Agentic AI In Legal And Regulatory Tech Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

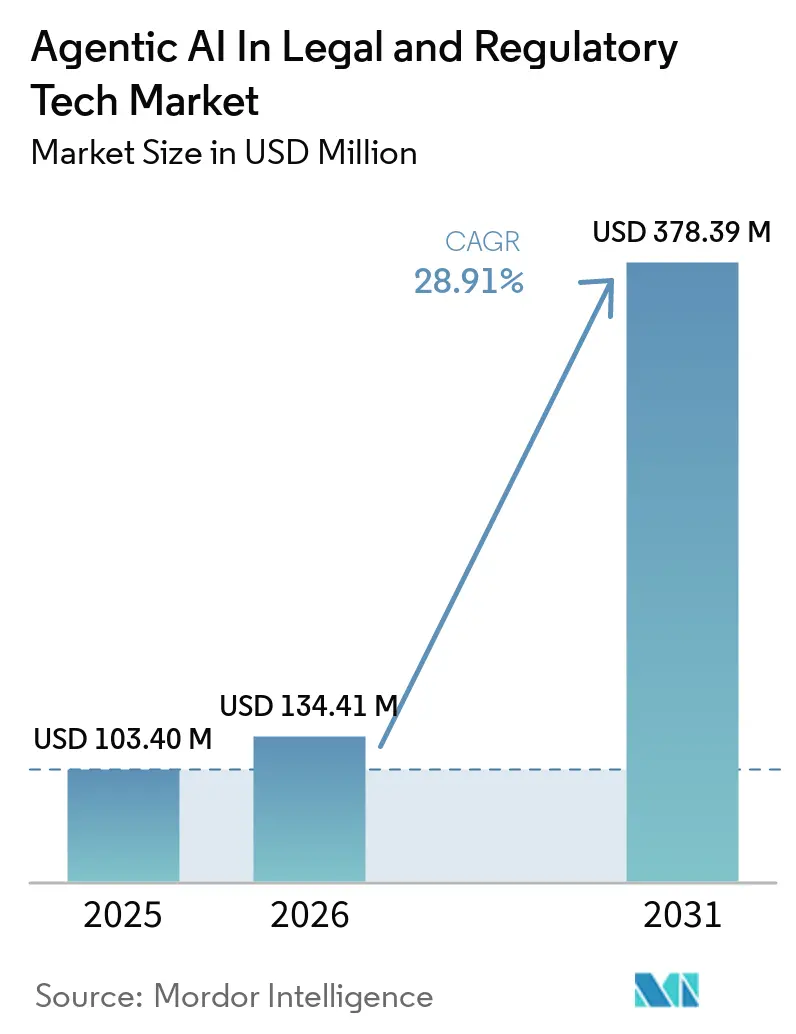

| Market Size (2026) | USD 134.41 Million |

| Market Size (2031) | USD 378.39 Million |

| Growth Rate (2026 - 2031) | 28.91% CAGR |

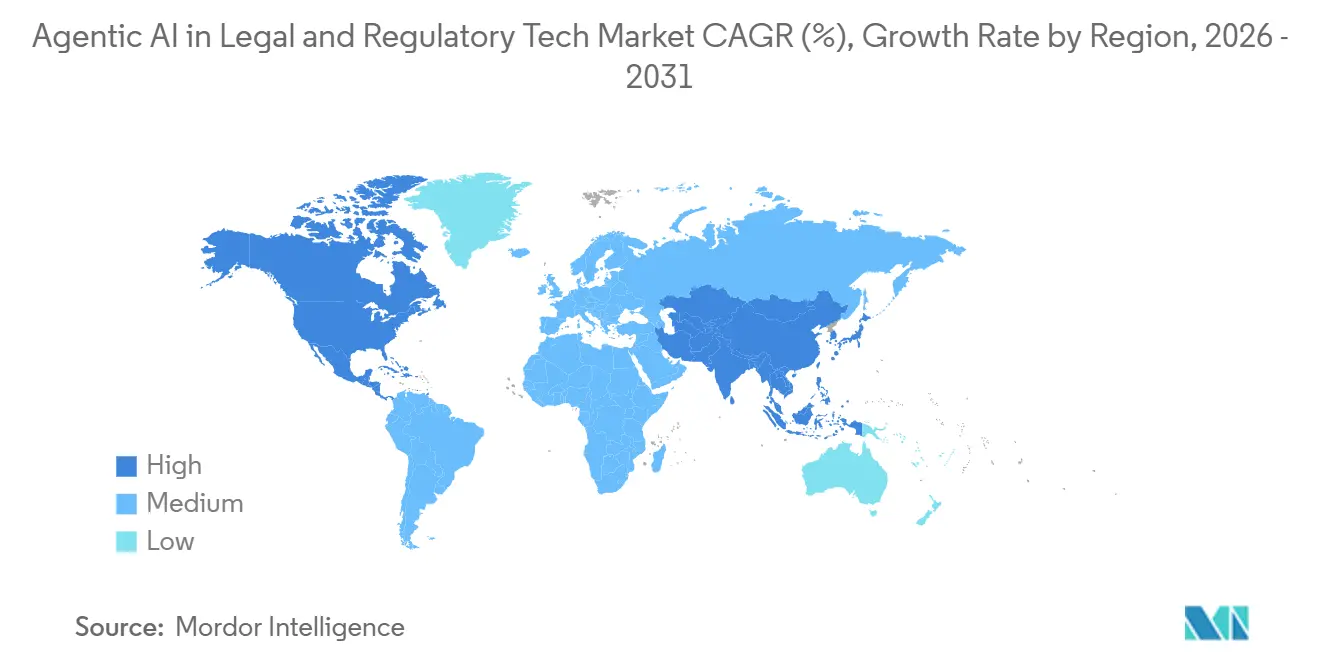

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agentic AI In Legal And Regulatory Tech Market Analysis by Mordor Intelligence

The agentic AI market in the legal and regulatory tech market is expected to grow from USD 103.4 million in 2025 to USD 134.41 million in 2026, and is forecast to reach USD 478.39 million by 2031 at a 28.91% CAGR over 2026-2031. Strong budget re-allocations toward autonomous document review, litigation analytics, and compliance monitoring are accelerating adoption, while large-language-model (LLM) maturity keeps integration costs low. Law firms now treat AI as a margin-preservation tool that mitigates rising associate salaries and blended billing rates. Corporate legal departments are equally active, using agents to shorten contract cycles and maintain audit-ready trails across multiple jurisdictions. Vendors that combine retrieval-augmented generation with explainability reporting are winning share because courts have begun sanctioning counsel for hallucinated citations.

Key Report Takeaways

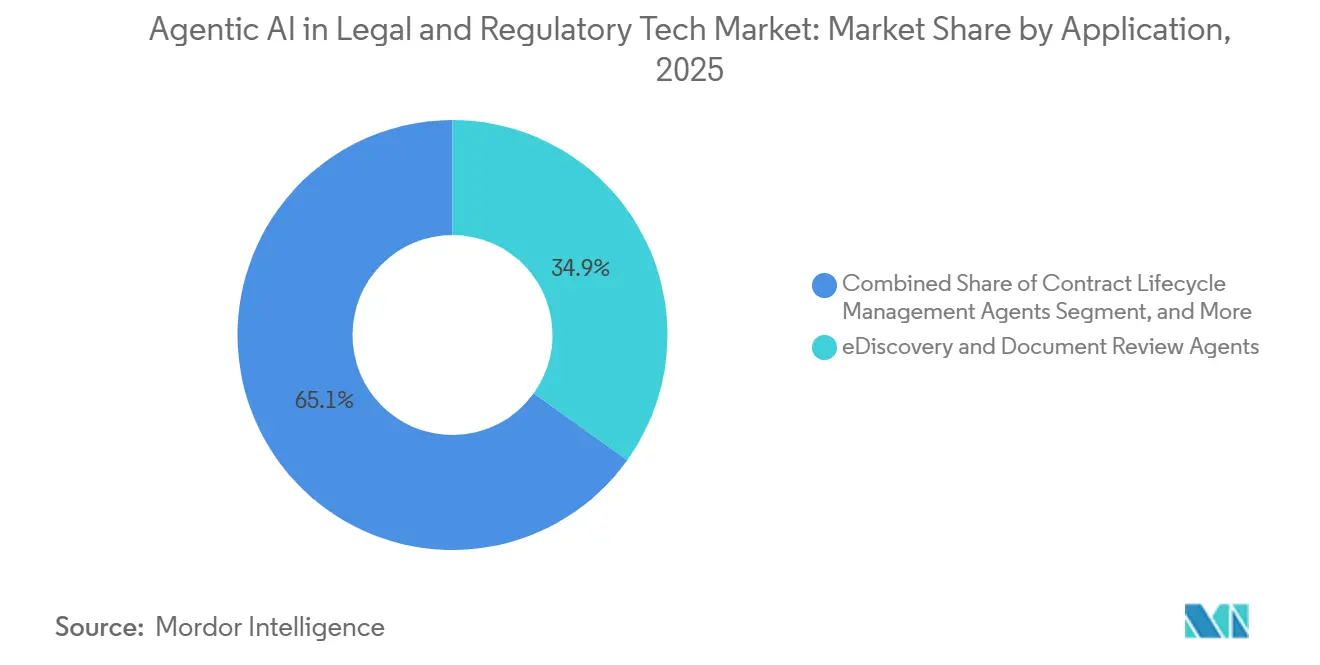

- By application, eDiscovery and document review agents led with 34.89% of the agentic AI in the legal and regulatory tech market, while litigation outcome prediction agents are projected to expand at a 30.11% CAGR through 2031 as firms seek data-driven venue selection and risk pricing.

- By deployment model, cloud-based platforms captured 61.89% of revenue in 2025, yet edge and embedded architectures are advancing at a 29.71% CAGR because privilege-sensitive documents often remain on-premises.

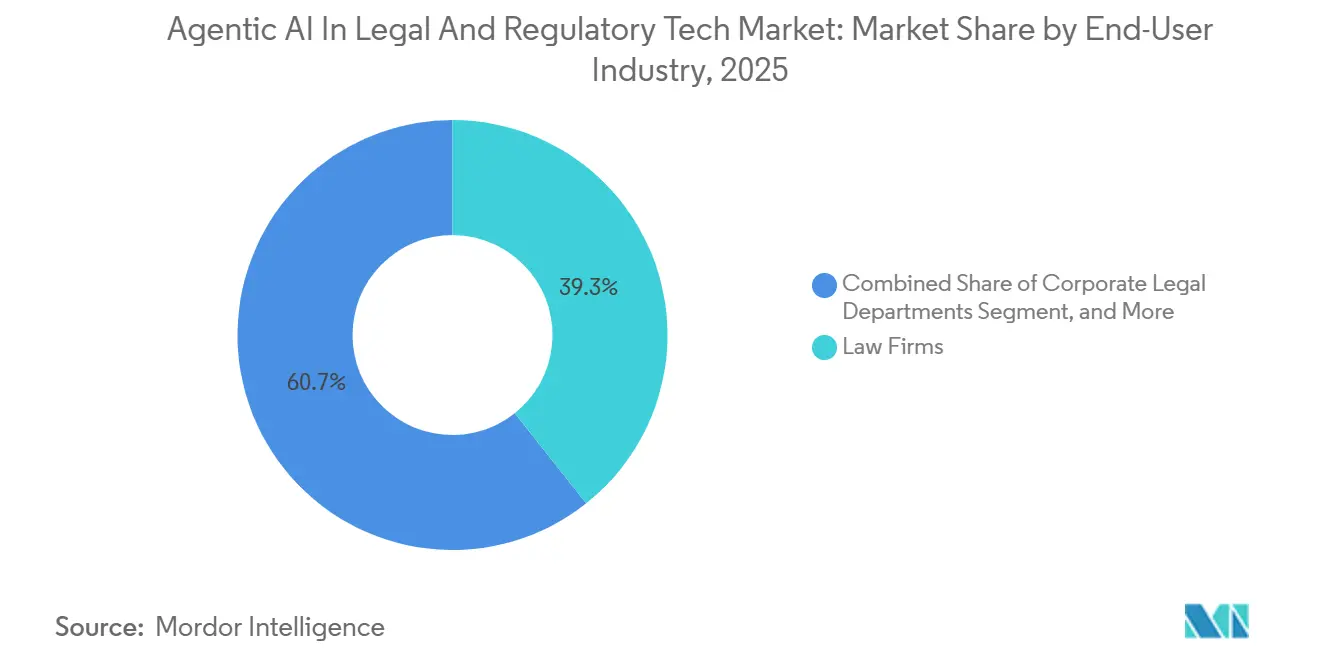

- By end user, law firms accounted for 39.31% of total 2025 revenue, reflecting their early-adopter status and deeper innovation budgets. Yet corporate legal departments are expected to grow at a 30.51% CAGR, shifting the mix of agentic AI in the legal and regulatory tech market.

- By core technology, LLM-centric agents held 46.18% of 2025 spending, while multi-agent orchestration platforms are scaling at 29.71% CAGR to coordinate cross-border due diligence, contract drafting, and regulatory monitoring.

- By geography, North America accounted for 41.89% of 2025 revenue, whereas Asia-Pacific is forecast to record a 29.91% CAGR through 2031 on the back of court-digitization programs and compliance reforms.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agentic AI In Legal And Regulatory Tech Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Mainstream Adoption of GenAI Tools Within Legal Workflows | +8.2% | Global, with North America and Europe leading enterprise deployment | Short term (≤ 2 years) |

| Cost-Reduction Imperatives Amid Rising Outside-Counsel Fees | +6.5% | North America and Europe, particularly AmLaw 100 and Magic Circle clients | Medium term (2-4 years) |

| Cloud-First Digital-Transformation Initiatives Across Legal Operations | +5.1% | Global, with Asia-Pacific accelerating cloud migration | Medium term (2-4 years) |

| Increasing Regulatory Scrutiny Demanding Audit-Ready Compliance Automation | +4.3% | North America, Europe, Asia-Pacific financial services hubs | Long term (≥ 4 years) |

| Under-Served Demand for Multi-Agent Orchestration in Cross-Border Matters | +2.8% | Europe and Asia-Pacific, driven by cross-border M&A and trade compliance | Long term (≥ 4 years) |

| Emerging VC-Backed Point Solutions Targeting Niche Litigation Tasks | +1.9% | North America and Europe, concentrated in venture-capital hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Mainstream Adoption of GenAI Tools Within Legal Workflows

Corporate Legal Operations Consortium data show that 52% of corporate legal teams had production-grade generative AI systems in 2025, more than double the prior year, and 85% had an internal AI committee guiding policy. Widespread committees signal permanent budget lines rather than one-off pilots. Thomson Reuters noted that 40% of legal professionals now use generative AI and 53% expect to add fully autonomous agents within 12 months. The steep curve is unique because LLMs require minimal custom coding, giving mid-market firms immediate access to capabilities once reserved for the exclusive domain of large firms.

Cost-Reduction Imperatives Amid Rising Outside-Counsel Fees

Thomson Reuters reported an 8.3% blended-rate increase for outside counsel in 2024, prompting corporate legal heads to expand in-house teams and adopt AI-driven review tools that replace low-complexity external work. A 500-attorney firm documented a drop in intake time from 48 hours to 5 minutes after deploying AI-supported triage, cutting partner hours and improving responsiveness. Legal operations groups increasingly rank technology proficiency as a talent-retention factor, linking cost control to workforce strategy.

Cloud-First Digital-Transformation Initiatives Across Legal Operations

The International Legal Technology Association found that 67% of firms already host document systems in the cloud, up 12 percentage points since 2022. Cloud elasticity matches the compute spikes that accompany LLM inference without the capital burden of GPUs. Yet the US District Court for the Southern District of New York ruled in February 2026 that privilege can be waived when consumer-grade AI tools lack enterprise safeguards, pushing buyers toward ISO 27001-certified vendors. As a result, legal IT teams now evaluate cloud providers on both performance and privilege controls.

Increasing Regulatory Scrutiny Demanding Audit-Ready Compliance Automation

The US Securities and Exchange Commission’s proposed real-time monitoring rules require broker-dealers to continuously track communications, a scale that is beyond the capacity of manual reviewers.[1]U.S. Securities and Exchange Commission, “Proposed Rules for Real-Time Communications Monitoring,” sec.gov FINRA’s 2025 examination priorities include documenting AI governance and raising the demand for agents to log model inputs, outputs, and bias-mitigation steps. Similar pressures appear in healthcare, where HIPAA penalties averaged USD 2.3 million per case in 2024. Vendors that embed granular audit trails and explainability functions are therefore winning multi-year licenses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy and Privilege Concerns Over Cloud-Hosted LLM Inference | -3.7% | Global, with heightened scrutiny in North America and Europe under attorney-client privilege doctrines | Short term (≤ 2 years) |

| Hallucination Liability and Ethical-Competence Obligations for Attorneys | -3.2% | Global, with U.S. courts leading sanctions and disciplinary actions | Short term (≤ 2 years) |

| Fragmented Legacy Systems Limiting Seamless AI Integration | -2.1% | North America and Europe, particularly large law firms with decades-old document management systems | Medium term (2-4 years) |

| Under-Reported Shortage of Legal-Domain AI Talent for Model Fine-Tuning | -1.6% | Global, with acute shortages in Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy And Privilege Concerns Over Cloud-Hosted LLM Inference

A February 2026 ruling in US v. Heppner declared that using consumer chatbots without contractual protections waived attorney-client privilege. The decision accelerated migration to enterprise-grade tiers that promise zero-retain data handling, regional residency controls, and SOC 2 Type II attestations. Forty-seven state bars now require written client consent before confidential data passes through AI tools. Risk-averse general counsel in healthcare and finance are delaying deployments until vendors deliver on-premises or hybrid options.

Hallucination Liability And Ethical-Competence Obligations For Attorneys

Legal Dive documented at least 486 sanction orders tied to AI-generated hallucinations by early 2026, 324 of which were in US courts. Penalties range from USD 1,000 fines to USD 100,000 fee awards, and dismissal of claims, reinforcing that counsel must manually verify outputs. The American Bar Association’s Model Rule 1.1 now explicitly covers AI competence, and professional-liability insurers are adding coverage exclusions or surcharges for AI-related claims.[2]American Bar Association, “Formal Opinion 512,” americanbar.org Firms therefore embed retrieval-augmented generation pipelines and human-in-the-loop reviews as standard operating procedure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: E-Discovery Agents Lead While Outcome Prediction Accelerates

In 2025, eDiscovery and document review agents secured 34.89% of the agentic AI (artificial intelligence) market share in the legal and regulatory tech market, a dominance driven by their ability to cut discovery budgets that often exceed USD 1 million per matter. Relativity’s aiR for Review reached 90% accuracy in privilege classification, halving human review hours. Litigation outcome prediction agents, though smaller today, are forecast to expand at a 30.11% CAGR, adding significant volume to the agentic artificial intelligence market in legal and regulatory tech by 2031.

Rapid adoption of predictive analytics stems from firms seeking data-backed settlement ranges and venue strategies. Lex Machina’s judge analytics module is now standard among 60% of AmLaw 200 practices.[3]LexisNexis, “Lex Machina Judge Analytics Adoption,” lexisnexis.com At the same time, contract-lifecycle agents attract corporate legal departments eager to shorten negotiation cycles, as evidenced by Ironclad’s USD 150 million Series F funding. Compliance-intelligence and IP-management agents round out demand, especially in sectors with intensive regulatory duties or large patent estates.

By Deployment Model: Cloud Dominates But Edge Gains Privilege-Sensitive Workloads

Cloud platforms accounted for 61.89% of revenue in 2025, confirming that most buyers prefer subscription economics and continuous model upgrades. The agentic artificial intelligence in legal and regulatory tech market therefore remains closely tied to hyperscaler GPU availability. However, edge and embedded deployments are growing at a 29.71% CAGR because sensitive data, such as cross-border M&A, must remain within firm firewalls. This shift is expanding the agentic artificial intelligence in the legal and regulatory tech market size for hardware-optimized inference appliances.

Hybrid architectures allow routine work to stay in the cloud while confidential data is processed on-premises, but they also introduce API duplication costs. Large AmLaw firms with legacy document systems often choose on-premises clusters to integrate with existing records. Meanwhile, practice-management vendors embed lightweight LLMs so that small firms can gain agentic features without juggling multiple logins.

By End-User Industry: Corporate Legal Departments Catch Up With Large Firms

Law firms accounted for 39.31% of total 2025 revenue, reflecting their early-adopter status and deeper innovation budgets. Yet corporate legal departments are expected to grow at a 30.51% CAGR, shifting the mix of agentic artificial intelligence in the legal and regulatory tech market. Pressure to curb outside-counsel fees and maintain constant compliance monitoring drives purchasing.

Financial services compliance units illustrate the trend as US broker-dealers prepare for real-time surveillance mandates. Healthcare and life-science teams, wary of HIPAA penalties, are also significant buyers. Government agencies, although slower due to procurement cycles, are trialing AI case-management tools. Technology companies lead IP-management adoption, automating patent-portfolio analysis and cross-licensing strategies.

By Core Technology: LLM Agents Dominate While Multi-Agent Orchestration Emerges

LLM-centric agents accounted for 46.18% of 2025 spending, primarily due to the efficiency and adaptability of transformer models such as GPT-4 and Claude. These models can be fine-tuned with minimal effort, making them highly appealing for a wide range of applications. Over the past two years, the adoption of agentic AI in the legal and regulatory tech market has undergone a significant transformation. The market has evolved from relying on basic keyword search tools to utilizing advanced conversational research assistants. These assistants are now capable of performing complex tasks, such as drafting interrogatories, thereby streamlining workflows and improving operational efficiency in the sector.

Multi-agent orchestration platforms, however, are the fastest-growing slice with a 29.71% CAGR. Harvey AI’s USD 100 million Series C validates investor belief that complex workflows, contract drafting, compliance checking, and negotiation require multiple coordinating agents. Rule-based systems remain in tax and securities filing, where regulation leaves little ambiguity, but their share is slipping. Vendors that layer retrieval-augmented generation and human oversight report hallucination rates below 5%, satisfying emerging court standards.

Geography Analysis

North America accounted for 41.89% of 2025 revenue for agentic AI in the legal and regulatory tech market. AmLaw 100 firms and Fortune 500 legal operations drive volume through cross-practice rollout of contract lifecycle and compliance agents. Enterprise adoption surged after the US District Court for the Southern District of New York clarified privilege obligations in February 2026. Canada’s growth is steadier; Toronto firms favor eDiscovery agents to stay competitive with U.S. counterparts, while Mexico sees uptake mainly among multinational subsidiaries complying with the United States-Mexico-Canada Agreement.

Asia-Pacific is projected to record a 29.91% CAGR through 2031, the fastest worldwide. China’s Smart Courts handle more than 30 million cases annually using AI case-routing and sentencing support.[4]Supreme People’s Court of China, “Smart Courts Initiative,” court.gov.cn Japan’s ministry pilots AI-enabled contract review to modernize corporate transactions, while India’s digital court projects raise demand for budget-friendly research agents. Singapore’s Smart Nation strategy and South Korea’s regulatory complexity in semiconductors and finance add further momentum.

Europe trails slightly but benefits from GDPR enforcement and active cross-border M&A, expanding the agentic AI market within the bloc's legal and regulatory tech. Magic Circle firms in London buy orchestration platforms to manage multi-jurisdictional due diligence, while German practices focus on EU AI Act compliance audits. France’s start-up scene cultivates contract negotiation agents tuned to civil-law systems. The Middle East, led by the United Arab Emirates and Saudi Arabia, is adopting sovereign-AI mandates to implement compliance and dispute-resolution tools. In Africa, adoption is concentrated in South Africa and Egypt due to infrastructure gaps elsewhere.

Competitive Landscape

The agentic AI market in legal and regulatory tech is moderately fragmented but edging toward consolidation. Thomson Reuters and RELX integrate newly acquired AI start-ups, and Casetext added a generative agent to Westlaw in 2025, to protect legacy research franchises. LexisNexis, for its part, embedded litigation prediction in Lexis+ AI. Venture-backed companies pursue orchestration white space; Harvey AI partnered with a Magic Circle firm in March 2026 to deploy the first enterprise-wide multi-agent stack.

Contract lifecycle specialists maintain high valuations, Ironclad’s Series F and Icertis’s Series G each raised USD 150 million, signaling confidence in workflow-centric platforms. Luminance extended beyond document review into autonomous negotiation, buoyed by a USD 40 million raise in January 2026. eDiscovery stalwarts Relativity and DISCO invest in privilege-classification modules to keep pace with the demands of hallucination mitigation. Technology differentiators now center on retrieval-augmented pipelines, zero-retain data contracts, and explainability dashboards that align with ABA Formal Opinion 512.

White space persists in areas such as mid-market litigation prediction, cross-border regulatory intelligence, and edge-deployed platforms for privilege-sensitive workloads. These gaps present significant opportunities for innovation and growth. Start-ups addressing these specific niches are anticipated to become prime acquisition targets for established players in the market. These incumbents are likely to pursue such acquisitions to enhance their orchestration suites, strengthen their service offerings, and expand their presence in regional markets, thereby gaining a competitive edge in the evolving landscape.

Agentic AI In Legal And Regulatory Tech Industry Leaders

Thomson Reuters Corporation

RELX PLC (LexisNexis Legal & Professional)

Harvey AI Inc.

Ironclad Inc.

Luminance Technologies Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Thomson Reuters expanded CoCounsel AI to deliver real-time regulatory intelligence across all U.S. states and the European Union.

- March 2026: Harvey AI formed a strategic partnership with a Magic Circle law firm to roll out multi-agent orchestration for global transactions.

- February 2026: Relativity launched aiR for Privilege Review, achieving 95% accuracy in privileged documents during AmLaw 100 beta tests.

- January 2026: Luminance raised USD 40 million in Series C funding to expand autonomous negotiation features across Asia-Pacific.

Global Agentic AI In Legal And Regulatory Tech Market Report Scope

The Agentic AI in Legal and Regulatory Tech Market refers to the global industry focused on the development, deployment, and commercialization of autonomous and semi-autonomous artificial intelligence systems designed to perform, optimize, and orchestrate legal, compliance, and regulatory workflows. These agentic AI systems leverage technologies such as machine learning, large language models (LLMs), generative AI, natural language processing (NLP), predictive analytics, rule-based reasoning, and multi-agent orchestration frameworks to automate legal research, document analysis, compliance monitoring, contract management, litigation support, and regulatory intelligence tasks with varying levels of autonomy.

The Agentic AI in Legal and Regulatory Tech Market Report is Segmented by Application (Contract Lifecycle Management Agents, eDiscovery and Document Review Agents, Legal Research and Analytics Agents, Compliance and Regulatory Intelligence Agents, Litigation Outcome Prediction Agents, and IP-Management Agents), Deployment Model (Cloud-based, On-premises, Hybrid, and Edge/Embedded), End-User Industry (Law Firms, Corporate Legal Departments, Financial-Services Compliance Units, Government and Regulatory Bodies, Healthcare and Life Sciences, Insurance, and Technology and Telecom), Core Technology (Machine-Learning and Predictive Models, Rule-based Expert Systems, Large-Language-Model GenAI Agents, and Multi-agent Orchestration Platforms), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Contract Lifecycle Management Agents |

| eDiscovery and Document Review Agents |

| Legal Research and Analytics Agents |

| Compliance and Regulatory Intelligence Agents |

| Litigation Outcome Prediction Agents |

| IP-Management Agents |

| Cloud-based |

| On-premises |

| Hybrid |

| Edge / Embedded |

| Law Firms |

| Corporate Legal Departments |

| Financial-Services Compliance Units |

| Government and Regulatory Bodies |

| Healthcare and Life Sciences |

| Insurance |

| Technology and Telecom |

| Machine-Learning and Predictive Models |

| Rule-based Expert Systems |

| Large-Language-Model (GenAI) Agents |

| Multi-agent Orchestration Platforms |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Application | Contract Lifecycle Management Agents | ||

| eDiscovery and Document Review Agents | |||

| Legal Research and Analytics Agents | |||

| Compliance and Regulatory Intelligence Agents | |||

| Litigation Outcome Prediction Agents | |||

| IP-Management Agents | |||

| By Deployment Model | Cloud-based | ||

| On-premises | |||

| Hybrid | |||

| Edge / Embedded | |||

| By End-User Industry | Law Firms | ||

| Corporate Legal Departments | |||

| Financial-Services Compliance Units | |||

| Government and Regulatory Bodies | |||

| Healthcare and Life Sciences | |||

| Insurance | |||

| Technology and Telecom | |||

| By Core Technology | Machine-Learning and Predictive Models | ||

| Rule-based Expert Systems | |||

| Large-Language-Model (GenAI) Agents | |||

| Multi-agent Orchestration Platforms | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the agentic AI in legal and regulatory tech market and how fast will it grow?

The market stood at USD 103.40 million in 2025, is projected at USD 134.41 million in 2026, and is set to reach USD 478.39 million by 2031, translating into a 28.91% CAGR.

Which application leads spending on autonomous agents inside law firms?

EDiscovery and document review agents commanded 34.89% revenue in 2025 because they slash manual review costs that can exceed USD 1 million per matter.

Why are corporate legal departments increasing investment in AI platforms?

Corporate teams seek to curb outside-counsel fees that rose 8.30% in 2024, and they favor agents that automate contract drafting, compliance checks, and discovery.

Which geographic region is expected to grow the fastest through 2031?

Asia-Pacific is forecast to record a 29.91% CAGR thanks to court digitization in China, legal-tech reforms in Japan, and India's e-Courts program.

How are regulators influencing AI adoption in legal services?

Bodies such as the SEC and FINRA now require detailed model governance and real-time monitoring, so buyers prefer platforms with audit-ready logs and explainability.

What technology trend is emerging beyond single-agent tools?

Multi-agent orchestration platforms are scaling rapidly, coordinating drafting, compliance, and negotiation steps inside one workflow to cut transaction times by about 40%.

Page last updated on: