Agricultural Adjuvants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

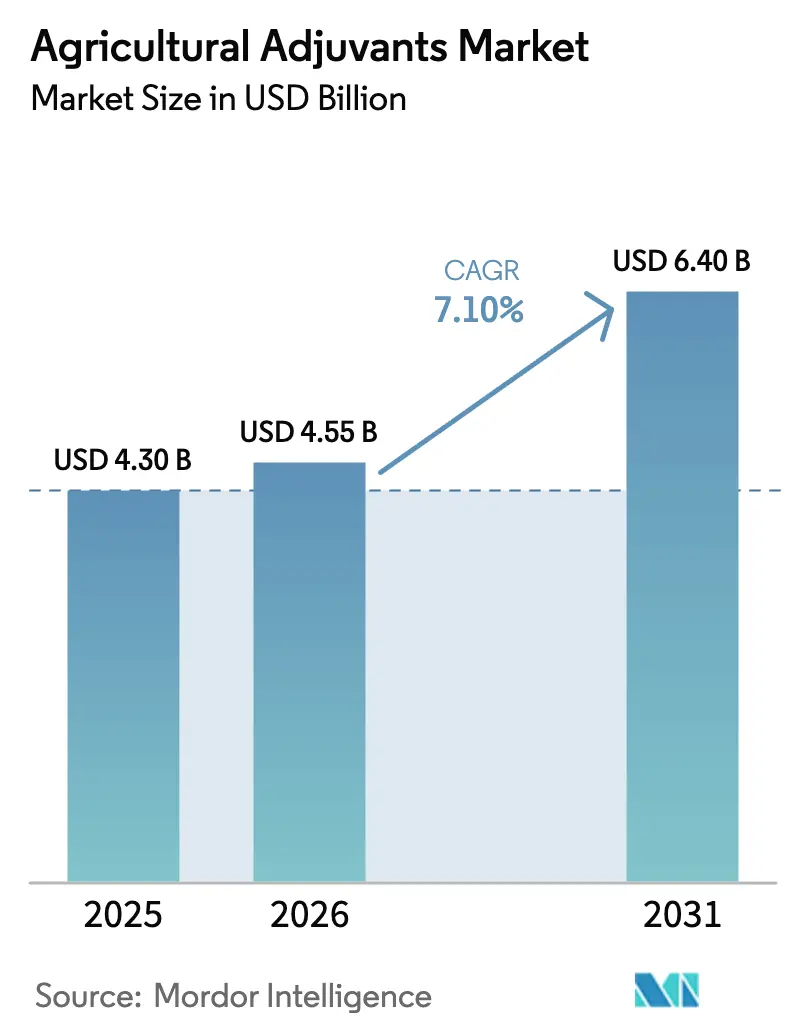

| Market Size (2026) | USD 4.55 Billion |

| Market Size (2031) | USD 6.40 Billion |

| Growth Rate (2026 - 2031) | 7.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

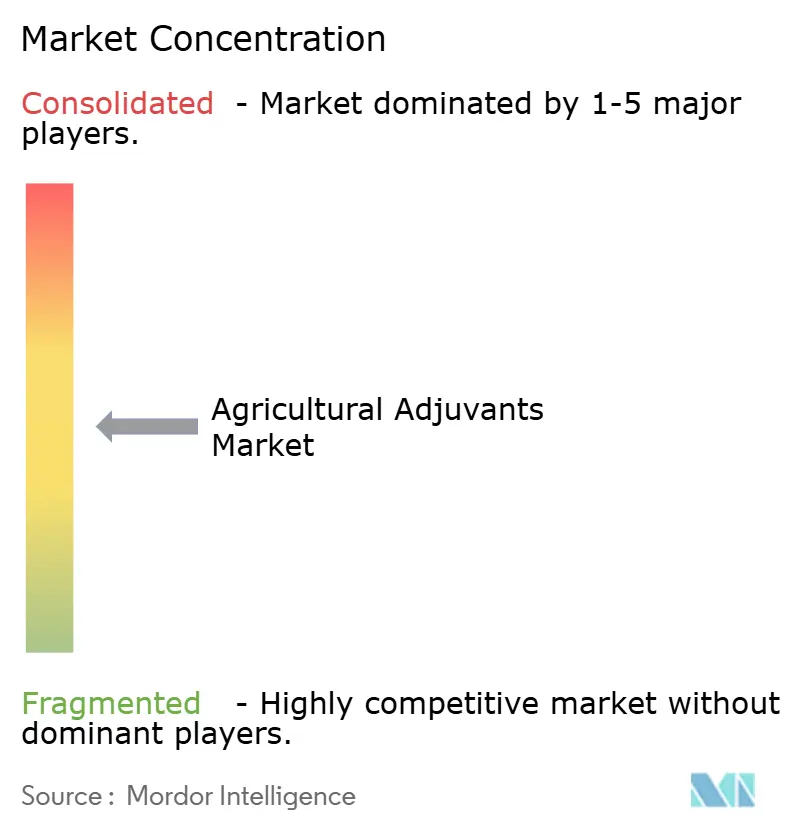

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agricultural Adjuvants Market Analysis by Mordor Intelligence

The agricultural adjuvants market size was valued at USD 4.30 billion in 2025 and is estimated to grow from USD 4.55 billion in 2026 to USD 6.40 billion by 2031, at a CAGR of 7.1% during the forecast period (2026-2031). Rising input costs, stricter spray-drift rules, and the spread of herbicide-tolerant seeds are prompting growers to add precision-engineered surfactants, oils, and drift-control polymers to every tank. Activator adjuvants dominate revenue because most post-emergence herbicides list a specific surfactant on the label, yet utility adjuvants are capturing the fastest incremental growth as unmanned aerial vehicles, variable-rate rigs, and hard-water geographies create fresh use cases. Regional demand is tilting toward Asia-Pacific, where a large fleet of plant-protection drones now spray cereal, cotton, and vegetable fields at ultra-low volumes that require superspreader chemistry to maintain coverage. Carbon-credit programs that pay for reduced pesticide doses also lift adjuvant intensity, because lower active-ingredient rates require higher surfactant loading to sustain control thresholds.

Key Report Takeaways

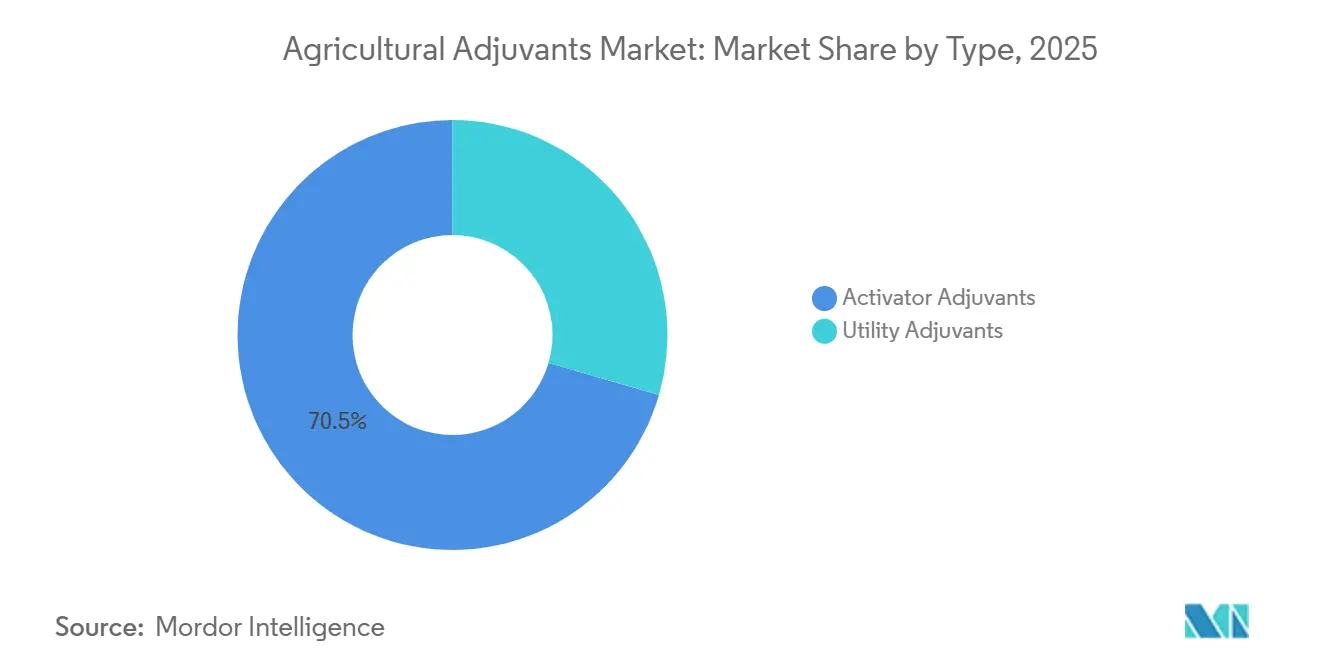

- By type, activator adjuvants were the largest segment, accounting for 70.5% of the agricultural adjuvants market share in 2025, while utility adjuvants are the fastest-growing segment, forecast to post an 8.4% CAGR through 2031.

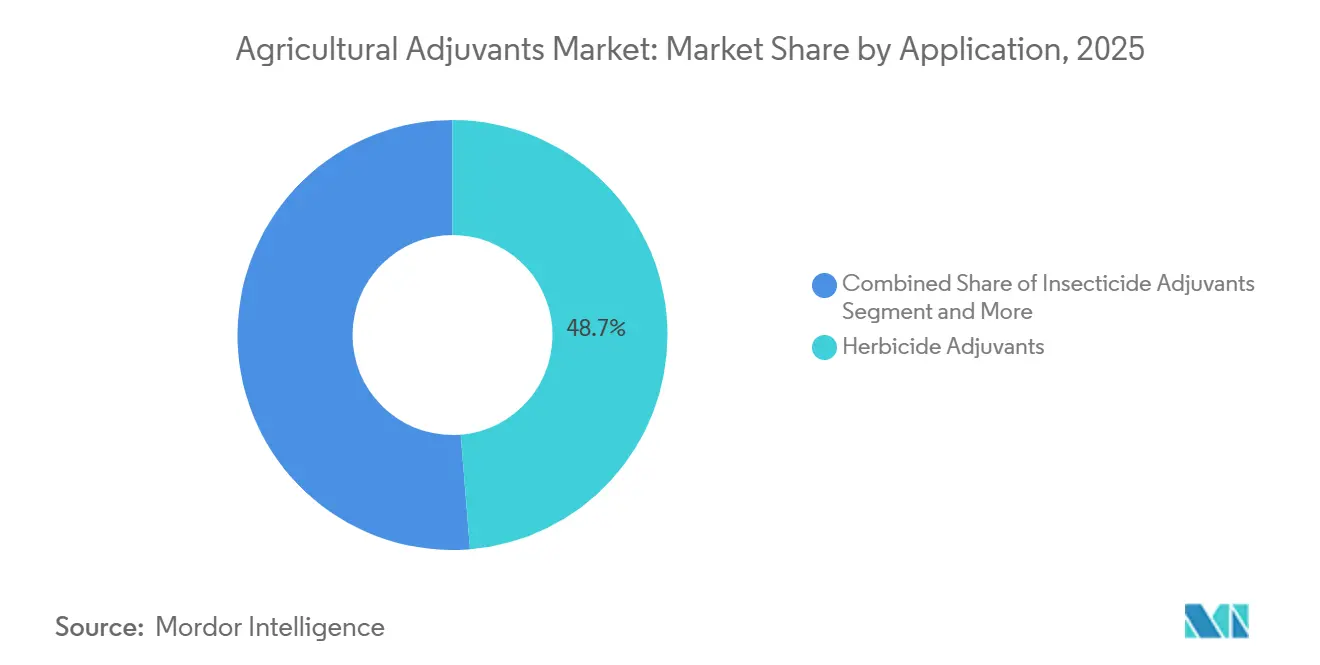

- By application, herbicide adjuvants were the largest segment, commanding 48.7% of the agricultural adjuvants market in 2025, whereas insecticide adjuvants were the fastest-growing segment, projected to grow at a 7.9% CAGR to 2031.

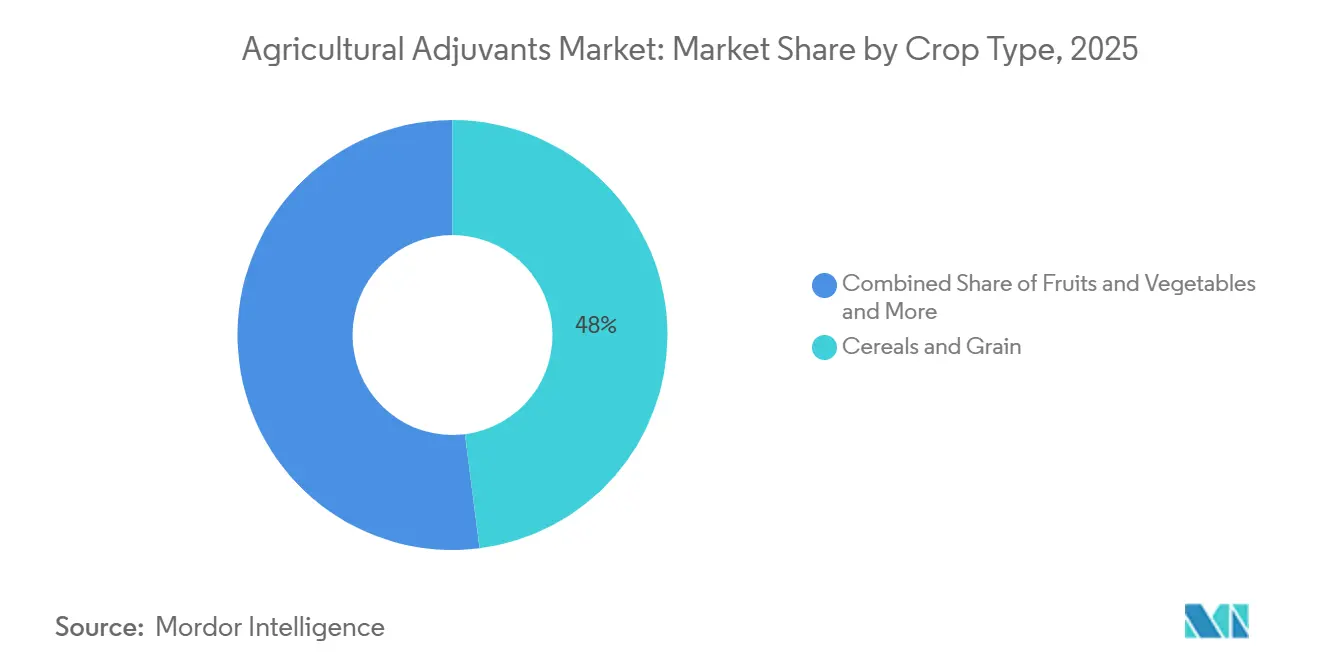

- By Crop Type, Cereals and grains were the largest segment, accounting for 48% of the agricultural adjuvants market in 2025, while fruits and vegetables were the fastest-growing segment, with a 9.2% CAGR through 2031.

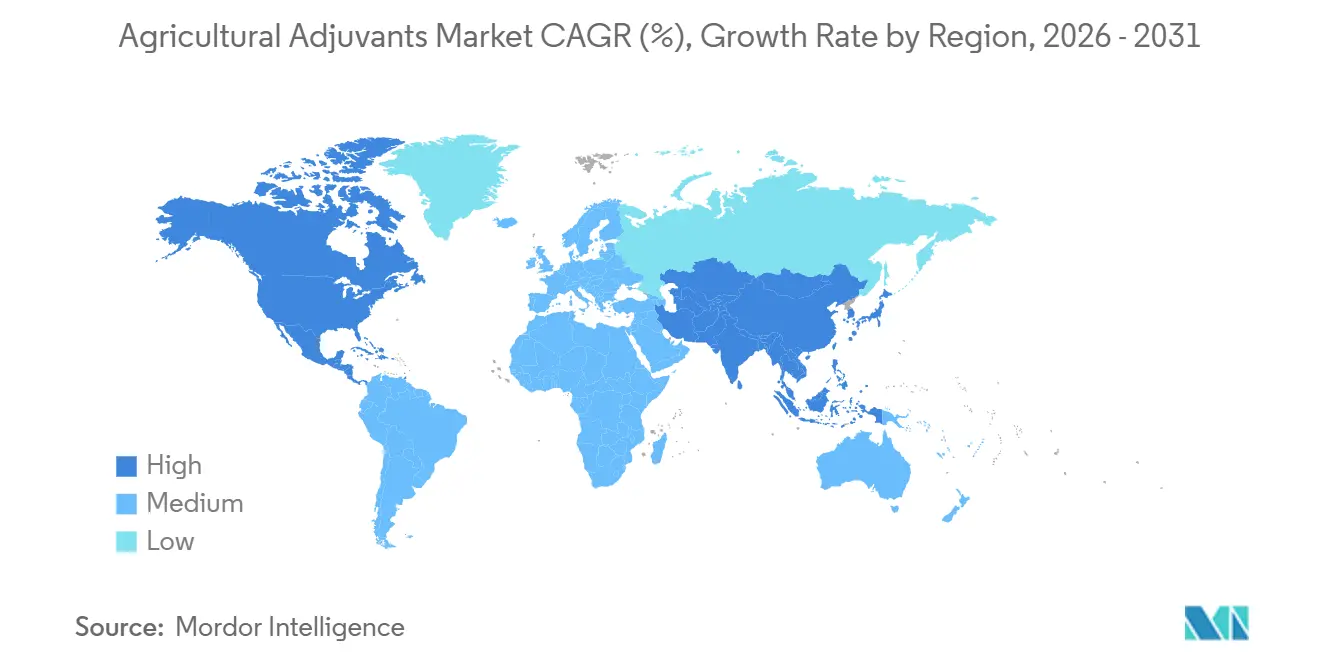

- By geography, North America was the largest region, holding 35.4% of the agricultural adjuvants market size in 2025. Asia-Pacific is the fastest-growing region, on track to expand at an 8.1% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agricultural Adjuvants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing food demand versus declining arable land | +1.2% | Global, with acute pressure in Asia-Pacific (China, India, and Bangladesh) and Sub-Saharan Africa | Long term (≥ 4 years) |

| Precision-farming adoption boosting spray accuracy | +1.5% | North America and Europe lead, Asia-Pacific core (China, India, and Japan) accelerating spill-over to Brazil, and Argentina | Medium term (2-4 years) |

| Shift to herbicide-tolerant seeds elevates adjuvant need | +1.3% | North America (the United States and Canada), South America (Brazil and Argentina), expanding into India and select African markets | Medium term (2-4 years) |

| Surge in bio-based surfactant innovation, lowering toxicity | +0.9% | European Union regulatory pull, North America, and Asia-Pacific adoption driven by sustainability mandates | Long term (≥ 4 years) |

| Drone-enabled ultra-low-volume spraying necessitating ultra-spreaders | +1.1% | Asia-Pacific core (China leading with 170,000+ ag drones), early gains in Japan, Australia, and North America niche adoption | Short term (≤ 2 years) |

| Carbon-credit-linked dose-reduction incentives | +0.6% | North America (United States carbon programs), Europe Union pilot schemes, and emerging in Brazil and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Food Demand Versus Declining Arable Land

According to United Nations projections, the world's population is projected to reach 9.7 billion by 2050, and demand for additional arable land is projected to reach 165 million hectares[1]Source: United Nations Fao, “FAOSTAT Land Use,” fao.org. As cultivable land per capita declines, governments are promoting yield intensification programs that encourage the use of adjuvant-enhanced sprays to reduce repeat applications and improve input efficiency. This widening gap between food demand and available farmland compels growers to maximize productivity on existing acreage, increasing dependence on crop protection products. Agricultural adjuvants support this shift by improving spray deposition, spreading, and uptake, enabling more effective pest and weed control while optimizing agrochemical use.

Precision-Farming Adoption Boosting Spray Accuracy

Precision agriculture technologies, such as GPS-guided sprayers, variable rate technology (VRT), and sensor-based application systems, are significantly influencing crop protection practices. Such systems cut spray volumes by 15% to 25%, but only if droplets remain uniform, drift-control polymers and low-foam surfactants are now required additives. Similar trends hold in Western Europe, where the Farm-to-Fork strategy’s 50% reduction target forces growers to squeeze more efficacy from each liter. China’s drone fleet delivers 5-15 liters per hectare compared with 100 liters from ground rigs, making organosilicone superspreaders indispensable to maintain leaf coverage. These dynamics accelerate demand across every subsegment of the agricultural adjuvants market.

Shift to Herbicide-Tolerant Seeds Elevating Adjuvant Need

The global adoption of herbicide-tolerant (HT) crops, particularly soybean, corn, and cotton, has significantly increased dependence on herbicide performance. Many herbicides require specific surfactants or oil-based adjuvants to ensure optimal absorption and effective weed control. As resistance to glyphosate and other herbicides continues to rise, newer formulations increasingly rely on advanced adjuvant systems to maintain efficacy. By 2025, herbicide-tolerant traits are projected to cover substantial hectares globally, with each application often requiring a specific surfactant, ammonium sulfate conditioner, or volatility-reduction agent, as indicated on the product label. Brazil and Argentina doubled per-hectare adjuvant volumes over the last five years as post-emergence programs displaced manual weed control.

Surge in Bio-Based Surfactant Innovation Lowering Toxicity

The European Union banned nonylphenol ethoxylates in crop formulations in 2024, prompting rapid substitution with alkyl polyglucosides, fatty alcohol ethoxylates, and sophorolipid biosurfactants. In 2025, BASF announced the expansion of its Alkyl Polyglucosides (APGs) operations in Asia by establishing a new plant at the Bangpakong site in Thailand[2]Source: BASF SE, “Thailand Alkyl Polyglucoside Plant Press Release,” basf.com. This initiative aims to strengthen its position in a growing market and enhance customer service through improved agility and flexibility within a robust regional network. Early adopters in greenhouse vegetables have already shifted from adjuvant spend to certified bio-based products. These innovations expand the premium tier of the agricultural adjuvants market and reduce regulatory risk for suppliers.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening toxicology thresholds for co-formulants | -0.8% | Europe Union leading via Registration, Evaluation, Authorisation, and Restriction of Chemicals, North America following with Environmental Protection Agency inert-ingredient reviews, and spillover to Asia-Pacific export markets | Medium term (2-4 years) |

| Volatility in petrochemical feedstock pricing | -0.5% | Global, with acute margin pressure in Asia-Pacific and Europe, reliant on imported naphtha and palm oil | Short term (≤ 2 years) |

| Compatibility gaps with microbial biocontrol agents | -0.3% | North America and Europe Union, where biological adoption exceeds 15% of crop-protection spend, emerging in Brazil, India | Medium term (2-4 years) |

| AI-guided spray systems reducing broad-spectrum adjuvant use | -0.4% | North America (United States and Canada) early adoption, Australia and Western Europe following, limited near-term impact in price-sensitive markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Toxicology Thresholds for Co-Formulants

Regulatory agencies are intensifying their scrutiny of inert ingredients and co-formulants used in adjuvants. The European Union, through the Registration, Evaluation, Authorisation, and Restriction of Chemicals (REACH) framework, and the Environmental Protection Agency (EPA) have implemented stricter toxicity benchmarks for surfactants and alkylphenol ethoxylates. In 2022, the European Union's Farm to Fork strategy targets a 50% reduction in pesticide use by 2030[3]Source: European Commission, “Farm to Fork Strategy: For a Fair, Healthy and Environmentally-Friendly Food System,” European Commission, ec.europa.eu. As a result, member states are enforcing stringent maximum residue limits that surpass Codex standards. These measures have increased compliance costs and necessitated reformulations, leading to higher R&D expenditures. Compliance costs can reach high per-chemistry level, a burden that sidelines small formulators and shifts share toward vertically integrated majors in the agricultural adjuvants market. Cold-weather performance gaps still plague vegetable-oil surfactants, forcing reformulation cycles that sap margins.

Compatibility Gaps with Microbial Biocontrol Agents

As biological crop protection products gain popularity, compatibility challenges have arisen between chemical adjuvants and microbial formulations. Certain surfactants can reduce the viability of microbial biopesticides, thereby restricting their simultaneous tank-mixing. In regions such as North America and the European Union, where biological products account for a significant share of crop protection spending in specific segments, integration challenges persist. Emerging markets, including Brazil and India, are also encountering issues related to compatibility adjustments. Suppliers, including Croda, are developing lecithin-based formulations designed to protect spores. The adoption of these formulations is tied to the expansion of biological acreage, limiting growth potential within this segment of the agricultural adjuvants market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Activators Remain the Anchor While Utilities Accelerate

Activator adjuvants were the largest segment, led with 70.5% of the agricultural adjuvants market share in 2025, because surfactants and oils remain mandatory on most post-emergence herbicide labels. The global demand for agricultural activator adjuvants is rising significantly, driven by agronomic, economic, and regulatory factors influencing modern crop protection practices. As agricultural systems work to meet the growing global demand for food, feed, and fiber, farmers are increasingly prioritizing the efficiency and effectiveness of crop protection products, including herbicides, fungicides, insecticides, and foliar nutrients.

Utility adjuvants are fastest fastest-growing segment, forecast to post an 8.4% CAGR through 2031, fueled by drift-control polymers and water conditioners that help growers satisfy ever-tighter nozzle and pH specifications. The agricultural adjuvants market size for utility products is forecast to expand steadily as drone protocols and hard-water fields multiply use cases. Precision rules are embedding utilities into core agronomy. Drift-control agents meet ISO 22866 droplet standards, water conditioners neutralize mineral antagonism that can cut glyphosate performance by 40%, and antifoams protect high-pressure pumps from overflow. Each added tank-mix input increases the risk of incompatibility, which drives demand for buffers and polymers that stabilize emulsions.

By Application: Herbicide Dominance Persists, Insecticide Use Gains Pace

Herbicide adjuvants were the largest segment, commanding 48.7% of the agricultural adjuvants market size in 2025, reflecting their established role in weed-control practices for soy, corn, and cotton. Agricultural adjuvants are essential for enhancing herbicide effectiveness. The increasing prevalence of herbicide-resistant weeds has heightened the demand for adjuvants. Farmers are adopting more complex herbicide combinations and precise application methods to address resistance issues, with adjuvants playing a critical role in enhancing the effectiveness of these formulations. Environmental regulations in several regions promote reduced chemical application rates, making adjuvants vital for ensuring efficacy at lower dosages.

Insecticide adjuvants are the fastest-growing segment, projected to grow at a 7.9% CAGR to 2031, driven by organosilicone superspreaders that enhance systemic insecticide penetration and compatibility agents that stabilize tank mixes combining neonicotinoids with biological insecticides. As pyrethroids lose potency, diamides and biologicals depend on adjuvants to sustain field efficacy at reduced rates. Drone spraying also favors organosilicone insecticide adjuvants because low-volume droplets require extreme spreading power. Consequently, the agricultural adjuvants market share tied to insect control is projected to increase each year of the forecast window.

By Crop Type: Broad-Acre Stability with High-Value Horticulture Acceleration

Cereals and grains were the largest segment, accounting for 48.0% of the agricultural adjuvants market size in 2025, reflecting vast wheat, rice, and corn acreage. Their growth is modest but steady because per-hectare adjuvant doses stay flat and gains track planted area. Oilseeds and pulses, especially soybeans and canola, consume about one-third of global liters, and their adjuvant needs climb in lockstep with herbicide-tolerant trait spread.

Fruits and vegetables hold the fastest-growing segment, experiencing a 9.2% CAGR through 2031. Protected cultivation systems in China, the Netherlands, and Mexico are increasingly adopting foliar nutrition programs. These programs require compatibility agents to prevent precipitation when mixing micronutrients with fungicides. Specialty producers in the Netherlands, Mexico, and China integrate compatibility agents into foliar-nutrition cocktails, delivering the highest dollar margins across the agricultural adjuvants market.

Geography Analysis

North America was the largest region, holding 35.4% of the agricultural adjuvants market share in 2025, as its highly mechanized farms and extensive dealer networks already integrate adjuvant packages into routine crop-protection programs. Growth is projected to increase slightly behind the worldwide pace, because saturation in the United States caps incremental acreage. Canada adds resilience with canola and wheat programs that still depend on surfactant-optimized glyphosate passes, while Mexico, expanding drip-irrigated vegetables, brings faster growth to the continental mix.

Asia-Pacific is the fastest-growing region, on track to expand at an 8.1% CAGR to 2031, as China and India modernize their spraying equipment and push yield targets higher. China’s policy backing for Unmanned Aerial Vehicles (UAVs) and smart machinery funnels adjuvant demand into superspreaders and drift-reducers. India’s Digital Agriculture Mission funds half of the qualifying costs for precision-spray equipment, stoking sales of activators for cotton, mustard, and pulses. Japan and Australia round out regional growth with drone deployments in aging rural districts and cotton insecticide programs that rely heavily on drift control.

Europe and South America demonstrate moderate performance, balancing steady policy support with market limitations. In Europe, growth is primarily driven by stringent environmental regulations, which are shifting purchasing preferences toward bio-based blends rather than increasing overall volumes. In South America, a notable CAGR is observed as Brazilian and Argentine farmers expand soybean and corn cultivation. However, fluctuating currency values and input costs hinder the adoption of premium adjuvants. Africa lags behind other regions but maintains consistent single-digit growth, supported by the development of commercial farming and donor-funded training programs emphasizing drift control and water conditioning.

Regulatory Landscape

Regulation of agricultural adjuvants is tightening around co-formulant toxicology, labeling transparency, and environmental controls for spray operations. In the European Union, Commission Regulation (EU) 2026/1120 (adopted 26 May 2026) amended Annex III to Regulation (EC) No 1107/2009 by adding 12 co-formulants prohibited for use in plant protection products and adjuvants. Member States are required to withdraw authorizations for products containing the listed co-formulants by 16 June 2028. The EU also adopted Commission Regulation (EU) 2026/1123 on 26 May 2026 to introduce updated labeling requirements aligned with Regulation (EC) No 1272/2008, applying from 1 January 2028. This increases the compliance burden for suppliers selling stand-alone tank-mix adjuvants across multiple Member States.

In North America and the United Kingdom, requirements extend across chemical disclosure and application-side environmental controls. California Department of Pesticide Regulation (CDPR) finalized regulation 22-004 to strengthen ingredient statement clarity on spray adjuvant product labels, pushing manufacturers toward more robust documentation and label governance. In the United States, the EPA 2026 Pesticide General Permit becomes effective on 31 October 2026 under the National Pollutant Discharge Elimination System, governing point source discharges from pesticide applications that can include adjuvant-containing sprays. This adds operational compliance considerations for applicators and supports demand for drift-control and deposition-focused utility adjuvants. In Great Britain, the 2020 Official Controls (Plant Protection Products) Regulations and oversight by the Health and Safety Executive (HSE) reinforce scrutiny of components, including co-formulants and adjuvants used with plant protection products.

Competitive Landscape

The agricultural adjuvants market is moderately concentrated, with the top five companies, BASF SE, Corteva Agriscience, Evonik Industries, Solvay SA, and Croda International, holding a significant share of the market by 2025. BASF SE leads the market with its integrated raw-material base and global formulation capabilities, enabling the swift introduction of new bio-based blends. Corteva Agriscience follows closely, leveraging proprietary seed traits and customized surfactants to enhance adjuvant adoption and strengthen retailer relationships. Both companies invest heavily in research and development, focusing on multifunctional carriers that align with the growing demand for precision spraying and biological actives.

The second tier of market leaders, including Evonik Industries and Solvay SA's crop solutions division, holds strong regional positions and offers specialized technology portfolios. Syngenta utilizes its active-ingredient pipeline to integrate compatible adjuvants, while Evonik Industries differentiates itself with silicone and silica systems designed for drone and low-volume applications. Solvay emphasizes renewable surfactants that comply with increasingly stringent toxicology standards, particularly appealing to sustainability-focused markets in Europe. These companies' efforts drive competitive pressure, fostering continuous advancements in droplet control, tank-mix stability, and residue reduction.

All top five companies are actively expanding their market presence through local production facilities, joint ventures, and collaborations in digital agriculture. Capacity expansions in the Asia-Pacific region reduce lead times and align pricing with local demand, while acquisitions of specialty formulators enhance access to biological-ready carriers. Partnerships with equipment manufacturers and agronomic data platforms enable real-time adjuvant recommendations, creating integrated service ecosystems that increase switching costs for growers. These strategic initiatives strengthen the leadership positions of these companies and raise entry barriers for new competitors.

Agricultural Adjuvants Industry Leaders

BASF SE

Corteva Agriscience

Evonik Industries

Solvay SA

Croda International

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The market is concentrating around low-toxicity, biodegradable, and bio-based adjuvant chemistries that can help formulators and tank-mix suppliers manage co-formulant restrictions and evolving EU labeling rules, while still meeting performance needs under precision-application conditions. Demand is also building for compatibility-focused additives that support co-application of conventional crop protection and biologicals, since compatibility gaps with microbial biocontrol agents reduce tank-mix flexibility and raise the case for adjuvants that protect microbial viability. BASF's 2025 expansion move for Alkyl Polyglucosides (APGs) in Thailand, along with the broader shift away from restricted chemistries such as nonylphenol ethoxylates in Europe, reflects supplier investment in substitute surfactant families that can scale across regions.

Drone and ultra-low-volume spraying is a second opportunity axis that is already being translated into R&D and field protocols, particularly in Asia-Pacific. China runs 170,000+ agricultural drones and application volumes can fall to 5-15 liters per hectare, increasing the need for utility and activator chemistries tuned for ultra-low-volume coverage. In early 2026, Rovensa Next collaborated with Universite de Technologie de Compiegne (UTC) through the FAUVE project to study Natural Deep Eutectic Solvents (NADES)-based adjuvants for drone applications, and reported improvements including fewer fine droplets and lower foam during high-speed blending. That work points to measurable formulation levers for UAV-focused utility and activator products. Policy actions also support precision-enabled adjuvant packages, including the United Kingdom's Pesticides National Action Plan 2025 and ongoing EU workstreams on pesticide-market rules and implementation measures, which increase demand for adjuvants that support drift reduction, efficacy at lower doses, and improved application stewardship.

Recent Industry Developments

- May 2026: BASF SE launched Basta ULTRA, a non-selective herbicide using Glu-L technology, featuring an upgraded formulation package designed to improve droplet stability and field performance. The formulation focus aligns with tighter drift and application-quality requirements that elevate the role of utility and activator adjuvant systems in tank mixes. This strengthens competitive emphasis on performance enhancers used in precision spraying and low-volume protocols.

- May 2026: Corteva Agriscience announced the launch of Verpixo fungicide with Adavelt active after U.S. EPA registration for the U.S. sugarbeet market. The registration-led launch creates a new use-case where adjuvant selection and spray-quality management influence coverage and uptake in specialty crop programs. It also reinforces how new product registrations feed into demand for compatible adjuvant packages used by retailers and growers.

- April 2025: BASF SE introduced Sokalan CP 301, a readily biodegradable dispersant positioned for agricultural formulations. The launch reflects the industry shift toward additives that help meet sustainability and chemical-risk scrutiny, particularly around co-formulants and inert ingredients. It expands the options available to formulators seeking biodegradable performance additives that can fit evolving compliance expectations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the agriculture adjuvants market includes stand-alone additives that are tank-mixed or blended with crop protection sprays to improve coverage, deposition, penetration, or spray stability across major crop systems worldwide.

Scope exclusions: We exclude adjuvant chemistries that are already built into formulated crop protection products (in-can) and are not sold as separate adjuvant products.

Segmentation Overview

- By Type

- Activator Adjuvants

- Surfactants

- Oil Adjuvants

- Utility Adjuvants

- Drift Control Agents

- Water Conditioners

- Antifoaming Agents

- Acidifiers and Buffers

- Activator Adjuvants

- By Application

- Herbicide Adjuvants

- Insecticide Adjuvants

- Fungicide Adjuvants

- Other Applications

- By Crop Type

- Cereals and Grains

- Oilseeds and Pulses

- Fruits and Vegetables

- Other Crops

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping where adjuvants are used and how demand moves with crop protection spray intensity, which helped us set the right boundaries and build a first cut demand pool. We leaned on non-paywalled sources such as FAOSTAT, the United States Department of Agriculture, Eurostat, and OECD-FAO outlook publications to understand crop area, crop mix, and longer term acreage and yield trends.

We also used regulatory and technical references, such as EPA pesticide and drift guidance pages and peer-reviewed agronomy journals, to sanity check where adjuvants are required due to water hardness, drift restrictions, or spray equipment changes. Company filings, investor presentations, association websites, and reputable agri press were reviewed to align on product definitions and typical pricing direction, while a paid subscription covering company financials and a patents database helped confirm active R&D areas and map supplier footprints. This source list is illustrative, and many other public references were used for data capture, cross-checking, and clarification.

Primary Interviews and Surveys

Primary discussions were run with adjuvant manufacturers, formulators and distributors, ag input retailers, and large farm or applicator voices across major consuming regions, and then the findings were compared back to the desk model. These conversations helped validate what gets counted as stand-alone adjuvants, typical application rates by crop protection program, and how pricing shifts with formulation type and mix rates in different geographies.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | APAC: 41% |

| Mid tier: 47% | Functional/Unit leaders: 41% | EMEA: 32% |

| Smaller Players: 22% | Managers: 46% | Americas: 27% |

Market-Sizing & Forecasting

Sizing begins with a top-down build where crop area and crop protection intensity by region are translated into an addressable spray volume, which is then adjusted using typical adjuvant adoption and mix-rate ranges by application. To keep the model practical, a few key inputs were tracked closely, including planted area by major crop groups, herbicide and fungicide treatment intensity, prevalence of hard-water and drift-control needs, the share of aerial or drone spraying where relevant, and average price movement by adjuvant type.

The totals were then checked using selective bottom-up approximations, such as sampling supplier and channel revenue disclosures, using price times volume checks for common adjuvant functions, and confirming whether large regional distributors were seeing the same demand direction. Where direct gaps appeared in smaller countries, adoption assumptions were bridged using similar agronomy profiles and regulatory similarity, and then re-tested through follow-up expert calls.

For forecasting, scenario analysis was used because the market is sensitive to weather-driven acreage shifts, crop protection program changes, and regulatory drift limits. Input trajectories were set using consensus ranges from interviewees and public crop outlooks, and then the model was rerun to see how adoption, mix rates, and pricing combine into the value forecast.

Data Validation & Update Cycle

Outputs were validated in steps, starting with cross-checks against independent signals like crop protection spending direction, planting and acreage updates, and regional spray program shifts. When unusual jumps were seen, the assumptions behind adoption, mix rates, or price were reviewed, and a targeted re-contact was triggered to confirm what changed.

Before sign-off, the model and key assumptions go through an internal analyst review so that calculation logic, units, and currency timing are consistent. Reports are refreshed annually, and interim updates are made when a material change occurs, such as a new restriction on drift, a large pricing shock in key inputs, or a major shift in crop planting patterns. Right before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's Global Agriculture Adjuvants Market Market Estimate Compared With Other Published Estimates

Published values for agriculture adjuvants can vary even when the same words are used, since teams can count different product boundaries, apply different price logic, and start from different demand indicators. Differences also show up when one estimate uses a more aggressive adoption curve while another stays conservative around spray program changes.

By tracking stand-alone adjuvant sales at the factory-gate and checking in-can exclusions consistently, Mordor Intelligence keeps the total tied to what is actually sold as an adjuvant product, rather than blending it with formulated crop protection value. In addition, some estimates apply broad global average prices, while others adjust by crop mix and application intensity, and currency timing can also shift the stated USD value when exchange rates move during the base year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.30 B (2025) | |

| Industry Publisher A | USD 4.27 B (2025) | Uses a similar year but may include a wider bundle around spray additives, and the price build can rely on averaged regional pricing rather than function-level mix rates by crop protection program. |

| Research Publisher B | USD 3.97 B (2024) | Anchors the estimate to an earlier base year and a slower growth path, which can understate the impact from recent spray intensity changes and pricing resets in adjuvant formulations. |

Overall, the spread across sources is mainly explained by what is counted as a stand-alone adjuvant versus adjacent spray additives, and by whether pricing and adoption are updated with current season signals. Our approach stays repeatable because the market total can be traced back to acreage, spray intensity, adoption, mix rates, and a clear USD conversion timing.

Key Questions Answered in the Report

How large will the agricultural adjuvants market be in 2026?

The agricultural adjuvants market size was valued at USD 4.30 billion in 2025 and estimated to grow USD 4.55 billion in 2026.

Which region is projected to record the fastest growth through 2031?

Asia-Pacific is projected to advance at an 8.1% CAGR, driven by drone adoption in China and precision-spray subsidies in India.

Which adjuvant type currently generates the highest revenue?

Activator adjuvants lead with a 70.5% revenue share in 2025.

Which application segment is set to accelerate the most by 2031?

Insecticide adjuvants are fastest fastest-growing segment, projected to grow at a 7.9% CAGR to 2031.

Page last updated on: