Agentic AI Frameworks Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.11 Billion |

| Market Size (2031) | USD 19.32 Billion |

| Growth Rate (2026 - 2031) | 36.28% CAGR |

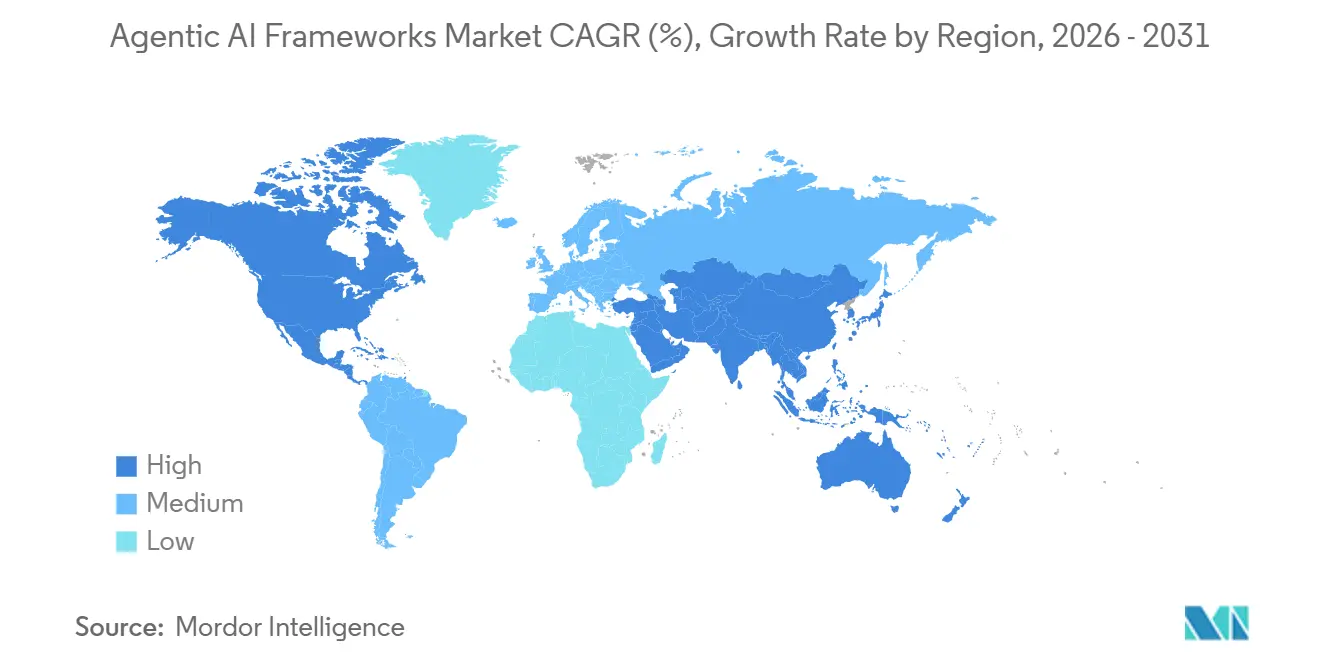

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agentic AI Frameworks Market Analysis by Mordor Intelligence

The agentic AI frameworks market size is expected to grow from USD 2.99 billion in 2025 to USD 4.11 billion in 2026 and is forecast to reach USD 19.32 billion by 2031 at 36.3% CAGR over 2026-2031. The shift from passive generative tools to autonomous systems enables enterprises to streamline workflows with minimal human input. Agents are now used as operating layers across departments, business rules, and software systems, rather than just front-end assistants. The Model Context Protocol, with over 11,000 active public servers by early 2026, demonstrates faster integration-layer maturity than market penetration, enabling earlier production use. North America leads due to its concentration of cloud vendors, framework developers, and enterprise buyers, while Asia-Pacific sees rapid growth driven by policy support and software capacity. Competition intensifies among platform providers bundling orchestration into cloud environments, but open-source tools continue to influence developer choices, keeping the agentic AI frameworks market dynamic.

Key Report Takeaways

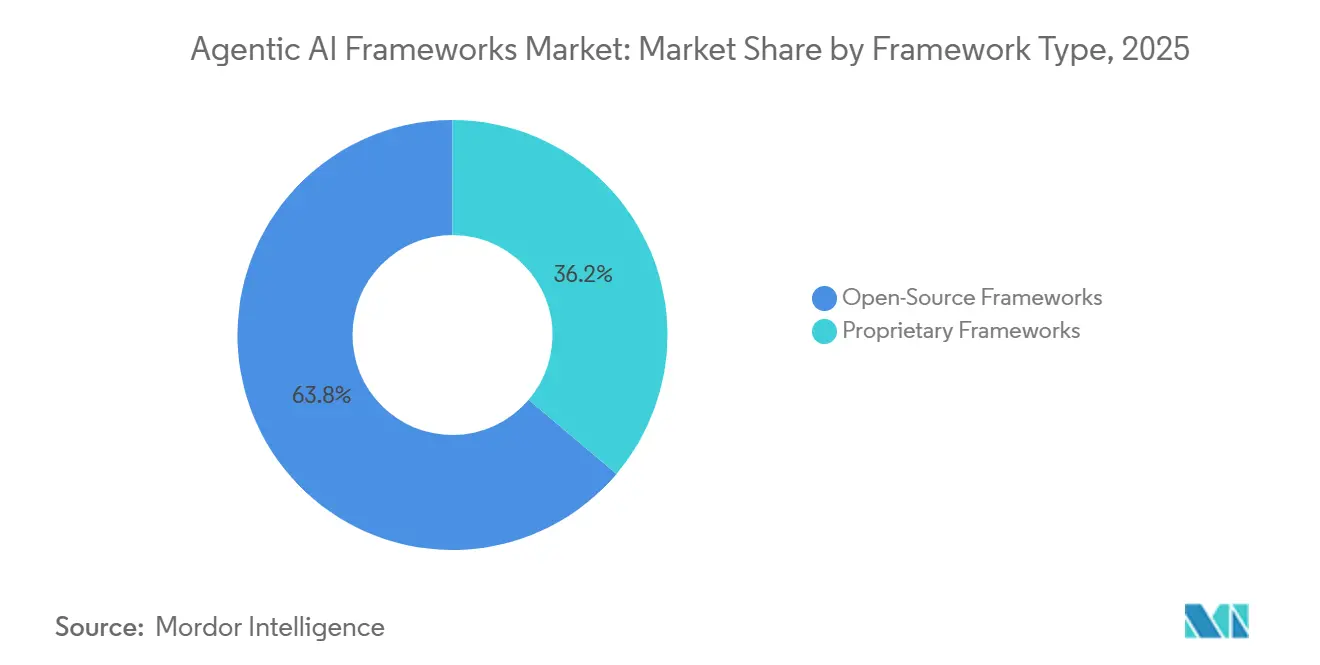

- By framework type, open-source solutions held 63.81% share of the agentic AI frameworks market in 2025, while proprietary frameworks are projected to expand at a 36.68% CAGR through 2031.

- By deployment mode, cloud-hosted deployments held 71.32% share of the agentic AI frameworks market in 2025, while on-premises and edge deployments are projected to grow at a 36.63% CAGR through 2031.

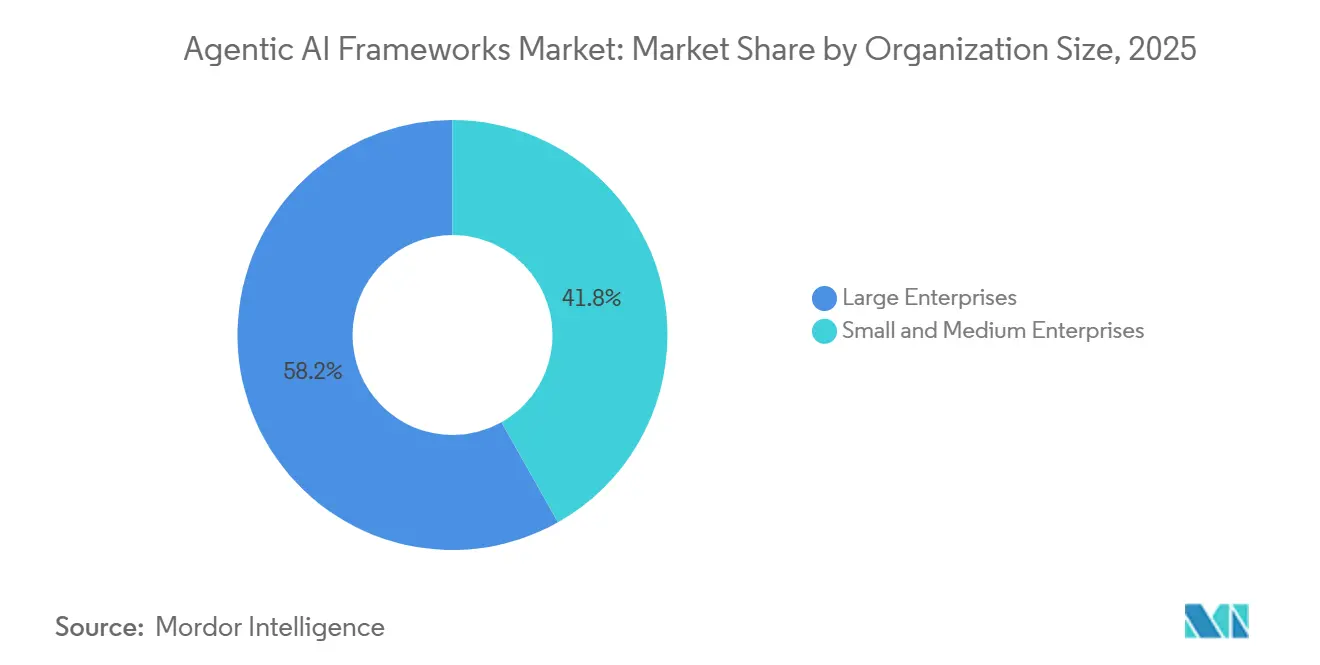

- By organization size, large enterprises accounted for 58.16% share of the agentic AI frameworks market in 2025, while small and medium enterprises are forecast to grow at a 36.59% CAGR through 2031.

- By end-user industry, ICT and software development accounted for 32.89% share of the agentic AI frameworks market in 2025, while healthcare and life sciences are projected to advance at a 37.48% CAGR through 2031.

- By geography, North America held 37.51% of global revenue of the agentic AI frameworks market in 2025, while Asia-Pacific is forecast to grow at a 37.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agentic AI Frameworks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Autonomous Agents in Enterprise Workflows | +8.5% | Global, with highest intensity in North America and Western Europe | Short term (≤ 2 years) |

| Rapid Advances in Generative AI Model Capabilities | +7.2% | Global, concentrated in North America and APAC core | Short term (≤ 2 years) |

| Rising Investments by Big Tech and Venture Capital | +6.4% | North America primary, spillover to Europe and APAC | Short term (≤ 2 years) |

| Scalability Benefits of Framework-Agnostic Tooling | +5.1% | Global | Medium term (2-4 years) |

| Emergence of AI Function Calling Standards | +4.3% | Global, led by North America with early gains in the EU and Japan | Medium term (2-4 years) |

| Integration of Agentic Frameworks Into Low-Code Platforms | +3.8% | North America and Europe, with spillover to APAC and the Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Autonomous Agents in Enterprise Workflows

Enterprise demand in the agentic AI frameworks market has moved beyond isolated chatbot pilots and into production systems that coordinate work across teams. IBM reported in May 2026 that 82% of C-suite executives identified functional silos as the main barrier to AI value extraction, and 60% planned next-generation delivery structures in which AI agents coordinate workflows across departments.[1]IBM Institute for Business Value, “Agentic AI Workflows and Enterprise Operations,” IBM Institute for Business Value, ibm.com That shift changes buying behavior because enterprises now want memory, tool use, approvals, and escalation paths in one governed flow. The value case is strongest where agents can manage repetitive handoffs between departments instead of answering one prompt at a time. This is also pushing organizations to redesign workflows before deployment, since agent performance depends on how tasks, context, and accountability move across the business. Projects that add agents to unchanged processes face a higher cancellation risk, so workflow architecture is becoming nearly as important as framework selection in the agentic AI frameworks market.

Rapid Advances in Generative AI Model Capabilities

Rapid model progress is widening the production scope of the agentic AI frameworks market. Frontier models now combine stronger tool use with longer context windows, reducing the manual prompting required to slow production deployment. Microsoft said its April 2026 release of GPT-5.5 on Microsoft Foundry was designed for more reliable agentic execution, stronger long-context reasoning, and better token efficiency. Microsoft also made Claude Opus 4.6 available in Foundry, with a 1-million-token context window for coding, agents, and enterprise workflows. These gains matter because they make multi-step orchestration more stable and lower the cost penalty that once limited agent pipelines to narrow pilots. Google DeepMind noted that compute available for the largest training runs rose by around 300,000x between 2012 and 2018 and continued to grow at an annual pace of around 4x through 2024, which helps explain why capability ceilings and efficiency are moving together.

Rising Investments by Big Tech and Venture Capital

Capital spending in the agentic AI frameworks market is moving from single model bets toward orchestration, memory, and tooling layers. LangChain raised USD 125 million in October 2025, with Cisco Investments, ServiceNow Ventures, and Workday Ventures joining the round, indicating that strategic investors want direct ties to the framework layer. Neo4j committed USD 100 million in October 2025 to GenAI and agentic AI innovation and positioned graph infrastructure as a memory layer for complex agent deployments. This funding pattern is widening the number of enterprise-grade products that can support governed deployment, observability, and workflow integration. It also shows that large platform vendors do not view orchestration as a temporary add-on, but as a control point that can pull more workload into their broader software stacks. As a result, buyers are seeing more product maturity, faster feature cycles, and tighter partnerships between framework vendors and enterprise software channels across the agentic AI frameworks market.

Scalability Benefits of Framework-Agnostic Tooling

Interoperability is becoming a major purchase criterion in the agentic AI frameworks market because enterprises do not want to rebuild integrations whenever the model or framework mix changes. Google Cloud described MCP as an open standard that connects AI applications to external data sources and tools through a common interface. That structure reduces the custom N-by-M integration burden to a single protocol layer, making it easier to swap components without rewriting the entire application. The World Economic Forum noted that the Agent-to-Agent protocol has gained backing from more than 50 technology partners, including AWS, Cisco, IBM, SAP, Salesforce, and ServiceNow, which also extends interoperability across agent boundaries. Standards support portability and improve governance by making it easier to document tool calls, handoffs, and permissions in a common format. Organizations that align early with open protocol layers are likely to carry less technical debt as the agentic AI frameworks market consolidates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Analysis |

|---|---|---|---|

| Persistent Concerns Around AI Safety and Alignment | -3.2% | Global, most acute in the EU and U.S. regulated sectors | Long term (≥ 4 years) |

| Lack of Skilled Workforce for Multi-Agent Orchestration | -2.8% | Global, especially APAC developing markets and South America | Medium term (2-4 years) |

| High Compute Costs for Large-Scale Agent Simulations | -2.1% | Global, disproportionate in data-dense verticals | Short term (≤ 2 years) |

| Fragmentation Due to Divergent Prompt Engineering Dialects | -1.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Concerns Around AI Safety and Alignment

Safety and alignment remain a structural brake on the agentic AI frameworks market because multi-agent errors can compound across memory, tools, and chained decisions. The World Economic Forum said that evaluation and governance for AI agents still need stronger foundations, especially as systems operate with greater autonomy within business processes.[2]World Economic Forum, “AI Agents in Action, Foundations for Evaluation and Governance,” World Economic Forum, reports.weforum.org The risk is not limited to wrong answers, since agents can also escalate privileges, expose data, or trigger actions that are hard to trace after several handoffs. This keeps regulated buyers focused on audit trails, human oversight, and runtime controls before they scale deployment. The August 2026 activation of the EU AI Act high-risk provisions adds another layer of caution for enterprises that need conformity documentation and incident logging. Until security teams can monitor agent behavior with the same confidence they apply to other enterprise systems, some high-value deployments in the agentic AI frameworks market will move more slowly than the technology itself.

Lack of Skilled Workforce for Multi-Agent Orchestration

The skills gap in multi-agent orchestration is slowing the rollout of agentic AI frameworks, especially outside the deepest enterprise engineering hubs. The Partnership on AI found that organizations still lack shared terminology and practical governance templates for assessing autonomy levels, control mechanisms, and escalation rules in enterprise AI systems. That weakness increases reliance on system integrators and slows debugging when several agents, tools, and memory layers interact within a single workflow. Low-code products help teams launch earlier pilots, but they do not remove the need for production skills in orchestration design, monitoring, and exception handling. The shortage is more than a coding issue because many failures stem from weak process design, fragmented data architecture, or unclear accountability between human teams and agents. Until enterprises build repeatable operating models and internal training paths, adoption will remain uneven across regions and end users in the agentic AI frameworks market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Framework Type: Open-Source Leadership, Proprietary Momentum

Open-source frameworks held 63.81% of the agentic AI frameworks market share in 2025. That lead came from developers' preference for composability, auditability, and broad integration across models, vector stores, and enterprise data systems. LangChain said in October 2025 that LangChain and LangGraph reached 90 million combined monthly downloads and that 35% of Fortune 500 companies used its services. The same update pointed to production use across large enterprises, which helps explain why open-source tools still shape engineering standards even when buyers later purchase commercial support.

Open-source leadership does not remove its own friction, since rapid release cycles and breaking API changes can create internal rework for teams already in production. That instability is helping proprietary vendors close the production gap, and proprietary frameworks are projected to grow at a 36.68% CAGR through 2031. Microsoft said the Foundry Agent Service supports LangGraph, the Claude Agent SDK, and the OpenAI Agents SDKs in a single, governed runtime, demonstrating how enterprise vendors are packaging framework flexibility within managed environments. In practice, the agentic AI frameworks market is separating into open-source tools that lead experimentation and proprietary platforms that gain ground when buyers need service levels, auditability, and centralized controls.

By Deployment Mode: Cloud Scale, Local Control

Cloud-hosted deployments held 71.32% of the agentic AI frameworks market in 2025. Cloud remains the default because managed services shorten setup time, provide fast access to frontier models, and scale with variable agent workloads. Google Cloud launched the Gemini Enterprise Agent Platform in April 2026, including Agent Studio, Agent Development Kit, Agent Runtime, Agent Identity, and Agent Gateway, demonstrating how platform vendors are packaging development and governance as a single service. Microsoft made similar moves by expanding Foundry and Microsoft 365 agent tooling, reinforcing its cloud leadership in rapid iteration and standard business workflows.

The agentic AI frameworks market size for on-premises and edge deployments is projected to expand at 36.63% CAGR through 2031. That growth reflects needs that public cloud cannot fully solve, including data sovereignty, low-latency inference, and protection of proprietary workflows. Smaller task-specific models and quantized variants are narrowing the capability gap between local and hosted deployments, reducing one of the old barriers to edge adoption. The result is an architecture split in which enterprises keep development and routine workflows in the cloud, while moving sensitive or time-critical use cases to on-premises and edge environments.

By Organization Size: Enterprise Revenue Base, SME Expansion

Large enterprises held 58.16% of the agentic AI frameworks market in 2025. Their lead reflects stronger governance programs, deeper hyperscaler relationships, and more capacity to redesign workflows around persistent agents. Large buyers also have more tolerance for hybrid acquisition models that combine embedded platform tools for standard work with custom frameworks for proprietary logic. That spending pattern supports a long tail of observability, memory, and policy tooling around the core orchestration layer in the agentic AI frameworks market.

The agentic AI frameworks market size for small and medium enterprises is projected to grow at 36.59% CAGR through 2031. Low-code products are the main enabler because they shorten the path from idea to first agent and lower the engineering threshold for adoption. Oracle said in March 2026 that AI Agent Studio for Fusion Applications introduced natural-language agent composition, workflow orchestration with human oversight, contextual memory, and an ROI dashboard across a base of more than 65,000 certified enterprise deployments. As these tools mature, smaller organizations can enter the agentic AI frameworks market earlier, but sustained value still depends on governance, data readiness, and support processes after launch.

By End-User Industry: ICT Lead, Healthcare Acceleration

ICT and software development accounted for 32.89% of the agentic AI frameworks market size in 2025. This vertical was adopted early because developers already work in API-first environments and see direct gains from autonomous coding, testing, and debugging flows. LangChain said LangGraph was in production at companies such as LinkedIn, Uber, Cisco, BlackRock, and JPMorgan, demonstrating how quickly engineering teams have moved agent orchestration into live software workflows. The sector also faces fewer data-readiness barriers than many other industries, so deployment can move faster from pilot to production in the agentic AI frameworks market.

The agentic AI frameworks market in healthcare and life sciences is projected to grow at a 37.48% CAGR through 2031. Growth is tied to administrative work such as prior authorization, denials management, and revenue cycle processes, where automation can reduce delays and lower manual burden. IBM positioned watsonx Orchestrate in 2025 around multi-agent coordination, a no-code Agent Builder, and prebuilt procurement and HR templates with SAP and Workday integrations, which support the broader move toward enterprise-ready workflow automation in regulated settings.[3]IBM, “IBM Unveils Next-Generation Agentic AI Orchestration Capabilities for watsonx Orchestrate,” IBM, newsroom.ibm.com Healthcare buyers are likely to favor platforms with audit trails, access controls, and human override mechanisms because privacy rules and interoperability requirements leave less room for ad hoc deployment in the agentic AI frameworks market.

Geography Analysis

North America held 37.51% of the global agentic AI frameworks market share in 2025. The United States remains the single largest national market because it combines the deepest enterprise AI budgets, the highest vendor concentration, and the closest links to hyperscaler ecosystems. This creates a fast feedback loop among foundation model providers, cloud platforms, and enterprise buyers, enabling the region to deploy new orchestration tools to production faster than peers. Canada adds research depth through its AI clusters, while Mexico is gaining relevance as a near-shore deployment base for bilingual operational workflows.

Europe accounted for a substantial share of the global agentic AI frameworks market in 2025. Demand in Germany, the United Kingdom, and France centers on production-grade orchestration for industrial processes, enterprise software workflows, and regulated business functions. Procurement in the region places unusual emphasis on data sovereignty, private cloud deployment, and audit-ready documentation, which pushes buyers toward more structured platform choices. The coming enforcement of high-risk AI rules is not removing demand, but it is redirecting spend toward frameworks that can document actions, controls, and human oversight with less customization.

The agentic AI frameworks market in Asia-Pacific is projected to grow at a 37.28% CAGR through 2031. China is accelerating adoption through national targets for AI agent penetration and industrial deployment, while Japan is using its May 2026 AI Promotion Act to support a risk-based, yet innovation-oriented, path to production. India benefits from deep software engineering expertise and a large services base, which supports open-source adoption in outsourcing and financial workflows. The Middle East is building momentum through national AI programs in the United Arab Emirates and Saudi Arabia, while South America remains centered on Brazil and Argentina as early entry points. Across these regions, sovereignty rules and local operating needs are not simply barriers; they are steering the agentic AI frameworks market toward more auditable and locally adaptable deployment models.

Competitive Landscape

The agentic AI frameworks market is moderately fragmented in developer tooling, but it is tightening at the enterprise platform tier, where distribution and governance matter most. Microsoft, Google, and Amazon are embedding orchestration into their cloud and productivity stacks, turning framework selection into a broader platform decision. Microsoft said in April 2026 that Foundry Agent Service supports declarative agents from LangGraph, the Claude Agent SDK, and the OpenAI Agents SDK in a single, governed runtime, a direct attempt to capture orchestration spend without forcing a single framework choice. That approach puts pressure on standalone vendors because bundled pricing, identity management, and shortcuts in security reviews are hard to match from outside the hyperscaler stack.

Open-source and independent vendors still hold significant influence in the agentic AI frameworks market because developers often choose initial tools before central procurement steps in. LangChain said in October 2025 that its LangChain and LangGraph products had reached 90 million monthly downloads and were used by 35% of Fortune 500 companies, confirming that developer adoption remains a real competitive moat. Neo4j is taking a complementary position by tying graph memory and retrieval to agent workflows, and it backed that strategy with a USD 100 million investment plan in October 2025.[4]Michael Hunger, “Neo4j Invests USD 100 Million in GenAI and Launches Key Agentic AI Innovations,” Neo4j Blog, neo4j.com This leaves room for specialists in observability, memory, and role-based orchestration even as the largest platforms expand their reach.

White space remains largest in vertical-specific orchestration and independent governance tooling, where no single platform has established category control. IBM’s 2025 watsonx Orchestrate update added multi-agent coordination, a no-code Agent Builder, and prebuilt templates with SAP and Workday integrations, which shows how incumbents are using domain workflows to defend enterprise accounts. Google Cloud launched the Gemini Enterprise Agent Platform with identity and gateway services, while Oracle expanded AI Agent Studio with workflow orchestration, contextual memory, and ROI measurement, indicating that platform vendors are racing to own both the build and control layers. MCP has become a de facto tool-integration standard,with more than 10,000 active public servers and native support across major AI applications, indicating that standards control is becoming as important as model control in the agentic AI frameworks market. The result is a competitive field where platform scale, protocol influence, and enterprise governance features matter more each quarter, even though niche vendors still win in specialized deployment pockets.

Agentic AI Frameworks Industry Leaders

OpenAI LLC

Microsoft Corporation

Google LLC

Anthropic PBC

Meta Platforms Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Microsoft made Agent 365 generally available on May 1 at USD 15 per user per month, providing a centralized control plane for observing, securing, and governing AI agents across enterprise deployments. The company simultaneously launched Microsoft 365 E7 and The Frontier Suite at USD 99 per user per month, bundling Copilot, Agent 365, and Microsoft Entra security capabilities into a unified governance layer for multi-agent environments.

- April 2026: Google Cloud launched the Gemini Enterprise Agent Platform on April 22, comprising Agent Studio, Agent Development Kit, Agent Runtime with persistent memory via Memory Bank, and governance services including Agent Identity and Agent Gateway. Launch enterprise customers included PayPal, Comcast, L'Oréal, and Color Health.

- April 2026: Microsoft announced the general availability of OpenAI’s GPT-5.5 on Microsoft Foundry on April 23, specifically engineered for improved agentic execution, long-context reasoning, and a USD 5.0-per-million input tokens pricing tier. The release confirmed native runtime support for LangGraph, Claude Agent SDK, and OpenAI Agents SDK within the Foundry Agent Service.

- March 2026: Oracle expanded AI Agent Studio for Oracle Fusion Applications on March 24, introducing an Agentic Applications Builder for natural-language agent composition, workflow orchestration with built-in human oversight, contextual memory, and an Agent ROI Dashboard measuring time saved and cost per agent. The studio serves more than 65,000 certified enterprise deployments.

Global Agentic AI Frameworks Market Report Scope

The Agentic AI Frameworks Market refers to the global industry focused on developing, adopting, and commercializing software frameworks and infrastructure tools that enable the creation, orchestration, deployment, and management of autonomous artificial intelligence agents. These frameworks provide the foundational architecture, development environments, APIs, workflow orchestration tools, memory management systems, and integration capabilities required for building AI agents capable of reasoning, planning, decision-making, task execution, and autonomous interaction across digital environments.

The Agentic AI Frameworks Market Report is Segmented by Framework Type (Open-Source Frameworks, and Proprietary Frameworks), Deployment Mode (Cloud-Hosted, and On-Premises and Edge), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (ICT and Software Development, Financial Services, Healthcare and Life Sciences, Manufacturing and Industrial, Retail and E-Commerce, and Media and Entertainment), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Open-Source Frameworks |

| Proprietary Frameworks |

| Cloud-Hosted |

| On-Premises and Edge |

| Large Enterprises |

| Small and Medium Enterprises |

| ICT and Software Development |

| Financial Services |

| Healthcare and Life Sciences |

| Manufacturing and Industrial |

| Retail and E-Commerce |

| Media and Entertainment |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Framework Type | Open-Source Frameworks | ||

| Proprietary Frameworks | |||

| By Deployment Mode | Cloud-Hosted | ||

| On-Premises and Edge | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-User Industry | ICT and Software Development | ||

| Financial Services | |||

| Healthcare and Life Sciences | |||

| Manufacturing and Industrial | |||

| Retail and E-Commerce | |||

| Media and Entertainment | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the agentic AI frameworks market?

The agentic AI frameworks market was valued at USD 2.99 billion in 2025, stands at USD 4.11 billion in 2026, and is forecast to reach USD 19.32 billion by 2031.

How fast is demand expected to grow through 2031?

The market is projected to grow at a 36.28% CAGR from 2026 to 2031, supported by broader use of autonomous agents in enterprise workflows.

Which framework type leads adoption today?

Open-source frameworks led with 63.81% share in 2025 because developers favored composability, auditability, and broad integration support.

Why do cloud-hosted deployments remain dominant?

Cloud-hosted models held 71.32% share in 2025 because they shorten deployment time, simplify scaling, and provide direct access to managed model and governance services.

Which end-user group is growing the fastest?

Healthcare and life sciences is the fastest-growing end-user segment, with a projected 37.48% CAGR through 2031, driven by administrative automation and revenue cycle use cases.

What is shaping vendor competition right now?

Competition is being shaped by hyperscaler bundling, open protocol adoption such as MCP, and demand for governance, identity, and workflow control features in enterprise deployments.

Page last updated on: