Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

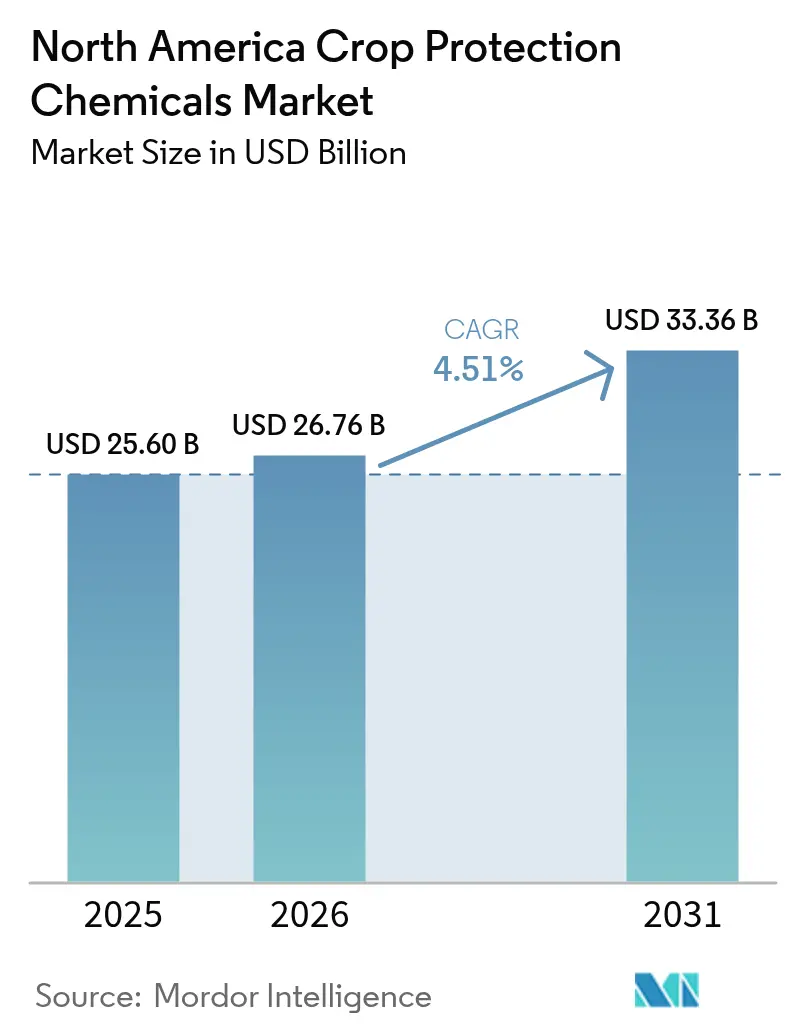

| Base Year Market Size (2025) | USD 25.6 Billion |

| Market Size (2026) | USD 26.76 Billion |

| Market Size (2031) | USD 33.36 Billion |

| Growth Rate (2026 - 2031) | 4.51% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Crop Protection Chemicals Market Analysis by Mordor Intelligence

The North America crop protection chemicals market size in 2026 is estimated at USD 26.76 billion, growing from 2025 value of USD 25.6 billion with 2031 projections showing USD 33.36 billion, growing at 4.51% CAGR over 2026-2031. Rising weed resistance, surging fungal outbreaks, and the widening regulatory preference for reduced-risk actives are reinforcing chemical demand even as precision-agriculture tools curb waste. Growers continue to favor synthetic herbicides for broad-acre efficiency, yet biological and biorational products are scaling rapidly under the United States Environmental Protection Agency (EPA) fast-track pathway. The region’s large grain footprint, stable export channels under the United States–Mexico–Canada Agreement, and carbon-credit incentives for conservation tillage all sustain spending despite litigation over legacy chemistries. Competitive intensity remains high as leading firms bundle seeds, chemistry, and digital agronomy to capture wallet share while navigating tightening residue thresholds.

Key Report Takeaways

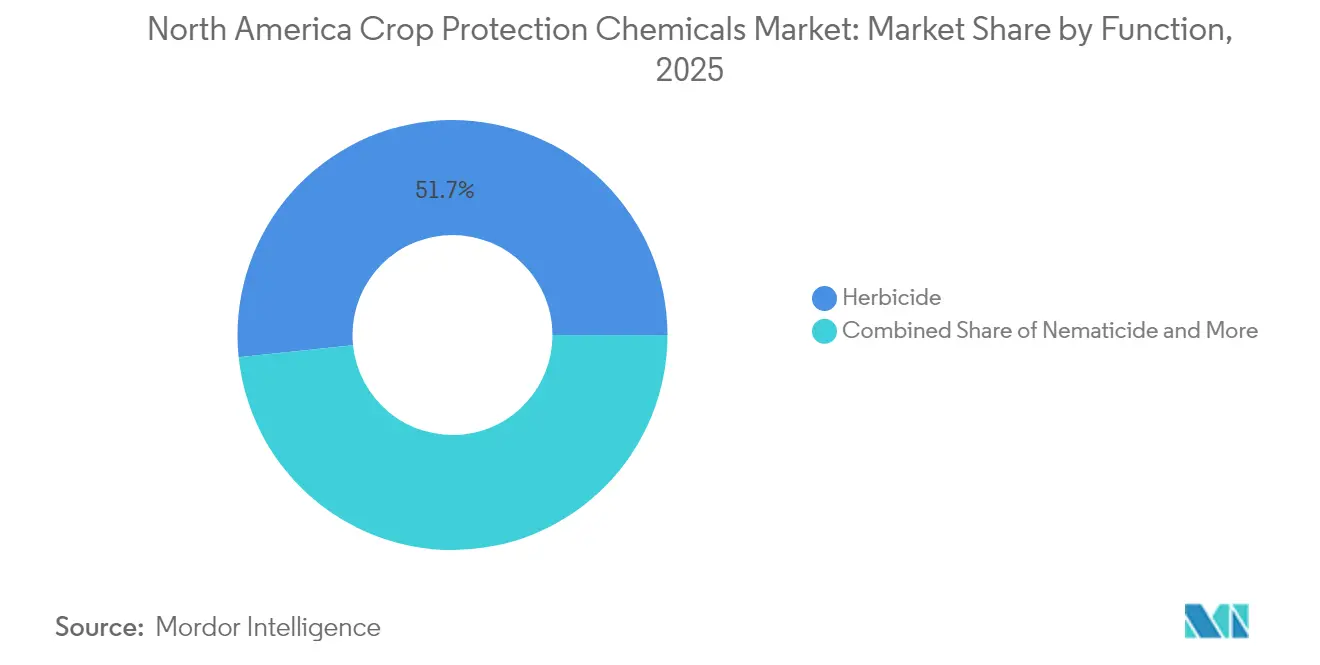

- By function, herbicides commanded 51.65% of revenue in 2025; the same segment is also projected to post the fastest 4.88% CAGR through 2031.

- By application mode, foliar treatments led with a 40.55% share in 2025; soil treatment is forecast to expand at the highest 4.86% CAGR to 2031.

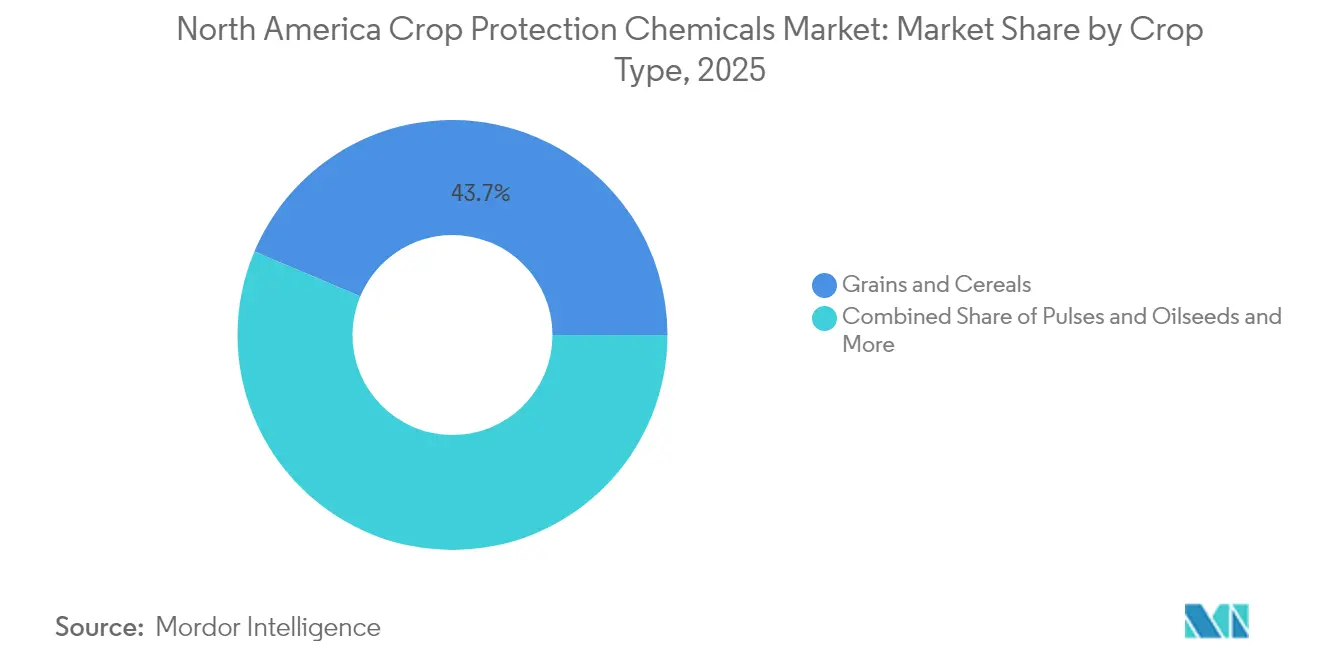

- By crop type, grains and cereals accounted for 43.65% of demand in 2025; the segment is likewise set to grow the quickest at a 4.82% CAGR over the forecast period.

- By geography, the United States held 82.95% of sales in 2025, while Canada is poised for the strongest 5.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Crop Protection Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated herbicide-tolerant trait adoption | +0.8% | United States and Canada core, spillover to Mexico | Medium term (2-4 years) |

| Precision-spraying equipment lowering cost per acre | +0.6% | Corn Belt and Prairie regions | Short term (≤ 2 years) |

| Surge in soybean rust and tar spot outbreaks | +0.9% | Midwest expanding to Canada | Short term (≤ 2 years) |

| U.S. EPA fast-track approvals for biorational actives | +0.7% | United States with spillover to Canada and Mexico | Medium term (2-4 years) |

| Carbon-credit programs rewarding reduced tillage | +0.5% | United States and Canada | Long term (≥ 4 years) |

| Mexican government subsidies for IPM tools | +0.4% | Mexico agricultural states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated herbicide-tolerant trait adoption

Adoption rates of herbicide-tolerant soybeans now exceed 95% while corn reaches 89% across principal production areas. These traits allow wider post-emergence windows that lift seasonal herbicide volumes and expand rotational flexibility. The EPA clearance of dicamba- and 2,4-D-based platforms delivers new modes of action just as glyphosate-resistant weeds such as Palmer amaranth intensify. Stacked technologies like Corteva Enlist E3 and Bayer XtendFlex foster premium pricing and encourage bundled chemistry-seed packages. Integrated variable-rate spraying optimizes dose by zone, further embedding these traits into modern agronomy.[1]Source: U.S. Environmental Protection Agency, “Biopesticide Registration,” Environmental Protection Agency, epa.gov The resulting synergy between genetics and precision hardware sustains demand for selective herbicides despite price pressure from generics.

Precision-spraying equipment lowering cost per acre

Computer-vision sprayers identify individual weeds and reduce chemical volumes by up to 77% while maintaining control levels, as field trials of John Deere See and Spray demonstrate. Public support through the United States Department of Agriculture (USDA) FARMER grants accelerates adoption by offsetting equipment costs.[2]Source: U.S. Department of Agriculture, “FARMER Program Funding,” United States Department of Agriculture, usda.gov On-board sensors adjust rates in real time, minimizing overlaps and drift, which lowers input spend and addresses regulatory scrutiny of off-target movement. The time saved on refills and the labor reductions boost operational efficiency for large farms that manage thousands of acres. Equipment dealers now bundle data analytics subscriptions that help growers verify savings, reinforcing repeat purchases of compatible chemistries.

Surge in soybean rust and tar spot outbreaks

Tar spot impacted more than 70% of corn acreage in Illinois, Indiana, and Iowa during 2024, causing yield losses as high as 30 bushels per acre in some fields.[3]Source: University of Illinois Extension, “Tar Spot Disease Management,” University of Illinois, extension.illinois.edu Concurrent northward expansion of soybean rust triggered prophylactic fungicide programs far beyond the Gulf Coast. Climate variability, including wetter springs and warmer autumns, extends pathogen life cycles and geographic reach. Growers increasingly apply multi-site fungicide mixtures to delay resistance and protect yield ceilings worth USD 1,100 per hectare in revenue at 2025 commodity prices. Premium co-formulations capturing both curative and preventative modes of action are gaining market share despite their higher cost profiles.

U.S. EPA fast-track approvals for biorational actives

The EPA expedited 47 new reduced-risk active ingredient registrations in 2024, a 23% year-over-year rise. Microbial strains based on Bacillus and Trichoderma dominate approvals due to favorable safety data that shortens review time. Pheromone-based mating disruption and plant-incorporated protectants also benefit, enabling integrated pest management (IPM) strategies with lower environmental footprints. Faster clearances shorten commercialization cycles for firms like Syngenta and FMC, which have doubled biological research spending since 2023. Downstream food brands favor these tools to satisfy residue-free pledges, pulling demand through the supply chain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Glyphosate litigation-driven retailer delisting | -0.6% | United States national, spillover to Canada | Short term (≤ 2 years) |

| Canada's proposed MRL cutbacks limiting exports | -0.4% | Canada export-dependent regions | Medium term (2-4 years) |

| Rising biological alternatives squeezing synthetic margins | -0.7% | North America specialty crop areas | Long term (≥ 4 years) |

| West Coast port congestion inflating input prices | -0.3% | Pacific Coast states and inland corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Canada's proposed MRL cutbacks limiting exports

Health Canada proposes halving MRLs for several actives, such as 2,4-D, in agricultural exports at risk if foreign buyers adopt stricter thresholds. Divergent standards compel growers to meet the lowest common denominator, adding analytical testing costs and encouraging shifts toward lower-residue actives. Export-dependent producers in British Columbia and Ontario foresee tighter shipment windows and higher compliance documentation. Chemical firms allocate extra budget to residue studies and label amendments, elongating return-on-investment timelines for new products.

Rising biological alternatives squeezing synthetic margins

Registrations of biological pesticides climbed 34% in 2024 as EPA fast-tracking coincided with escalating retailer sustainability mandates. Supermarket chains now favor produce sourced with reduced synthetic inputs, granting pricing premiums that offset biological costs. Start-ups backed by agricultural technology funds are releasing broad-spectrum microbial solutions that challenge synthetic incumbents during key application windows. While tank-mix programs combine both approaches, the proportional synthetic volume per acre declines in premium segments like berries and leafy greens. Established players face portfolio margin compression and must rebalance research portfolios toward mixed-mode offerings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Herbicides Anchor Demand yet Diversification Gains Pace

Herbicides generated 51.65% of the North America crop protection chemicals market revenue in 2025, reflecting widespread reliance on chemical weed control across 180 million corn and soybean acres. Precision application and trait-driven selectivity support continuous grower preference for post-emergence products that safeguard season-long yield potential. The segment is projected to expand at a 4.88% CAGR through 2031 as resistance management requires multiple modes of action and as conservation tillage increases herbicide intensity. At the same time, fungicide usage accelerates due to expanding tar spot and soybean rust zones, further diversifying overall spending. Insecticides face pressure from biological competitors and tightened pollinator safety rules, yet remain essential in integrated programs for sporadic outbreaks of Western corn rootworm.

A shift toward stackable biological herbicides is emerging, particularly in fruit and vegetable acreage where buyers impose residue caps. Leading firms launch micro-encapsulated formulations that combine synthetic and microbial actives to prolong efficacy while meeting environmental standards. Product stewardship initiatives now educate growers on rotating chemistries and incorporating cover crops to slow resistance. Collectively these trends ensure that herbicides remain market linchpins even as the broader mix evolves.

By Application Mode: Soil Treatment Surges on Early-Season Control

Foliar spraying still accounted for 40.55% of the total value in 2025, due to its adaptability across growth stages and pests. Soil treatment applications are poised for the fastest 4.86% CAGR as growers seek pre-emergence weed and soilborne insect control that reduces in-season passes. The North America crop protection chemicals market size for soil treatment solutions is set to exceed USD 6.25 billion by 2031, following advances in microgranular placement technology that minimize surface runoff. Chemigation adoption rises in irrigated western states where water delivery infrastructure allows precise metering of nutrients and crop protection products through existing lines. Seed treatment gains share as manufacturers roll out biological coatings that enhance root vigor, offering a prophylactic layer against early pests without extra field visits.

The combination of drone-assisted scouting and geo-referenced disease models prompts growers to reserve foliar interventions for verified pressure, thereby improving return on investment. Meanwhile, regulatory scrutiny of volatilization from foliar dicamba underscores the appeal of subsurface placement. Equipment providers innovate shielded nozzles and soil-injection rigs that integrate seamlessly with strip-till bars, signaling further convergence between tillage and chemical delivery.

By Crop Type: Grains and Cereals Remain Consumption Epicenter

Grains and cereals represented 43.65% of the North America crop protection chemicals market demand during 2025. Extensive corn and soybean acreage combined with strong ethanol and feed markets undergird chemical utilization. The staple segment’s projected 4.82% CAGR to 2031 results from rising fungicide adoption as tar spot migrates northward and as grain price strength justifies intensive protection. Commercial crops such as cotton and sugarcane command high per-acre chemical spend yet contribute a smaller share to aggregate value. Fruits and vegetables, though lower in acreage, drive differentiated demand for residue-compliant products and biological alternatives.

Oilseed and pulse rotations grow across Canadian Prairies to diversify farm revenue and improve soil nitrogen profiles, thereby widening market opportunities for selective broadleaf herbicides and seed treatments. Turf and ornamental uses remain niche but stable, anchored by golf course standards that prioritize visual quality. Collectively, the crop segmentation underscores the enduring primacy of grain production in shaping regional chemical volumes.

Geography Analysis

The United States holds the commanding 82.95% share of the North America crop protection chemicals market due to its expansive row-crop base and rapid adoption of precision hardware. Tar-spot epidemics intensified fungicide demand in Midwestern corn, while herbicide-tolerant traits kept post-emergence applications robust in soybean rotations. EPA registration of 47 new biological actives in 2024 illustrated regulatory momentum toward sustainable solutions that still maintain agronomic performance.

Canada is poised for the strongest 5.24% CAGR through 2031. Canada emerges as the growth bright spot as Prairie growers lift herbicide volumes to manage weed pressure in conservation-tillage systems favored by provincial carbon credit frameworks. Expanding canola acreage and price premiums for high-protein wheat justify investment in premium crop protection programs. Proposed MRL reductions add complexity that may shift product mix toward lower-residue offerings or accelerate biological uptake.

Mexico’s IPM subsidy through 2028 allocates MXN 8.5 billion (USD 472 million) annually for biological agents and precision equipment, driving market expansion in states such as Sinaloa and Sonora. Government efforts to reduce illegal pesticide imports and to modernize smallholder value chains further open channels for registered products. Climatic diversity, from arid Northwestern plains to humid central highlands, yields a mosaic of pest profiles that require both broad-acre chemistry and specialty solutions.

Competitive Landscape

The top five suppliers, Bayer AG, BASF SE, Syngenta Group, Corteva Agriscience, and FMC Corporation, collectively hold a significant share of regional revenue, giving the North America crop protection chemicals market a consolidated profile. Bayer leads via its integrated seed and chemistry portfolio alongside digital agronomy tools that reinforce grower loyalty.

BASF’s 2024 launch of Tirexor introduced the first novel herbicide mode of action in a decade, addressing herbicide-resistant weeds. Syngenta and Corteva invest heavily in biological research centers to capture growth in biorational demand. Partnerships between chemical companies and equipment manufacturers accelerate precision-delivery solutions, exemplified by the FMC John Deere alliance integrating variable-rate technology with proprietary herbicides.

Generic manufacturers expand in post-patent molecules yet face tighter stewardship rules that favor branded formulations with enhanced drift control. Market entrants specializing in microbial pesticides attract venture capital and licensing interest from majors that seek to fill portfolio gaps without lengthy discovery timelines. Overall, competitive strategy revolves around balanced investment in synthetic innovation, biological expansion, and digital differentiation.

North America Crop Protection Chemicals Industry Leaders

BASF SE

Bayer AG

Corteva Agriscience

FMC Corporation

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Nufarm introduced two new insecticides at Cultivate '25: OpteraPro DUO GC, a dual-action non-neonicotinoid product that controls more than 39 pests, and Simpell, a biological insecticide for foliar pest management in North American greenhouse and nursery operations.

- June 2025: FMC Corporation and Corteva Agriscience formed a partnership to provide U.S. growers with increased access to fluindapyr fungicide technology. The agreement allows Corteva to distribute fluindapyr-based products, expanding disease control solutions for major crops.

North America Crop Protection Chemicals Market Report Scope

Fungicide, Herbicide, Insecticide, Molluscicide, Nematicide are covered as segments by Function. Chemigation, Foliar, Fumigation, Seed Treatment, Soil Treatment are covered as segments by Application Mode. Commercial Crops, Fruits & Vegetables, Grains & Cereals, Pulses & Oilseeds, Turf & Ornamental are covered as segments by Crop Type. Canada, Mexico, United States are covered as segments by Country.Function

| Fungicide |

| Herbicide |

| Insecticide |

| Molluscicide |

| Nematicide |

Application Mode

| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

Crop Type

| Commercial Crops |

| Fruits and Vegetables |

| Grains and Cereals |

| Pulses and Oilseeds |

| Turf and Ornamental |

Geography

| Canada |

| Mexico |

| United States |

| Rest of North America |

| Function | Fungicide |

| Herbicide | |

| Insecticide | |

| Molluscicide | |

| Nematicide | |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| Crop Type | Commercial Crops |

| Fruits and Vegetables | |

| Grains and Cereals | |

| Pulses and Oilseeds | |

| Turf and Ornamental | |

| Geography | Canada |

| Mexico | |

| United States | |

| Rest of North America |

Market Definition

- Function - Crop Protection Chemicals are apllied to control or prevent pests, including insects, fungi, weeds, nematodes, and mollusks, from damaging the crop and to protect the crop yield.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms