Healthcare Quality Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.02 Billion |

| Market Size (2031) | USD 3.97 Billion |

| Growth Rate (2026 - 2031) | 14.43% CAGR |

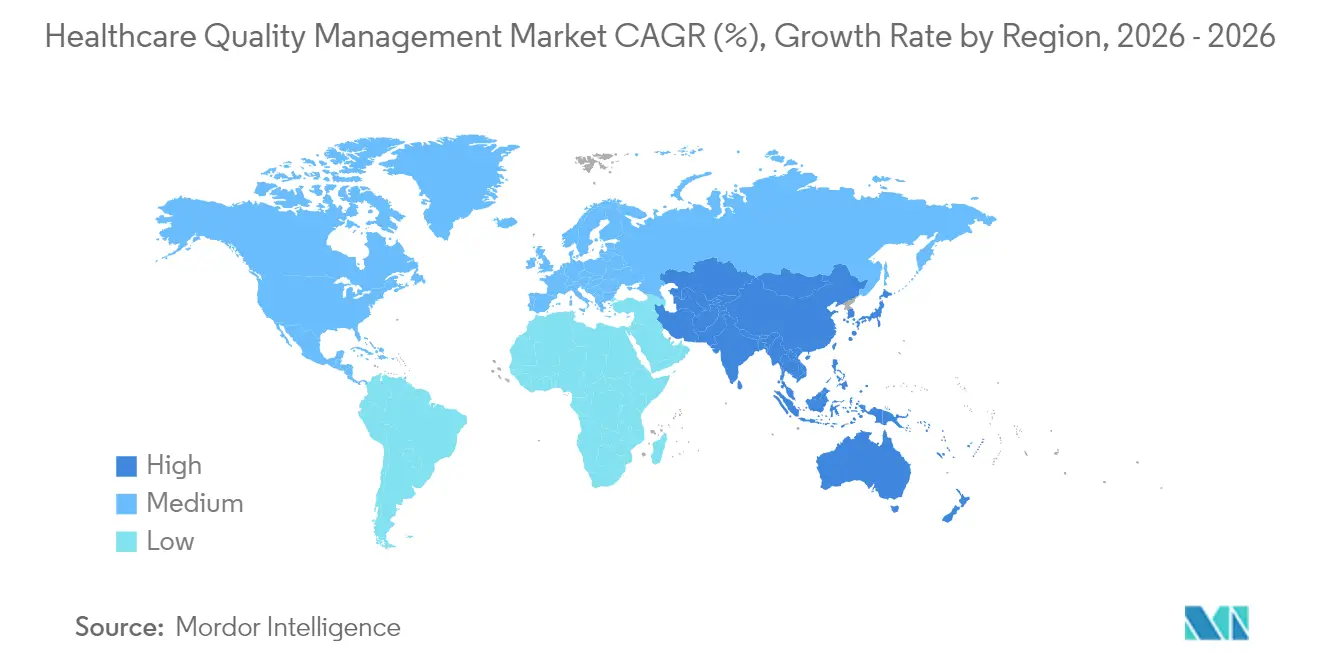

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

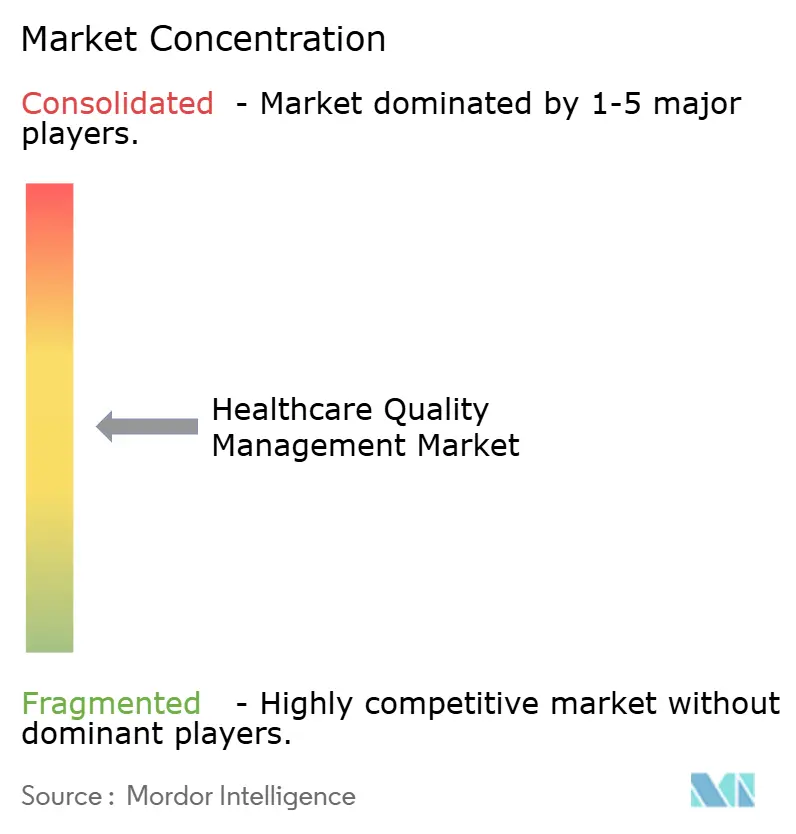

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Quality Management Market Analysis by Mordor Intelligence

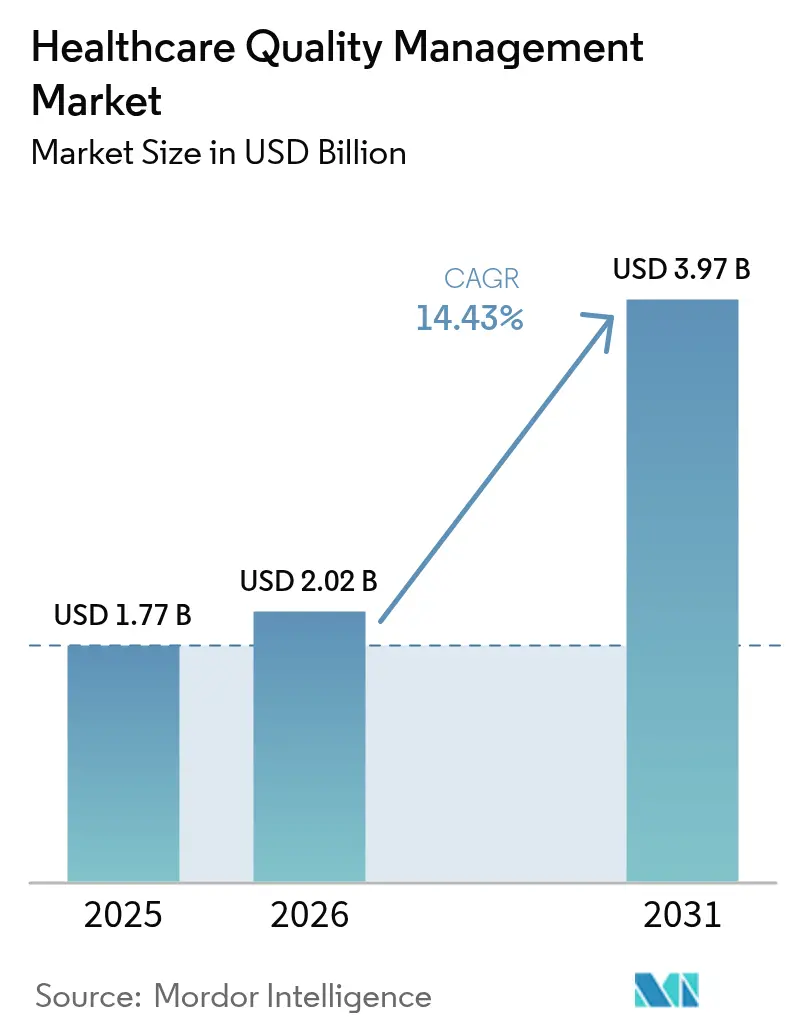

The Healthcare quality management market size was valued at USD 1.77 billion in 2025 and estimated to grow from USD 2.02 billion in 2026 to reach USD 3.97 billion by 2031, at a CAGR of 14.43% during the forecast period (2026-2031). This rapid expansion reflects a shift from retrospective compliance reporting toward predictive intelligence platforms that improve clinical outcomes and margins. Escalating electronic clinical quality-measure mandates, expanding value-based payment models, and rising volumes of structured and unstructured health data are pushing providers and payers to adopt integrated analytics suites. Cloud deployment now dominates as organizations trade capital outlays for subscription models that offer swift scalability and tighter cyber-resilience. AI-enabled population-health modules are gaining traction because they help identify high-risk cohorts, automate care-gap closure, and lower readmissions. Competitive intensity is increasing as electronic-health-record incumbents acquire or partner with AI-native firms to defend installed bases and meet growing interoperability requirements.

Key Report Takeaways

- By software type, Business Intelligence & Advanced Analytics led with 34.12% of Healthcare quality management market share in 2025, while Population-Health Quality Management is projected to expand at 16.28% CAGR to 2031.

- By mode of delivery, cloud-based solutions held 58.05% share of the Healthcare quality management market size in 2025 and Web-Hosted SaaS is advancing at 15.63% CAGR through 2031.

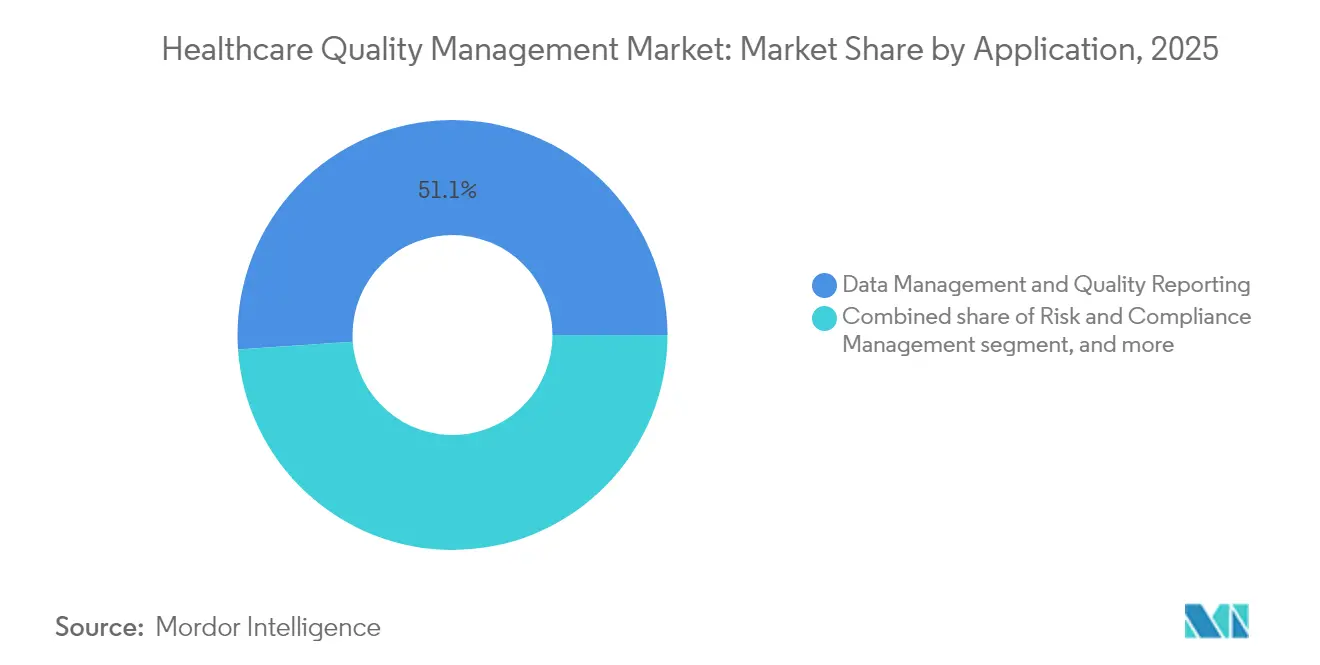

- By application, Data Management & Quality Reporting accounted for 51.08% share of the Healthcare quality management market size in 2025; Outcome & Cost Analytics is growing fastest at 16.07% CAGR to 2031.

- By end user, hospitals & integrated delivery networks controlled 60.89% of the Healthcare quality management market share in 2025, whereas payers & ACOs are set for a 17.33% CAGR during 2026-2031.

- By geography, North America remained dominant with 40.02% share in 2025, yet Asia-Pacific is forecast to rise at 15.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Healthcare Quality Management Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Mandates And Incentives For Quality Reporting | +3.2% | North America & EU lead; global applicability | Short term (≤ 2 years) |

| Surge In Healthcare Data Volume And Complexity | +2.8% | Global | Medium term (2 – 4 years) |

| Aging Population And Chronic Disease Burden | +2.1% | Asia-Pacific core; spill-over to North America & EU | Long term (≥ 4 years) |

| Digital Transformation Of Provider Workflows | +2.5% | Global | Medium term (2 – 4 years) |

| Advancement Of Artificial Intelligence Analytics | +3.1% | North America & EU; expanding to Asia-Pacific | Short term (≤ 2 years) |

| Rise Of Consumer Transparency And ESG Accountability | +1.8% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Mandates and Incentives for Quality Reporting

Regulators now embed financial carrots and sticks in reimbursement, compelling hospitals and accountable-care organizations to elevate reporting sophistication. The Centers for Medicare & Medicaid Services will expand accountable-care quality measures from 4 in 2025 to 11 in 2028, turning manual spreadsheets into high-risk liabilities[1]Centers for Medicare & Medicaid Services, “Promoting Interoperability Programs,” cms.gov. Annual submission of six electronic clinical quality measures determines payment adjustments, pushing laggards toward modern platforms. Hospitals that ignore these rules risk both revenue loss and exclusion from value-based programs. The 21st Century Cures Act adds penalties for information blocking, making interoperable data flows a non-negotiable requirement. As a result, investment in end-to-end quality suites has shifted from discretionary to mission-critical budgeting.

Aging Population and Chronic Disease Burden

Noncommunicable diseases account for 74% of global deaths, creating multicomorbidity challenges that strain fee-for-service economics[2]Asian Development Bank, “Noncommunicable Diseases in Asia and the Pacific,” adb.org. Asia-Pacific bears the heaviest demographic load, spurring investments in population-health quality platforms that orchestrate longitudinal care plans across providers. Value-based contracts place downside financial risk on outcomes, making proactive disease-management dashboards indispensable. Organizations deploying such systems see hospital-readmission reductions and per-patient cost savings, demonstrating that demographic pressure is fuelling sustained platform demand well into the next decade.

Advancement of Artificial-Intelligence Analytics

Predictive algorithms have moved from pilot projects to enterprise rollouts, with hospitals pairing historical data and real-time feeds to flag sepsis risk or equipment downtime. Wolters Kluwer’s AI-enabled decision-support modules exemplify embedded intelligence within clinician routines. Explainability is now mandatory under the federal HTI-1 rule, guiding vendors to surface algorithm logic in plain language. Providers deploying transparent AI report sharply lower readmissions and improved audit scores, substantiating the technology’s pivotal role in future growth.

Rise of Consumer Transparency and ESG Accountability

Patients demand clear outcome metrics while institutional investors screen environmental, social, and governance performance. Public scorecards and equity-focused initiatives pressure health systems to disclose quality indicators. Platforms that unify clinical, financial, and experience data therefore gain strategic relevance. Over time, ESG-driven procurement policies may reward vendors that capture and report metrics on health-equity interventions and carbon footprints.

Restraints Impact Analysis of Healthcare Quality Management Market*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation and integration costs | −2.1% | Global; strongest in emerging markets | Short term (≤ 2 years) |

| Data security and privacy concerns | −1.8% | Global; regulatory focus in North America & EU | Medium term (2 – 4 years) |

| Lack of interoperability standards | −1.5% | Global | Medium term (2 – 4 years) |

| Algorithmic bias and regulatory liability | −1.2% | North America & EU; rising attention in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Implementation and Integration Costs

Smaller providers struggle to fund platform rollouts when HIPAA security amendments alone require USD 9.3 billion nationwide in first-year compliance costs[3]U.S. Department of Health & Human Services, “HIPAA Security Rule Proposed Modifications,” hhs.gov. Linking new quality modules with legacy EHRs often extends timelines by up to two years and multiplies consulting fees. Total cost of ownership includes ongoing upgrades and user training that frequently double or triple initial license expenditure. As a result, some mid-tier systems revert to manual workarounds that eventually prove unsustainable, slowing market penetration in cost-sensitive regions.

Data Security and Privacy Concerns

Healthcare leads all industries in breach frequency and average incident cost, with cyberattacks up 239% from 2018 to 2023. Proposed rules require multi-factor authentication, encryption at rest, and routine vulnerability scans, raising the bar for vendors. Payers and providers must balance expansive data-sharing mandates with strict privacy controls, especially as AI engines demand access to complete longitudinal records. Two-thirds of organizations admit they are unprepared for tighter standards, delaying purchase decisions until security roadmaps mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Healthcare Quality Management Market Segment Analysis

By Software Type:

Analytics Platforms Drive Intelligence EvolutionBusiness Intelligence & Advanced Analytics retained the largest footprint, reflecting fundamental demand for dashboards that fulfill reporting obligations. Population-Health Quality Management however is accelerating at 16.28% CAGR because payers and integrated networks need proactive risk-stratification tools. Vendors embed AI prediction into these modules, shifting the Healthcare quality management market from retrospective charts toward real-time intervention engines. Quality Reporting & Benchmarking suites remain vital for CMS compliance, while Clinical Risk & Patient-Safety platforms gain attention amid stricter accreditation rules.

The convergence trend favours unified stacks that merge visualization, predictive analytics, and safety surveillance. Wolters Kluwer’s UpToDate-powered AI Labs illustrates how decision support and quality analytics now coexist in one workflow. Hospitals adopting full-spectrum platforms report USD 13.3 million annual savings and rapid ROI, propelling further uptake. As AI transparency rules tighten, vendors with explainable models enjoy a competitive edge in the Healthcare quality management market.

By Mode of Delivery:

Cloud Migration Accelerates Platform AdoptionCloud-based deployment captured 58.05% of 2025 revenue, underscoring provider appetite for elastic infrastructure. Web-Hosted SaaS leads growth at 15.63% CAGR, highlighting movement toward subscription economics that sidestep capital budgets. Average annual health-system cloud spend has surpassed USD 38 million, signalling confidence in vendor-managed security and redundancy. On-premise implementations persist mainly where data-sovereignty law or legacy interfaces dictate local hosting.

Oracle Health’s pursuit of Qualified HIN status within TEFCA underscores the priority on secure information exchange across cloud backbones oracle.com. SaaS delivery also democratizes advanced analytics for rural and community hospitals that lack extensive IT staff. Consequently, cloud-native suppliers are poised to outpace legacy competitors in the Healthcare quality management market.

By Application:

Data Management Foundations Enable Advanced AnalyticsData Management & Quality Reporting formed the backbone in 2025 with 51.08% share, reflecting unavoidable regulatory workloads. Outcome & Cost Analytics is scaling fastest at 16.07% CAGR as executives seek visibility into margin performance. Risk & Compliance modules remain essential to navigate shifting rules, while Patient-Safety surveillance gains urgency amid zero-harm initiatives.

Health-system leaders increasingly favour integrated suites that fuse these applications. Vizient’s collaboration with Qualtrics combines patient-experience metrics with clinical outcomes, illustrating cross-domain convergence. Unified solutions reduce duplicate interfaces, lower training needs, and improve data trustworthiness, amplifying growth across the Healthcare quality management market.

By End User:

Payers Drive Value-Based Care TransformationHospitals and integrated delivery networks held 60.89% share in 2025 because CMS mandates directly affect inpatient reimbursement. Payers and accountable-care organizations however are advancing at 17.33% CAGR, propelled by shared-savings contracts that make quality performance financially material. Ambulatory and specialty clinics also invest as care gravitates toward outpatient settings.

ACO quality-measure counts will nearly triple by 2028, forcing payers to secure platforms that ingest multi-provider data streams. Innovaccer’s acquisition of Pharmacy Quality Solutions broadens access to 95% of community pharmacies, demonstrating payer focus on whole-ecosystem oversight. This dynamic cements payers as pivotal growth engines within the Healthcare quality management market.

Geography Analysis

North America Healthcare Quality Management Market

North America retained leadership at 40.02% revenue share in 2025, supported by rigorous CMS programs and large-scale IT budgets. Proposed HIPAA security amendments alone will drive billions in compliance spend, pressing even mid-size hospitals to modernize infrastructures. Canada and Mexico add momentum through federal digitization strategies, but the United States remains the anchor of regional demand.

APAC Healthcare Quality Management Market

Asia-Pacific is the fastest-growing territory at 15.52% CAGR to 2031, catalyzed by national digital-health blueprints across Australia, India, and Malaysia. Integrated primary-care technology investments combat high noncommunicable-disease prevalence, creating fertile territory for population-health modules. Cloud uptake lets emerging markets leapfrog on-premise constraints, further stimulating the Healthcare quality management market.

Europe Healthcare Quality Management Market

Europe shows steady expansion as interoperability and health-technology-assessment frameworks spread across the bloc. Germany’s Hospital Future Act, France’s MaSanté2022 plan, and the United Kingdom’s NHS digitization agenda all demand transparent outcome metrics. GDPR compliance shapes vendor roadmaps, favouring platforms with advanced consent and pseudonymization controls. Collectively, these dynamics sustain regional growth while raising the regulatory bar for global entrants.

Competitive Landscape

Competition is moderate and intensifying. Legacy EHR suppliers such as Oracle Health and IBM Merative leverage installed bases to embed quality tools, while analytics specialists like Health Catalyst target best-of-breed replacement cycles. Strategy has tilted toward ecosystem building: Oracle Health joined forces with Cleveland Clinic and G42 to co-develop AI-enabled delivery models, signalling that partnerships can accelerate capability gaps.

M&A activity accelerates consolidation. RLDatix bought SocialClimb to marry patient-experience insights with safety workflows, whereas McKesson invested USD 3.34 billion across oncology platforms to create vertical quality stacks. Vendors differentiate through AI explainability, cloud architecture, and adherence to interoperability frameworks such as TEFCA. Those unable to modernize face attrition as procurement teams gravitate toward integrated, standards-ready platforms.

White-space persists in ambulatory-care quality management and high-growth emerging markets. Agile SaaS vendors offering modular pricing can penetrate these niches faster than bulky incumbents. Meanwhile, alliances like the Joint Commission-NAHQ partnership elevate accreditation thresholds, tightening entry requirements but rewarding firms that can document compliance. Overall, technology depth and ecosystem breadth now outweigh brand tenure in determining share gains within the Healthcare quality management market.

Healthcare Quality Management Industry Leaders

Oracle

Optum, Inc.

Merative

Premier Inc.

RLDatix

- *Disclaimer: Major Players sorted in no particular order

Healthcare Quality Management Market Companies Covered in this Report

- Oracle

- Optum

- Merative

- Premier

- Mckesson

- RLDatix

- Health Catalyst

- CitiusTech

- Nuance (Microsoft)

- Dolbey Systems

- Medisolv

- Clarity Group

- Riskonnect Inc.

- Press Ganey

- Quantros Inc.

- Wolters Kluwer Health

- Flatiron Health

- MedeAnalytics

- Koninklijke Philips

Recent Industry Developments in Healthcare Quality Management Market

- February 2025: McKesson Corporation acquired an 80% stake in PRISM Vision Holdings for USD 850 million, adding retina analytics to its specialty-care quality platform.

- January 2025: The Joint Commission and the National Association for Healthcare Quality formed a strategic alliance to enhance global patient-safety standards.

- November 2024: Veradigm introduced Ambient Scribe, an AI tool that automates documentation and captures quality metrics during encounters.

- October 2024: Oracle Health applied for TEFCA Qualified Health Information Network status to bolster interoperable data exchange.

- August 2024: McKesson agreed to buy a controlling interest in Core Ventures for USD 2.49 billion to deepen oncology quality capabilities.

Healthcare Quality Management Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the global healthcare quality management market as all software platforms and associated analytics service modules that let providers, payers, and accountable-care groups collect, analyze, report, and act on clinical, operational, and financial quality indicators so patient outcomes improve, adverse events fall, and regulatory performance mandates are met.

Scope Exclusions: Consultancy projects delivered without a licensed digital platform and generic enterprise quality tools used outside healthcare are not counted.

Segments Covered in This Report

- By Software Type

- Business Intelligence & Advanced Analytics

- Quality Reporting & Benchmarking Suites

- Clinical Risk & Patient-Safety Management

- Provider Performance & Productivity Improvement

- Population-Health Quality Management

- By Mode Of Delivery

- Cloud-Based

- Web-Hosted (SaaS)

- On-Premise

- By Application

- Data Management & Quality Reporting

- Risk & Compliance Management

- Outcome & Cost Analytics

- Patient-Safety & Adverse-Event Surveillance

- By End User

- Hospitals & Integrated Delivery Networks

- Ambulatory Care & Specialty Clinics

- Payers & Accountable-Care Organizations

- Other Providers (Rehab, Long-Term Care)

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed hospital CIOs, payer quality directors, and health-IT integrators across North America, Europe, and Asia-Pacific. They then surveyed software resellers in the Middle East and Africa and Latin America. These conversations confirmed adoption triggers, average selling prices, and implementation timelines that secondary data alone could not surface.

Desk Research

We began with publicly available datasets from the Centers for Medicare and Medicaid Services, the Agency for Healthcare Research and Quality, Eurostat, the World Health Organization, and multiple national health ministries, which publish volumes of mandatory quality reports, incentive pools, and penalty payments. Trade-body releases from HIMSS and CHIME, plus peer-reviewed articles on electronic health-record maturity, supplied adoption fingerprints. Company 10-Ks, investor decks, and press releases revealed pricing ranges and module uptake rates. Paid resources such as D&B Hoovers and Dow Jones Factiva helped our team profile vendor revenues and recent contract wins across regions. The sources listed are illustrative; many additional open and subscription assets informed data collection, validation, and clarification.

Market-Sizing and Forecasting

A top-down model converts national value-based purchasing penalties, meaningful-use incentives, and care-episode volumes into an addressable spending pool, which is then pressure-tested through selective bottom-up supplier roll-ups and channel checks. Five market fingerprints, cloud penetration, hospital EHR maturity, regulatory expansion of patient-safety indicators, growth in accountable-care contracts, and average module price erosion, feed a multivariate regression that projects demand through 2030. Where bottom-up inputs are thin, calibrated adoption curves agreed upon during expert calls bridge gaps.

Data Validation and Update Cycle

Outputs are triangulated against independent IT-budget surveys, vendor earnings surprises, and regional procurement notices. Anomalies trigger analyst escalation before sign-off. Reports refresh annually, with interim updates whenever policy shifts or mergers materially alter the baseline.

How Mordor Intelligence's Healthcare Quality Management Market Size Compares to Other Published Estimates

Published estimates often diverge because firms slice the market differently, refresh at uneven intervals, or impute prices from very limited interviews. Our disciplined scope, yearly rebuild, and dual-lens modeling limit such drift.

Key gap drivers include whether services revenue is bundled, the inflation factors used for multi-year contracts, and how aggressively cloud conversions are projected.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.31 B | Mordor Intelligence | |

| USD 4.40 B | Global Consultancy A | Narrower component focus and older adoption multipliers |

| USD 6.64 B | Industry Association B | Bundled professional services and optimistic cloud uptake assumptions |

These comparisons show that Mordor delivers a transparent, repeatable baseline grounded in clearly defined boundaries and routinely updated variables, giving clients a dependable starting point for strategic planning.

Key Questions Answered in the Report

What is the current value of the healthcare quality management market?

The market is valued at USD 6.06 billion in 2026 and is projected to hit USD 11.79 billion by 2031.

Which software segment is growing fastest?

Population-Health Quality Management solutions are expanding at a 16.28% CAGR through 2031 as organizations shift toward value-based care.

Why are cloud-based deployments dominating?

Cloud platforms offer scalable infrastructure, automatic updates, and lower upfront costs, giving them 58.05% share in 2025 with SaaS models rising quickest.

What region shows the highest growth potential?

Asia-Pacific leads in growth with a 15.52% CAGR to 2031, driven by large-scale digital-health initiatives and a high chronic-disease burden.

How are new HIPAA security proposals affecting adoption?

Proposed amendments could cost USD 9.3 billion in first-year compliance, pressuring smaller providers but also increasing demand for secure, integrated quality platforms.

What role does artificial intelligence play in quality management today?

AI now powers predictive analytics that lower readmissions and equipment downtime; explainable models are essential for regulatory acceptance and clinician trust.

Page last updated on: