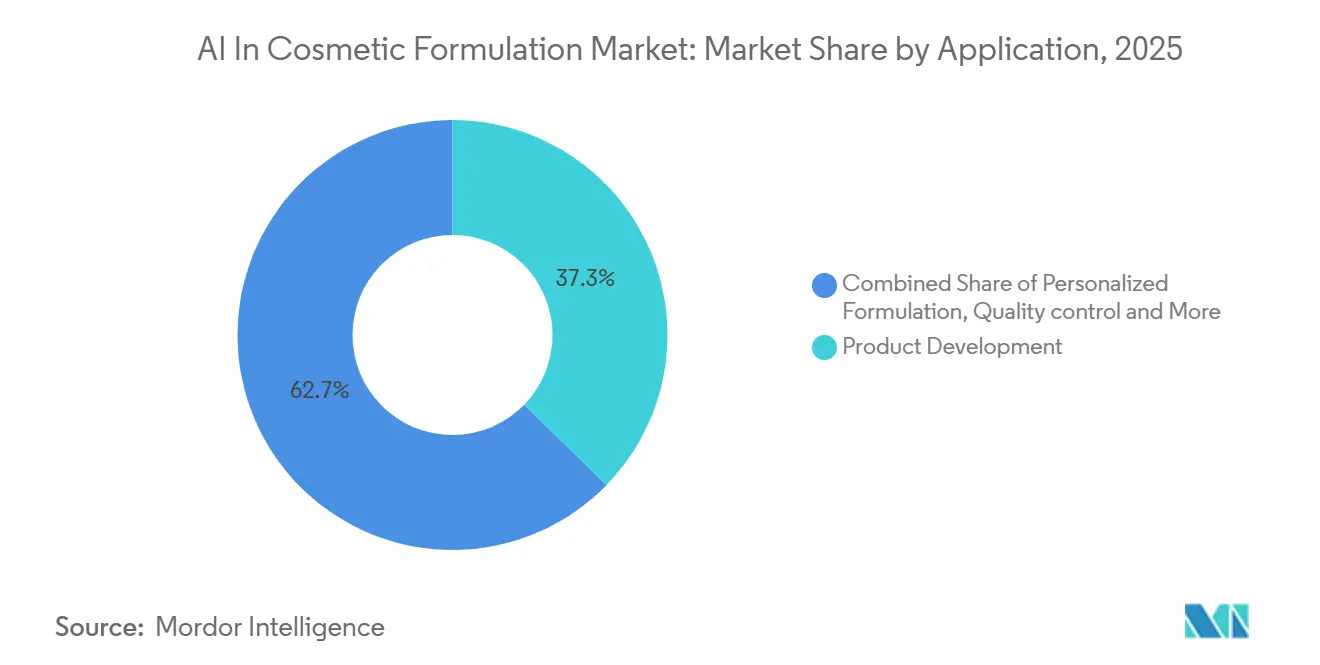

- By application, product development accounted for 37.29% of the AI in cosmetic formulation market size in 2025, while personalized formulation is projected to expand at 28.19% CAGR through 2031.

- By end user, cosmetic manufacturers held 49.77% of revenue in 2025, while contract manufacturers and private-label formulators are set to grow at 26.48% CAGR through 2031.

- By geography, North America captured 38.18% of the AI in cosmetic formulation market share in 2025, while Asia-Pacific is forecast to advance at 27.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Cosmetic Formulation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand For Hyper-Personalized Beauty | +4.8% | Global, with early concentration in North America, South Korea, and China | Short term (≤ 2 years) |

| Faster Formulation Cycles | +4.2% | Global, highest operational impact in APAC ODM-heavy markets | Short term (≤ 2 years) |

| Clean And Safe Formulation Pressure | +3.5% | EU and North America primarily, with spill-over to APAC and GCC | Medium term (2-4 years) |

| Regulatory Workflow Automation | +2.8% | EU and North America, with early gains in Brazil and Japan | Medium term (2-4 years) |

| Foundation-Model Reformulation For Bio-Based Inputs | +2.5% | North America and EU, with spill-over to Japan and South Korea | Long term (≥ 4 years) |

| AI Biodegradability And Safety Screening Unlocks New Actives | +2.0% | Japan and EU core, expanding to North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demand for Hyper-Personalized Beauty

Consumer demand has moved beyond broad skin categories, and the AI in cosmetic formulation market is gaining because brands increasingly need formulation systems that can respond to individual biology, lifestyle inputs, and environmental conditions. This shift changes personalization from a marketing message into an operating model, since companies now need tools that can translate consumer data into viable formulas without expanding development time or cost. In this setting, AI narrows a vast formulation search space into a smaller set of workable options, which makes personalized product design more practical for brands that want speed as well as specificity. It also raises the value of platforms that sit close to ingredient libraries, testing data, and production planning, because those systems become harder to replace once they are embedded in daily formulation work.

The result is that the AI in cosmetic formulation market is not only responding to demand for customized products, it is also being shaped by the need to industrialize customization in a repeatable way. Scientific literature on AI-led personalization in cosmetics supports this direction, especially where predictive modeling is used to improve fit between consumer profiles and formulation outcomes.

Faster Formulation Cycles

Speed remains one of the clearest reasons brands are investing in the AI in cosmetic formulation market, because formulation teams can test more hypotheses when first-draft generation and screening take minutes instead of days. The practical benefit is not only time saved, it is the ability to explore a wider range of textures, actives, and combinations within the same budget and launch window. That matters most in color cosmetics, skin care, and trend-sensitive categories, where timing often determines whether a concept reaches shelf space before demand shifts.

South Korea provides a clear operating example, where Cosmax improved first-attempt color-matching success from 52% to 78.1%, reducing costly reformulation loops and improving floor-level efficiency in production-linked R&D. The same pattern appears in ingredient discovery, where LG Household & Health Care and LG AI Research used EXAONE Discovery AI to cut efficacy ingredient discovery timelines from 22 months to 1 day, showing how AI can expand competitive lead time rather than just automate routine tasks. As a result, the AI in cosmetic formulation market is benefiting from a direct link between faster cycles and stronger launch economics, which makes adoption easier to justify at the R&D leadership level.

Clean and Safe Formulation Pressure

The clean beauty shift now operates as a formulation and compliance challenge, which gives the AI in cosmetic formulation market a stronger role in ingredient screening, reformulation planning, and early risk detection. Regulatory review in Europe is especially important here, because the 2025-2026 evaluation of Regulation (EC) No. 1223/2009 is examining whether environmental effects should be considered more directly in cosmetics oversight[1]European Commission, “Evaluation of Regulation (EC) No. 1223/2009 on Cosmetic Products,” European Commission, europa.eu. If scope expands, many formulas that are currently viable could require reformulation, and that would increase demand for systems that can screen biodegradability, restricted substance exposure, and annex updates at the same time. This is where AI becomes defensible, since the cost of a late compliance miss is much higher than the cost of routine inefficiency in lab work.

Shiseido’s biodegradability tool, developed with Japan’s National Institute of Technology and Evaluation, shows how AI-QSAR methods can predict degradation from chemical structure and reduce dependence on specialized testing expertise for early-stage sustainability screening. The broader outcome is that the AI in cosmetic formulation market is being pulled forward not only by consumer preference, but also by the need to manage a more demanding safety and environmental review environment.

Regulatory Workflow Automation

Regulatory documentation takes a significant share of formulation time, and the AI in cosmetic formulation market is gaining ground because brands need faster ways to manage multi-country launches without building separate teams for each jurisdiction. Automated crosschecks for the EU, the United States, China, Japan, South Korea, Brazil, and Australia reduce repetitive work and make it easier to identify issues earlier in the development cycle. That matters more in 2026 because regulatory systems themselves are becoming more data-driven, which raises the standard for traceability, auditability, and adverse event monitoring.

The EU AI Act and the broader EU regulatory framework are pushing companies toward explainable systems that can document how AI influences regulated product decisions. In practice, this creates a closed-loop environment where stronger screening tools improve both submission readiness and downstream monitoring quality, while weaker manual workflows become easier to expose. For the AI in cosmetic formulation market, that means regulatory automation is shifting from a support feature into a core buying criterion, especially for brands that want scale across several regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation And Integration Cost | -2.5% | Global, most acute for SMEs in South America and MEA | Short term (≤ 2 years) |

| Data Privacy And Formula IP Risk | -2.0% | EU and North America, with spill-over to APAC | Medium term (2-4 years) |

| Tacit Formulator Know-How Is Hard To Digitize | -1.5% | Global, acute in APAC heritage formulation markets | Long term (≥ 4 years) |

| Physical Validation Bottleneck After AI Ideation | -1.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Implementation and Integration Cost

The AI in cosmetic formulation market still faces a real adoption barrier in the form of software, workflow, and organizational integration cost, especially for mid-tier brands and independent formulators. Buying a platform is only the first step, because most users also need cleaner data, compatible architecture, revised approval flows, and staff that can work confidently with AI-supported formulation outputs. Legacy PLM and ERP systems add another constraint, since many were not built to exchange data easily with newer formulation tools and therefore require custom integration work. This problem is most visible among smaller operators and emerging-market manufacturers, where capital budgets are tighter and payback periods above 2 years can delay decisions. Cloud-native delivery models help reduce upfront infrastructure burden, but they do not remove the need for change management and internal process redesign. As a result, the AI in cosmetic formulation market can advance quickly at the enterprise end while still developing unevenly across smaller customers that lack the resources to operationalize the same tools at scale.

Data Privacy and Formula IP Risk

Formula data sits at the center of competitive advantage, and the AI in cosmetic formulation market must therefore grow within strict limits around privacy, ownership, and traceability. Cloud-based systems often need access to detailed ingredient interactions, historical formulas, and testing outcomes, which creates concern over how proprietary knowledge is stored, shared, and used in model improvement. This pressure is sharper in Europe, where GDPR and the EU AI Act raise expectations around transparency, auditability, and data handling whenever AI contributes to regulated product decisions. A French laboratory guidance note published in February 2026 stated that no AI solution currently generates a complete, traceable, and compliant Product Information File on its own, which keeps legal responsibility with the brand and reinforces human review as a regulatory safeguard. That means hybrid and private-cloud models may gain favor among larger companies, even if those setups reduce some of the cross-client learning benefits available in shared environments. For the AI in cosmetic formulation market, privacy and IP control are not side issues, they are shaping deployment architecture, procurement preference, and the boundaries of acceptable automation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominates While Services Reflects Adoption Maturity Gap

Software accounted for 53.16% of revenue in 2025, which made it the largest component in the AI in cosmetic formulation market and reflected the central role of formulation lifecycle platforms, ingredient intelligence engines, and prediction tools. This leadership came from the ability of software to bring ingredient data, regulatory checks, and stability modeling into a single workflow, reducing the need for fragmented research and repeated manual reviews. In practice, these platforms serve as the operating layer through which formulators move from concept screening to draft formulas and compliance preparation. Nouryon’s April 2025 launch of BeautyCreations showed how ingredient suppliers are embedding AI into customer-facing discovery tools rather than treating it as a separate software category, which strengthens retention and deepens commercial relationships. Hardware and lab automation remained the smallest component, because physical execution tools still depend on AI-generated recommendations and matter most in high-volume, made-to-order settings where throughput discipline is critical. This pattern indicates that digital intelligence still captures more value than physical automation alone in the current stage of the AI in cosmetic formulation market.

Services are projected to grow at 24.88% CAGR through 2031, and that trajectory says as much about capability gaps as it does about software demand. The faster rise of services suggests that buyers have moved beyond awareness and licensing, but many still need outside help to integrate models, redesign workflows, and prepare internal teams for new decision processes. That is why consultants, systems integrators, and implementation partners are becoming a premium layer within the AI in cosmetic formulation industry, even as software platforms expand their feature sets. IBM’s January 2025 collaboration with L’Oréal is a strong example, because the project combined a custom generative AI foundation model with workflow redesign aimed at sustainable cosmetics creation, showing that value depends on both model quality and operating change[2]IBM, “IBM and L'Oréal to Build First AI Model to Advance the Creation of Sustainable Cosmetics,” IBM Newsroom, ibm.com. For mid-market users, the same logic makes third-party support the fastest path to adoption, since internal data science and systems integration teams are often limited. The gap between software share and services growth therefore shows that the AI in cosmetic formulation market is entering a maturity phase where deployment expertise remains scarce and commercially important.

By Deployment Mode: Cloud's Dual-Leader Status Points to a Winner-Takes-Most Dynamic

Cloud deployment held 61.17% of revenue in 2025, giving it the lead in the AI in cosmetic formulation market because SaaS delivery lowers upfront cost, speeds updates, and makes regulatory database maintenance easier across multiple countries. This architecture fits brands and contract formulators that want continuous model improvement without managing internal infrastructure or rebuilding compliance rules by hand. It also supports mid-sized users that need faster adoption and lower total ownership cost, which helps explain why cloud became the dominant choice even before the market reached full scale. The regulatory case for cloud is especially strong in Europe, where frequent updates under Regulation (EC) No. 1223/2009 make manual internal refresh cycles expensive and slow. Cloud platforms also benefit from broader product velocity, since new assistants, interface changes, and screening features can be deployed across the user base without long local upgrade cycles. This has helped the AI in cosmetic formulation market build a practical adoption path for brands that want faster experimentation without large IT commitments.

Cloud is also the fastest-growing deployment mode, with 30.12% CAGR through 2031, which is notable because leading segments usually slow once they reach scale. That combination suggests continued migration from on-premises and hybrid setups rather than stable coexistence, especially among customers that value flexibility and lower implementation friction. It also points to a concentration effect where vendors that can combine strong models, current databases, and frequent product updates may widen their advantage over slower rivals. Even so, hybrid and private cloud options will remain relevant where formula confidentiality, audit control, or internal governance standards outweigh the benefits of shared architecture. These concerns are especially important for larger brands with proprietary formula libraries, since their historical data is one of the few assets capable of creating defensible performance gaps in the AI in cosmetic formulation industry. The long runway for cloud in the AI in cosmetic formulation market therefore comes from both mainstream SaaS expansion and newer adoption in APAC markets where penetration is still earlier.

By Application: Personalized Formulation Drives Growth While Product Development Anchors Revenue

Product development accounted for 37.29% of revenue in 2025, which made it the largest application and showed where commercial urgency has been strongest in the AI in cosmetic formulation market. Companies have focused first on idea-to-formula acceleration because faster SKU refresh, quicker trend response, and lower iteration cost create immediate business value across most categories. This makes product development the most natural entry point for AI, since it connects directly to launch cadence and resource efficiency. Shiseido’s VOYAGER platform illustrates the direction of travel, because it uses more than 500,000 formulation data points gathered across a century of research and has advanced from formula search toward generative recommendation. That shift matters because it shows the technology moving from retrieval support into proposal generation, which changes how formulation teams use internal knowledge. In the current AI in cosmetic formulation market size structure, this explains why product development remains the main revenue anchor even as other use cases rise.

Personalized formulation is projected to expand at 28.19% CAGR through 2031, making it the fastest-growing application as brands respond to stronger demand for individualized skin care and more precise matching of formulas to user needs. AI makes this possible because it can work across broader biological, lifestyle, and environmental variables than manual formulation methods can manage at commercial speed. That ability becomes more valuable as companies try to turn personalization into a repeatable business model instead of a premium niche offer. Debut’s BeautyORB platform, which screens more than 50 billion potential ingredients against a proprietary dataset of 60 million data points with 99% predictive consistency, reflects how AI can push personalized active discovery toward commercial viability. The challenge is that customized output can strain traditional batch economics, so faster formula generation must be matched by more responsive manufacturing and fulfillment models. That is why the AI in cosmetic formulation market is seeing personalized formulation as both a growth engine and a pressure point for broader operating redesign.

By End User: Contract Manufacturers Emerge as the Growth Pivot in the Value Chain

Cosmetic manufacturers held 49.77% of revenue in 2025, which placed them at the center of the AI in cosmetic formulation market because they control the broadest R&D operations and the deepest internal libraries of historical formula data. Those assets matter because model performance improves when companies can train systems on large sets of ingredient interactions, testing records, and prior development outcomes. Large manufacturers also have the budget and technical scale to connect AI tools with product development, regulatory affairs, and supplier collaboration. L’Oréal’s scale, supported by USD 41.18 billion in 2023 revenue, 4,000 researchers, and 20 global research centers, helps explain why bespoke foundation model development is feasible for a small group of global leaders. Personal care brands and ingredient suppliers also play active roles, but they often use AI to accelerate concepting, support claims, or strengthen customer partnership rather than build the full stack internally. This keeps major manufacturers in the lead position within the AI in cosmetic formulation market share structure, at least in the current phase.

Contract manufacturers and private-label formulators are forecast to grow at 26.48% CAGR through 2031, which makes them the fastest-rising end-user group because AI lowers the expertise barrier that once favored large in-house teams. Their growth reflects a deeper shift in the value chain, where outsourced product development becomes more capable when AI compresses ideation time, organizes compliance work, and speeds up iteration. Kolmar Korea’s Loud Labs platform shows this clearly, since it reduced full product development from 1-3 months to around 30 seconds and opened access to its R&D data for smaller beauty founders. This expands who can participate in the AI in cosmetic formulation market, because smaller brands can tap advanced formulation capability without building a full internal science team. Research institutes and independent laboratories remain smaller in revenue terms, but they still matter because they develop methods and peer-reviewed datasets that improve screening quality over time. Taken together, these changes suggest the AI in cosmetic formulation market will increasingly reward companies that can package formulation intelligence as a scalable service rather than keep it only inside vertically integrated R&D structures.

Geography Analysis

North America held 38.18% of global revenue in 2025, which gave it the leading position in the AI in cosmetic formulation market because the region combines strong software capability, well-funded beauty innovators, and a regulatory setting that is becoming more data-intensive. The MoCRA framework has already increased the need for stronger safety substantiation and adverse event management, which makes AI-based screening and documentation more relevant in everyday formulation work. The FDA’s April 2026 deployment of an AI-powered Adverse Event Monitoring System further strengthens this direction, because it signals that oversight itself is becoming more automated and more dependent on data quality. North America also has a commercial advantage in personalized production models, where AI links consumer inputs to formula generation and manufacturing execution. That connection keeps the region important not only for software development, but also for proving that AI-led formulation can operate at real scale in customer-facing businesses.

Europe’s position is shaped by the strictest regulatory environment in the field, which creates both friction and specialized demand for explainable and traceable systems in the AI in cosmetic formulation market. The European Commission’s 2025-2026 evaluation of Regulation (EC) No. 1223/2009 is reviewing topics that include environmental chemical effects, digital labeling, and governance implications tied to AI use in cosmetic oversight. At the same time, the EU AI Act increases pressure on vendors to show model transparency and decision traceability when AI influences regulated outcomes. This favors vendors that can document how recommendations are generated and how formula decisions are reviewed by humans before launch. Germany, France, and the UK remain the core demand centers, supported by large regional ingredient suppliers whose R&D footprints help connect AI tools to real formulation workflows.

Asia-Pacific is the fastest-growing region, with 27.36% CAGR through 2031, which shows that the AI in cosmetic formulation market is expanding rapidly in ODM and OEM ecosystems where speed and flexibility directly affect competitiveness. South Korea is especially active, combining government-backed AI programs with manufacturing networks that can move from formulation concept to scaled production quickly. Japan adds depth through large beauty groups such as Shiseido and Kao, where internal AI platforms are being used for skin analysis, formulation recommendation, and sustainability screening. Kao’s upgraded Kirei Skin AI, which evaluates 77 skin parameters using 25 machine learning models and 70,389 training images, shows how regional players are turning AI into a differentiated science and product development asset. South America, the Middle East and Africa, and GCC markets remain earlier-stage adoption zones, but cloud delivery and supplier-led partnerships are making entry easier where local infrastructure is still developing.

Competitive Landscape

The AI in cosmetic formulation market remains moderately fragmented, and no single participant controls a dominant cross-segment position. Competition is forming around 3 main models, large technology companies that partner with beauty groups, specialist software firms that solve focused workflow problems, and beauty or ingredient companies that build proprietary AI as a strategic asset. This structure keeps the field open, because customers still choose among different combinations of software depth, scientific knowledge, regulatory support, and implementation capability. The most powerful players today are not necessarily those with the broadest software catalog, but those that can connect models to proprietary datasets and real formulation workflows. That is why the AI in cosmetic formulation market still offers room for partnerships, licensing, and embedded service models rather than showing a clear winner-takes-most outcome. It also explains why investment and product strategy are spreading across several layers of the value chain instead of concentrating in a single vendor class.

Large-scale partnerships are setting the pace at the top end of the market. IBM and L’Oréal’s January 2025 collaboration on a custom AI foundation model for sustainable cosmetics showed how major players are combining domain-specific data with external AI capabilities to create proprietary research advantage. L’Oréal then deepened that posture in March 2026 by integrating NVIDIA’s Alchemi framework for atomic-scale molecular simulation, a move aimed at accelerating discovery and cutting down the need for large volumes of physical testing. Shiseido’s VOYAGER platform reflects a similar strategy from the beauty side, where decades of accumulated formulation knowledge are being converted into a recommendation engine that becomes stronger as more internal data is added. These examples matter because they show that competitive advantage in the AI in cosmetic formulation market is increasingly linked to proprietary data scale, scientific depth, and the ability to convert those assets into day-to-day R&D speed.

The middle of the market remains the main opening, especially for brands large enough to benefit from enterprise tools but too small to build bespoke systems. Ingredient suppliers are using that gap to extend formulation support into AI-enabled services, which helps them secure deeper roles in customer development processes. Nouryon’s BeautyCreations is one example of this approach, since it embeds natural language discovery into the supplier relationship rather than asking customers to adopt a disconnected tool set. Givaudan Active Beauty and Haut.AI have taken a related path by combining ingredient innovation with AI-based skin simulation and diagnostics, positioning evidence-backed actives and digital validation as part of one integrated offer[3]Haut.AI, “Haut.AI & Givaudan Active Beauty Showcase AI-Powered Ingredient Innovations at In-Cosmetics Global 2026,” Haut.AI, haut.ai. At the same time, patent awareness and explainability are becoming more important, because AI-generated combinations need stronger IP protection and more transparent logic under European rules. This means the AI in cosmetic formulation market is likely to reward vendors that can pair scientific credibility with auditable outputs, rather than those offering faster but less traceable black-box recommendations.

AI In Cosmetic Formulation Industry Leaders

L'Oréal

Shiseido

Unilever

BASF

Givaudan

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Givaudan Active Beauty and Haut.AI debuted an integrated AI ingredient innovation suite at in-cosmetics Global 2026, incorporating SkinGPT generative simulation, AI Skin Expert diagnostics, and the PrimalHyal NeuroYouth active ingredient, commercially positioning AI-validated clinical evidence as the new category standard for active ingredient launches.

- March 2026: L'Oréal integrated NVIDIA's Alchemi machine learning framework into its research labs, enabling atomic-scale molecular simulation that tests thousands of formulation variables simultaneously and accelerates discovery cycles by up to 100x compared to conventional methods; the technology was presented at the NVIDIA GTC AI Conference in San Jose.

- February 2026: Shiseido introduced two AI-based technologies for cosmetic ingredient screening: a biodegradability AI-QSAR model developed with Japan's National Institute of Technology and Evaluation, and a safety information identification AI that assesses repeated-dose toxicity and skin sensitization, tools the company aims to open to the broader industry.

Global AI In Cosmetic Formulation Market Report Scope

As per the scope of the report, AI in cosmetic formulation refers to the application of artificial intelligence technologies to develop, optimize, and personalize cosmetic products. It involves using machine learning algorithms, data analysis, and automation to enhance ingredient selection, stability testing, efficacy prediction, and formulation processes, ultimately leading to more innovative, effective, and customized skincare and beauty products.

The segmentation for the AI in cosmetic formulation market is categorized by component, deployment mode, application, end user, and geography. By component, the market is divided into software, services, and hardware and lab automation tools. By deployment mode, it is segmented into cloud, on-premises, and hybrid and private cloud. By application, the market includes product development, ingredient analysis and discovery, personalized formulation, quality control and stability prediction, and regulatory compliance and safety assessment. By end user, the segmentation covers cosmetic manufacturers, personal care brands and brand owners, contract manufacturers and private-label formulators, ingredient suppliers, and research institutes and independent labs. By geography, the market is analyzed across North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Software |

| Services |

| Hardware and lab automation tools |

| Cloud |

| On-premises |

| Hybrid and private cloud |

| Product development |

| Ingredient analysis and discovery |

| Personalized formulation |

| Quality control and stability prediction |

| Regulatory compliance and safety assessment |

| Cosmetic manufacturers |

| Personal care brands and brand owners |

| Contract manufacturers and private-label formulators |

| Ingredient suppliers |

| Research institutes and independent labs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| Hardware and lab automation tools | ||

| By Deployment Mode | Cloud | |

| On-premises | ||

| Hybrid and private cloud | ||

| By Application | Product development | |

| Ingredient analysis and discovery | ||

| Personalized formulation | ||

| Quality control and stability prediction | ||

| Regulatory compliance and safety assessment | ||

| By End User | Cosmetic manufacturers | |

| Personal care brands and brand owners | ||

| Contract manufacturers and private-label formulators | ||

| Ingredient suppliers | ||

| Research institutes and independent labs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in AI for cosmetic formulation through 2031?

Growth is being led by stronger demand for hyper-personalized beauty, faster formulation cycles, rising pressure for clean and safe formulation, and the need to automate regulatory workflows across multiple markets. These factors support expansion from USD 0.49 billion in 2026 to USD 1.41 billion by 2031 at a 23.44% CAGR.

Which component category leads revenue today?

Software leads the current revenue mix, accounting for 53.16% in 2025, because formulation lifecycle tools, ingredient intelligence platforms, and prediction engines are the first systems brands use to centralize R&D and compliance work.

Why is cloud deployment growing so quickly in this space?

Cloud leads with 61.17% of revenue in 2025 and is also the fastest-growing deployment mode at 30.12% CAGR through 2031. Buyers prefer it because it lowers upfront IT cost, supports continuous model updates, and makes regulatory database maintenance easier across countries.

Which application area is expanding the fastest?

Personalized formulation is the fastest-growing application, with 28.19% CAGR through 2031. The main reason is that AI can process skin, lifestyle, and environmental inputs at a scale that manual formulation methods cannot handle efficiently.

Which end users are creating the next wave of adoption?

Cosmetic manufacturers still hold the largest share at 49.77% in 2025, but contract manufacturers and private-label formulators are the fastest-growing end users at 26.48% CAGR. AI is lowering the expertise barrier and letting outsourced partners deliver faster ideation and compliance-ready development.

Which region offers the strongest growth outlook?

Asia-Pacific has the strongest regional growth outlook, with 27.36% CAGR through 2031, while North America remains the largest regional base at 38.18% in 2025. APAC momentum is supported by government-backed AI programs, strong ODM and OEM networks, and active commercialization in South Korea and Japan.

Page last updated on: