Agentic AI Governance And Policy Management Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

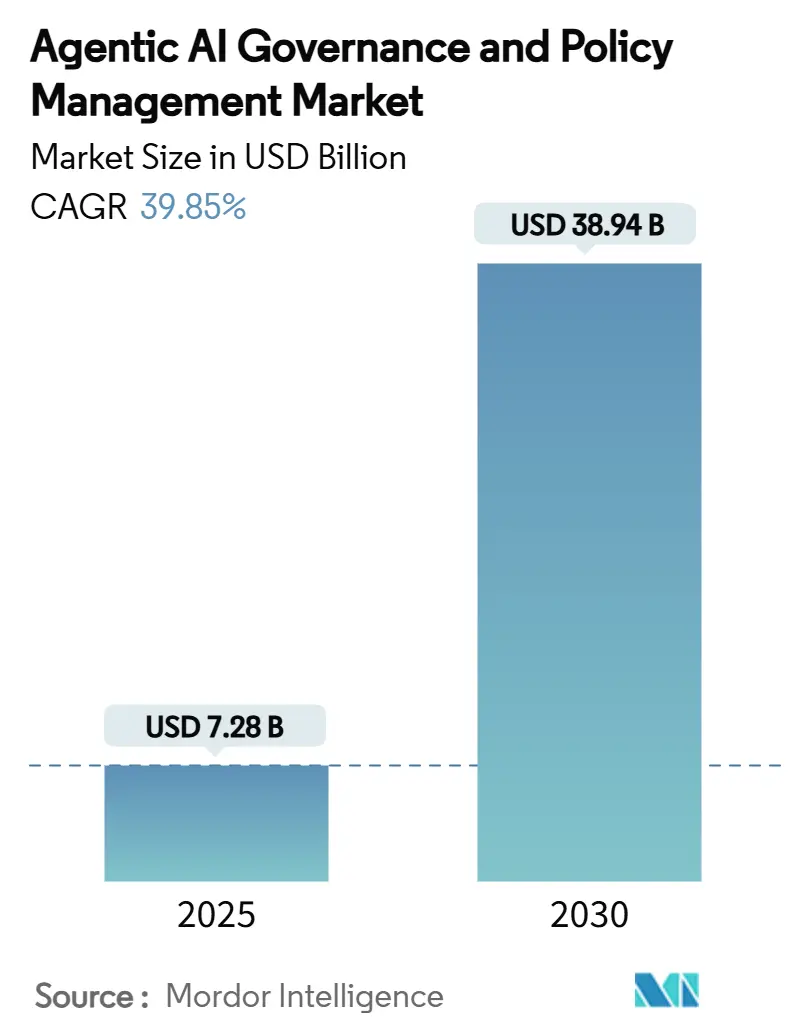

| Market Size (2025) | USD 7.28 Billion |

| Market Size (2030) | USD 38.94 Billion |

| Growth Rate (2025 - 2030) | 39.85% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agentic AI Governance And Policy Management Market Analysis by Mordor Intelligence

The Agentic AI Governance and Policy Management market size reached USD 7.28 billion in 2025 and is forecast to reach USD 38.94 billion by 2030 at a 39.85% CAGR. Surging demand for frameworks that can supervise autonomous agents, coupled with tightening worldwide regulation, is driving this rapid expansion. Enterprises are shifting from ad-hoc guardrails to full-lifecycle oversight platforms that embed policy logic directly into development pipelines. Vendors that can deliver integrated monitoring, explainability, and compliance tooling in a single stack are gaining a clear competitive edge. At the same time, mid-market adoption is accelerating as cloud-based offerings lower both cost and complexity barriers.

Key Report Takeaways

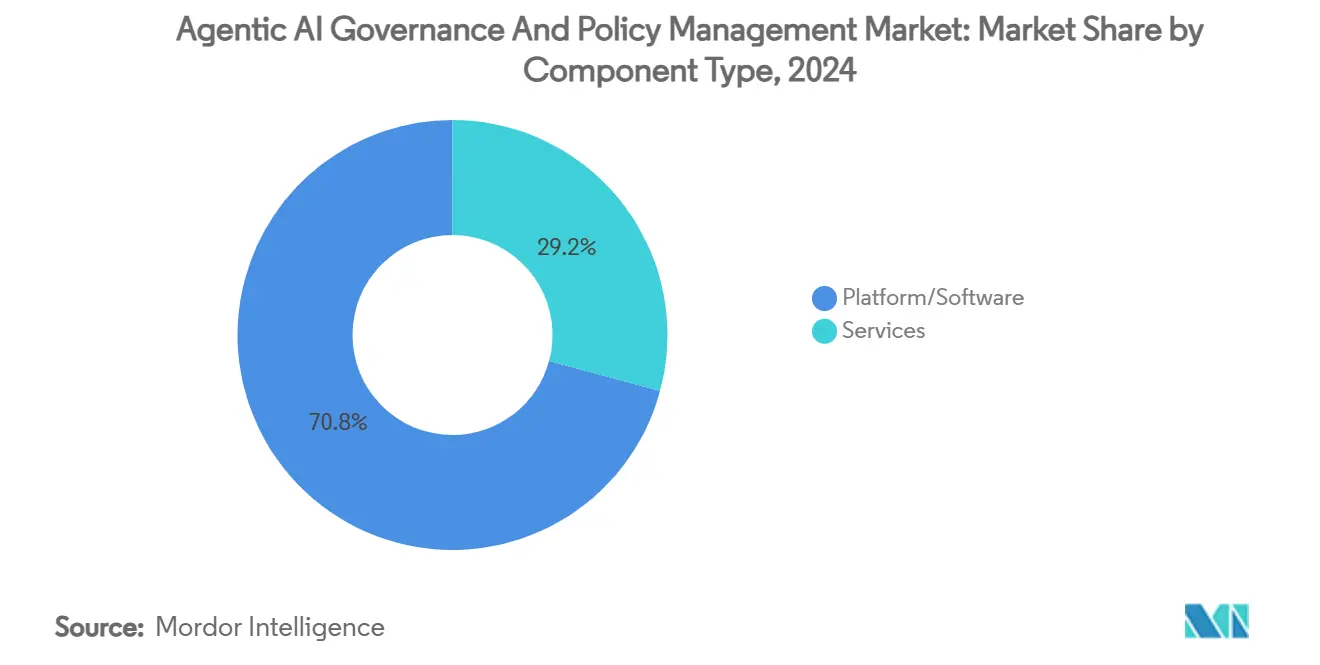

- By component, Platform/Software led with 70.80% revenue share in 2024; Services is projected to expand to a 42.20% CAGR through 2030.

- By governance function, Policy Management and Compliance accounted for 27.50% share of the Agentic AI Governance and Policy Management market size in 2024; Bias and Fairness Monitoring is advancing at a 41.71% CAGR through 2030.

- By deployment mode, Cloud deployment captured 65.20% share in 2024; Hybrid deployment is forecast to grow at a 42.50% CAGR to 2030.

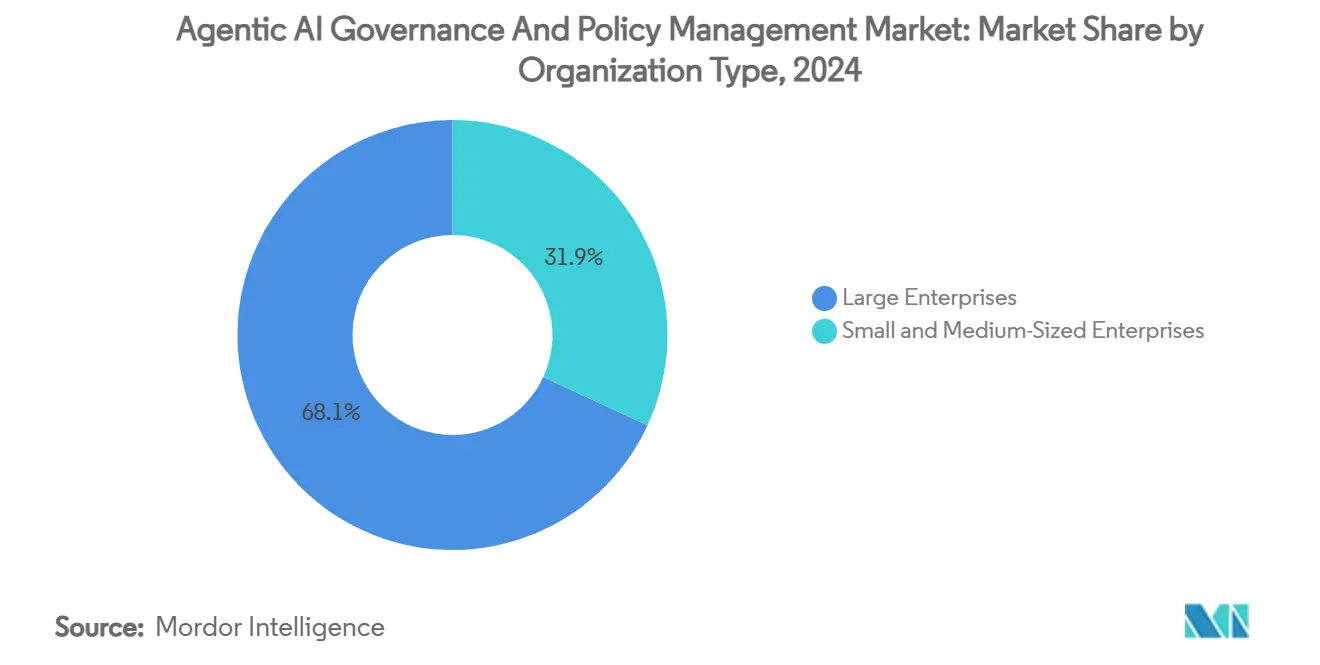

- By organisation size, Large Enterprises held 68.10% of 2024 revenue; Small and Medium-sized Enterprises are poised to grow at a 41.83% CAGR over the outlook period.

- By end-use industry, Banking, Financial Services and Insurance accounted for 25.40% share in 2024; Healthcare and Life Sciences exhibits the highest 43.20% CAGR to 2030.

- By geography, North America dominated with 38.10% market share in 2024; Asia-Pacific is set to register a 41.55% CAGR through 2030.

Global Agentic AI Governance And Policy Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying global AI-risk regulations | 12.5% | Global, with early enforcement in EU and North America | Short term (≤ 2 years) |

| Sharply rising compliance penalties for opaque AI | 8.2% | EU, North America, expanding to Asia Pacific | Medium term (2-4 years) |

| Integration of governance inside MLOps toolchains | 7.8% | Global, led by North America and EU | Medium term (2-4 years) |

| Vendor race to embed policy engines in foundation models | 6.1% | Global, concentrated in major AI development hubs | Short term (≤ 2 years) |

| Under-served demand from mid-market firms | 4.3% | Global, particularly pronounced in Asia Pacific and emerging markets | Long term (≥ 4 years) |

| Cross-border algorithmic import clauses | 3.1% | Global, with focus on trade-intensive regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Global AI-Risk Regulations

Mandatory rules now govern high-risk AI. The EU AI Act became enforceable in 2025 and introduced a tiered compliance model with fines up to 7% of global turnover . China’s AI Safety Governance Framework requires continuous system monitoring, prompting multinationals to seek multi-jurisdictional platforms. Japan is following a lighter, sector-specific path that still demands verifiable governance artefacts. Collectively, these measures force enterprises to harmonise policies across borders rather than manage isolated rule sets. Providers offering pre-configured control libraries and automatic regulatory-change alerts are winning early contracts.

Sharply Rising Compliance Penalties for Opaque AI

Financial risk has become tangible. The EU regime’s 7% ceiling dwarfs the 4% cap under GDPR, altering board-level risk calculus. US healthcare providers face certification loss if algorithms fail the ONC HTI-1 transparency rule. UK auditors gained new authority in 2025 to scrutinise AI controls across finance, energy, and telecom sectors. Penalty escalation is converting governance spending from “nice-to-have” into mandatory insurance, accelerating platform uptake among budget-sensitive industries such as retail and manufacturing.

Integration of Governance Inside MLOps Toolchains

Platforms now weave policy logic into the same pipelines that train and deploy models. IBM’s watsonx.governance combines bias checks, drift alerts, and regulatory mappings inside its hybrid cloud stack.[1]IBM, “IBM watsonx.governance,” ibm.com Open Policy Agent lets developers codify rules that travel with software artefacts across environments. [2]Open Policy Agent, “Open Policy Agent,” openpolicyagent.orgGoogle Cloud advises executives to embed controls early, so violations are blocked before release.[3]Google Cloud, “Five questions every executive should ask about gen AI,” cloud.google.com As a result, compliance overhead falls and release cycles shorten. Vendors lacking native MLOps hooks risk marginalisation as clients favour “governance-by-design” architectures.

Vendor Race to Embed Policy Engines in Foundation Models

Model creators are shipping governance as an intrinsic feature. The Unified Control Framework sets up 42 machine-readable safeguards that can be hard-wired into model weights. ShieldAgent demonstrates verifiable safety reasoning directly inside autonomous agents, removing dependence on external monitors. FAIRTOPIA adds multi-agent guardianship that continuously patches fairness gaps across pipelines. These advances blur the line between model and policy layer, enabling lower-latency enforcement and strengthening vendor lock-in.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Poor ROI visibility for stand-alone governance software | -6.8% | Global, particularly acute in cost-sensitive SME segments | Medium term (2-4 years) |

| Skill-set scarcity in Responsible-AI engineering | -5.2% | Global, most pronounced in emerging markets and SME segments | Long term (≥ 4 years) |

| Fragmented jurisdictional standards | -4.1% | Global, with highest impact on multinational enterprises | Long term (≥ 4 years) |

| Latency overhead on real-time agentic systems | -3.3% | Global, critical for high-frequency applications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Poor ROI Visibility for Stand-Alone Governance Software

Many firms still struggle to link governance to revenue gains. A CSO Online study found only 24% of organisations have fully enforced AI policies, largely due to unclear value metrics.[4]CSO Online Staff, “How AI is changing the GRC strategy,” csoonline.com Board members often regard tools as insurance rather than growth drivers, leading to protracted purchasing cycles. Providers are responding with dashboards that quantify avoided fines, reduced model-retraining costs, and shortened audit times. Until these value narratives mature, the uptake among cost-sensitive sectors will lag.

Skill-Set Scarcity in Responsible-AI Engineering

Demand for interdisciplinary talent—part data scientist, part ethicist, part compliance officer—continues to outstrip supply. European SMEs report that only 5% have the internal expertise to operationalize new EU obligations, pushing them toward managed-service models.[5]Nikkei Asia Staff, “Asia’s AI policy gaps pose headaches for business,” nikkei.com Rising salary premiums widen the gap between global majors and regional challengers. University courses are catching up but will not deliver volume until the latter half of the decade. Managed-service providers therefore play a pivotal role in the Agentic AI Governance and Policy Management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platform Dominance Drives Integration

Platform/Software offerings captured 70.80% of the Agentic AI Governance and Policy Management market share in 2024, underpinned by enterprise demand for single-pane visibility across multiple AI applications. Integrated suites that bundle policy definition, monitoring, and audit logging minimise siloed tooling and simplify regulator interactions. Services, while smaller, is the fastest-expanding component at a 42.20% CAGR as firms outsource complex configuration tasks they cannot staff internally.

Service vendors provide readiness assessments, policy codification, and ongoing drift analytics, often under managed-service contracts that scale with usage. This recurring engagement model converts one-time consulting into predictable revenue, reinforcing the Agentic AI Governance and Policy Management market’s pivot toward continuous compliance. As regulatory scope widens, demand for hands-on expertise will keep service growth above the platform baseline.

By Governance Function: Policy Management Leads Compliance Focus

Policy Management and Compliance commanded 27.50% share of the Agentic AI Governance and Policy Management market size in 2024. Boards prioritise audit-ready artefacts that demonstrate rule adherence, making policy repositories the anchor layer for any deployment. Bias and Fairness Monitoring, though smaller, is set to advance 41.71% annually, fueled by landmark retail, lending, and healthcare cases that exposed discriminatory outcomes.

Explainability tools convert opaque model decisions into human-readable narratives, while Security and Privacy modules protect training data from leakage or poisoning. Risk and Incident Management adds workflows for rapid rollback and remediation. Together, these functions build a staged maturity curve that guides buyers from baseline policy capture to full, end-to-end oversight.

By Deployment Mode: Cloud Flexibility Drives Adoption

Cloud delivery captured 65.20% revenue in 2024 as governance workloads—telemetry ingestion, bias scans, rules-engine processing—fit naturally in elastic environments. Subscription pricing also reduces up-front capital expenditure, widening access for mid-cap firms. Hybrid deployments, forecast to grow 42.50% annually, satisfy sectors with low-latency or data-sovereignty constraints by locating policy engines near on-premises data while reserving burst capacity in public clouds.

On-premises installations persist in defence, critical infrastructure, and regulated public services where external connections remain restricted. Yet even here, containerised components and zero-trust gateways are easing the path toward hybrid governance topologies that share a unified policy backbone across environments.

By Organization Size: Enterprise Leadership With SME Acceleration

Large Enterprises contributed 68.10% of spending in 2024, reflecting both higher regulatory exposure and greater budget. They integrate governance across global business units, often layering custom rules atop vendor templates. Small and Medium-sized Enterprises, while today a minority, will compound at 41.83% through 2030 as user-friendly SaaS products lower adoption hurdles and regulators apply equal obligations regardless of firm size.

SMEs typically start with policy templates for hiring or credit scoring use-cases and then scale outward. Low-code interfaces reduce specialist head-count needs, narrowing the talent gap that otherwise restricts SME compliance efforts. This democratisation broadens the Agentic AI Governance and Policy Management market addressable pool beyond Fortune 1000 accounts.

By End-Use Industry: Financial Services Lead Regulatory Compliance

Banking, Financial Services and Insurance retained 25.40% share in 2024. Algorithmic trading, credit modelling, and fraud detection all fall under stringent disclosure rules, making governance a non-negotiable operational cost. Healthcare and Life Sciences will post the highest 43.20% CAGR to 2030 as electronic health-record vendors and hospital networks comply with transparency provisions under the US HTI-1 final rule.

Government adoption is also rising, driven by fairness mandates in benefits allocation and judicial decision-support systems. Manufacturing and Retail focus on supply-chain optimisation and personalised marketing, requiring bias monitoring to guard against demographic exclusion. Each vertical thus pilots a distinct governance maturation path yet converges on unified tooling that supports cross-sector best practice exchange.

Geography Analysis

North America is the most mature buyer community for Agentic AI Governance and Policy Management market solutions. Large federal programmes and sector-specific edicts translate into predictable multi-year contracts, while extensive venture funding stimulates innovation clusters across the United States and Canada. Academic–industry partnerships funnel research on verifiable safety into commercial products, reinforcing first-mover advantage.

Asia-Pacific represents the fastest-expanding theatre. China’s compulsory risk assessments and Japan’s pragmatic compliance playbook encourage multinational enterprises to roll out multi-lingual policy engines that support both prescriptive and principles-based regimes. Southeast Asian economies, led by Singapore, adopt reference frameworks that can be localised quickly, further enlarging addressable demand.

Europe’s uniform but stringent stance under the EU AI Act creates a sizeable replacement cycle. Firms are retiring home-grown checklists in favour of off-the-shelf suites capable of automatic severity classification and notification. Cross-border data transfer clauses in Germany and France create additional complexity, favouring platforms with granular policy-scoping and encryption controls.

Competitive Landscape

Competition is moderate. Global technology leaders such as IBM, Microsoft, and Google leverage existing cloud stacks to bundle governance as an add-on module, offering single invoices and unified SLAs. Their advantage lies in scale and embedded channel networks. Mid-sized specialists including Credo AI, Fiddler, and Arthur differentiate through domain-specific bias metrics and configurable explainability widgets.

Strategic moves are accelerating. IBM fused Guardium data-security capabilities into watsonx.governance in March 2025, aligning model oversight with data-protection mandates. Microsoft previewed a policy-as-code kit that allows Azure customers to push rules into GitHub workflows, merging developer experience with compliance controls. Credo AI secured USD 21 million to extend fairness modules to non-English datasets, signalling global expansion intent.

Partnership ecosystems matter. Consultancy majors—Accenture, Deloitte, PwC—package governance advisory with system integration, pitching “rapid compliance readiness” to firms under enforcement deadlines. Open-source orchestration remains pivotal, as shown by vendor alignment around Open Policy Agent to avoid proprietary lock-in. Market prises will increasingly hinge on seamless plug-ins for MLOps, incident-response, and security information event-management suites.

Agentic AI Governance And Policy Management Industry Leaders

International Business Machines Corporation

Microsoft Corporation

Alphabet Inc. (Google LLC)

Amazon.com Inc. (Amazon Web Services)

SAS Institute Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Transcend introduced Pathfinder, a mid-market governance suite offering real-time deployment mapping.

- March 2025: IBM launched an enhanced watsonx.governance release that merges data-security controls with model oversight, delivering real-time enforcement across hybrid environments.

- September 2024: China’s National Technical Committee published its comprehensive AI Safety Governance Framework, mandating lifecycle monitoring.

- July 2024: Credo AI closed a USD 21 million Series A round to scale bias detection tooling.

Global Agentic AI Governance And Policy Management Market Report Scope

| Platform / Software |

| Services |

| Policy Management and Compliance |

| Biasand Fairness Monitoring |

| Explainability and Transparency |

| Security and Privacy |

| Risk and Incident Management |

| Performance and Drift Monitoring |

| Other functions |

| On-Premises |

| Cloud |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Government and Public Sector |

| Manufacturing |

| Retail and E-commerce |

| Other End-user Industries |

| North America |

| South America |

| Europe |

| Asia-Pacific |

| Middle East and Africa |

| By Component | Platform / Software |

| Services | |

| By Governance Function | Policy Management and Compliance |

| Biasand Fairness Monitoring | |

| Explainability and Transparency | |

| Security and Privacy | |

| Risk and Incident Management | |

| Performance and Drift Monitoring | |

| Other functions | |

| By Deployment Mode | On-Premises |

| Cloud | |

| Hybrid | |

| By Organisation Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By End-Use Industry | Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences | |

| Government and Public Sector | |

| Manufacturing | |

| Retail and E-commerce | |

| Other End-user Industries | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia-Pacific | |

| Middle East and Africa |

Key Questions Answered in the Report

What is the current value of the Agentic AI Governance and Policy Management market?

The market generated USD 7.28 billion in 2025 and is forecast to reach USD 38.94 billion by 2030 at a 39.85% CAGR.

Which component segment leads revenue?

Platform/Software solutions deliver 70.80% of 2024 revenue because firms prefer integrated suites over isolated tools.

Why is Bias and Fairness Monitoring growing so rapidly?

Regulators now require evidence of non-discriminatory outcomes, propelling Bias and Fairness Monitoring functions at a 41.71% CAGR.

Which region will grow the fastest?

Asia-Pacific is projected to post a 41.55% CAGR through 2030, supported by new mandates in China, Japan, and Southeast Asia.

How are vendors embedding governance into AI workflows?

Market leaders integrate policy engines directly into MLOps pipelines and foundation models, enabling real-time rule enforcement and reducing compliance overhead.

What industries are adopting governance platforms most aggressively?

Financial Services lead to spending due to stringent disclosure rules, while Healthcare shows the fastest growth as clinical AI faces new transparency obligations.

Page last updated on: