Grain Fumigants Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

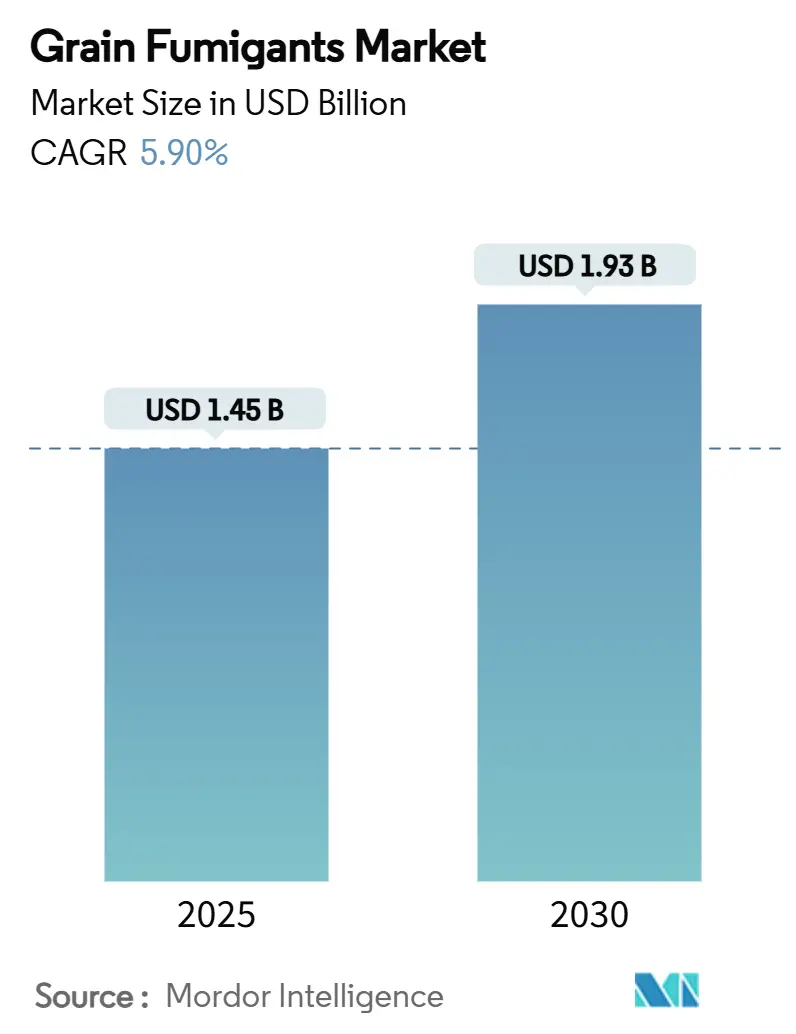

| Market Size (2025) | USD 1.45 Billion |

| Market Size (2030) | USD 1.93 Billion |

| Growth Rate (2025 - 2030) | 5.90% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Grain Fumigants Market Analysis by Mordor Intelligence

The grain fumigants market size reached USD 1.45 billion in 2025 and is projected to increase to USD 1.93 billion by 2030, growing at a 5.9% CAGR over the forecast period. Expansion relies on the rising scale of global grain output, stricter phytosanitary regulations, and continuous upgrades in storage infrastructure, particularly across the Asia-Pacific. Ongoing regulatory phase-outs of methyl bromide, combined with persistent concerns about insect resistance, are prompting operators to shift toward next-generation phosphine blends and emerging carbon dioxide systems. Technology advancements such as (IOT) Internet-of-Things gas monitoring devices are helping large facilities lower labor costs and prove compliance. Moderate market concentration leaves room for both multinational suppliers seeking scale efficiencies and regional specialists solving crop or climate-specific challenges in the grain fumigants market.

Key Report Takeaways

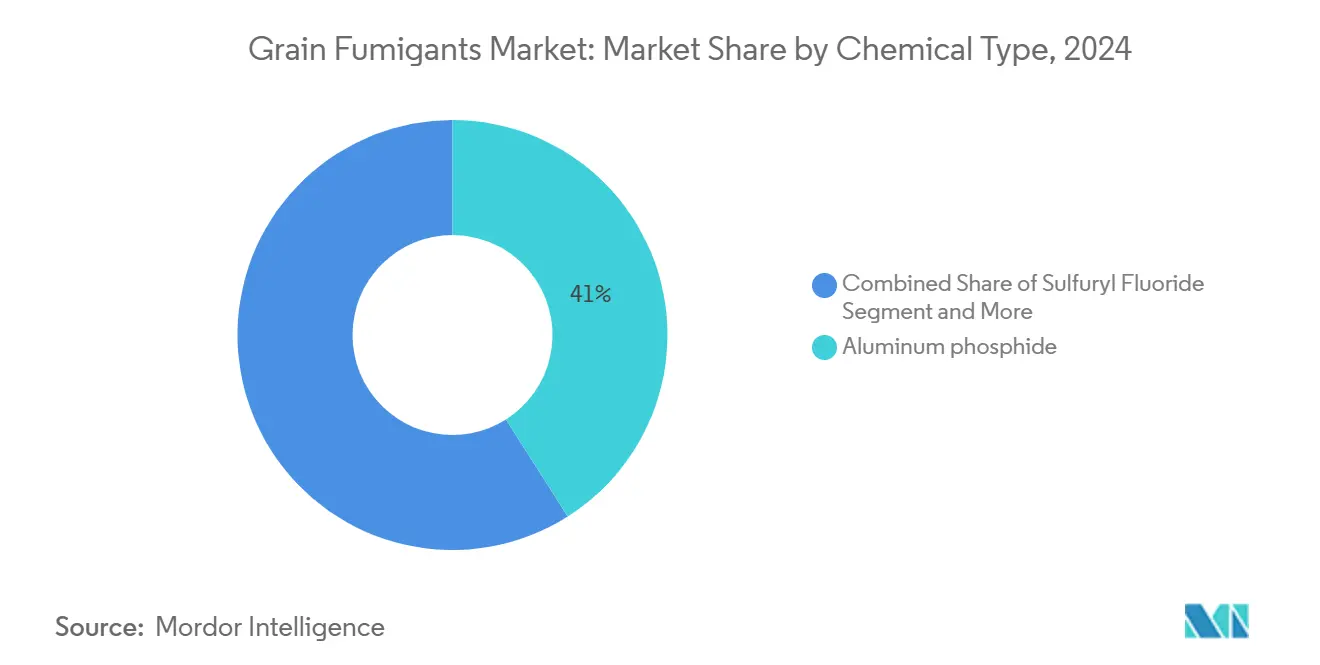

- By chemical type, aluminum phosphide led with 41% of the grain fumigants market share in 2024, while carbon dioxide is projected to expand at an 8% CAGR to 2030.

- By form, solid tablets and pellets accounted for 57% share of the grain fumigants market size in 2024, and gas formulations are advancing at a 7% CAGR through 2030.

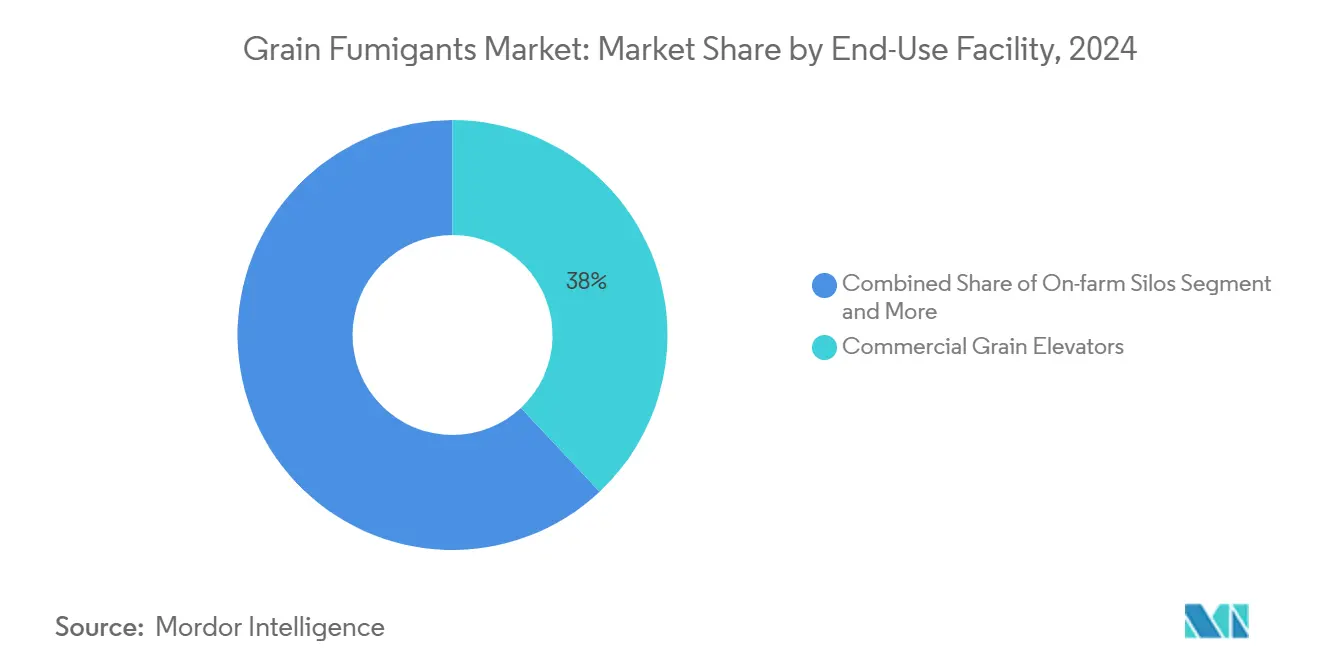

- By end-use facility, commercial elevators held a 38% share of the grain fumigants market in 2024, whereas shipping containers and barges posted the fastest 8.2% CAGR to 2030.

- By crop, wheat retained 40% of the grain fumigants market share in 2024, and rice fumigation is forecast to grow at a 7% CAGR through 2030.

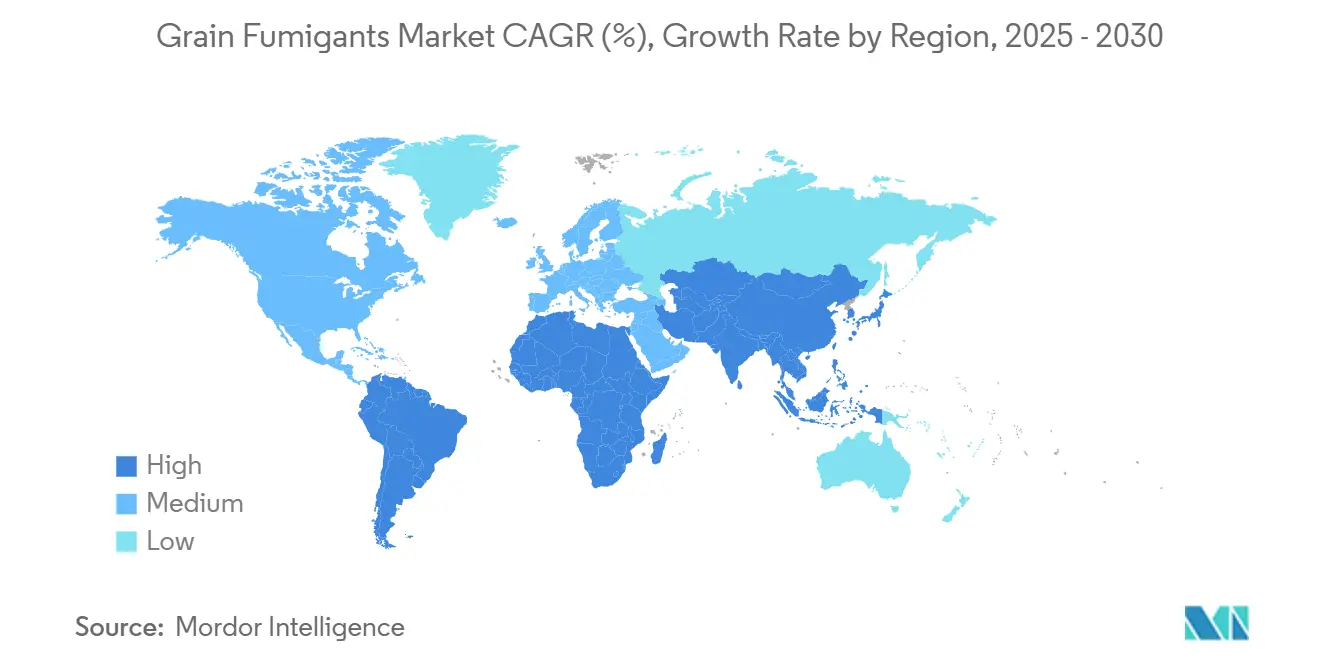

- By region, Asia-Pacific dominated with 36% of the grain fumigants market in 2024, and Africa is projected to grow at a CAGR of 7.2% through 2030.

Global Grain Fumigants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global grain output and larger commercial storage capacities | +1.2% | Global, strongest in Asia-Pacific and South America | Medium term (2-4 years) |

| Stricter phytosanitary import regulations on stored-grain insects | +1.0% | North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Regulatory phase-out of methyl bromide accelerates phosphine substitution | +0.8% | Developed markets, with spillover worldwide | Long term (≥ 4 years) |

| Consolidation of grain handling infrastructure in Asia-Pacific | +0.7% | Asia-Pacific core, Middle East and Africa spillover | Medium term (2-4 years) |

| Growth in controlled-atmosphere bulk grain shipping corridors | +0.6% | Global trade routes, notably Asia-Pacific to Europe and Middle East | Medium term (2-4 years) |

| IoT-enabled real-time gas monitoring lowers fumigation cost and risk | +0.5% | North America and Europe initially, Asia-Pacific expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Grain Output and Larger Commercial Storage Capacities

Brazil’s 2024/25 crop plan allocated USD 88.2 billion to boost production, illustrating the capital pouring into grain value chains [1]Source: U.S. Department of Agriculture, “Brazil 2024/25 Crop Plan Mobilizes Record Credit,” usda.gov . Higher output magnifies the need for airtight storage that minimizes the USD 4 billion annual cereal losses still plaguing Sub-Saharan Africa. New elevators typically specify aluminum phosphide tablets because of their low unit cost and ease of use, yet many are wiring silos with sensors to automate dosage and track gas decay. The resulting procurement model bundles chemicals, detection hardware, and training into multi-year service contracts. Each new million metric ton facility represents recurring demand rather than a one-off sale in the grain fumigants market.

Stricter Phytosanitary Import Regulations on Stored-Grain Insects

Regulators now require exporters to present treatment logs aligned with International Standards for Phytosanitary Measures No. 15. In Europe, detailed sulfuryl fluoride assessments for wood packaging underscore how rigorously each active ingredient is vetted [2]Source: EFSA Panel on Plant Health, “Risk Assessment of Sulfuryl Fluoride Treatments,” efsa.europa.eu . Because customs inspectors reject uncertified cargo, fumigation has shifted from a discretionary practice to a mandatory cost of entry in many corridors. The immediate winners are registered aluminum phosphide and phosphine products with a proven residue profile. Simultaneously, software providers are embedding QR-coded certificates and wireless gas-monitor outputs into export documentation, a shift that expands the total addressable technology layer within the grain fumigants market.

Regulatory Phase-out of Methyl Bromide Accelerates Phosphine Substitution

The Montreal Protocol’s methyl bromide sunset has already eliminated more than 8,000 metric tons across 55 countries, according to the United Nations Industrial Development Organization (UNIDO) case tracking. Phosphine tablets and on-site generated phosphine gas have become the standard replacements due to their comparable efficacy at lower ozone-depletion potential. China’s November 2024 pesticide amendments fast-tracked biopesticides but still preserved phosphine listings, signaling regulatory pragmatism. Although substitution is largely complete in North America and Europe, emerging economies, projected to phase out residual methyl bromide stocks through 2027, sustaining incremental demand.

Consolidation of Grain Handling Infrastructure in Asia-Pacific

Regional investors are scaling up terminal capacities. Saudi Arabia’s private operator, Arabian Agricultural Services Company (ARASCO), alone manages 500,000 metric tons of storage while importing 3.5 million metric tons annually. Consolidation allows procurement teams to standardize fumigation protocols and negotiate multi-country supply contracts, thereby favoring suppliers with a broad geographic reach. Bulk orders of phosphide tablets dominate, yet integrated service packages that combine chemical, safety training, and gas analytics are winning tenders. Smaller local applicators risk displacement unless they pivot to specialized crops or remote geographies in the grain fumigants market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing insect resistance to phosphine | -0.9% | Asia-Pacific and North America | Short term (≤ 2 years) |

| High toxicity concerns and tightening worker-safety regulations | -0.7% | North America and Europe, global expansion | Medium term (2-4 years) |

| Rapid adoption of hermetic storage systems in smallholder settings | -0.5% | Sub-Saharan Africa and South Asia | Long term (≥ 4 years) |

| Carbon-footprint scrutiny on sulfuryl fluoride emissions | -0.3% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Insect Resistance to Phosphine

Field reports confirm the presence of resistant strains of the lesser grain borer and red flour beetle in Australia, India, and certain parts of the United States. Operators respond by lengthening exposure cycles or switching to combination treatments, which raises labor and chemical inputs. Research institutes are testing synergists that break resistance mechanisms, but commercial launch timelines remain uncertain. Until alternatives scale, pockets of resistance will force higher costs per metric ton, trimming profitability for elevator operators.

High Toxicity Concerns and Tightening Worker-Safety Regulations

The United States Environmental Protection Agency’s 2024 sulfuryl fluoride mitigation proposal illustrates the trend toward lower occupational exposure limits and the use of mandatory personal protective equipment [3]Source: U.S. Environmental Protection Agency, “Draft Risk Assessments for Residential Fumigation,” epa.gov . Compliance now involves obtaining gas-clearance certificates and performing dual-sensor confirmation before re-entry, which extends turnaround times in processing plants. Small applicators lacking training budgets face market exit, nudging the landscape toward larger, certified operators in the grain fumigants market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Chemical Type: Aluminum Phosphide Dominance Faces Carbon Dioxide Challenge

Aluminum phosphide held a 41% share of the grain fumigants market size in 2024. This domination is due to its low cost per treated metric ton and compatibility with existing silo protocols. Stable demand persists across wheat and corn warehouses, yet sales growth is modest as usage rates plateau. Carbon dioxide is projected to grow at an 8% CAGR through 2030, driven by organic certification programs and customer pressure to cut synthetic residues. In Europe, CO₂ use jumped after a major malt exporter adopted Cocoon inflatables that double as both hermetic liners and fumigation chambers.

Phosphine gas remains essential for emergency knock-down treatments where infestations threaten export timelines, while magnesium phosphide serves geographies with aluminum-based import restrictions. Sulfuryl fluoride’s trajectory is mixed as structural fumigators value its penetrative power, but food-contact limitations dampen growth prospects. Regulatory scrutiny is pushing suppliers to invest in combination products that pair phosphine with carbon dioxide to achieve quicker kill rates at lower dosages, an innovation likely to reshape the chemical mix in the grain fumigants market.

By Form: Solid Formulations Lead While Gaseous Applications Gain Momentum

Solid tablets and pellets dominated with a 57% share of the grain fumigants market size in 2024, as elevator managers favor their simple handling and long shelf life. No special compressors or hoses are needed, so capital outlay stays minimal. That convenience underpins steady re-order cycles in mature markets. Gas cylinders and on-site generators, though, will expand 7% CAGR because controlled-atmosphere shipping demands precise dosage tied to voyage length. IoT-equipped valves now regulate gas flow automatically, mitigating the historic safety concerns that had capped adoption.

Liquid formulations retain a minor niche for damp storage scenarios where solids degrade. Across all forms, training content is evolving with suppliers embedding QR-linked micro-videos on labels, guiding applicators on dosage math and safety checkpoints. The format shift toward gases is therefore not merely chemical but also digital, supporting broader productivity gains inside the grain fumigants market.

By End-Use Facility: Commercial Elevators Anchor Market While Shipping Applications Surge

Commercial grain elevators captured 38% of the grain fuimgants market share in 2024 because they sit at the intersection of farm supply and export channels, continuous loading cycles drive year-round treatment schedules. These high-volume hubs favor aluminum phosphide tablets for cost control, but leading chains are installing central dosing manifolds for phosphine gas to streamline large bunker fumigations. Shipping containers and barges, although smaller in base, will outpace all other facilities at 8.2% CAGR as maritime grain traffic rises on Asia-Pacific to Middle East routes. The shift is amplified by canal disruptions that have lengthened transit times, increasing infestation risk.

On-farm silos show moderate growth as mid-sized growers modernize, while warehouse and transit depots capture spillover demand tied to multimodal logistics. Each facility type thus maps to distinct product-service packages, forcing suppliers to segment their portfolios accordingly within the grain fumigants market.

By Crop Type: Wheat Applications Dominate While Rice Storage Drives Growth

Wheat held about 40% of grain fumigants market share in 2024, a testament to its global acreage and the multi-month storage windows demanded by milling schedules. The segment’s maturity supports incremental upgrades like sensor-guided fumigation. Rice, conversely, is projected to post 7% CAGR through 2030 as Asia-Pacific exporters double warehouse capacities to meet rising African demand.

High-humidity storage creates ideal conditions for the lesser grain borer, accelerating adoption of phosphine plus carbon dioxide blends. Corn remains influential across the Americas, where ethanol and feed markets sustain year-round inventory buffers. Specialty grains such as sorghum, millet, and quinoa show smaller but premium margins, creating niches for customized fumigation protocols in the grain fumigants market.

Geography Analysis

The Asia-Pacific region is the largest contributor to the grain fumigants market, accounting for 36% of the market share in 2024. This dominance is supported by extensive wheat and rice production areas, as well as the rapid development of warehouses in countries such as China, India, and Vietnam. In late 2024, China implemented regulatory reforms that streamlined the registration of biopesticides while maintaining approvals for phosphides, thereby ensuring steady demand. India approved 416 new products in the first half of 2024, reflecting a proactive compliance environment that benefits certified suppliers. Urban migration trends are driving the centralized storage of grain, with multi-silo parks located near port clusters requiring integrated fumigation and monitoring systems.

Africa is the fastest-growing region, with a projected CAGR of 7.2% through 2030. Annual post-harvest cereal losses of USD 4 billion have spurred donor-funded initiatives to co-finance modern silos and promote professional fumigation practices. In Nigeria, grain merchant associations now conduct mandatory certification workshops, while Ghana’s adoption of CO₂ hermetic liners for organic export lots is attracting technology providers. Although knowledge gaps remain, increasing food security concerns are ensuring continued policy focus in the region.

North America and Europe represent mature markets characterized by innovation-driven growth. In North America, the Environmental Protection Agency (EPA’s) ongoing registration reviews are tightening exposure guidelines, prompting operators to adopt IoT-enabled gas-monitoring equipment. In Europe, fluctuations in energy prices are encouraging some grain storage facilities to adopt low-temperature controlled atmospheres to reduce aeration costs. Meanwhile, South America is projected to grow during the forecast period, driven by Brazil’s USD 88.2 billion 2024/25 farm credit program, which links loan disbursements to post-harvest infrastructure development. Across all regions, differentiation remains critical, with suppliers needing to adapt product offerings to align with local residue regulations, crop types, and infrastructure maturity to succeed in the grain fumigants market.

Competitive Landscape

In 2024, the grain fumigants market exhibited moderate concentration, with the top five players accounting for a significant portion of total revenue. UPL Limited stood out, supported by its vertically integrated capabilities in active-ingredient synthesis and an extensive distribution footprint spanning 130 countries. Detia Degesch Group maintained a strong position due to its long-standing expertise in aluminum phosphide and a physical presence across all major grain-producing regions.

Douglas Products and Syensqo built competitive advantages through their respective patent portfolios in phosphine and sulfuryl fluoride technologies, while Cardinal Professional Products maintained a solid foothold by focusing on service coverage throughout North America. Strategic developments in 2024–2025 reflected trends in horizontal expansion and digital innovation. In 2024, Ecotec (Rentokil Initial Plc) acquired HiCare in India to boost service density and broaden its fumigation offerings to commercial grain millers. In 2024, GrainPro received approval from India's Directorate of Plant Protection, Quarantine, and Storage (DPPQ&S) for its CO₂-based Cocoon system, further solidifying its position at the forefront of eco-friendly fumigation solutions.

UPL Limited and Syensqo collaborated on the development of sensor-integrated tablets linked to mobile dashboards, streamlining compliance and documentation for HACCP audits. As regulatory demands grow more complex, competitive pressures are anticipated to intensify. Nevertheless, smaller regional firms can still succeed by focusing on niche crops or offering monitoring technologies that enhance the value propositions of larger multinational chemical portfolios.

Grain Fumigants Industry Leaders

UPL Limited

Detia Degesch Group

Ecotec (Rentokil Initial plc)

Syensqo

Douglas Products

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The Environmental Protection Agency (EPA) approved an amendment to the ProFume (sulfuryl fluoride) label for use in food-handling facilities and grain warehouses, adding stricter stewardship and site-specific fumigation logging provisions. This enhances compliance and traceability in commercial grain fumigation.

- November 2024: Detia Degesch Group established a dedicated Organic Division to focus on green fumigation solutions and low-residue formulations. This move aligns with increasing global demand for residue-free grain protection and regulatory pressure favoring bio-based or safer alternatives to traditional phosphide fumigants.

- January 2024: Degesch America, Inc. launched U‑Phos, a cylinderized phosphine fumigant, in the United States. This gas-based alternative to tablets/pellets offers residue-free fumigation and simplified disposal, strengthening its positioning in the grain fumigants market.

Global Grain Fumigants Market Report Scope

| Aluminum Phosphide |

| Magnesium Phosphide |

| Phosphine Gas |

| Sulfuryl Fluoride |

| Carbon Dioxide |

| Others |

| Solid Tablets and Pellets |

| Liquid |

| Gas |

| Commercial Grain Elevators |

| On-farm Silos |

| Shipping Containers and Barges |

| Warehouse and Transit Storage |

| Wheat |

| Corn |

| Rice |

| Sorghum and Millet |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Chemical Type | Aluminum Phosphide | |

| Magnesium Phosphide | ||

| Phosphine Gas | ||

| Sulfuryl Fluoride | ||

| Carbon Dioxide | ||

| Others | ||

| By Form | Solid Tablets and Pellets | |

| Liquid | ||

| Gas | ||

| By End-Use Facility | Commercial Grain Elevators | |

| On-farm Silos | ||

| Shipping Containers and Barges | ||

| Warehouse and Transit Storage | ||

| By Crop Type | Wheat | |

| Corn | ||

| Rice | ||

| Sorghum and Millet | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the grain fumigants market?

The market stands at USD 1.45 billion in 2025 and is projected to reach USD 1.93 billion by 2030.

Which chemical type holds the largest market share?

Aluminum phosphide leads with 41% of grain fumigants market share in 2024.

Why is Asia-Pacific the dominant regional market?

The region combines massive wheat and rice output with rapid modernization of storage facilities that require professional fumigation services.

How do regulations influence market growth?

Stricter phytosanitary import rules and the phase-out of methyl bromide compel exporters to adopt certified phosphine-based or CO₂ systems, sustaining demand.

Page last updated on: