Agentic AI In Media, Entertainment, And Content Creation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

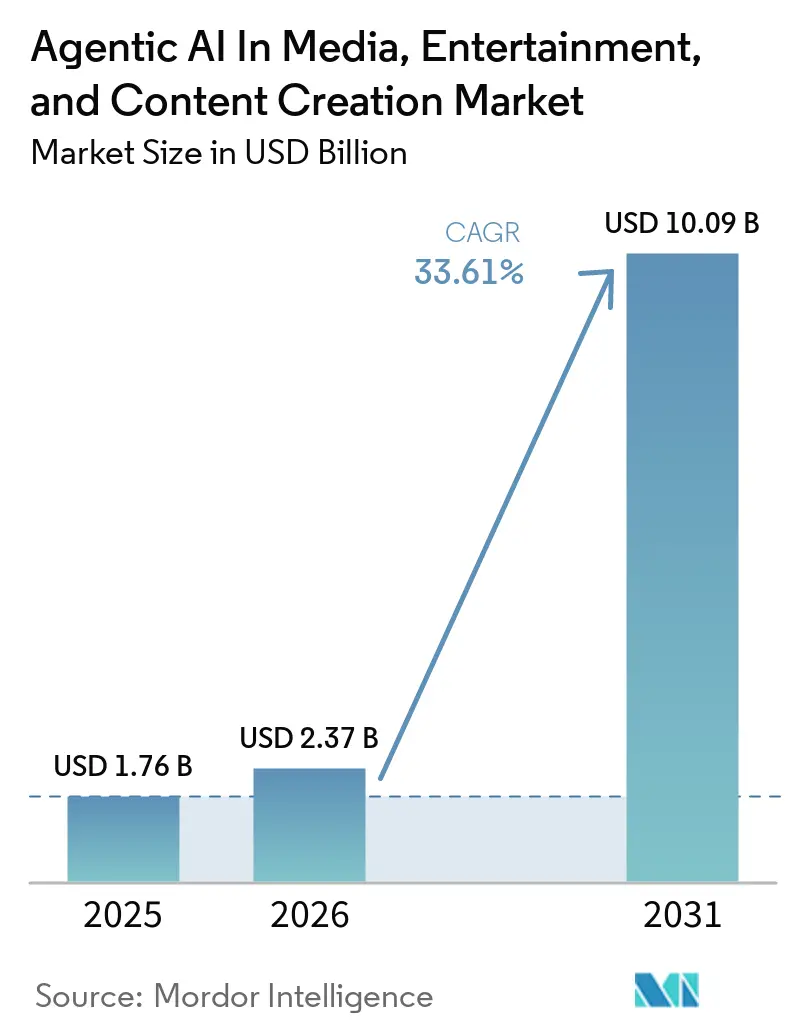

| Market Size (2026) | USD 2.37 Billion |

| Market Size (2031) | USD 10.09 Billion |

| Growth Rate (2026 - 2031) | 33.61% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agentic AI In Media, Entertainment, And Content Creation Market Analysis by Mordor Intelligence

The Agentic AI market size in media, entertainment, and content creation is expected to grow from USD 1.76 billion in 2025 to USD 2.37 billion in 2026, and is forecast to reach USD 10.09 billion by 2031 at a 33.61% CAGR over 2026-2031. Adoption is moving beyond isolated assistive tools as multi-agent orchestration frameworks mature, letting studios and independent creators automate script breakdown, asset tagging, and metadata generation with minimal oversight. A 70% decline in generative-AI inference costs between 2024 and 2025 opened studio-grade capabilities to small teams, while hyperscalers’ 40% cuts to cloud-GPU prices removed major compute barriers. Virtual production stages expanded in Los Angeles, London, and Atlanta, proving real-time LED volumes can shorten location shoots and shrink logistical costs. Simultaneously, streaming platforms’ appetite for hyper-personalized libraries pushed recommendation engines to guide more than 80% of viewer choices, cementing AI as a revenue lever rather than an experimental add-on.

Key Report Takeaways

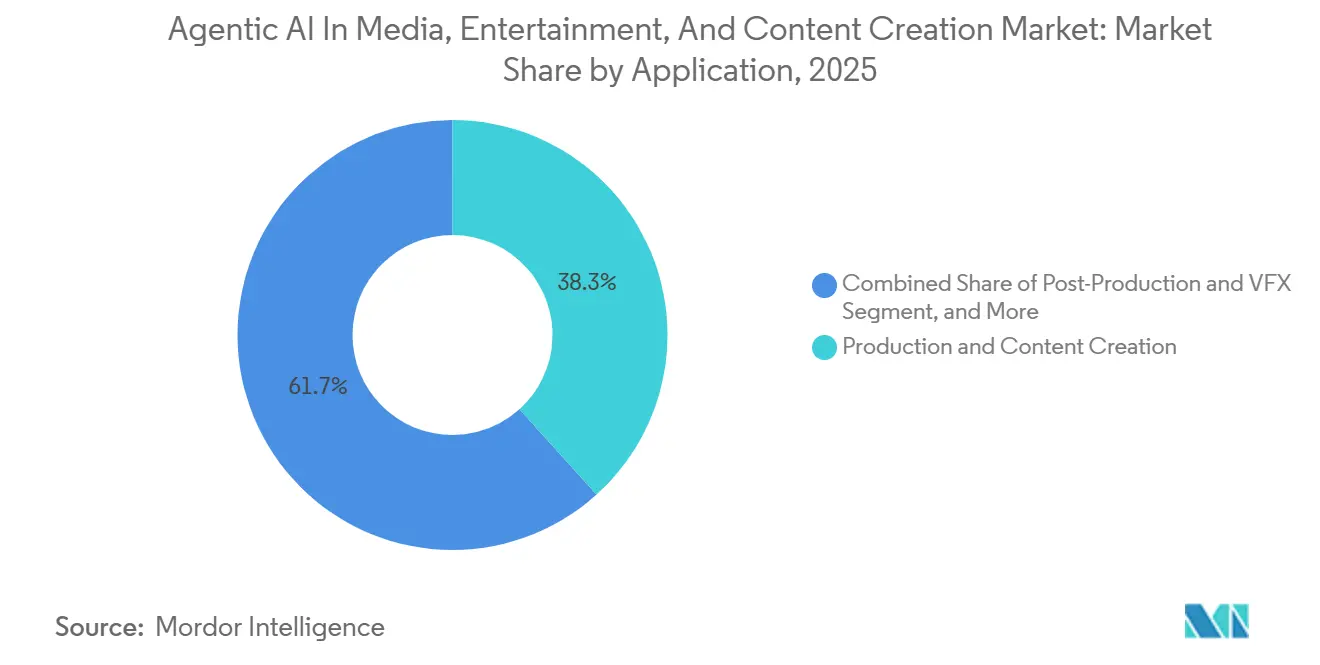

- By application, production and content creation led with 38.31% of 2025 revenue, while localization and translations is projected to post the fastest 34.81% CAGR to 2031.

- By AI autonomy level, assistive AI accounted for 51.24% of the market in 2025, whereas fully agentic AI is forecast to expand at a 34.21% CAGR through 2031.

- By deployment model, cloud held 61.89% share during 2025, yet hybrid architectures are on track for the highest 34.18% CAGR over the forecast window.

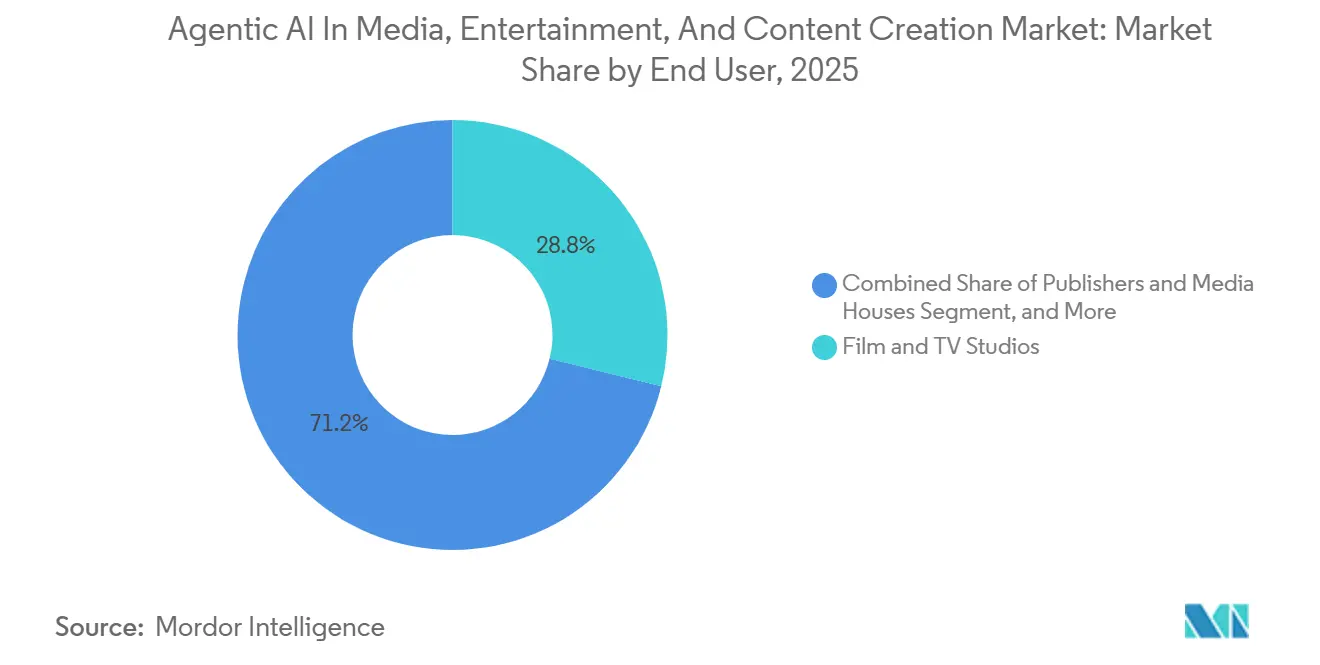

- By end user, film and TV studios captured 28.83% of 2025 sales, but independent creators and SMEs are expected to grow at a 34.61% CAGR through 2031.

- By component, software platforms represented 54.33% of the 2025 value, while services are anticipated to grow fastest at a 33.56% CAGR to 2031.

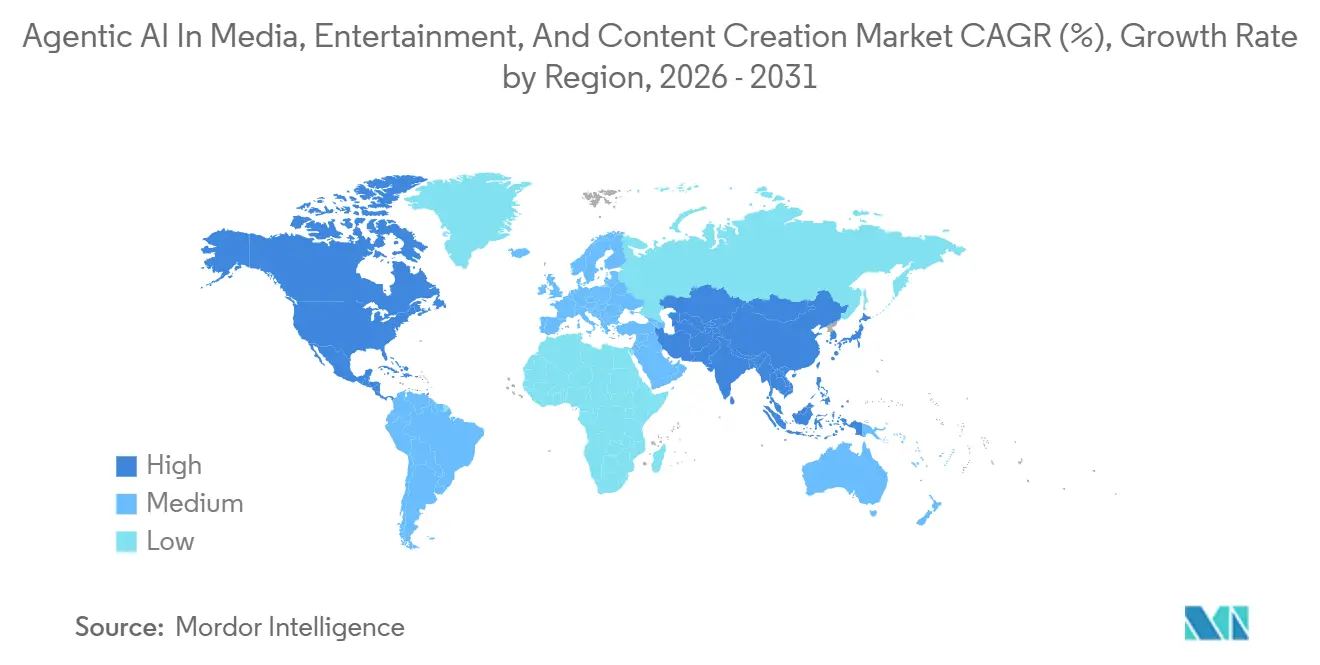

- By geography, North America contributed 37.72% of 2025 revenue, although Asia-Pacific is positioned for the strongest 34.59% CAGR across the outlook.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agentic AI In Media, Entertainment, And Content Creation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generative AI Cost Declines Enabling Indie Creators | +6.2% | Global, with concentration in North America, Europe, and Asia-Pacific urban centers | Short term (≤ 2 years) |

| Streaming Platforms' Demand for Hyper-Personalized Content | +5.8% | Global, led by North America and Europe; rapid adoption in Asia-Pacific | Medium term (2-4 years) |

| Rise of Virtual Production Stages in Film-Making | +4.9% | North America and Europe core, expanding to Middle East and Asia-Pacific | Medium term (2-4 years) |

| Cloud-GPU Price Wars Among Hyperscalers | +4.3% | Global, with highest impact in North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Generative Voice and Dubbing Tools Localizing Back-Catalogs | +3.7% | Global, with outsized gains in Asia-Pacific, South America, and Middle East and Africa | Long term (≥ 4 years) |

| Foundation Model Fine-Tuning Marketplaces | +2.9% | North America and Europe early adopters, spillover to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Generative AI Cost Declines Enabling Indie Creators

A 70% drop in inference pricing between early 2024 and late 2025 lowered entry barriers and allowed YouTube producers to complete minute-long videos for under USD 50. Funding flowed to AI-native outfits such as Sozee and Channel Farm, which automate scripting, storyboard creation, and asset generation. No-code orchestration tools that chain OpenAI, Anthropic, and Cohere models removed the need for engineering talent. OpenAI's pricing for GPT-4 Turbo dropped from USD 0.03 per 1,000 tokens in January 2024 to USD 0.01 by December 2025, while image-generation costs on platforms like Midjourney and Stability AI fell below USD 0.01 per frame, enabling creators to produce short-form video content for under USD 50 per minute of finished output.[1]OpenAI Pricing, “GPT-4 Turbo Pricing Updates,” openai.com As costs fall further, independent creators seize long-tail niches that large studios overlook, reshaping the volume and diversity of new releases.

Streaming Platforms’ Demand for Hyper-Personalized Content

Recommendation engines now influence more than four out of five viewing hours, and services like Disney+ and Spotify embed generative AI to craft localized trailers, thumbnails, podcast intros, and even alternate story arcs. Research indicates that tailored experiences can increase retention by up to 25%, translating into billions in additional recurring revenue. This economic logic drives platforms to adopt semi-agentic systems that generate and tag content at scale while adhering to cultural nuance and regional rules.

Rise of Virtual Production Stages in Film-Making

LED volumes of 18,000-20,000 square feet came online in Los Angeles, London, and Atlanta during 2025, enabling crews to capture complex indoor scenes and cut location costs by up to 40%. Asia-Pacific facilities followed China and South Korea, while Unreal Engine 5 updates enabled photorealistic digital humans and AI-driven motion-matching. The result is a compressed feedback loop between creative intent and on-screen output, placing virtual stages at the center of future production roadmaps.

Cloud-GPU Price Wars Among Hyperscalers

Hourly rates on top-tier NVIDIA H100 instances dropped by roughly one-third in 2025 as Amazon Web Services, Microsoft Azure, and Google Cloud competed for AI workloads. Lower compute pricing made real-time rendering and agentic orchestration routine rather than budget-draining luxuries. Studios now mix reserved, on-demand, and spot instances to optimize cost, driving broader reliance on cloud and nudging on-premises operators toward hybrid models for latency-sensitive tasks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ethical Concerns Over Synthetic Actors and Deepfakes | -3.4% | Global, with heightened regulatory scrutiny in North America and Europe | Short term (≤ 2 years) |

| High IP Licensing Costs for Model Training | -2.8% | Global, with most acute impact in North America and Europe due to litigation | Medium term (2-4 years) |

| Regulatory Uncertainty Around AI-Generated Content | -2.1% | North America, Europe, and Asia-Pacific; evolving frameworks in Middle East and South America | Long term (≥ 4 years) |

| Compute Supply Bottlenecks for Agentic Orchestration | -1.6% | Global, with concentration in regions lacking hyperscaler infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ethical Concerns Over Synthetic Actors and Deepfakes

The Screen Actors Guild secured contract clauses in 2025 that require consent and residuals for the use of digital likeness, reducing compliance costs for studios. High-profile lawsuits, including a USD 5 million settlement involving an unauthorized AI replica of a major actor, highlighted legal exposure. Surveys show most consumers favor stricter rules on synthetic media, and EU regulations now mandate watermarking. Companies must embed consent management and disclosure into workflows or risk reputational damage and enforcement penalties.

High IP Licensing Costs for Model Training

Pending lawsuits from publishers and media houses over the use of unlicensed datasets pushed developers to strike multi-million-dollar agreements for archive access. A paradox emerged, firms pay steep fees to ingest copyrighted content, yet AI-only outputs remain ineligible for copyright protection in many jurisdictions. Licensing can absorb up to one-fifth of model budgets, favoring vendors that secure early, broad content deals or pivot toward synthetic training datasets. The United States Copyright Office's 2025 guidance reiterated that AI-generated works lacking human authorship cannot be copyrighted, creating a paradox, companies must license copyrighted material to train models, yet the output may not qualify for copyright protection, complicating monetization strategies.[2]U.S. Copyright Office, “AI-Generated Works and Copyright Eligibility,” copyright.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Localization Gains Momentum as Catalogs Go Global

The Agentic AI market in media, entertainment, and content creation recorded a 38.31% share in production and content creation in 2025, reflecting widespread adoption of generative video editors and AI-assisted asset builders. Studios shortened editing cycles from weeks to days and cut concept-art costs by up to 40%. In contrast, localization and translations are projected to post a 34.81% CAGR through 2031, fueled by multilingual voice cloning that unlocks archival libraries for Hindi, Portuguese, and Arabic audiences at a fraction of prior re-dubbing costs.

Localization technology now replicates tone and cadence across 32 languages with 95% fidelity, enabling platforms to refresh back catalogs and expand addressable markets quickly. As a result, the Agentic AI market size in media, entertainment, and content creation, tied to localization roles, is poised to expand far faster than legacy tasks such as color grading. Studios also harness post-production AI for mask removal, frame interpolation, and 4K upscaling, further compressing workloads previously handled by large VFX teams.

By AI Autonomy Level: Fully Agentic Systems Move From Trials to Production

Assistive AI maintained 51.24% of 2025 spending as creators relied on text-prompt editors and image generators to augment manual workflows. Semi-agentic solutions added structured autonomy, chaining subtasks while still requiring user approval at decision nodes. Looking ahead, fully agentic systems should log a 34.21% CAGR to 2031, driven by function-calling large language models that query databases, schedule renders, and publish assets without human mediation.

In content moderation and real-time subtitle creation, fully agentic deployments already shrink turnaround from hours to minutes. Yet scriptwriting and cinematography remain assistive domains where human taste carries premium value. Providers that map autonomy levels to task complexity will achieve optimal productivity, pushing the Agentic AI market share of full agents in media, entertainment, and content creation higher without alienating creative teams.

By Deployment Model: Hybrid Approaches Reconcile Compliance and Elasticity

Cloud stood at 61.89% of 2025 revenue because on-demand GPUs removed capital hurdles for rendering, model training, and multi-agent orchestration. Enterprises embraced reserved and spot pricing strategies, slashing per-frame costs by 30-40%. Even so, hybrid architectures are on track for a 34.18% CAGR, balancing cloud elasticity with on-premises control over proprietary footage governed by data-residency laws.

Under a hybrid blueprint, latency-sensitive captions or live-sports highlights run on local servers, while archival analysis and back-catalog remastering shift to the cloud. This workload placement flexibility safeguards compliance with regulations such as the EU’s GDPR and China’s Data Security Law while still leveraging hyperscalers’ declining GPU prices, strengthening overall Agentic AI market resilience in media, entertainment, and content creation.

By End-User: Democratized Tools Propel Creator Economy Growth

Film and TV studios occupied 28.83% of 2025 spending as they integrated AI for script scoring, virtual storyboards, and predictive audience analytics. Yet independent creators and SMEs are forecast to grow at a 34.61% CAGR as low-code editors and text-to-video models enable them to publish daily shorts and niche explainers. The Agentic AI market in media, entertainment, and content creation is growing quickly, driven by platforms that reward rapid iteration over high-budget polish.

Publishers and media houses employ generative tools for headline testing and newsletter curation, but tread cautiously to protect editorial trust. Advertising agencies automate campaign versioning across 100+ markets in under 48 hours, while game studios deploy AI to animate characters and draft environments at AAA quality for a fraction of historical cost. This rebalancing disperses creative authority, reshaping supply chains long dominated by Hollywood majors.

By Component: Services Capture Value as Enterprises Seek Turnkey Execution

Software platforms generated 54.33% of 2025 revenue, driven primarily by suites that integrate advanced features such as generative fill, video synthesis, and real-time rendering, which are increasingly being adopted across various design workflows. These platforms enable businesses to streamline creative processes, enhance productivity, and reduce time-to-market for their products. Meanwhile, services that include integration, fine-tuning, and managed orchestration are projected to grow the fastest, with a compound annual growth rate (CAGR) of 33.56% through 2031. This growth is attributed to enterprises focusing on immediate returns on investment (ROI) by leveraging ready-made solutions rather than investing time and resources into building proprietary AI stacks from scratch. These services provide businesses with the flexibility and scalability needed to adapt to evolving market demands efficiently.

Consulting firms now bundle vertical templates that compress deployment from six months to eight weeks, steering clients toward best-practice pipelines and governance frameworks. Hardware accelerators, GPUs, and specialized inference chips remain essential but are often consumed via cloud instances, masking direct sales. Vendors coupling software subscriptions with white-glove services are positioned to command premium pricing and reinforce switching costs, thereby increasing their Agentic AI market share in the media, entertainment, and content creation markets.

Geography Analysis

North America delivered 37.72% of 2025 revenue thanks to Hollywood’s early investment in LED volumes and Silicon Valley’s concentration of foundation-model labs. U.S. studios benefit from flexible, sector-specific regulation, although new union clauses on synthetic likenesses tighten permissible use. Canada’s 58% VFX tax credit has attracted overseas post-production work to Vancouver, while Mexico’s nearshore facilities offer cost advantages for episodic shoots, keeping the regional Agentic AI market stable yet distributed across media, entertainment, and content creation.

Asia-Pacific is projected to register a 34.59% CAGR through 2031, fueled by China’s mass-market Douyin video avatars, Japan’s AI-assisted anime in-betweening that offsets skilled-labor shortages, and India’s 200 million-strong creator base leveraging local-language text-to-video generation. ByteDance's 2025 rollout of AI-generated video avatars on Douyin, which allows users to create personalized content without filming, reached over 100 million users within six months, demonstrating the scale at which Chinese platforms can deploy agentic systems.[3]ByteDance Newsroom, “AI-Generated Video Avatars on Douyin,” bytedance.com South Korea’s mobile game leaders are integrating AI assets to reduce level design time by roughly 40%, reinforcing the region’s upward trajectory and closing the revenue gap with North America.

Europe continues to demonstrate strong adoption of advanced technologies, driven by the United Kingdom's innovative virtual stages and Germany's highly specialized VFX studios. However, the region faces challenges that could impact its growth trajectory, particularly due to the compliance costs associated with the EU AI Act and the mandatory watermarking requirements. These regulatory measures may slow down growth when compared to the more dynamic markets of North America and Asia-Pacific. On the other hand, South America, the Middle East, and Africa, while currently smaller markets, are showing promising potential. Brazil’s USD 500 million investment in the gaming sector is expected to drive significant advancements, while the United Arab Emirates is actively fostering growth through sovereign AI incentives. These incentives aim to establish post-production hubs in key locations such as Abu Dhabi and Dubai, signaling the emergence of budding hotspots that could help increase regional market share by 2031.

Competitive Landscape

Application-layer competition remains moderately fragmented, with more than 50 startups competing in the voice cloning, script generation, and automated editing niches. Infrastructure is converging, with hyperscalers absorbing compute demand and foundation-model vendors locking multi-year studio deals. Adobe, NVIDIA, and Microsoft wield vertical integration, embedding Firefly across Creative Cloud, tying Omniverse to GPU sales, and bundling GPT-4 Turbo with Azure media APIs, which encourages customer lock-in.[4]NVIDIA Omniverse, “Rendering and AI Inference Integration,” nvidia.com

Challengers Runway, Stability AI, and Synthesia specialize in generative video, open-weight diffusion, and synthetic presenters to sidestep broad-suite incumbents. Partnerships such as Epic Games-WPP create combined content engines, while acquisition chatter around video-AI upstarts underlines accelerating consolidation. White-space opportunities lie in automated rights management, consent tracking, and watermark verification, where no clear leader exists despite mounting compliance pressure.

Open-source hubs democratize access, eroding proprietary pricing power, while GPU makers build software ecosystems that raise switching costs. Winning positions will cluster either around compute and foundational models or workflow orchestration and compliance tooling. Pure-play application vendors risk margin compression unless they secure defensible data moats or specialized IP aligned with expanding Agentic AI in media, entertainment, and content creation market demands.

Agentic AI In Media, Entertainment, And Content Creation Industry Leaders

Adobe Inc.

NVIDIA Corporation

Alphabet Inc.

Amazon Web Services, Inc.

OpenAI L.L.C.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: OpenAI launched GPT-5 with native video understanding and generation capabilities, enabling developers to perform text-to-video analytics.

- March 2026: NVIDIA unveiled the H200 GPU, boosting inference throughput by 40% compared with the H100 and lowering cost per token by nearly one-third.

- February 2026: Adobe acquired Frame.io for USD 1.275 billion, integrating real-time review and approval inside Creative Cloud video workflows.

- January 2026: Unity and Microsoft partnered to embed the Azure OpenAI Service into Unity tools, letting 1.5 million developers generate assets through natural-language prompts.

Global Agentic AI In Media, Entertainment, And Content Creation Market Report Scope

The Agentic AI in Media, Entertainment, and Content Creation Market refers to the global industry focused on the development, deployment, and commercialization of autonomous and semi-autonomous artificial intelligence systems designed to perform, coordinate, and optimize creative, production, operational, and decision-making tasks across media and entertainment workflows. Agentic AI systems leverage technologies such as large language models (LLMs), generative AI, multimodal AI, computer vision, speech synthesis, reinforcement learning, and autonomous workflow orchestration to independently execute or assist with tasks including content generation, editing, localization, visual effects, audience engagement, and production management.

The Agentic AI in Media, Entertainment, and Content Creation Market Report is Segmented by Application (Production and Content Creation, Post-Production and VFX, Marketing and Advertising, Gaming and Interactive Media, Broadcast and Streaming Operations, and Localisation and Translations), AI Autonomy Level (Assistive AI, Semi-Agentic AI, and Fully Agentic AI), Deployment Model (On-Premises, Cloud, and Hybrid), End-User (Film and TV Studios, Publishers and Media Houses, Advertising and Creative Agencies, Game Studios, and Independent Creators and SMEs), Component (Software Platforms, Services, and Hardware Accelerators), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Production and Content Creation |

| Post-Production and VFX |

| Marketing and Advertising |

| Gaming and Interactive Media |

| Broadcast and Streaming Operations |

| Localisation and Translations |

| Assistive AI |

| Semi-Agentic AI |

| Fully Agentic AI |

| On-Premises |

| Cloud |

| Hybrid |

| Film and TV Studios |

| Publishers and Media Houses |

| Advertising and Creative Agencies |

| Game Studios |

| Independent Creators and SMEs |

| Software Platforms |

| Services |

| Hardware Accelerators |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Application | Production and Content Creation | ||

| Post-Production and VFX | |||

| Marketing and Advertising | |||

| Gaming and Interactive Media | |||

| Broadcast and Streaming Operations | |||

| Localisation and Translations | |||

| By AI Autonomy Level | Assistive AI | ||

| Semi-Agentic AI | |||

| Fully Agentic AI | |||

| By Deployment Model | On-Premises | ||

| Cloud | |||

| Hybrid | |||

| By End-User | Film and TV Studios | ||

| Publishers and Media Houses | |||

| Advertising and Creative Agencies | |||

| Game Studios | |||

| Independent Creators and SMEs | |||

| By Component | Software Platforms | ||

| Services | |||

| Hardware Accelerators | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and growth outlook for the Agentic AI in media, entertainment, and content creation market?

The market stands at USD 2.37 billion in 2026 and is projected to reach USD 10.09 billion by 2031, advancing at a 33.61% CAGR according to Mordor Intelligence.

Which application area is expanding fastest within this space?

Localization and translations show the strongest momentum, expected to grow at a 34.81% CAGR as studios use AI voice cloning and dubbing to monetize global back catalogs.

Why are hybrid deployment models gaining popularity among media companies?

Hybrid models help studios keep sensitive assets on-premises for compliance while tapping cloud elasticity and recently lower GPU prices for rendering spikes.

How are independent creators affecting the competitive landscape?

Affordable generative tools let small teams publish high-volume short-form content, driving a forecast 34.61% CAGR for the independent creator segment and challenging traditional studio economics.

What are the main ethical hurdles facing agentic AI adoption?

Consent requirements for digital likenesses and deepfake watermark mandates raise compliance costs and expose companies to litigation if they deploy synthetic actors without clear rights.

Which regions will likely add the most incremental revenue through 2031?

Asia-Pacific, led by China, Japan, and India, is projected for a 34.59% CAGR thanks to massive user bases, mobile-first consumption, and rapid platform integration of generative video.

Page last updated on: