Agentic AI In HR Workflows Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.63 Billion |

| Market Size (2031) | USD 9.80 Billion |

| Growth Rate (2026 - 2031) | 21.97% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

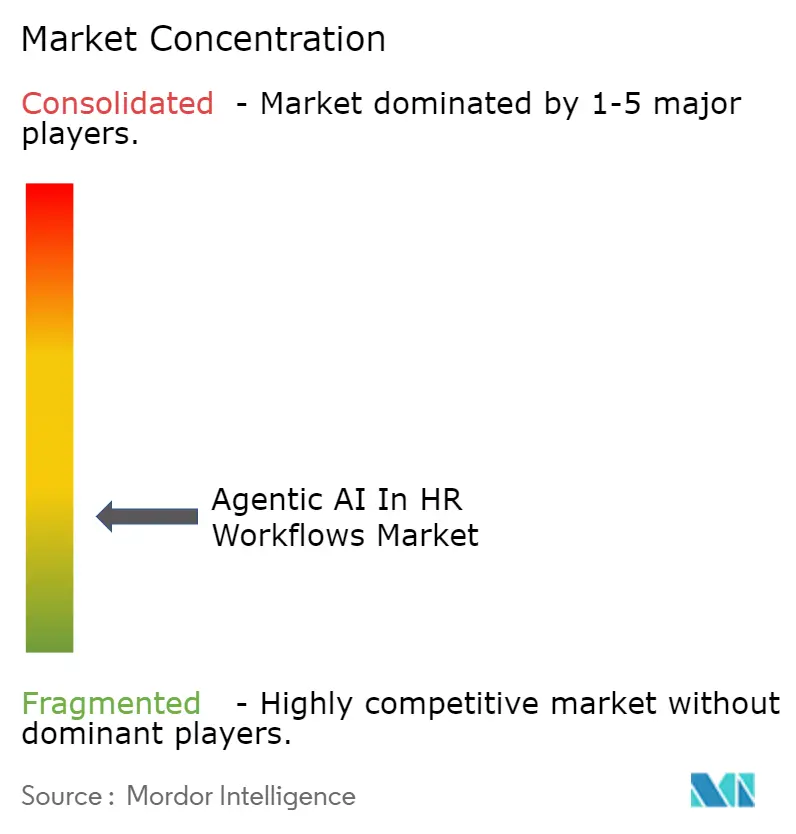

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agentic AI In HR Workflows Market Analysis by Mordor Intelligence

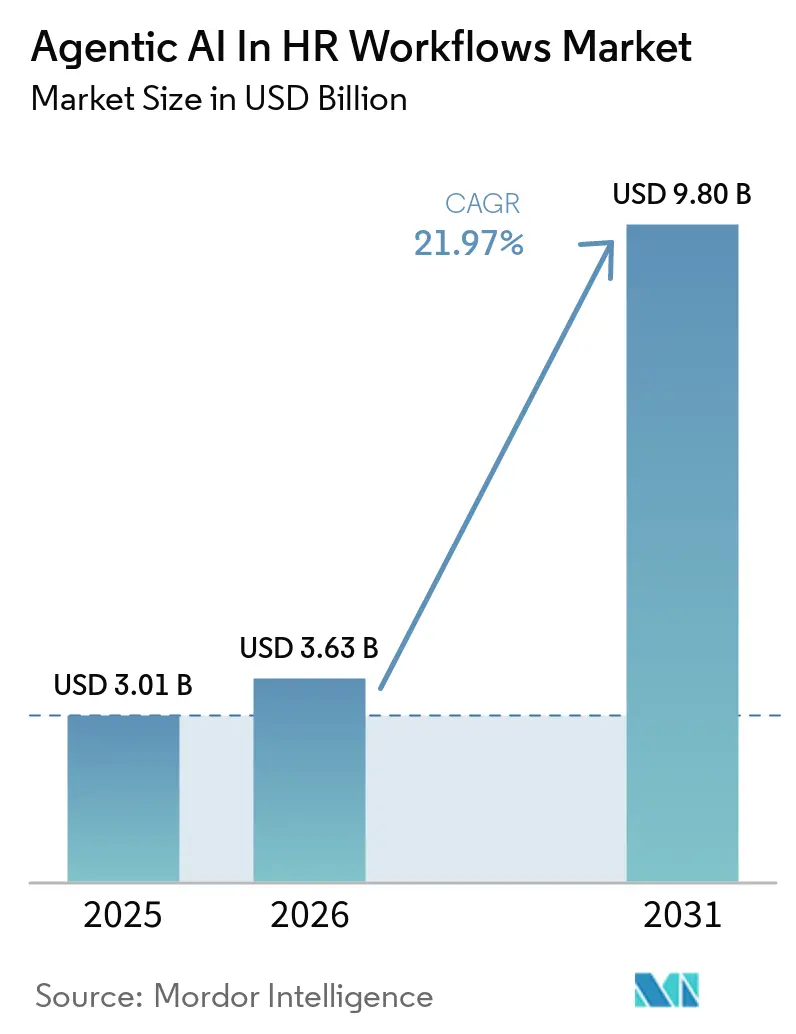

The agentic AI in HR workflows market size is expected to grow from USD 3.01 billion in 2025 to USD 3.63 billion in 2026 and is forecast to reach USD 9.80 billion by 2031 at 21.97% CAGR over 2026-2031. The expansion reflects a clear shift in enterprise HR delivery, where organizations are moving beyond rule-based automation toward systems that can reason, plan, and complete multi-step HR work with less continuous human input. Structural headcount limits within HR teams are reinforcing that shift, even as service expectations are rising, even when teams are not expanding at the same pace. North America led demand in 2025, while Asia-Pacific is set to grow the fastest, and this regional pattern is shaping where vendors are concentrating product rollout and go-to-market activity. Cloud remained the leading deployment model, but hybrid adoption is rising quickly because regulated sectors still need tighter control over sensitive employee records. Competition is increasing across platforms, workflow tools, and services, while integration gaps and governance requirements continue to shape how quickly the agentic AI in HR workflows market can scale.

Key Report Takeaways

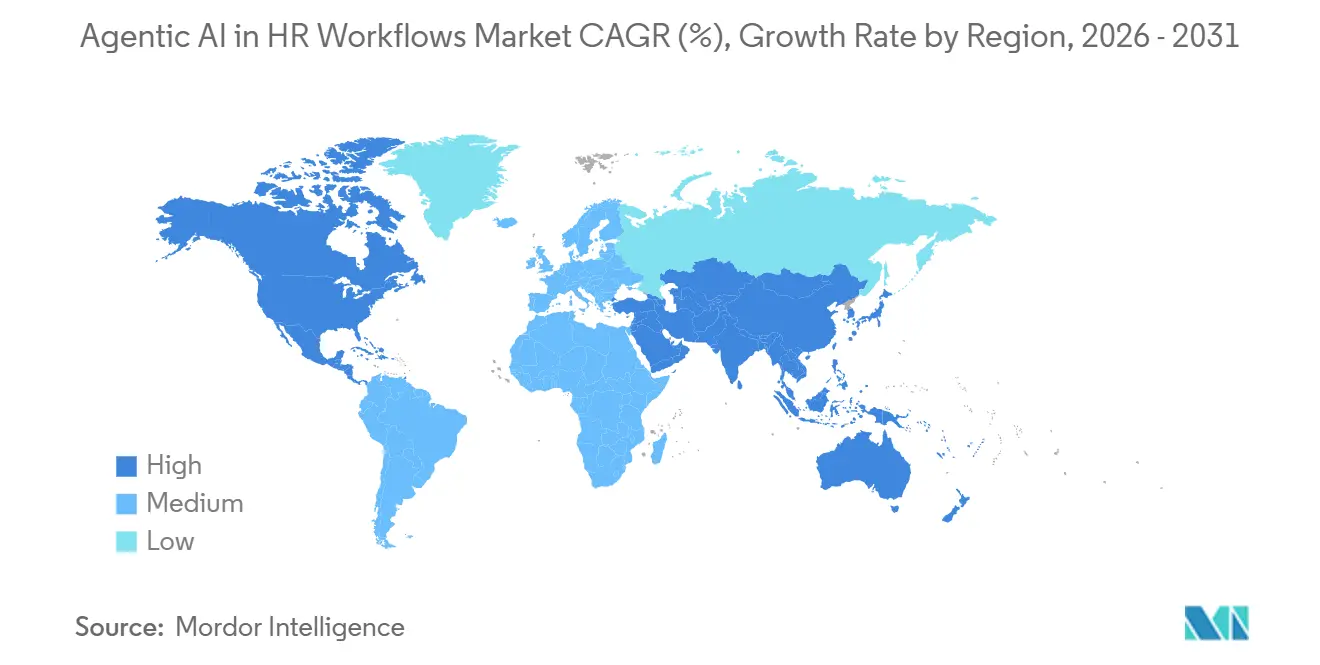

- By geography, North America held 39.66% of the agentic AI in HR workflows market share in 2025, while Asia-Pacific is projected to expand at a 28.47% CAGR through 2031.

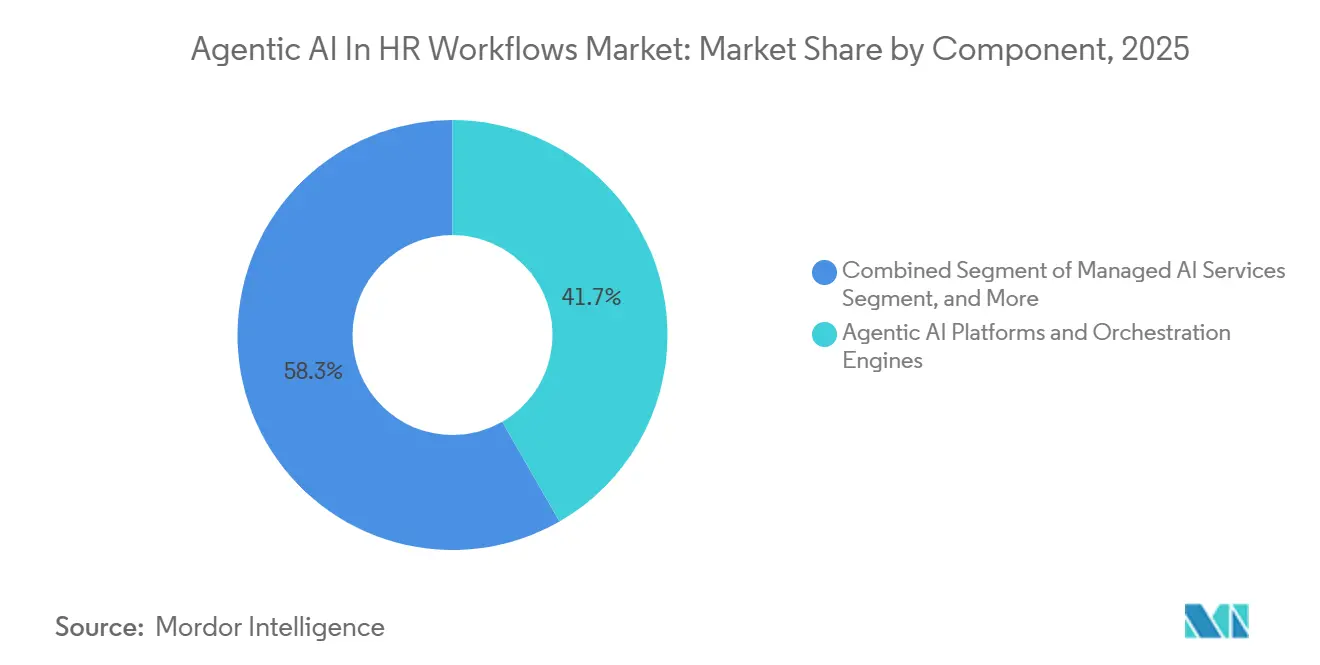

- By component, Agentic AI Platforms and Orchestration Engines led with 41.71% share in 2025, while Managed Agentic AI Services is projected to expand at a 24.36% CAGR through 2031.

- By function, Talent Acquisition and Recruiting Agents held 26.82% share in 2025, while HR Operations Automation Agents are expected to grow at a 27.14% CAGR through 2031.

- By deployment model, cloud-based deployment commanded 67.91% of 2025 revenue, while hybrid deployment is projected to grow at a 25.42% CAGR through 2031.

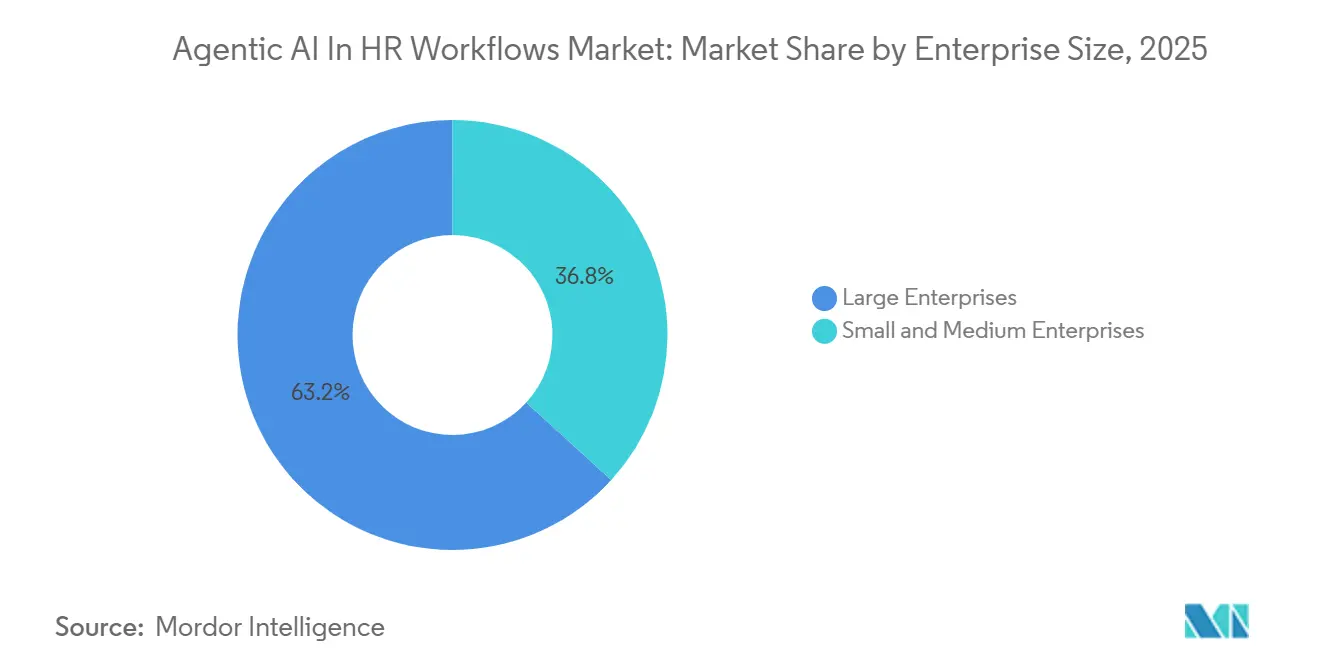

- By enterprise size, Large Enterprises accounted for 63.21% share of the agentic AI in HR workflows market in 2025, while SMEs are projected to advance at a 26.73% CAGR through 2031

- By end-user industry, Information Technology and Telecom retained the largest share at 29.41% in 2025, while Healthcare and Life Sciences are projected to expand at a 23.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agentic AI In HR Workflows Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Need for Autonomous HR Service Delivery | +5.2% | Global | Short term (≤ 2 years) |

| Growing Demand for Skills-Based Talent Decisions | +4.8% | Global, with early gains in North America and Asia-Pacific | Medium term (2-4 years) |

| Rising Pressure to Reduce HR Cycle Times Without Adding Headcount | +4.3% | Global | Short term (≤ 2 years) |

| Fragmented HR Tech Stacks Creating Orchestration Demand | +3.6% | North America and Europe | Medium term (2-4 years) |

| Expansion of Employee Self-Service Expectations Across the Workforce | +2.9% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Early Compliance by Design Advantage for Governance-Ready Vendors | +1.8% | Europe, with early gains in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Need For Autonomous HR Service Delivery

The productivity gap inside HR teams has become large enough that simple automation no longer solves it. Organizations still face rising case volumes, employee service expectations, and more compliance work, even when HR headcount stays tight. In the agentic AI in HR workflows market, which is pushing buyers toward systems that can take tier-1 requests from intake to resolution with less manual intervention. Autonomous service delivery also reduces the tendency to move sensitive requests into local spreadsheets or email threads when teams are overloaded. A 2026 executive survey found that 62% of C-suite leaders were dissatisfied with how people data connects to business performance, which supports demand for more governed HR workflows. That gap is helping the agentic AI in HR workflows market favor vendors that combine service automation with stronger visibility, controls, and data discipline.[1]SAP, “SAP SuccessFactors Innovations: New Era of Autonomous HCM,” SAP News Center, sap.com

Growing Demand For Skills-Based Talent Decisions

Skills-based talent decisions are moving from policy statements into day-to-day workflow design. LinkedIn's Economic Graph found that a skills-based approach expands the AI talent pipeline by 8.2 times globally for AI roles, a 34% improvement over non-AI roles. In the agentic AI in HR workflows market, this makes dynamic skills graphs and matching logic more valuable than static credential filters. When assessment results, internal mobility paths, and workforce planning signals feed the same environment, each new action improves future recommendations. This also increases demand for orchestration tools, as point solutions cannot keep skills data synchronized across recruiting, learning, and mobility tasks. A 2026 survey found that 87% of CHROs expected greater AI adoption in HR processes, up from 83% in 2025, underscoring stronger demand for systems that operationalize skills-based decisions at scale.[2]LinkedIn Economic Graph, “Skills-Based Hiring,” LinkedIn Economic Graph, linkedin.com

Rising Pressure To Reduce HR Cycle Times Without Adding Headcount

The pressure to reduce HR cycle times without adding staff remains a direct buying trigger across the agentic AI in HR workflows market. Buyers are prioritizing visible outcomes such as time-to-hire, faster response to employee requests, and lower manager effort on routine HR work. Once routine screening, scheduling, and employee support tasks move into agentic flows, HR teams can devote more time to exceptions and judgment-intensive cases. That shift changes vendor evaluation because buyers want clear workflow coverage, role-based controls, and easy handoffs back to humans when needed. Recent HR agent deployments reflect this preference for practical workflow execution over broad AI experimentation. As a result, the agentic AI in HR workflows market is rewarding vendors that can demonstrate operational relief in specific HR processes rather than only promising future productivity gains.[3]Society for Human Resource Management, “State of AI in HR 2026: Full Report,” SHRM, shrm.org

Fragmented HR Tech Stacks Creating Orchestration Demand

Fragmented HR technology stacks are creating lasting demand for orchestration layers across the agentic AI in HR workflows market. Many employers still run separate systems for core HR, recruiting, learning, performance, and payroll, which makes end-to-end automation difficult. Buyers, therefore, need a control layer that can connect permissions, trigger actions, and monitor outcomes across multiple systems. Workday's Agent System of Record shows that governance and registration are becoming core product requirements rather than optional features. Oracle's AI Agent Studio and Fusion agentic applications also point to coordinated execution across linked HR tasks rather than stand-alone copilots. This is why the agentic AI in HR workflows market continues to support infrastructure spending before broader application layer rollout.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Sensitivity to Hiring Bias, Privacy, and Audit Requirements | -2.8% | Global, particularly Europe | Short term (≤ 2 years) |

| Legacy HRIS and Payroll Integration Complexity | -2.4% | Global, highest in North America and Asia-Pacific | Medium term (2-4 years) |

| Human Oversight Requirements Limiting Full Autonomy in Critical Workflows | -1.9% | Global | Long term (≥ 4 years) |

| Low Process Standardization in Mid-Market Deployments | -1.4% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Sensitivity To Hiring Bias, Privacy, And Audit Requirements

Bias, privacy, and audit requirements remain the most persistent barriers to wider adoption of agentic AI in HR workflows. The EU AI Act classifies AI used in recruitment, performance evaluation, and workforce management as high-risk under Annex III, which raises the bar for documentation, testing, and oversight. That means vendors and buyers need clear records of data quality, model behavior, human oversight, and post-deployment monitoring before scaled use. The European Commission's 2026 implementation timeline provided additional time for compliance, but it did not eliminate the need to build those controls before the deadline. Fifty-seven percent of HR professionals in U.S. states with employment AI laws were unaware of those rules, and only 12% of aware organizations had compliant policies in place. This keeps the agentic AI in HR workflows market tilted toward vendors that can show audit trails and human override paths from the start.[4]European Parliament and Council of the European Union, “Regulation (EU) 2024/1689 Laying Down Harmonised Rules on Artificial Intelligence,” Official Journal of the European Union, eur-lex.europa.eu

Legacy HRIS And Payroll Integration Complexity

The complexity of legacy HRIS and payroll integration continues to slow implementation across the agentic AI in HR workflows market. Payroll-adjacent workflows cannot move into autonomous execution until employee records, approval rules, and policy data are consistent across systems. Older HR data models often vary by business unit, geography, or acquired entity, which forces schema mapping before agents can act reliably. This slows deployment even when the business case is clear, because technical cleanup must occur before process automation can scale. The burden is heavier in mid-market organizations that lack dedicated integration engineering teams or formal data governance programs. It also supports demand for managed deployment and phased rollout models inside the agentic AI in HR workflows market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platforms And Orchestration Engines Anchor Market Share

Agentic AI Platforms and Orchestration Engines accounted for 41.71% share of the agentic AI in HR workflows market size in 2025, giving the infrastructure layer the largest commercial position. Buyers are starting here because agent registration, permissions, observability, and workflow control must be in place before application agents can run across sensitive HR processes. This sequencing also limits governance risk because enterprises can set policies for how agents access records, trigger actions, and hand off exceptions before wider automation begins. More than 1,200 customers were registering and monitoring agents in early 2026, indicating that governance-first deployment is moving into production environments. Pre-built HR AI Agents and Workflow Applications are closely followed because they offer faster time-to-value for organizations that want visible use cases without a full orchestration buildout.

Managed Agentic AI Services is projected to expand at 24.36% CAGR through 2031, the fastest pace within the component mix. The agentic AI in HR workflows market is seeing stronger demand for these services because many buyers want outside support for configuration, monitoring, retraining, and policy management over time. This is especially relevant when HR teams lack deep internal AI operations talent or sufficient technical staff to maintain complex multi-agent workflows after launch. A 2026 roadmap featuring 15 new HR focused assistants within a broader release of 200 enterprise agents shows how vendors are packaging more managed, guided capabilities instead of leaving all deployment work to clients. Professional Services still matter because workflow redesign, change management, and governance setup remain necessary before autonomous execution can scale across the agentic AI in HR workflows market.

By Function: Talent Acquisition Leads, HR Operations Automation Gains Pace

Talent Acquisition and Recruiting Agents accounted for 26.82% of 2025 revenue, making hiring the largest functional segment in the agentic AI in HR workflows market. Recruiting remains the primary entry point because it generates high transaction volume and results are easier to measure through screening speed, interview coordination, and time-to-hire metrics. Employers also face ongoing pressure to widen candidate pools without overwhelming recruiters, which makes structured agent support attractive. The function is now moving beyond screening into interviewing and workflow execution inside large HCM environments. The integration of an AI Interviewer with a major cloud recruiting platform in May 2026 shows that autonomous skills-based interviewing is moving into mainstream enterprise recruiting stacks.

HR Operations Automation Agents is projected to grow at 27.14% CAGR through 2031, the fastest rate among functions in the agentic AI in HR workflows market. This growth comes from repetitive case handling, benefits administration, absence processing, document collection, and tier 1 query resolution, where process volumes are high, and decisions are often rules-based. These workflows also directly affect the employee experience, enabling buyers to see service improvements quickly after deployment. An AI specialist designed to resolve common HR cases through historical case retrieval and policy knowledge search aligns with this segment's commercial direction. As language models improve on unstructured requests, the agentic AI in HR workflows market is likely to push deeper into operational HR before fully autonomous decisions expand into more sensitive processes.

By Deployment Model: Cloud Commands Share, Hybrid Grows Fastest

Cloud-based deployment held 67.91% of 2025 revenue and remained the largest delivery model in the agentic AI in HR workflows market. Cloud environments make it easier to update models, connect external services, and scale workflows across multiple business units without heavy local infrastructure. The model also aligns with usage-based commercial structures, which gives buyers more flexibility when hiring volumes and service demand shift during the year. This matters for both large enterprises and smaller firms because cloud deployment reduces the operational burden of keeping agentic tools up to date. Discussion of flex-style consumption and HR agent use cases underscores why cloud delivery remains the default path for many organizations entering this market.

Hybrid deployment is projected to expand at 25.42% CAGR through 2031, the fastest pace among deployment models. The growth reflects the need to keep sensitive employee records in controlled environments while continuing to use cloud-based orchestration for broader workflow execution. In the agentic AI in HR workflows industry, this balance is especially important for healthcare, financial services, and government users working under residency and audit rules. The EU AI Act's high-risk treatment of employment AI reinforces why many buyers prefer architectures that separate sensitive records from scalable execution layers. On-premises deployment still has a place in highly controlled settings, but hybrid is becoming the more practical compromise across regulated parts of the agentic AI in HR workflows market.

By Enterprise Size: Large Enterprises Dominate, SMEs Narrow The Gap

Large Enterprises accounted for 63.21% of 2025 revenue, giving them the leading position in the agentic AI in HR workflows market. Their advantage comes from larger HR transaction volumes, stronger budgets, and dedicated teams that can handle integration, governance, and change management in parallel. These organizations also see a clearer payoff from orchestration layers because they run more workflows across more business units and geographies. Eight agentic HR applications launched in April 2026 were clearly targeted for enterprise-scale rollout across hiring, scheduling, manager support, and workforce operations. This keeps the large enterprise segment at the front of adoption because complexity makes coordinated automation more valuable.

SMEs are projected to expand at a 26.73% CAGR through 2031, the fastest growth rate among enterprise sizes in the agentic AI in HR workflows market. Pre-built agents and usage-based pricing are making it easier for companies with small HR teams and limited IT capacity to enter the category. Simpler deployment models also reduce the need for long configuration projects, which is important when buyers want quick operational gains. A leading HR software provider reported profitability in Q1 2026 while serving 16,000 customers and 1.5 million end users, and integrated an AI-focused team into its product and engineering organization to accelerate its AI roadmap. That pattern suggests the agentic AI in HR workflows market will expand as smaller firms adopt packaged capabilities rather than build custom automation stacks.

By End-User Industry: IT And Telecom Anchors Demand, Healthcare And Life Sciences Accelerates

Information Technology and Telecom held 29.41% of 2025 revenue, making it the largest end-user segment in the agentic AI in HR workflows market. The vertical benefits from high digital maturity, large contractor populations, and constant pressure to source, assess, and move talent quickly. These conditions support steady demand for recruiting, internal mobility, and HR service automation tools that can work across distributed teams. The segment also tends to accept new workflow models sooner because HR and IT teams already collaborate closely on enterprise software rollouts. That early willingness to test and scale new tools has helped this vertical anchor demand for agentic AI in HR workflows.

Healthcare and Life Sciences are projected to grow at 23.91% CAGR through 2031, the fastest pace among end users. The growth reflects staffing shortages, credential verification requirements, compliance demands, and high onboarding volumes, which make slow, manual workflows hard to sustain. These employers are under pressure to automate screening, credentialing, and service tasks without losing auditability. In the agentic AI in HR workflows industry, that makes governance and traceability are as important as raw automation speed. This mix of urgency and oversight is pushing vendors to tailor workflows for regulated settings rather than only for digital-first sectors inside the agentic AI in HR workflows market.

Geography Analysis

North America held 39.66% of the agentic AI market share in HR workflows in 2025, making it the largest regional market. The United States remained the main demand center because enterprise buyers, platform vendors, and integration partners are concentrated there. A 2026 survey found that 87% of CHROs expected greater AI adoption in HR processes, up from 83% in 2025, which supports continued demand momentum in the region. Large organizations set the regional pace because they can fund governance, integration, and workflow redesign simultaneously. Europe shows slower deployment cycles because the EU AI Act and local labor consultation requirements add documentation, review, and approval steps before going live.

Asia-Pacific is projected to record the fastest growth in the agentic AI in HR workflows market, with a 28.47% CAGR through 2031. Demand is rising across Southeast Asia, India, South Korea, China, Japan, and Australia as employers look for ways to manage recruiting, onboarding, and workforce planning with leaner teams. Japan stands out because corporate adoption is already broad, but several HR use cases still have room to deepen. Around 90% of surveyed member companies were using AI in some form in April 2026, while AI adoption for performance evaluation remained near 5%, leaving room for wider HR workflow deployment. National AI policy initiatives and workforce surveys show that policy development and governance planning are moving alongside adoption, which affects vendor qualification and procurement.

South America, the Middle East, and Africa held smaller shares of the agentic AI in HR workflows market in 2025, but they remain important for long-term expansion. Brazil is leading early demand in South America, while the United Arab Emirates and Saudi Arabia are serving as early rollout markets in the Middle East because workforce planning and hiring automation align with their labor policy priorities. South Africa is the clearest demand center in Africa, and Nigeria and Kenya are attracting cloud-native HR platforms that can shorten adoption timelines for mid-market employers. These regions still face budget and process standardization constraints, but they offer room for vendors that can package compliant workflows without heavy integration work in the agentic AI in HR workflows market.

Competitive Landscape

The agentic AI in HR workflows market remains moderately fragmented because competition is spread across infrastructure, application, and services layers. A major enterprise software provider strengthened its position in May 2026 by announcing 200 specialized AI agents across enterprise functions, including 15 new HR focused assistants for payroll, recruiting, onboarding, and HR service delivery. Another major vendor followed with eight agentic HR applications in April 2026, reinforcing its strategy of embedding coordinated agents inside a broader enterprise platform. More than 1,200 customers were registering and monitoring agents in early 2026 through a leading agent governance platform. These moves show that incumbents want agentic capability to be treated as part of the platform core, not as a separate add-on.

Competition is also being shaped by how well vendors connect skills data, workflow permissions, and interoperability inside the same operating environment. The integration of an AI interviewing solution with a major cloud recruiting platform illustrates how partnerships are being used to place agentic interviewing inside established HR systems instead of forcing a full platform replacement. A service-led approach centered on autonomous HR case handling is also gaining traction because many enterprises start with employee support before expanding into more sensitive decisions. AI roadmaps from SME focused HR software providers show that smaller market participants are also moving quickly to embed agentic features into standard HR software. This means competitive pressure is not limited to the largest HCM platforms in the agentic AI in HR workflows market.

The most durable differentiation is moving toward orchestration depth, compliance readiness, and deployment simplicity rather than generic AI positioning. Vendors that can show secure workflow execution across multiple tools are more likely to win earlier in regulated buying cycles. Those that can also package ready-to-use workflows for smaller buyers have a better chance of widening adoption beyond top-tier enterprises. Over time, the agentic AI in HR workflows market is likely to reward companies that combine governance, usable automation, and flexible commercial models in a single offer.

Agentic AI In HR Workflows Industry Leaders

Eightfold AI, Inc.

Phenom People, Inc.

iCIMS, Inc.

Paradox, Inc.

Beamery, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Eightfold AI integrated AI Interviewer with Oracle Fusion Cloud Recruiting, enabling autonomous skills based interviewing and streamlined procurement through Oracle Universal Credits.

- May 2026: SAP unveiled its Autonomous HCM vision, introducing Joule Assistants for payroll, recruiting, onboarding, and HR service delivery, along with AI driven workforce planning capabilities.

- April 2026: Oracle launched eight Fusion Agentic Applications for HR, powered by specialized AI agents through Oracle AI Agent Studio for coordinated HR workflow automation.

- April 2026: Personio achieved profitability while serving 16,000 customers and 1.5 million users, and accelerated its AI roadmap by integrating the aurio team into its product organization.

Global Agentic AI In HR Workflows Market Report Scope

The Agentic AI in HR Workflows market refers to intelligent platforms and services that embed autonomous AI agents into HR processes, enabling dynamic, skills-based decision-making and workflow orchestration. These solutions include orchestration engines, pre-built HR AI agents, professional services, and managed AI offerings that automate and optimize functions such as talent acquisition, employee lifecycle management, internal mobility, workforce planning, and HR operations.

The Agentic AI in HR Workflows market report is segmented by Component (Agentic AI Platforms and Orchestration Engines, Pre-built HR AI Agents and Workflow Applications, Professional Services, Managed Agentic AI Services), Function (Talent Acquisition and Recruiting Agents, Employee Lifecycle and HR Service Agents, Talent Development and Internal Mobility Agents, Workforce Planning and Intelligence Agents, HR Operations Automation Agents), Deployment Model (Cloud-Based, Hybrid, and On-Premises), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-user Industry (Information Technology and Telecom, Healthcare and Life Sciences, Banking, Financial Services and Insurance, Retail and E-Commerce, Industrial Manufacturing, Government and Public Sector, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa), The Market Forecasts are Provided in Terms of Value (USD).

| Agentic AI Platforms and Orchestration Engines |

| Pre-built HR AI Agents and Workflow Applications |

| Professional Services |

| Managed Agentic AI Services |

| Talent Acquisition and Recruiting Agents |

| Employee Lifecycle and HR Service Agents |

| Talent Development and Internal Mobility Agents |

| Workforce Planning and Intelligence Agents |

| HR Operations Automation Agents |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Information Technology and Telecom |

| Healthcare and Life Sciences |

| Banking, Financial Services and Insurance |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Component | Agentic AI Platforms and Orchestration Engines | |

| Pre-built HR AI Agents and Workflow Applications | ||

| Professional Services | ||

| Managed Agentic AI Services | ||

| By Function | Talent Acquisition and Recruiting Agents | |

| Employee Lifecycle and HR Service Agents | ||

| Talent Development and Internal Mobility Agents | ||

| Workforce Planning and Intelligence Agents | ||

| HR Operations Automation Agents | ||

| By Deployment Model | Cloud-Based | |

| Hybrid | ||

| On-Premises | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By End-User Industry | Information Technology and Telecom | |

| Healthcare and Life Sciences | ||

| Banking, Financial Services and Insurance | ||

| Retail and E-Commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the HR transformation services market in 2026, and what is the outlook to 2031?

The HR transformation services market was worth USD 23.12 billion in 2026 and is forecast to reach USD 36.29 billion by 2031, growing at a 9.44% CAGR over 2026-2031.

What is driving demand for HR transformation services right now?

Demand is being lifted by enterprise operating model redesign, cloud HCM optimization, workforce analytics adoption, and pressure to improve employee experience and agility across distributed workforces.

Which service type leads spending in this space?

HR Process Transformation and Reengineering led spending with a 28.37% share in 2025, showing that clients still prioritize workflow redesign before broader technology layering.

Which buyer group is expanding the fastest?

Small and Medium Enterprises are projected to grow at a 12.84% CAGR through 2031 as pre-configured cloud platforms and modular delivery models lower the entry barrier.

Which end-user sector is growing the fastest?

Healthcare and Life Sciences is expected to post the fastest growth at a 13.47% CAGR through 2031, supported by workforce redesign, upskilling, and administrative burden reduction needs.

Which region offers the strongest growth opportunity through 2031?

Asia-Pacific is the fastest-growing region with a 14.26% CAGR, supported by workforce formalization, digitalization programs, and broader reassessment of operating models across large employers.

Page last updated on: