Agentic AI in Retail and E-commerce Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Market Size (2026) | USD 60.43 Billion |

| Market Size (2031) | USD 218.37 Billion |

| Growth Rate (2026 - 2031) | 29.29% CAGR |

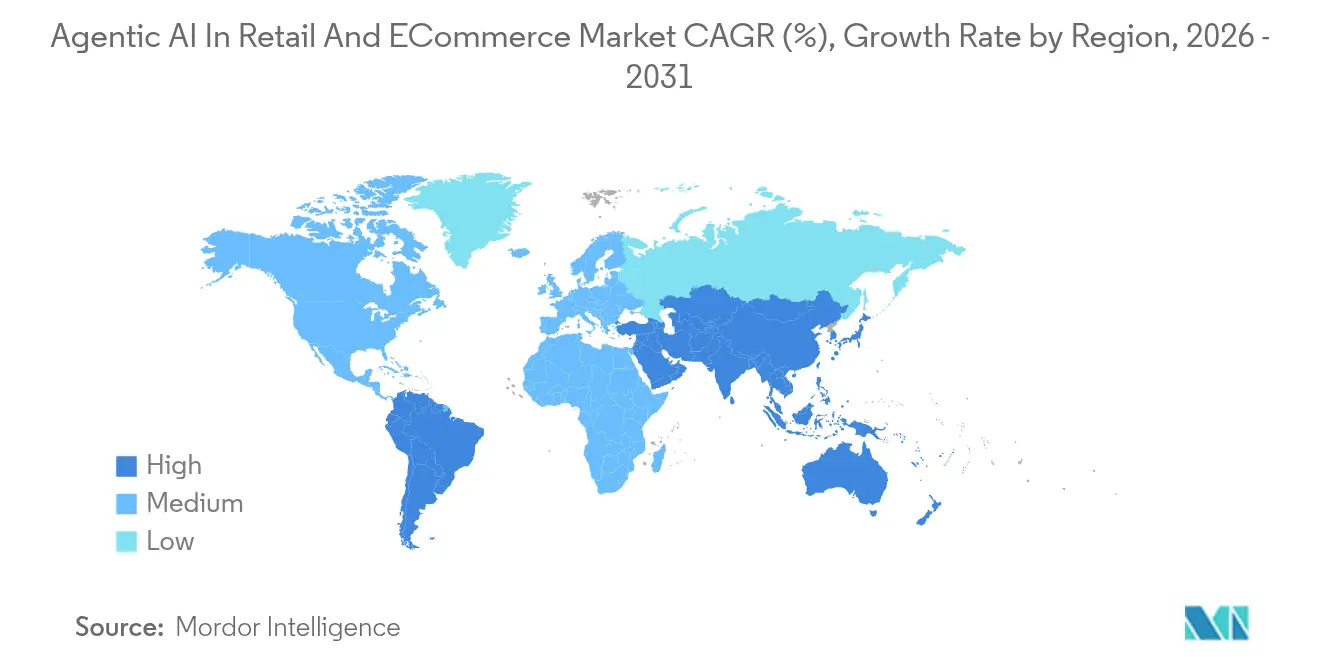

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

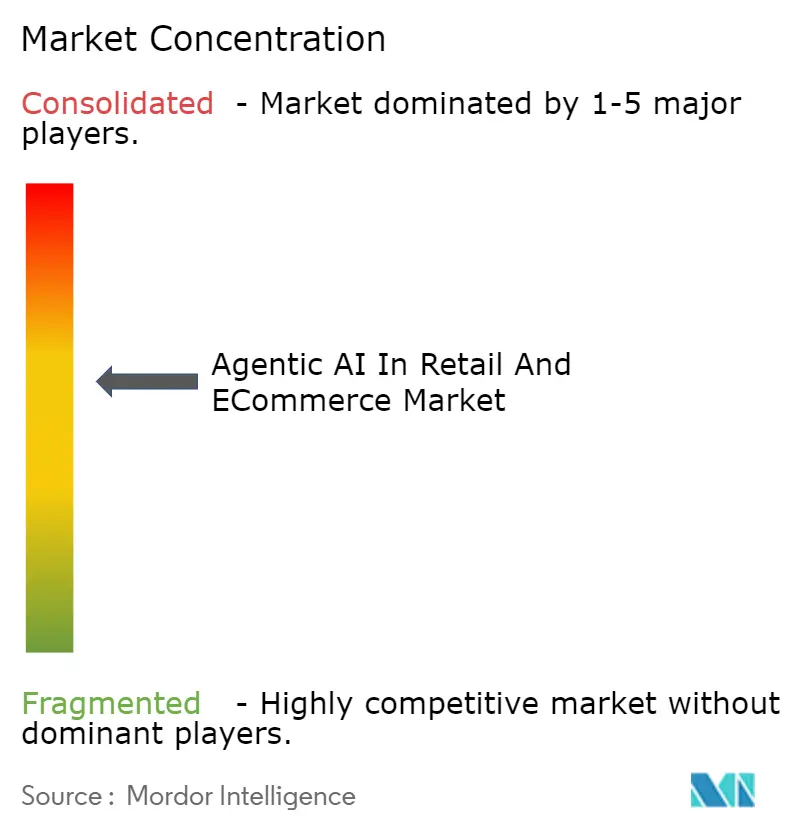

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agentic AI in Retail and E-commerce Market Analysis by Mordor Intelligence

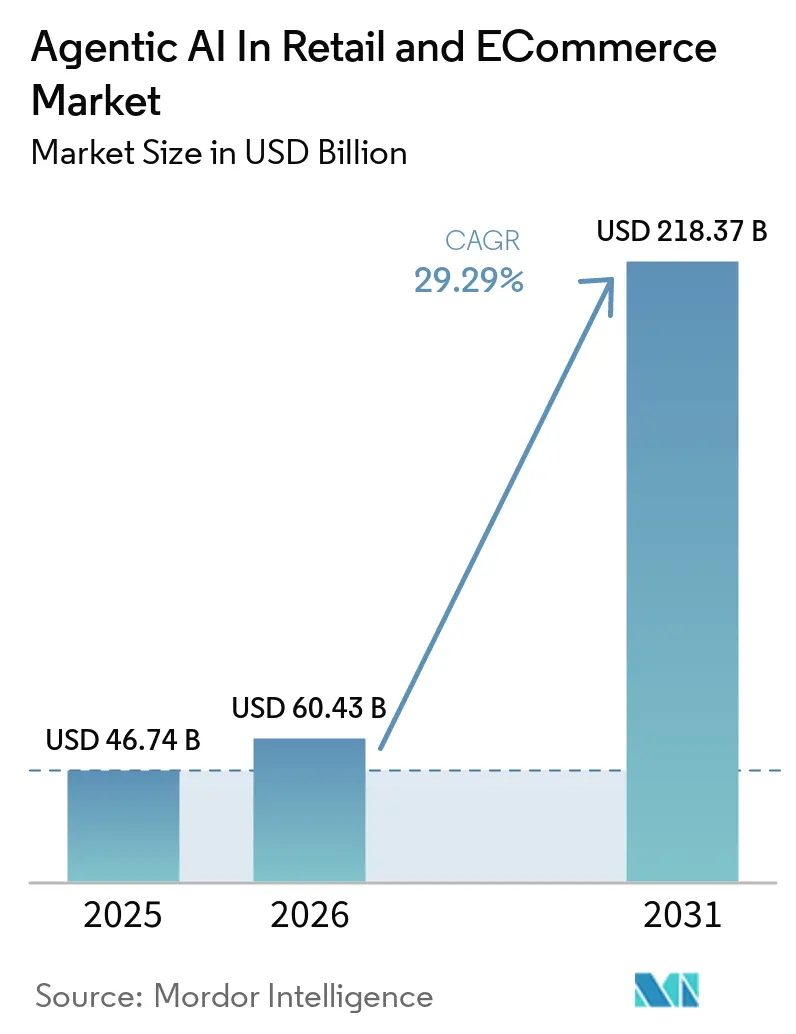

The Agentic AI in Retail and E-commerce Market size in 2026 is estimated at USD 60.43 billion, growing from 2025 value of USD 46.74 billion with 2031 projections showing USD 218.37 billion, growing at 29.29% CAGR over 2026-2031. The rapid ascent springs from retailers shifting away from static, rules-based software toward autonomous agents that handle complex tasks such as dynamic pricing, supply-chain orchestration, and hyper-personalized engagement without human supervision. Cost-to-serve pressures, rising labour costs, and GPU-powered model advances underpin adoption, while cloud hyperscale’s’ investment cycles—Microsoft Azure’s AI revenue already tops USD 13 billion annually—signal sustained capital support for large-scale deployments. Early pilots show clear bottom-line gains: Walmart’s autonomous waste-reduction engine cuts spoilage before it occurs and Target’s Store Companion chatbot slashes new-hire ramp-up time, illustrating how autonomous reasoning directly improves store economics. GPU shortages and governance concerns temper rollouts, yet the strategic imperative to personalize at scale keeps investment momentum intact.

Key Report Takeaways

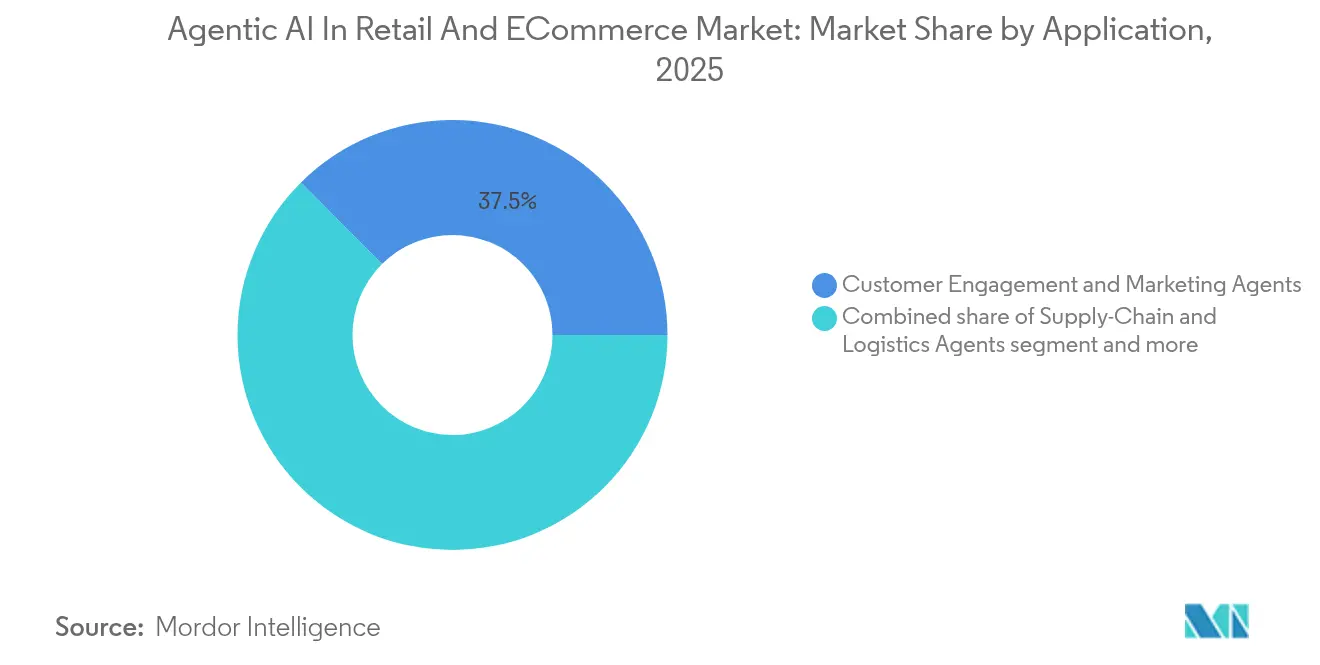

- By application, Customer Engagement and Marketing Agents led with 37.45% of the Agentic AI in Retail and E-commerce Market share in 2025.

- By retail format, Omnichannel Retailers held 41.02% revenue share in 2025, while Grocery and Convenience is poised for a 32.86% CAGR to 2031.

- By technology approach, Generative Dialogue Agents captured 45.80% share of the Agentic AI in Retail and E-commerce Market size in 2025; Voice-Commerce Agents register the strongest 36.25% CAGR outlook through 2031.

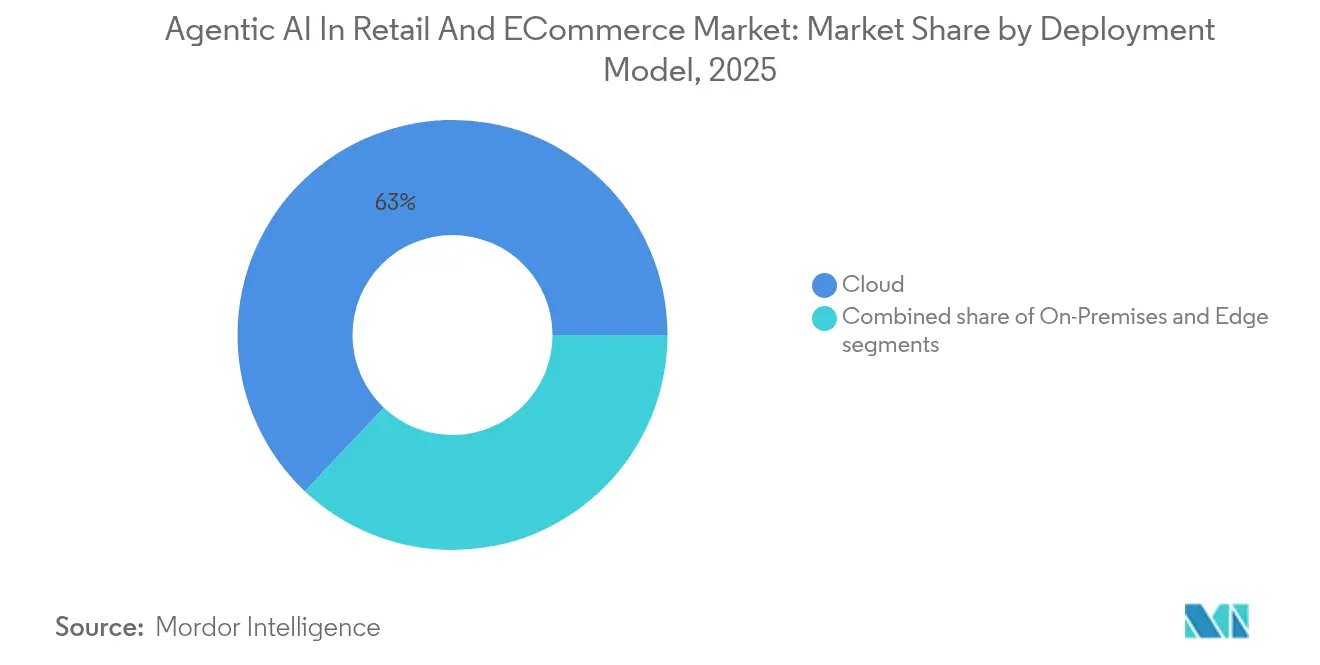

- By deployment model, Cloud accounted for 62.95% share, yet Edge computing is forecast to advance at a 35.95% CAGR during the same horizon.

- By geography North America dominated with 37.35% share in 2025, whereas Asia-Pacific will grow fastest at a 34.88% CAGR owing to unmanned-store proliferation.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Agentic AI in Retail and E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generative-AI cost-to-serve reduction imperatives | 8.20% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Hyper-personalised CX race among Tier-1 retailers | 7.50% | North America and APAC core, spill-over to EU | Short term (≤ 2 years) |

| Autonomous supply-chain control-towers | 6.80% | Global, concentrated in large retail networks | Medium term (2-4 years) |

| AI-talent retention/attrition arms-race | 4.10% | North America and EU primarily | Long term (≥ 4 years) |

| ESG-linked shrinkage and waste mandates | 2.90% | EU leading, expanding to North America and APAC | Long term (≥ 4 years) |

| Synthetic data for low-margin SKU expansion | 1.50% | Global, with focus on emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Generative-AI Cost-to-Serve Reduction Imperatives

Retailers face unrelenting cost pressure and thin margins, prompting swift adoption of autonomous agents that trim labour hours while preserving service quality. Walmart’s AI-driven waste dashboards forecast spoilage and guide associates to pre-empt losses, whereas Target’s 2,000-store rollout of Store Companion chatbots accelerates onboarding by giving employees instant procedural answers. The shift from scripted bots to reasoning agents eliminates tier-1 support queues and reduces average handling time, improving satisfaction scores. Analysts at EY India project a 35–37% productivity lift for the country’s retail sector within five years from generative AI alone[2]EY India, “GenAI to boost productivity in India by 35–37%,” ey.com. Early adopters spread fixed GPU costs across millions of interactions, reinforcing economies of scale not available to late entrants.

Hyper-Personalized CX Race Among Tier-1 Retailers

Retail leaders weaponize agentic AI to tailor every interaction. Victoria’s Secret relies on Google Cloud large-language agents for real-time product suggestions, integrating sentiment analytics with inventory data to surface relevant SKUs instantly. Amazon’s internal count of 1,000 generative AI shopping applications shows the magnitude of personalization bets, all accelerated by custom Trainium 2 silicon that lowers inference cost. Google Cloud cites a home-improvement chain adding USD 16 million of incremental revenue from visual-search agents alone. As recommendations grow context-aware, consumers develop loyalty to platforms that “know” them, raising competitive barriers.

Autonomous Supply-Chain Control-Towers

Supply-chain agents now orchestrate replenishment, routing, and pallet building with marginal human touch. Walmart’s Symbotic-powered distribution centers deploy fleets of mobile robots that stack store-ready pallets at high speed, trimming warehouse dwell time and store back-room congestion. Sam’s Club’s seamless-exit edge-AI gates clear baskets in milliseconds and relay accurate inventory decrements, illustrating how local compute eliminates network latency. Studies show AI-driven supply optimization can cut waste by 30% and enhance forecast accuracy, reinforcing working-capital gains.

AI-Talent Retention/Attrition Arms-Race

Scarce AI engineering talent shapes competitive tempo. Yahoo Japan mandates generative-AI use for all 11,000 staff, aiming to double productivity by 2028. Colgate-Palmolive’s internal AI Hub yielded 3,000 custom assistants, illustrating how democratized tooling can offset hiring gaps. Yet 79% of strategists call AI critical while only 20% use it daily, highlighting execution risk. Organizations that nurture in-house communities of practice retain know-how and accelerate iteration cycles, widening the adoption gap.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Governance debt and hallucination risk | -4.80% | Global, with stricter EU regulations | Short term (≤ 2 years) |

| GPU-cluster power-supply bottlenecks | -3.20% | Global, acute in North America and EU | Medium term (2-4 years) |

| Workforce resistance to agentic co-workers | -2.10% | North America and EU primarily, emerging in APAC | Short term (≤ 2 years) |

| Rising synthetic-content fraud | -1.40% | Global, concentrated in e-commerce platforms | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Governance Debt and Hallucination Risk

Retailers push AI faster than governance frameworks mature. IKEA’s early EU AI Act alignment demonstrates best practice, yet many peers lack similar rigor. Harvard Business School found 84% of AI-generated shift rosters required manual overrides due to bad inputs, eroding trust. Customer-facing hallucinations risk defamation or regulatory fines; Deloitte stresses multi-disciplinary centers of excellence, but many retailers still lack system-level validation.[3]Aparupa Bhattacharya et al., “Generative AI Governance Considerations,” Deloitte, deloitte.com

GPU-Cluster Power-Supply Bottlenecks

AI workloads require dense compute and power. Goldman Sachs models a 50-fold power-density jump by 2027, straining datacentre cooling budgets. NVIDIA H100 scarcity, tied to substrate chokepoints in Japan and Taiwan, turns GPU procurement into a competitive weapon. Edge AI mitigates cloud overload—Sam’s Club shows latency gains—but smaller retailers face high upfront costs and limited talent to manage on-prem clusters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Customer Engagement Dominates, Fraud Prevention Accelerates

Customer Engagement and Marketing Agents held 37.45% of the Agentic AI in Retail and E-commerce Market share in 2025, reflecting retailers’ focus on revenue-generating touchpoints. Demand for conversational agents that handle product discovery, upsell, and service resolutions keeps overall application spend elevated. The Agentic AI in Retail and E-commerce Market size tied to Customer Engagement is forecast to rise in tandem with loyalty-program overhauls, embedding real-time offer engines that refine decisions every interaction.

Fraud and Risk Management, though smaller today, posts a 34.12% CAGR to 2031, underscoring loss-prevention urgency. Veesion’s gesture-recognition algorithm, live in 5,000 stores, alerts security within seconds and shows 85% relevance, proving ROI. Retailers integrate CCTV-native models such as Mazaal’s Retail Guardian to curb self-checkout shrink. As regulations mandate stricter fraud reporting, adoption spreads to mid-tier chains.

By Retail Format: Omnichannel Leadership Meets Grocery Momentum

Omnichannel Retailers captured 41.02% share of the Agentic AI in Retail and E-commerce Market in 2025, leveraging unified data lakes that span web, app, and store. Agents synchronize inventory views, price parity, and fulfilment promises, sustaining competitive parity with pure-play e-commerce rivals.

Grocery and Convenience accelerates at a 32.86% CAGR, making it the fastest-growing format. High-velocity SKU turns, perishability, and labour intensity create fertile ground for autonomous agents. Lawson’s Real x Tech lab in Tokyo combines AI cameras and virtual cashiers for touchless journeys, while 7-Eleven’s AI-Clerk unmanned stores in Seoul demonstrate feasibility in high-footfall environments. Dynamic pricing engines such as Puzl AI let grocers balance margin and waste, nudging market-wide adoption.

By Technology Approach: Generative Dialogue Leads Voice-Commerce Surge

Generative Dialogue Agents accounted for 45.80% share in 2025 as retailers embrace natural-language experiences that cut menu fatigue. Amazon’s new Alexa+ framework embodies this, letting shoppers re-order or book services via unstructured prompts. The Agentic AI in Retail and E-commerce Market size attached to dialogue agents grows with each new language and domain they master.

Voice-Commerce Agents rise at a 36.25% CAGR, pushed by smart-speaker penetration. Panera Bread’s adoption of Amazon Food Skills API confirms that even quick-service operators value hands-free ordering. Convergence with computer-vision modules will generate multimodal agents that comprehend speech, images, and context simultaneously, deepening behavioural data pools.

By Deployment Model: Cloud Dominance Faces Edge Upswing

Cloud retained 62.95% share of the Agentic AI in Retail and E-commerce Market in 2025 as hyperscalers bundle model libraries, data governance, and DevOps in one invoice. Microsoft and Google each posted 30%+ cloud revenue growth, underscoring demand for elastic AI capacity.

Edge computing, however, gains momentum with a 35.95% CAGR. Retailers place inference engines in-store to meet sub-100-millisecond latency targets and to keep personally identifiable data local. Dell’s NativeEdge platform highlights a turnkey path, adding theft-detection and drive-through voice ordering on the same box. Hybrid orchestration will likely dominate as chains split training workloads to the cloud and inference to the edge.

By Organization Size: Enterprise Leadership Spurs SME Democratization

Enterprises enjoy first-mover scale advantages, yet small-and-mid-sized businesses (SMBs) now join the Agentic AI in Retail and E-commerce Market thanks to low-code tools. Salesforce finds 75% of SMBs experimenting with AI as data stewardship and security templates mature. The agentic AI in retail and eCommerce industry thus broadens its user base beyond big-box incumbents.

Indian apparel chain Raymond shows how in-store agent JARVIS guides shoppers and associates without heavy infrastructure, while Kochi’s unmanned neighbourhood marts use sensors and AI for 24/7 service. As subscription-priced agents emerge, SMB adoption will compound, reshaping local retail competitiveness.

Geography Analysis

North America accounted for 37.35% of the Agentic AI in Retail and E-commerce Market in 2025, supported by dense cloud regions, venture capital access, and leading retailers that operate as living labs for autonomous systems. Amazon’s 1,000-application generative AI roadmap and custom silicon demonstrate entrenched commitment. Walmart and Target validate use cases at multi-billion-dollar scale, attracting vendor ecosystems that cluster around Bentonville and Seattle. Regulation remains favourable, but GPU and datacentre-power shortages lengthen project queues.

Asia-Pacific posts the fastest 34.88% CAGR to 2031. SoftBank aims for 1 billion AI agents by 2026, signalling bold investment attitudes and reinforcing growth across the Japan eCommerce market. China’s AI avatars outperform human live streamers, generating USD 7 million in seven hours, underscoring consumer openness to agentic commerce. India sees 48% of retailers piloting generative AI, backed by government skilling funds, pushing diffusion beyond metro centers. Diverse languages and payment ecosystems favour agents that localize seamlessly.

Europe emphasizes responsible AI, balancing innovation with consumer protection. IKEA’s governance blueprint guides peers through EU AI Act compliance. Labor-scarce UK grocers introduce AI shelf labels and cameras to offset wage inflation. Vendor opportunity lies in out-of-the-box compliance toolkits that embed transparency reports and algorithm audit trails.

Competitive Landscape

The Agentic AI in Retail and E-commerce Market remains moderately fragmented. Cloud hyperscale’s, AWS, Azure, Google Cloud, supply foundational models and GPUs while releasing retail-vertical agents, thus operating as both suppliers and competitors. Retailers build in-house teams: Walmart Labs publishes open-source retail-LLM benchmarks, and Target’s tech hub prototypes edge inference chips. Specialist vendors such as Revionics deliver multi-agent pricing platforms that converse in natural language, targeting pain points hyperscale’s overlook.

Strategic alliances dominate over outright acquisitions. For example, Walgreens licenses Theatro’s voice-AI to bolster associate efficiency rather than developing its own stack. Platform ecosystems become stickier as each added agent feeds data back to centralized knowledge graphs, raising switching costs. Value shifts to orchestration, players able to coordinate fleets of micro-agents across pricing, inventory, and engagement win share irrespective of single-algorithm superiority.

Smaller disruptors exploit white space in emerging markets. Veesion’s shrink-detection algorithm thrives in mid-sized European grocers with limited security budgets, while Puzl AI bundles dynamic pricing for independent supermarkets. As SMB uptake rises, vendors offering simple subscription pricing and industry-encoded agents will carve niches. Given top five players collectively command well under 60% of total spend, competitive intrigue and partnership realignment will persist through the decade.

Agentic AI in Retail and E-commerce Industry Leaders

Amazon Web Services Inc.

Microsoft Corporation

Google LLC

International Business Machines Corporation

NVIDIA Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: SoftBank outlined plans to deploy 1 billion AI agents by year-end 2025, each capable of autonomous negotiation and decision making.

- June 2025: Baidu-powered AI avatars sold goods worth over USD 7 million in a seven-hour livestream, eclipsing human influencer metrics.

- April 2025: Revionics unveiled its alpha multi-agent pricing system at Google Cloud Next, promising natural-language collaboration among pricing bots.

- March 2025: Colgate-Palmolive staff created 3,000 personalized AI assistants via an internal AI Hub, easing organizational change management.

Global Agentic AI in Retail and E-commerce Market Report Scope

| Customer Engagement and Marketing Agents |

| Supply-Chain and Logistics Agents |

| In-Store Ops and Loss-Prevention Agents |

| Merchandising and Dynamic-Pricing Agents |

| E-Commerce Pure-Plays |

| Omnichannel Retailers |

| Grocery and Convenience |

| Specialty Stores |

| Generative Dialogue Agents |

| Prescriptive Analytics Agents |

| Computer-Vision Agents |

| Voice-Commerce Agents |

| Cloud |

| On-Premises |

| Edge |

| Large Enterprises |

| Small and Mid-Sized Enterprises |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Customer Engagement and Marketing Agents | |

| Supply-Chain and Logistics Agents | ||

| In-Store Ops and Loss-Prevention Agents | ||

| Merchandising and Dynamic-Pricing Agents | ||

| By Retail Format | E-Commerce Pure-Plays | |

| Omnichannel Retailers | ||

| Grocery and Convenience | ||

| Specialty Stores | ||

| By Technology Approach | Generative Dialogue Agents | |

| Prescriptive Analytics Agents | ||

| Computer-Vision Agents | ||

| Voice-Commerce Agents | ||

| By Deployment Model | Cloud | |

| On-Premises | ||

| Edge | ||

| By Organization Size | Large Enterprises | |

| Small and Mid-Sized Enterprises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the Agentic AI in Retail and E-commerce Market?

The Agentic AI in Retail and E-commerce Market size stands at USD 60.43 billion in 2026.

How fast will the market grow through 2031?

It is projected to expand at a 29.29% CAGR, reaching USD 218.37 billion by 2031.

Which application segment is expanding quickest?

Fraud and Risk Management agents record the highest growth trajectory with a 34.12% CAGR through 2031.

Why is Asia-Pacific considering the most attractive growth region?

Asia-Pacific posts a 34.88% CAGR due to unmanned-store rollouts, government AI programs, and consumer acceptance of automated experiences.

What are the main obstacles to wider AI deployment in retail?

Key restraints include governance debt leading to hallucination risks and global GPU-cluster power-supply bottlenecks that delay infrastructure rollouts.

How concentrated is supplier power in this market?

Top vendors capture roughly 60% of spend which suggests room for emerging specialists alongside incumbent hyperscale’s.

Page last updated on: