AI In Predictive Toxicology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

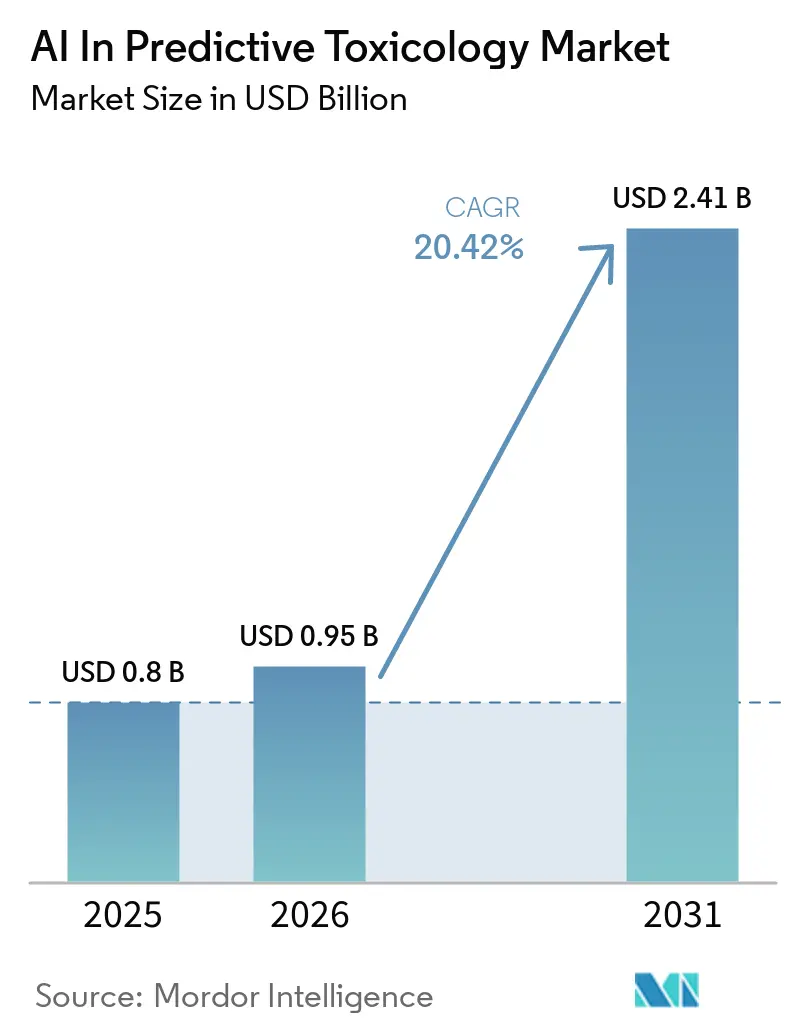

| Market Size (2026) | USD 0.95 Billion |

| Market Size (2031) | USD 2.41 Billion |

| Growth Rate (2026 - 2031) | 20.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Predictive Toxicology Market Analysis by Mordor Intelligence

The AI in predictive toxicology market size is expected to grow from USD 0.80 billion in 2025 to USD 0.95 billion in 2026 and is forecast to reach USD 2.41 billion by 2031 at 20.42% CAGR over 2026-2031. Regulatory momentum is reshaping preclinical safety practices as the U.S. FDA’s April 2025 roadmap prioritizes new approach methods and sets a clear path for reducing animal studies over the next several years, which strengthens business cases for in silico safety evaluation in the AI in predictive toxicology market. The ICH M7(R3) addendum published in 2025 formalizes enhanced read across and QSAR frameworks for nitrosamine risk assessment, which is expanding adoption of model based impurity evaluations across submissions in the AI in predictive toxicology market. Cardiac safety workflows are widening as CiPA aligned in silico models demonstrate high discriminative accuracy for Torsades de Pointes risk stratification, helping teams triage liabilities earlier in the pipeline. Open data ecosystems remain a growth catalyst since EPA ToxCast and the broader Tox21 program now provide high throughput screening results across thousands of chemicals and more than a thousand assays, enabling reproducible ML pipelines and standardized reporting in the AI in predictive toxicology market. Cloud based PBPK platforms with AI enabled features are also gaining favor as Simcyp Version 25 advances regulatory qualification milestones and supports more efficient model building and submissions, which supports distributed collaboration and scaling across global teams.

Key Report Takeaways

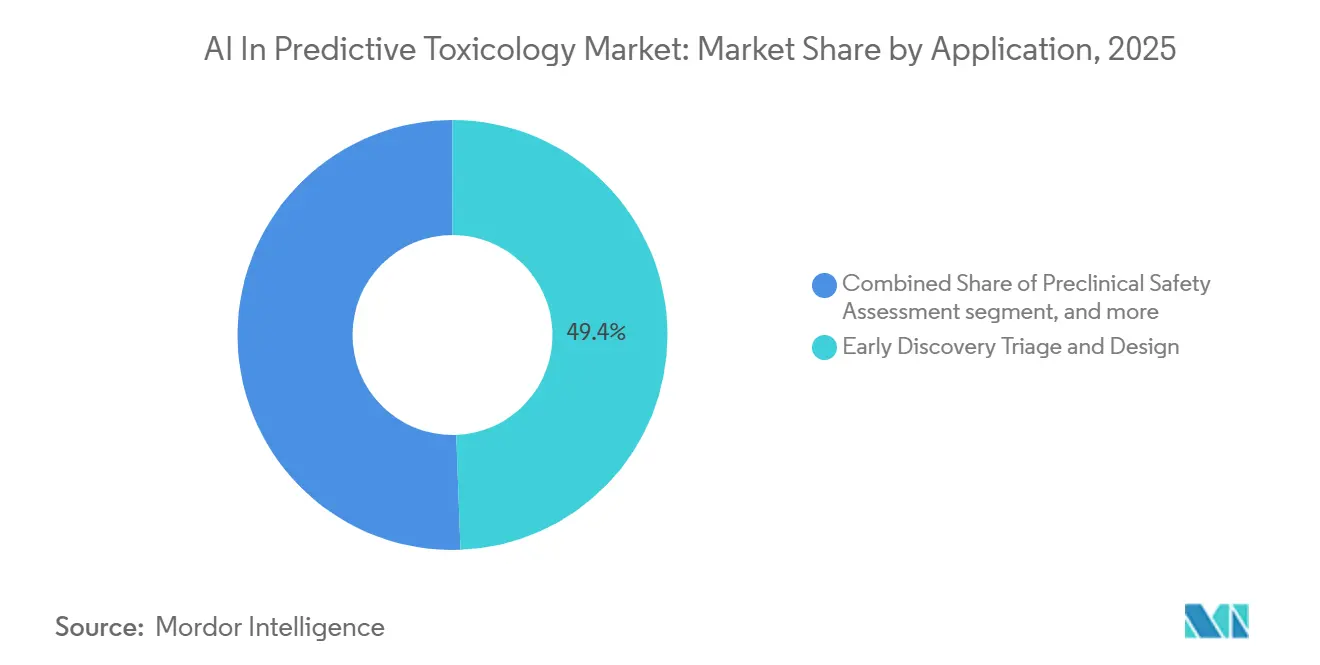

- By application, Early Discovery Triage & Design led with 49.41% revenue share in 2025, and Preclinical Safety Assessment is projected to expand at a 22.61% CAGR through 2031.

- By end user, Pharmaceutical & Biotechnology Companies contributed 47.43% of 2025 revenue, while Contract Research Organizations (CROs) & Consultancies are forecast to grow at a 21.13% CAGR over 2026 to 2031.

- By technology, Machine Learning captured 50.35% share in 2025, and Natural Language Processing is expected to post a 22.24% CAGR through 2031.

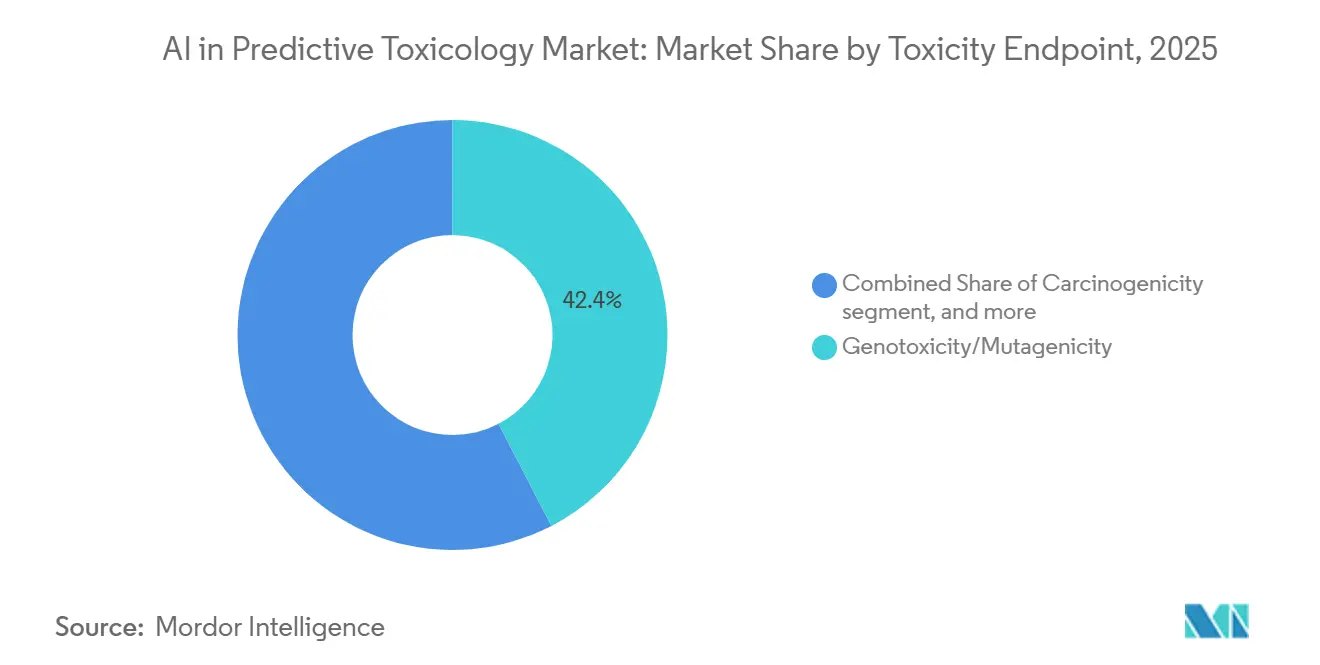

- By toxicity endpoint, Genotoxicity/Mutagenicity accounted for 42.39% share in 2025, whereas Carcinogenicity is forecast to grow at a 23.56% CAGR over 2026 to 2031.

- By deployment, Cloud/SaaS captured 50.27% share in 2025 and is set to expand at a 21.36% CAGR through 2031.

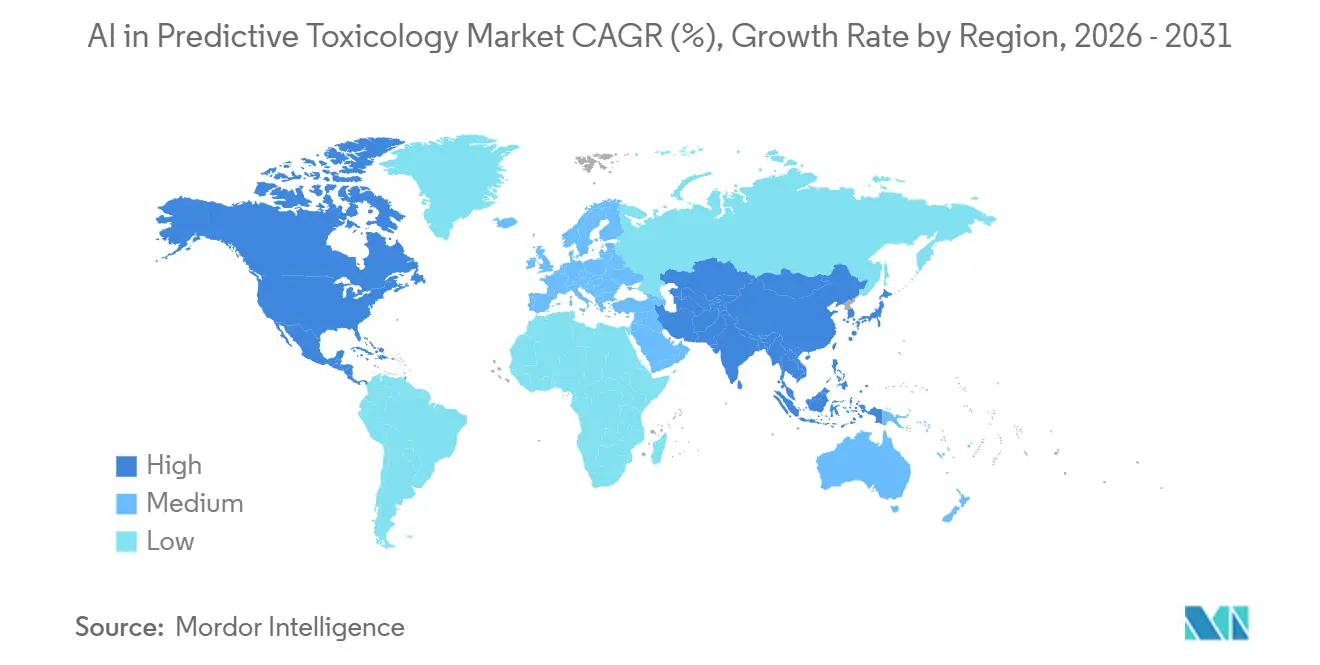

- By geography, North America commanded 48.67% of 2025 revenue, yet Asia-Pacific will accelerate at a 24.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Predictive Toxicology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ICH M7 And NAMs Accelerate in Silico Adoption | +4.2% | Global, with early adoption in US, EU, Japan | Medium term (2-4 years) |

| FDA/EPA Shift Away from Animal Testing Spurs AI Tox | +5.8% | North America core, cascading to APAC and EU | Short term (≤ 2 years) |

| Open Toxicology Datasets (ToxCast/Tox21) Enable ML Workflows | +3.1% | Global, particularly US, EU, Canada | Medium term (2-4 years) |

| Pharma Needs to Cut Attrition and Timelines to Boost AI Tox | +4.5% | Global, concentrated in US, Switzerland, UK, Japan | Short term (≤ 2 years) |

| CiPA‑Validated in Silico Cardiac Safety Expands Scope | +2.4% | US, EU, Japan, South Korea | Long term (≥ 4 years) |

| Standardized QSAR Reporting (QMRF/QPRF, AD) Builds Trust | +2.7% | Global, led by OECD member states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

ICH M7 And NAMs Accelerate in Silico Adoption

The 2025 ICH M7(R3) addendum consolidates nitrosamine risk assessment and formalizes expanded QSAR and read across methodologies that reinforce model informed impurity evaluations across submissions. Under this framework, model developers highlight standardized QMRF/QPRF reporting practices that document endpoints, algorithms, applicability domains, and validation, which helps establish traceable and fit for purpose QSAR evidence across the AI in predictive toxicology market. National guidance in the UK further endorses combining rule based systems with statistical models under expert oversight for genotoxicity predictions, which encourages blended approaches for Ames related decision making.[1]Committee on Mutagenicity, “Guidance on the Use of (Q)SAR Models to Predict Genotoxicity,” GOV.UK, gov.uk Data sharing and curated knowledge bases continue to grow through efforts like Lhasa Limited’s nitrosamine resources and Vitic Excipients, which support pre competitive exchanges that reduce duplication and improve reproducibility.[2]Lhasa Limited, “Where Can N Nitrosamine Data Support an Alternative AI Beyond the CPCA?,” Lhasa Limited, lhasalimited.org Practical integration with medicinal chemistry environments, for example through Derek Nexus access within discovery decision platforms, allows teams to screen risk motifs during design and to prioritize safer series earlier. These elements together improve confidence in in silico evidence packages and increase the operational role of QSAR across the AI in predictive toxicology market.

FDA/EPA Shift Away from Animal Testing Spurs AI Tox

The FDA’s April 2025 roadmap sets a near term path to make animal studies the exception, which elevates the role of new approach methods and AI enabled models in regulatory decision support for the AI in predictive toxicology market.[3]U.S. Food and Drug Administration, “Roadmap to Reducing Animal Testing in Preclinical Safety Studies,” U.S. Food and Drug Administration, fda.gov The FDA’s ISTAND pilot had accepted eight NAMs by early 2025 and continues to promote model credibility frameworks that emphasize data governance, lifecycle maintenance, and transparent documentation aligned with intended use. EPA’s ToxCast portfolio provides high throughput assay data and harmonized retrieval pipelines that are enabling reproducible ML workflows and consistent reporting formats for concentration–response modeling. This alignment is complemented by PBPK platforms licensed by multiple global regulators and enhanced with AI enabled features in 2026, which streamline model building and submission packages. As these policies propagate across the AI in predictive toxicology market, development teams are able to reduce reliance on long duration animal studies and redirect resources to model informed study design.

Open Toxicology Datasets (ToxCast/Tox21) Enable ML Workflows

EPA’s ToxCast Phase II and the broader Tox21 collaboration provide public access to high throughput results for more than 10,000 chemicals across 1,400+ assays, with distribution through programmatic interfaces that help automate data extraction and curation for ML pipelines in the AI in predictive toxicology market. Programmatic updates to invitrodb and aligned software tooling enable reproducible concentration–response modeling and metadata standards that reduce friction in model training and evaluation. Tox21’s operational framework continues to expand the assay landscape, providing a common reference for academic, government, and industry labs that integrate NAMs into discovery and preclinical workflows.[4]NCATS, “Tox21 Operational Model,” National Center for Advancing Translational Sciences, ncats.nih.govDevelopmental toxicity modeling that combines assay features with curated reference sets shows improving performance and clear routes to scale, which reinforces the value of shared datasets for hazard prediction. Open QSAR suites such as OPERA add coverage for endocrine activity, acute toxicity, and key physicochemical properties with uncertainty estimates, which helps improve regulatory trust in predictions. Northern European regulators also draw from large QSAR databases in plant protection assessments, which signals continued cross-border harmonization and knowledge transfer across the AI in predictive toxicology market.

Pharma Needs to Cut Attrition and Timelines to Boost AI Tox

R&D teams are expanding model based design and triage to compress cycle times and reduce late stage safety failures, which strengthens demand for the AI in predictive toxicology market. Generative design platforms have documented faster design cycles and lower synthesis counts, which reduces spend while preserving decision quality in early discovery. Company programs report advances in multi omics predictive modeling that screen success and failure signals at scale, supporting scenario analysis and portfolio decisions. Large pharmas are investing in internal AI models that predict molecular behavior, flag likely off target risks, and reduce rework across medicinal chemistry sprints. Discovery groups are also embedding AI across research IT stacks, using cloud environments to extend compute elasticity while maintaining governance standards. These operating gains reinforce the shift toward model informed triage as teams balance speed, cost, and safety rigor in the AI in predictive toxicology market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sparse, Heterogeneous Labels for Complex Endpoints (DART, Chronic) | -3.8% | Global, acute in APAC and Latin America | Medium term (2-4 years) |

| Regulatory Acceptance Still Narrow Beyond ICH M7/CiPA | -2.6% | Global, particularly stringent in Japan, South Korea | Short term (≤ 2 years) |

| EU AI Act High‑Risk Controls Add Compliance Overhead | -1.9% | EU core, spill‑over to UK, Switzerland | Long term (≥ 4 years) |

| Data/IP Silos Restrict Precompetitive Model Training | -2.4% | Global, concentrated in US, EU pharma hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sparse, Heterogeneous Labels for Complex Endpoints (DART, Chronic)

Developmental and reproductive toxicity and long latency endpoints remain hard to model because labeled datasets are fragmented and uneven across species and assay types, which limits generalization outside training domains. While public programs expanded chemical coverage and increased the number of high throughput assays, many complex endpoints still have data scarcity that constrains balanced performance and reduces external validity. Combined modeling approaches that integrate multiple assay features show improvements on curated sets for developmental toxicity, but the limited compound counts emphasize the need for sustained data generation. Heterogeneous assay protocols and species differences introduce harmonization challenges that require additional metadata standards and guardrails for model transfer. Addressing these constraints will require further investment in public datasets and stronger cross industry sharing to unlock robust models for DART and chronic endpoints in the AI in predictive toxicology market.

Regulatory Acceptance Still Narrow Beyond ICH M7/CiPA

Formal regulatory acceptance is still concentrated around well established paradigms such as ICH M7 and CiPA, and broader qualification of AI models for endpoints like hepatotoxicity and neurotoxicity is evolving at a measured pace. The FDA’s ISTAND pathway has limited throughput, which underscores the need for clear credibility frameworks and endpoint specific validation standards to scale review predictability. Regulators emphasize expert oversight and mechanistic justification alongside statistical predictions for genotoxicity, which indicates that hybrid expert in the loop processes will remain important in the near term. Progress on standardized read across practice and guidance continues in the scientific literature and across agencies, but full integration into chronic toxicity decisions will take time and iterative evidence generation. This dynamic encourages developers to pair AI predictions with transparent documentation and to align use cases with current regulatory comfort in the AI in predictive toxicology market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Early Discovery Commands Share, Preclinical Assessment Surges

Early Discovery Triage and Design accounted for 49.41% of the AI in predictive toxicology market size in 2025 as R&D teams scaled virtual screening and design space exploration before synthesis. Generative design workflows report faster design cycles with lower synthesis counts, which helps reduce costs during hit to lead and lead optimization. Platform integrations that surface toxicity alerts inside medicinal chemistry tools help scientists avoid risky substructures and prioritize safer series earlier in cycles. Curated nitrosamine resources and impurity frameworks enable consistent decision support for impurity control strategies in regulated submissions. Expanded programmatic access to high throughput screening data continues to provide training corpora and benchmarking sets for discovery stage classification and prioritization across the AI in predictive toxicology market.

Preclinical Safety Assessment is forecast to grow at 22.61% CAGR from 2026 to 2031 as model informed DILI prediction and virtual trial simulations compress assay timelines and focus confirmatory testing. Commercial DILI modules that achieve strong predictive performance are being embedded into broader translational platforms, which standardizes feature extraction and case review. In silico cardiac risk tools complement wet lab ion channel assays by aggregating multi channel effects and delivering clear risk classifications for study design. PBPK platforms with AI enabled guidance and chat support reduce manual steps and accelerate scenario testing for formulation and DDI risk. Public funding for high throughput genetic toxicology and collaborative datasets is also expanding access to transcriptomic information that complements conventional preclinical endpoints.

By End user: Pharma Dominates, CROs Accelerate Through AI Infrastructure

Pharmaceutical and Biotechnology Companies commanded 47.43% of revenue in 2025 as internal platforms scaled ML guided design, safety triage, and PBPK workflows across discovery and early development. Enterprise programs in 2026 highlight internal foundation models that forecast compound behavior and identify likely off target effects to de risk earlier. Partnerships that combine knowledge graphs and multimodal biomedical data with pharmaceutical domain expertise continue to expand, which supports target discovery and mechanistic annotation. Early deployment examples show design acceleration and synthesis reduction with generative platforms, which helps conserve resources in high throughput ideation settings. Broader access to NAMs and standardized QSAR reporting supports consistent internal governance for submission ready evidence packets across the AI in predictive toxicology market.

Cpntract Research Organizations (CROs) and Consultancies are expected to grow at 21.13% CAGR as sponsors outsource AI enabled screening, QSAR reporting, and preclinical simulations to partners that operate at scale. Service providers are launching AI driven discovery platforms trained on proprietary assay archives to improve ADMET classification performance and provide consistent reporting at enterprise scale. Strategic collaborations that link AI with clinical and preclinical expertise continue to expand the service scope for sponsors seeking end to end coverage. Public awards to build NAM based toxicity models are supporting ecosystem capacity by funding data assets and shared tools for DILI and cardiotoxicity across networks of academic and biopharma collaborators. As sponsors seek flexible capacity and specialized capabilities, CROs are integrating cloud based analytics and model libraries to shorten turnaround times and support compliance in the AI in predictive toxicology market.

By Technology: Machine Learning Dominates, NLP Expands for Mechanistic Clarity

Machine Learning captured 50.35% of the AI in predictive toxicology market share in 2025 as random forests, gradient boosting, and graph based methods remained the workhorses for regulatory grade classification and endpoint coverage. Expert rule and statistical models combine to deliver mechanistic justification and robust accuracy for genotoxicity calls that align with guidance on validation and applicability domains. Multi endpoint ADMET platforms integrate hERG and cardiotoxicity features with uncertainty estimates and alerts, which support early risk communication in chemistry decisions. Open QSAR libraries provide endocrine, acute toxicity, and key PK property predictions with transparent documentation, which encourages consistent and auditable deployment in workflow automation. Model informed submissions leverage PBPK with expanding transporter and biopharmaceutics capabilities, which shortens the time from analysis to decision in regulatory files.

Natural Language Processing is forecast to grow at 22.24% CAGR to 2031 as knowledge graphs and biomedical text mining enrich mechanism discovery, link assays to biological pathways, and enable conversational explainability across model outputs. Enterprise knowledge graphs that integrate dozens of biomedical sources are expanding signal detection and hypothesis generation, which accelerates target discovery and indication expansion. NLP enabled triage and report generation are also improving developer workflows by reducing manual synthesis of model rationales and supporting consistent documentation. These advances help teams connect predictive outputs with mechanistic narratives, which supports reviewer understanding and cross functional decision making in the AI in predictive toxicology market.

By Toxicity Endpoint: Genotoxicity Anchors Market, Carcinogenicity Surges with EPA Mapping

Genotoxicity/mutagenicity held 42.39% of 2025 endpoint revenue, supported by ICH M7 acceptance of QSAR based evidence when supported with transparent algorithms, validation, and applicability domains. Expert guidance from national committees emphasizes combining knowledge based systems with statistical models, which improves confidence in final calls and supports fit for purpose submissions. Carcinogenicity is projected to grow at 23.56% CAGR as public high throughput data expand coverage of key biological characteristics that inform hazard mapping and prioritization. CiPA aligned cardiac safety models and GNN based hERG tools further refine compound triage by quantifying proarrhythmia and channel blockade risks with high AUROC performance. Broad ADMET toolkits add robust hERG classification with uncertainty quantification that assists in ranking and documentation. Advancing endpoint modules for hepatotoxicity, supported by dedicated DILI predictors, provide additional momentum to scale model informed safety assessment across the AI in predictive toxicology market.

By Deployment: Cloud/SaaS Leads with Regulatory Integration, On Premise Persists for IP Control

Cloud/SaaS captured 50.27% share of the AI in predictive toxicology market in 2025 and is on track for 21.36% CAGR as teams consolidate PBPK, QSP, and safety analytics in secure environments with automated documentation and AI enabled guidance. Recent platform updates introduced EMA qualified PBPK capabilities and expanded transporter mediated DDI features, which improve confidence for regulatory submissions. Cloud native reporting with generative assistance shortens write ups and standardizes technical narratives for internal and external stakeholders. AI driven discovery platforms trained on proprietary assay databases are being delivered through flexible deployment models to meet enterprise data governance needs. Sponsors continue to prefer hybrid architectures that preserve sensitive IP on premise while leveraging elastic compute for model training and simulation scale out in the AI in predictive toxicology market.

On premise deployments remain important for organizations with strict data sovereignty and integration requirements that connect safety models with LIMS, ELNs, and discovery informatics. In these settings, expert review workflows and curated knowledge bases integrate with statistical QSAR and ML modules to support internal policies and audit trails. Vendors continue to support both deployment modes so sponsors can manage infrastructure choices while keeping a common model library and validation framework. As cross functional model usage rises, role based access, version control, and validation documentation become central to scaling model informed decisions across sites in the AI in predictive toxicology market. The net effect is a steady migration to cloud for collaboration and compute heavy steps with a durable on premise footprint for sensitive datasets and regulated workflows.

Geography Analysis

North America accounted for 48.67% of the AI in predictive toxicology market size in 2025 as the FDA roadmap shifted the center of gravity toward NAM adoption and model informed planning across preclinical programs. The region’s policy signals and pilot qualifications support stepwise validation and model credibility frameworks that foster investment in in silico tools. Public funding for model based cardiac and liver safety is expanding infrastructure and datasets through consortium awards and collaborative development programs. Government portfolios also advance high throughput genetic toxicology capabilities that can be leveraged by ML pipelines to augment classification performance and mechanistic inference in the AI in predictive toxicology market. These elements combine with cloud PBPK platforms licensed by multiple agencies to streamline model development and submission ready reporting.

Europe held a significant share in 2025 and continues to emphasize standardized QSAR reporting, expert review of out of domain predictions, and knowledge based justification as part of case specific assessments. Collaborative initiatives on read across and mechanistic frameworks in the literature support convergence across agencies and help developers prepare more transparent dossiers. Northern European regulators also leverage regional QSAR databases in plant protection assessments, which reinforces the practical value of shared tools and harmonized practices. Pre competitive databases and tooling from companies headquartered in the region help reduce duplication and enable consistent re use of curated results across programs in the AI in predictive toxicology market. Expanded access to open QSAR suites across European labs complements this foundation and continues to broaden standard practice.

Asia Pacific is the fastest growing region through 2031 with a 24.33% CAGR as sponsors and CROs increase adoption of model informed approaches and cloud based analytics for safety triage and study design. Laboratories in the region continue to integrate public high throughput datasets and open QSAR tools that support scalable ML pipelines for screening and prioritization. Growth in AI enabled design and simulation platforms also supports distributed collaboration across discovery and preclinical workflows within the AI in predictive toxicology market. As regional R&D footprints expand, hybrid deployment models help maintain data sovereignty while accessing elastic compute for training and scenario analysis. Over the forecast period, the combination of public datasets, vendor platform maturity, and regional capacity building will continue to underpin strong adoption curves across Asia Pacific.

Competitive Landscape

The AI in predictive toxicology market is characterized by a diverse vendor set that includes safety software specialists, translational platform providers, and CROs with integrated AI offerings. Platform roadmaps show steady expansion in PBPK features, transporter coverage, and AI assisted workflows that support faster scenario testing and standardized documentation. Vendors are also embedding generative assistance for PK report drafting, which reduces manual effort and enhances consistency in narrative outputs. Knowledge graph platforms continue to grow data coverage and relationship density, which improves target discovery and mechanistic explanations that translate into safety hypotheses in the AI in predictive toxicology market.

CROs are differentiating through proprietary datasets and AI driven discovery environments that raise baseline ADMET accuracy and provide scalable service capacity for sponsors. Partnerships between AI platform companies and large pharmas demonstrate continued appetite for multimodal approaches that can tie discovery insights to downstream safety indicators. Academic industry consortia are also receiving awards to build new toxicity models, which bring additional data assets and method validation to the ecosystem. These moves expand capacity, data breadth, and service coverage while creating positive feedback loops for performance and trust in the AI in predictive toxicology market.

Scientific advances in CiPA aligned modeling and GNN based hERG classification are improving interpretability and quantifying uncertainty, which reduces risk of false negatives and supports earlier chemistry decisions. Open QSAR suites and standardized reporting formats provide shared baselines for training and evaluation, which accelerates deployment and auditability across sponsors and CROs. As vendors compete on data assets, explainability, and regulatory alignment, the overall trajectory continues to favor platforms that combine transparent documentation with strong endpoint coverage in the AI in predictive toxicology market.

AI In Predictive Toxicology Industry Leaders

Lhasa Limited

Instem (Leadscope)

Simulations Plus

Dassault Systèmes

ACD/Labs

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Simulations Plus announced collaboration with Lonza and U.S. FDA to develop mechanistic predictive frameworks for amorphous solid dispersion drug products, integrating advanced in vitro dissolution systems with PBBM using DDDPlus and GastroPlus platforms. This aims to improve early risk identification, strengthen regulatory confidence, and expand AI-enabled workflows connecting data to decision-making.

- April 2026: DeepCyte launched with $1.5 million seed funding, introducing the MetaCore single-cell metabolomics platform, achieving 94% accuracy across 17 detailed toxicity mechanisms, and the DeeImmuno AI solution trained on proprietary single-cell metabolomics atlases for biomarker identification. This addresses drug-toxicity challenges causing billions in annual losses from clinical-trial failures and post-market withdrawals.

- March 2026: Certara released Simcyp Simulator Version 25, the first EMA-qualified PBPK platform, expanding transporter-mediated DDI modeling, enhancing biopharmaceutics capabilities for enabling formulations, and integrating AI-enabled chat support. This update contributed to over 120 FDA-approved novel drugs and supports clinical trial waivers in DDI and pediatric trials.

Global AI In Predictive Toxicology Market Report Scope

According to the report’s scope, AI in predictive toxicology refers to the use of machine‑learning models and advanced algorithms to analyze chemical, biological, and experimental data to forecast the potential toxicity of drugs, compounds, and environmental substances. It accelerates early‑stage risk assessment, reduces reliance on animal testing, and supports more accurate, data‑driven safety evaluations across research and regulatory settings.

The AI in predictive toxicology market is segmented into application, end-user, technology, toxicity endpoint, deployment, and geography. By application, the market is segmented into early discovery triage & design, preclinical safety assessment, regulatory compliance dossiers, consumer products & cosmetics safety, and others. By end-user, the market is segmented into Pharmaceutical & biotechnology companies, contract research organizations (CROs) & consultancies, cosmetics & personal care, and others. By technology, the market is segmented into machine learning, natural language processing, and others. By toxicity endpoint, the market is segmented into genotoxicity/mutagenicity, carcinogenicity, cardiotoxicity, dermal sensitization & irritation, neurotoxicity, and others. By deployment, the market is segmented into cloud / SaaS and on-premise. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Early Discovery Triage and Design |

| Preclinical Safety Assessment |

| Regulatory Compliance Dossiers |

| Consumer Products and Cosmetics Safety |

| Others |

| Pharmaceutical and Biotechnology Companies |

| Contract Research Organizations (CROs) and Consultancies |

| Cosmetics and Personal Care |

| Others |

| Machine Learning |

| Natural Language Processing |

| Others |

| Genotoxicity / Mutagenicity |

| Carcinogenicity |

| Cardiotoxicity |

| Dermal Sensitization and Irritation |

| Neurotoxicity |

| Others |

| Cloud / SaaS |

| On-Premise |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Early Discovery Triage and Design | |

| Preclinical Safety Assessment | ||

| Regulatory Compliance Dossiers | ||

| Consumer Products and Cosmetics Safety | ||

| Others | ||

| By End-user | Pharmaceutical and Biotechnology Companies | |

| Contract Research Organizations (CROs) and Consultancies | ||

| Cosmetics and Personal Care | ||

| Others | ||

| By Technology | Machine Learning | |

| Natural Language Processing | ||

| Others | ||

| By Toxicity Endpoint | Genotoxicity / Mutagenicity | |

| Carcinogenicity | ||

| Cardiotoxicity | ||

| Dermal Sensitization and Irritation | ||

| Neurotoxicity | ||

| Others | ||

| By Deployment | Cloud / SaaS | |

| On-Premise | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the AI in predictive toxicology market?

The AI in predictive toxicology market size is USD 0.95 billion in 2026 and is forecast to reach USD 2.41 billion by 2031 at 20.42% CAGR over 2026 2031.

Which segments lead growth and where are the fastest gains expected?

Early Discovery Triage & Design led 2025 revenue, while Preclinical Safety Assessment is projected to grow the fastest through 2031 as DILI and cardiac risk models compress timelines and support model informed study design.

Which technologies are most adopted across workflows today?

Machine Learning anchors adoption for classification and ADMET coverage, while NLP enabled knowledge graphs and generative report tools improve mechanistic context and documentation quality.

Where are regional opportunities strongest over the next five years?

North America holds the largest share given regulatory momentum and public awards, while Asia Pacific grows fastest as sponsors and CROs scale cloud PBPK, ML screening, and hybrid deployments.

Page last updated on: