AI In Healthcare Zero-Trust Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

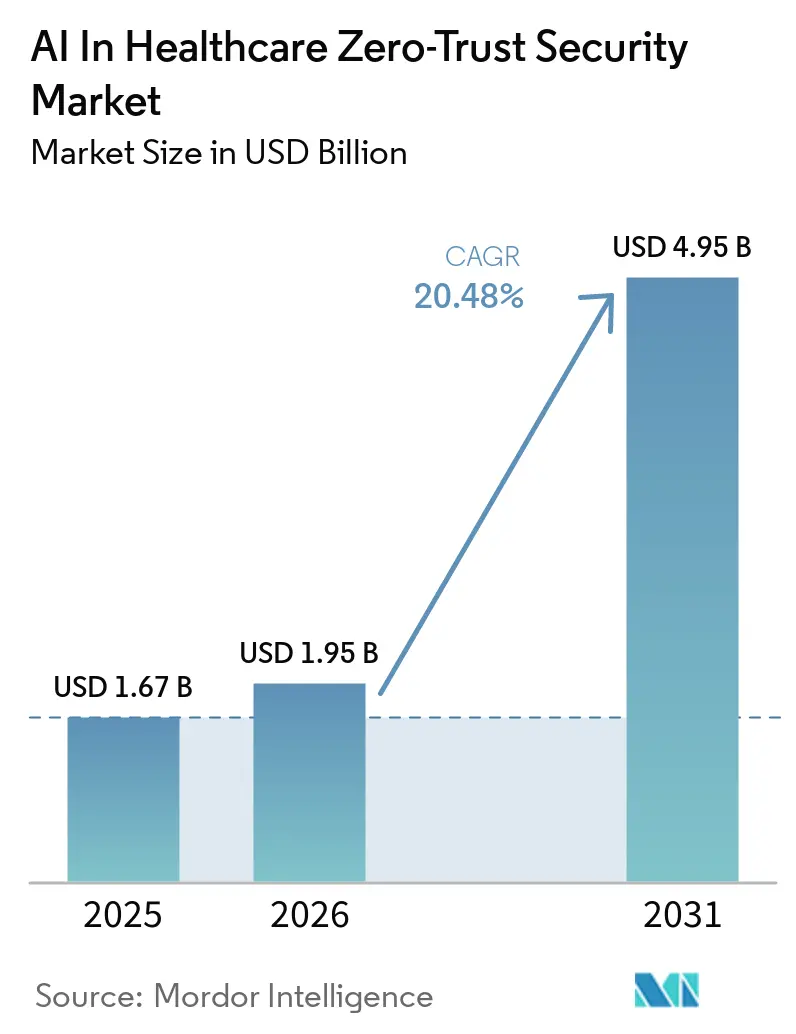

| Market Size (2026) | USD 1.95 Billion |

| Market Size (2031) | USD 4.95 Billion |

| Growth Rate (2026 - 2031) | 20.48% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Healthcare Zero-Trust Security Market Analysis by Mordor Intelligence

The AI in healthcare zero-trust security market size is expected to grow from USD 1.67 billion in 2025 to USD 1.95 billion in 2026 and is forecasted to reach USD 4.95 billion by 2031 at 20.48% CAGR over 2026-2031. Ransomware pressure is pushing healthcare boards to move spending away from perimeter defense and toward continuous, identity-based controls after 278 confirmed healthcare ransomware incidents were logged in 2025. The AI in healthcare zero-trust security market is also benefiting from the way health systems now operate across cloud EHRs, connected medical devices, and hospital-to-home monitoring programs, which makes a fixed network edge far less useful than workload-level and session-level verification. A compliance-led buying cycle is emerging as proposed U.S. HIPAA rule changes move microsegmentation from a recommended practice to a required technical control. Vendor competition is intensifying because integrated platform providers, microsegmentation specialists, and cloud-native security firms are all trying to win healthcare-specific deployments at the same time. Over the forecast period, the strongest opportunities in the AI in healthcare zero-trust security market are likely to come from cloud workload security, device-centric trust controls, and privacy-preserving AI models that need verified access at every inference point.

Key Report Takeaways

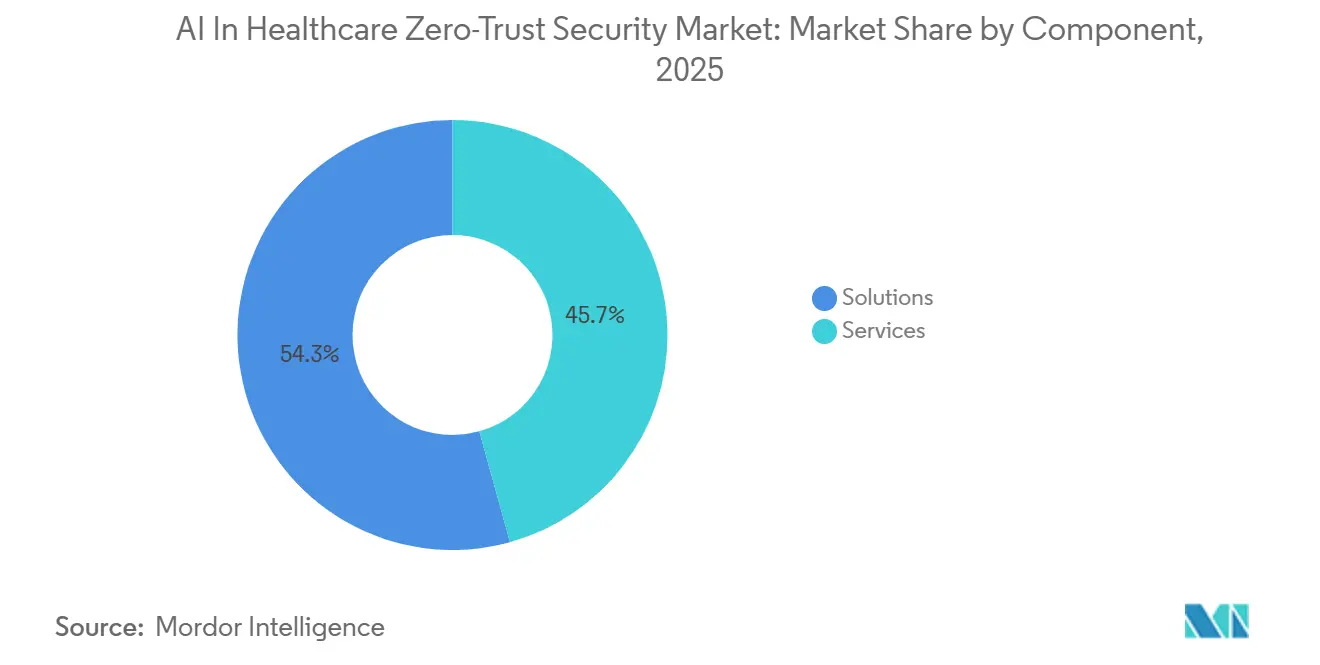

- By component, solutions held a 54.32% share of the market in 2025 and is projected to grow at a CAGR of 21.44% through 2031.

- By deployment mode, cloud accounted for 56.34% of the market share in 2025 and is expected to expand at a CAGR of 22.25% through 2031.

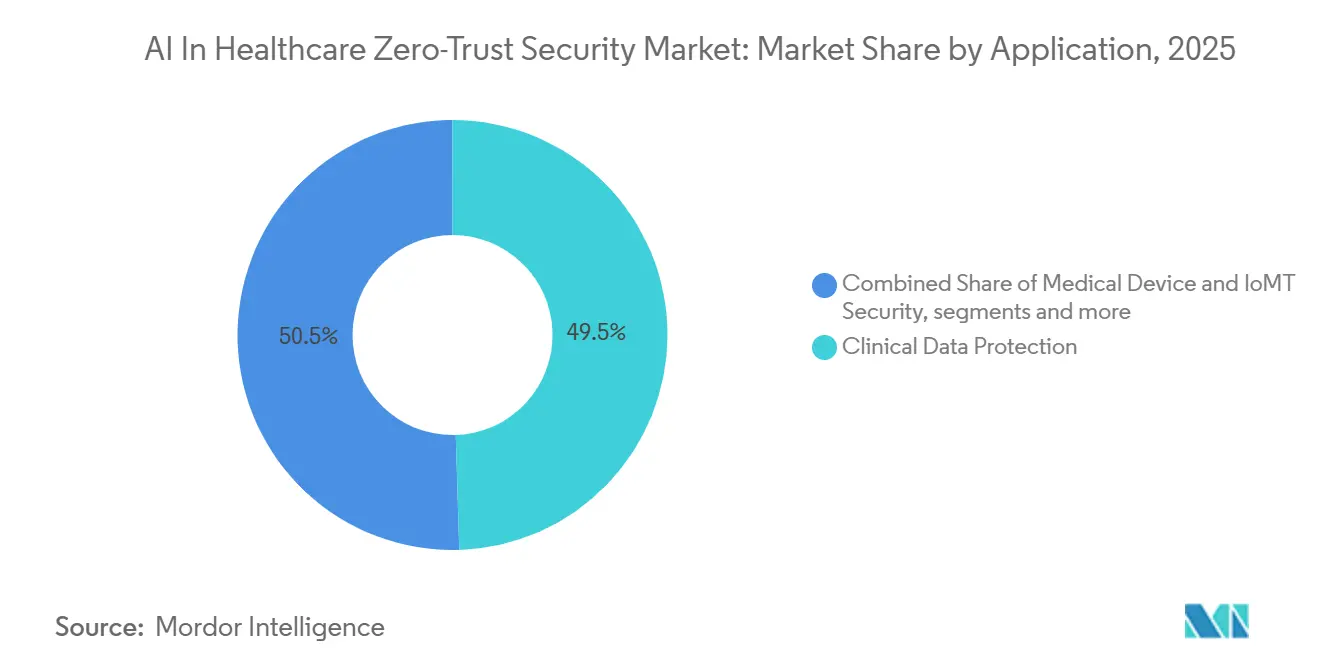

- By application, EHR and EMR security held a 49.52% share in 2025, while clinical data protection is projected to grow at a CAGR of 21.68% through 2031.

- By end user, healthcare providers accounted for 48.49% of the market share in 2025, while pharmaceutical and biotech companies are anticipated to advance at a CAGR of 22.86% through 2031.

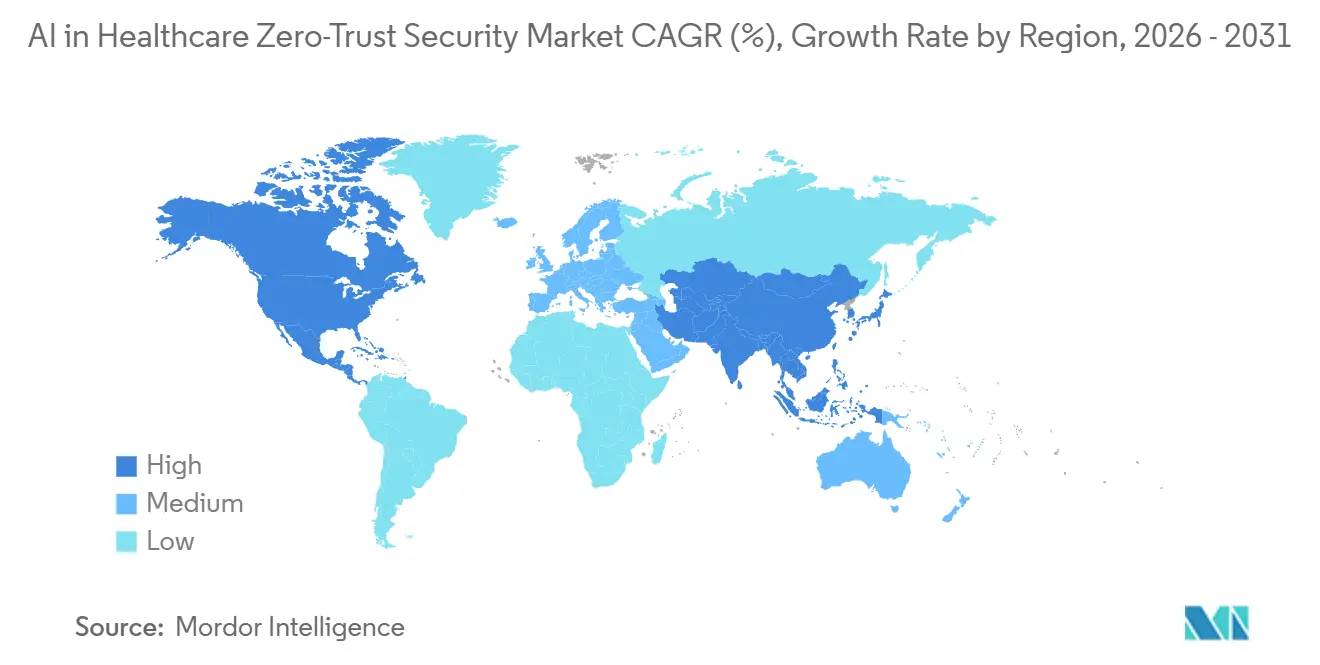

- By geography, North America held a 49.36% share of the market in 2025, while Asia-Pacific is forecast to grow at a CAGR of 23.27% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Healthcare Zero-Trust Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Driven Micro-Segmentation Reduces Lateral Threat Movement | +3.5% | Global, with concentrated early gains in North America and EU | Short term (≤ 2 years) |

| Rapid Cloud Adoption of Electronic Health Records | +2.8% | Global, highest velocity in North America and APAC core | Short term (≤ 2 years) |

| Surge in Ransomware Targeting Connected Medical Devices | +3.9% | Global, with disproportionate impact on North America and EU healthcare providers | Short term (≤ 2 years) |

| Regulatory Push for Zero-Trust in HIPAA and HITECH Updates | +3.2% | North America primary, with spillover to EU and APAC privacy regimes | Medium term (2-4 years) |

| Integration of Federated Learning for Privacy-Preserving Analytics | +1.9% | APAC core, EU, and North America where data residency rules are stricter | Medium term (2-4 years) |

| Hospital-to-Home Tele-Monitoring Expansion Requiring Edge Trust | +1.7% | North America and Western Europe, with emerging adoption in South Korea and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Driven Micro-Segmentation Curbs Lateral Breach Spread

AI-driven micro-segmentation has become a practical growth driver because it automates a task that was once too complex for most hospital IT teams. In large health systems, thousands of devices and applications change status constantly, so manual least-privilege rules are hard to keep current without machine learning support. MultiCare Health System used identity-based microsegmentation across more than 40,000 connected devices in 13 hospitals and more than 350 clinics during a 2025-2026 program, and it ran the effort with 2 full-time equivalents against a benchmark of up to 14.[1]PR Newswire, “MultiCare Health System Wins 2026 CSO Award for Microsegmentation Initiative,” PR Newswire, prnewswire.com This operational leverage matters in the AI in healthcare zero-trust security market because hospitals need segmentation that can adapt without interrupting clinical workflows. It also improves protection around imaging systems and other rarely patched assets, which are high-value attack paths in the AI in healthcare zero-trust security market. As more providers look for lower-touch deployment models, automated segmentation is becoming one of the clearest ways to turn zero-trust from concept into day-to-day clinical security practice.

Surge in Ransomware Targeting Connected Medical Devices

The AI in healthcare zero-trust security market is seeing strong demand from the sharp rise in ransomware pressure on healthcare operations. The FBI's Internet Crime Complaint Center logged 278 confirmed healthcare ransomware incidents in 2025, which kept cybersecurity near the top of budget agendas. Verizon's 2026 Data Breach Investigations Report found that ransomware was involved in 48% of healthcare breaches, up from 44%, across 1,492 tracked incidents.[2]Verizon, “Verizon DBIR 2026 Healthcare,” Verizon, hipaajournal.com Source: RunSafe Security, “Medical Device Cybersecurity in 2026, Key Findings,” RunSafe Security, runsafesecurity.com Connected devices widen the problem because 24% of organizations experienced a cyberattack on a connected device in 2026, and 80% of those attacks caused moderate or significant impact on patient care. Remote access exploitation targeting medical devices also rose from 28% in 2025 to 38% in 2026, which shows how attackers are moving toward always-on clinical endpoints. In response, the AI in healthcare zero-trust security market is shifting toward continuous device authentication and fine-grained traffic controls that can block lateral movement without forcing a full device refresh.

Regulatory Push for Zero-Trust in HIPAA and HITECH Updates

Regulatory change is turning the AI in healthcare zero-trust security market into a more predictable spending category. The HHS Notice of Proposed Rulemaking published on January 6, 2025 explicitly listed network segmentation policies designed to limit access and prevent lateral movement by intruders under 45 CFR 164.312. The same proposal also set out prescriptive controls that include encryption for ePHI at rest, TLS 1.2 or higher in transit, multi-factor authentication, biannual vulnerability scanning, and annual penetration testing. This moves hospital security investment away from optional improvement programs and toward audit-driven implementation plans in the AI in healthcare zero-trust security market. Germany is reinforcing the same direction at national infrastructure scale after gematik awarded the zero-trust software development contract for TI 2.0 in July 2025, with productive deployment beginning from July 2026.[3]gematik, “Zero Trust Als Sicherheitsstandard Für Die TI 2.0, Zuschlag Erteilt,” gematik, gematik.deThat combination of threat pressure and compliance enforcement is widening the addressable base for the AI in healthcare zero-trust security market across both providers and digital health infrastructure operators.

Rapid Cloud Adoption of Electronic Health Records

Cloud migration is strengthening the AI in healthcare zero-trust security market because healthcare applications now depend on application programming interfaces, session-level controls, and distributed access patterns that older perimeter models do not manage well. When EHR and clinical workloads move into cloud and hybrid settings, each service integration creates a new policy enforcement point that must be verified continuously rather than trusted by default. Healthcare organizations were using an average of 11 different cloud services at the same time in 2025, which increased the number of lateral paths that security teams had to control. The 2024 Change Healthcare breach, which exposed an estimated 190 million records, showed how cross-service trust gaps can scale quickly in healthcare environments. As a result, the AI in healthcare zero-trust security market is seeing faster adoption of cloud workload protection, unified policy planes, and identity-aware controls that can follow users and applications across distributed care settings. This cloud-led architecture shift is also making buyers favor platforms that can secure both workloads and the application interfaces that connect them.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skills Gap in AI-Security DevSecOps Talent | -2.1% | Global, most acute in North America and APAC where AI security roles remain unfilled | Short term (≤ 2 years) |

| Legacy On-Prem Devices Lacking Agent Support | -1.6% | Global, with disproportionate effect in MEA and South America where capital refresh cycles are longer | Medium term (2-4 years) |

| High TCO of Continuous Verification Frameworks | -1.8% | Global, most pronounced in tier-2 and rural healthcare providers | Medium term (2-4 years) |

| Inter-Vendor Algorithmic Bias Risk in Patient-Data Models | -1.0% | North America and EU where AI model governance audits are more advanced | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skills Gap in AI-Security DevSecOps Talent

The main operational restraint on the AI in healthcare zero-trust security market is the shortage of people who can run AI-assisted security programs day to day. ISC2 reported a global cybersecurity workforce gap of more than 4 million professionals in 2025, which leaves many healthcare organizations without enough staff to tune policy engines, review model behavior, or maintain continuous verification. This shortage matters more in lean provider settings, where security teams often have to manage identity, devices, cloud workloads, and compliance with the same limited staff. Even when hospitals buy new platforms, deployment can slow because the hardest work begins after purchase, when teams must define policies, set behavioral baselines, and test exceptions across clinical operations. Smaller and rural providers face the sharpest strain because they cannot spread specialist labor across large estates or dedicated security functions. Vendors that reduce the need for specialist labor through automation and healthcare-specific templates are therefore gaining preference in the AI in healthcare zero-trust security market.

High TCO of Continuous Verification Frameworks

High total cost of ownership remains a clear brake on the AI in healthcare zero-trust security market, especially for tier-2 hospitals and rural systems. A mature zero-trust program adds costs across identity orchestration, behavioral analytics, policy enforcement, device attestation, and around-the-clock monitoring, not just software licenses. The burden rises further when older on-premise devices cannot run modern agents and need compensating controls at the network layer. More than 25% of healthcare organizations still operate medical devices beyond manufacturer end-of-support dates, and each of those assets requires extra containment measures that add cost without simplifying operations. ISC2 also found that zero trust dropped as a prioritized skill from 27% of respondents in 2024 to 24% in 2025, which suggests some organizations are pacing deployments as they weigh resource commitments. This is creating room in the AI in healthcare zero-trust security market for agentless visibility platforms and hybrid enforcement models that lower implementation costs around legacy estates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Segment Anchors Enterprise-Grade Zero-Trust Deployments

Solutions held 54.32% of the AI in healthcare zero-trust security market share in 2025, and is also projected to grow at 21.44% CAGR through 2031, which shows that software platforms still form the base layer of deployment. This category includes micro-segmentation engines, AI-driven identity and access management, behavioral analytics, and security monitoring integrations that give hospitals the telemetry needed for continuous policy refinement. Healthcare AI generated 71 billion AI and ML transactions across Zscaler's Zero Trust Exchange in 2025, and healthcare was the largest public-sector contributor by volume, which indicates that solution platforms are already handling clinical-scale activity rather than small pilots. This scale helps vendors train detection and access models on real operational behavior instead of relying only on static policy libraries. In the AI in healthcare zero-trust security industry, that feedback loop makes solution platforms harder to displace once they are embedded in clinical operations.

Services remain important because many health systems still need managed detection and response, implementation support, and compliance guidance around zero-trust rollouts. Service providers also help hospitals adapt generic platforms to medical device estates, clinical application flows, and audit documentation needs. Over time, the AI in healthcare zero-trust security market is likely to see services shift from basic deployment work toward model validation, audit support, and policy design for complex clinical environments.

By Deployment Mode: Cloud Architecture Drives the Fastest Adoption Cycle

Cloud held 56.34% share in the market and is also the fastest-growing deployment mode, with AI in healthcare zero-trust security market size for cloud-based delivery projected to rise at 22.25% CAGR through 2031. This growth reflects the need for one policy plane across hospitals, clinics, remote staff, and third-party applications that do not sit inside a single network boundary. Cloud delivery also gives buyers elasticity, so policy and inspection capacity can expand with admissions spikes, remote consultations, or data-intensive AI workloads. Illumio introduced an agentless visibility and breach containment platform for hybrid environments in February 2026, using existing firewall telemetry from Check Point and Fortinet to extend protection across mixed estates. That approach fits the AI in healthcare zero-trust security market because healthcare buyers want cloud-scale policy control without leaving older on-premise assets unmanaged.

On-premise deployment still holds a defined role in academic medical centers, government health systems, and research settings where air-gap requirements or data residency concerns limit full cloud migration. The hybrid model is therefore common, with centralized policy and distributed enforcement working together across cloud and local infrastructure. Healthcare organizations were using an average of 11 different cloud services at the same time in 2025, which helps explain why uniform policy is hard to maintain without a blended approach.

By Application: EHR and EMR Dominance Masks Faster Growth in Clinical Data Protection

EHR and EMR security accounted for 49.52% of revenue in 2025, which keeps the core clinical record system at the center of spending priorities. These systems carry the largest concentration of electronic protected health information and remain primary ransomware targets in healthcare environments. The January 2025 HHS proposal makes that focus more durable because mandatory segmentation, vulnerability scanning, and penetration testing apply directly to systems that handle electronic protected health information. This gives the AI in healthcare zero-trust security market a recurring compliance anchor around the applications that providers cannot take offline and cannot leave under legacy trust models. It also helps explain why EHR protection remains the entry point for broader zero-trust adoption across identity, workload, and data layers.

Clinical data protection is the fastest-growing application, with AI in healthcare zero-trust security market size for this segment projected to expand at 21.68% CAGR through 2031. Proofpoint reported in 2025 that 60% of healthcare organizations had difficulty protecting confidential data used within AI systems, which shows why access control at the data level is becoming more urgent. This pressure is stronger in fields such as oncology, genomics, and distributed diagnostics, where data collaboration is valuable but centralizing sensitive records is not always practical. Medical device and healthcare cloud workload security are also expanding because connected endpoints and distributed applications create more sessions, interfaces, and service links that need verified access

By End User: Pharma Sector's Faster Growth Reveals Clinical Trial Security Gap

Healthcare providers held 48.49% of total end-user revenue in 2025, reflecting the scale of their EHR estates, connected devices, and daily clinical access events. Provider organizations also carry the heaviest concentration of clinical workflows that cannot tolerate downtime or false-positive disruption. Proofpoint found that 96% of healthcare organizations experienced at least 2 data loss incidents involving sensitive healthcare data over the prior 2 years, which helps explain why provider spending remains the largest base in this market. Covered entities also sit closest to HIPAA enforcement, so their buying decisions often start with compliance exposure and then widen into broader cyber resilience planning. In the AI in healthcare zero-trust security industry, providers remain the most immediate revenue pool because they combine the highest operational exposure with the most urgent audit risk.

Pharmaceutical and biotech companies are projected to grow at 22.86% CAGR through 2031, making them the fastest-growing end-user group. Their security model is changing because decentralized trials, cross-border research collaboration, and AI-led drug discovery distribute patient and trial data across many organizations and jurisdictions. That creates a wider trust perimeter than most hospital campuses, which is why the AI in healthcare zero-trust security market is finding strong expansion room in clinical data protection, identity governance, and partner access control for this group. The same pattern also raises demand for detailed audit trails because regulated trial data must move across sponsors, sites, contract research organizations, and remote patient endpoints. Payers and other healthcare entities are also steadily adopting these platforms as automated claims, digital ecosystems, and business associate obligations bring more sensitive workflows under policy-based verification.

Geography Analysis

North America held 49.36% of the AI in healthcare zero-trust security market share in 2025, giving the region the largest installed base and the strongest near-term buying power. The United States leads that position because it combines high breach exposure with proposed HIPAA changes that make microsegmentation a required control rather than a flexible option. Healthcare data breach costs in the United States reached USD 10.93 million in 2024, which gave boards a clear financial case for stronger access control and containment. Canada and Mexico add to regional growth through healthcare digitization and hospital network expansion, even though their adoption pace remains below the United States. Through 2031, the AI in healthcare zero-trust security market should keep finding stable demand in North America because compliance deadlines, insurer pressure, and enterprise procurement are moving in the same direction.

Asia-Pacific is projected to grow at 23.27% CAGR through 2031, making it the fastest-growing regional pocket. The region is expanding because digital health programs in India, Japan, South Korea, China, and Australia are increasing the number of cloud-connected records, devices, and remote care workflows that need verified trust controls. This creates a large runway for the AI in healthcare zero-trust security market, especially where governments are building national health data infrastructure and providers are moving into more connected care models. Providers in the region are also balancing growth with data residency rules, which makes federated learning and edge security a practical fit. The growth profile is also supported by stricter data governance expectations, which make privacy-preserving analytics and edge-based security more relevant across APAC deployments.

Europe holds a significant position in the market, with Germany setting the strongest formal direction through its TI 2.0 zero-trust program. The United Kingdom, France, Italy, and Spain are also advancing along the same path as critical-sector cyber rules and health system modernization programs push security spending higher. The Middle East, Africa, and South America remain earlier-stage opportunities in the AI in healthcare zero-trust security market, with adoption led by GCC digital health programs while broader uptake is still held back by slower capital refresh cycles.

Competitive Landscape

The AI in healthcare zero-trust security market shows moderate concentration at the top tier, where large integrated vendors compete for enterprise-wide mandates and specialist players focus on device and hybrid gaps. Platform unification is the main strategy because providers want identity, network, endpoint, and cloud policy in fewer tools. Cisco also announced its intent to acquire Astrix Security in 2026, which points to growing concern around non-human identities and automated workflows in zero-trust environments. These moves show that the AI in healthcare zero-trust security market is shifting from isolated point controls toward broader identity-led security platforms.

Competition is also widening around AI-native protection for applications and workflows that sit outside the classic hospital perimeter. CrowdStrike announced the acquisition of Pangea in September 2025 to extend Falcon with AI Detection and Response capabilities, which aligns with the rising use of AI models inside healthcare operations. Illumio's February 2026 launch of agentless visibility and breach containment for hybrid environments targeted another gap that matters in the AI in healthcare zero-trust security market, namely older devices and workloads that cannot support modern agents. Smaller vendors such as Cynerio and Medigate, now part of Claroty, remain relevant where buyers want deeper IoMT discovery and clinical asset context than generalist platforms usually provide. This mix of large suites and focused specialists keeps competitive pressure high even when large vendors dominate major enterprise deals.

The open space in the market is clearest around hospital-to-home monitoring, decentralized trials, and legacy medical devices, where trust must be enforced across fragmented environments and many third parties. NIST's telehealth smart home guidance from late 2025 made clear that connected home care workflows bring cybersecurity and privacy risks that still lack fully standardized implementation approaches. That is why the AI in healthcare zero-trust security market continues to reward vendors that can combine agentless containment, healthcare-specific policy templates, and compliance-ready reporting. Procurement barriers such as HITRUST and FedRAMP alignment also favor established platforms, which shortens the runway for undifferentiated entrants and supports continued consolidation.

AI In Healthcare Zero-Trust Security Industry Leaders

Palo Alto Networks

IBM

Cisco Systems

Microsoft Corporation

Fortinet

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: IGEL and Zscaler released joint Healthcare Security Blueprints for Distributed Care Delivery at HIMSS26 Europe in Copenhagen, providing architectural guidance covering PHI protection, distributed endpoint security using IGEL's immutable OS, and operational continuity planning for clinics and remote care settings.

- April 2026: Palo Alto Networks announced its intent to acquire Portkey, an AI Gateway security company processing trillions of tokens monthly, to build centralized control-plane governance for autonomous AI agents across enterprise healthcare deployments.

- April 2026: Palo Alto Networks completed the acquisition of Koi, establishing a new product category called Agentic Endpoint Security (AES) to secure AI coding agents and autonomous endpoint tools operating within clinical workflows.

Global AI In Healthcare Zero-Trust Security Market Report Scope

According to the report’s scope, the AI in healthcare zero-trust security market refers to the use of artificial intelligence-driven security solutions that apply the zero-trust model in healthcare environments, where no user, device, or application is automatically trusted. These solutions continuously verify access, detect threats, monitor network activity, and protect sensitive healthcare data, helping organizations strengthen cybersecurity, ensure regulatory compliance, and safeguard patient information.

The AI in healthcare zero-trust security market is segmented into component, deployment mode, application, end user, and geography. By component, the market is segmented into solutions and services. By deployment mode, the market is segmented into cloud and on-premise. By application, the market is segmented into clinical data protection, medical device and IoMT security, EHR and EMR security, healthcare cloud workload security, and others. By end user, the market is segmented into healthcare providers, pharmaceutical and biotech companies, healthcare payers, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Solutions |

| Services |

| Cloud |

| On-Premise |

| Clinical Data Protection |

| Medical Device and IoMT Security |

| EHR and EMR Security |

| Healthcare Cloud Workload Security |

| Others |

| Healthcare Providers |

| Pharmaceutical and Biotech Companies |

| Healthcare Payers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Solutions | |

| Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By Application | Clinical Data Protection | |

| Medical Device and IoMT Security | ||

| EHR and EMR Security | ||

| Healthcare Cloud Workload Security | ||

| Others | ||

| By End User | Healthcare Providers | |

| Pharmaceutical and Biotech Companies | ||

| Healthcare Payers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 outlook for AI in healthcare zero-trust security?

The market is projected to reach USD 4.95 billion by 2031 from USD 1.95 billion in 2026, growing at 20.48% CAGR over 2026-2031.

Which component currently leads spending?

Solutions led with 54.32% of revenue in 2025, supported by demand for micro-segmentation, identity controls, behavioral analytics, and monitoring integrations.

Which deployment model is growing the fastest?

Cloud is expected to be the fastest-growing deployment mode at 22.25% CAGR through 2031 because healthcare environments increasingly span hospitals, remote staff, cloud records, and hybrid applications.

Which application area is expanding the fastest?

Clinical data protection is projected to grow at 21.68% CAGR through 2031 as healthcare organizations try to secure confidential data used inside AI systems and distributed analytics workflows.

Page last updated on: