Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

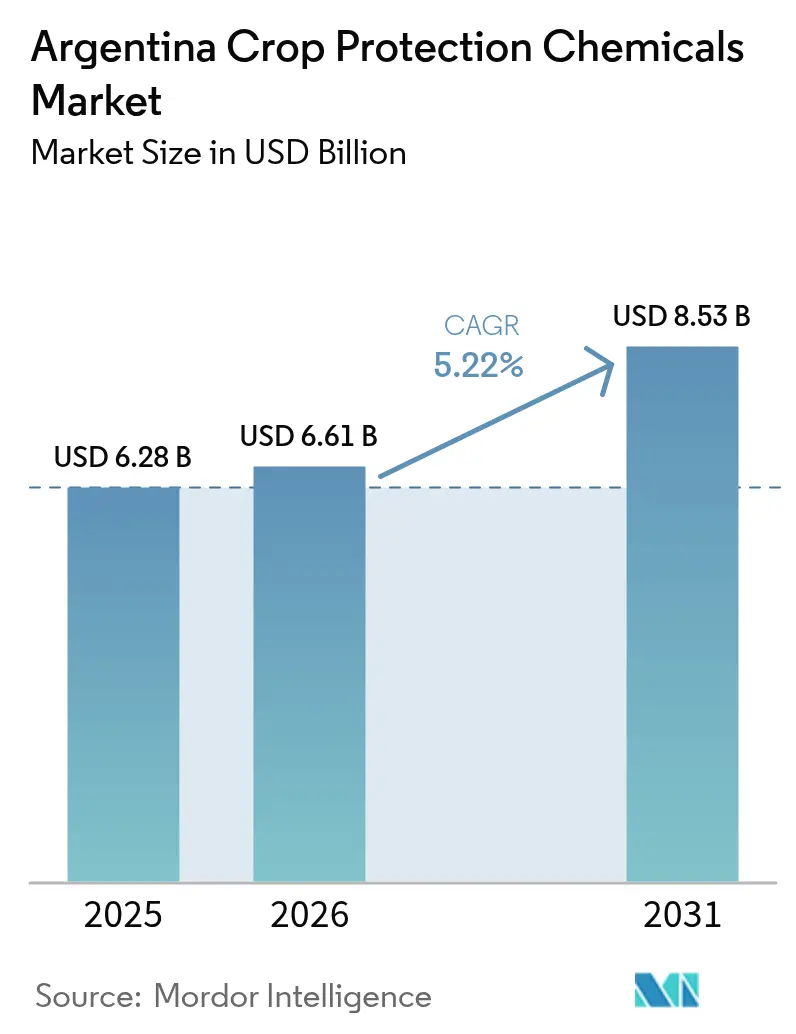

| Base Year Market Size (2025) | USD 6.28 Billion |

| Market Size (2026) | USD 6.61 Billion |

| Market Size (2031) | USD 8.53 Billion |

| Growth Rate (2026 - 2031) | 5.22% CAGR |

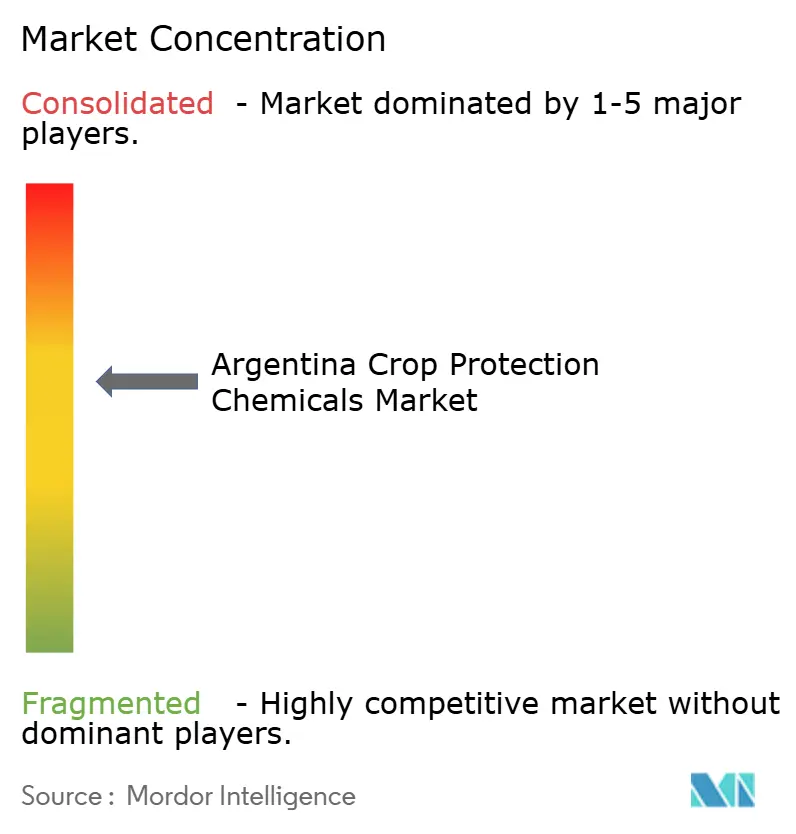

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Crop Protection Chemicals Market Analysis by Mordor Intelligence

The Argentina crop protection chemicals market size in 2026 is estimated at USD 6.61 billion, growing from 2025 value of USD 6.28 billion with 2031 projections showing USD 8.53 billion, growing at 5.22% CAGR over 2026-2031. Rising soybean and maize acreage, intensifying herbicide-resistant weed pressure, and regulatory modernization under SENASA keep demand on a steady climb. Currency volatility after the December 2023 peso devaluation lifted import costs for active ingredients, nudging growers toward locally produced or generic formulations. Momentum also comes from stacked-trait biotech seeds that pair well with premium herbicide packages, plus growing adoption of drone-based variable-rate spraying that reduces waste yet raises formulation specificity. Still, structural headwinds such as counterfeit pesticide inflows and 1,000-meter aerial-spray buffer zones in Santa Fe and Buenos Aires provinces temper upside potential.

Key Report Takeaways

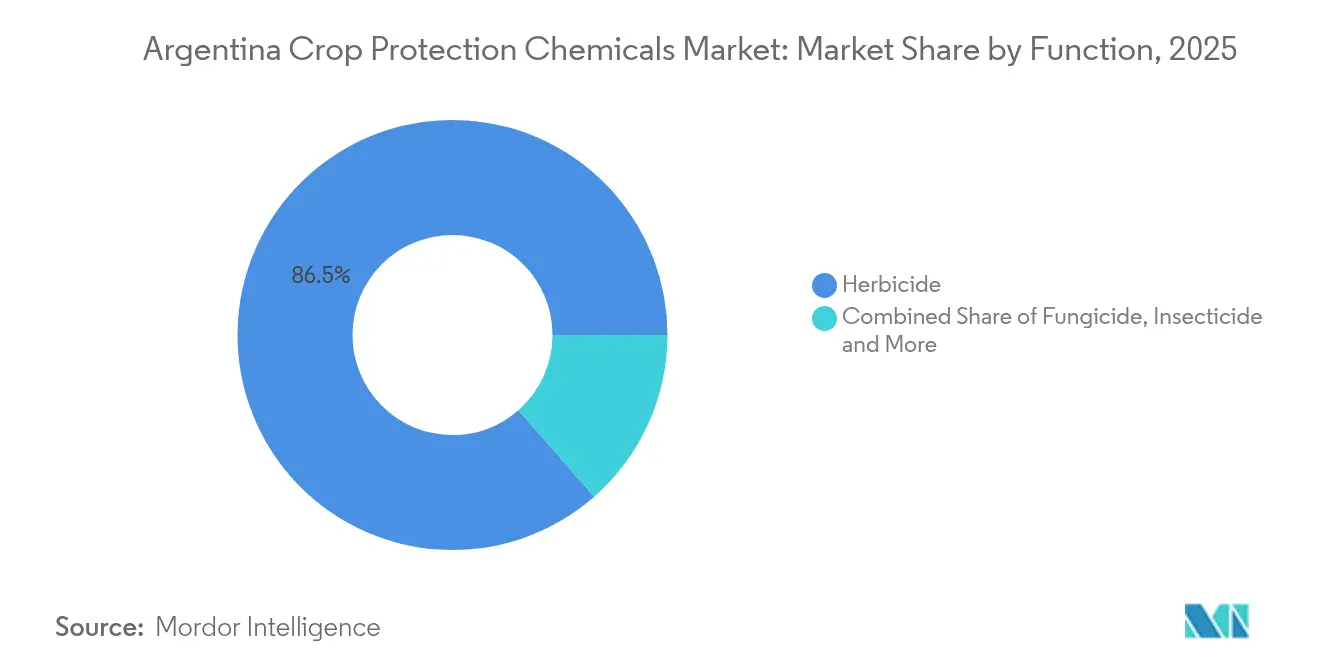

- By function, herbicide led with 86.45% Argentina crop protection chemicals market share in 2025 and are projected to grow at a 5.29% CAGR to 2031.

- By application mode, soil treatment accounted for a 46.60% share of the Argentina crop protection chemicals market size in 2025, and is set to record the fastest 5.55% CAGR through 2031.

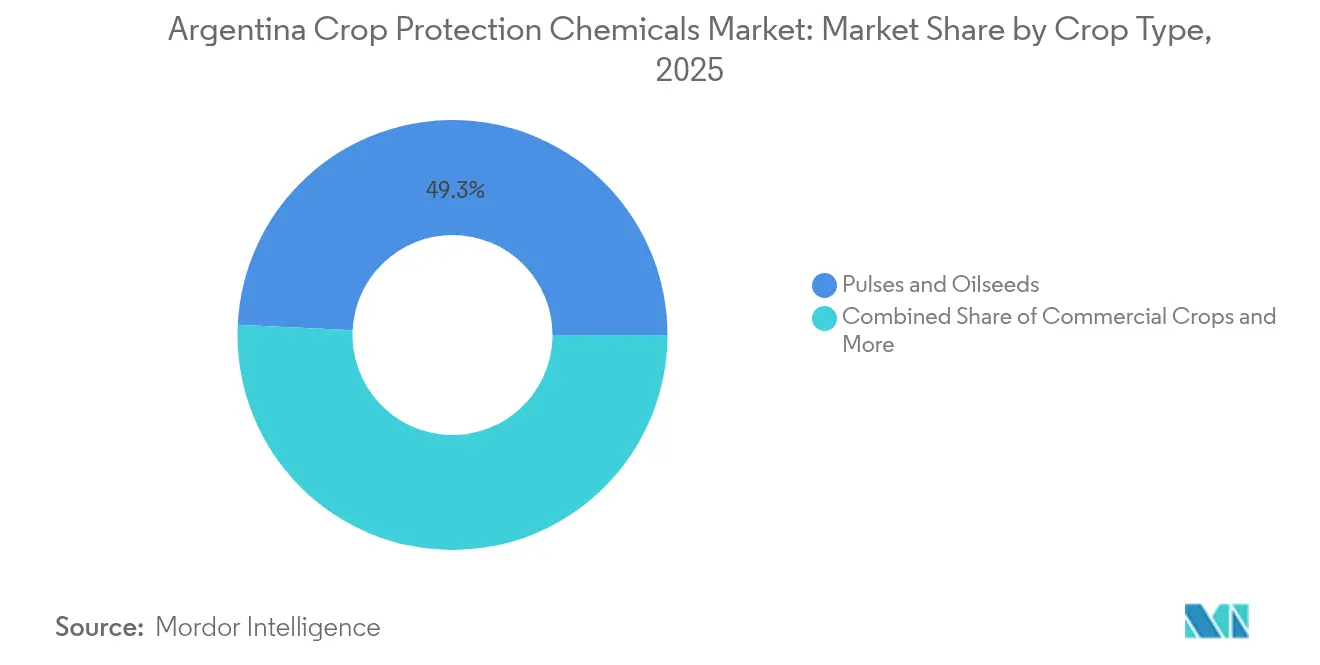

- By crop type, pulses and oilseeds captured 49.25% of the Argentina crop protection chemicals market in 2025 while grains and cereals are advancing at a 5.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Crop Protection Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding soybean and maize acreage | +1.8% | Buenos Aires, Córdoba, Santa Fe | Medium term (2-4 years) |

| Herbicide-resistant weed proliferation | +1.5% | Pampas and northern expansion zones | Long term (≥ 4 years) |

| Government push for Good Agricultural Practices | +0.9% | Nationwide | Medium term (2-4 years) |

| Growth of biotech stacked-trait seeds | +1.2% | Core soybean and maize belts | Medium term (2-4 years) |

| Regenerative agriculture bioherbicide rotation | +0.6% | Early adoption in Buenos Aires and Córdoba | Long term (≥ 4 years) |

| Drone-based variable-rate spraying services | +0.4% | Technology hubs and adjoining rural areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Soybean and Maize Acreage

Soybean plantings reached 16.8 million hectares in the 2024-25 campaign, a 2.1% rise from the prior year, while maize stabilized at 6.2 million hectares despite macroeconomic strain [1]USDA Foreign Agricultural Service, “Argentina: Oilseeds and Products Annual,” FAS.USDA.gov . Expansion into marginal northern lands such as Santiago del Estero and Chaco introduces diverse weed populations that demand multilayered herbicide programs. Farmers working poorer soils apply residual actives before seeding, then follow with post-emergence mixtures once crops establish. La Niña weather windows amplify this effect because short-term moisture lets growers risk sowing in drier territory, spawning demand surges beyond baseline growth. Dealers in frontier provinces report herbicide volumes per hectare sitting 15-20% above Pampas averages as growers hedge against uncertain control windows. The acreage story, therefore, feeds a structurally larger herbicide envelope, sustaining the Argentina crop protection chemicals market even when commodity prices soften.

Herbicide-Resistant Weed Proliferation

Glyphosate resistance now spans 12 weed species, including Palmer amaranth across 4.2 million hectares and johnsongrass on 2.8 million hectares [2]Instituto Nacional de Tecnología Agropecuaria, “Herbicide Resistance Management in Argentine Agriculture,” Argentina.gob.ar. Growers routinely tank-mix glyphosate with dicamba, 2,4-D, or saflufenacil, lifting chemical costs 35-45% per hectare compared with single-mode programs. Pre-emergence agents such as atrazine and metribuzin posted 18% volume gains in 2024 as integrated weed management became mainstream. Resistance also accelerates adoption of new modes of action awaiting SENASA clearance, including HPPD inhibitors. The shift anchors premium positions for manufacturers able to bundle multiple chemistries at farm-gate. For distributors, resistance translates into a predictable upsell pathway as each new harvest season brings fresh weed escapes and calls for stronger or additional products. Consequently, persistent resistance adds tangible thickness to revenue pipelines, reinforcing the upward arc of the Argentina crop protection chemicals market.

Government Push for Good Agricultural Practices

SENASA codified Good Agricultural Practices under Resolution 302/2024, compelling farms to document rotation and tank-mix discipline, plus certify operator training. Compliance audits funnel growers toward selective herbicides with lower environmental load yet higher price tags. Buenos Aires extends tax credits for GAP-verified operations, while Córdoba offers agronomic coaching subsidies, creating an incentive patchwork that shapes purchase patterns by province. Because GAP focuses on resistance management, adoption spurs use of soil residuals and biological seed treatments, both commanding 25-30% higher margins than generic foliar sprays. Certified growers also gain smoother access to export channels that impose sustainability scorecards, effectively embedding GAP herbicide regimes into commercial contracts. The rule therefore pulls the Argentina crop protection chemicals market toward more sophisticated chemistries even when total kilograms applied per hectare taper.

Drone-Based Variable-Rate Spraying Services

Drone service acreage expands 25% per year, spurred by lower capital thresholds and recent SENASA approval of broader herbicide labels in Resolution 445/2024 [3]Source: Argentine Association of Precision Agriculture, “Technology Adoption Survey 2024,” Aapresag.org.ar . Operators like AgroFly merge satellite imagery with prescription maps, cutting herbicide use 12-18% yet improving hit rates on dense weed patches. Growers lacking self-owned precision rigs acquire pay-per-hectare packages that include formulation advice, steering product demand toward low-volume, high-concentration formulations optimized for electrostatic spray nozzles. Retail agronomists confirm that drone-friendly 400+ g ai/L glyphosate variants now outsell legacy 360 g ai/L grades in targeted areas. This channel democratizes precision agriculture beyond mega farms, embedding a new tier of differentiated products and sustaining incremental growth for the Argentina crop protection chemicals market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent SENASA registration timelines | -0.8% | Nationwide | Medium term (2-4 years) |

| Currency volatility inflating import costs | -1.2% | Nationwide | Short term (≤ 2 years) |

| Civil-society lawsuits on aerial-spray buffers | -0.6% | Buenos Aires and Santa Fe | Long term (≥ 4 years) |

| Counterfeit pesticide trade expansion | -0.4% | Border provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent SENASA Registration Timelines

New active ingredients traverse an 18-24-month registration path versus Brazil’s 12 months, widening technology gaps and slowing local adoption. Resolution 1081/2024 added advanced residue analysis, piling USD 150,000–200,000 extra onto dossiers and extending reviews another 4-6 months. Generic firms, notably Chinese and Indian, face added hurdles meeting equivalence rules under Resolution 694/2024, locking out lower-cost options that could ease grower budgets. SENASA’s evaluator pool of 45 professionals processes more than 200 annual applications, creating an inherent pipeline bottleneck. Delays push farms back toward dated chemistries, elevating resistance risk and forcing larger dose rates to achieve control, which in turn inflates per-hectare spend without advancing efficacy. The backlog may only ease with significant staffing and digitalization investments, neither of which appears imminent, thereby moderating the Argentina crop protection chemicals market growth trajectory.

Civil-Society Lawsuits on Aerial-Spray Buffers

Court rulings in Santa Fe and Buenos Aires instituted 1,000-meter no-spray rings around populated areas, removing roughly 800,000 ha from aerial application coverage. Ground rigs must take over, driving up operational costs and often requiring narrower nozzle arrays that slow fieldwork. Small parcels that previously relied on custom aerial services now face equipment affordability issues, risking under-application or switching to less effective manual methods. Environmental groups plan copycat suits in Córdoba and Entre Ríos, indicating the buffer model may spread. Chemical distributors that specialized in aerial-optimized formulations see volume contractions and must pivot to backpack or tractor-spray segments. Uncertainty regarding future legal boundaries keeps aerial service investments on hold, dampening certain product category sales and weighing on the Argentina crop protection chemicals market outlook.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Herbicide Command Market Leadership

Herbicide represented 86.45% of 2025 revenue, reflecting a nationwide reliance on no-till cultivation that substitutes chemistry for mechanical weed disruption. The Argentina crop protection chemicals market size for herbicide is projected to grow at a 5.29% CAGR, supported by stacked-trait seeds that broaden application windows. Pre-emergence use intensifies as growers proactively fight resistant weeds with atrazine, metribuzin, and pendimethalin cocktails. Insecticides hold close to 8.10% share, driven by escalating fall armyworm pressure on maize, whereas fungicides claim just 3.65%, centered in wheat zones. Nematicide and molluscicide use remains marginal but vital in localized outbreaks.

Momentum in herbicide also ties to regulatory approvals of new modes such as HPPD inhibitors, which promise rotational relief in resistance programs. Yet dependence on a single category heightens vulnerability if glyphosate or related actives face legal curbs. Multinationals hedge by introducing dual-mode premixes that deliver efficacy at lower per-ai rates, sustaining revenue while appeasing stewardship guidelines. Consequently, herbicide will stay the revenue anchor of the Argentina crop protection chemicals market even as adjacent categories search for incremental ground.

By Application Mode: Soil Treatment Drives Precision

Soil treatments held a 46.60% share in 2025 as farmers embraced residual control tactics that limit early weed flushes and cut in-season labor. This application mode's 5.55% CAGR through 2031 benefits from increasing adoption of residual herbicides like atrazine, metribuzin, and pendimethalin that provide extended weed control. The Argentina crop protection chemicals market share for soil treatments benefits from the financial logic of one-and-done passes amid rising diesel and labor costs. Chemistries such as atrazine and flumioxazin deliver season-long suppression, reducing follow-up sprays. Foliar applications still account for about 35.40% of value, mainly in corrective post-emergence and fungicide passes. Seed treatments capture roughly 12.30% and enjoy double-digit growth as biological coatings gain GAP endorsements.

Chemigation remains niche but expands in northwestern irrigated maize belts where pivot systems allow efficient distribution. Fumigation and aerial fogging stay confined to specialty crops because of cost and regulation. Soil treatment’s lead aligns with GAP mandates favoring preventative programs that minimize drift and off-target exposure, reinforcing its position as the precision cornerstone of the Argentina crop protection chemicals market.

By Crop Type: Oilseeds Anchor Market Demand

Pulses and oilseeds, dominated by soybeans, secured 49.25% of 2025 revenue, a function of 20.5 million ha reliant on intensive herbicide schedules. Grains and cereals form the fastest growing subsegment at a 5.56% CAGR, lifted by maize and wheat acreage gains that diversify farm rotations. Commercial crops such as cotton and sugarcane combine for about 15.10% share, requiring bespoke insect and weed solutions in hotter northern climates.

Fruit and vegetable hectarage is limited yet chemically intensive owing to strict residue tolerances from export buyers, driving premium formulation sales. Turf and ornamental uses stay marginal, linked to urban market size rather than agronomic factors. Dependence on soybean profitability poses cyclical risk; however, diversification into grains may smooth revenue curves while enlarging the Argentina crop protection chemicals market size across crop types.

Geography Analysis

Three provinces dominate demand, with Buenos Aires responsible for a significant share of market value in 2025 due to its 6.2 million hectares of soybeans and 2.1 million hectares of maize clustered near export ports. Córdoba adds 17.60% share through high-adoption of no-till systems that prize pre-emergent herbicides. Santa Fe contributes 11.80% but commands above-average spend per hectare as Palmer amaranth resistance inflates dose rates. The core Pampas thus supplies the bulk of the Argentina crop protection chemicals market and provides early testing grounds for new chemistries.

Northern provinces including Santiago del Estero, Chaco, and Salta log the swiftest expansion, triggered by land conversion under favorable commodity cycles. Soil fertility challenges and tropical weed spectra push chemical intensity upward. Regulatory stringency remains lighter in these areas, giving generic and local players a foothold.

Conversely, tighter enforcement in Pampas regions elevates barrier costs but rewards premium stewardship-aligned brands. Climate oscillations drive regional swings; La Niña years shift activity northward, while El Niño episodes refocus spraying within the heartland, stressing supply chains that must juggle inventory between zones.

Competitive Landscape

Market concentration is moderate with the top five companies holding a significant share of revenue, led by Syngenta Group, followed by Bayer AG, BASF SE, Corteva Agriscience, and FMC Corporation. Syngenta Group leverages local formulation and seed-treatment lines to cushion currency impacts, whereas Bayer AG wrestles with glyphosate litigation headwinds and integration costs. BASF SE and Corteva Agriscience push trait-linked herbicide systems, banking on captive customer bases. Local manufacturer Rizobacter punches above its scale through biologicals and seed treatments favored in GAP certification schemes.

Market disruption emerges from regulatory changes that favor technical equivalence over brand loyalty, enabling generic manufacturers to capture share from premium products through SENASA's streamlined approval processes for equivalent formulations. White-space opportunities exist in biologicals and specialty formulations, segments where regulatory barriers remain lower and farmer willingness to pay premiums persists despite economic pressures.

Local companies like Rizobacter leverage biotechnology expertise to develop niche products for specific regional conditions, while international players focus on defending market share through portfolio optimization and supply chain localization. The competitive landscape increasingly rewards companies that can navigate Argentina's complex regulatory environment while maintaining cost competitiveness during periods of currency instability.

Argentina Crop Protection Chemicals Industry Leaders

BASF SE

Bayer AG

Corteva Agriscience

Syngenta Group

FMC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: Syngenta announced that it received registration in Argentina for two insecticides aimed at controlling the maize leafhopper (‘chicharrita’), the vector of the Spiroplasma pathogen causing “achaparramiento” of maize. The two products are VERDAVIS (a foliar-applied insecticide with PLINAZOLIN technology) and FORTENZA (a seed-treatment insecticide formulation) that target early plant growth stages (e.g., V2) for effective pest control.

- April 2023: Rainbow Agro announced that it expanded its Argentina site by purchasing an additional 6 hectares of land at Ezeiza (Buenos Aires) to boost its local manufacturing capacity. This investment reflects the company’s intent to strengthen production and supply of crop-protection formulations in Argentina’s key agricultural region. The expansion supports its strategic alignment with growing demand for pest- and weed-control solutions in the country’s extensive soybean and grain belt.

- August 2022: BASF and Corteva Agriscience collaborated to provide soybean farmers with the weed control of the future. By working together, BASF and Corteva aim to satisfy farmers' demand for specialized weed control solutions that are distinct from those that are currently available or being developed.

Argentina Crop Protection Chemicals Market Report Scope

Fungicide, Herbicide, Insecticide, Molluscicide, Nematicide are covered as segments by Function. Chemigation, Foliar, Fumigation, Seed Treatment, Soil Treatment are covered as segments by Application Mode. Commercial Crops, Fruits & Vegetables, Grains & Cereals, Pulses & Oilseeds, Turf & Ornamental are covered as segments by Crop Type.Function

| Fungicide |

| Herbicide |

| Insecticide |

| Molluscicide |

| Nematicide |

Application Mode

| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

Crop Type

| Commercial Crops |

| Fruits and Vegetables |

| Grains and Cereals |

| Pulses and Oilseeds |

| Turf and Ornamental |

| Function | Fungicide |

| Herbicide | |

| Insecticide | |

| Molluscicide | |

| Nematicide | |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| Crop Type | Commercial Crops |

| Fruits and Vegetables | |

| Grains and Cereals | |

| Pulses and Oilseeds | |

| Turf and Ornamental |

Market Definition

- Function - Crop Protection Chemicals are apllied to control or prevent pests, including insects, fungi, weeds, nematodes, and mollusks, from damaging the crop and to protect the crop yield.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms