Agentic Artificial Intelligence In Telecommunications and Network Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.63 Billion |

| Market Size (2031) | USD 8.74 Billion |

| Growth Rate (2026 - 2031) | 13.55% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agentic Artificial Intelligence In Telecommunications and Network Management Market Analysis by Mordor Intelligence

The agentic Artificial Intelligence In Telecommunications And Network Management Market size is expected to grow from USD 4.00 billion in 2025 to USD 4.63 billion in 2026 and is forecast to reach USD 8.74 billion by 2031 at 13.55% CAGR over 2026-2031. Traffic expansion from immersive video, IoT telemetry, and network slicing is forcing operators to automate capacity planning and service assurance. Vendors are shifting from one-time software licenses toward consumption-based pricing that aligns fees with data-plane usage. Edge deployment momentum is rising because real-time fraud prevention and autonomous vehicle coordination cannot tolerate cloud latency. Competitive dynamics now turn on data-governance credibility, explainability of model decisions, and the breadth of pre-trained use cases rather than raw hardware scale.

Key Report Takeaways

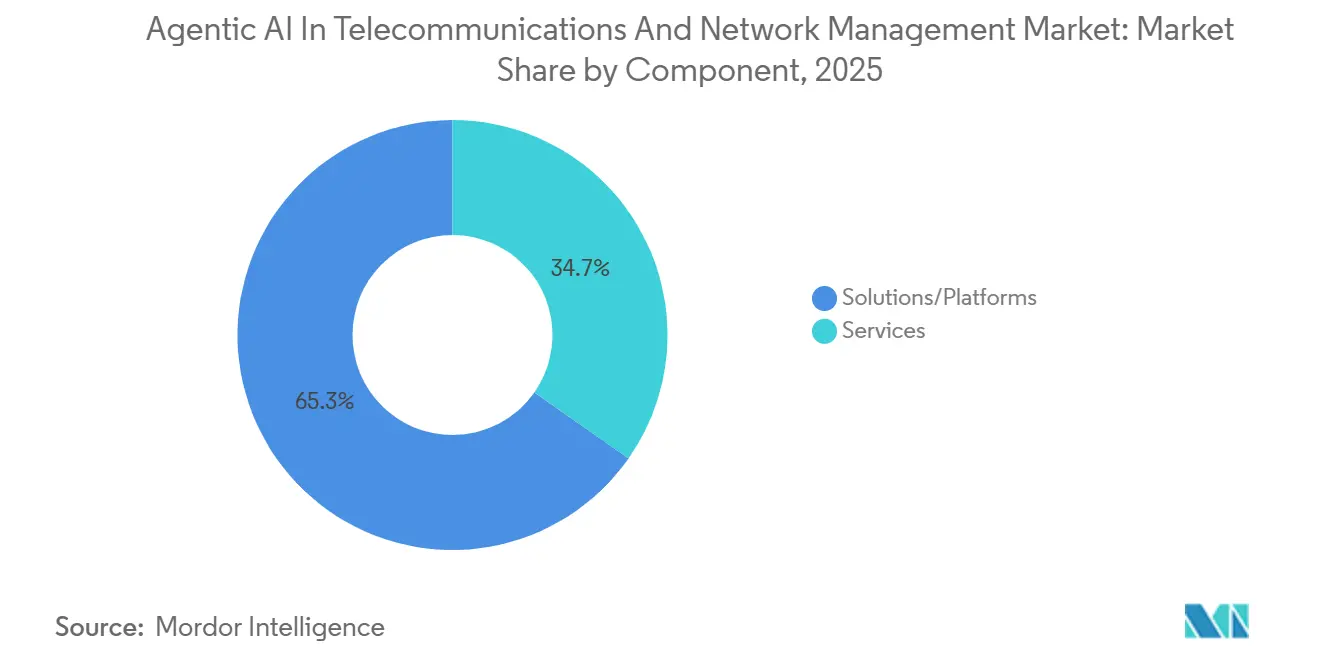

- By component, solutions and platforms owned 65.28% revenue in 2025 while the services segment is advancing at 14.01% CAGR through 2031.

- By deployment mode, cloud captured 60.19% of the agentic Artificial Intelligence In Telecommunications And Network Management Market share in 2025 and edge infrastructure is projected to expand at 13.89% CAGR to 2031.

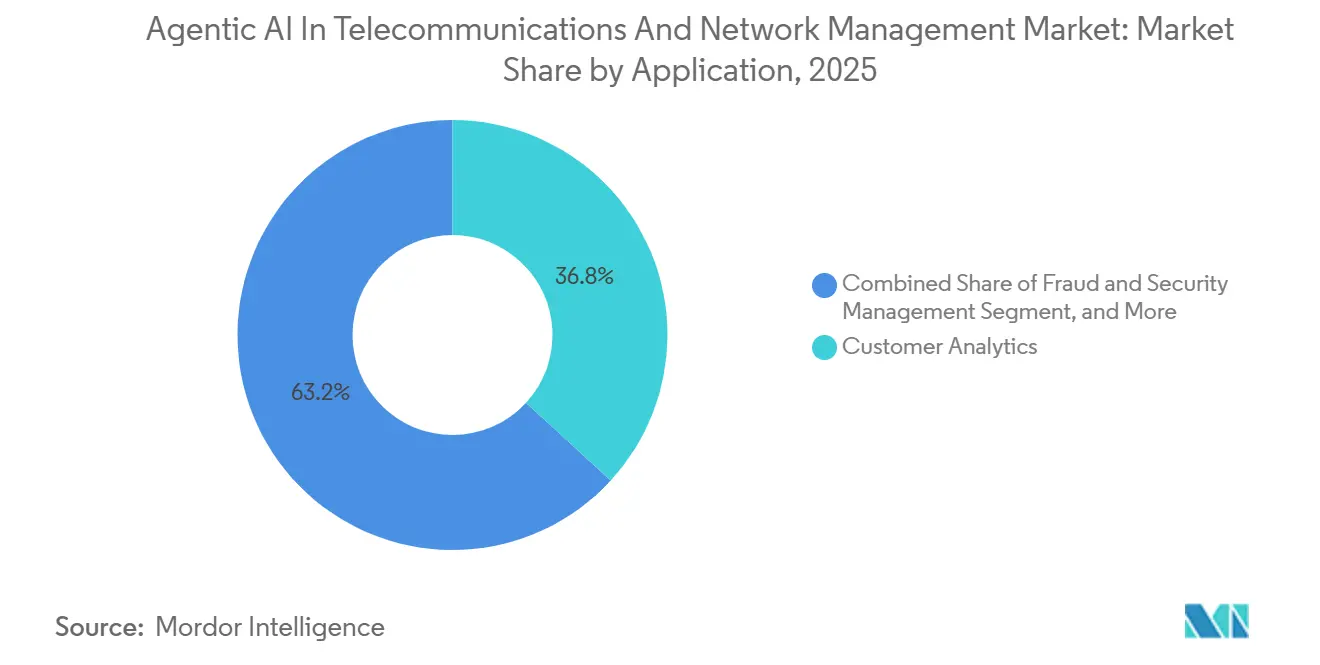

- By application, customer analytics led with 36.84% share of the 2025 agentic AI in telecommunications and network management market size, whereas fraud and security management records the fastest 13.94% CAGR.

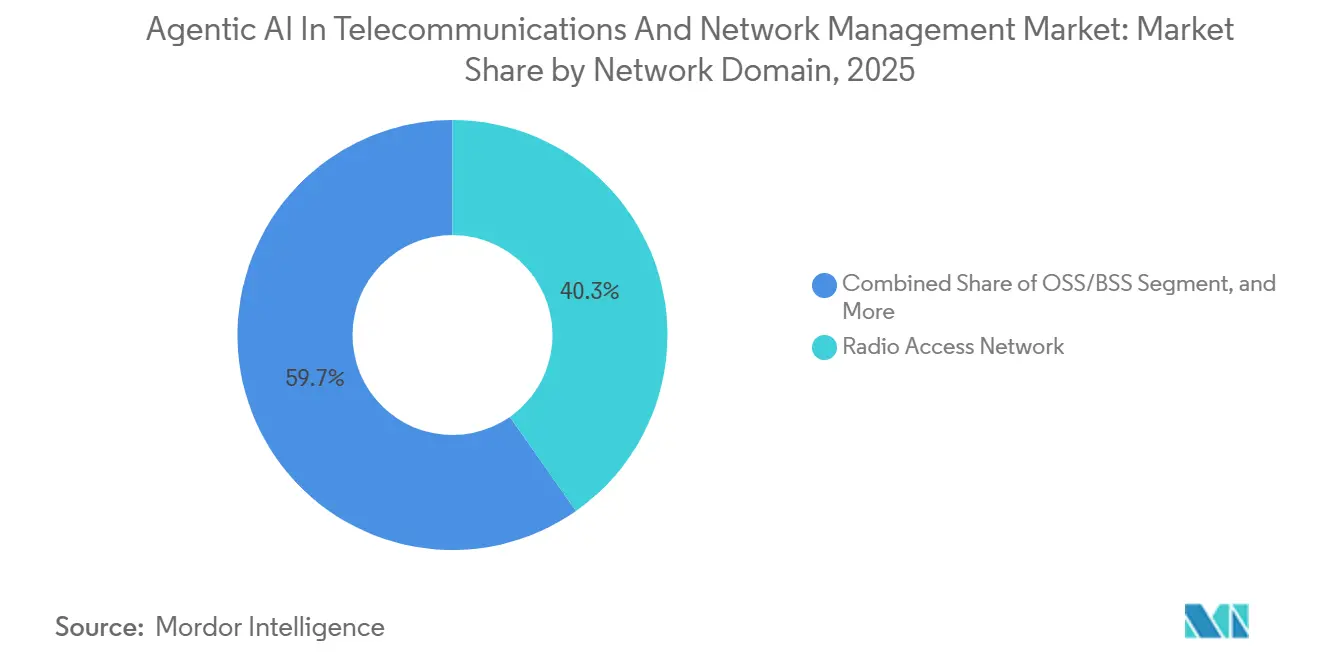

- By network domain, the radio access segment accounted for 40.27% share in 2025 while OSS/BSS transformation is growing at 14.06% CAGR through 2031.

- By AI technology, traditional machine-learning methods generated 50.55% of 2025 revenue but generative AI is accelerating at 14.22% CAGR.

- North America contributed 37.84% of 2025 value and Asia-Pacific shows the highest regional 14.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Agentic Artificial Intelligence In Telecommunications and Network Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising 5G/6G network complexity driving autonomous orchestration | +3.20% | Global, with peak intensity in North America and Asia-Pacific | Medium term (2-4 years) |

| Surging data traffic and need for predictive network optimisation | +2.80% | Global, particularly Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Growing demand for churn-reducing customer analytics | +2.30% | North America and Europe core, expanding to South America | Medium term (2-4 years) |

| Operator CAPEX shift toward AI-powered Open RAN and vRAN roll-outs | +2.10% | Asia-Pacific and North America lead, Europe following | Long term (≥ 4 years) |

| Emergence of sovereign AI data centers operated by telcos | +1.60% | Middle East, Asia-Pacific (China, India, Singapore), selective European markets | Long term (≥ 4 years) |

| Adoption of agentic AI for autonomous field-service operations | +1.50% | Global, with early traction in North America and Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising 5G/6G Network Complexity Driving Autonomous Orchestration

Each standalone 5G cell site now exposes more than 1 500 control parameters, overwhelming manual tuning. Nokia reported a 28% truck-roll reduction after deploying AI-based RAN optimisation across European networks, proving the cost leverage of closed-loop control.[1]Nokia Corporation, “Annual Report 2025,” nokia.com Early 6G trials introduce terahertz bands and reconfigurable intelligent surfaces that further widen the configuration space. Samsung’s 2025 architecture white paper described millisecond decision cycles as non-negotiable for ultra-reliable low-latency slices.[2]Samsung Electronics, “AI-Native 6G Architecture White Paper,” samsung.com Ericsson’s Intelligent Automation Platform dynamically idles radios during off-peak periods, trimming energy use by up to 22% across multivendor estates.[3]Ericsson AB, “Intelligent Automation Platform Overview,” ericsson.com As complexity rises, operators judge vendors on the maturity of embedded agents more than on raw radio performance.

Surging Data Traffic and Need for Predictive Network Optimisation

Global mobile data volume rose 32% in 2025, fueled by short-form video and cloud gaming.[4]Cisco Systems, “Annual Internet Report 2025,” cisco.com Reactive capacity augments no longer suffice when spectrum auction costs soar. China Mobile’s AI traffic forecasting curtailed unnecessary base-station activations by 19%, slashing diesel generator runtime in rural areas and lowering Scope 1 emissions. Bharti Airtel used predictive analytics to refarm spectrum dynamically, deferring major capital outlays. Accurate foresight translates directly into higher quality of experience without parallel cost growth, creating a widening moat for operators with mature models.

Growing Demand for Churn-Reducing Customer Analytics

In saturated markets, retention interventions cost far less than new subscriber acquisition. Verizon’s AI churn-prediction engine flags at-risk accounts 45 days earlier than rule-based methods, letting marketing teams issue targeted incentives that reduced post-paid attrition measurably. Telefónica’s Aura virtual assistant now resolves 62% of inbound queries without human hand-off, elevating Net Promoter Scores by eight points. Beyond saving costs, real-time micro-segmentation reveals new premium-latency or capacity tiers, converting analytics from defensive play to revenue catalyst.

Operator CAPEX Shift Toward AI-Powered Open RAN and vRAN Roll-Outs

The GSMA’s January 2026 tracker shows Open RAN captured 8% of 2025 RAN spend and is trending toward 20% by 2028. Dish Network’s cloud-native build demonstrated that software upgrades, rather than hardware swaps, can deliver feature velocity. Rakuten Mobile reported 40% lower total cost of ownership thanks to AI-driven automation across its fully virtualised network. Parallel Wireless added reinforcement-learning handover optimisation in 2025, underscoring how open interfaces accelerate AI experimentation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and regulatory hurdles for telco AI initiatives | -1.80% | Europe (GDPR, AI Act), North America (state-level privacy laws), Asia-Pacific (China, India data localization) | Short term (≤ 2 years) |

| Acute shortage of telecom-grade AI talent | -1.50% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Escalating inference energy costs at network edge | -1.20% | Global, with peak impact in regions with high electricity tariffs (Europe, Japan) | Medium term (2-4 years) |

| Vendor lock-in risk in proprietary AI-native network stacks | -0.90% | Global, particularly affecting operators with legacy installed bases | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Regulatory Hurdles for Telco AI Initiatives

The EU AI Act imposes conformity assessments for high-risk telecom AI such as real-time surveillance, adding 6-12 months of compliance delay. GDPR limits the granularity of location data, dulling predictive accuracy, while India’s Data Protection Act now requires fresh consent for profiling, with recent penalties reinforcing enforcement seriousness. China’s localisation rules force region-specific model training, fragmenting operator data lakes. Large carriers with dedicated governance teams can absorb compliance overhead; smaller rivals face disproportionate cost burdens that depress adoption.

Escalating Inference Energy Costs at Network Edge

Moving AI workloads from central clouds to thousands of edge sites exposes operators to rising power tariffs, especially in Europe and Japan. Ericsson measured 15-22% energy savings by dynamically reallocating traffic yet edge inference still competes with radio transmission for limited power budgets. Operators now evaluate AI frameworks on watt-per-inference efficiency, not merely accuracy. Renewable micro-grids and specialised accelerators such as NVIDIA Jetson help, but capital intensity remains a gating factor for wide edge rollout.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platforms Lead While Services Surge

Solutions platforms commanded 65.28% of 2025 revenue within the agentic Artificial Intelligence In Telecommunications And Network Management Market. Vendors bundle model lifecycle management, orchestration APIs, and pre-trained detectors, reducing integration friction for operators that lack extensive data-science teams. Subscription and usage-based fees are replacing perpetual licenses, aligning vendor income with network traffic cycles. The services segment, though smaller, is scaling at a 14.01% pace to 2031 as operators confront heterogeneous multivendor estates that stretch internal skill sets. Customized model tuning, data-pipeline engineering, and 24-hour managed operations transform one-time deployments into recurring partnerships. IBM’s 2025 managed-AI offering illustrates how hyperscalers monetize expertise while letting carriers retain data sovereignty.

The shift toward services means value accrues to providers that blend domain knowledge with AI science. Smaller regional operators increasingly outsource to global integrators, accelerating time-to-value but creating strategic reliance on external teams. As continuous retraining becomes essential, recurring service fees will rival software revenue, reshaping vendor balance sheets and customer procurement processes in the agentic AI in telecommunications and network management market.

By Deployment Mode: Edge Inference Challenges Cloud Supremacy

Cloud instances held 60.19% share of the agentic Artificial Intelligence In Telecommunications And Network Management Market size in 2025, leveraging elastic GPU pools and mature MLOps toolchains. Operators centralize training and non-latency-sensitive inference to exploit economies of scale. Yet edge and multi-access edge computing is growing at 13.89% CAGR through 2031, powered by sub-10 millisecond needs for augmented reality commerce and real-time fraud blocking. Verizon’s 30-city deployment of AWS Wavelength illustrated how hyperscalers extend the cloud paradigm right into operator networks.

Hybrid architectures now dominate. Training and heavy batch analytics run in national or regional clouds while inference executes on site-mounted accelerators. Energy optimisation and physical-security constraints limit full AI stacks at remote towers, so lightweight models and pruning techniques gain importance. Regulatory requirements around data residency further tilt certain workloads toward edge nodes. The agentic AI in telecommunications and network management market therefore evolves into a distributed fabric where workload placement is a dynamic optimisation problem guided by cost, latency, and compliance.

By Application: Security and Fraud Detection Accelerate

Customer analytics held 36.84% revenue share in 2025, reflecting the priority of churn containment. Operators ingest CDRs, billing data, and social sentiment to personalise retention offers. However, the fraud and security segment is expanding at a 13.94% clip as SIM-swap attacks and roaming abuse rise with mobile payments. Subex demonstrated a 73% false-positive reduction versus rule systems, freeing operator fraud desks for sophisticated cases.

Virtual assistants are evolving from scripted chatbots to multilingual agents that close 60% of tier-1 tickets. Predictive maintenance leans on IoT sensor data to forecast equipment failure weeks in advance, converting emergency truck rolls into planned visits that cost half as much. Network orchestration remains fundamental, but its growth rate moderates as initial deployments reach scale. As liability for payment fraud shifts onto carriers in some jurisdictions, fraud use cases will command board-level urgency, ensuring security analytics remains the fastest rower in the agentic AI in telecommunications and network management market.

By Network Domain: OSS/BSS Modernisation Gains Velocity

The radio access network generated 40.27% of 2025 spending thanks to dense small-cell rollouts and dynamic spectrum sharing that demand on-device intelligence. Vendors embed reinforcement learning agents directly into base-station software, enabling millisecond beamforming corrections without backhaul delay. Yet OSS/BSS modernisation is expanding at 14.06% CAGR as billing, provisioning, and service assurance systems built for circuit-switched eras choke on API-driven 5G services. Amdocs surveyed carriers in 2025 and found over half rated OSS/BSS overhaul as their top IT priority.

Modern, cloud-native stacks expose network capabilities through programmable interfaces, unlocking network-as-a-service offerings with automated service-level agreements. Transport and backhaul domains follow, using predictive analytics to pre-empt congestion. Core network AI directs user-plane traffic across distributed edge cores. Collectively, these advances position OSS/BSS as the digital foundation that lets operators monetise 5G beyond raw connectivity in the agentic AI in telecommunications and network management market.

By AI Technology: Generative Models Emerge From Niche to Necessity

Machine-learning techniques accounted for 50.55% of 2025 revenue, anchored by supervised classification and reinforcement learning for spectrum allocation. Generative AI is advancing at 14.22% CAGR, creating synthetic data for model training where privacy or data sparsity blocks conventional collection. Ericsson’s GenAI network assistant synthesises log insights and recommends remediation steps in readable language.

Deep learning remains vital for vision tasks such as drone-based tower inspections, but inference cost pushes heavier models toward regional data centers. Natural language processing underpins sentiment detection and multilingual virtual agents. Hybrid model stacks that blend generative, deep, and reinforcement learning are becoming standard, recognising that telecom challenges span forecasting, optimisation, and human-machine interaction. This multi-paradigm shift will redefine intellectual property battles as data curation overtakes algorithmic novelty within the agentic AI in telecommunications and network management market.

Geography Analysis

North America contributed 37.84% to 2025 revenue, led by aggressive Open RAN pilots and cloud partnerships. Verizon integrates AWS 5G Edge zones while AT&T anchors core workloads on Microsoft Azure, proving that telcos can outsource compute yet retain service control. The FCC’s USD 9 billion rural 5G fund mandates automated network management, catalysing AI uptake in sparsely populated regions. Canadian operators deploy churn analytics to defend share against upstarts, and Mexico’s wholesale player Altán offers AI-driven slicing to MVNOs. Fragmented state privacy laws add compliance burden but also create differentiation for carriers with mature data-governance playbooks.

Asia-Pacific is projected to climb at 14.29% CAGR through 2031. China’s CNY 500 billion new-infrastructure program accelerates domestic AI research and 5G coverage, with state carriers running joint AI and connectivity data centers. India’s energy-efficiency mandate obliges all new equipment to support AI-based optimisation, compressing vendor roadmaps. Japan’s NTT Docomo achieved 99.995% availability after automating operations, showing labor substitution benefits in high-wage economies. Southeast Asian multinationals share cross-border models that internalize diverse regulatory codes, gaining scale synergies unattainable by single-country operators. Australia’s NBN applies predictive maintenance AI to cut costly remote-area dispatches.

Europe balances innovation with strict oversight. The EU AI Act compels explainability, prompting vendors to embed model audit trails. Deutsche Telekom trimmed network energy consumption by 18% via AI scheduling, aligning with its net-zero pathway. Vodafone’s Google Cloud migration merges hyperscaler agility with telco SLA discipline, a template other European carriers now study. Orange’s virtual assistants achieved major cost savings while improving customer satisfaction. Smaller Central European markets prefer managed AI suites that trade flexibility for turnkey compliance. In the Middle East, sovereign funds bankroll telco-hosted AI data centers, bundling compute and connectivity for regional enterprises. Sub-Saharan Africa lags except for South Africa and Nigeria, where satellite-backed AI optimisation pilots mitigate terrestrial backhaul gaps.

Competitive Landscape

The top five vendors held around 45% share in 2025, indicating moderate concentration. Ericsson, Nokia, Huawei, Samsung, and Cisco upsell AI modules to entrenched hardware footprints, leveraging multi-year support contracts. Challengers such as Mavenir, Parallel Wireless, and Rakuten Symphony target greenfield or modernising operators with containerised stacks promising vendor-agnostic AI integration. Hyperscalers monetize inference by embedding compute at the edge and exposing telecom-specific AI APIs. Patent activity grew 34% year over year, with Huawei and Qualcomm leading the way in reinforcement-learning filings for spectrum control.

Standards groups including the O-RAN Alliance define open model interfaces that may erode proprietary advantages and shift competition toward data depth, labelling quality, and domain tuning. Start-ups like DeepSig focus on narrow high-value niches such as interference cancellation, outpacing broad platforms on specific KPIs.

Winning strategies now hinge on pairing algorithmic prowess with datasets that capture site-level idiosyncrasies, an asset incumbents still command through decades of logged network telemetry. As open interfaces mature, differentiation increasingly stems from the speed of continuous learning cycles and the energy efficiency of in-field inference devices.

Agentic Artificial Intelligence In Telecommunications and Network Management Industry Leaders

Telefonaktiebolaget LM Ericsson

Huawei Technologies Co., Ltd.

Nokia Corporation

Samsung Electronics Co., Ltd.

Cisco Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Nokia and Microsoft began integrating Azure AI into Nokia’s network-operations platform to automate root-cause analysis, targeting a 40% reduction in mean-time-to-repair.

- December 2025: Ericsson acquired a European reinforcement-learning firm for USD 250 million to deepen its spectrum optimisation portfolio.

- November 2025: Huawei introduced Intelligent RAN 3.0 with on-device generative AI, boosting handover success by 23% across initial China Mobile deployments.

- October 2025: Cisco invested USD 150 million in Rakuten Symphony to co-develop AI-driven orchestration tools for cloud-native infrastructure.

Global Agentic Artificial Intelligence In Telecommunications and Network Management Market Report Scope

The Agentic AI in Telecommunications and Network Management Market Report is Segmented by Component (Solutions/Platforms, Services), Deployment Mode (Cloud, On-Premises, Edge/MEC), Application (Customer Analytics, Network Optimisation and Orchestration, Fraud and Security Management, Virtual Assistants and CX Automation, Predictive Maintenance, Other Applications), Network Domain (Core Network, Radio Access Network, Transport/Backhaul, OSS/BSS), AI Technology (Machine Learning, Natural Language Processing, Deep Learning, Generative AI, Reinforcement Learning), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions/Platforms |

| Services |

| Cloud |

| On-Premises |

| Edge/MEC |

| Customer Analytics |

| Network Optimisation and Orchestration |

| Fraud and Security Management |

| Virtual Assistants and CX Automation |

| Predictive Maintenance |

| Other Applications |

| Core Network |

| Radio Access Network (RAN) |

| Transport/Backhaul |

| OSS/BSS |

| Machine Learning |

| Natural Language Processing |

| Deep Learning |

| Generative AI |

| Reinforcement Learning |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Singapore | |

| Malaysia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Solutions/Platforms | |

| Services | ||

| By Deployment Mode | Cloud | |

| On-Premises | ||

| Edge/MEC | ||

| By Application | Customer Analytics | |

| Network Optimisation and Orchestration | ||

| Fraud and Security Management | ||

| Virtual Assistants and CX Automation | ||

| Predictive Maintenance | ||

| Other Applications | ||

| By Network Domain | Core Network | |

| Radio Access Network (RAN) | ||

| Transport/Backhaul | ||

| OSS/BSS | ||

| By AI Technology | Machine Learning | |

| Natural Language Processing | ||

| Deep Learning | ||

| Generative AI | ||

| Reinforcement Learning | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the agentic AI in telecommunications and network management market?

The market stands at USD 4.63 billion in 2026 and is projected to reach USD 8.74 billion by 2031.

Which segment grows fastest within this space?

Services are expanding at 14.01% CAGR as operators seek integration, customization, and managed-AI expertise.

Why is edge deployment gaining traction?

Latency-sensitive use cases such as real-time fraud blocking and autonomous vehicle coordination require sub-10 millisecond response that centralized clouds cannot reliably deliver.

How significant is Asia-Pacific in future growth?

Asia-Pacific is forecast to record a 14.29% CAGR through 2031, the highest among regions, driven by large-scale 5G rollouts and government AI mandates.

Which technology area offers new differentiation?

Generative AI is emerging fast, providing synthetic training data, automated configuration scripts, and conversational troubleshooting assistance.

What key restraint could slow adoption?

Fragmented privacy regulations and the EU AI Acts conformity obligations can delay deployments by up to a year, especially for smaller carriers lacking deep compliance resources.

Page last updated on: