Digital Healthcare Supply Chain Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.88 Billion |

| Market Size (2031) | USD 4.32 Billion |

| Growth Rate (2026 - 2031) | 8.44% CAGR |

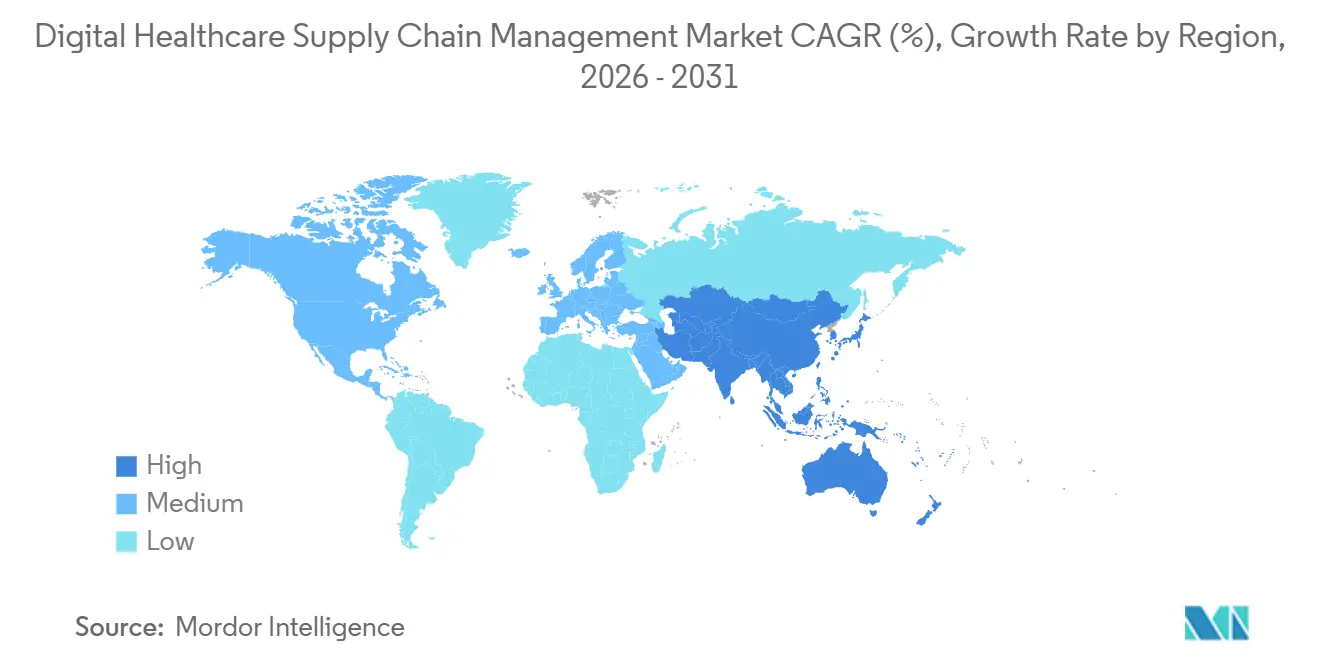

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

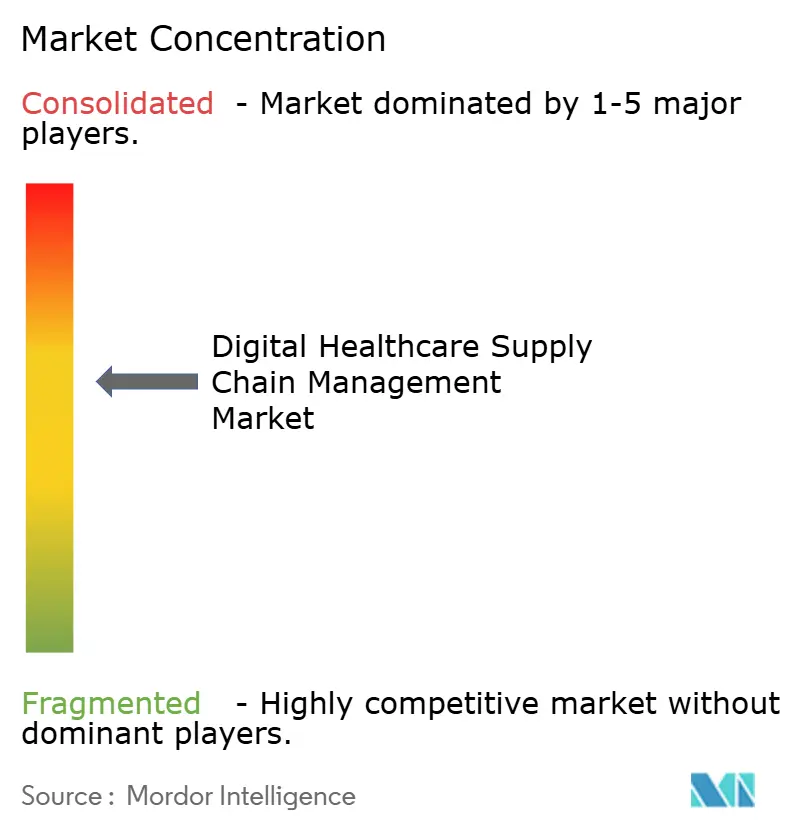

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Healthcare Supply Chain Management Market Analysis by Mordor Intelligence

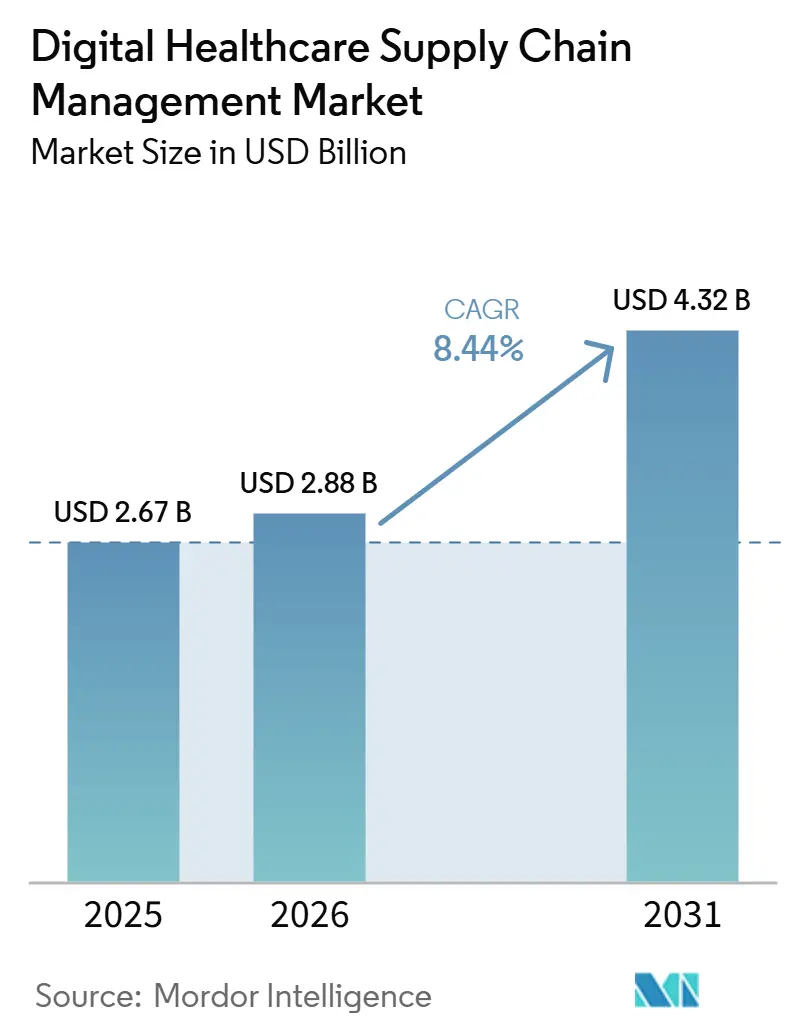

The digital healthcare supply chain management market is projected to be USD 2.67 billion in 2025, USD 2.88 billion in 2026, and reach USD 4.32 billion by 2031, growing at a CAGR of 8.44% from 2026 to 2031. The digital healthcare supply chain management market is also gaining from a firm shift toward cloud adoption, with GHX reporting that nearly 70% of U.S. hospitals and health systems were on track to adopt a cloud-based approach to supply chain management by 2026, while full DSCSA enforcement is making serialized and interoperable product tracing a core software requirement rather than an optional upgrade. Competition in the digital healthcare supply chain management market remains active because ERP vendors, healthcare exchange platforms, and workflow specialists are moving into the same operating areas, especially AI-supported orchestration and traceability. Inventory management is now growing faster than procurement management, which shows that the digital healthcare supply chain management market is shifting from back-office buying efficiency toward continuous stock visibility, replenishment control, and point-of-care responsiveness. Integration debt, weak data standards, and budget limits among smaller providers still slow adoption, yet supply chain software spending is moving closer to a non-discretionary category as health systems treat it as part of margin protection and service continuity.

Key Report Takeaways

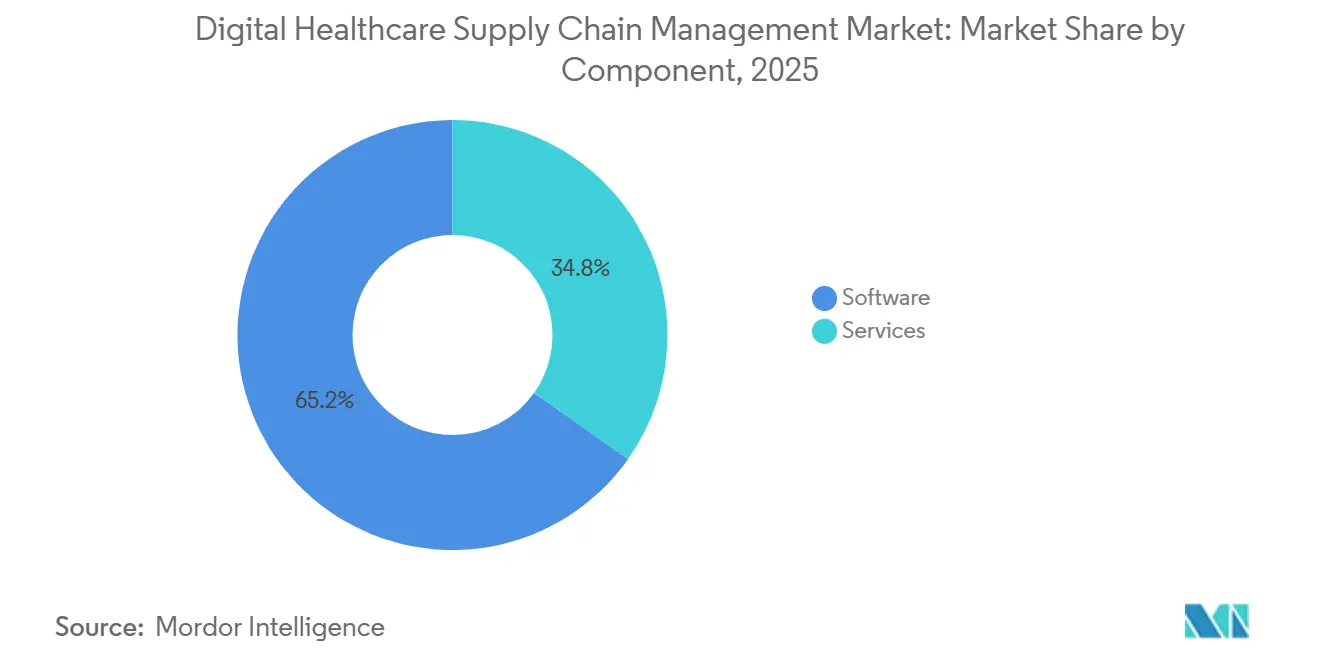

- By component, software led with 65.18% revenue share in 2025, while services are forecast to grow at a 9.58% CAGR through 2031.

- By deployment mode, cloud-based deployment held 59.42% share of the digital healthcare supply chain management market size in 2025 and is also expected to advance at a 10.26% CAGR through 2031.

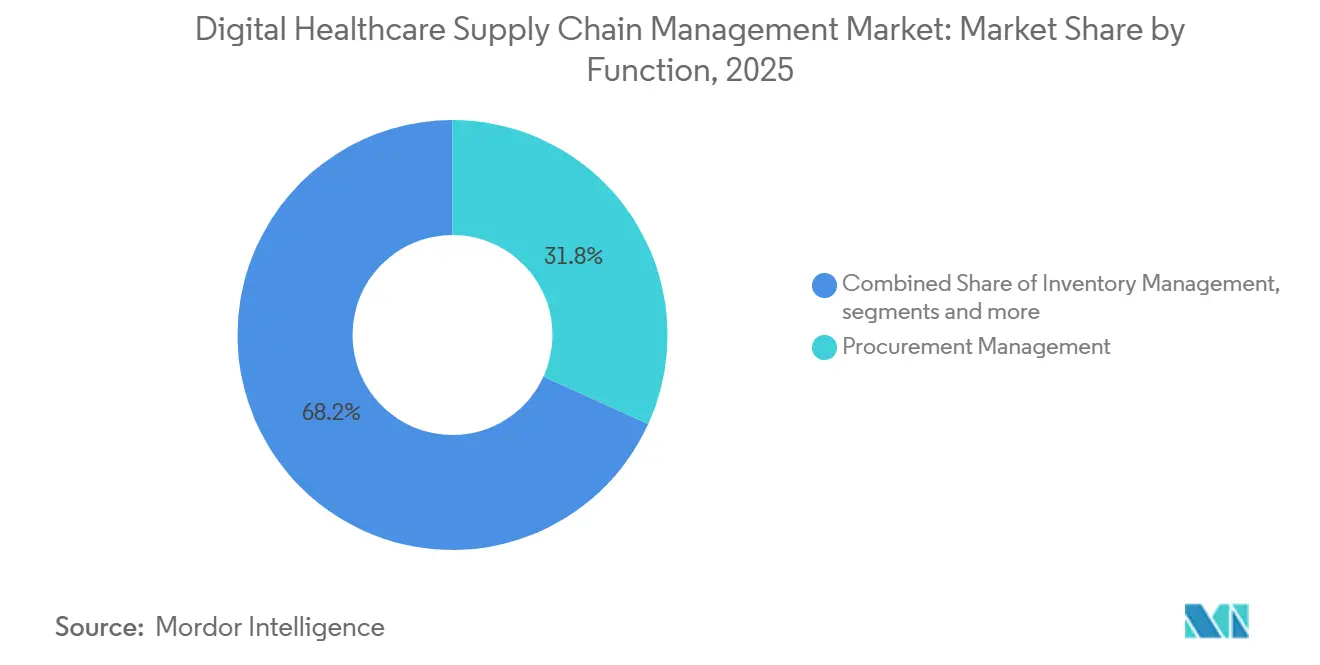

- By function, procurement management accounted for 31.76% of revenue in 2025, while inventory management is projected to expand at a 10.73% CAGR through 2031.

- By end-user, hospitals and health systems held 52.84% of revenue in 2025, while pharmaceutical and biotechnology companies are projected to grow at a 9.91% CAGR through 2031.

- By geography, North America accounted for 43.68% of revenue in 2025, while Asia-Pacific is projected to expand at a 11.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Digital Healthcare Supply Chain Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Real-Time Inventory Visibility Across Healthcare Networks | +2.0% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Increasing Pressure to Reduce Stockouts and Expired Inventory | +1.6% | Global, concentrated in North America & APAC | Short term (≤ 2 years) |

| Expansion of Interoperable Cloud-Based Supply Chain Platforms | +1.4% | Global, led by North America and Western Europe | Medium term (2-4 years) |

| Regulatory Push for Traceability and Product Authentication | +1.2% | North America & EU core, expanding to APAC | Short term (≤ 2 years) |

| Growing Need for Automated Demand Forecasting and Replenishment | +0.9% | Global, priority in complex biologics supply chains | Medium term (2-4 years) |

| Rising Adoption of AI-Enabled Exception Management in Hospital Procurement | +0.8% | Global, led by North America innovation hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Real-Time Inventory Visibility Across Healthcare Networks

Real-time inventory visibility has become a daily operating requirement in the digital healthcare supply chain management market because shortages at the point of care disrupt procedures and staff productivity. Health systems are moving beyond simple asset tracking and are asking platforms to convert live location, census, and usage signals into replenishment actions. This is changing the buying logic in the digital healthcare supply chain management market, because providers now value workflow response and not just data capture. Kontakt.io launched its Supply Chain Agent in February 2026 and said the system reduced nurse search time by 80% by using care demand signals to route equipment more proactively.[1]Kontakt.io, “Kontakt.io Introduces Supply Chain AI to Transform Care Support Operations,” PR Newswire, prnewswire.comThat kind of move shows why the digital healthcare supply chain management market is shifting toward software layers that can see inventory, decide what matters, and trigger action without waiting for manual intervention. As a result, vendors with stronger orchestration features are gaining a better position in provider buying decisions.

Increasing Pressure to Reduce Stockouts and Expired Inventory

The digital healthcare supply chain management market is also being pulled forward by tighter pressure to reduce stockouts, expired products, and avoidable waste across hospitals and distribution networks. Healthcare organizations are now less willing to approve technology that only improves reporting, and they increasingly want direct savings from better stock rotation, fewer missed replenishment events, and lower emergency sourcing costs. This has raised the bar for vendors in the digital healthcare supply chain management market, because buyers expect measurable operational results within a shorter payback period. The same pressure is pushing provider networks to rationalize disconnected point tools and favor systems that combine procurement, inventory, and supplier coordination in one operating layer. That trend supports cloud-native and analytics-led offerings, while older high-maintenance deployments face more pressure during capital review cycles. It also strengthens renewal prospects for vendors that can tie software usage to reduced waste and more stable supply continuity.

Expansion of Interoperable Cloud-Based Supply Chain Platforms

The expansion of interoperable cloud platforms is widening the addressable scope of the digital healthcare supply chain management market. Buyers increasingly want supply chain systems to connect with ERP, hospital information systems, pharmacy systems, and distributor data feeds without long custom integration cycles. This favors the digital healthcare supply chain management market segments that offer standard connectors, continuous updates, and private cloud options for organizations that still need tighter control over sensitive environments. GHX has already highlighted the scale of the cloud shift among hospitals, and that signal supports a broader move toward hosted supply chain operating models in provider networks. Oracle also expanded AI-powered inventory and material handling capabilities inside Oracle Fusion Cloud Applications in September 2025, which shows how large vendors are using cloud architecture to add new supply chain functions faster.[2]Oracle Corporation, “Oracle Helps Healthcare Organizations Streamline Supply Chain Operations,” Oracle News, oracle.com As these interoperable platforms mature, the digital healthcare supply chain management market is moving away from isolated software modules and toward broader operating environments that can support procurement, traceability, and execution together.

Regulatory Push for Traceability and Product Authentication

Regulation is one of the clearest growth anchors for the digital healthcare supply chain management market. The FDA requires package-level serialization and interoperable product tracing under DSCSA, and this is forcing manufacturers, distributors, and dispensers to strengthen their data exchange and compliance infrastructure. In March 2026, the FDA also issued a final rule that established a uniform 12-digit NDC format and allowed 2D data matrix barcodes that can carry serial number, lot, and expiry information in one code.[3]U.S. Government Publishing Office, “Federal Register, Volume 91 Issue 43, March 5, 2026, FDA NDC12 Uniform Format Final Rule,” Federal Register, govinfo.gov That change improves labeling and traceability alignment and raises the value of software that can manage product identity, event capture, and auditability in the digital healthcare supply chain management market. McKesson’s March 2026 SAP case study also showed that major distributors are treating traceability as part of a long-cycle platform decision and not as a stand-alone compliance patch. The result is a more durable demand base for serialization, verification, and trading partner connectivity tools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Legacy ERP and Procurement Environments | -1.5% | Global, most acute in North America & EU large academic centers | Long term (≥ 4 years) |

| High Integration Complexity with Clinical and Logistics Systems | -1.2% | Global, with healthcare API maturity gaps in APAC and MEA | Medium term (2-4 years) |

| Data Standardization Gaps Across Suppliers, Distributors, and Providers | -0.9% | Global, APAC and MEA face highest standardization deficits | Medium term (2-4 years) |

| Budget Constraints in Smaller Healthcare Providers | -0.7% | Global, concentrated in emerging markets and independent providers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Legacy ERP and Procurement Environments

Fragmented ERP estates remain a major drag on the digital healthcare supply chain management market because many provider and manufacturer organizations still operate mixed procurement and finance environments. New supply chain applications often need to work with older transaction systems, local databases, custom interfaces, and different governance rules at the same time. This raises implementation time in the digital healthcare supply chain management market and can delay the benefits that buyers expect from cloud migration and workflow automation. It also keeps some customers on phased modernization paths where they add point capabilities before they can replace core transaction systems. Vendors that can support hybrid deployment models are better placed because they can connect new analytics and orchestration tools to older operational systems with less disruption. Even so, the digital healthcare supply chain management market still loses momentum when technology adoption depends on a broader ERP transition that has not yet been completed.

High Integration Complexity with Clinical and Logistics Systems

Integration complexity is another meaningful restraint for the digital healthcare supply chain management market because supply transactions often depend on pharmacy systems, patient activity, billing rules, logistics data, and ERP records at once. When those environments do not exchange clean data in real time, organizations struggle to automate replenishment, product tracing, and order resolution. DSCSA adds to that pressure because it requires interoperable tracing and stronger event-level data exchange across trading partners. The digital healthcare supply chain management market therefore faces longer deployment cycles in environments where connectivity still depends on custom mapping and brittle middleware. This slows time to value for buyers and pushes vendors to spend more on services, data modeling, and change management before software benefits become visible. It also explains why buyers increasingly prefer platforms with healthcare-specific connectors and prebuilt workflow logic.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platform Depth Drives Structural Share Premium

Software held 65.18% of the digital healthcare supply chain management market share in 2025, and this reflected buyer preference for platforms that can combine analytics, compliance, and workflow execution inside one environment. In the digital healthcare supply chain management industry, software has become the main control layer for procurement, inventory, traceability, and supplier coordination. Healthcare organizations prefer recurring software capability because it supports continuous process improvement and faster feature delivery across multiple facilities.

Services are expected to be the fastest-growing component at a 9.58% CAGR through 2031, which shows that the digital healthcare supply chain management market still needs training, integration, and managed support as the installed base grows. The digital healthcare supply chain management market also creates service demand when organizations modernize in phases and need support across both old and new environments. Over time, services should remain important, but the share premium is likely to stay with software because it owns the recurring transaction logic and the data model that customers depend on every day.

By Deployment Mode: Cloud Leads on Both Share and Growth

Cloud-based deployment accounted for 59.42% of the digital healthcare supply chain management market size in 2025, and it is also expected to be the fastest-growing mode at a 10.26% CAGR through 2031. That combination is important because it shows the digital healthcare supply chain management market is not only adding new cloud users, but also shifting the center of value creation toward hosted and continuously updated platforms. Hospitals increasingly want lower maintenance burden, quicker feature activation, and better interoperability with distributed sites and trading partners. Cloud architecture also supports AI rollout more effectively because new models, rules, and workflow changes can be delivered without major local reconfiguration.

On-premises deployment still remains relevant for some large institutions with older integration structures, internal control requirements, or staged migration plans. Even in those cases, the digital healthcare supply chain management industry is moving toward private cloud or hybrid models rather than defending full on-premises estates indefinitely. As more buyers seek a common operating layer for procurement, traceability, and workflow intelligence, cloud deployment is likely to remain the strongest structural driver across the digital healthcare supply chain management market.

By Function: Inventory Management, Acceleration Signals a Clear Priorities Shift

Procurement management held 31.76% of revenue in 2025, which kept it as the largest functional segment in the digital healthcare supply chain management market. This position reflected years of investment in sourcing, contract alignment, supplier transactions, and structured purchasing workflows. Procurement remains central because providers and manufacturers still need stronger control over prices, supplier compliance, and purchase execution. Yet the growth profile has changed because inventory management is projected to expand at a 10.73% CAGR through 2031, ahead of the more mature procurement layer. That shows the digital healthcare supply chain management market is placing more value on stock visibility, replenishment timing, and direct operational control closer to care delivery.

The digital healthcare supply chain management market is therefore moving from procurement digitization alone toward a broader control model that can see what is being consumed and act on it quickly. Traceability and serialization functions are also gaining importance because the FDA’s March 2026 NDC12 rule supports more unified barcode-based compliance workflows. The result is a more balanced functional landscape where procurement still leads in share, while inventory and traceability are taking a larger role in new spending.

By End-User: Hospitals Anchor Revenue While Pharma Expands Faster

Hospitals and health systems represented 52.84% of revenue in 2025, making them the largest end-user group in the digital healthcare supply chain management market. Their lead reflects broad SKU complexity, multi-site distribution requirements, and the need to coordinate pharmaceuticals, consumables, equipment, and implantables inside one operating structure. In the digital healthcare supply chain management industry, this makes hospitals the most defensible customer base for full-suite platform vendors. These organizations also gain from software that can connect purchasing decisions with actual care activity, inventory status, and supplier response. That supports steady demand for solutions that can manage daily variability across procedure-heavy and pharmacy-intensive environments.

Pharmaceutical and biotechnology companies are projected to be the fastest-growing end-user segment at a 9.91% CAGR through 2031, and regulation is a major reason. The digital healthcare supply chain management market also benefits here from biologics expansion, because cold-chain and lot-sensitive products require tighter visibility and handling discipline. Medical device manufacturers remain relevant as they strengthen traceability and identification workflows across regulated channels. This keeps end-user expansion broad, even though hospitals remain the core revenue anchor of the digital healthcare supply chain management market.

Geography Analysis

North America held 43.68% of the digital healthcare supply chain management market share in 2025, which kept it as the largest regional segment. The region benefits from strong healthcare IT maturity, a deep hospital network scale, and the most developed regulatory push around pharmaceutical traceability. Cloud readiness is another advantage, with GHX stating that nearly 70% of U.S. hospitals and health systems were on track to adopt a cloud-based approach by 2026. This combination keeps the digital healthcare supply chain management market in North America well ahead on both platform adoption and workflow modernization.

Europe remained the second-largest regional block in the digital healthcare supply chain management market, supported by a mix of health system digitization and interoperability reform. Germany is an important reference point because the Federal Ministry of Health advanced its digitalization strategy in February 2026 and also published the GeDIG framework in 2026 to support data and digital innovation in healthcare. SAP and Fresenius also announced a strategic partnership in January 2026 to build an interoperable AI-supported healthcare system using HL7 FHIR standards. These moves support a regional market where procurement, data sharing, and digital operating standards are becoming more aligned.

Asia-Pacific is projected to be the fastest-growing regional segment in the digital healthcare supply chain management market, with a projected 11.24% CAGR through 2031. Growth in the region is supported by a lower installed base, ongoing hospital modernization, and broader use of automated logistics and digital procurement systems. China and Japan remain the main scale anchors, while India, South Korea, and Australia add momentum from expanding digital healthcare infrastructure. Other regions, including the Middle East and Africa and South America, are still earlier in adoption, but hospital investment and local pharmaceutical development programs continue to open first-generation demand for the digital healthcare supply chain management market.

Competitive Landscape

The digital healthcare supply chain management market shows moderate concentration because large ERP vendors, healthcare exchange platforms, and specialist workflow companies all compete across overlapping process areas. SAP and Oracle are strong in broad enterprise integration, while GHX, McKesson, Tecsys, Manhattan Associates, Kinaxis, and Blue Yonder compete more directly in healthcare exchange, planning, inventory, and execution layers. This keeps the digital healthcare supply chain management market active and limits the ability of any one vendor to dominate all use cases. It also means buyers often choose vendors based on workflow depth, deployment model, and integration fit rather than on broad scale alone. The most important competitive shift now is the move toward AI-supported orchestration, where software is expected to recommend actions and increasingly carry them out.

Manhattan Associates advanced that position in January 2026 when it announced commercial availability of its AI Agent Workforce inside its platform. Oracle strengthened its own position earlier through AI-powered inventory capabilities inside Oracle Fusion Cloud Applications. These moves show that the digital healthcare supply chain management market is rewarding vendors that embed workflow intelligence into the operating layer and not just into reporting tools. They also raise renewal pressure on providers that still depend on older architectures with weaker automation depth.

Capital moves also show where the digital healthcare supply chain management market is heading. McKesson closed a USD 1.25 billion investment from Apollo Funds in June 2026 tied to its Medical-Surgical Solutions business, which signaled a material reshaping of one important distribution segment. McKesson’s March 2026 work with SAP on pharmaceutical traceability also reinforced how large participants are linking compliance execution with long-horizon platform architecture. White-space opportunities remain strongest in mid-sized hospital systems, underpenetrated emerging markets, and cold-chain-sensitive pharmaceutical workflows. That leaves the digital healthcare supply chain management market competitive, but still open to specialist differentiation where workflow needs remain too specific for generic enterprise software.

Digital Healthcare Supply Chain Management Industry Leaders

Oracle

SAP SE

GHX, Inc.

McKesson Corporation

Tecsys Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: McKesson Corporation closed a USD 1.25 billion convertible preferred equity investment from Apollo Funds, representing approximately 13% of McKesson's Medical-Surgical Solutions business at a total enterprise valuation of approximately USD 13 billion, marking a key step toward separating MMS into an independent, publicly traded company and materially reshaping the competitive structure of the healthcare supply chain distribution segment.

- June 2026: Tecsys unveiled TecsysIQ AI and agentic capabilities at its 2026 User Conference, including TecsysIQ Inventory Visibility, consolidating ADC, pharmacy, and ERP data into a single real-time view, a 340B Integrity Agent, and a Point of Use Expiry Agent, a coordinated AI capability launch targeting the pharmacy environment's most persistent compliance and waste challenges.

- May 2026: GHX launched a next-generation AI-powered orchestration platform designed to enable healthcare providers and suppliers to sense disruptions earlier, coordinate decisions faster, and act before patient care is impacted. GHX cited Roche's elimination of workflow debt across 20,000+ transactions, saving thousands of hours, as a validation case for the platform.

- March 2026: McKesson's case study with SAP confirmed deployment of SAP Advanced Track and Trace for Pharmaceuticals on SAP S/4HANA Cloud Private Edition and SAP Traceability Hub Connectivity, delivering end-to-end pharmaceutical traceability and scalable regulatory compliance aligned with DSCSA requirements.

Global Digital Healthcare Supply Chain Management Market Report Scope

According to the report’s scope, the digital healthcare supply chain management market refers to the segment of healthcare operations that leverage digital platforms, software, and services to manage the flow of medical products, pharmaceuticals, devices, and consumables across hospitals, distributors, and manufacturers. It covers inventory management, procurement systems, logistics and cold‑chain monitoring, supplier relationship management, demand forecasting, and analytics tools, ensuring efficiency, compliance, and cost‑effectiveness in healthcare supply chains.

The digital healthcare supply chain management market is segmented into component, deployment mode, function, end-user, and geography. By component, the market is segmented into software and services. By deployment mode, the market is segmented into cloud-based and on-premises. By function, the market is segmented into procurement management, inventory management, order and supplier management, demand planning and forecasting, analytics and reporting, and traceability and serialization. By end-user, the market is segmented into hospitals and health systems, pharmaceutical and biotechnology companies, medical device manufacturers, and other end-users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Procurement Management |

| Inventory Management |

| Order and Supplier Management |

| Demand Planning and Forecasting |

| Analytics and Reporting |

| Traceability and Serialization |

| Hospitals and Health Systems |

| Pharmaceutical and Biotechnology Companies |

| Medical Device Manufacturers |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| By Function | Procurement Management | |

| Inventory Management | ||

| Order and Supplier Management | ||

| Demand Planning and Forecasting | ||

| Analytics and Reporting | ||

| Traceability and Serialization | ||

| By End-User | Hospitals and Health Systems | |

| Pharmaceutical and Biotechnology Companies | ||

| Medical Device Manufacturers | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 value expected for digital healthcare supply chain management market?

The market is projected to reach USD 4.32 billion by 2031, rising from USD 2.67 billion in 2025 to USD 2.88 billion in 2026 at an 8.44% CAGR.

Which end-user group contributes the most revenue?

Hospitals and health systems are the largest end-user group, with 52.84% of revenue in 2025 because they manage the broadest mix of products and workflows.

Why is inventory management growing faster than procurement management?

Inventory management is expected to be at a 10.73% CAGR through 2031 because providers now place more value on real-time stock visibility, replenishment control, and point-of-care responsiveness.

Which region is growing the fastest?

Asia-Pacific is projected to post the fastest growth at an 11.24% CAGR through 2031, supported by hospital modernization and broader digital supply chain adoption.

Page last updated on: