AI-based Infection Control Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

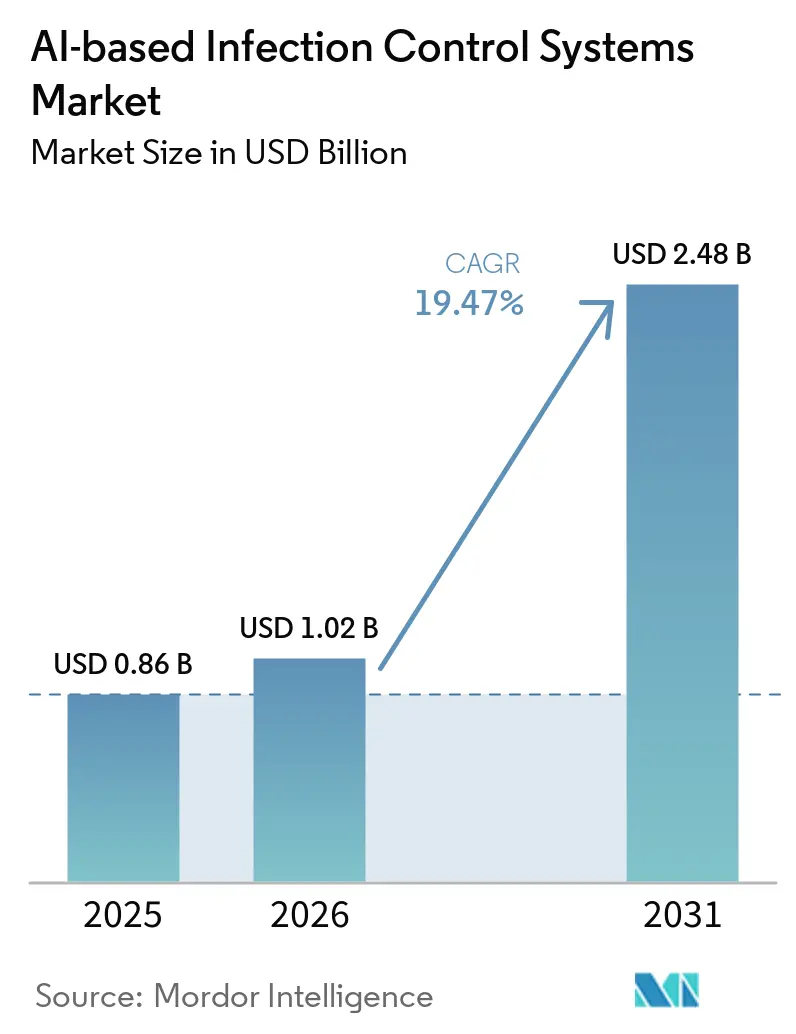

| Market Size (2026) | USD 1.02 Billion |

| Market Size (2031) | USD 2.48 Billion |

| Growth Rate (2026 - 2031) | 19.47% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-based Infection Control Systems Market Analysis by Mordor Intelligence

The AI-based Infection Control Systems Market size is expected to grow from USD 0.86 billion in 2025 to USD 1.02 billion in 2026 and is forecast to reach USD 2.48 billion by 2031 at 19.47% CAGR over 2026-2031.

The growth path reflects the persistent burden of healthcare-associated infections, with nearly 1.7 million hospitalized patients in the United States contracting HAIs each year and the related economic loss reaching USD 28 billion to USD 45 billion annually. Demand is also rising because infection prevention teams still spend large portions of their time on surveillance work, while hospitals face stricter digital reporting obligations that manual processes cannot support reliably at scale. Better EHR connectivity and broader cloud readiness are expanding the usable data pool for predictive surveillance, antimicrobial stewardship, and workflow automation in the AI-based infection control systems market. The pressure from antimicrobial resistance adds another layer, as the 2024 United Nations General Assembly political declaration set a target to reduce AMR-related deaths by 10% from the 2019 baseline of 4.95 million fatalities, which raises the value of tools that can flag risk earlier and support better antibiotic use. Competition in the AI-based infection control systems market remains moderate to high because specialist surveillance vendors still lead on usability, while larger platform providers are investing in connected care, cloud infrastructure, and broader clinical AI bundles that can narrow those gaps over time.

Key Report Takeaways

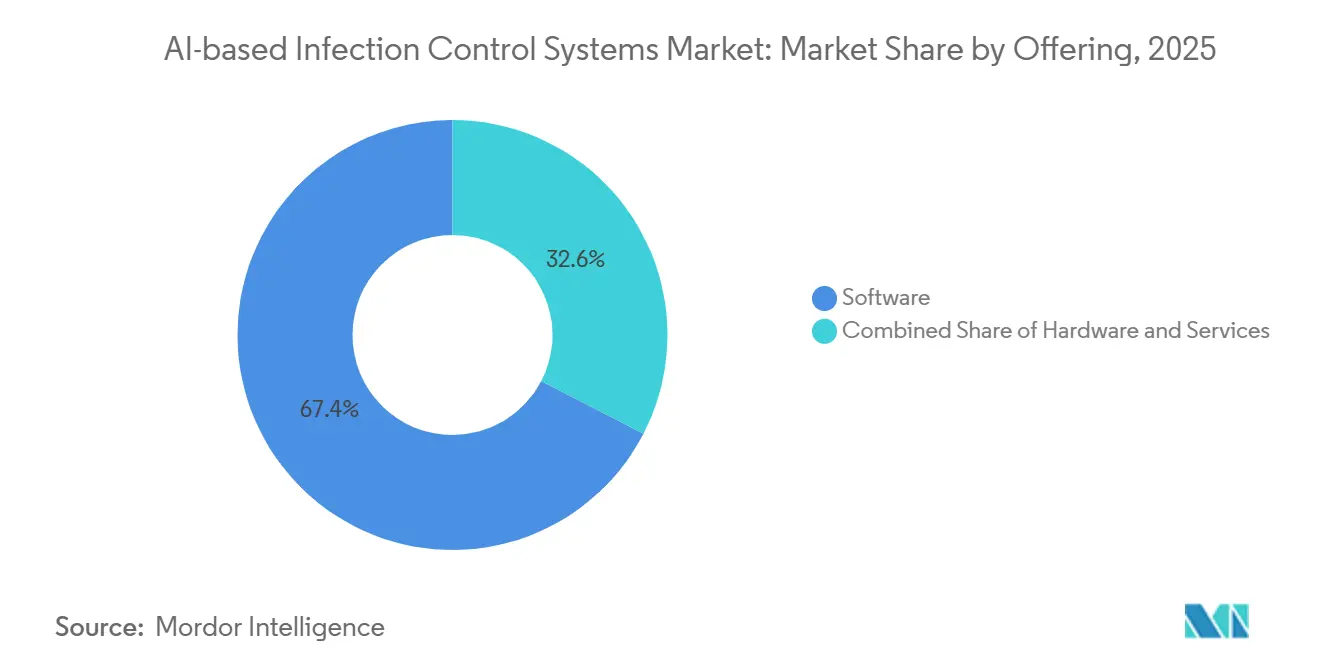

- By offering, software held 67.42% of the AI-based infection control systems market share in 2025, while services are forecast to expand at a 21.89% CAGR through 2031.

- By deployment model, on-premise accounted for 74.78% share of the AI-based infection control systems market size in 2025, while cloud-based deployment is projected to grow at a 22.11% CAGR through 2031.

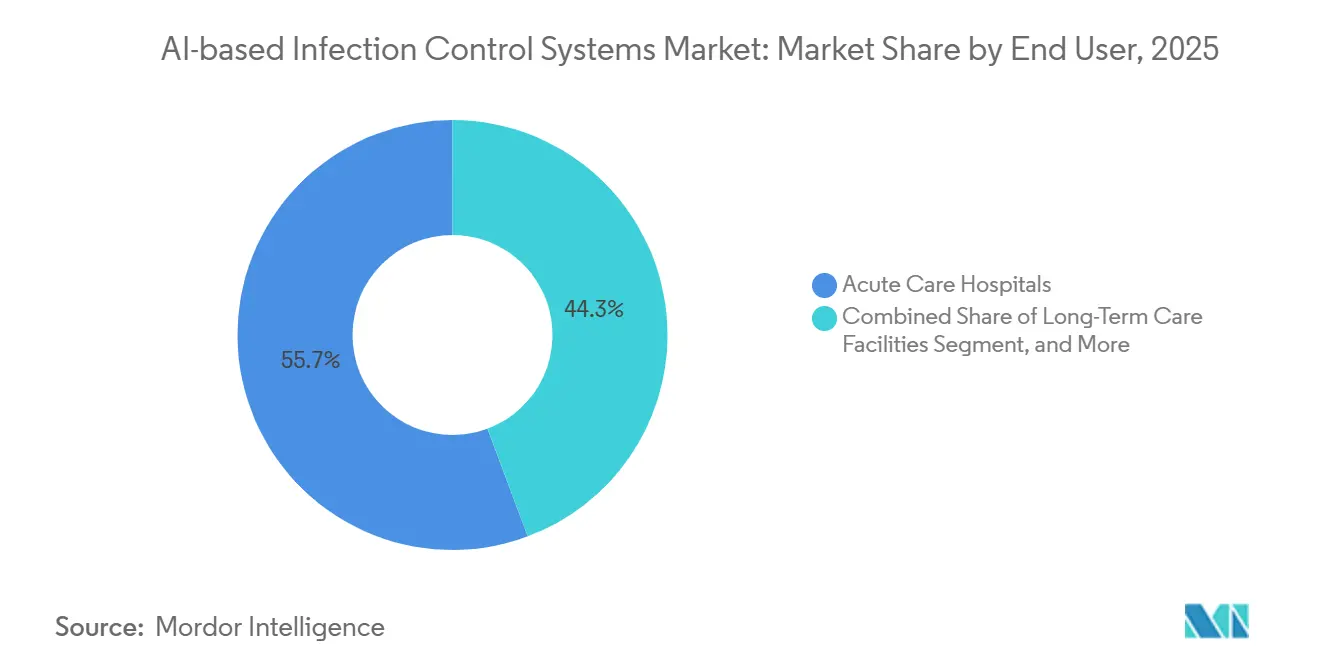

- By end user, acute care hospitals captured 55.73% of the AI-based infection control systems market in 2025, while long-term care facilities are expected to record the fastest growth at a 23.55% CAGR through 2031.

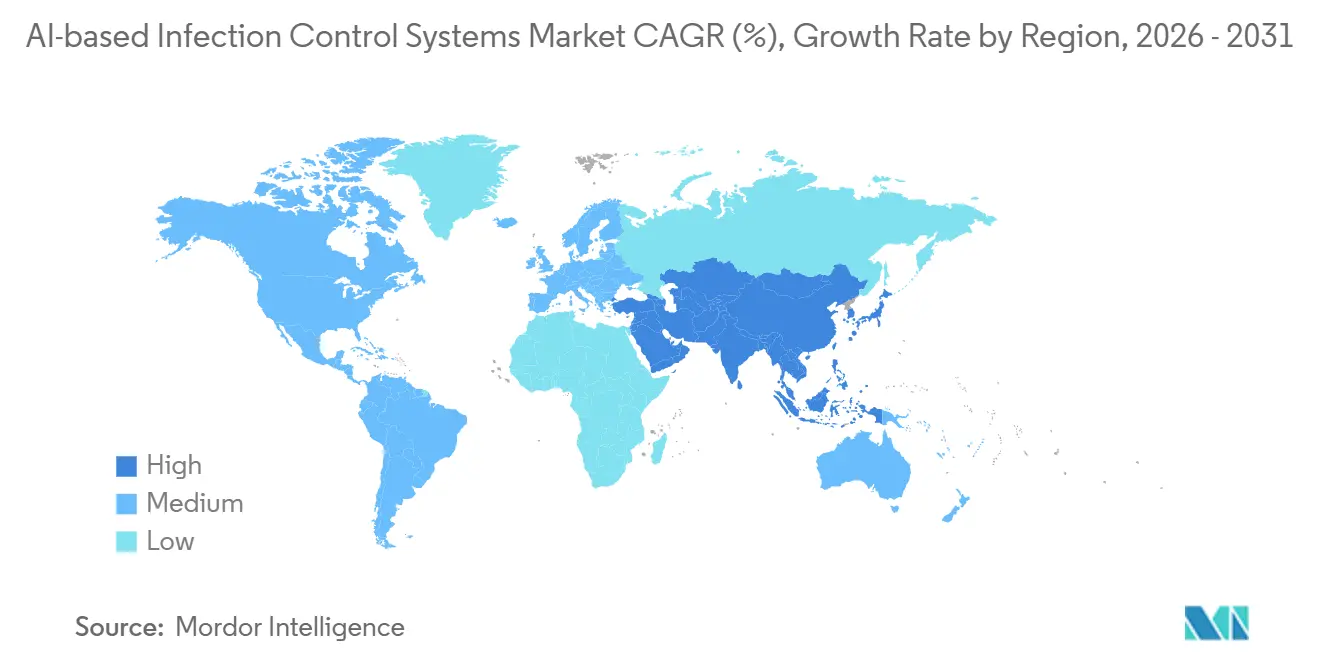

- By geography, North America led with 39.23% share in 2025, while Asia-Pacific is set to advance at a 23.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-based Infection Control Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising HAI And AMR Burden | +4.5% | Global, with acute concentration in North America, EU, and South and Southeast Asia | Short term (≤ 2 years) |

| Tightening Infection Reporting Mandates | +3.2% | North America and EU | Short term (≤ 2 years) |

| EHR And Clinical Data Interoperability Expansion | +2.8% | Global, with early gains in the United States, Germany, Denmark, and Australia | Medium term (2-4 years) |

| Growth In Cloud-Based Surveillance Adoption | +2.5% | Global, with spillover to MEA and South America through SaaS models | Medium term (2-4 years) |

| Infection Prevention Workforce Shortages | +2.2% | North America and EU, with secondary spillover to core APAC markets | Short term (≤ 2 years) |

| Privacy-Preserving Ambient Sensing Adoption | +1.5% | North America and core APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising HAI and AMR Burden

The clinical case for the AI-based infection control systems market starts with a burden that manual surveillance has not contained. A 2024 systematic review found that infection preventionists spend nearly half of their work hours on surveillance-related tasks, while HAI incidence in ICUs ranged from 17% in neonatal units to 68% in adult critical care units globally. The same review noted that hospital-acquired bloodstream infections carry a 10% to 20% mortality rate and add nearly USD 40,000 in cost per surviving patient, which keeps the financial case for earlier detection very clear. Published studies also show that AI-enabled surveillance can reduce HAI incidence from 1.31% to 0.58% and cut manual chart review workloads by 83.9%, which gives hospital buyers a direct link between automation and labor relief.[1]Rabie Adel El Arab et al., “Artificial Intelligence in Hospital Infection Prevention, An Integrative Review,” Frontiers in Public Health, frontiersin.org The pressure rises further as antimicrobial resistance remains a central policy focus, with the UN target tied to the 2019 baseline of 4.95 million deaths and global antibiotic consumption expected to rise by more than 30% by 2030. That combination keeps predictive surveillance and stewardship tools near the center of adoption decisions across the AI-based infection control systems market.

Tightening Infection Reporting Mandates

Regulation is turning procurement into a compliance decision for many hospitals in the AI-based infection control systems market. Since January 2024, the CMS Medicare Promoting Interoperability Program has required eligible hospitals and critical access hospitals to submit antimicrobial use and resistance data to the CDC’s NHSN. By 2024, 73% of hospitals were meeting the requirement through a mix of automated and manual methods, but 57% identified AUR reporting as their most difficult public health reporting task, which shows where manual workflows still break down.[2]Priscilla Owusu-Mensah and Chelsea Richwine, “Electronic Public Health Reporting Among Non-Federal Acute Care Hospitals, 2024,” ASTP Data Brief No. 78, healthit.gov CMS also tied fiscal year 2026 payment exposure to HAI-related performance under the HAC Reduction Program, including CLABSI, CAUTI, MRSA bacteremia, CDI, and surgical site infection measures.[3]Centers for Medicare & Medicaid Services, “Hospital-Acquired Condition Reduction Program Fiscal Year 2026 Key Dates,” Centers for Medicare & Medicaid Services, cms.gov The fiscal year 2026 proposed IPPS rule moves further toward digital quality measurement using FHIR standards, which will increase the value of platforms that can capture, normalize, and transmit infection data in real time.

EHR and Clinical Data Interoperability Expansion

Interoperability is a core performance driver in the AI-based infection control systems market because model quality depends on how much clinical context the system can use. Studies reviewed in 2025 showed that AI models connected to EHR data through methods such as neural networks, decision trees, and random forests regularly achieved area-under-the-curve results above 0.80 for predicting surgical site infection and urinary tract infection risk. Hospitals using leading EHR environments also participated in 6.7 types of electronic public health reporting on average, compared with 5.8 among other systems, which widens the input advantage for surveillance tools that rely on structured reporting pipelines. Germany’s RISK PRINCIPE program shows how this works in practice, with interoperable data integration centers supporting semi-automated hospital-onset bacteremia surveillance and published results from Charité Berlin covering 3.6 million patient-days with 14-day case fatality monitoring. The European Health Data Space, enacted in 2025, should steadily widen the data environment available to certified tools, which supports further scaling in the AI-based infection control systems market.

Growth in Cloud-Based Surveillance Adoption

Cloud delivery is changing the economics of the AI-based infection control systems market because it lowers infrastructure burden and shortens update cycles. Cloud-native surveillance platforms can push continuous model updates, support benchmarking across sites, and reduce the up-front capital intensity that often slows adoption in smaller hospitals and long-term care settings. BD’s October 2025 launch of the Incada Connected Care Platform on AWS showed how vendors are packaging medication, infection, and device data into a single cloud-based analytics layer with natural language query features. Kontakt.io’s installed base of more than 4 million devices and its infrastructure-led deployment approach also show how cloud and managed service models are removing physical infrastructure as a major constraint for real-time monitoring environments. In France, AP-HP reported nearly 300 internal AI initiatives as of June 2025, with cloud data warehouse architecture supporting much of that activity, which signals that large hospital systems are already building the foundation that future AI-based infection control systems market growth will use.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Deployment And Validation Costs | -2.1% | Global, with the highest pressure in LMICs, rural North America, and Southern and Eastern Europe | Short term (≤ 2 years) |

| Data Privacy And Cybersecurity Concerns | -1.8% | North America and EU, with secondary spillover to APAC | Medium term (2-4 years) |

| Workflow Integration And Interoperability Gaps | -1.4% | Global, concentrated in fragmented or legacy EHR environments | Medium term (2-4 years) |

| Alert Fatigue And Model Generalizability Limits | -1.2% | Global, strongest in ICU and other high-acuity acute care settings | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Deployment and Validation Costs

Cost remains a real barrier in the AI-based infection control systems market because implementation goes well beyond software licensing. Hospitals still need data integration work, workflow redesign, user training, and local validation before infection surveillance models can be trusted in daily practice. The burden is heavier in systems with limited digital maturity, and Germany’s DigitalRadar 2024 average of 42 out of 100 shows that even funded hospital systems can still lack the foundation needed for easy AI deployment. Validation also remains a live concern because independent reviews have shown that AI performance can weaken outside controlled deployment settings, which forces providers to budget for monitoring and retraining after go-live. These factors slow decisions in mid-sized hospitals, rural facilities, and lower-resource settings where infection control needs are high, but capital and technical staffing remain limited.

Data Privacy and Cybersecurity Concerns

Privacy and security rules are raising the deployment threshold for the AI-based infection control systems market. The January 2025 HHS proposed update to the HIPAA Security Rule expands risk analysis expectations for tools that access electronic protected health information, including AI systems that touch training data and model outputs. In Europe, the EU AI Act classifies many medical AI applications as high risk, which adds documentation, oversight, and conformity demands that can stretch implementation timelines. These rules do not stop adoption, but they do favor vendors that can show mature governance, certified controls, and clear auditability. Smaller suppliers without that compliance depth face longer sales cycles and a narrower path into large hospital systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Entrenched, Services Accelerating on Deployment Demand

Software held 67.42% of the AI-based infection control systems market share in 2025, which reflects the scalability of analytics and surveillance platforms compared with hardware-led deployments. This lead also mirrors how hospitals buy, because most providers prefer a software layer that can sit on top of existing EHR, laboratory, and pharmacy systems instead of replacing physical infrastructure. Products such as Wolters Kluwer’s Sentri7 show why software remains entrenched, with the platform ranking first in KLAS for infection control and monitoring in 2026 and reinforcing the value of usable surveillance workflows for clinical teams. The software-heavy mix also fits a budget pattern where infection prevention teams continue to prioritize automation tools that reduce manual review, reporting burden, and repetitive follow-up work.

Services in the AI-based infection control systems industry are projected to expand at a 21.9% CAGR through 2031, which makes them the fastest-rising part of the service mix. The growth reflects the practical challenge of integrating AI into heterogeneous hospital environments where validation, tuning, and workflow adaptation continue well after the initial installation. Managed support is becoming more important because providers need help maintaining model performance, aligning alerts to local clinical practice, and keeping reporting outputs consistent with evolving compliance rules. Hardware remains a supporting layer in the AI-based infection control systems industry, but product refreshes such as Vitalacy’s Gen5 wearable and BioVigil’s AccuWash rollout show that badges, sink beacons, and sensing devices still matter where hand hygiene and staff behavior monitoring are core use cases.

By Deployment Model: Legacy On-Premise Share Masks Rapid Cloud Erosion

On-premise deployment accounted for 74.78% share of the AI-based infection control systems market size in 2025, reflecting hospital procurement inertia, data sovereignty needs, and the continued preference for local audit control in regulated clinical settings. Many early installations were built on legacy infrastructure after the pandemic period, and those systems remain tied to multiyear contracts that slow visible share movement even when new demand starts shifting elsewhere. Hospitals also remain cautious when infection data connects to medication records, laboratory systems, and public health reporting, which keeps locally governed environments attractive for large providers. Hybrid models are growing in importance because they let providers retain local EHR connections while moving analytics, dashboards, and benchmarking layers into more flexible architectures.

Cloud deployment in the AI-based infection control systems market is forecast to grow at a 22.1% CAGR through 2031, which signals a faster change in buying behavior than the current installed share suggests. The appeal is straightforward because cloud delivery reduces the need for on-site infrastructure, makes updates easier to manage, and allows faster rollout across multisite systems. BD’s Incada platform on AWS is one of the clearest examples, showing how vendors are building cloud ecosystems that combine device data, clinical signals, and AI-driven analytics in a single environment. The same shift is visible in infrastructure-led models from Kontakt.io and in broader hospital data environments such as AP-HP, where cloud architecture now supports a large internal AI pipeline.

By End User: Acute Care Anchors the Base, Long-Term Care Redefines Growth

Acute care hospitals captured 55.73% of the AI-based infection control systems market in 2025, supported by the highest concentration of device-associated infections, formal reporting obligations, and payment risk tied to HAI performance. This setting also has the strongest need for continuous surveillance across surgery, intensive care, pharmacy, and microbiology workflows, which keeps adoption concentrated in larger hospital systems. Stanford Health Care’s 2026 ChatEHR pilot for surgical site infection surveillance shows how acute care providers are now testing large language model workflows to automate retrospective review and extend surveillance across more procedure types. Ambulatory surgical centers and specialty clinics remain less penetrated, but infection monitoring tools are moving into operating room environments through computer vision, sensing, and environmental monitoring use cases.

Long-term care facilities are expected to expand at a 23.6% CAGR through 2031, making them the fastest-growing end-user group in the AI-based infection control systems market. The growth reflects a patient base that is older, more immunocompromised, and exposed for longer periods, while staffing for infection prevention is usually thinner than in acute care hospitals. AARP’s 2026 review found that most AI use in long-term care is still at the pilot stage and centered on monitoring, assessment, and decision support, which means the segment remains early but has a long runway for commercial adoption. As post-acute providers shift from paper-heavy processes to digital compliance and surveillance workflows, long-term care is set to capture a larger share of new demand in the AI-based infection control systems market.

Geography Analysis

North America held 39.23% of the AI-based infection control systems market share in 2025, which reflects strong regulatory infrastructure, a large NHSN-reporting hospital base, and a vendor ecosystem centered in the United States. The region’s demand accelerated after CMS made AUR reporting mandatory from January 2024 for eligible hospitals and critical access hospitals under the Promoting Interoperability Program. By 2024, 73% of hospitals were already submitting AUR data, but 57% still identified that requirement as their most difficult reporting task, which directly supports demand for automated surveillance platforms. North America also benefits from a dense field of established vendors and reference sites that make procurement less experimental than in many other regions. Platforms such as Sentri7 and Premier’s clinical surveillance tools continue to benefit from this environment because hospitals want measurable workflow savings and easier public health reporting.

Europe remains an important part of the AI-based infection control systems market because funding support, public digital health policy, and research networks are moving in the same direction, even if implementation is uneven across the region. Germany’s Krankenhauszukunftsgesetz created a EUR 50 billion fund, equivalent to USD 53.5 billion, for hospital transformation, yet the 2024 DigitalRadar average of 42 out of 100 still shows that digital readiness remains incomplete. The RISK PRINCIPE consortium and the Charité surveillance work show that interoperable data pipelines can already produce hospital-onset bacteremia monitoring at scale, which gives Europe a solid research-to-deployment bridge. France’s AP-HP also reported nearly 300 internal AI initiatives by mid-2025, while the EU AI Act and the European Health Data Space are likely to concentrate growth around vendors that can meet strict certification and data governance requirements.

Asia-Pacific AI-based infection control systems market size is projected to expand at 23.5% CAGR through 2031, making it the fastest-growing regional block. Growth in this region reflects more than headline HAI burden, because governments and health systems are also building stronger infectious disease intelligence and hospital data infrastructure. Japan’s establishment of the Japan Institute for Health Security in April 2025 supports that direction by creating a more centralized infectious disease intelligence framework, while hospital-level AI readiness continues to improve in parallel. India and other emerging Asian markets add a different demand profile, where ICU infection rates remain high and lighter surveillance tools can be attractive when full EHR integration is not yet available. The Middle East and Africa and South America remain smaller parts of the AI-based infection control systems market, but growth should follow hospital digitization, GCC healthcare infrastructure investment, and gradual modernization of public networks in countries such as Brazil.

Competitive Landscape

The AI-based infection control systems market is moderately fragmented, with software-led clinical surveillance vendors competing alongside RTLS and sensing specialists that approach infection control through workflow visibility. Wolters Kluwer remains one of the clearest software leaders, and Sentri7’s repeated first-place KLAS performance supports its standing with infection prevention teams that want usable surveillance tools rather than deeply embedded but less adaptable modules. Hardware-anchored players such as Kontakt.io, Sonitor Technologies, and Cognosos are also moving beyond location tracking toward broader hand hygiene, patient flow, and clinical contact monitoring use cases. This means competition is no longer limited to stand-alone infection surveillance software, because vendors are bundling medication data, location intelligence, environmental signals, and workflow automation into broader connected care offers. The result is a shorter differentiation window for pure-play specialists in the AI-based infection control systems market.

A clear pattern in the AI-based infection control systems market is platform convergence through product expansion, partnerships, and selective consolidation. Sonitor’s enterprise platform expansion in late 2025 and the Sonitor-Tagnos merger logic both point to the value of combining location data with workflow orchestration in a single stack. BD is pushing the same direction from a different starting point, using the Incada platform and related hospital partnerships to connect medication, infusion, and analytics environments under one AI-enabled architecture. Oracle Health’s 2025 cloud-native, AI-first EHR launch also shows that large health IT vendors see infection-related surveillance and workflow use cases as part of a wider clinical AI opportunity. These moves keep the field open, but they also raise the bar for smaller vendors that cannot match integration breadth or compliance depth.

White-space demand remains visible in post-acute care, ambulatory surgery, and lower-resource hospital settings where surveillance needs are real but enterprise-grade infrastructure is not always available. That leaves room for cloud-delivered offerings, lighter integration models, and workflow tools that do not depend on a full hospital IT rebuild. BioVigil’s performance disclosure in 2026, including sustained HAI reduction and large gains in captured hand hygiene opportunities, shows why buyers are increasingly looking for proof tied to operational outcomes rather than technical claims alone. At the same time, HIPAA compliance demands and the EU AI Act’s high-risk requirements make scale, governance, and certification more important in vendor selection, which gives established players an advantage even as the AI-based infection control systems market continues to broaden.

AI-based Infection Control Systems Industry Leaders

Becton, Dickinson and Company

Epic Systems Corporation

Ecolab Inc.

Oracle Corporation

PatientVoice AI, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Epic Systems launched county-level communicable disease Health Alerts powered by its Cosmos database (300 million patient records, 2,067 hospitals, 47,000+ clinics), using the Farrington Improved Algorithm to detect year-over-year anomalies for measles, strep, and viral gastroenteritis, the first population-scale real-time epidemiological alert system embedded in an EHR at this geographic granularity.

- March 2026: BD (Becton, Dickinson and Company) announced a strategic partnership with Wellstar Health System to integrate BD Pyxis Pro medication dispensing with BD Alaris Infusion Systems via the AI-powered Incada platform, extending enterprise-wide AI-driven medication-infection workflow connectivity across one of the US's largest health systems.

- March 2026: Kontakt.io launched its Universal Dispenser Module, a vendor-agnostic AI hand hygiene solution compatible with any hospital dispenser, using RTLS to alert nurses before patient room entry, the company cited a 45% reduction in central line infections and 55% in catheter-associated UTIs across deployments.

- March 2026: BD and Sinteco established a technological partnership to deploy advanced pharmaceutical robotics and AI-driven medication traceability across European hospitals, automating unit-dose packaging to reduce human error in medication preparation, a move that extends BD's infection risk mitigation capabilities into pharmacy workflows.

Global AI-based Infection Control Systems Market Report Scope

The AI-Based Infection Control Systems Market refers to the industry segment providing software, hardware, and services that use artificial intelligence (AI) and machine learning (ML) to proactively prevent, detect, and manage infections, primarily within healthcare facilities.

The AI-Based Infection Control Systems Market Report is segmented across multiple dimensions to provide a comprehensive view of industry dynamics. By offering, the market is categorized into software, hardware, and services. In terms of deployment models, the market is categorized into cloud-based, on-premise, and hybrid systems. The end-user landscape includes acute care hospitals, long-term care facilities, ambulatory surgical centers, clinics, and specialty centers. Geographically, the market spans North America, Europe, Asia-Pacific, Middle East and Africa, and South America. Forecasts are provided in terms of market value (USD), offering insights into growth potential and investment opportunities across these segments.

| Software |

| Hardware |

| Services |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Acute Care Hospitals |

| Long-Term Care Facilities |

| Ambulatory Surgical Centers |

| Clinics and Specialty Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Offering | Software | |

| Hardware | ||

| Services | ||

| By Deployment Model | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By End User | Acute Care Hospitals | |

| Long-Term Care Facilities | ||

| Ambulatory Surgical Centers | ||

| Clinics and Specialty Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the AI-based infection control systems space in 2026?

It is valued at USD 1.02 billion in 2026 and is forecast to reach USD 2.48 billion by 2031, growing at a 19.47% CAGR over 2026-2031.

What is driving hospital demand for AI-enabled infection surveillance?

The main demand drivers are the ongoing burden of HAIs, increasing AMR pressure, workforce strain in infection prevention, and mandatory digital reporting requirements from regulators.

Which offering category leads current revenue?

Software leads with 67.42% share in 2025 because hospitals prefer scalable analytics and surveillance layers that can connect with existing clinical systems.

Which deployment model is growing the fastest?

Cloud-based deployment is growing the fastest at a 22.11% CAGR through 2031 as providers look for lower infrastructure burden, faster updates, and multisite scalability.

Which region is expanding the quickest?

Asia-Pacific is the fastest-growing region with a 23.46% CAGR through 2031, supported by rising infection burden, stronger disease intelligence systems, and broader hospital digitization.

Page last updated on: