Agentic AI In Manufacturing And Industrial Automation Market Size and Share

Market Overview

| Study Period | 2024 - 2030 |

|---|---|

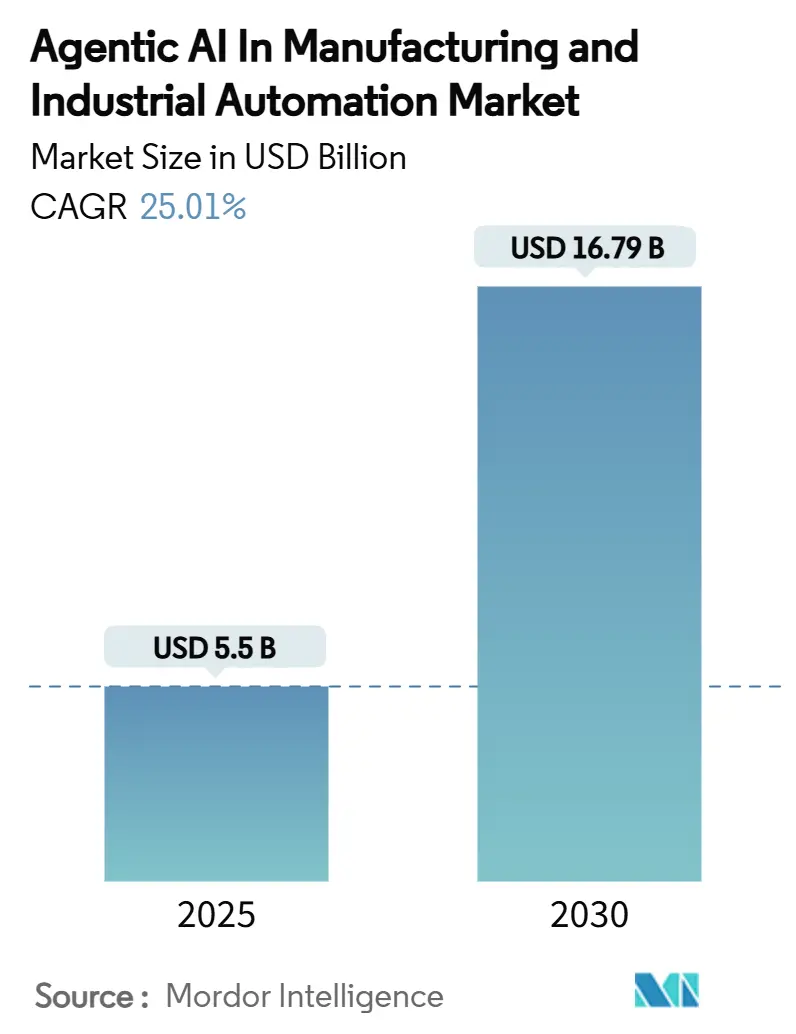

| Market Size (2025) | USD 5.5 Billion |

| Market Size (2030) | USD 16.79 Billion |

| Growth Rate (2025 - 2030) | 25.01% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agentic AI In Manufacturing And Industrial Automation Market Analysis by Mordor Intelligence

The agentic AI in manufacturing and industrial automation market reached a market size of USD 5.5 billion in 2025 and is forecast to expand to USD 16.79 billion by 2030, reflecting a robust 25.01% CAGR over the period. This growth stems from factories adopting autonomous decision-making systems that learn from live production data instead of following rigid scripts [1]AI that gets things moving: Bosch makes everyday life easier with algorithms,” Robert Bosch GmbH, bosch-presse.de. Rapid gains in defect-detection accuracy, predictive-maintenance savings, and supply-chain orchestration prove the economic case for agentic deployments, prompting CFOs to release larger AI budgets. Partnerships such as Siemens-NVIDIA, Samsung-ASML, and ABB-Microsoft highlight how software, silicon, and systems specialists are co-creating full-stack solutions that shorten engineering cycles and widen margins. Regionally, Asia-Pacific firms benefit from massive public incentives and robot density, while South America accelerates through new AI data-center complexes tying renewable power to high-performance compute. However, OT-IT data silos, up-front energy requirements for real-time inference, and workforce skill gaps remain important checks on momentum.

Key Report Takeaways

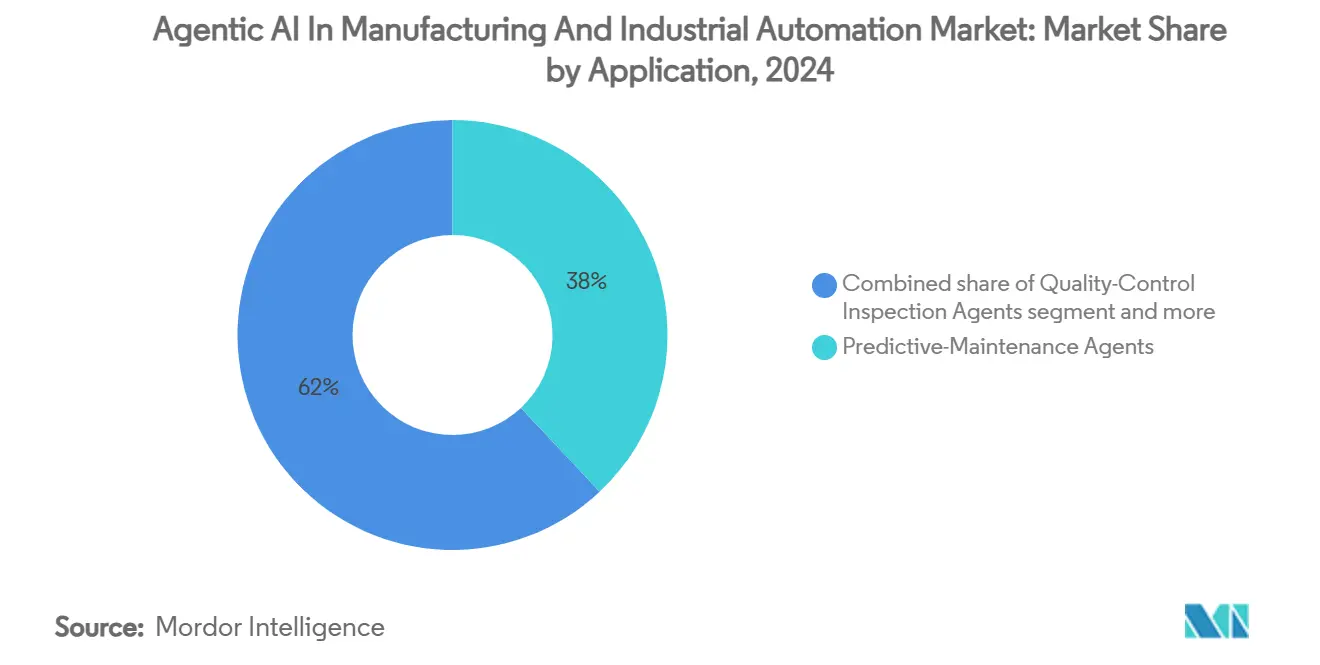

- By application, predictive-maintenance agents led with 38% of the agentic AI in manufacturing and industrial automation market share in 2024, while supply-chain optimisation agents are projected to advance at a 30% CAGR to 2030.

- By deployment mode, the cloud segment held 45% of the agentic AI in manufacturing and industrial automation market size in 2024; edge deployment records the highest projected CAGR at 31% through 2030.

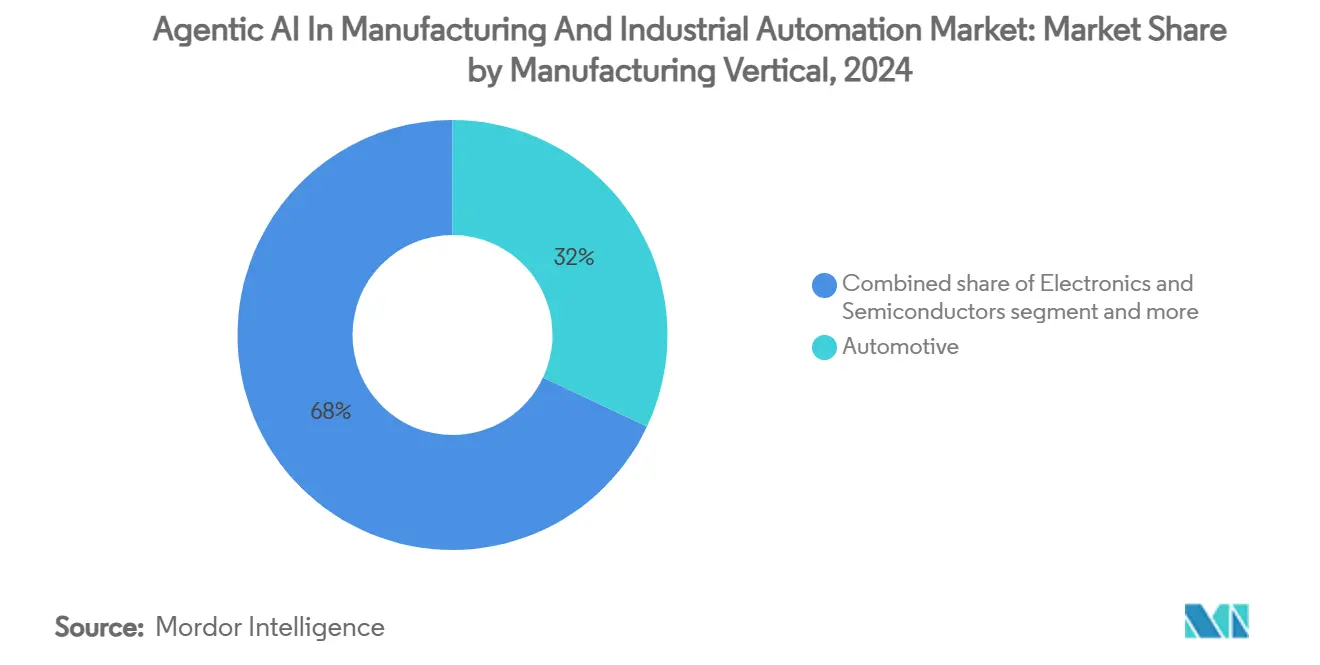

- By manufacturing vertical, automotive accounted for 32% share of the agentic AI in manufacturing and industrial automation market size in 2024 and electronics and semiconductors are advancing at a 29% CAGR through 2030.

- By component, software platforms captured 55% revenue share in 2024, whereas services are forecast to expand at a 28% CAGR up to 2030.

- By geography, Asia-Pacific led with 34% of the agentic AI in manufacturing and industrial automation market share in 2024, while South America exhibits the fastest regional CAGR at 29% to 2030.

Global Agentic AI In Manufacturing And Industrial Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gen-AI ROI proof-points accelerate budget release | 4.20% | Global, with early adoption in North America And EU | Short term (≤ 2 years) |

| OEM mega-investments in smart factories | 3.80% | Global, concentrated in Asia-Pacific and Europe | Medium term (2-4 years) |

| Predictive-maintenance cost-avoidance imperatives | 3.50% | Global, particularly in heavy industry regions | Medium term (2-4 years) |

| Edge inference enables sub-second autonomous control loops | 2.90% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| LLM agent plug-ins retrofit legacy MES without rip-and-replace | 2.10% | North America And EU, expanding to emerging markets | Medium term (2-4 years) |

| AI gigafactories dedicated to manufacturing agent training | 1.80% | China, Japan, South Korea, with expansion to EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Gen-AI ROI Proof-Points Accelerate Budget Release

Manufacturers now record six- to seven-figure annual savings per site from agentic quality control and scheduling initiatives, with defect-detection hitting 98.5% accuracy and throughput improving 15%. These hard figures replace theoretical pilots, moving projects from R and D to plant-wide roadmaps. Multi-year agreements such as Danone-Microsoft’s training of 100,000 staff show that enterprise-wide adoption is no longer optional but core to competitiveness. Finance teams approve larger capex once agentic AI demonstrates immediate margin uplift, shifting prioritisation away from incremental PLC upgrades toward autonomous optimisation capabilities.

OEM Mega-Investments in Smart Factories Drive Market Expansion

Capital commitments exceed EUR 2.5 billion at Bosch, USD 150 million at ABB Shanghai, and multi-billion plans in Brazil and Japan, signalling that next-generation plants are being designed around agentic AI from the ground up. Such greenfield projects anchor regional ecosystems, drawing component suppliers and software partners into clustered innovation hubs. Government co-funding amplifies private spend, accelerating time-to-scale for emerging agentic vendors.

Predictive-Maintenance Cost-Avoidance Imperatives

Field data prove that AI-based failure prediction can cut maintenance budgets 25–30% and breakdowns 70–75%. Nordic Sugar’s steam-dryer models identified faults within 13 days of occurrence, while NextEra Energy avoided USD 25 million annually by protecting turbines. These savings intensify as equipment grows more capital-intensive and downtime costs rise, making autonomous condition-monitoring a board-level priority across heavy industry.

Edge Inference Enables Sub-Second Autonomous Control Loops

Cloud latency cannot match milliseconds-level demands of safety-critical robotics. Edge AI consumes only 100 µW for inference versus 1 W in the cloud and avoids outbound data transfer, reducing both power and IP-exposure risks[2]“Edge AI in 2025: Bold Predictions and a Reality Check,” Barbara, barbara.tech. Affordable one-petaflop devices such as NVIDIA Project DIGITS push supercomputer-class power to line-side operators, unlocking closed-loop optimisation without network dependence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-silo/OT-IT integration complexity | -3.10% | Global, particularly in legacy manufacturing regions | Medium term (2-4 years) |

| Industrial skills gap and workforce resistance | -2.40% | North America And EU, with spillover to emerging markets | Long term (≥ 4 years) |

| Rising on-prem compute-energy costs for real-time AI inference | -1.90% | Global, concentrated in energy-intensive regions | Short term (≤ 2 years) |

| Regulatory ambiguity on autonomous decision accountability | -1.30% | EU and North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Silo / OT-IT Integration Complexity

Many plants still operate proprietary protocols that pre-date Ethernet, blocking real-time data flow into AI platforms. Integration overruns erode ROI and stall rollouts, particularly in multi-site enterprises with non-standardised PLC estates. Vendors now offer LLM-based middleware that translates legacy tags, but wide uptake will require continued service spending and patient change management.

Industrial Skills Gap and Workforce Resistance

Up to 2.1 million industrial roles may remain vacant by 2030 as AI competencies outpace training pipelines[3]“Preparing the Manufacturing Workforce for Greater Use of Robotics and AI,” Automation World, automationworld.com. Veteran operators often distrust black-box recommendations, forcing firms to pair upskilling with culture-shift programmes. Without new curricula that merge domain experience with AI literacy, deployment will lag in high-wage economies even as technology matures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Predictive-Maintenance Agents Anchor Early Value Realisation

Predictive-maintenance agents captured 38% of the agentic AI in manufacturing and industrial automation market share in 2024, proving to be the most accessible entry point for autonomous decision-making. Manufacturers deploy these agents to analyse vibration, temperature, and acoustic signals, achieving 23% fewer outages and multi-million-dollar savings. As reference cases grow, adjacent functions such as scheduling and quality control integrate seamlessly, with supply-chain optimisation agents escalating at a 30% CAGR to automate procurement and logistics.

The agentic AI in manufacturing and industrial automation market size for supply-chain agents is projected to multiply as disrupted shipping lanes and raw-material volatility demand self-healing networks[4] “Scaling Supply Chain Resilience: Agentic AI for Autonomous Operations,” IBM, ibm.com. Energy-optimisation agents are rising too, exemplified by Bosch’s Changsha site lowering electricity use 18% and CO₂ emissions 14%, indicating how environmental, social, and governance (ESG) targets align with cost efficiency. Cross-application orchestration is therefore expected to dominate later in the decade as integrated agent suites replace siloed point tools.

By Deployment Mode: Cloud Strength Meets Edge Speed

Cloud platforms retained 45% share of the agentic AI in manufacturing and industrial automation market size in 2024 thanks to instant scalability and simplified updates. Nevertheless, edge solutions march forward at a 31% CAGR because autonomous control loops cannot tolerate WAN lag for safety-critical movements. Manufacturers also cite data-sovereignty and IP-protection when opting for on-prem or hybrid architectures that localise inference but centralise model training.

Edge-friendly chipsets, fan less industrial GPUs, and federated-learning toolkits lower adoption hurdles, allowing small and mid-sized firms to bypass large-scale cloud contracts. Hybrid architecture is likely to become default, enabling fine-grained workload allocation that maximises both resilience and cost. As a result, the agentic AI in manufacturing and industrial automation market continues to blend cloud convenience with edge immediacy.

By Manufacturing Vertical: Automotive Sets the Pace for Cross-Sector Spillover

Automotive plants commanded 32% market share in 2024, adopting agentic AI for aerodynamic simulation, inline vision inspection, and real-time logistics. BMW’s 30× simulation speed-up through NVIDIA-Siemens underscores how high-volume, high-complexity production benefits first from autonomous optimisation. Electronics and semiconductors, forecast at a 29% CAGR, follow close behind as clean-room tolerances and 24/7 cycle times make self-configuring fabs attractive.

Food-and-beverage, chemicals, and heavy equipment segments are integrating lessons learned from these pioneers. Nordic Sugar’s predictive-maintenance proves viability in process industries, while Caterpillar pilots autonomous monitoring for harsh-environment machinery. Such cross-vertical diffusion expands the total addressable agentic AI in manufacturing and industrial automation market.

By Component: Software Platforms Lead Yet Services Scale Fastest

Software platforms accounted for 55% revenue in 2024, laying the algorithmic groundwork for perception, planning, and action loops. However, services are rising at a 28% CAGR as integrators bridge legacy OT with next-gen AI, customise models, and provide lifecycle optimisation. Hardware still matters; NVIDIA’s 10,000-GPU industrial cloud in Germany underpins Europe’s digital-twin workloads.

Servitisation shifts risk from manufacturers to vendors through performance-based contracts, ensuring that AI outcomes, not licenses, drive revenue. This model reinforces long-term vendor relationships and continuous improvement, accelerating adoption among firms lacking deep internal AI talent.

Geography Analysis

Asia-Pacific held 34% of the agentic AI in manufacturing and industrial automation market share in 2024, supported by Japan’s JPY 10 trillion AI-semiconductor agenda, China’s 38% contribution to global robot output, and South Korea’s autonomous fab initiatives. National roadmaps, high broadband penetration, and abundant engineering talent deliver fertile ground for autonomous plants. OpenAI’s choice of Tokyo for its first Asian office reflects policy clarity and ecosystem density that favour rapid commercialisation.

South America is the fastest-expanding sub-market at 29% CAGR as Brazil’s USD 4 billion AI program and USD 90 billion Scala AI City transform the region into an HPC stronghold. Government support, renewable-energy abundance, and rising industrial digitalisation combine to attract multinational OEMs looking for low-carbon AI operations. Chile and Uruguay follow Brazil as early adopters, leveraging regional AI maturity indexes to target manufacturing competitiveness.

North America and Europe remain influential through established industrial bases and legislative frameworks such as the EU AI Act. Yet both face headwinds from ageing power grids, prompting joint ventures into grid-interactive data centers and green hydrogen to power inference clusters. Strategic collaborations—Siemens-Microsoft, ABB-Hitachi—signal that trans-Atlantic partners aim to sustain leadership even as Asian manufacturers scale faster.

Competitive Landscape

Competition is moderate. Siemens, Rockwell, and ABB embed agentic layers into existing PLC, SCADA, and MES suites while NVIDIA, Microsoft, and IBM supply foundational GPUs and cloud APIs. Siemens’ Industrial Copilot, winner of the Hermes Award 2025, showcases generative AI coding assistance that shrinks engineering hours dramatically. NVIDIA’s industrial AI cloud and omnipresent GPU roadmaps position it as indispensable infrastructure, collaborating with Rockwell on vision inspection and with Foxconn on edge boxes.

Traditional barriers between automation vendors and hyperscale’s blur as both chase platform dominance. Emerging specialists such as Automatic focus on semiconductor-specific agents, while KIOTI explores AI-powered equipment management. White-space persists in low-power inference silicon, cross-plant agent orchestration, and vertical-specific knowledge graphs. M and A and co-development deals are expected to intensify as full-stack offerings prove sticky in long plant lifecycles.

Agentic AI In Manufacturing And Industrial Automation Industry Leaders

NVIDIA Corporation

Siemens Aktiengesellschaft

Robert Bosch GmbH

Rockwell Automation, Inc.

General Electric Company (GE Digital)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: NVIDIA began building the world’s first industrial AI cloud in Germany with 10,000 GPUs to serve manufacturers including BMW and Mercedes-Benz.

- June 2025: Bosch pledged EUR 2.5 billion for AI by 2027, aiming for EUR 10 billion AI-based sales by 2035.

- June 2025: SoftBank revealed plans for a trillion-dollar AI-robotics industrial complex.

- June 2025: ABB launched its OmniCore robotics control platform after a USD 170 million investment.

Global Agentic AI In Manufacturing And Industrial Automation Market Report Scope

| Predictive-Maintenance Agents |

| Quality-Control Inspection Agents |

| Supply-Chain Optimisation Agents |

| Production Scheduling Agents |

| Energy Optimisation Agents |

| Cloud |

| Edge |

| On-Premise |

| Hybrid |

| Automotive |

| Electronics and Semiconductors |

| Food and Beverage |

| Chemicals and Materials |

| Heavy Machinery and Industrial Equipment |

| Software Platforms |

| Services |

| Edge Hardware and Devices |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Predictive-Maintenance Agents | |

| Quality-Control Inspection Agents | ||

| Supply-Chain Optimisation Agents | ||

| Production Scheduling Agents | ||

| Energy Optimisation Agents | ||

| By Deployment Mode | Cloud | |

| Edge | ||

| On-Premise | ||

| Hybrid | ||

| By Manufacturing Vertical | Automotive | |

| Electronics and Semiconductors | ||

| Food and Beverage | ||

| Chemicals and Materials | ||

| Heavy Machinery and Industrial Equipment | ||

| By Component | Software Platforms | |

| Services | ||

| Edge Hardware and Devices | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the agentic AI in manufacturing and industrial automation market?

The market is valued at USD 5.5 billion in 2025 and is set to reach USD 16.79 billion by 2030.

Which application holds the largest share today?

Predictive-maintenance agents lead with 38% share, offering rapid ROI through downtime reduction.

Why is edge deployment growing so fast?

Edge solutions deliver millisecond-level latency and data sovereignty, driving a 31% CAGR through 2030.

Which region is expanding quickest?

South America is projected to grow at 29% CAGR owing to Brazil’s large-scale AI infrastructure investments.

Which vertical is adopting agentic AI most aggressively?

Automotive manufacturing commands 32% share due to complex assembly operations requiring autonomous optimisation.

How concentrated is the competitive landscape?

The market scores 6/10 for concentration; the top five vendors retain just over 60% combined share, leaving room for new entrants.

Page last updated on: