AI-Powered Emergency Department Optimization Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

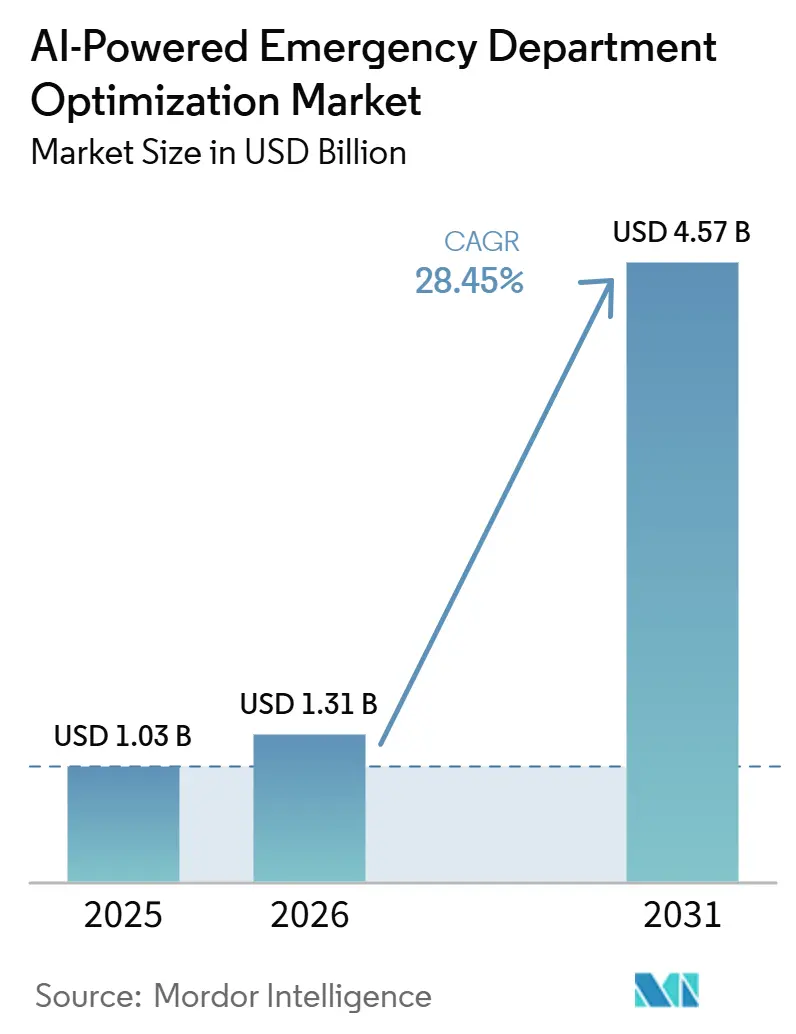

| Market Size (2026) | USD 1.31 Billion |

| Market Size (2031) | USD 4.57 Billion |

| Growth Rate (2026 - 2031) | 28.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-Powered Emergency Department Optimization Market Analysis by Mordor Intelligence

The AI-powered emergency department optimization market is expected to grow from USD 1.03 billion in 2025 to USD 1.31 billion in 2026 and is forecasted to reach USD 4.57 billion by 2031 at 28.45% CAGR over 2026-2031. The AI-powered emergency department optimization market is expanding because emergency care systems are operating under sustained volume pressure, and older patient cohorts are set to raise emergency demand further over the coming decade. Capacity limits are also tighter than before, as U.S. hospitals removed nearly 30,000 beds between 2019 and 2022, which has increased the need for tools that improve throughput without adding physical infrastructure. The AI-powered emergency department optimization market is also supported by a stronger clinical evidence base, because peer-reviewed work now shows that machine learning and natural language processing can improve emergency triage accuracy and consistency. Regulatory progress is reducing buyer hesitation, as broader AI clearances are beginning to replace fragmented single-condition tools and lower the implementation burden for health systems. Reimbursement gaps and liability concerns still slow some purchases, but persistent staffing stress and measurable operational gains continue to support a durable growth path for the AI-powered emergency department optimization market through 2031.

Key Report Takeaways

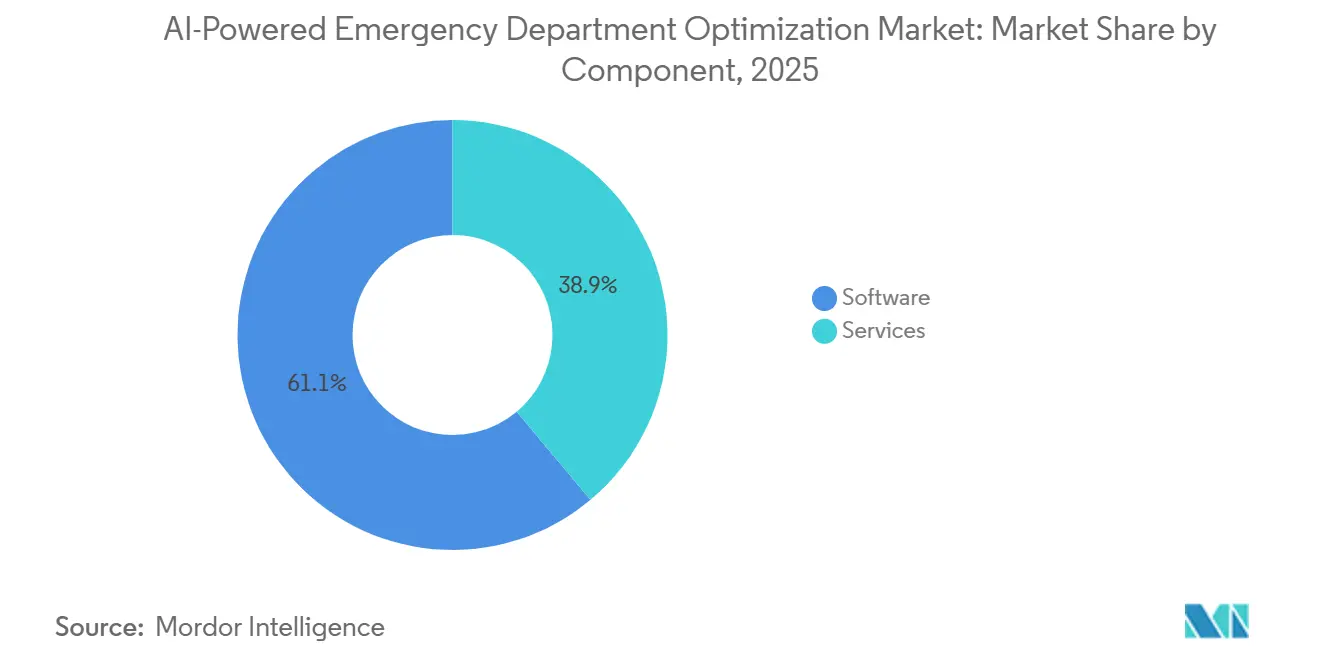

- By component, software led with 61.13% revenue share in 2025, and it is also projected to advance at the fastest 28.54% CAGR through 2031.

- By deployment mode, cloud-based deployment held 50.27% share in 2025, and it is also expected to record the fastest 28.81% CAGR through 2031.

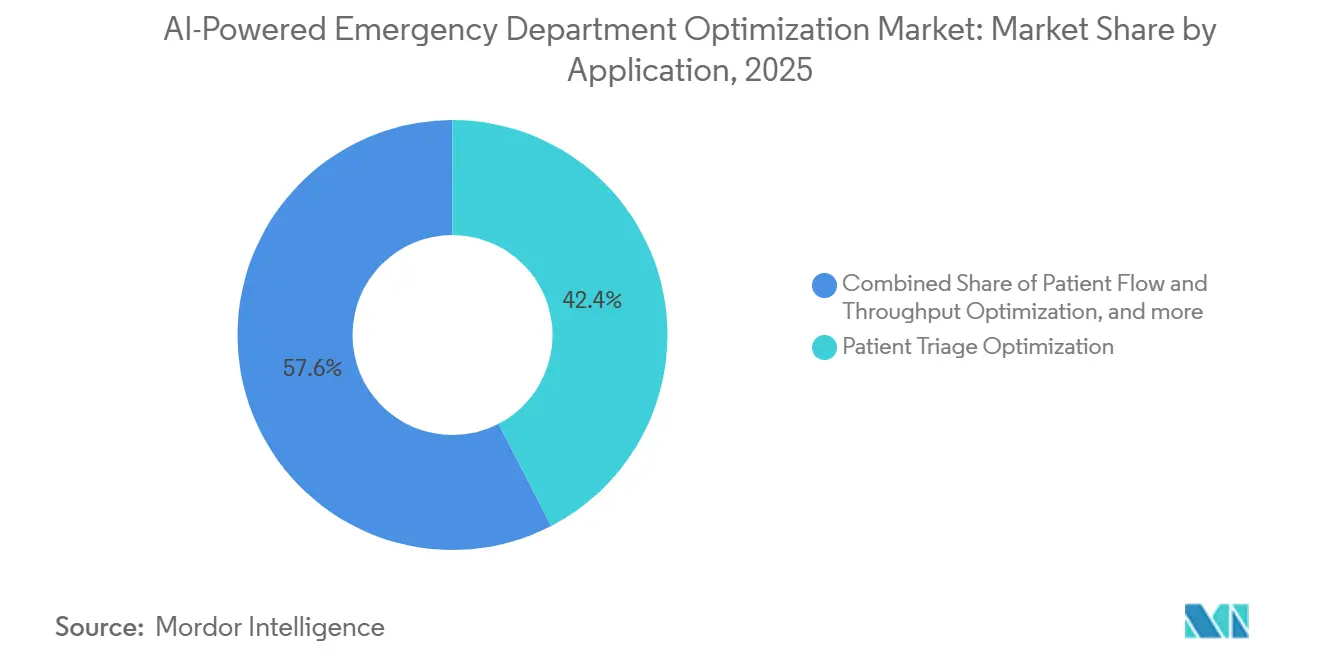

- By application, patient triage optimization accounted for 42.38% share in 2025, while patient flow and throughput are forecasted to expand at a 29.35% CAGR through 2031.

- By end-user, hospitals and health systems held 52.22% of the AI-powered emergency department optimization market share in 2025, while urgent care centers are projected to grow at the fastest 29.47% CAGR through 2031.

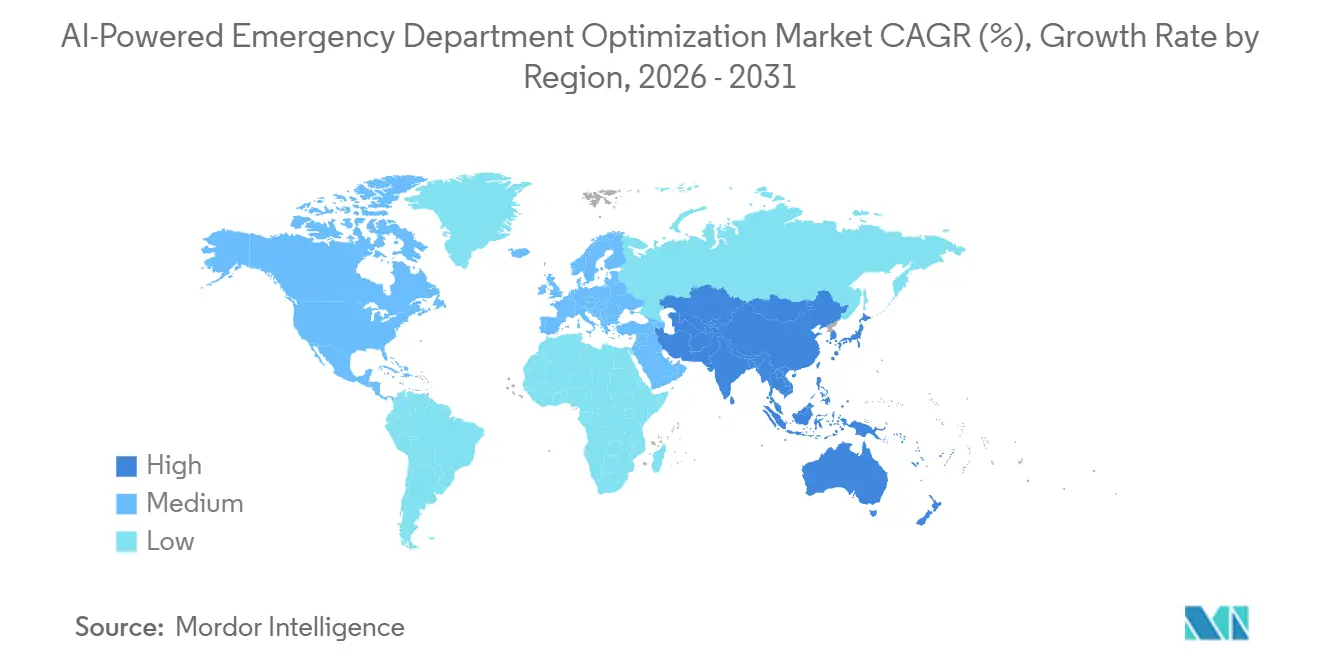

- By geography, North America accounted for 45.36% of the AI-powered emergency department optimization market share in 2025, while Asia-Pacific is projected to advance at the fastest 30.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-Powered Emergency Department Optimization Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Emergency Department Crowd-ing and Boarding Pressure | +7.2% | Global, concentrated in North America and APAC | Long term (≥ 4 years) |

| AI-Enabled Triage and Throughput Gains in High-Acuity Care | +6.8% | North America and Europe, accelerating in APAC | Medium term (2-4 years) |

| Interoperable EHR, PACS, and Command-Center Integration Demand | +4.5% | North America, the United Kingdom, and Northern Europe | Medium term (2-4 years) |

| Ambient Documentation Automation Reducing Clinician Burnout | +3.8% | North America leading, Europe expanding | Short term (≤ 2 years) |

| Growing Shortage of Emergency Care Clinicians and Staff | +3.5% | North America, the United Kingdom, and rural APAC | Long term (≥ 4 years) |

| Increasing Adoption of Predictive Analytics for Emergency Preparedness | +3.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Emergency Department Crowd-ing and Boarding Pressure

The AI-powered emergency department optimization market is tied closely to the structural overcrowding now seen across emergency systems. Americans made 139.8 million emergency department visits in 2024, and the 75 to 84 age cohort alone is projected to drive a 45% increase in emergent visits over the next decade, which is far beyond what manual staffing models can absorb on their own.[1]Vizient, “From Every Angle: Emergency Department Overcrowding,” Vizient Insights, vizientinc.comThe pressure is stronger because capacity has moved in the opposite direction, with nearly 30,000 hospital beds eliminated in the United States between 2019 and 2022. A 2025 retrospective cohort study in BMC Emergency Medicine found that prior-day overcrowding independently raised the risk of next-day crowding, which shows how quickly congestion can become self-reinforcing without predictive intervention.[2]A. Remi et al., “Improving Triage Performance in Emergency Departments Using Machine Learning and Natural Language Processing: A Systematic Review,” BMC Emergency Medicine, link.springer.com Behavioral health patients add another layer of demand because they represent 5% to 6% of visits while averaging 9 to 10 hours of length of stay, compared with 4 to 5 hours for the broader emergency population, which makes them a high-value target for AI-based throughput tools.

AI-Enabled Triage and Throughput Gains in High-Acuity Care

The AI-powered emergency department optimization market is also moving forward because the clinical support case for AI triage is much stronger than it was even a few years ago. A 2024 systematic review in BMC Emergency Medicine showed that machine learning and natural language processing models consistently outperformed human-only triage methods in both accuracy and consistency, especially when class imbalance correction and feature engineering were handled well. In January 2026, Aidoc received FDA 510(k) clearance for its CARE foundation model covering 14 acute CT indications in one workflow, with mean sensitivity of 97% and specificity of 98%, while also reducing false alerts by nearly tenfold against leading single-condition tools. As broader clearances become more common, the AI-powered emergency department optimization market is shifting away from fragmented one-off products toward platforms that reduce integration work and simplify vendor management for hospital buyers.

Ambient Documentation Automation Reducing Clinician Burnout

The AI-powered emergency department optimization market is benefiting from a wider move toward ambient documentation tools in emergency settings, because documentation still consumes a large share of clinical time in high-pressure environments. In NHS emergency settings, ambient AI tools reduced documentation time by 85.8% and saved clinicians an average of 5.27 minutes per patient encounter, which translates directly into throughput gains when staffing is constrained. These tools are gaining attention not only for time savings, but also because more complete capture of clinical nuance can improve coding accuracy and recorded patient acuity in value-based payment settings.

Growing Shortage of Emergency Care Clinicians and Staff

The AI-powered emergency department optimization market is also supported by persistent staffing strain, because health systems need tools that can absorb lower-cognitive tasks without adding equivalent headcount. Burnout and documentation burden remain central problems in emergency care, and that makes automation appealing even before direct reimbursement pathways become clear. A 2025 qualitative analysis in the Journal of Medical Internet Research found that AI systems designed around sociotechnical principles reduced stress and improved work conditions for critical care staff, which suggests that design quality matters as much as deployment scale.[3]S. Peeters et al., “Evaluating an AI Decision Support System for the Emergency Department: Retrospective Study,” JMIR AI, ai.jmir.org As triage scoring, documentation, and discharge prediction become more automated, clinicians can shift more of their time toward higher-acuity decisions that still depend on human judgment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clinical Liability Concerns Over AI-Driven Prioritization | -2.8% | Global, most pronounced in North America and Europe | Long term (≥ 4 years) |

| Poor Data Standardization Across Emergency Department Workflows | -1.9% | Global, most acute in the Middle East, Africa, and South America | Medium term (2-4 years) |

| High Implementation and Integration Costs | -1.5% | Rural and safety-net hospitals globally | Medium term (2-4 years) |

| Limited Clinical Validation and Trust in AI Recommendations | -1.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Clinical Liability Concerns Over AI-Driven Prioritization

Clinical liability remains one of the clearest constraints on the AI-powered emergency department optimization market because emergency medicine leaves little room for uncertainty around accountability. When an AI-assisted recommendation influences diagnosis or triage, liability can be spread across the clinician, the vendor, and the deploying institution, but most jurisdictions still lack a uniform allocation standard. The problem is sharper for foundation-model tools that cover many indications under one clearance, because it is often unclear where responsibility sits when broad output influences a harmful decision. Post-market surveillance expectations under Software as a Medical Device rules and Article 9 risk management requirements under the EU AI Act are starting to shape procurement contracts, but smaller health systems often lack the legal capacity to negotiate these provisions effectively.

Poor Data Standardization Across Emergency Department Workflows

Poor interoperability is another major brake on the AI-powered emergency department optimization market because emergency AI models need continuous access to clean and consistent patient data across settings. Advances in APIs, HL7 FHIR adoption, and national interoperability efforts have improved the foundation, but record sharing and payer-provider exchange still lag what emergency workflows require. In emerging markets and many rural settings, low levels of structured EHR use make it harder for models trained in data-rich hospital systems to perform reliably once deployed in lower-resource facilities. That creates a difficult pattern for the AI-powered emergency department optimization market, because many providers that would benefit most from optimization are the least prepared to meet the data and IT conditions needed for strong model performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Architecture Drives Market Value

Software captured 61.13% of revenue in 2025, which means it accounted for the largest portion of the AI-powered emergency department optimization market size in that year. Hospitals have favored modular, EHR-integrated software because it can be added to existing clinical systems in stages instead of forcing full replacement of core infrastructure. This layer includes ambient documentation engines, triage systems, patient flow dashboards, command center tools, and decision support applications, and each of these categories tends to gain more value as models learn from larger operating datasets over time. Software is also the fastest-growing component, with a projected 28.54% CAGR through 2031, which reinforces the central role of software-led platforms across the AI-powered emergency department optimization market.

Services still matter in the AI-powered emergency department optimization industry, because implementation, training, clinical informatics support, and managed analytics grow alongside software deployments. Procurement teams now treat HL7 FHIR R4 compatibility and HIPAA business associate agreement readiness as standard requirements, which gives an advantage to vendors with deeper regulatory and integration capacity. Health systems are also rationalizing earlier purchases of single-condition tools and moving toward broader workflow platforms under fewer contracts.

By Deployment Mode: Cloud Infrastructure Becomes the Default Architecture

Cloud-based deployment held 50.27% of revenue in 2025 and is also the fastest-growing deployment mode, with a projected 28.81% CAGR through 2031. Hospitals prefer cloud architecture because real-time inference in busy emergency settings requires elastic capacity that can handle sudden spikes in demand without large up-front hardware spending. Surge events can raise inference loads by 3 to 4 times normal levels within hours, and that pattern is difficult to support economically with fixed on-premises capacity alone.

On-premises deployment still has a place in the AI-powered emergency department optimization industry, especially at large academic medical centers and public hospital systems operating under strict data sovereignty rules. Germany’s and China’s data protection requirements continue to support local inference in some settings, even as the wider model still favors cloud adoption. Hybrid architecture is therefore becoming more relevant, because it allows latency-sensitive triage inference to remain inside institutional boundaries while training, updates, and longitudinal analytics move through cloud pipelines. This is likely to keep hybrid and edge configurations growing through the forecast period across the AI-powered emergency department optimization market.

By Application: Patient Flow and Throughput Leads Growth While Triage Holds Volume

Patient triage optimization retained the largest application share at 42.38% in 2025, which made it the leading use case within the AI-powered emergency department optimization market size. Triage has kept this lead because it has the most mature regulatory path and the deepest body of peer-reviewed validation, which makes procurement approval easier for hospitals. Patient flow and throughput management is expected to be the fastest-growing application at a 29.35% CAGR through 2031, because hospital leaders increasingly recognize that faster discharge and better bed use depend on coordinated movement across the whole emergency pathway, not only better front-end triage.

Resource allocation is another relevant application inside the AI-powered emergency department optimization market, because staffing prediction and capacity balancing directly affect cost and wait times. Clinical documentation is also moving quickly into emergency settings, as ambient AI scribes expand from ambulatory care into acute care workflows. Houston Methodist’s enterprise deployment of Ambience Healthcare reached 80% utilization across specialties, including emergency and inpatient care, in February 2026.

By End-User: Hospitals Anchor the Market as Urgent Care Chains Accelerate

Hospitals and health systems held 52.22% share in 2025, which made them the largest end-user group in the AI-powered emergency department optimization market. These organizations remain the main buyers because they manage the highest-acuity emergency volumes and have the strongest financial reason to improve throughput, reduce boarding, and coordinate care across several facilities. Multi-hospital networks gain added value because AI can help them rebalance patient loads across campuses in real time and change capacity use at the network level instead of only at one site.

Urgent care centers are the fastest-growing end-user segment, with a projected 29.47% CAGR through 2031. Their growth reflects the structural movement of lower-acuity emergency demand into settings that offer faster access and lower out-of-pocket cost than hospital emergency departments. Telehealth and virtual care providers are also using AI triage to screen patients before physical emergency presentation, which supports care deflection into lower-acuity channels when appropriate. Ambulatory surgery centers are adopting related tools for post-procedure deterioration detection and discharge prediction, which broadens the commercial use case surrounding the AI-powered emergency department optimization market.

Geography Analysis

North America held 45.36% share in 2025, which gave the region the largest position in the AI-powered emergency department optimization market. The United States remains the main deployment and innovation center because it combines large integrated health systems, FDA-cleared clinical AI tools, and stronger financial incentives tied to throughput and value-based care. Canada remains a follow-on opportunity under broader digital health investment plans, while Mexico’s private hospital groups are testing cloud-based triage platforms in larger urban centers.

Europe remains the second-largest regional cluster in the AI-powered emergency department optimization market, led by Germany, the United Kingdom, and France. The United Kingdom has become an active testing ground for ambient documentation in emergency settings, and NHS-based deployments reported an 85.8% reduction in documentation time per encounter in short-stay emergency environments. Germany benefits from strong hospital digitalization support, while the EU AI Act and wider electronic health record rules are beginning to shape how vendors structure product entry, compliance, and risk management. Italy, France, and Spain are still earlier in commercial scaling, and most growth there depends on broader digital health policy support rather than large emergency-specific procurement waves. GCC countries, especially Saudi Arabia and the UAE, are attracting more vendor attention through smart hospital investment, while Brazil and Argentina are emerging as early South American pilots for AI resource allocation and operational tools.

Asia-Pacific is projected to post the fastest regional growth in the regional AI-powered emergency department optimization market size is projected to expand at a 30.24% CAGR through 2031. China is the clearest example of compressed adoption, because by 2025, 90 tertiary hospitals had deployed the DeepSeek large language model for clinical use and domestic enterprises had already released more than 50 healthcare vertical AI models. South Korea has built a more structured validation path, and Gil Medical Center’s pilot reported 94% concordance between AI and specialist diagnosis in emergency use.

Competitive Landscape

The AI-powered emergency department optimization market remains moderately fragmented, but the competitive structure is becoming clearer as major health IT incumbents and specialist AI vendors move into overlapping workflow areas. Epic Systems and Oracle Health hold a strong installed-base advantage because deep EHR integration allows them to add AI into existing accounts with lower friction than outside vendors. Epic’s 2025 roadmap included nearly 200 AI features in development and a co-developed charting tool with Microsoft, which shows how the EHR layer is evolving toward a broader orchestration role in hospital operations.

Specialist vendors are responding through depth, regulatory differentiation, and workflow breadth. Aidoc has invested more than USD 150 million in its CARE foundation model and used FDA clearance for a multi-indication triage solution to create a regulatory moat that is harder for single-condition vendors to match. GE HealthCare is concentrating on the capacity management layer rather than only on triage, and its operating examples with large health systems show a strategy built around throughput, staffing, and command-center performance. White space remains strongest in discharge planning, behavioral health routing, and smaller community hospital deployment, where implementation cost and complexity still limit broad penetration.

The AI-powered emergency department optimization market is therefore moving toward platform competition rather than isolated tool competition. Switching costs are rising because documentation, triage, and throughput tools increasingly sit inside broader workflow systems that are difficult to replace one module at a time. Procurement teams are also starting to treat ISO/IEC 42001 readiness and HL7 FHIR compliance as informal entry requirements, which favors vendors with stronger governance and audit processes. Patent activity around foundation-model triage, ambient natural language processing, and patient flow prediction is also concentrating among the better-funded participants, which should help the leading group defend differentiated positions even as some workflow features become easier to replicate.

AI-Powered Emergency Department Optimization Industry Leaders

Epic Systems Corporation

Oracle Corporation

Aidoc

Qventus, Inc.

TeleTracking Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Sayvant published the largest multicenter study of AI-assisted clinical documentation in emergency medicine, covering over 250,000 patient encounters across 50 EDs ranging from academic medical centers to rural facilities, delivering the most comprehensive real-world acute care evidence set to date.

- March 2026: Oracle Corporation launched Oracle Health Clinical AI Agent for emergency department and inpatient settings in the U.S. market, enabling real-time ambient note generation that captures multi-encounter clinical context without post-encounter transcription, directly addressing one of the most cited productivity drains in emergency medicine.

- February 2026: Qventus launched the Care Gap and Coding Automation Suite, combining AI-driven missed diagnosis identification, real-time care orchestration, and automated documentation in a single EHR-embedded workflow, the first solution to link detection, intervention, and coding in a continuous loop.

- February 2026: Houston Methodist deployed Ambience Healthcare's ambient AI platform enterprise-wide across ambulatory, emergency, and inpatient settings, achieving 80% utilization across specialties and marking one of the broadest ambient AI deployments at a U.S. academic medical center to date.

Global AI-Powered Emergency Department Optimization Market Report Scope

According to the report’s scope, the AI‑powered emergency department optimization market is the healthcare technology segment where artificial intelligence is applied to streamline ED workflows, including triage, surge prediction, and resource allocation. It focuses on reducing wait times, improving patient safety, and enhancing staff efficiency in high‑acuity emergency settings, making it a critical growth area within hospital operations and predictive analytics.

The AI‑powered emergency department optimization market is segmented into component, deployment mode, application, end-user, and geography. By component, the market is segmented into software and services. By deployment mode, the market is segmented into cloud-based, on-premises, and hybrid. By application, the market is segmented into patient triage optimization, patient flow and throughput optimization, resource allocation and staffing optimization, clinical documentation automation, discharge planning and bed management, and other applications. By end-user, the market is segmented into hospitals and health systems, urgent care centers, ambulatory surgery centers, and telehealth and virtual care networks. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Patient Triage Optimization |

| Patient Flow and Throughput Optimization |

| Resource Allocation and Staffing Optimization |

| Clinical Documentation Automation |

| Discharge Planning and Bed Management |

| Other Applications |

| Hospitals and Health Systems |

| Urgent Care Centers |

| Ambulatory Surgery Centers |

| Telehealth and Virtual Care Networks |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Application | Patient Triage Optimization | |

| Patient Flow and Throughput Optimization | ||

| Resource Allocation and Staffing Optimization | ||

| Clinical Documentation Automation | ||

| Discharge Planning and Bed Management | ||

| Other Applications | ||

| By End-User | Hospitals and Health Systems | |

| Urgent Care Centers | ||

| Ambulatory Surgery Centers | ||

| Telehealth and Virtual Care Networks | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected 2031 value of AI-powered emergency department optimization?

The AI-powered emergency department optimization market is forecasted to reach USD 4.57 billion by 2031, rising from USD 1.03 billion in 2025 to USD 1.31 billion in 2026 at a 28.45% CAGR.

Which component leads revenue in AI-powered emergency department optimization?

Software led the market with a 61.13% share in 2025 and is also projected to be the fastest-growing component with 28.54% CAGR through 2031.

Which application is growing the fastest in emergency department optimization?

Patient flow and throughput management is projected to grow at 29.35% CAGR through 2031, ahead of other application areas.

Which region is expanding the fastest for emergency department AI solutions?

Asia-Pacific is projected to grow the fastest at a 30.24% CAGR through 2031, supported by rapid hospital AI deployment in China and structured validation programs in South Korea.

Page last updated on: