AI-Based Healthcare Supply Chain Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

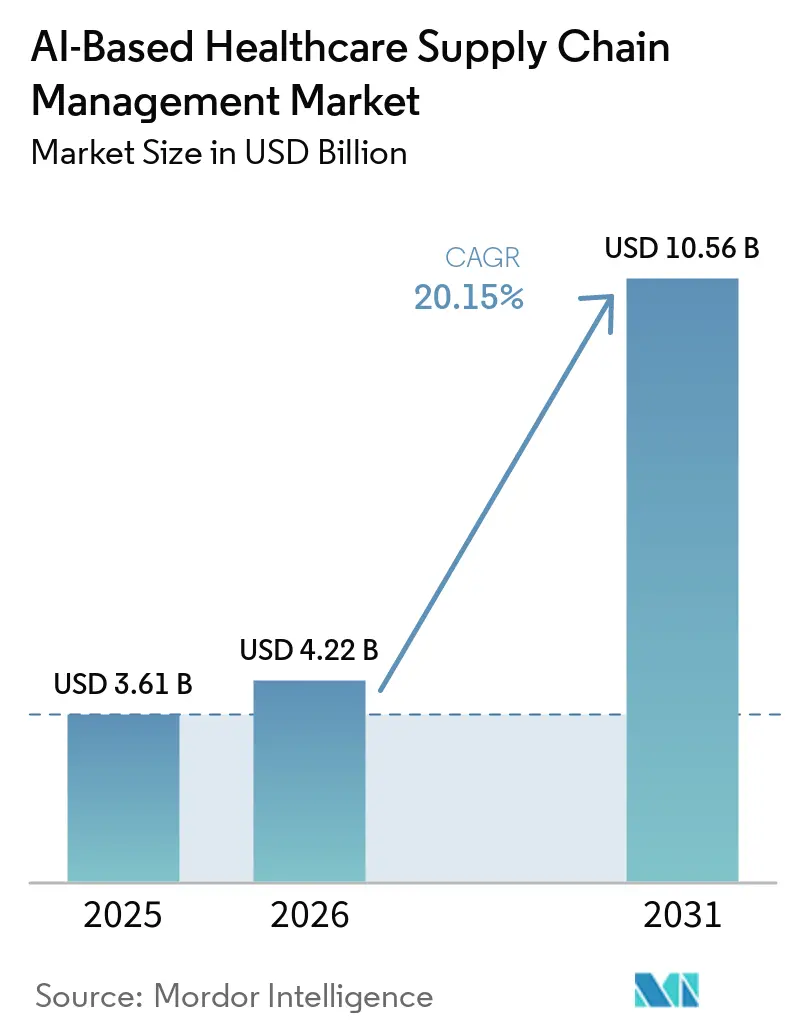

| Market Size (2026) | USD 4.22 Billion |

| Market Size (2031) | USD 10.56 Billion |

| Growth Rate (2026 - 2031) | 20.15% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-Based Healthcare Supply Chain Management Market Analysis by Mordor Intelligence

The AI-based healthcare supply chain management market is expected to grow from USD 3.61 billion in 2025 to USD 4.22 billion in 2026 and is forecasted to reach USD 10.56 billion by 2031 at 20.15% CAGR over 2026-2031. The AI-based healthcare supply chain management market is moving beyond pilot programs because cost pressure, stricter traceability rules, and the operational burden of biologics distribution are forcing health systems and manufacturers to redesign how they plan, source, and fulfill critical supplies. The AI-based healthcare supply chain management market is also benefiting from a broader shift toward connected data environments, where ERP, EHR, warehouse, and supplier systems are being linked so that procurement, inventory, and logistics decisions can be made with less manual intervention and with faster response cycles. A growing part of the opportunity in the AI-based healthcare supply chain management market now sits in enterprise platforms that can unify contracting, demand sensing, exception handling, and distribution visibility across fragmented provider and manufacturer networks. Competitive activity in the AI-based healthcare supply chain management market shows that large platform vendors are investing in proprietary AI capabilities and agent-based architectures, while focused challengers are trying to win on healthcare workflow depth, implementation speed, and deployment flexibility. The AI-based healthcare supply chain management market also faces a more cautious buying environment because cybersecurity exposure, integration cost, and shortages of hybrid supply chain and AI talent can delay large deployments even when the savings case is clear.

Key Report Takeaways

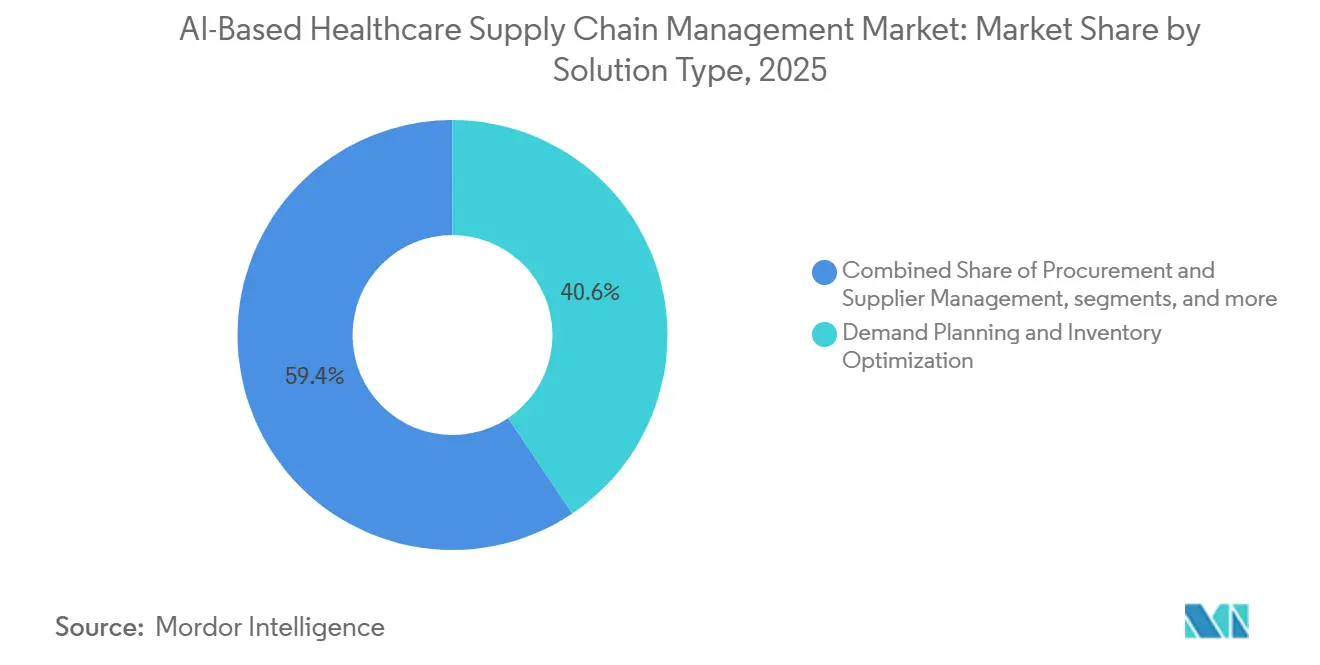

- By solution type, demand planning and inventory optimization led with 40.61% revenue share in 2025, while procurement and supplier management is projected to expand at a 24.59% CAGR through 2031.

- By deployment mode, cloud-based deployment held 54.33% of revenue in 2025, and the same segment is projected to record the highest CAGR at 22.84% through 2031.

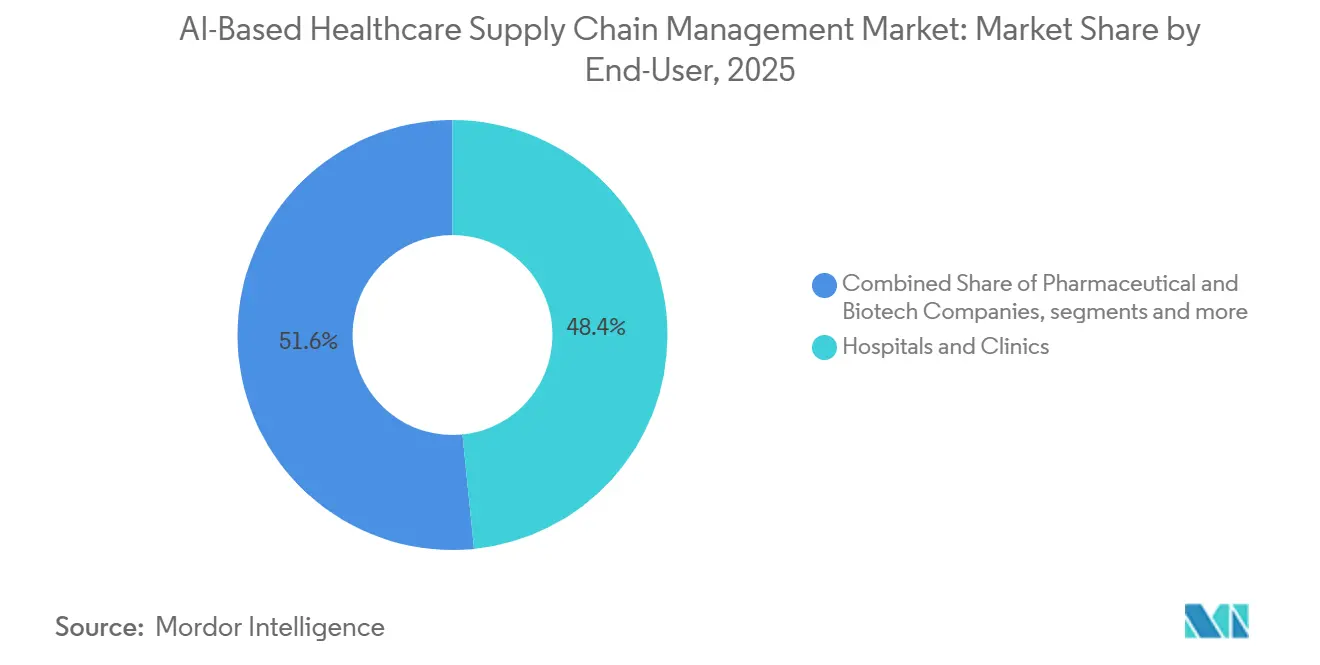

- By end-user, hospitals and clinics accounted for 48.40% of revenue in 2025, while pharmaceutical and biotech companies are expected to advance at a 22.41% CAGR through 2031.

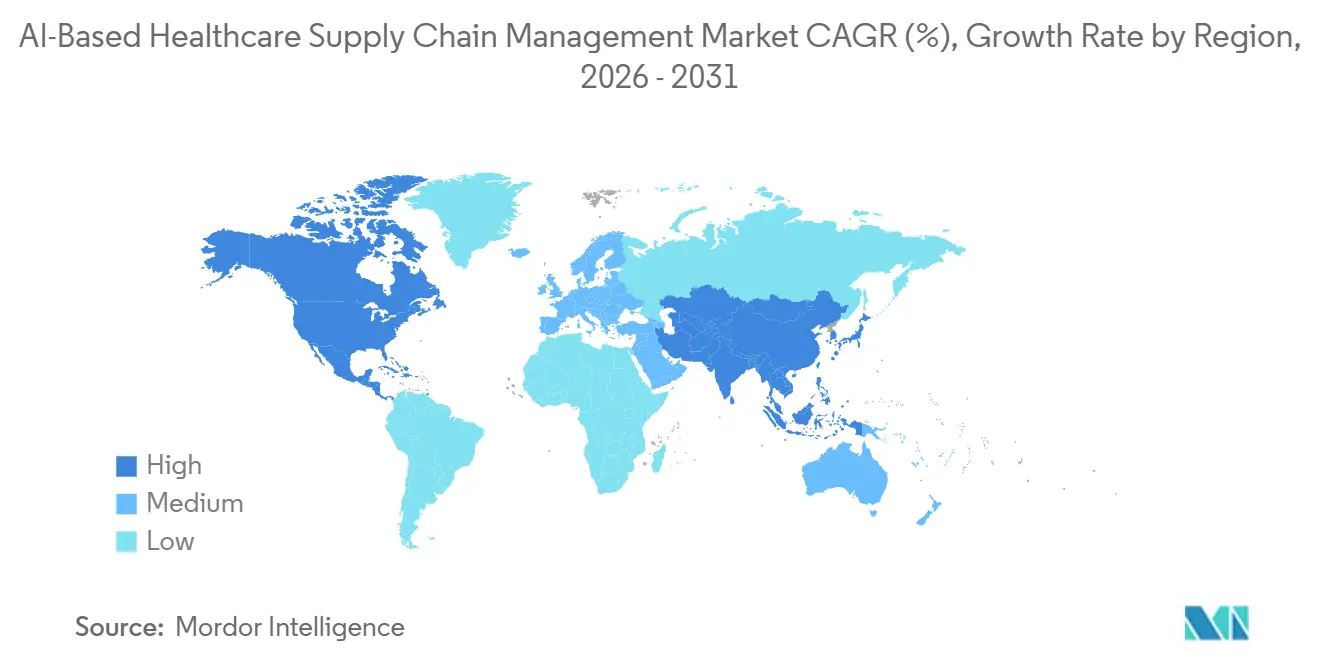

- By geography, North America represented 40.11% of revenue in 2025, while Asia-Pacific is forecasted to grow at a 23.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-Based Healthcare Supply Chain Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Pressure to Cut Healthcare Operating Costs | +4.2% | Global, with highest intensity in North America and Western Europe | Short term (≤ 2 years) |

| AI and Big-Data Adoption in Healthcare Logistics | +5.1% | Global, highest in North America and Asia-Pacific | Medium term (2-4 years) |

| Growing Complexity of Cold-Chain Biologics Flows | +3.4% | Global, with APAC and North America as primary zones | Medium term (2-4 years) |

| Global Serialization / Track-and-Trace Mandates | +2.8% | Global, 26 markets enforceable, 8 more deadline-bound | Short term (≤ 2 years) to Medium term (2-4 years) |

| Autonomous Mobile Robots Optimizing Hospital Stock | +2.3% | North America, Western Europe, East Asia, including Japan and Singapore | Medium term (2-4 years) |

| Hospital-at-Home Models Needing Dynamic Fulfillment | +1.7% | North America, expanding to Europe and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Pressure to Cut Healthcare Operating Costs

The AI-based healthcare supply chain management market is gaining momentum because provider margins remain under pressure and supply chain leaders are being asked to show measurable savings within shorter budgeting cycles. Health systems are therefore focusing first on use cases where savings are easiest to verify, especially demand planning, contract compliance, and automated procurement checks that can reduce leakage and avoid excess stock. A 2025 partnership between Tufts Medicine and Premier generated USD 15 million in annual supply chain savings through AI-assisted inventory management and contracting analytics, which supports the case for broader operational rollouts.[1]Premier Inc., “Tufts Medicine Transforms Supply Chain Operations for USD 15 Million in Annual Savings,” Premier Inc. Newsroom, premierinc.comThe AI-based healthcare supply chain management market is also benefiting from a structural change in procurement behavior, where health systems are moving away from static catalog dependence toward real-time monitoring of pricing, supplier compliance, and off-contract buying. That change expands the role of software beyond purchasing administration and brings AI deeper into sourcing strategy, spend governance, and replenishment planning. GHX also noted that a 2025 Experian survey found that 50% of healthcare decision-makers saw data quality as a top barrier to capturing these savings, which shows that the savings logic is established even when execution remains uneven.[2]GHX, “GHX Deploys New Wave of AI Capabilities to Advance the Healthcare Supply Chain,” GHX News Releases, ghx.com

AI and Big-Data Adoption in Healthcare Logistics

The AI-based healthcare supply chain management market is still in an early scale-up stage, even though demand forecasting, inventory optimization, and supply planning are already recognized as high-value AI use cases. The real barrier is often not the AI model itself, but the absence of normalized item masters, clean procurement records, and reliable interfaces between ERP, EHR, warehouse, and supplier systems. GHX reported in July 2025 that it supports more than USD 220 billion in annual supply chain spend across over 4,100 providers and 600 suppliers in North America, which shows why incumbents with rich transaction data can train stronger domain models than many software-only entrants. The AI-based healthcare supply chain management market is therefore being shaped by data scale and data quality as much as by algorithm choice, and that favors vendors that already sit inside high-volume healthcare trading networks.

Growing Complexity of Cold-Chain Biologics Flows

The AI-based healthcare supply chain management market is being pushed forward by the rising share of biologics, GLP-1 injectables, monoclonal antibodies, and advanced therapies that move through narrow temperature windows and carry high write-off risk when excursions occur. In this part of the market, the value of AI is shifting from reactive alerting toward predictive orchestration, because operators want to intervene before a shipment leaves the dock rather than after a temperature breach has already happened. Cargo Newswire reported in April 2026 that Tempmate and PAXAFE announced a partnership at LogiPharma 2026 to replace reactive monitoring with AI-driven and risk-aware orchestration across international transport lanes.[3]tempmate and PAXAFE, “AI-Driven Alliance to Advance Predictive Cold Chain Intelligence in Pharmaceutical Logistics,” Cargo Newswire, cargonewswire.com The more strategic value lies in lane-level and carrier-level risk scoring, where systems can estimate excursion probability before departure and guide packaging, routing, and service-level choices while a correction is still economical. Moderna also described an autonomous cold-chain blueprint that links GxP-validated acceptance and rejection decisions to live logistics data and uses those results to improve lane qualification over time. As biologics volumes expand, the AI-based healthcare supply chain management market is likely to treat this predictive capability as essential operating infrastructure rather than as an optional premium feature.

Global Serialization / Track-and-Trace Mandates

The AI-based healthcare supply chain management market is also being strengthened by serialization and track-and-trace rules that require more granular and more interoperable transaction data across pharmaceutical supply chains. SoftGroup’s May 2026 tracker stated that 26 markets had mandatory serialization in force, with 8 additional markets operating against binding enforcement deadlines, which reflects the widening compliance burden carried by manufacturers, distributors, and logistics partners. In the United States, the Drug Supply Chain Security Act requires electronic and package-level transaction data exchange across trading partners, which pushes the supply base toward the digital infrastructure that AI platforms need. The practical effect is that serialization does more than support compliance, because it also creates a minimum real-time data layer that can support anomaly detection, counterfeit identification, recall prioritization, and multi-party exception handling. The AI-based healthcare supply chain management market benefits when this data starts to move across suppliers, providers, and distributors in usable formats, since AI tools can then operate on live serialized events rather than on delayed and incomplete records.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy and Cyber-Risk Exposure | -3.2% | Global, most acute in North America under HIPAA and in Europe under GDPR | Short term (≤ 2 years) to Medium term (2-4 years) |

| High Up-Front Integration Cost | -2.4% | Global, most acute in mid-market hospitals and emerging markets | Medium term (2-4 years) |

| Sparse Labeled Data for Niche SKUs | -1.8% | Global, with higher severity in specialty pharmaceutical segments | Medium term (2-4 years) |

| Shortage of AI-Supply-Chain Hybrid Talent | -1.4% | Global, with talent concentration skewed to North America and APAC technology hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Cyber-Risk Exposure

The AI-based healthcare supply chain management market faces a meaningful adoption brake because healthcare buyers are being asked to trust AI systems that sit across large vendor ecosystems and influence critical stock, contract, and compliance decisions. The HSCC Cybersecurity Working Group stated in its April 2026 AI Third-Party Risk Guide that many healthcare organizations still maintain incomplete or outdated vendor inventories and that AI-specific risks often go unreported by vendors. Proofpoint’s 2025 Ponemon healthcare cybersecurity report also found that 93% of healthcare organizations experienced a cyberattack in the previous 12 months and that 60% of respondents said protecting data used in AI systems was difficult or very difficult. This concern goes beyond simple breach risk, because procurement committees also worry about regulatory exposure, operational disruption, and the credibility of vendors that cannot clearly explain how their AI models are governed. The AI-based healthcare supply chain management market will therefore continue to see slower decisions in organizations where legal, security, and procurement teams want stronger assurance before expanding AI authority across replenishment and supplier workflows.

High Up-Front Integration Cost

The AI-based healthcare supply chain management market also slows when buyers confront the large technical effort required to connect new AI tools with legacy ERP, EHR, warehouse, and procurement systems. Integration work often includes middleware, master data cleanup, API development, testing, and process redesign, which means a large share of project cost arrives before the first model produces any usable decision support. Diginomica reported in 2026 that Blue Yonder’s multiyear program to rebuild its technology stack carried a USD 2.5 billion commitment, which illustrates how deep platform modernization can run even for a leading vendor. The cost burden is often heavier for hospitals because AI projects expose data quality problems that were hidden inside older systems and now must be corrected before training and deployment can proceed. The AI-based healthcare supply chain management market therefore sees a gap between executive interest and funded execution, especially in mid-market providers and in regions where capital budgets remain constrained. Emerging AI governance standards may gradually help vendors justify total cost of ownership, but the near-term reality is that many buyers still view integration as the largest practical obstacle to scaling beyond targeted pilots.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Demand Intelligence Anchors Market, Procurement Automation Accelerates

Demand Planning and Inventory Optimization held 40.61% of AI-based healthcare supply chain management market share in 2025, making it the largest solution category by revenue. The segment leads because hospitals, distributors, and manufacturers can see direct value when AI models combine historical demand, procedure schedules, epidemiological indicators, and supplier lead times to improve replenishment timing. The AI-based healthcare supply chain management market rewards this category because it addresses a daily operating problem with measurable consequences in waste, stockouts, emergency buying, and working capital.

Procurement and Supplier Management is the fastest-growing solution type and is forecasted to expand at a 24.6% CAGR through 2031, which reflects how quickly supplier governance is becoming a digital and continuous process. The AI-based healthcare supply chain management industry is moving in this direction because health systems want AI-monitored contract compliance, automated exception handling, and supplier risk scoring instead of periodic manual review cycles. Warehouse and Inventory Execution remains an important part of the AI-based healthcare supply chain management market because labor shortages, error reduction, and throughput reliability matter as much as forecasting accuracy. AI-guided autonomous mobile robots and goods-to-person systems reduce pick errors and lower dependence on manual movement in consolidated service centers and hospital distribution environments. Workflow Automation and Control Tower Platforms are becoming more central because buyers want a single place to manage planning alerts, procurement signals, logistics disruptions, and fulfillment priorities. Medline launched its Mpower AI platform with Northwestern Medicine and Providence in September 2025, using Microsoft Azure AI to create a next-generation supply chain solution that ties multiple operational layers together. In the AI-based healthcare supply chain management market, this integration layer matters because it turns separate forecasting and procurement tools into part of one coordinated operating model.

By Deployment Mode: Cloud Dominance Reinforces but Hybrid Architectures Gain Nuance

Cloud-based deployment accounted for 54.33% of the AI-based healthcare supply chain management market size in 2025, and it is also the fastest-growing deployment mode with a 22.84% CAGR through 2031. This dual lead shows that buyers increasingly prefer architectures that can scale across sites, handle large data volumes, and support continuous model updates without the hardware refresh burden carried by on-premise environments. The AI-based healthcare supply chain management market has moved in this direction because cross-site and cross-supplier analytics require elastic compute, shared data pipelines, and faster integration across trading partners. Cloud economics also align with healthcare procurement preferences, since subscription spending can be easier to phase than large capital commitments tied to local infrastructure. These benefits are strongest when organizations want to connect demand signals, supplier data, contract performance, and shipment events in a common operating environment rather than in separate local systems.

On-premise deployment still retains a structural role in parts of the AI-based healthcare supply chain management market where data sovereignty, institutional risk tolerance, or national policy creates limits on shared cloud use. This is more relevant in compliance-sensitive environments where organizations want tighter local control over data, user permissions, and system validation.

By End-User: Hospital Networks Set the Baseline, Pharma-Biotech Companies Drive Margin-Led AI Investment

Hospitals and Clinics accounted for 48.40% revenue in 2025, which made them the largest end-user group in the AI-based healthcare supply chain management market. Their leading share reflects the sector’s role as the main consumption point for medical products, drugs, surgical supplies, and fast-moving inventory that must be managed across many departments and care sites. Hospitals generate the data density that AI tools need, since procurement activity, procedure schedules, and replenishment events occur every day and across very large item catalogs. The AI-based healthcare supply chain management industry sees hospitals as a foundational user group because adoption in these organizations creates reference cases, workflow depth, and recurring data volume that can support broader platform expansion. Third-party logistics providers, medical device manufacturers, and distributors also represent active demand pockets, but their investment logic is more closely tied to service-level compliance and customer requirements than to direct clinical operations.

Pharmaceutical and Biotech Companies are the fastest-growing end-user group and are projected to grow at a 22.41% CAGR in the AI-based healthcare supply chain management market size through 2031. This growth reflects the combined effect of biologics expansion, broader serialization requirements, and the high financial cost of cold-chain failures, expired stock, and delayed clinical supply. The AI-based healthcare supply chain management market is especially compelling for these companies because AI can protect revenue and compliance at the same time, which makes the return on investment easier to identify. The result is a segment that carries high technical demands but also some of the strongest monetizable benefits in the entire market.

Geography Analysis

North America held 40.11% of AI-based healthcare supply chain management market share in 2025, which kept it as the largest regional market. The region leads because healthcare delivery networks are large, digital maturity is relatively high, and provider and distributor systems are more deeply integrated than in many other markets. The full enforcement milestone for the Drug Supply Chain Security Act on May 27, 2025 strengthened that position by requiring electronic and package-level traceability across prescription drug trading partners. The United States also sees stronger demand for tools that can reduce contract leakage, improve replenishment discipline, and support more auditable workflows across large health systems. This regional structure makes North America the clearest current proof point for enterprise-scale deployment in the AI-based healthcare supply chain management market.

Europe remains an important but more mixed regional environment for the AI-based healthcare supply chain management market because strong compliance demand sits beside more complex integration realities. The region’s direction is shaped by the EU Falsified Medicines Directive, the European Medicines Verification Organization framework, and the added friction created by GDPR requirements for data handling and cross-border deployments. The United Kingdom, France, and Italy are also advancing AI-assisted procurement and supply pilots as hospitals work under tighter operating budgets and ongoing service pressure. The AI-based healthcare supply chain management market in Europe therefore combines strong regulatory logic with a slower operational rollout pattern.

Asia-Pacific is projected to expand at a 23.35% CAGR in AI-based healthcare supply chain management market size through 2031, making it the fastest-growing regional market. Growth is being driven by regulatory reform, pharmaceutical export complexity, rising digital infrastructure investment, and stronger supply chain modernization across China, India, Japan, and Southeast Asia. The AI-based healthcare supply chain management market in Asia-Pacific is therefore expanding quickly because manufacturers and distributors are facing both regulatory and operational reasons to digitize. Middle East and Africa, along with South America, remain earlier-stage regions in the AI-based healthcare supply chain management market, but their long-term structure is improving. The GCC benefits from established serialization systems in Saudi Arabia and the UAE, while South Africa offers a focused use case in multi-temperature pharmaceutical distribution. Brazil’s SNCM framework and Argentina’s ANMAT traceability model create stronger data foundations in South America, especially for pharmaceutical distributors and larger hospital networks. GS1-aligned barcode and EPCIS standards also help lower integration friction for multi-country deployments by giving trading partners a more common data vocabulary.

Competitive Landscape

The AI-based healthcare supply chain management market is moderately concentrated at the enterprise platform tier, where SAP, Oracle, Blue Yonder, IBM, and major distribution-linked operators compete on platform breadth, data connectivity, and workflow coverage. The largest vendors hold an advantage because they can connect AI functions to established ERP environments, procurement workflows, and trading partner ecosystems that customers already use. In the AI-based healthcare supply chain management market, this matters because buyers are usually not looking for isolated algorithms, but for systems that can sit inside compliance-sensitive processes and still scale across sourcing, planning, inventory, and fulfillment. McKesson and Cardinal Health compete from a different position, using their distribution infrastructure and network reach to embed AI into operational environments that software-only vendors cannot replicate easily. That creates a layered competitive structure where platform vendors, distributors, and focused healthcare specialists each try to control different parts of the value chain.

Several strategic moves show how this competition is evolving. Tecsys launched TecsysIQ in June 2025 as a cloud-native intelligence layer built on the Databricks Data Intelligence Platform, with the explicit goal of delivering machine learning insights across clinical, operational, and financial systems for healthcare supply chains. Oracle introduced AI Advanced Inventory Management in September 2025 to help healthcare organizations manage urgent surgical kits, cross-docking, and operational decision support inside its Fusion Cloud environment. SAP introduced Supply Chain Orchestration in October 2025 as an AI-driven and multi-tier visibility platform built on SAP Business Technology Platform and integrated with SAP Business Network, which signals a clear move toward more connected supply control. Blue Yonder then raised the competitive bar in May 2026 with its Model Training Factory initiative, built with NVIDIA Nemotron models and synthetic data, which points to a strategy centered on proprietary supply chain agent development.

Procurement standards and governance requirements are becoming another competitive filter. ISO and AI governance frameworks are beginning to appear more often in advanced health system procurement processes, which means vendors are being judged not only on features, but also on how clearly they can explain control, validation, and accountability. The AI-based healthcare supply chain management market is therefore becoming more formal in how buyers evaluate vendors, especially when AI tools start to influence replenishment, contracting, and traceability decisions. Mid-market challengers such as Tecsys and Kinaxis still have room to differentiate by offering narrower, faster, and more healthcare-specific deployments than the largest enterprise suites. That mix of strong incumbents and open workflow gaps supports the view of a market that is concentrated in the upper tier but still actively contested below it.

AI-Based Healthcare Supply Chain Management Industry Leaders

IBM

SAP SE

Oracle

Microsoft Corporation

Tecsys Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Blue Yonder announces Model Training Factory in partnership with NVIDIA. Built on NVIDIA Nemotron models and NeMo Agent Toolkit, the factory develops specialized AI agents for autonomous supply chain workflows using synthetic data rather than customer data, targeting warehouse and planning decisioning at scale. This positions Blue Yonder to compete on owned AI model economics rather than dependency on general-purpose frontier models, with first production deployments planned through its Cognitive Solutions portfolio later in 2026.

- May 2026: Arrive AI expands autonomous logistics network at Hancock Health. Building on a successful initial deployment at Hancock Regional Hospital, Arrive AI extended its AI-powered Arrive Points autonomous logistics system to the Parkway outpatient facility in Greenfield, Indiana, for transport of lab specimens from outpatient draw centers. The expansion advances Hancock Health's broader initiative to modernize laboratory operations through workflow-first automation.

- January 2026: Rohto Pharmaceutical begins multi-AI agent supply chain validation with Fujitsu. Piloting Fujitsu's multi-AI agent coordination technology integrated with Rohto's cyber-physical system at its Ueno Techno Center in Mie Prefecture, the program targets full supply chain optimization from procurement through distribution and sales with real manufacturing and logistics data. The validation runs through March 2027.

Global AI-Based Healthcare Supply Chain Management Market Report Scope

According to the report’s scope, the AI-based healthcare supply chain management market refers to the use of artificial intelligence technologies to optimize the planning, procurement, inventory management, logistics, and distribution of healthcare products and medical supplies. These solutions leverage machine learning, predictive analytics, and automation to improve supply chain visibility, reduce costs, minimize shortages, and enhance operational efficiency across healthcare organizations.

The AI-based healthcare supply chain management market is segmented into solution type, deployment mode, end-user, and geography. By solution type, the market is segmented into demand planning and inventory optimization, procurement and supplier management, logistics and distribution optimization, warehouse and inventory execution, and workflow automation and control tower platforms. By deployment mode, the market is segmented into cloud-based and on-premise. By end-user, the market is segmented into hospitals and clinics, pharmaceutical and biotech companies, medical device manufacturers, third-party logistics providers (3PLs), and distributors and wholesalers. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Demand Planning and Inventory Optimization |

| Procurement and Supplier Management |

| Logistics and Distribution Optimization |

| Warehouse and Inventory Execution |

| Workflow Automation and Control Tower Platforms |

| Cloud-Based |

| On-Premise |

| Hospitals and Clinics |

| Pharmaceutical and Biotech Companies |

| Medical Device Manufacturers |

| Third-Party Logistics Providers (3PLs) |

| Distributors and Wholesalers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Solution Type | Demand Planning and Inventory Optimization | |

| Procurement and Supplier Management | ||

| Logistics and Distribution Optimization | ||

| Warehouse and Inventory Execution | ||

| Workflow Automation and Control Tower Platforms | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| By End-User | Hospitals and Clinics | |

| Pharmaceutical and Biotech Companies | ||

| Medical Device Manufacturers | ||

| Third-Party Logistics Providers (3PLs) | ||

| Distributors and Wholesalers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in AI-based healthcare supply chain management through 2031?

Growth is being driven by cost pressure, wider AI use in logistics, more complex biologics cold chains, and stricter serialization requirements. The market is projected to rise from USD 4.22 billion in 2026 to USD 10.56 billion by 2031 at a 20.15% CAGR.

Which solution area currently leads spending?

Demand Planning and Inventory Optimization leads spending, with a 40.61% revenue share in 2025. Buyers favor it because it delivers measurable savings through better replenishment timing, lower waste, and improved stock availability.

Which deployment model is expanding the fastest?

Cloud-based deployment is both the largest and fastest-growing model. It held 54.33% share in 2025 and is projected to grow at a 22.84% CAGR through 2031 because it supports enterprise-scale analytics and faster integration.

Which region offers the strongest near-term opportunity?

North America remains the largest regional opportunity with 40.11% share in 2025, supported by digital maturity and DSCSA enforcement. Asia-Pacific offers the strongest growth outlook, with a projected 23.35% CAGR through 2031.

Page last updated on: