Regenerative Agriculture Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

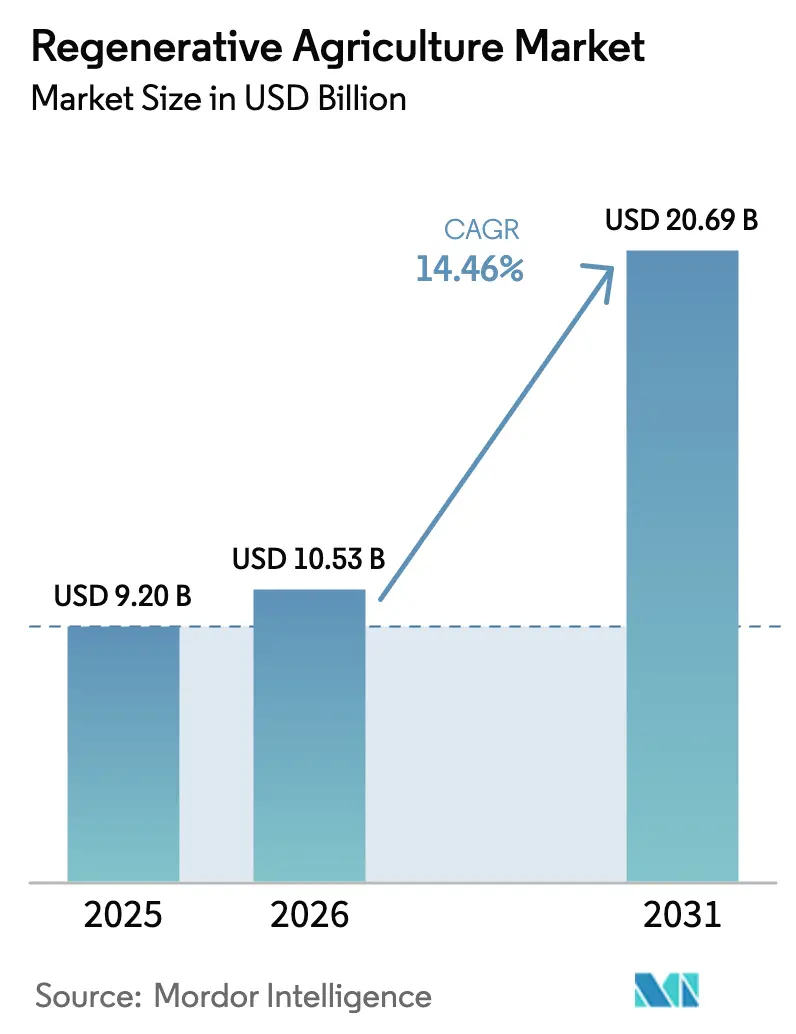

| Market Size (2026) | USD 10.53 Billion |

| Market Size (2031) | USD 20.69 Billion |

| Growth Rate (2026 - 2031) | 14.46% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Regenerative Agriculture Market Analysis by Mordor Intelligence

The Regenerative Agriculture Market size was valued at USD 9.20 billion in 2025 and estimated to grow from USD 10.53 billion in 2026 to reach USD 20.69 billion by 2031, at a CAGR of 14.46% during the forecast period (2026-2031). Rising demand for climate-smart farming, corporate net-zero pledges, and supportive public policy are shifting capital away from conventional input-intensive systems and toward practices that restore soil health, biodiversity while keeping yields steady. Regulatory requirements such as the European Union Nature Restoration Law, which obliges Member States to rehabilitate 20% of degraded ecosystems by 2030, anchor long-term growth for the regenerative agriculture market. Growing integration between digital farm management platforms, remote sensing technologies, and tokenised carbon marketplaces is lowering transaction barriers for smallholders and broadening participation in environmental-service revenue streams. The market’s expansion is also propelled by multibillion-dollar corporate programs that embed regenerative specifications in raw-material contracts, turning once-marginal pilot projects into mainstream sourcing requirements.

Key Report Takeaways

- By practice, soil health management led with 26.02% regenerative agriculture market share in 2025, while agri-pv integration is forecast to advance at a 20.85% CAGR through 2031.

- By application, crop production commanded 45.88% of the regenerative agriculture market size in 2025, whereas carbon sequestration services showed the fastest trajectory at an 17.86% CAGR.

- By input type, biologicals held a 39.36% share of the regenerative agriculture market size in 2025, and sensors and IoT devices are expanding at a 17.42% CAGR.

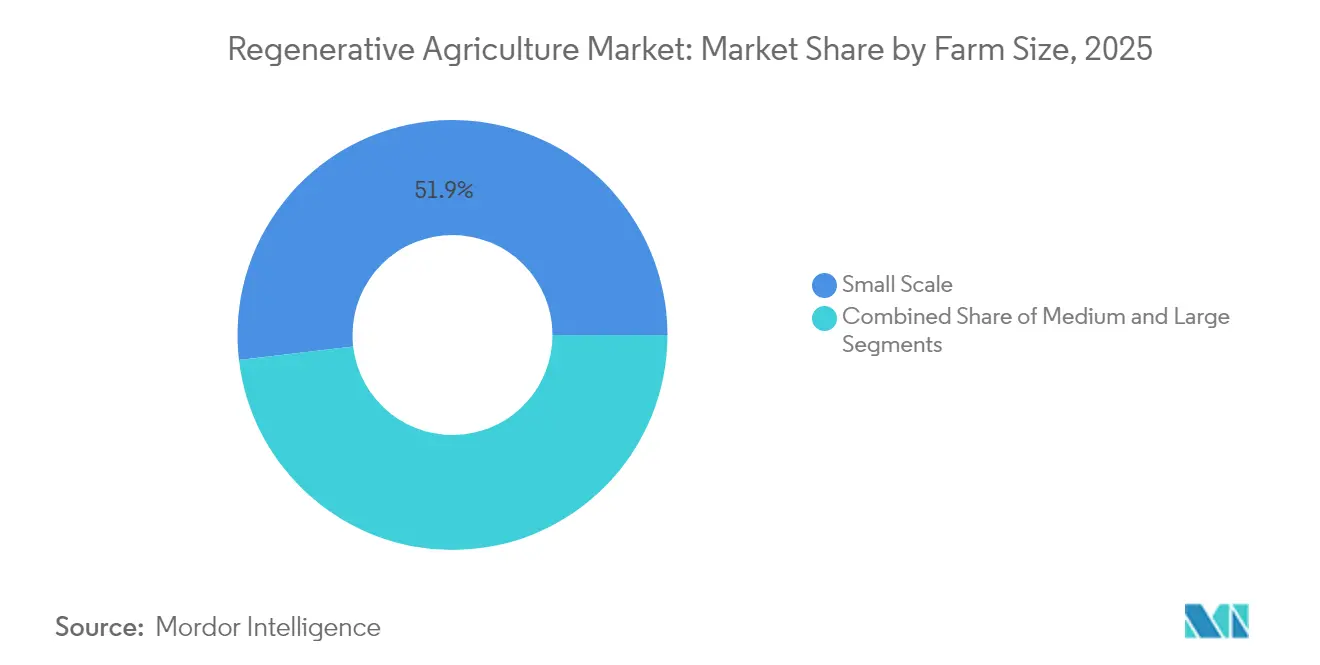

- By farm size, small-scale operations captured a 51.85% share and are growing quickest at 16.21% CAGR.

- By geography, North America accounted for 36.58% of the regenerative agriculture market in 2025, while Africa is the fastest-growing region at 14.86% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Regenerative Agriculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer demand for sustainable food | +3.2% | Global, strongest in North America and EU | Medium term (2-4 years) |

| Corporate pledges and carbon-neutral supply chains | +4.1% | Global, concentrated in multinational value chains | Short term (≤2 years) |

| Government incentives for soil-health practices | +2.8% | North America and EU, emerging in Asia-Pacific | Medium term (2-4 years) |

| Climate-change mitigation and adaptation pressure | +2.4% | Global, acute in climate-vulnerable regions | Long term (≥4 years) |

| Agri-PV dual-use land monetization | +1.6% | Europe and North America, expanding to Asia-Pacific | Long term (≥4 years) |

| Tokenized carbon-credit marketplaces | +1.4% | Global, led by developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Demand for Sustainable Food

Consumer willingness to pay price premiums for responsibly sourced ingredients has moved from niche retailers to mainstream chains, prompting 63% of surveyed food companies to mention regenerative agriculture in public sustainability roadmaps. Nestlé SA alone committed CHF 1.2 billion (USD 1.49 billion) through 2025 to source half of priority raw materials from regenerative farms by 2030, pivoting procurement teams toward suppliers with verifiable soil-health outcomes[1]Nestlé S.A., “Nestlé Accelerates Regenerative Agriculture,” nestle.com. This new pull factor rewards growers who can document ecological benefits alongside crop volumes, raising the profile of carbon-positive grains and livestock. As brand owners turn environmental metrics into shelf labels, regenerative practices shift from a value-added niche to a baseline market expectation, giving early-adopting regions a first-mover advantage. For growers, demand certainty linked to premium contracts shortens payback cycles and de-risks capital outlays for cover-cropping or reduced-tillage programs.

Corporate Pledges and Carbon-Neutral Supply Chains

Food and beverage multinationals have collectively pledged to transition millions of acres, creating hard procurement triggers that cascade through supplier tiers. PepsiCo targets 7 million acres, backed by USD 216 million, while Mars collaborates with grain aggregators to shift 1 million acres by 2030. Because some growers supply multiple brands, acreage-based mandates propagate rapidly, multiplying demand for soil-health services and digital verification. Tight reporting cycles imposed by corporate ESG (environmental, social, and governance) teams bring near-term cash incentives, propelling the regenerative agriculture market during the forecast window. Dedicated corporate funds also finance transition costs, lessening the credit-access barrier that stalls adoption in traditional subsidy regimes.

Government Incentives for Soil-Health Practices

The USDA’s USD 3.1 billion partnerships for Climate-Smart Commodities program pivots federal payments from practice-based to outcome-based structures, rewarding verified improvements in soil carbon and water quality. In Europe, 25% of Common Agricultural Policy direct payments now flow into eco-schemes aligned with regenerative metrics, while 40% of the overall budget carries explicit climate relevance. Denmark pairs livestock-methane taxation with on-farm support, signaling a shift toward comprehensive ag-climate packages. These policy shifts close the revenue gap that farmers face during multi-year transition periods, stimulating equipment upgrades and expanding advisory markets. Outcome-linked public incentives also boost investor confidence in soil-carbon projects by anchoring floor prices for verified tonnage.

Climate-Change Mitigation and Adaptation Pressure

Agriculture generates 22% of anthropogenic emissions, making regenerative methods central to national climate strategies. Large-scale cover-crop datasets indicate annual emission reductions of 1.29 metric tons CO₂e per hectare, verified across more than 550,000 hectares in Indigo Ag’s monitoring program. Parallel adaptation benefits include yield increases of up to 300% on degraded soils, driven by improved water retention and root structure. As extreme weather escalates, growers seek resilient rotations and diversified income sources from ecosystem service credits, reinforcing the growth loop for the regenerative agriculture market. Financial institutions are beginning to treat soil-carbon gains as risk mitigants in loan underwriting, reducing interest rates for verified projects.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront transition and certification costs | −2.8% | Global, pronounced in developing markets | Short term (≤2 years) |

| Limited farmer awareness and skills | −1.9% | Developing regions and underserved rural areas | Medium term (2-4 years) |

| Fragmented monitoring, reporting and verification standards | −1.2% | Global, enabling regulatory arbitrage | Medium term (2-4 years) |

| Soil-biome data-ownership disputes | −0.8% | Developed markets subject to data-privacy law | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Upfront Transition and Certification Costs

Capital outlays of EUR 2,000-5,000 (USD 2,282.64 - 5,706.60) per hectare and payback periods of nearly nine years deter adoption when subsidies target operational expenses rather than conversion costs[2]World Business Council for Sustainable Development, “OP2B Five-Year Report,” wbcsd.org. Certification fees add procedural complexity, particularly for smallholders who lack a credit history or collateral. Although transition-finance pilots and shared-risk platforms are emerging, their scale remains insufficient relative to the USD 250-430 billion annual funding gap identified for global regenerative transitions. Without larger anchor funds or public-private guarantees, cost hurdles will cap near-term acreage growth, especially in regions with limited collateral lending.

Limited Farmer Awareness and Skills

The shift from input-intensive monocultures to biology-based systems demands new knowledge of soil microbial dynamics, multispecies rotations, and data-driven grazing plans. Peer-to-peer learning networks outperform traditional extension models yet remain patchy. Only 27% of U.S. farms had adopted precision agriculture tools by 2023, despite nearly USD 200 million in federal assistance since 2017. In sub-Saharan Africa and South Asia, shortages of agronomists slow the diffusion of best practices, especially where literacy rates limit the uptake of digital modules. Start-up platforms that embed agronomic tips into vernacular audio are gaining traction. Yet, scaling such services requires upgrades to telecom and power infrastructure. Unless training ecosystems expand swiftly, knowledge gaps will continue to constrain the regenerative agriculture market in emerging economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Practice: Dual-Revenue Systems Accelerate Adoption

Soil Health Management captures 26.02% of the regenerative agriculture market in 2025, anchoring its primacy in both arable and pastoral systems. Growers prioritize practices like cover-cropping, reduced tillage, and compost incorporation because these actions deliver measurable gains in soil organic matter that translate into higher carbon credit issuance. At the other end of the growth spectrum, Agri-PV Integration advances at a 20.85% CAGR, reflecting surging land-optimization projects that produce food and power simultaneously.

Yield-neutral solar layouts and guaranteed long-term feed-in tariffs make Agri-PV attractive even in regions with low subsidy support, a trend that elevates the overall regenerative agriculture market size for energy-crop hybrids. Water and Nutrient Management practices post steady growth, supported by municipal restrictions on fertilizer run-off and irrigation quotas. Livestock Grazing Management and Agroforestry show regional variance, expanding faster in land-abundant geographies where silvopastoral systems match cultural norms and property tenure. Biodiversity Enhancement garners attention through pollinator corridors and integrated pest management rules in the EU eco-scheme framework.

By Application: Environmental Services Outpace Staple Crops

Crop Production preserved 45.88% of the regenerative agriculture market size in 2025, sustaining dominance due to its direct breadbasket role. Meanwhile, carbon sequestration services grow at an 17.86% CAGR as buyers chase verifiable offsets to meet science-based targets. The issuance of 296,662 metric tons CO₂e soil credits from a single 553,743-hectare project demonstrates scalable monetisation absent in previous compliance eras.

Livestock grazing conversions improve methane intensity per kilogram of protein while raising pasture resilience. Forestry and agroforestry applications unlock tree-crop revenue and longer-term carbon premiums, positioning them as strategic rotations for landholders facing deforestation moratoria. Niche segments like agro-tourism and ecosystem-services trading diversify and grow cash flows, buffering price shocks in commodity markets and enlarging regenerative agriculture market opportunities across rural communities.

By Input Type: Biologics and Sensors Reshape Spend Patterns

Biological inputs held 39.36% of 2025 spending, propelled by growing bans on contentious chemistries and stronger supermarket residue tests. Precision probes feed yield-forecast models and soil-moisture dashboards, allowing site-specific application that underwrites biological efficacy. On the other hand, sensors and IoT devices are expanding at a 17.42% CAGR through 2031.

Software advisory suites integrate satellite imagery, sensor data, and ledger proofs to produce auditable carbon ledgers, weaving digital layers into the regenerative agriculture market. Equipment manufacturers are retrofitting planters for minimal-disturbance seeding, and compost inoculant suppliers now bundle microbial assays to substantiate activity scores.

By Farm Size: Smallholders Anchor Inclusive Growth

Holdings below 50 hectares occupy a 51.85% slice of the regenerative agriculture market and expand the fastest at 16.21% CAGR as cooperative finance schemes and mobile apps aggregate dispersed parcels. Programs such as Cargill’s RegenConnect enrol over 1 million acres across 1,500 farmers, proving the viability of smallholder aggregation models. Medium-sized farms act as bridge adopters, often piloting technologies that later diffuse into smaller plots.

Large farms still dominate headline acreage conversions due to capital access and vertically integrated supply relationships, yet their growth lags behind smallholder cohorts because base adoption already sits higher. By tailoring verification costs to parcel size, tokenised credit pools lower barriers and sustain inclusive expansion within the regenerative agriculture market.

Geography Analysis

North America generated 36.58% of global revenue in 2025, underpinned by the USDA’s USD 3.1 billion Climate-Smart Commodities initiative that finances outcome-based soil and livestock protocols. Mature extension networks, widespread precision-tech use, and advanced carbon marketplaces allow growers to monetize environmental outputs rapidly. Corporate targets, such as General Mills’ plan to source from 1 million regenerative acres by 2030, create a reliable downstream pull.

Africa posts the highest regional CAGR, nearly 14.86%, buoyed by projections that regenerative methods could add USD 15 billion in annual Gross Value Added and create five million jobs by 2030. Kenyan and Ugandan coffee pilots have lifted yields by 30% and farm income by 62%, validating the smallholder business case.

Asia-Pacific blends high technology penetration with acute biodiversity loss exposure. Several surveyed executives report active regenerative programs driven by policy signals in Australia, Japan, and India. With 63% of regional GDP at risk from ecosystem decline, governments frame regenerative farming as an economic-stability lever, projecting USD 19.5 trillion in impact under nature-positive scenarios. China’s push for green consumption and India’s digital-ag stack accelerate data-ready acreage enrollment, enlarging the regenerative agriculture market footprint across diverse climatic zones.

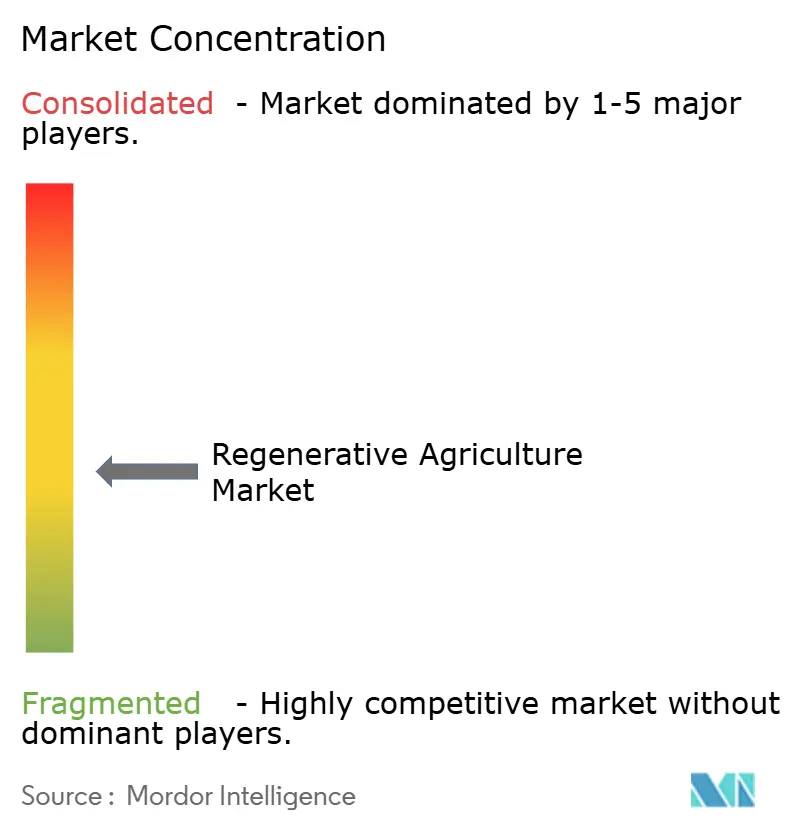

Competitive Landscape

The regenerative agriculture market includes several key players driving innovation and growth. Indigo Ag focuses on soil-carbon platforms that combine satellite analytics, microbial assays, and brokerage services. Bayer emphasizes the integration of biologics with digital scouting tools to enhance agricultural practices. Syngenta collaborates with partners to develop biological solutions, such as insecticides, aimed at improving sustainability in farming.

Strategic moves center on ecosystem platforms rather than individual product launches. Bayer bundles input sales with Climate FieldView analytics, offering outcome assurance to corporate buyers. Syngenta’s biological alliances fast-track pipeline diversity without lengthy in-house research and development. Emerging firms like Terramera spin out soil-enrichment subsidiaries, supported by USD 6 million seed rounds that target data-driven microbial cocktails. Aggregators such as Soil Capital secure ISO-validated carbon methodologies and pair them with transition loans, a model suited for European smallholders.

Mergers and Acquisitions appetite is building as incumbents seek integrated toolkits that span inputs, advisory, and verification. While no single operator tops 15% share, platform convergence hints at future clustering once protocols standardize. For now, niche specialists flourish, anchoring a dynamic yet unconsolidated regenerative agriculture market that rewards innovation and regional customization.

Regenerative Agriculture Industry Leaders

Nestle SA

Indigo Ag, Inc.

General Mills Inc,

Syngenta

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Cargill surpassed 1 million enrolled acres in RegenConnect, extending coverage across 24 U.S. states and 15 countries.

- October 2024: Mars launched partnerships with ADM, The Andersons, Riceland Foods, and Soil and Water Outcomes Fund to transition 150,000 acres in its North American pet-food supply chain before scaling globally.

- May 2024: BioCarbon Cert released tokenization guidelines to standardize blockchain-based credit issuance.

- February 2024: Syngenta and Lavie Bio agreed to co-develop biological insecticidal solutions using AI-enabled strain optimization.

Global Regenerative Agriculture Market Report Scope

Regenerative agriculture is a sustainable farming approach focused on restoring and enhancing the health of ecosystems. It emphasizes practices that regenerate soil health, increase biodiversity, improve water cycles, and enhance ecosystem resilience. The method aims to sequester carbon, reduce greenhouse gas emissions, and create healthier, more productive agricultural systems.

The Regenerative Agriculture Market is segmented by Application into Crop Protection, Livestock Grazing, Forestry, and Others. By Type into Soil Health Management, Water Management, Biodiversity Enhancement, Nutrient Management, Livestock Grazing Management, and Others. And by Geography into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The report offers the market size and forecasts in terms of value (USD) for all the above segments.

| Soil Health Management |

| Water Management |

| Biodiversity Enhancement |

| Nutrient Management |

| Livestock Grazing Management |

| Agroforestry |

| Agri-PV Integration |

| Others |

| Crop Production |

| Livestock Grazing |

| Forestry |

| Carbon Sequestration Services |

| Others |

| Biologicals |

| Seeds and Cover Crops |

| Sensors and IoT Devices |

| Software and Advisory Services |

| Equipment and Machinery |

| Others |

| Small-scale (less than 50 ha) |

| Medium (50-500 ha) |

| Large (greater than 500 ha) |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Thailand | |

| Rest of Asia-Pacific | |

| Middle East | UAE |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Practice | Soil Health Management | |

| Water Management | ||

| Biodiversity Enhancement | ||

| Nutrient Management | ||

| Livestock Grazing Management | ||

| Agroforestry | ||

| Agri-PV Integration | ||

| Others | ||

| By Application | Crop Production | |

| Livestock Grazing | ||

| Forestry | ||

| Carbon Sequestration Services | ||

| Others | ||

| By Input Type | Biologicals | |

| Seeds and Cover Crops | ||

| Sensors and IoT Devices | ||

| Software and Advisory Services | ||

| Equipment and Machinery | ||

| Others | ||

| By Farm Size | Small-scale (less than 50 ha) | |

| Medium (50-500 ha) | ||

| Large (greater than 500 ha) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| Middle East | UAE | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the regenerative agriculture market size in 2026?

The Regenerative Agriculture Market is valued at USD 10.53 billion in 2026 and is projected to reach USD 20.69 billion by 2031, growing at a 14.46% CAGR.

Which region holds the largest share of the regenerative agriculture market?

North America leads with about 36.58% market share in 2025, supported by sizeable USDA climate-smart funding and advanced carbon-credit infrastructure.

Which segment is expanding the fastest within the market?

Agri-PV Integration is the fastest-growing practice segment, projected to advance at a 20.85% CAGR through 2031.

How significant are carbon-sequestration services to future growth?

Carbon Sequestration Services are forecast to rise at an 17.86% CAGR, reflecting strong demand for verified soil-carbon credits.

Page last updated on: