Artificial Intelligence In Drug Discovery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

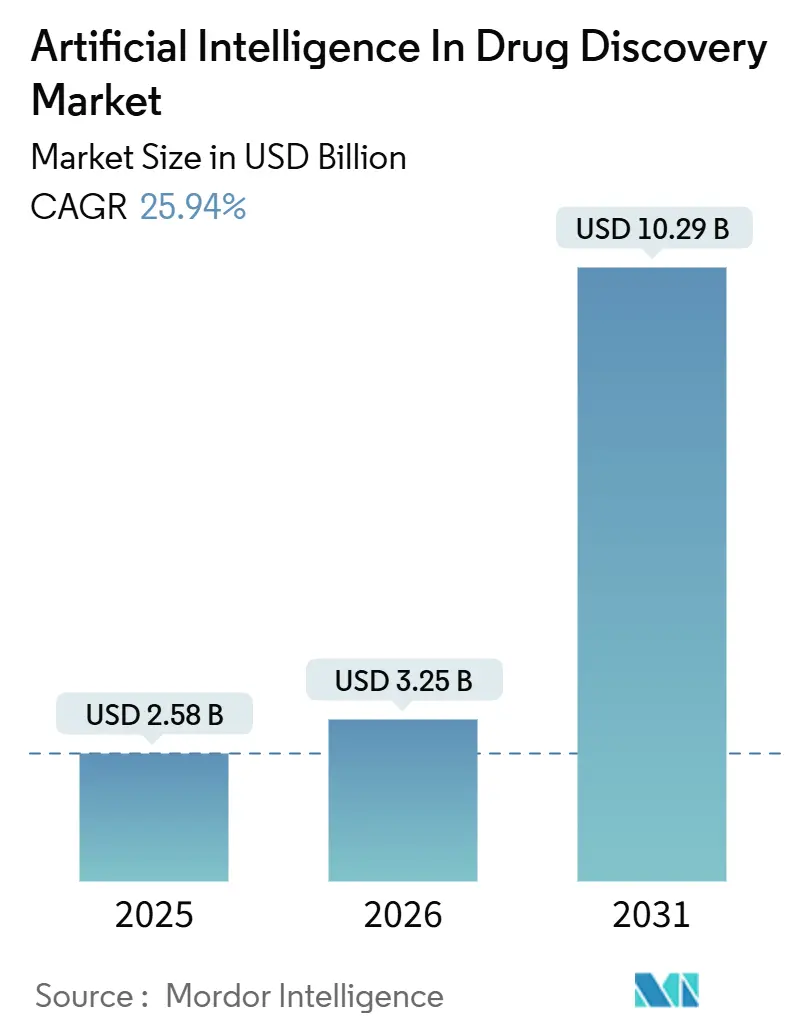

| Market Size (2026) | USD 3.25 Billion |

| Market Size (2031) | USD 10.29 Billion |

| Growth Rate (2026 - 2031) | 25.94% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Artificial Intelligence In Drug Discovery Market Analysis by Mordor Intelligence

The Artificial Intelligence In Drug Discovery Market size was valued at USD 2.58 billion in 2025 and is estimated to grow from USD 3.25 billion in 2026 to reach USD 10.29 billion by 2031, at a CAGR of 25.94% during the forecast period (2026-2031).

Growing pressure to compress multiyear discovery cycles, combined with the USD 2.6 billion average cost of commercializing a single molecule, is steering budget toward platforms that simulate medicinal-chemistry tasks at an industrial scale. The artificial intelligence in drug discovery market is also benefiting from cloud providers that supply elastic infrastructure, lowering entry barriers for mid-sized biotechs. Specialized start-ups validated by clinical-stage assets are attracting late-stage venture capital, intensifying competition for proprietary biomedical data. Meanwhile, regulators on both sides of the Atlantic issued draft guidances that clarify acceptable audit trails for AI models, giving large pharmaceutical companies the confidence to move more programs from pilot to production.

Key Report Takeaways

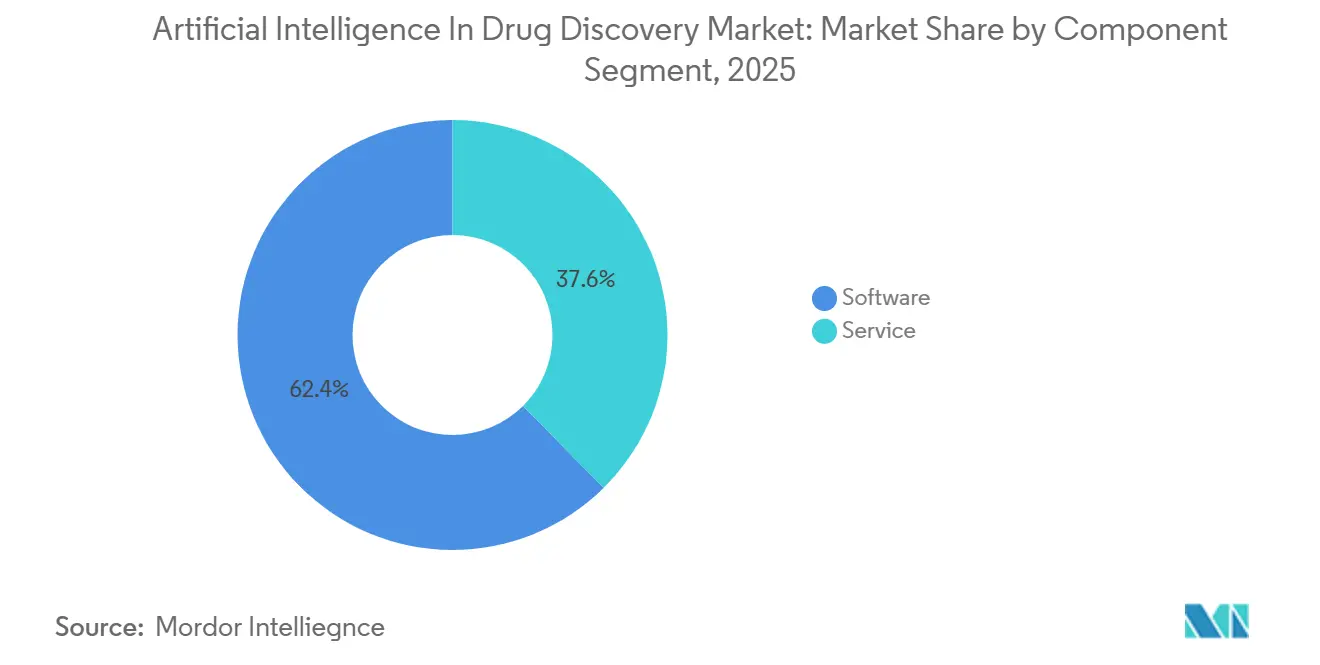

- By component, software led with 62.43% revenue share in 2025, while services are projected to expand at 27.54% CAGR through 2031.

- By technology, machine learning represented 46.54% share in 2025, whereas quantum machine learning is advancing at 27.65% CAGR to 2031.

- By application, target identification and validation held 28.43% share of the artificial intelligence in drug discovery market size in 2025, yet de novo design is growing at 28.54% CAGR toward 2031.

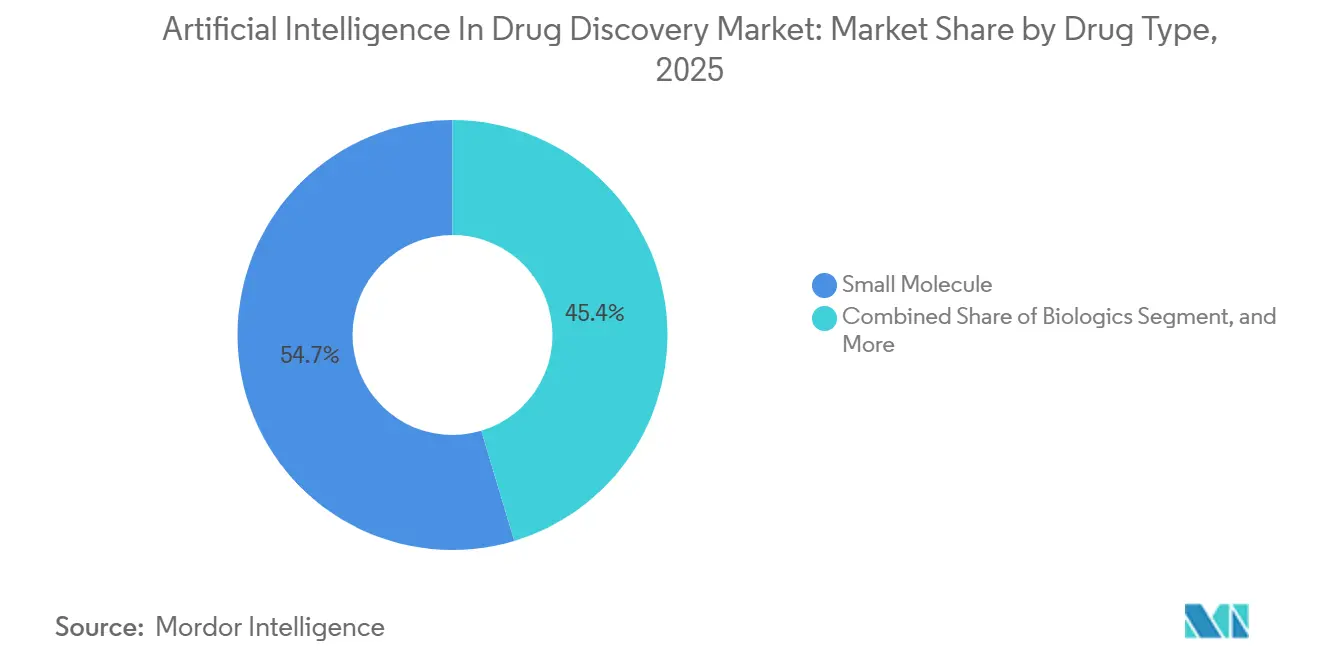

- By drug type, small molecules accounted for 54.65% of the artificial intelligence in drug discovery market share in 2025; gene and cell therapy registers the fastest 25.32% CAGR through 2031.

- By deployment, cloud-based platforms captured 82.43% share in 2025 and are expanding at a 27.43% CAGR, as on-premises clusters cede to scalable infrastructure.

- By end-user, pharmaceutical & biotechnological companies captured 67.43% share in 2025. Academic & Research Institutes registers the fastest 28.43% CAGR through 2031.

- By geography, North America captured 43.54% share in 2025. Asia-Pacific registers the fastest 26.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Artificial Intelligence In Drug Discovery Market*

| Market Driver | (~) % Impact on CAGR | Forecast Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Biopharmaceutical R&D Cost Pressures | +6.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Growing Global Disease Burden Across Chronic And Infectious Areas | +5.8% | Global, with acute impact in APAC and Africa | Long term (≥ 4 years) |

| Increasing Strategic Collaborations Between Pharmaceutical And AI Companies | +5.1% | North America, Europe, APAC core | Short term (≤ 2 years) |

| Expansion Of High-Quality Biomedical Data Assets | +4.3% | North America and Europe, spill-over to APAC | Medium term (2-4 years) |

| Advancing Cloud And High-Performance Computing Accessibility | +3.7% | Global | Short term (≤ 2 years) |

| Emergence Of Next-Generation AI Drug Design Paradigms | +4.5% | North America, Europe, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Biopharmaceutical R&D Cost Pressures

A 40% decline in R&D productivity between 2010 and 2024 prompted executives to fund predictive algorithms that shortened lead-optimization cycles from 18 months to 6 months. Exscientia demonstrated in 2025 that its AI-designed molecules progressed to first-in-human studies inside a single year, evidencing cash-on-cash returns that traditional medicinal-chemistry workflows cannot match. Rare-disease programs stand to gain most because limited patient pools restrict break-even sales. Budget-constrained biotechs increasingly license turnkey AI services, helping explain why services outpace software in compound annual growth. The artificial intelligence in drug discovery market, therefore, functions as a cost-avoidance mechanism rather than an incremental expense line.

Growing Global Disease Burden Across Chronic and Infectious Areas

Chronic illnesses accounted for 74% of worldwide mortality in 2025, yet only a fraction of new molecular entities addressed metabolic or cardiovascular pathways. AI platforms interrogate multi-omic datasets to surface polygenic targets that elude reductionist screening. During the 2024 mpox resurgence, a generative-chemistry engine identified repurposing candidates inside 48 hours, illustrating real-time responsiveness that manual methods lack. Oncology still concentrates 38% of AI projects, but neurodegeneration is the fastest-expanding domain as algorithms merge brain imaging with proteomics to stratify patient subsets. The artificial intelligence in drug discovery market, therefore, scales in direct proportion to the global epidemiological shift toward chronic, multi-factorial conditions.

Increasing Strategic Collaborations Between Pharmaceutical and AI Companies

Eighty-seven partnership announcements in 2025 underscore the pivot from tech-licensing deals to equity-based, co-development models. Sanofi’s USD 150 million expansion with Exscientia typifies risk-sharing structures that embed medicinal chemists alongside data scientists. Bayer’s minority stake in Recursion further signals that incumbents consider platform ownership strategically material. As a result, vendors with validated clinical pipelines command nine-figure upfronts, while early-stage start-ups compete on speed-to-clinic metrics. Collaboration velocity shortens adoption lead times, reinforcing near-term revenue for the artificial intelligence in drug discovery market.

Expansion of High-Quality Biomedical Data Assets

The UK Biobank scaled to 500,000 whole-genome sequences in 2025, enabling AI pipelines to refine target hypotheses with population-level granularity[1]UK Biobank, “Whole-Genome Sequencing Milestone,” UK Biobank, ukbiobank.ac.uk. Consortia such as the Pistoia Alliance curate 2.2 million historical compounds, letting models learn from failed scaffolds and sidestep synthetic dead ends. Real-world evidence from electronic health records feeds predictive safety models, while federated-learning architectures preserve data privacy under GDPR and HIPAA regimes. The artificial intelligence in drug discovery market thus converts heterogeneous biomedical repositories into competitive advantage.

Restraints Impact Analysis of Artificial Intelligence In Drug Discovery Market*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory And Clinical Adoption Challenges Related To AI Explainability | -3.2% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Limited Availability Of Integrated Multidisciplinary Talent | -2.1% | Global, most severe in APAC | Short term (≤ 2 years) |

| Data Fragmentation And Lack Of Standardization Across Research Silos | -1.8% | Global | Long term (≥ 4 years) |

| Intellectual Property And Liability Uncertainties For AI-Generated Molecules | -1.5% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory and Clinical Adoption Challenges Related to AI Explainability

FDA’s 2025 draft guidance obliges sponsors to document model lineage and decision boundaries, yet most neural networks remain opaque. Without mechanistic rationales, clinical investigators hesitate to enroll patients, slowing trial accrual. The European Medicines Agency formed an AI committee in 2025, but harmonized rules are years away[2]European Medicines Agency, “EMA Establishes AI Working Party,” EMA, ema.europa.eu. Attention mechanisms improve interpretability but at the cost of predictive power, creating a trade-off that sponsors must navigate. In the artificial intelligence in drug discovery market, these compliance hurdles translate into longer validation timelines and greater documentation overhead.

Limited Availability of Integrated Multidisciplinary Talent

Universities graduated only 1,200 professionals fluent in medicinal chemistry, machine learning, and computational biology in 2025, far below the 8,000 roles industry sought. Median salaries for computational chemists with deep-learning skills reached USD 220,000, a 45% premium over traditional chemists. The talent gap is acute in APAC, where CRO build-outs outpace academic pipelines. Smaller firms lacking cash competitiveness outsource algorithmic work, increasing project-management complexity. Until curricula evolve, the artificial intelligence in drug discovery market will contend with a structural skills bottleneck.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Artificial Intelligence In Drug Discovery Market Segment Analysis

By Component:

Services Gain as Pharma Outsources AI WorkflowsServices expanded at a 27.54% CAGR through 2031, outpacing the 62.43% baseline share held by software in 2025. This shift indicates that many companies view algorithmic discovery as an enabling layer rather than a core competency. The artificial intelligence in drug discovery market size for services reached USD 0.79 billion in 2026, reflecting heightened demand for turnkey target-identification pipelines. Contract research organizations now integrate active-learning modules that clients pay for per project, thereby converting fixed costs into variable outlays. Software remains indispensable because it preserves internal IP control over proprietary libraries. However, the spread of per-simulation pricing blurs boundaries, effectively turning license models into usage-based services. Over time, if AI-discovered molecules demonstrate superior Phase III success rates, large pharma may rationalize vendor rosters, dampening service-segment fragmentation.

Pharmaceutical majors, therefore, hedge by maintaining small in-house data-science teams alongside external contracts, ensuring optionality. The service value proposition resonates strongly with seed-stage biotechs that lack capital for a dedicated compute stack. Regulatory demand for validated audit trails further favors specialized vendors offering documentation as a managed service. Consequently, the artificial intelligence in drug discovery market continues to bifurcate between platform providers with recurring subscription revenue and project-based consultancies that monetize depth of therapeutic expertise.

By Technology:

Quantum Machine Learning Emerges as Long-Term DisruptorMachine-learning frameworks dominated 46.54% of 2025 spend, but quantum approaches are on track for a 27.65% CAGR to 2031. The artificial intelligence in drug discovery market size attributable to quantum algorithms is projected to surpass USD 1 billion by 2031 if hardware error-correction milestones arrive on schedule. Presently, algorithms such as neural-quantum states simulate under 100 atoms, limiting scope. Natural-language processing, with 18% share, mines 30 million biomedical publications to enrich knowledge graphs. Computer-vision models process 10-terabyte image sets from phenotypic screens, holding 12% share.

Model-foundation trends are converging: several firms fine-tune open-source protein models like ESM-2 rather than train bespoke architectures, cutting data requirements by 80%. Quantum readiness partnerships—for example, IBM and Moderna—signal future scaling paths for complex biologic simulations. Should fault-tolerant qubits become commercially viable, the artificial intelligence in drug discovery market could witness a rapid reweighting toward quantum-native vendors.

By Application:

De Novo Design Redefines Discovery EconomicsTarget identification and validation captured 28.43% of 2025 expenditure, reflecting industry desire to de-risk programs before chemistry begins. De novo design, however, is accelerating at 28.54% CAGR, and its artificial intelligence in drug discovery market share is expected to reach 35% by 2031. Hit prioritization, lead optimization, and candidate screening collectively hold roughly 41% share, with AI-powered ADMET filters eliminating low-probability molecules early in the funnel. Drug repurposing remains a nimble strategy for rare diseases, leveraging electronic health record analytics to flag unexpected efficacy signals in weeks rather than months. Preclinical toxicity screening still commands only mid-single-digit spend, yet its strategic value is rising as regulators scrutinize mechanistic safety rationales.

Generative diffusion models now generate scaffolds optimized across multiple parameters, undermining traditional virtual screening mojo. As intellectual property pools shift from incremental analogs to first-in-class chemotypes, de novo design is poised to reconfigure value capture within the artificial intelligence in drug discovery market.

By Drug Type:

Gene and Cell Therapy AI Accelerates Precision MedicineSmall molecules retained 54.65% share in 2025, but biologics and cell-based therapies collectively posted the fastest growth. The artificial intelligence in drug discovery market size for gene and cell therapy surpassed USD 0.33 billion in 2026 and is projected to quadruple by 2031. AI engines optimize vector tropism and predict immunogenicity, turning once-trial-and-error tasks into in-silico design loops. Biologics, at 32% share, benefit from databases rich in antibody-antigen pairings, enabling platforms to project binding affinity and developability simultaneously.

Venture investors funneled USD 1.2 billion into AI-first cell-therapy platforms during 2025, triple 2023 totals. Although small molecules still enjoy an order-of-magnitude larger training corpus, novel biologic modalities yield higher clinical-success probabilities, enticing capital. Over the forecast horizon, the artificial intelligence in drug discovery market will likely see biologics and gene/cell therapies eclipse small molecules in aggregate project count.

By Deployment:

Cloud Dominance Reflects Data Scale and Collaboration NeedsCloud platforms accounted for 82.43% of deployments in 2025 and continue at 27.43% CAGR. The artificial intelligence in drug discovery market size linked to cloud subscriptions exceeded USD 2 billion in 2026. Elastic compute allows real-time scaling during intensive docking campaigns and supports federated learning, ensuring data never leaves proprietary silos. On-premise clusters linger primarily to satisfy data-localization statutes such as China’s Biosecurity Law, which mandates local genomic storage.

Hybrid architectures remain a temporary compromise; cost comparisons show 40% savings when molecular-dynamics simulations migrate to vendor-managed GPU nodes. As throughput demands surge, maintenance overhead renders owned hardware uneconomical for all but the five largest pharmaceutical conglomerates. By 2031, cloud adoption is projected to top 88%, embedding platform dependency deeper into the artificial intelligence in drug discovery market.

By End User:

Academic Institutes Drive Methodological InnovationPharmaceutical and biotech companies represented 67.43% of demand in 2025, reflecting their outsized R&D budgets. Academic and research institutes, though smaller in absolute dollars, are advancing at a blistering 28.43% CAGR on the back of multiyear NIH grant programs. Twelve university-anchored AI centers launched in 2025 alone, each aligned with a priority therapeutic area.

Academic labs publish algorithmic breakthroughs that pharmaceutical partners rapidly industrialize; Stanford’s 2025 diffusion-model paper spawned eight patent filings in six months. Government laboratories and CROs round out the segment landscape, collectively holding 10% share and embracing AI to vet sponsor submissions more efficiently. Over time, shrinking compute costs may prompt large pharma to outsource more upstream research, elevating academia’s contribution within the artificial intelligence in drug discovery market.

Geography Analysis

North America Artificial Intelligence In Drug Discovery Market

North America commanded 43.54% share in 2025, supported by FDA guidance that offers early clarity for AI-assisted dossiers. Venture funding in the United States reached USD 4.1 billion in 2025, of which 62% flowed to companies progressing at least one asset into Phase II. Canada’s Vector Institute partnered with eight pharmaceutical companies to co-develop protein-engineering foundation models. Mexico’s CRO community is onboarding AI modules to compete with Asian peers, yet broadband gaps delay full cloud migration. While the region’s share may ease to 40% by 2031, North America will likely remain the cradle for algorithmic advances, propelling the artificial intelligence in the drug discovery market.

Europe Artificial Intelligence In Drug Discovery Market

London’s Life-Sciences Accelerator injected GBP 100 million into 15 start-ups, burnishing the city’s status as Europe’s leading AI-biotech hub[3]. Germany trails on deployment: only 35% of pharma companies had operational AI pipelines in 2025. Southern Europe’s academic clusters—particularly Barcelona and Milan—leverage public funds to build open-science data lakes, creating fertile grounds for spinouts. Europe’s projected 24% CAGR ensures it will outpace North America but remain behind APAC in growth velocity.

APAC, MEA and South America Artificial Intelligence In Drug Discovery Market

Asia-Pacific is the fastest-growing region at 26.54% CAGR through 2031. China doubled its global project share to 12% in 2025, spurred by state incentives and sovereign-AI mandates. Insilico Medicine advanced three molecules into trials, the highest count for any APAC firm. India’s Syngene shortened lead-optimization cycles to three weeks using AI-enhanced retrosynthesis planning. Japan’s Takeda tapped Preferred Networks to auto-design antibodies, a move expected to seed regional know-how spillovers. South Korea and Australia run government-funded initiatives but still lack deep venture ecosystems. Middle East and Africa captured 4% share, while South America secured 3%, constrained by underdeveloped R&D infrastructure and human-capital shortages. APAC’s trajectory will determine whether the artificial intelligence in drug discovery market evolves into a tri-polar ecosystem or remains skewed toward the trans-Atlantic corridor.

Competitive Landscape

Roughly 150 vendors vie for wallet share, underscoring the market's fragmented nature. Exscientia, Recursion Pharmaceuticals, and Insilico Medicine each advanced at least two molecules into mid-stage trials by 2025, validating platform efficacy. Alphabet’s Isomorphic Labs wields AlphaFold 3 to expand design space for protein-protein therapeutics. NVIDIA positions itself as a horizontal enabler with BioNeMo, supplying computational horsepower without competing for drug-pipeline economics.

White-space persists in rare diseases and neglected tropical illnesses, which constitute 40% of unmet medical need yet attract just 8% of AI discovery investment. Niche contenders exploit these gaps: Turbine AI simulates tumor microenvironments for combo-therapy design, while Peptilogics tailors peptide scaffolds. Meanwhile, large pharmaceutical companies internalize algorithms; Roche’s 200-person AI division reduces dependence on external suppliers. Patent filings for AI-created molecules rose to 1,200 in 2025, but legal uncertainty around inventorship may favor incumbents with robust legal arms. Over 2026-2031, expected Phase III readouts will likely winnow under-performing platforms, nudging the artificial intelligence in drug discovery market toward moderate consolidation.

Artificial Intelligence In Drug Discovery Industry Leaders

Exscientia PLC

Insilico Medicine Inc.

BenevolentAI

Atomwise Inc.

Recursion Pharmaceuticals Inc.

- *Disclaimer: Major Players sorted in no particular order

Artificial Intelligence In Drug Discovery Market Companies Covered in this Report

- Aitia

- Ardigen

- Atomwise Inc.

- Auransa Inc.

- Benevolent AI

- BioXcel Therapeutics

- Cloud Pharmaceuticals

- Cyclica Inc.

- Deep Genomics

- Eagle Genomics

- Evotec

- Exscientia PLC

- Genesis Therapeutics

- Healx

- IBM

- Innoplexus AG

- Insilico Medicine

- Isomorphic Labs (Alphabet)

- Iktos

- Microsoft

- NVIDIA

- Peptilogics

- PostEra

- Recursion Pharmaceuticals Inc.

- Schrödinger Inc.

- Standigm

- Turbine AI

- Valo Health

- Verge Genomics

Read Analysis of Artificial Intelligence In Drug Discovery Companies

Recent Industry Developments in Artificial Intelligence In Drug Discovery Market

- January 2026: NVIDIA and Eli Lilly and Company announced a first-of-its-kind AI co-innovation lab focused on applying AI to tackle some of the most enduring challenges in the pharmaceutical industry.

- January 2026: NVIDIA announced a major expansion of NVIDIA BioNeMo, an open development platform that enables lab-in-the-loop workflows to develop breakthroughs in AI-driven biology and drug discovery.

Artificial Intelligence In Drug Discovery Market Report Scope and Research Methodology

Market Definition and Coverage

According to Mordor Intelligence, the artificial-intelligence-in-drug-discovery market covers all revenue generated when purpose-built AI software or cloud services (including machine-learning, deep-learning, and generative-AI tools) are licensed or contracted by pharmaceutical, biotechnology, or academic drug-research teams to accelerate target selection, hit generation, lead optimization, and pre-clinical assessment.

Scope exclusion: routine bio-informatics service fees and broad "AI in healthcare" platforms not marketed for drug-discovery workflows are left outside this study.

Segments Covered in This Report

- By Component

- Software

- Service

- By Technology

- Machine Learning

- Natural Language Processing

- Computer Vision

- Quantum Machine Learning

- By Application

- Target Identification & Validation

- Hit Generation & Prioritization

- Lead Optimization

- Candidate Screening

- Drug Repurposing

- De Novo Drug Design

- Pre-Clinical Safety & Toxicity Assessment

- By Drug Type

- Small Molecule

- Biologics

- Gene And Cell Therapy

- By Deployment

- Cloud-Based

- On-Premise

- By End User

- Pharmaceutical & Biotechnological Companies

- Academic & Research Institutes

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest Of Europe

- APAC

- China

- Japan

- India

- South Korea

- Australia

- Rest Of APAC

- Middle East And Africa

- Middle East

- GCC

- Turkey

- Rest Of Middle East

- Africa

- South Africa

- Rest Of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest Of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

We held structured interviews with computational-chemistry directors, AI platform vendors, and CRO project leads across North America, Europe, and Asia-Pacific. The conversations clarified typical license pricing, adoption hurdles, and regional funding patterns, allowing us to stress-test desk assumptions and calibrate growth drivers.

Desk Research

Our analysts extracted baseline demand signals from public bodies such as the US FDA, EMA, NIH clinical-trial registry, USPTO patent filings, and OECD R&D expenditure dashboards, then paired them with shipment and contract values visible in customs databases like Volza and tender portals such as Tenders Info. Trade associations (BIO, EFPIA), peer-reviewed journals, and company 10-Ks supplied pipeline counts, average R&D cycle times, and disclosed AI-licensing deals. Paid datasets (D&B Hoovers for company financials and Questel for patent analytics) added granularity. The sources cited here are illustrative; many additional publications were reviewed to validate facts and fill gaps.

Market-Sizing & Forecasting

Top-down modeling starts with global drug-R&D spending and new molecular-entity (NME) filings; AI penetration rates by discovery stage are applied, with adjustments for average seat licenses and service bundles. Select bottom-up checks, such as revenue roll-ups from 30 sampled vendors and median annual contract value multiplied by active users, anchor the totals. Key variables include: (1) venture funding inflow to AI bio-techs, (2) oncology pre-clinical pipeline counts, (3) cloud-computing unit prices, (4) average cost-avoidance claimed per program, and (5) regional regulatory guidance releases. A multivariate-regression forecast links these drivers to AI spend, while scenario analysis tests upside from quantum-ML deployment.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated anomaly flags, peer analyst audit, and sector-lead sign-off. Models refresh annually; interim updates trigger when funding spikes, landmark approvals, or landmark mergers alter the baseline.

How Mordor Intelligence's Artificial Intelligence In Drug Discovery Market Size Compares to Other Published Estimates

Published estimates often diverge because firms pick differing inclusion criteria, currency years, and refresh cadences.

Key gap drivers here include whether computational chemistry tool revenue is blended with broader AI-healthcare sales, how aggressively future price deflation is assumed, and the cadence at which pipeline statistics are refreshed before model lock. Mordor reports isolate pure discovery-stage spending, use mixed ASP trajectories vetted with buyers, and update every twelve months; steps some publishers skip.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.58 B (2025) | Mordor Intelligence | - |

| USD 1.86 B (2024) | Global Consultancy A | Bundles early clinical AI tools; relies on five-year-old adoption rates |

| USD 1.90 B (2024) | Industry Journal B | Uses static licence prices and omits cloud-service revenue |

The comparison shows that once scope alignment and current pricing are applied, figures converge toward Mordor's balanced view, underscoring why decision-makers trust our consistently refreshed, variable-driven baseline.

Key Questions Answered in the Report

How fast is funding growing for AI-enabled drug discovery platforms?

Venture investment reached USD 4.1 billion in 2025, up 38% from 2024, highlighting sustained capital inflows.

Which therapeutic area receives the most AI attention?

Oncology accounts for 38% of active projects, although neurodegeneration shows the fastest pipeline expansion on a percentage basis.

What drives cloud dominance in discovery workflows?

Ten-terabyte data sets from high-content screens and federated-learning needs make elastic, compliant cloud infrastructure more economical than on-premise clusters.

When might quantum algorithms become commercially significant?

If error-correction breakthroughs reach pilot readiness by 2029, quantum machine learning could capture 8-10% of workflows by 2031.

How are regulators addressing AI transparency?

FDA and EMA draft guidances issued in 2025 require explicit documentation of training data, validation metrics, and decision boundaries before trial authorization.

Where are the main talent gaps?

APAC faces the sharpest shortage of professionals trained simultaneously in medicinal chemistry, machine learning, and computational biology, slowing regional deployment plans.

Page last updated on: