AI In Healthcare Data Monetization Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

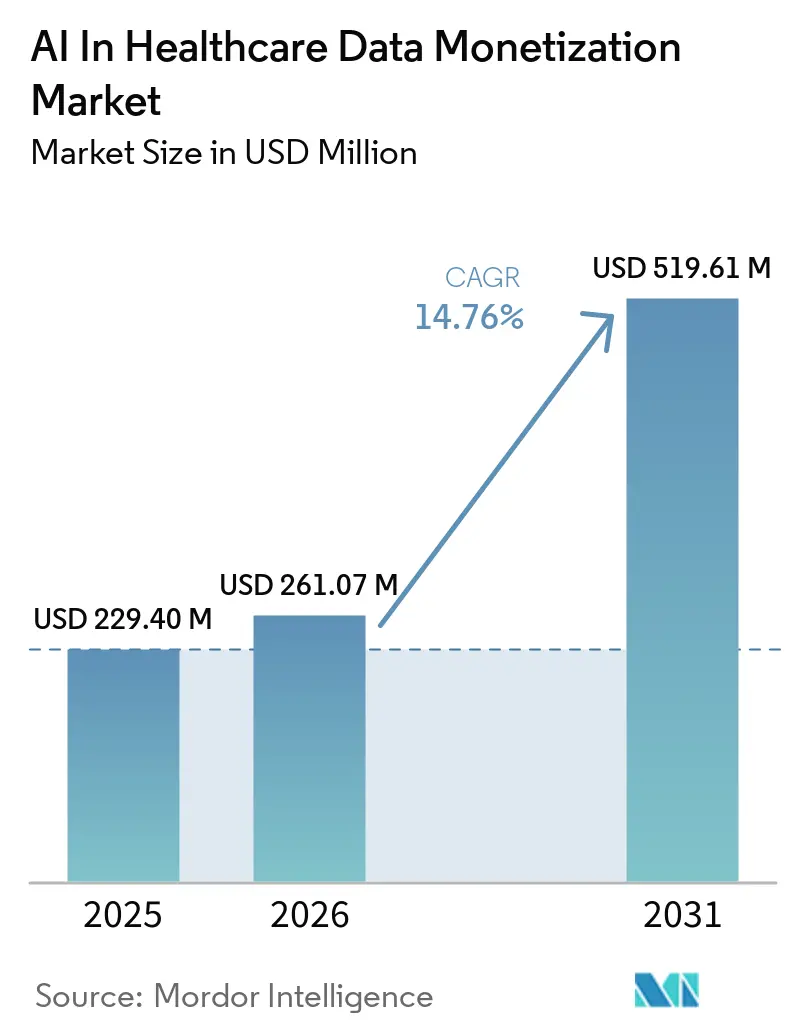

| Market Size (2026) | USD 261.07 Million |

| Market Size (2031) | USD 519.61 Million |

| Growth Rate (2026 - 2031) | 14.76% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Healthcare Data Monetization Market Analysis by Mordor Intelligence

The AI in healthcare data monetization market is expected to grow from USD 229.40 million in 2025 to USD 261.07 million in 2026 and is forecasted to reach USD 519.61 million by 2031 at 14.76% CAGR over 2026-2031. This expansion reflects a clear structural change, because health systems, payers, and life sciences companies are now treating fragmented clinical, claims, and operational records as managed commercial assets within the AI in healthcare data monetization market. AI is central to that change, since it can curate, connect, and summarize data that previously remained too fragmented or too unstructured to support repeatable commercial use. Governance frameworks are also becoming more usable at the same time, and this is opening datasets that had remained locked because legal review, secondary-use controls, and compliance risk were too difficult to manage under older models. The contrast with the pre-2020 period remains stark, because data monetization was not a formal revenue category for most health systems and rarely shaped capital allocation in a serious way before digitalization accelerated. Competition is therefore moving beyond simple ownership of records, and the main opportunity areas in the AI in healthcare data monetization market now sit in data lineage, privacy-safe access, unstructured data curation, and the infrastructure needed for secondary use across research, reimbursement, and operational settings.

Key Report Takeaways

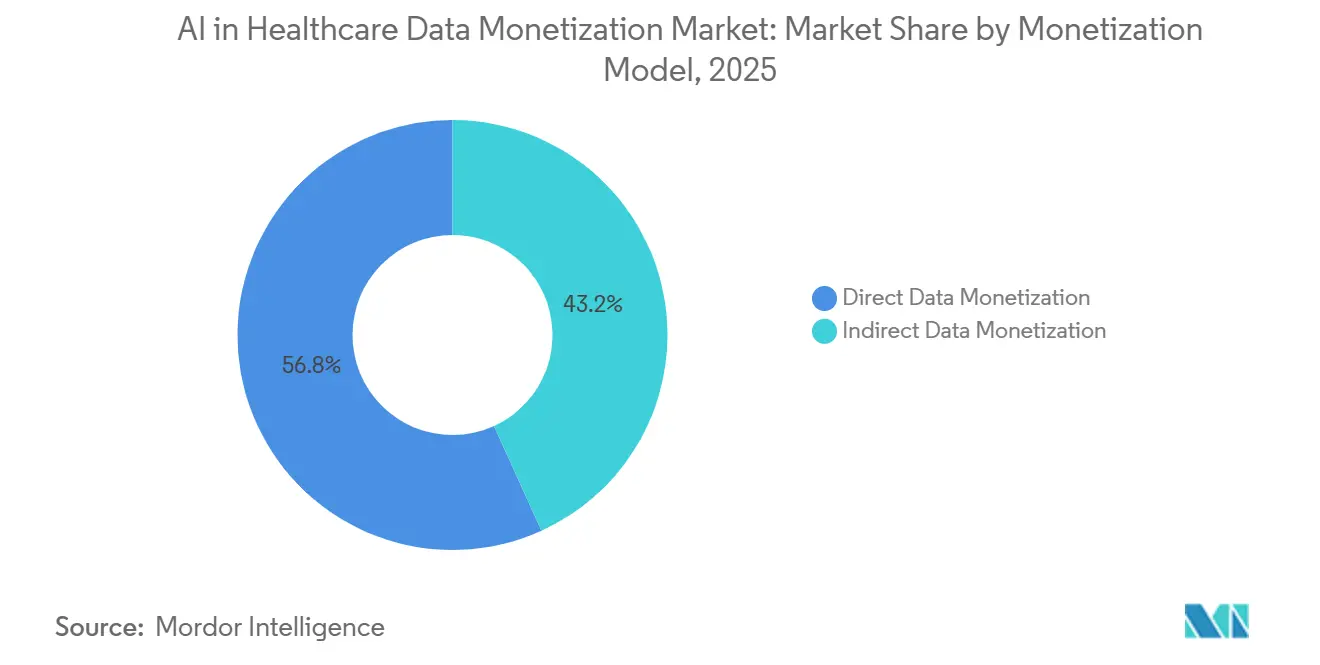

- By monetization model, direct data monetization held 56.76% of revenue in 2025, and the same segment is expected to grow at a 16.11% CAGR through 2031.

- By solution type, data monetization platforms held 44.33% of revenue in 2025, while data-as-a-service (DaaS) is projected to grow at a 16.76% CAGR through 2031.

- By data type, claims and financial data accounted for 45.59% of revenue in 2025, while clinical data is forecasted to expand at a 15.88% CAGR through 2031.

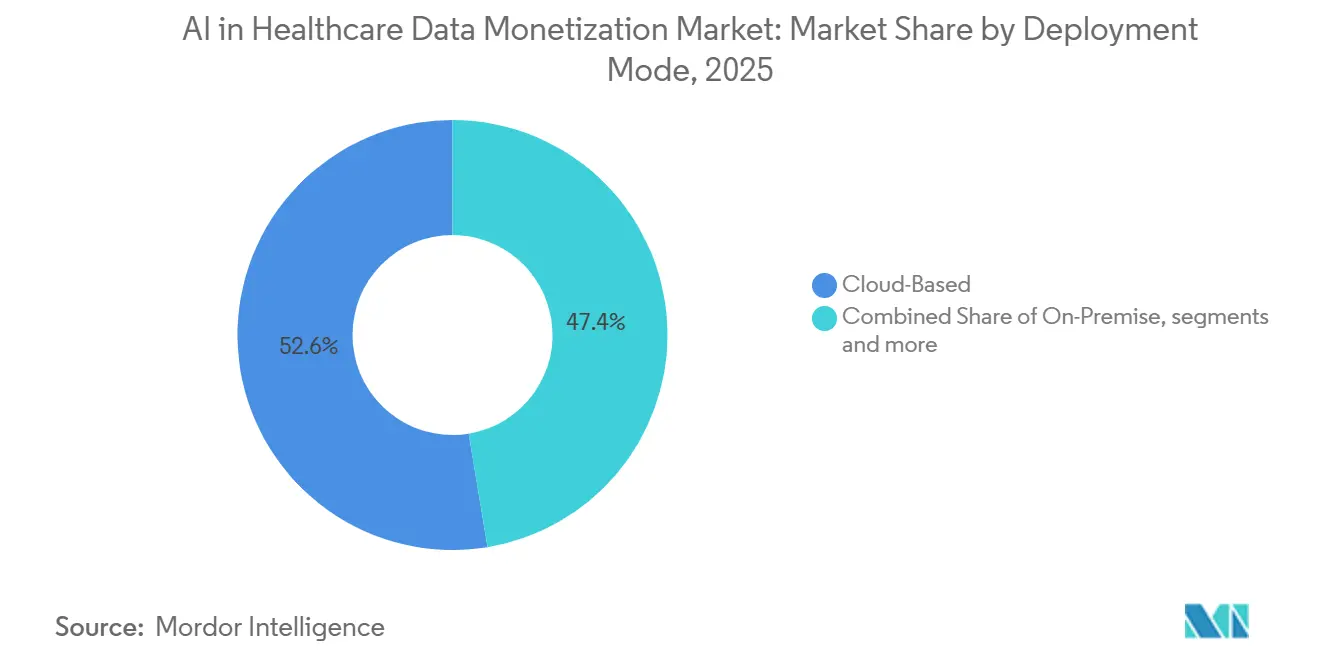

- By deployment mode, cloud-based deployment captured 52.64% of revenue in 2025, while hybrid deployment is expected to grow at a 15.74% CAGR through 2031.

- By end-user, healthcare providers held 42.87% of revenue in 2025, while healthcare payers are projected to advance at a 16.33% CAGR through 2031.

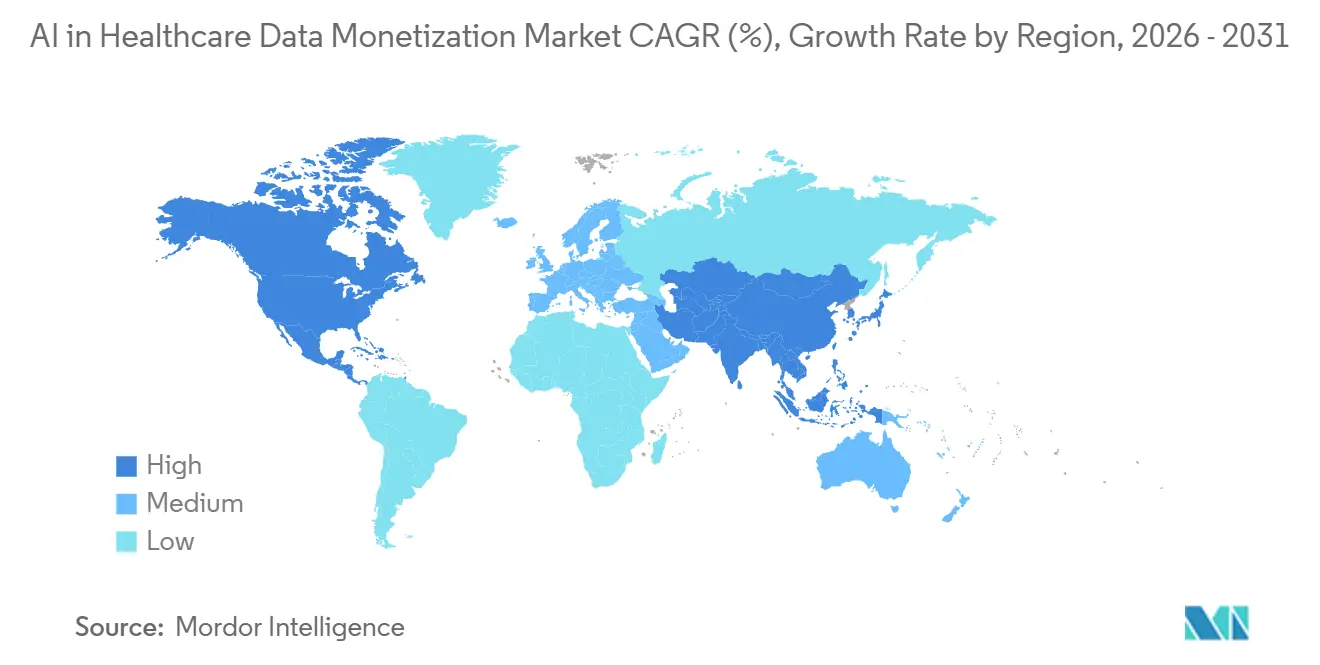

- By geography, North America captured 50.56% of global revenue in 2025, while Asia-Pacific is forecasted to grow at a 17.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Healthcare Data Monetization Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Driven Clinical and Operational Value Extraction | +3.5% | Global, most pronounced in North America and Western Europe | Medium term (2-4 years) |

| Real-World Evidence Demand from Payer and Pharma Workflows | +3.0% | Global, North America and EU core, spill-over to APAC | Medium term (2-4 years) |

| Privacy-Preserving Data Collaboration Networks | +2.5% | Global, EU regulatory-driven, North America technology-driven | Long term (≥ 4 years) |

| Expansion of Federated Learning and Secure Data Clean Rooms | +2.0% | Global, APAC emerging, EU compliance-driven | Long term (≥ 4 years) |

| Monetization of Longitudinal and Cross-Platform Patient Journeys | +1.8% | North America, Western Europe, Japan | Medium term (2-4 years) |

| Reimbursement Pressure Driving Data-Backed Efficiency Gains | +1.5% | North America primarily, spill-over to Western Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI-Driven Clinical and Operational Value Extraction

In the AI in healthcare data monetization market, AI-driven value extraction is widening the set of assets that can be commercialized because it finally makes large volumes of unstructured notes usable at scale. Clinical notes still represent the majority of EHR content, yet older analytics pipelines could not reliably convert them into standardized outputs that buyers could use for licensing, evidence generation, or reimbursement analysis. Tempus AI reported in June 2026 that its multimodal foundation model work spans more than 45 million de-identified patient journeys and more than 500 petabytes of data, which shows how large these new curation pools have already become.[1]Tempus AI, “Tempus Announces Initial Results from Its Multimodal Foundation Model Efforts for Novel and Scalable Insight Generation in Oncology,” BioSpace/BusinessWire, biospace.com Once AI reduces the cost gap between narrative records and structured fields, pathology notes, imaging reports, care plans, and longitudinal summaries can all enter the commercial inventory that providers and platforms manage. IQVIA reinforced this direction in March 2026 when it launched IQVIA.ai with NVIDIA, deploying more than 150 intelligent agents across clinical, commercial, and real-world workflows, with 19 of the top 20 pharmaceutical companies already using IQVIA agents in their work.[2]IQVIA Holdings Inc., “IQVIA Unveils IQVIA.ai, a Unified Agentic AI Platform Powered by NVIDIA to Improve Efficiency and Decision Making Across Life Sciences,” BusinessWire, businesswire.comThe same extraction logic is also spreading into hospital operations, where AI can surface coding errors, prior authorization friction, and revenue leakage patterns that are then packaged as monetizable insight products or embedded analytics services.

Real-World Evidence Demand from Payer and Pharma Workflows

In the AI in healthcare data monetization market, demand for real-world evidence is changing the commercial role of data from a passive archive into an active component of payer, pharma, and launch planning workflows. Buyers increasingly want linked datasets that can support coverage discussions, formulary reviews, regulatory submissions, and post-launch tracking without rebuilding methods across separate vendors. That preference favors data suppliers that can connect administrative, clinical, and outcomes records inside one governed environment rather than selling isolated files with limited reuse. As this model spreads, revenue in the AI in healthcare data monetization market moves closer to study design, evidence orchestration, and decision support instead of stopping at raw dataset delivery. The practical effect is that data owners with strong linkage quality and reproducible workflows can command higher value, because buyers are paying for end-to-end evidence readiness as much as they are paying for access to records.

Privacy-Preserving Data Collaboration Networks

In the AI in healthcare data monetization market, privacy-preserving collaboration networks are becoming more important because many institutions want commercial participation without exposing raw records to full external transfer. Clean-room and controlled-access models let multiple parties analyze aggregated or linked data while the underlying files remain under the control of the original owner. That changes the economic model, since recurring income can come from analytical access, governed queries, and workflow participation rather than a one-time dataset handoff. It also reduces a key source of liability, because organizations do not have to circulate the most sensitive patient-level records each time a new study or analytics request appears. This approach fits provider, payer, and life sciences procurement patterns, which increasingly require strict audit trails, role-based permissions, and configurable access rules before any collaboration begins. Vendors that build durable privacy-safe access layers therefore gain a stronger position in the AI in healthcare data monetization market, especially in regions where sovereignty, institutional governance, and legal review remain decisive buying criteria.

Expansion of Federated Learning and Secure Data Clean Rooms

In the AI in healthcare data monetization market, federated learning is moving beyond research pilots because regulated buyers need ways to train models and generate insights without centralizing sensitive data. A July 2025 scoping review in npj Digital Medicine found that healthcare federated learning requires sustainable business models, cultural alignment between commercial and open-science incentives, and clear financial returns for the institutions that contribute data.[3]Governing et al., “A Scoping Review of the Governance of Federated Learning in Healthcare,” npj Digital Medicine, nature.com That conclusion matters because technical feasibility alone does not create a commercial network, and monetization stalls when contributing institutions cannot justify the legal, staffing, and governance burden of participation. As these architectures mature, the AI in healthcare data monetization market gains a path to monetize models, queries, and insight layers while leaving source data inside the institutions that created it.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Re-Identification Risk in De-Identified Health Datasets | -2.0% | Global, most acute in North America and EU | Medium term (2-4 years) |

| Fragmented Consent Management Across Data Contributors | -1.5% | Global, US state-level patchwork and GDPR complexity in EU | Long term (≥ 4 years) |

| Interoperability Gaps Between Legacy EHR and Analytics Stacks | -1.0% | North America, MEA, parts of APAC | Medium term (2-4 years) |

| High Governance Cost for Continuous Model Validation and Auditability | -0.8% | Global, highest in highly regulated markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Re-Identification Risk in De-Identified Health Datasets

The AI in healthcare data monetization market faces a direct structural restraint because de-identified records no longer provide the simple legal comfort that earlier commercialization models assumed. A 2025 study in Scientific Reports found that current sanitization methods still left 74% of original information inferable with advanced removal tools, and even differentially private synthetic data showed 48% re-identification rates before full privacy settings were applied. That kind of evidence forces data owners, review boards, and buyers to treat de-identification as a continuing risk-management exercise instead of a completed preprocessing step. Commercially, this raises the review cost of each dataset, narrows the margin on direct licensing products, and slows the release schedule for new assets that were expected to move quickly into buyer workflows. Until trust, auditability, and defensible risk scoring improve further, this issue will continue to limit how quickly the AI in healthcare data monetization market can expand direct-access and high-granularity product offerings.

Fragmented Consent Management Across Data Contributors

The AI in healthcare data monetization market also slows when patient permissions cannot be interpreted in a standardized way across the many institutions that contribute to a pooled dataset. The Sequoia Project reported in April 2025 that current all-or-nothing consent models still force patients to withhold entire records instead of allowing selective sharing based on use case or data type. Civitas for Health noted in 2025 that sensitive data categories, including behavioral health and substance use disorder records governed by 42 CFR Part 2, often carry different consent requirements across jurisdictions. When those rules do not align, national datasets fragment into smaller state or institution-level cohorts, which reduces statistical power, narrows longitudinal continuity, and raises the acquisition cost of each usable panel. As long as consent remains difficult to compute and enforce at scale, the AI in healthcare data monetization market will struggle to assemble broad multi-contributor datasets with the geographic consistency that buyers want.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Monetization Model: Direct Channels Anchor Revenue, Indirect Models Signal Future Architecture

Direct data monetization held 56.76% of the AI in healthcare data monetization market share in 2025, and is expected to grow at a 16.11% CAGR through 2031, making it the dominant commercial model across current revenue streams. The segment stays large because health systems and specialty vendors can sell curated datasets through subscription, licensing, or controlled-access structures that are already familiar to pharma and payer buyers. Those buyers still prefer direct arrangements in cases where data provenance, reproducibility, and chain-of-custody documentation need to stand up to regulatory or payer review. This makes direct channels especially resilient in evidence generation and formal research workflows, where source control matters more than broad platform flexibility or marginal software savings.

Indirect data monetization remains smaller in current revenue terms, but it reveals where the AI in healthcare data monetization market is gradually moving as buyers pay for outcomes, insight delivery, and governed access rather than simple data transfer. In this model, value is created when data powers embedded AI services, reimbursement support, evidence workflows, or performance-linked commercial arrangements that do not require a traditional dataset sale. As value-based care, outcomes research, and clean-room workflows expand, the AI in healthcare data monetization industry is likely to see indirect models gain importance faster than their current share suggests.

By Solution Type: Platforms Lead Today, DaaS Defines the Next Cycle

Data monetization platforms held 44.33% of revenue in 2025, giving them the largest solution footprint across the AI in healthcare data monetization market. Their lead came from first-mover control of exchange rails, buyer relationships, and workflow integration long before open API standards began to mature across the wider healthcare technology stack. The segment also benefits from the fact that buyers often want a single coordination layer for access control, contract management, data discovery, and analytical handoff. That combination of operational convenience and embedded trust has allowed platforms to remain the default front end for many commercial transactions in this market.

Data-as-a-service (DaaS) is projected to grow at 16.76% CAGR through 2031, which makes it the fastest-expanding solution type in the AI in healthcare data monetization market. Demand is shifting in this direction because digital health buyers want API-first access, modular procurement, and consumption-based pricing instead of committing to broad platform ownership from the start. analytics-as-a-Service (AaaS) and insight-as-a-Service (IaaS) sit between full platforms and raw data access, and both are gaining relevance as buyers increasingly pay for interpretation, workflow speed, and decision-ready outputs. This means the revenue center of the AI in healthcare data monetization industry is gradually shifting from ownership of software environments toward reliable access to governed data and analytical intelligence delivered in smaller units.

By Data Type: Claims Data Anchors the Market, Clinical Data Reshapes the Growth Curve

Claims and financial data held 45.59% of revenue in 2025 and remained the most liquid commercial asset in the AI in healthcare data monetization market because administrative records are easier to normalize, link, and clear for external use. Decades of structured coding under ICD-10 and CPT standards make these files easier to package into repeatable products than data sources that depend on heavy narrative curation or image interpretation. Claims data also supports a wide range of buyer use cases, including utilization review, market access analysis, outcomes tracking, payer analytics, and real-world evidence studies built on standardized longitudinal history.

Clinical data is forecasted to grow at 15.88% CAGR through 2031, which gives it the strongest acceleration profile in the AI in healthcare data monetization market, even though it starts from a smaller share base than claims. Pharmaceutical and R&D data, patient-generated data, and operational data remain smaller segments, but they add depth that improves cohort definition, trial planning, remote monitoring, and hospital performance analysis. ISO 27001 and HITRUST credentials continue to matter in buyer diligence, because commercial adoption in the AI in healthcare data monetization market still depends on visible assurance that sensitive clinical and operational data are handled under recognized control frameworks.

By Deployment Mode: Cloud Infrastructure Leads, Hybrid Accelerates on Sovereignty Pressures

Cloud-based deployment accounted for 52.64% of the AI in healthcare data monetization market size in 2025 and remained the largest delivery model across the current installed base. The segment expanded first because major analytics workloads were already moving into HIPAA-compliant cloud environments that offered scalable storage, interoperable APIs, and faster setup for multi-party collaboration. Cloud also simplified access for buyers who wanted rapid onboarding, remote research teams, and elastic compute for data linkage, training, and evidence generation tasks that spike at irregular intervals. For many vendors, cloud remains the most efficient way to scale commercial access if national law and customer governance rules allow centralized processing.

Hybrid deployment is projected to grow at 15.74% CAGR through 2031, making it the fastest-growing model in the AI in healthcare data monetization market as sovereignty and residency concerns reshape architecture choices. This segment appeals to health systems and public data bodies that want cloud-native analytics and buyer connectivity while keeping the most sensitive patient records within national, regional, or institutional boundaries. On-premise environments remain relevant in large academic centers and national authorities with deep legacy investments, but they are no longer the only way to satisfy strict audit and governance expectations. Vendors that can secure on-premise data vaults while exposing flexible cloud interfaces are therefore better positioned to win the next wave of enterprise deals in the AI in healthcare data monetization industry.

By End-User: Providers Originate the Data, Payers Monetize it Fastest

Healthcare providers commanded 42.87% of revenue in 2025 and held the largest end-user position in the AI in healthcare data monetization market because they originate a large share of the clinical and operational records that buyers value most. Large academic medical centers and integrated delivery networks moved early because they controlled deep longitudinal data, had the internal governance capacity to structure commercial agreements, and could negotiate directly with life sciences buyers. Specialist brokers and intermediaries have made participation easier by handling de-identification, legal review, and commercial matching at scale, which allows more providers to enter without building full sales infrastructure in-house. This keeps providers at the center of supply even as platforms and brokers take on a larger share of orchestration and compliance work.

Healthcare payers are forecast to grow at 16.32% CAGR through 2031, making them the fastest-growing end-user group in the AI in healthcare data monetization market as reimbursement pressure pushes claims assets into more active commercial use. Payers are therefore monetizing utilization, claims, and care management records not only to support internal operations but also to build revenue streams tied to analytics, benchmarking, and evidence generation. Pharmaceutical and biotechnology companies remain the dominant buyer group, while medical technology firms, research organizations, and CROs continue to expand procurement budgets for patient-level linkage data and site selection support.

Geography Analysis

North America captured 50.56% of the AI in healthcare data monetization market share in 2025 and remained the largest regional contributor to global revenue. The region's lead rests on deep health IT infrastructure, mature payer-provider exchange networks, and a commercial real-world data ecosystem that is already connected to large pharmaceutical buyer bases. The 21st Century Cures Act and newer FHIR-based access rules continue to lower the marginal cost of aggregation, which intensifies competition at the infrastructure layer even as it broadens the revenue pool for the AI in healthcare data monetization market.

Asia-Pacific is projected to expand at 17.21% CAGR through 2031, which gives the AI in healthcare data monetization market its fastest regional growth profile. The region is moving quickly because China, India, and Japan are pushing government-backed digital health programs that convert large-scale registries, identifiers, and electronic records into assets suitable for secondary use. India's Ayushman Bharat Digital Mission is building a large federated health ID base, while South Korea's national claims databases and Australia's My Health Record system add depth to the regional pool of linkable data. Japan is also emerging as an entry point for international platforms through partnership models, which helps foreign AI data firms reach local buyers without building every part of the infrastructure themselves.

Europe is undergoing a governance-led buildout in the AI in healthcare data monetization market after EHDS Regulation (EU) 2025/327 came into force in March 2025 with EUR 810 million, or USD 849 million, committed to harmonized secondary-use infrastructure. Germany shows the scale of that effort, with 82 institutions registered with the National Health Data Lab in February 2026 and a target of more than 300 active research projects by the end of 2026 using pseudonymized data from 75 million statutorily insured people. Middle East and Africa and South America remain earlier-stage contributors, with GCC investment in national information platforms and Brazil's LGPD laying the governance foundation for future revenue expansion rather than near-term global leadership.

Competitive Landscape

The AI in healthcare data monetization market remains moderately concentrated, with IQVIA, Optum, and Datavant operating as anchor platforms across major real-world data exchange and commercialization workflows. Their position comes less from raw data volume and more from the linkage, governance, and buyer access layers that sit on top of fragmented source systems and make those systems usable at scale. Datavant's tokenization infrastructure underpins exchange across more than 80,000 hospitals and clinics and supports movement of more than 60 million healthcare records across more than 350 real-world data partners, which creates switching costs that are hard for smaller firms to match.

The AI in healthcare data monetization market still has meaningful white space where patient-generated data, specialty registries, and cross-platform longitudinal journeys remain only partially covered by the leading platforms. Smaller operators can therefore compete effectively when they control a narrow but difficult-to-replicate asset, such as consented wearable data, oncology pathways, or deep specialty registries that broad claims networks cannot reproduce. HealthVerity, Flatiron Health, Komodo Health, and other specialists continue to capture defined verticals such as payer analytics, oncology real-world evidence, and claims linkage where product fit matters more than absolute breadth. This keeps pricing and competitive positioning highly dependent on the clinical depth, interoperability quality, and audit readiness of each vendor's core data asset rather than on simple scale alone.

The AI in healthcare data monetization market also rewards firms that can meet governance thresholds without slowing delivery, because buyers increasingly treat HIPAA, the 21st Century Cures Act, EU AI Act transparency, HITRUST, and GxP alignment as entry requirements rather than optional features. These compliance layers filter out weaker entrants, since life sciences and payer customers do not want to build commercial programs on vendors that cannot defend data lineage, privacy controls, or model governance under formal scrutiny. At the same time, the presence of a sizable second tier means the market is not concentrated enough for the leaders to fully lock up every use case, geography, or specialty dataset. Competitive advantage therefore comes from combining privacy-safe access, reliable linkage, strong buyer relationships, and fast analytical workflows inside one commercial stack, which is why concentration remains moderate rather than extreme.

AI In Healthcare Data Monetization Industry Leaders

Oracle

Microsoft Corporation

IQVIA Holdings Inc.

Optum, Inc.

Datavant, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: HealthVerity completed the acquisition of Symphony Health Solutions from ICON plc, uniting clinical data depth with commercial analytics scale to create a patient-centric real-world and commercial data ecosystem built on 40 years of combined experience and a marketplace of over 70 curated data sources, including EMR, lab, and specialty datasets.

- May 2026: Datavant and Lighten Platforms announced a collaboration to deliver regulatory-grade AI-powered curation of unstructured EHR data directly into Datavant's RWE analytics platform, reducing study timeline from months to days and enabling longitudinal patient dataset construction at regulatory-submission standard.

- April 2026: Thermo Fisher Scientific's PPD clinical research business entered a strategic data collaboration with HealthVerity, gaining streamlined access to a marketplace of over 70 curated data sources, including EMR, lab results, and specialty datasets, to enhance trial feasibility, site selection, and real-world evidence generation for biopharma sponsors.

- April 2026: Tempus AI announced an expanded multi-year strategic collaboration with Gilead Sciences for oncology R&D, providing Gilead enterprise-wide access to Tempus' AI-driven Lens platform across multiple indications and integrating dedicated analytical services for biomarker strategy, health outcomes analysis, and clinical RWE.

Global AI In Healthcare Data Monetization Market Report Scope

According to the report’s scope, the AI in healthcare data monetization market refers to the ecosystem of technologies, platforms, and services that use artificial intelligence to transform healthcare data into economic value through data commercialization, analytics, insights generation, and data-driven decision support. These solutions enable healthcare providers, payers, life sciences companies, and research organizations to securely analyze, package, share, and monetize clinical, operational, claims, and real-world data while maintaining regulatory compliance and patient privacy.

The AI in healthcare data monetization market is segmented into monetization model, solution type, data type, deployment mode, end-user, and geography. By monetization model, the market is segmented into direct data monetization and indirect data monetization. By solution type, the market is segmented into data-as-a-service (DaaS), analytics-as-a-service (AaaS), insight-as-a-service (IaaS), and data monetization platforms. By data type, the market is segmented into clinical data, claims and financial data, pharmaceutical and R&D data, patient-generated data, and operational and administrative data. By deployment mode, the market is segmented into cloud-based, on-premise, and hybrid. By end-user, the market is segmented into pharmaceutical and biotechnology companies, healthcare providers, healthcare payers, medical technology companies, and research organizations and CROs. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Direct Data Monetization |

| Indirect Data Monetization |

| Data-as-a-Service (DaaS) |

| Analytics-as-a-Service (AaaS) |

| Insight-as-a-Service (IaaS) |

| Data Monetization Platforms |

| Clinical Data |

| Claims and Financial Data |

| Pharmaceutical and R&D Data |

| Patient-Generated Data |

| Operational and Administrative Data |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Pharmaceutical and Biotechnology Companies |

| Healthcare Providers |

| Healthcare Payers |

| Medical Technology Companies |

| Research Organizations and CROs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Monetization Model | Direct Data Monetization | |

| Indirect Data Monetization | ||

| By Solution Type | Data-as-a-Service (DaaS) | |

| Analytics-as-a-Service (AaaS) | ||

| Insight-as-a-Service (IaaS) | ||

| Data Monetization Platforms | ||

| By Data Type | Clinical Data | |

| Claims and Financial Data | ||

| Pharmaceutical and R&D Data | ||

| Patient-Generated Data | ||

| Operational and Administrative Data | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By End-User | Pharmaceutical and Biotechnology Companies | |

| Healthcare Providers | ||

| Healthcare Payers | ||

| Medical Technology Companies | ||

| Research Organizations and CROs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 size of AI in healthcare data monetization?

It stands at USD 261.07 million in 2026 and is projected to reach USD 519.61 million by 2031 at a 14.76% CAGR.

Which monetization model leads current revenue generation?

Direct data monetization led with 56.76% of revenue in 2025 because buyers still value provenance, auditability, and controlled access.

Why do claims and financial datasets remain the largest data type?

Claims and financial data held 45.59% of revenue in 2025 because standardized coding and easier legal clearance make these datasets faster to commercialize.

Which region is expanding the fastest through 2031?

Asia-Pacific is the fastest-growing region with a 17.21% CAGR, supported by government-led digital health programs across China, India, and Japan.

Page last updated on: