AI In In-Silico Drug Development Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.05 Billion |

| Market Size (2031) | USD 15.31 Billion |

| Growth Rate (2026 - 2031) | 30.50% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

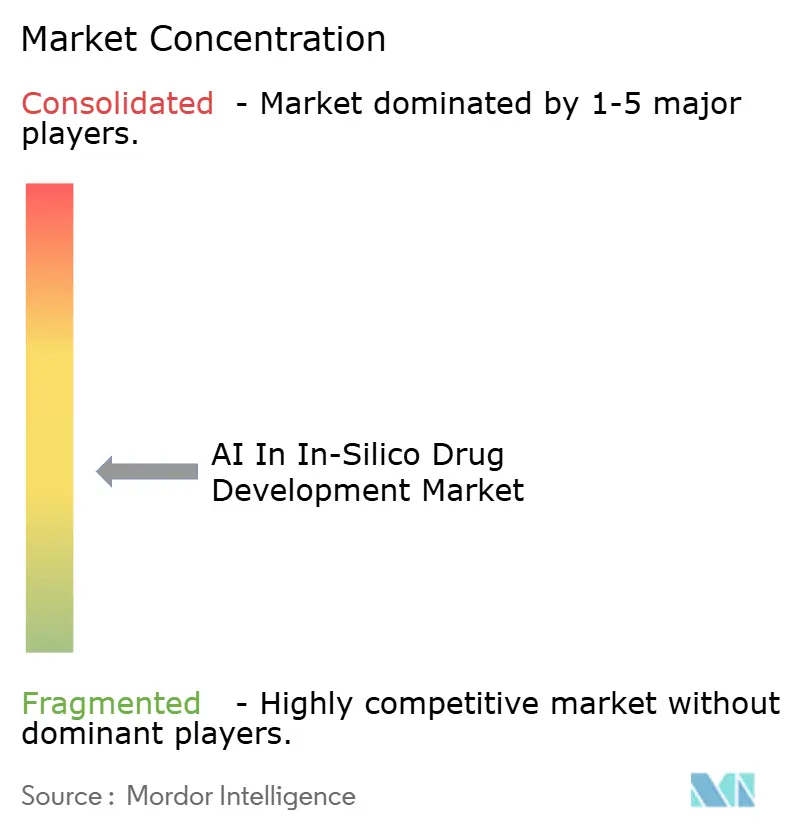

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In In-Silico Drug Development Market Analysis by Mordor Intelligence

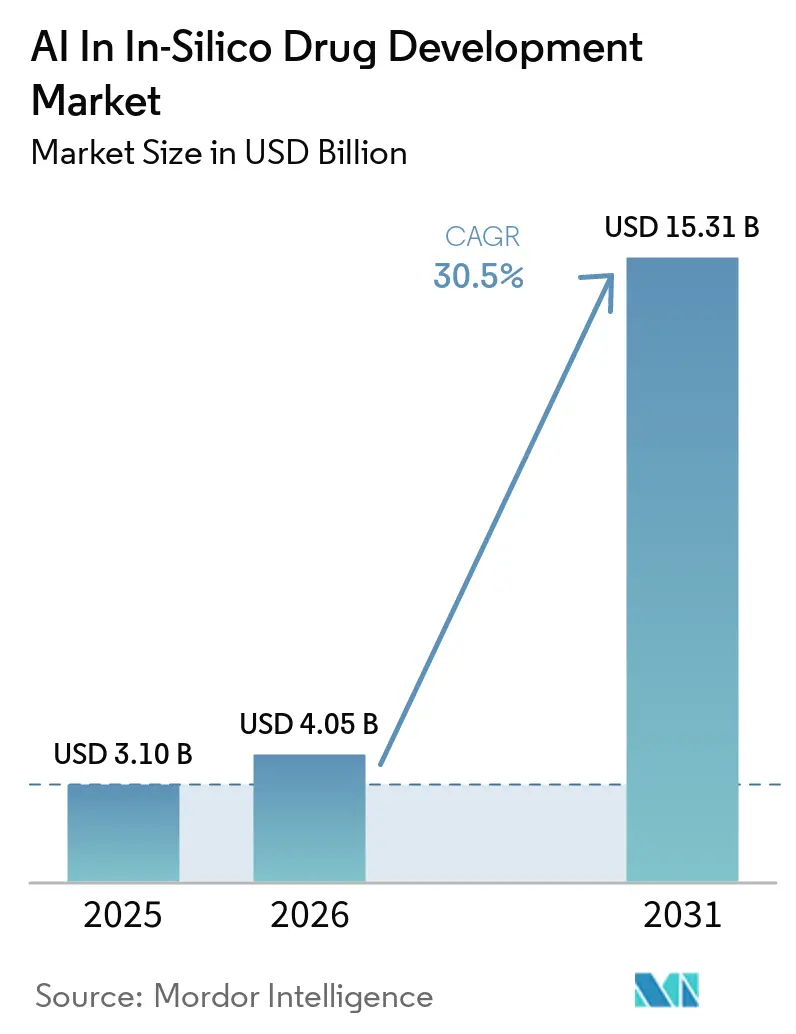

The AI In In-Silico Drug Development Market size is expected to increase from USD 3.10 billion in 2025 to USD 4.05 billion in 2026 and reach USD 15.31 billion by 2031, growing at a CAGR of 30.5% over 2026-2031.

Pharmaceutical giants are increasingly adopting model-driven portfolio governance. Johnson & Johnson, Pfizer, and Moderna have reported that AI now screens lead compounds in about half the time it previously took. As of early 2026, over 170 AI-discovered candidates are undergoing human testing, indicating a significant shift from traditional empirical screening to a more predictive design approach.

Leading platform suppliers are rapidly expanding. NVIDIA’s BioNeMo framework delivers model training that is twice as fast and inference that is six times quicker on H100 GPUs. This framework is already a key player in several top-10 pharmaceutical pipelines. Contract research organizations (CROs) like Charles River’s Logica and Atinary’s SDLabs have established comprehensive design-make-test-analyze (DMTA) loops, enhancing their outsourcing capabilities. Meanwhile, regulators are experimenting with real-time cloud data feeds to expedite their review processes. These synergistic developments highlight a robust growth trajectory for AI in the in-silico drug development arena.

Key Report Takeaways

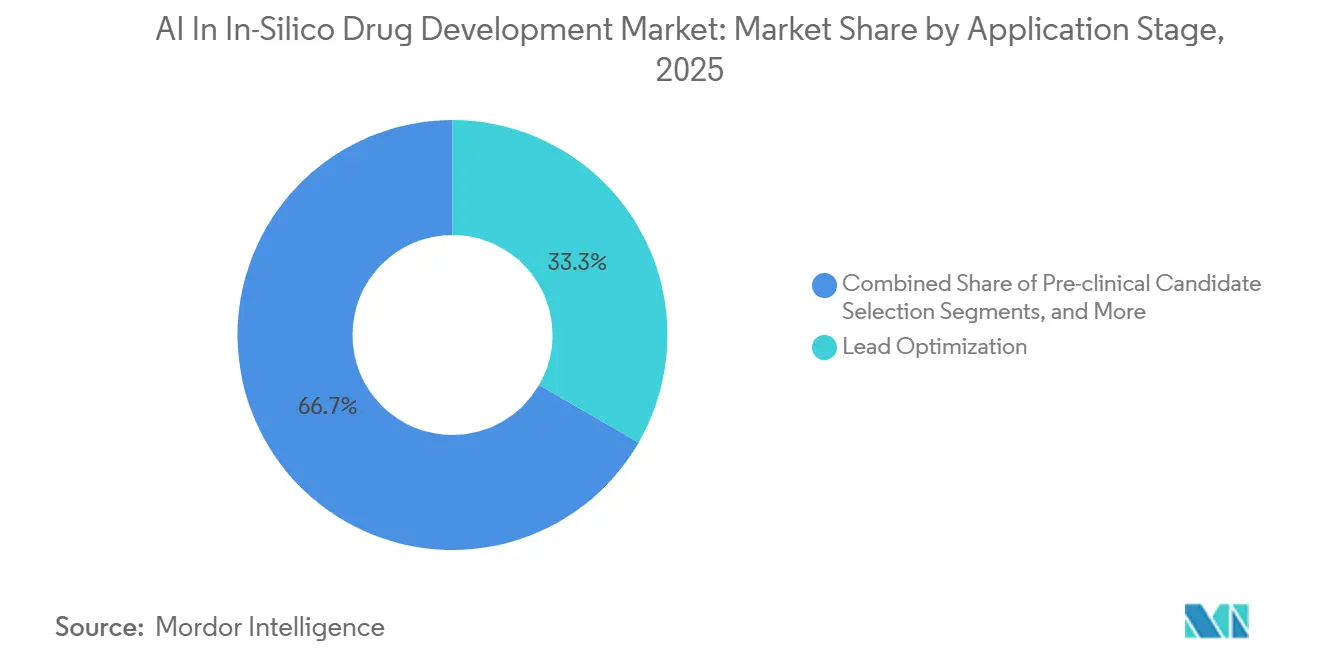

- By application, lead optimization led with 33.33% of AI in in-silico drug development market share in 2025, while pre-clinical candidate selection is forecasted to expand at a 33.30% CAGR through 2031.

- By AI technology, machine learning led with 46.45% of AI in in-silico drug development market share in 2025, while reinforcement learning is forecasted to expand at a 32.16% CAGR through 2031.

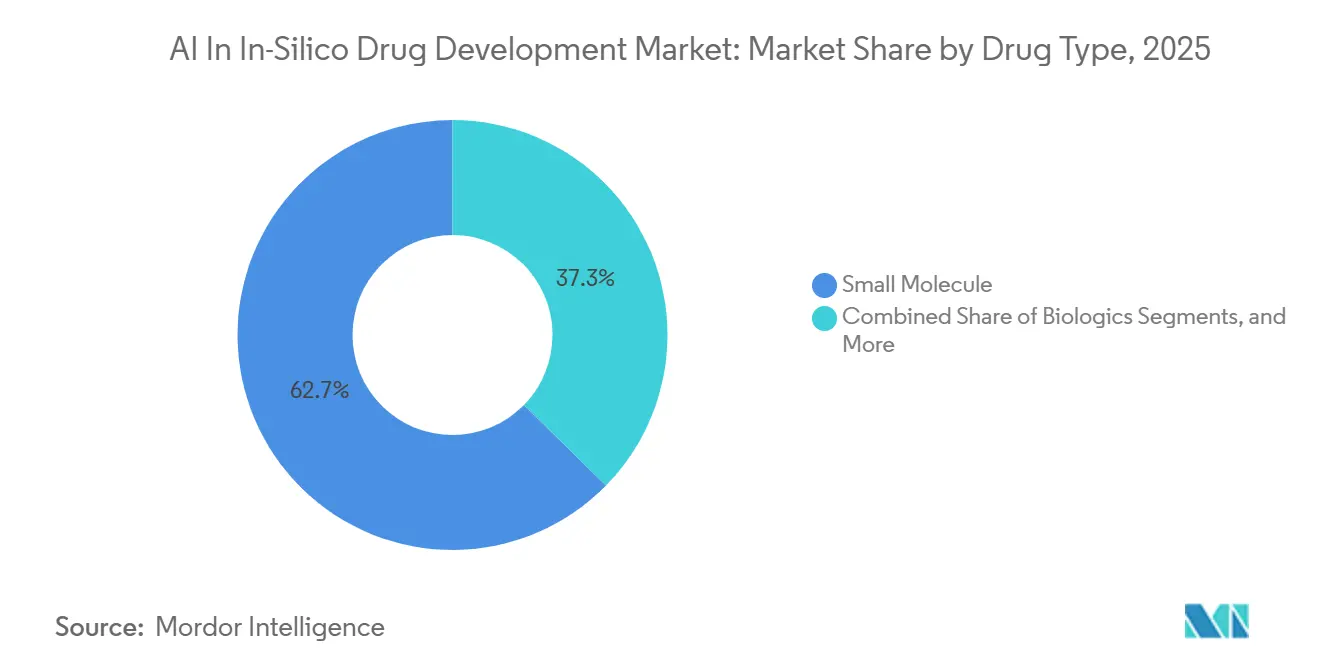

- By drug type, small molecules commanded 62.66% of AI in in-silico drug development market size in 2025, yet biologics are forecasted at a 33.45% CAGR to 2031.

- By therapeutic area, oncology accounted for 38.75% of spending in 2025, whereas infectious-disease programs are projected to grow fastest at a 33.65% CAGR over 2026-2031.

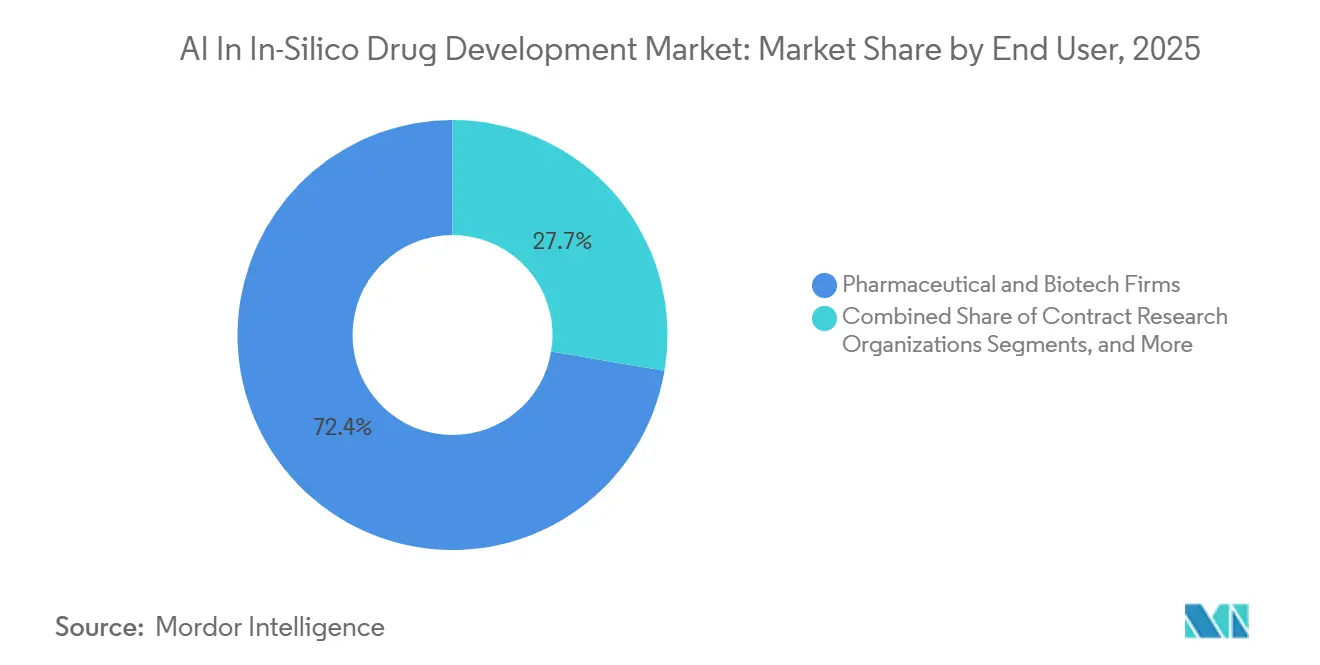

- By end user, pharmaceutical and biotech firms held 72.35% of market share in 2025, while CROs are expected to grow at a 34.25% CAGR over the forecast period.

- By deployment mode, cloud platforms captured 63.75% of revenue in 2025 and are expected to post the highest 34.75% CAGR out to 2031.

- By geography, North America captured 40.95% of revenue in 2025, and Asia-Pacific is expected to post the highest 33.98% CAGR out to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In In-Silico Drug Development Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surging cloud-native high-performance computing access | +4.8% | Global, early adoption in North America, EU, China | Medium term (2-4 years) |

| Pharma shift to fail-fast AI-assisted target validation | +5.2% | North America and EU; APAC following | Short term (≤ 2 years) |

| Growing venture and corporate funding for AI-first biotech | +3.9% | North America dominant; China accelerating | Short term (≤ 2 years) |

| Regulatory pilot programs for algorithm-derived submissions | +2.4% | U.S.-led; EU alignment via EMA | Long term (≥ 4 years) |

| Quantum-inspired AI accelerators reaching commercial maturity | +1.3% | U.S., Taiwan, EU semiconductor hubs | Long term (≥ 4 years) |

| Data-Centric Foundation Models Enabling Zero-Shot Target Prediction | +5.2% | North America and EU; APAC following | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cloud-Native High-Performance Computing Gains Traction

Widespread access to elastic GPU clusters is reducing the financial barriers to AI research. NVIDIA’s BioNeMo, operational at several pharmaceutical firms, cuts training latency for extensive protein language models by half and increases inference speed six-fold. Meanwhile, Denmark’s Gefion supercomputer enabled Orbis Medicines to analyze 140 billion macrocycles in just a few days. The shift to on-demand infrastructure transforms fixed capital expenses into flexible costs, allowing mid-tier biotech firms to conduct billion-molecule virtual screenings, a capability previously limited to the top 10 pharmaceutical companies five years ago. The FDA’s pilot program, set for April 2026, is now utilizing real-time cloud data from AstraZeneca and Amgen trials, streamlining administrative processes by 20 to 40 percent.[1]Cohrs Zhang, “FDA to Accelerate Drug Trials Using Real-Time Data and AI Tools,” Bloomberg, bloomberg.com This combination of cost-effective computing and regulatory support is driving sustained growth in the AI in in-silico drug development market.

Pharmaceuticals Embrace AI for Swift Target Validation

Data-driven validation methods are shifting attrition to the earliest stages. Valo Health’s Opal platform, which leverages 17 million de-identified patient records, is prioritizing genetically-backed programs. The company has expanded its partnership with Novo Nordisk to include 20 cardiometabolic targets, with a potential value of up to USD 4.6 billion. Recursion, using over a trillion induced pluripotent stem-cell images for phenotypic mapping, accelerated REC-4881's progression from target identification to Phase 1b-2 in under two years by streamlining SAR and toxicity evaluations.[2]Recursion Pharmaceuticals, “REC-1245 IND Filing Update,” recursion.comThese examples highlight how AI-driven strategies are transforming decision-making and timelines in the AI in in-silico drug development market.

Venture Capital and Corporations Rally Behind AI-Driven Biotechs

Investment momentum is favoring integrated platform companies. Biomedicines advanced its AI-designed anti-TSLP antibody (GB-0895) into global Phase 3 trials just four years after its design. In a significant move, Eli Lilly committed up to USD 2.75 billion for in-silico Medicine’s longevity pipeline in January 2026, marking the largest early-stage AI licensing agreement to date. Investors are increasingly demanding Phase 1 data within 30 months of target nomination, incentivizing platforms that integrate discovery and development processes.

Regulators Embrace Algorithmic Submissions

Regulatory bodies are taking on collaborative roles. In January 2025, the FDA introduced a risk-based model-validation framework in its AI guidance, noting over 500 AI components from previous submissions. The agency's 2026 cloud-data initiative supports ongoing safety assessments and aims to significantly reduce approval timelines. In 2025, EMA granted methodological qualification to AIM-NASH, and in January 2026, both the FDA and EMA established shared principles on validity, accountability, and clarity, reinforcing a global consensus on algorithmic evidence standards.[3]European Medicines Agency, “Qualification Opinion on AIM-NASH,” ema.europa.eu

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Sparse negative-result algorithm generalization | -3.2% | Global, acute in complex biologics and rare diseases | Medium term (2-4 years) |

| Unresolved IP ownership for co-designed molecules | -1.9% | U.S. and EU patent jurisdictions | Long term (≥ 4 years) |

| High switch-out costs from in-house CADD workflows | -2.8% | Large pharma in North America, EU, and Japan | Short term (≤ 2 years) |

| Regulatory Opacity on Explainability Thresholds for Generative Models | -1.9% | U.S. and EU patent jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Bias in Current Models Limits Performance on Underexplored Targets

Current models, influenced by publicly available positive data, face challenges in addressing underexplored targets. Approximately 90% of pre-clinical programs that fail are not included in shared repositories. This gap forces sponsors to repeatedly encounter the same challenges. In May 2025, Recursion discontinued REC-994 after Phase 2 signals proved insufficient, emphasizing the risks of relying on biased datasets. Establishing consortia to consolidate negative results may be crucial for improving transferability in the AI-driven in-silico drug development market.

Patent Law's Challenge with AI-Driven Molecular Design

Patent law requires a human inventor, yet generative systems can explore chemical spaces beyond human capabilities. The 2022 ruling reaffirmed that AI systems cannot hold inventorship rights. This has led to complex contractual solutions, such as those seen in the Recursion-Exscientia merger. However, these customized agreements are not scalable, creating uncertainties that slow down transactions, particularly in the U.S. and EU, which are key regions for AI-related patenting in the in-silico drug development sector.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Stage: Lead Optimization Dominates but Candidate Selection Rises

In 2025, lead optimization accounted for 33.33% of the AI-driven in-silico drug development market, highlighting the immediate advantages of AI-enhanced SAR and multiparameter optimization. For several oncology programs, fragment-based suites have significantly reduced synthesis iterations from over twenty to just a few. This segment's depth not only increases the market size but also drives higher investments in potency and selectivity by sponsors. Meanwhile, pre-clinical candidate selection is advancing rapidly, with a 33.30% CAGR, and is expected to narrow the gap by 2031. Integrated platforms are streamlining processes by combining design, ADME-Tox prediction, and manufacturability assessments into a continuous loop, accelerating IND filings.

By AI Technology: Machine Learning Holds the Moat, Reinforcement Learning Scales Quickly

In 2025, machine learning captured 46.45% of the revenue due to its mature supervised models, knowledge graphs, and gradient-boosting ensembles that seamlessly integrate into discovery workflows. Physics-augmented neural networks and graph embeddings exemplify the production readiness of this technology. The market's reliance on machine learning is further supported by proprietary historical SAR and crystallography data, which are challenging for new entrants to replicate.

Reinforcement learning is gaining traction with a 32.16% CAGR, as autonomous exploration bridges the gap between design and assay. Transformer engines have improved structure prediction coverage to 76% of the human proteome. Large language models have surpassed benchmarks in numerous therapeutic tasks. As closed-loop robotics becomes standard, reinforcement-learning agents are evolving from move-suggestion to real-time hypothesis generation and laboratory execution, enhancing the long-term market potential of this technology.

By Drug Type: Small Molecules Prevail, Biologics Accelerate

Small molecules retained a dominant 62.66% share, driven by established synthesis workflows, extensive chemical libraries, and decades of ADMET data. AI platforms efficiently optimize lipophilicity, solubility, and permeability, delivering measurable returns. Examples include small-molecule pipelines, inhibitors, and other advancements that have reduced hit-to-lead cycles to 12-18 months, compared to the previous 3-4 years. These productivity improvements reinforce the central role of small molecules in the AI-driven in-silico drug development market.

Biologics, however, are projected to grow at a 33.45% CAGR. Generative models are now achieving antibody hit rates of 16-20%, a significant improvement over the 0.1% achieved through traditional empirical discovery. Advances in protein structure prediction have reduced the "dark proteome," exposing new epitopes for AI-enabled biologic design.

By Therapeutic Area: Oncology Leads, Infectious Diseases Expand Fastest

Oncology accounted for 38.75% of expenditures in 2025, benefiting from decades of multi-omics data, biomarker-guided trial designs, and addressing significant unmet needs. AI systems integrate spatial transcriptomics, single-cell sequencing, and longitudinal imaging to optimize drug design and patient selection. Federated models are now operational, ensuring compliance with data protection regulations while providing real-time recommendations for clinical trial enrollment.

Infectious-disease programs are growing at a 33.65% CAGR, supported by open-access mandates and increased funding for antimicrobial resistance. New AI platforms are democratizing access by offering end-to-end design services for diseases like malaria and tuberculosis. As generative design becomes more widely adopted in neglected tropical disease pipelines, this segment is positioned for accelerated revenue growth, outpacing other therapeutic areas.

By End User: Pharma Vertical Integration Dominates, CROs Scale Rapidly

Pharmaceutical and biotech companies captured 72.35% of 2025 revenue by internalizing AI to maintain a competitive edge. These organizations have reported significant timeline reductions after embedding AI and robotics into discovery and development processes. Such advancements highlight why the AI-driven in-silico drug development market remains concentrated within sponsor organizations.

Contract research organizations (CROs) are expected to grow at a 34.25% CAGR. The surge in AI-generated leads has exceeded internal chemistry capacities, prompting sponsors to outsource DMTA loops. CROs have demonstrated scalability, achieving high success rates for advanceable leads and significantly reducing optimization timelines.

By Deployment Mode: Cloud Platforms Win on Elastic Economics

In 2025, cloud deployments accounted for 63.75% of the AI-driven in-silico drug development market and are projected to grow at a 34.75% CAGR. Cloud providers are enabling instant access to advanced computing resources, bypassing traditional procurement delays associated with on-premise clusters. Hybrid models, combining private supercomputers for baseline tasks with cloud resources for peak demands, are gaining popularity. As regulatory acceptance of cloud-generated data increases, barriers to adoption are diminishing, further driving market growth tied to SaaS delivery.

Geography Analysis

In 2025, North America accounted for 40.25% of the revenue, leveraging FDA guidance, Silicon Valley's hardware ecosystems, and discovery clusters in Boston and Salt Lake City. Venture funding remained concentrated, with significant follow-on rounds raised by key players. The region's policy clarity, including FDA's real-time trial monitoring and draft AI guidance, continues to attract global partnerships, reinforcing North America's central role in the AI in in-silico drug development market.

Europe maintained a mid-20% share, supported by stringent regulatory oversight and collaborative public-private federated-data initiatives. The EMA's AIM-NASH qualification and the anticipated EU AI Act provide clear yet demanding pathways for algorithmic submissions. Initiatives such as a safeguarded AI fund and GDPR-compliant hospital partnerships highlight efforts to integrate AI into healthcare while maintaining data privacy standards.

Asia-Pacific is expected to grow at the fastest rate, with a projected CAGR of 33.98% through 2031. China's Digital and Intelligent Transformation Plan, supported by state credits and provincial subsidies, aims to establish 100 digital drug factories and 10 large-model platforms by 2027. Japan's aging population drives a need for increased productivity, prompting investments from major companies. In India, the adoption of a cloud-native multiparameter-optimization platform is enabling a shift from generics to innovation, further expanding the regional AI in in-silico drug development market.

Competitive Landscape

The AI in in-silico drug development market remains moderately fragmented, with no player exceeding 15% share. Recursion Pharmaceuticals, following its 2024 merger with Exscientia, exemplifies the vertical-integrator model by combining 65 petabytes of proprietary phenotypic data, automated chemistry, and AI-enabled clinical-trial optimization. NVIDIA, Google DeepMind, and Microsoft supply enabling infrastructure, giving rise to a horizontal layer of platform vendors.

White-space opportunities persist in peptide and oligonucleotide discovery, where hit rates remain low despite strong therapeutic promise. Latent Labs and Genesis Therapeutics focus on macrocycles and peptide design, while incumbents like Schrödinger and BenevolentAI have limited exposure, setting the stage for specialized partnerships or acquisitions. Quantum computing represents a strategic tail risk; turnkey quantum drug-design platforms could leapfrog GPU-based models late in the decade, potentially redrawing competitive boundaries across the AI in in-silico drug development industry.

AI In In-Silico Drug Development Industry Leaders

BenevolentAI

BioAge Labs

Exscientia plc

Insilico Medicine

Schrödinger

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Eli Lilly and Insilico Medicine signed a licensing deal worth up to USD 2.75 billion for AI-discovered longevity targets, the largest early-stage AI agreement to date.

- December 2025: Generate:Biomedicines started global Phase 3 trials for GB-0895, an AI-designed long-acting anti-TSLP antibody spanning over 40 countries.

- December 2025: Beijing’s GHDDI launched AI Kongming, China’s first end-to-end AI drug-design platform covering target analysis through druggability optimization.

- May 2025: Insilico opened a UAE pilot to compress oncology discovery cycles from years to months using generative AI.

Global AI In In-Silico Drug Development Market Report Scope

As per the scope of the report, AI in in-silico drug development refers to the use of artificial intelligence, machine learning, and advanced algorithms to simulate, predict, and optimize the discovery of new medicine within a computer-based ("in-silico") environment.

The AI in in-silico drug development market is segmented by application stage, AI technology, drug type, therapeutic area, end-user, and deployment mode. By application stage, the market includes target identification, hit discovery, lead optimization, and pre-clinical candidate selection. By AI technology, the market is segmented into machine learning, deep learning, natural language processing, reinforcement learning, and other AI methods. By drug type, the market is categorized into small molecules, biologics, and other types. By therapeutic area, the market is segmented into oncology, neurology, infectious diseases, cardiovascular, metabolic disorders, and other therapeutic areas. By end-user, the market is segmented into pharmaceutical & biotech firms, contract research organizations, and academic & research institutes. By deployment mode, the market is segmented into cloud-based platforms and on-premise solutions. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Target Identification |

| Hit Discovery |

| Lead Optimization |

| Pre-clinical Candidate Selection |

| Machine Learning |

| Deep Learning |

| Natural Language Processing |

| Reinforcement Learning |

| Other AI Methods |

| Small Molecule |

| Biologics |

| Other Types |

| Oncology |

| Neurology |

| Infectious Diseases |

| Cardiovascular |

| Metabolic Disorders |

| Other Therapeutic Areas |

| Pharmaceutical & Biotech Firms |

| Contract Research Organizations |

| Academic & Research Institutes |

| Cloud-Based Platforms |

| On-Premise Solutions |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application Stage | Target Identification | |

| Hit Discovery | ||

| Lead Optimization | ||

| Pre-clinical Candidate Selection | ||

| By AI Technology | Machine Learning | |

| Deep Learning | ||

| Natural Language Processing | ||

| Reinforcement Learning | ||

| Other AI Methods | ||

| By Drug Type | Small Molecule | |

| Biologics | ||

| Other Types | ||

| By Therapeutic Area | Oncology | |

| Neurology | ||

| Infectious Diseases | ||

| Cardiovascular | ||

| Metabolic Disorders | ||

| Other Therapeutic Areas | ||

| By End User | Pharmaceutical & Biotech Firms | |

| Contract Research Organizations | ||

| Academic & Research Institutes | ||

| By Deployment Mode | Cloud-Based Platforms | |

| On-Premise Solutions | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the AI in insilico drug development market today?

The market was valued at USD 4.05 billion in 2026 and is forecast to reach USD 15.31 billion by 2031, expanding at a 30.5% CAGR.

Which AI technology currently leads commercial adoption?

Traditional machine-learning models account for 46.45% of 2025 revenue thanks to deep historical SAR and crystallography datasets.

What therapeutic area attracts the most spending?

Oncology commands 38.75% of global outlays because multi-omics datasets and biomarker-driven trial designs align well with AI-enabled discovery.

Why are CROs gaining traction in this space?

Sponsors increasingly outsource design-make-test-analyze cycles to CROs such as Charles River's Logica to manage the surge of AI-generated candidates, driving a 34.25% CAGR for the segment.

Which region is expected to grow fastest?

Asia-Pacific is projected to record a 33.98% CAGR through 2031, led by China's industrial policy and Japan's productivity initiatives.

Page last updated on: