Agentic AI In Energy And Utilities Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

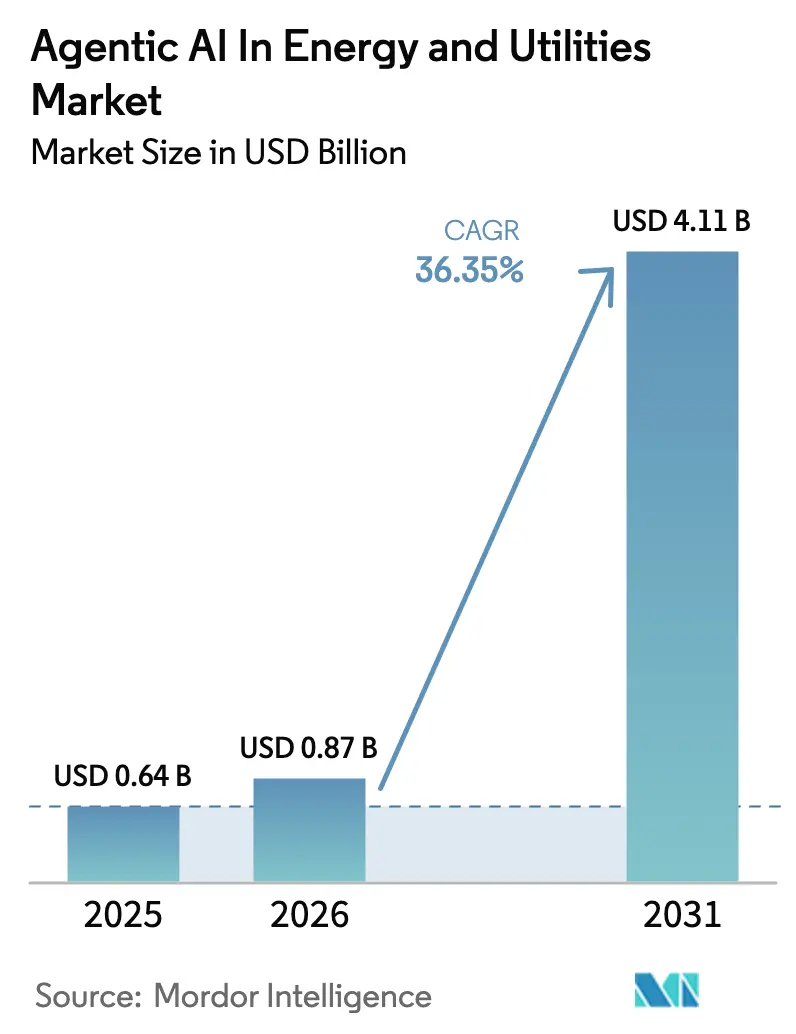

| Market Size (2026) | USD 0.87 Billion |

| Market Size (2031) | USD 4.11 Billion |

| Growth Rate (2026 - 2031) | 36.35% CAGR |

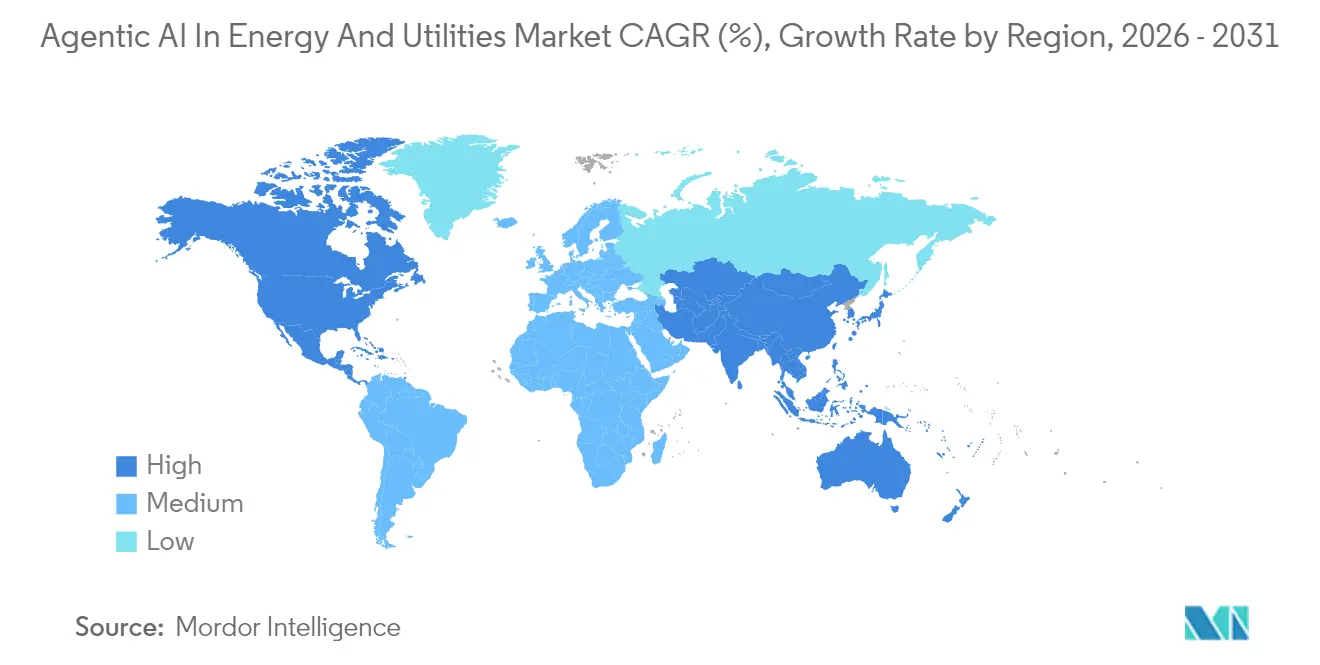

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

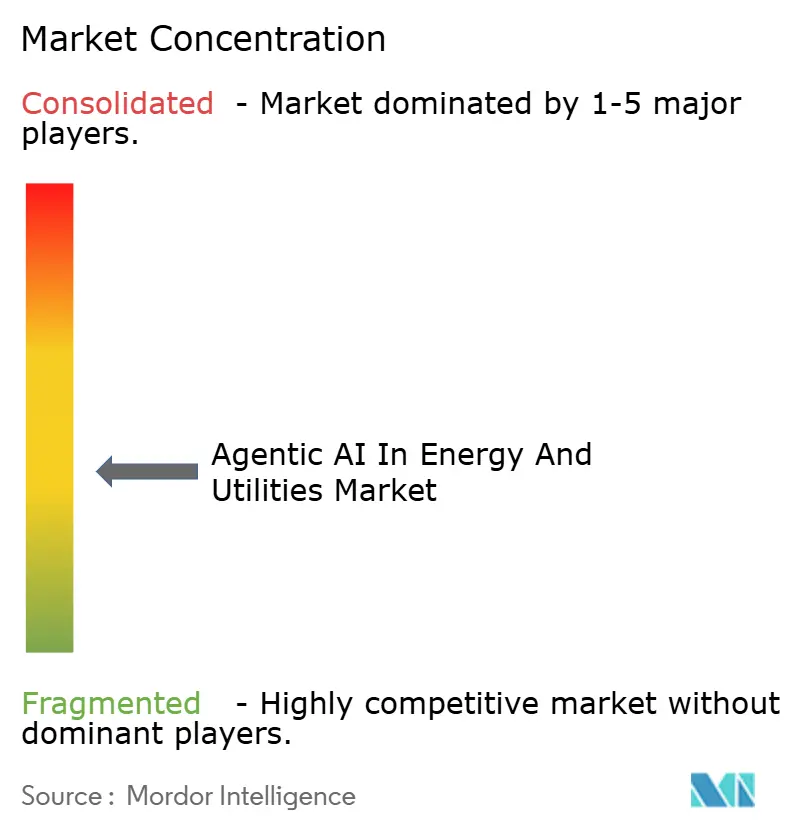

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agentic AI In Energy And Utilities Market Analysis by Mordor Intelligence

The Agentic AI in energy and utilities market size is expected to grow from USD 0.64 billion in 2025 to USD 0.87 billion in 2026 and is forecast to reach USD 4.11 billion by 2031 at 36.35% CAGR over 2026-2031. Large-scale grid digitalization, aggressive carbon-reduction mandates, and the proven cost advantages of autonomous decision-support tools underpin this growth. Utilities are pairing agent-based optimization with digital twins to orchestrate millions of distributed assets, while edge AI improves latency for protection schemes and demand-response dispatch. Early capital spending is heaviest in North America and Europe as regulators tighten outage-performance rules, yet Asia-Pacific shows the steepest acceleration thanks to state-funded smart-grid rollouts. Vendor competition is intensifying as industrial automation majors acquire analytics startups to embed conversational AI and generative diagnostics into routine operations. Parallel policy moves such as the U.S. Department of Energy’s AI infrastructure programs signal durable tailwinds for platform vendors that can balance safety, explainability, and cybersecurity.

Key Report Takeaways

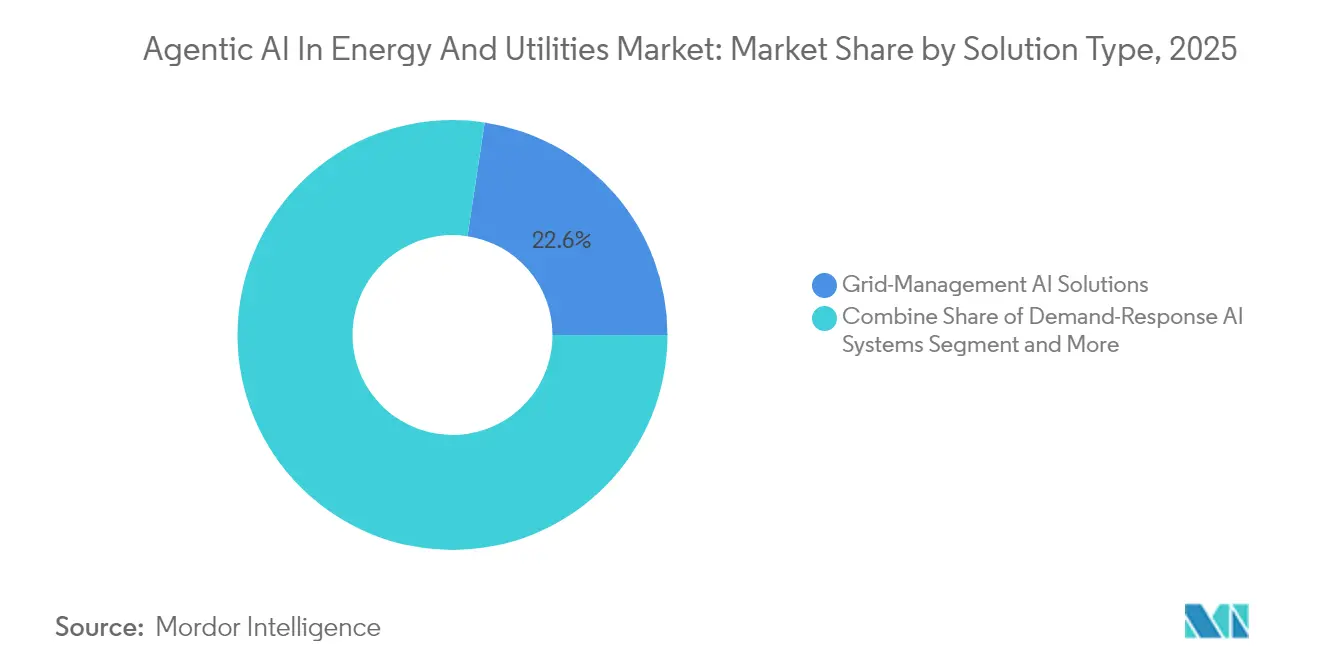

- By solution type, grid-management AI led with 22.61% revenue share in 2025, while demand-response AI is projected to grow at a 40.73% CAGR through 2031.

- By deployment model, the cloud segment held 67.94% of the Agentic AI in energy and utilities market share in 2025; edge/hybrid adoption is advancing at a 37.92% CAGR to 2031.

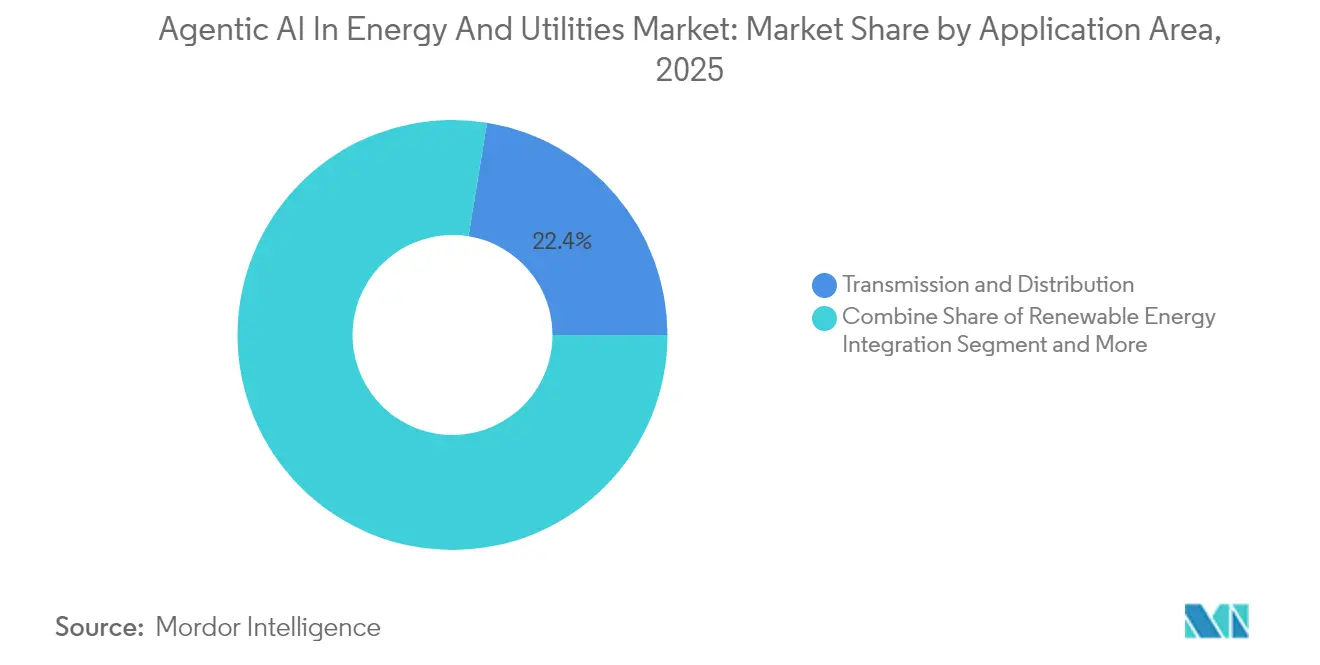

- By application, transmission and distribution accounted for a 22.44% share of the Agentic AI in energy and utilities market size in 2025 and renewable-energy integration is expanding at a 39.85% CAGR through 2031.

- By end-user, electric utilities captured 32.21% revenue share in 2025, whereas renewable independent power producers are forecast to post the fastest 38.21% CAGR to 2031.

- North America commanded 34.18% of 2025 global revenue; Asia-Pacific is on track for a 39.12% CAGR thanks to multibillion-dollar grid-modernization projects.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Agentic AI In Energy And Utilities Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising grid complexity demands AI-based optimization | +8.2% | Global, with early gains in North America, EU | Medium term (2-4 years) |

| Cost savings from predictive maintenance of aging infrastructure | +6.8% | North America and EU core, spill-over to APAC | Short term (≤ 2 years) |

| Increasing renewable energy penetration requiring real-time forecasting | +9.1% | Global, with APAC leading deployment | Medium term (2-4 years) |

| Regulatory push for energy-efficiency and carbon reduction | +5.4% | EU leading, North America following | Long term (≥ 4 years) |

| Convergence of autonomous trading agents in wholesale power markets | +4.7% | North America and EU advanced markets | Long term (≥ 4 years) |

| AI-based carbon accounting adoption for utility ESG reporting | +3.3% | Global, with EU regulatory mandate driving | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Grid Complexity Demands AI-Based Optimization

Distributed generation, bidirectional power flows, and electrification of transport raise the decision burden on control centers. The U.S. Department of Energy underscores AI-enabled optimization as the only viable path to millisecond-level balancing across thousands of feeders. Siemens’ Gridscale X digital-twin stack shows efficiency gains up to 30% by autonomously re-routing power around congestion. Regional grid operators with more than 30% renewable penetration already rely on agentic scheduling to avoid curtailment events. Real-time situational awareness coupled with reinforcement-learning dispatch is therefore moving from pilot to production. Investment momentum will accelerate as policymakers link outage-performance penalties to digital-control capabilities.

Cost Savings from Predictive Maintenance of Aging Infrastructure

Argonne National Laboratory measured 43-56% maintenance-expense reductions after utilities switched from run-to-failure regimes to agent-driven predictive scheduling. [1] Argonne National Laboratory, “Revolutionizing Energy Grid Maintenance,” ANL.GOVAI systems also trim truck rolls by up to 66% through image-based remote inspections of transformers and poles. The New York Power Authority’s drone-vision program validates the approach, ranking repair urgency within minutes. These savings extend asset lifecycles at a time when replacement budgets face rate-case scrutiny. Early adopters report two-year payback periods, reinforcing a rapid procurement cycle for predictive-maintenance platforms.

Increasing Renewable-Energy Penetration Requiring Real-Time Forecasting

Hitachi Energy’s Nostradamus AI delivers forecasts over 20% more accurate than industry baselines, enabling smoother scheduling of flexible generation. [2]Hitachi Energy, “AI-Powered Energy Forecasting Solution,” HITACHIENERGY.COMTexas grid data show solar contributing 21% of peak output in summer 2024, illustrating volatility that AI must absorb. BluWave-ai’s optimizer at the Sunbank farm demonstrates fast-loop learning that refines schedules every five minutes. As variable resources exceed 35% of generation in many balancing areas, grid operators shift from conventional statistical models to self-learning ensembles that anticipate weather shifts and price spikes in tandem.

Regulatory Push for Energy Efficiency and Carbon Reduction

The EU AI Act embeds cybersecurity, explainability, and audit trails into high-risk grid applications, effectively raising the floor for digital-maturity investment. Carbon-reduction mandates like the EU Fit for 55 package and state-level clean-energy standards in the United States incentivize utilities to automate curtailment management, demand-response, and loss minimization. AI-derived carbon accounting ties directly into environmental-social-governance reporting obligations, positioning autonomous agents as compliance tools rather than discretionary upgrades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of high-quality labeled operational data | -4.1% | Global, with emerging markets most affected | Short term (≤ 2 years) |

| Cyber-security concerns over AI-enabled control systems | -3.7% | Global, with critical infrastructure focus | Medium term (2-4 years) |

| Conservative utility procurement cycles slowing scale-up | -2.9% | North America and EU regulated markets | Medium term (2-4 years) |

| Emerging AI-model governance rules raising compliance costs | -2.2% | EU leading, global adoption following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of High-Quality Labeled Operational Data

Utilities hold decades of SCADA and outage logs, yet few datasets are labeled consistently enough for supervised learning. A 2024 MDPI study flagged data-governance gaps as the top implementation barrier in smart-grid pilots. [3]MDPI, “Impact of Artificial Intelligence on Distributed Energy Systems,” MDPI.COM Smaller cooperatives lack the staff to engineer features or enforce taxonomies, slowing model-training timetables. Data-trust frameworks and federated-learning methods show promise but add architectural complexity that only large investor-owned utilities can currently absorb.

Cyber-Security Concerns Over AI-Enabled Control Systems

The U.S. Department of Homeland Security warns that adversarial inputs could redirect autonomous grid controls.[4]U.S. Department of Homeland Security, “Safety and Security Guidelines,” DHS.GOVOak Ridge National Laboratory’s AI-PhyX suite identifies latent vulnerabilities in model pipelines before field deployment. Utilities must layer zero-trust architectures and real-time anomaly detection into every inference node, adding cost and elongating procurement cycles. Insurance carriers increasingly demand proof of model resilience, further heightening due-diligence thresholds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Grid-Management AI Leads Market Transformation

Grid-management AI controlled 22.61% of 2025 revenue, anchoring the Agentic AI in energy and utilities market as utilities prioritize visibility and control over geographically dispersed assets. Vendors integrate phasor-measurement-unit feeds, weather data, and participatory energy-resource signals to calculate optimal dispatch every second. The segment’s steady expansion stems from regulatory outage penalties and rising distributed-energy quotas. Demand-response AI, forecast to log a 40.73% CAGR, emerges as utilities link millions of smart thermostats and vehicle chargers to offset peak demand. Predictive-maintenance suites cut asset-downtime penalties, with ABB and Siemens bundling generative diagnostics that automate work-order creation. Smaller niches—carbon-capture monitoring, resilience analytics, and autonomous trading—show early traction where policy incentives align with decarbonization goals.

The competitive profile favors suppliers that deliver plug-and-play modules within broader operational-technology ecosystems. Open-API adoption allows utilities to add micro-services as regulations evolve, avoiding lock-in. Historical growth from 2019-2024 averaged closer to 20%, underscoring the post-2024 inflection linked to maturing cloud orchestration and edge inference chips. As more utilities publicize double-digit return-on-investment figures, budget committees show greater tolerance for multi-year, multi-site rollouts, sustaining momentum through the decade.

By Deployment Model: Cloud Dominance Meets Edge-Computing Revolution

Cloud deployments captured 67.94% of 2025 spending on the Agentic AI in energy and utilities market, driven by elastic compute economics and turnkey compliance toolsets offered by hyperscalers. Microsoft, AWS, and Google wrap domain-specific APIs around their generic AI stacks, accelerating proof-of-concept cycles for utilities with limited data-science staff. Nevertheless, edge/hybrid rollouts surge at a 37.92% CAGR because feeder-level control loops demand millisecond response unattainable when round-tripping to remote data centers. Edge inference devices now draw only 100 µW per task versus 1 W in earlier generations, slashing substation power overhead.

Utilities adopt hybrid architectures that keep non-critical analytics in the cloud while pushing fault isolation, islanding, and FLISR logic to pole-top devices. On-premise systems persist in nuclear-generation and defense-sensitive facilities where data sovereignty trumps cost efficiency. Regulatory frameworks, particularly in the EU, push for on-site logging of critical-infrastructure telemetry, further sustaining local-compute demand. The net effect is a bifurcated architecture where cloud remains the command-and-training hub and edge nodes execute context-aware, latency-sensitive inference.

By Application Area: Transmission Networks Drive Current Adoption

Transmission-and-distribution control rooms accounted for 22.44% of 2025 spend, cementing their role as the central buyers of the Agentic AI in energy and utilities market. High-fidelity digital twins catalog topology changes, enabling safe switching and congestion relief. Live streaming from enhanced grid sensors supplies 100% substation visibility, allowing operators to run near-real-time state estimators that feed autonomous switching logic. Renewable-integration applications, growing at 39.85% CAGR, align with utility-scale solar and wind fleet build-outs. Forecasting modules improve economic dispatch and reduce curtailment penalties, making them attractive to asset owners seeking merchant-market upside.

Power-generation control remains a sizeable niche where agentic AI tunes combustion turbines or hybrid combined-cycle plants. Oil-and-gas operators migrate AI upstream to reduce drilling downtime and downstream to squeeze refinery margins. Water utilities extract leakage alerts from acoustic signatures, proving that AI agents cut non-revenue-water losses. Emerging carbon-capture monitoring stacks apply computer vision to injection-well imaging, giving policymakers confidence in sequestration permanence.

By End-User Industry: Electric Utilities Lead Transformation

Electric utilities delivered 32.21% of 2025 revenue by deploying grid modernization initiatives that stretch from advanced metering to self-healing feeders. The Agentic AI in energy and utilities market size for electric-utility deployments is projected to cross USD 1.35 billion by 2031 as regulators link rate recovery to digital-resilience metrics. Eversource’s AI-enabled outage-prevention suite avoided 40,000 customer disruptions during pilot runs, illustrating tangible service-quality gains. Renewable IPPs grow fastest at 38.21% CAGR because merchant generators must forecast and trade power in near real time to hedge volatility.

Oil and gas majors adopt generative AI for reservoir modeling, cutting exploration timelines. Water utilities, motivated by drought regulations, turn to predictive leakage algorithms, while campus microgrids and industrial prosumers embed agentic schedulers to minimize demand charges. Growth from 2019-2024 was tempered by proof-of-concept hurdles, yet post-2025 momentum benefits from template-based procurement and pre-validated security architectures.

Geography Analysis

North America retained 34.18% of 2025 global revenue as federal programs, such as the USD 45 million grid-security AI initiative, underwrote pilot risk. The United States plans USD 12 billion of AI research funding, creating an ecosystem where utilities, cloud providers, and national labs co-develop use cases. Canada’s BluWave-ai export successes reinforce regional thought leadership.

Asia-Pacific is the fastest-growing territory with a 39.12% CAGR. Thailand’s USD 1.8 billion smart-grid blueprint exemplifies government-backed modernization. China promotes AI-enabled load forecasting to manage electrification booms and peak-shaving, while Singapore pilots district-scale smart grids as urban test beds. Growth here benefits from greenfield grid construction that skips legacy-system constraints.

Europe ranks third in revenue yet leads on regulation and industrial manufacturing. The EU AI Act establishes global compliance yardsticks, catalyzing investment in explainable AI and cybersecurity. Spain’s island-grid stabilization project with ABB demonstrates AI-integrated synchronous condensers that anchor weak networks. Eastern Europe and the Nordic region accelerate edge-AI rollouts for remote substations prone to harsh weather, driving resilient-infrastructure spending.

The Middle East and Africa show nascent adoption concentrated in Gulf Cooperation Council transmission operators and South African renewables developers. South America remains exploratory, with Brazil and Chile testing agentic trading bots in regional spot markets. Cross-regional learnings and falling silicon costs should narrow adoption gaps over the next five years.

Competitive Landscape

The Agentic AI in energy and utilities market hosts a mix of industrial automation veterans and hyperscale cloud entrants. Siemens, ABB, and Schneider Electric leverage decades of grid-equipment credentials to upsell AI modules bundled with hardware. Siemens’ 2025 acquisition of Altair Engineering bolsters digital-twin depth, enabling integrated simulation-plus-control offerings. ABB couples edge-compute relays with its new SACE Emax 3 breaker to promise sub-millisecond response in data-center switching.

Hyperscalers differentiate through scalable training infrastructure and subscription pricing. Google injects transformer-based models into grid-stability toolkits, while Microsoft co-develops predictive-maintenance copilots with industrial partners. AWS offers secure data lakes tailored for critical-infrastructure telemetry, lowering ingestion friction for utilities. Edge-native challengers, such as Edgecom Energy, attract strategic investment by focusing on low-latency inference and demand-charge mitigation.

The intellectual-property race centers on adaptive-control patents and privacy-preserving federated-learning frameworks. Collaboration footprints widen as vendors form joint labs with national research institutes to meet tightened security certifications. Mergers and venture stakes accelerate because large vendors seek domain talent and low-code interfaces that shorten sales cycles. Given the combined 45-50% revenue share held by the top five vendors, the market exhibits moderate concentration conducive to both specialist and platform-player success.

Agentic AI In Energy And Utilities Industry Leaders

Siemens AG

ABB Ltd.

Schneider Electric SE

IBM Corporation

Google LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Schneider Electric outlined grid-modernization roadmaps anticipating AI-driven demand surges

- February 2025: GE Appliances integrated ABB’s smart-panel hardware into its EcoBalance ecosystem

- January 2025: ABB invested in Edgecom Energy to expand generative AI demand-management solutions

- January 2025: ABB launched the SACE Emax 3 air circuit breaker with predictive-maintenance AI and IEC 62443 cybersecurity certification

Global Agentic AI In Energy And Utilities Market Report Scope

| Predictive-Maintenance AI Platforms |

| Energy-Optimization AI Software |

| Grid-Management AI Solutions |

| Demand-Response AI Systems |

| Autonomous Trading AI Agents |

| Other Solution Types |

| On-Premise |

| Cloud |

| Edge / Hybrid |

| Power Generation |

| Transmission and Distribution |

| Oil and Gas-Upstream |

| Oil and Gas-Mid/Downstream |

| Water Utilities |

| Renewable Energy Integration |

| Carbon Capture and Storage |

| Electric Utilities |

| Oil and Gas Companies |

| Water Utilities |

| Renewable Independent Power Producers (IPPs) |

| Energy Service Companies (ESCOs) |

| Industrial Prosumers |

| Other End User Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Solution Type | Predictive-Maintenance AI Platforms | ||

| Energy-Optimization AI Software | |||

| Grid-Management AI Solutions | |||

| Demand-Response AI Systems | |||

| Autonomous Trading AI Agents | |||

| Other Solution Types | |||

| By Deployment Model | On-Premise | ||

| Cloud | |||

| Edge / Hybrid | |||

| By Application Area | Power Generation | ||

| Transmission and Distribution | |||

| Oil and Gas-Upstream | |||

| Oil and Gas-Mid/Downstream | |||

| Water Utilities | |||

| Renewable Energy Integration | |||

| Carbon Capture and Storage | |||

| By End-User Industry | Electric Utilities | ||

| Oil and Gas Companies | |||

| Water Utilities | |||

| Renewable Independent Power Producers (IPPs) | |||

| Energy Service Companies (ESCOs) | |||

| Industrial Prosumers | |||

| Other End User Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the Agentic AI in energy and utilities market?

The market was valued at USD 0.87 billion in 2026 and is projected to reach USD 4.11 billion by 2031.

Which segment leads the market today?

Grid-management AI solutions hold the top position with a 22.61% share of 2025 revenue.

How fast is edge-based deployment growing?

Edge and hybrid architectures are expanding at a 37.92% CAGR between 2026 and 2031 as utilities seek sub-second control.

Which region will grow the fastest through 2031?

Asia-Pacific is forecast to post a 39.12% CAGR due to large-scale smart-grid investments.

What is the main barrier to adoption?

The lack of high-quality labeled operational data and associated governance frameworks remains the top implementation hurdle.

Page last updated on: