Human-AI Collaborative Work Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.59 Billion |

| Market Size (2031) | USD 23.28 Billion |

| Growth Rate (2026 - 2031) | 38.37% CAGR |

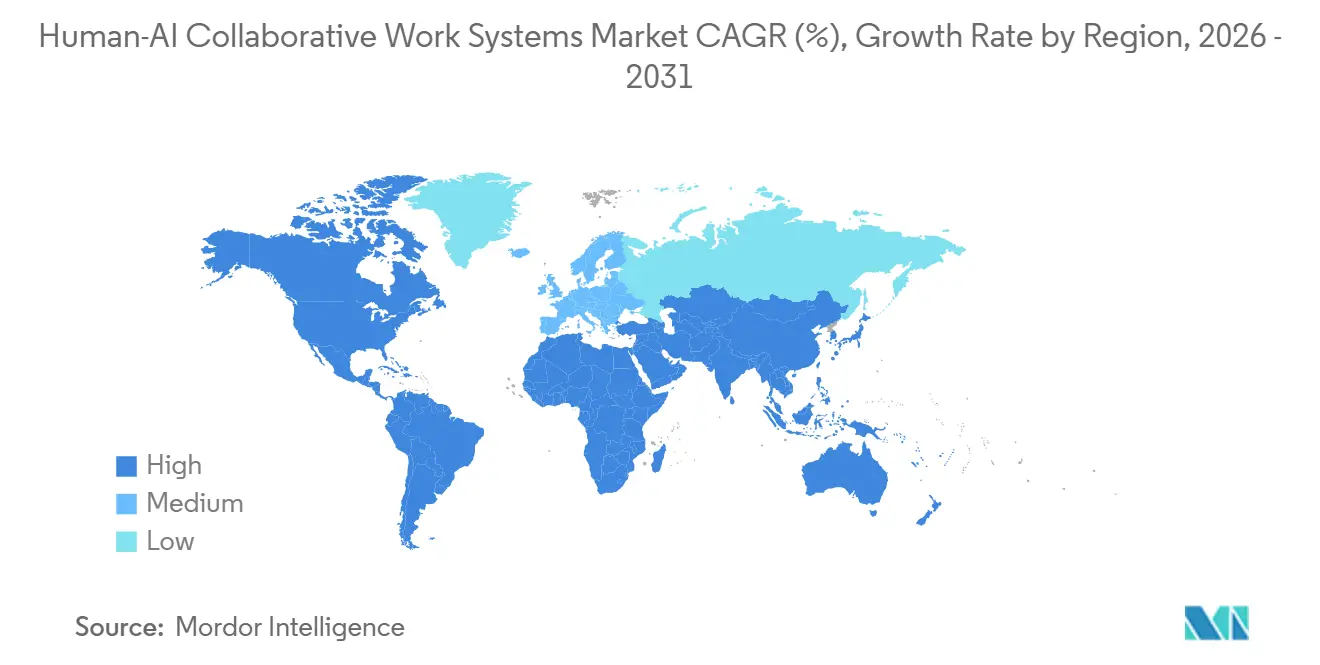

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

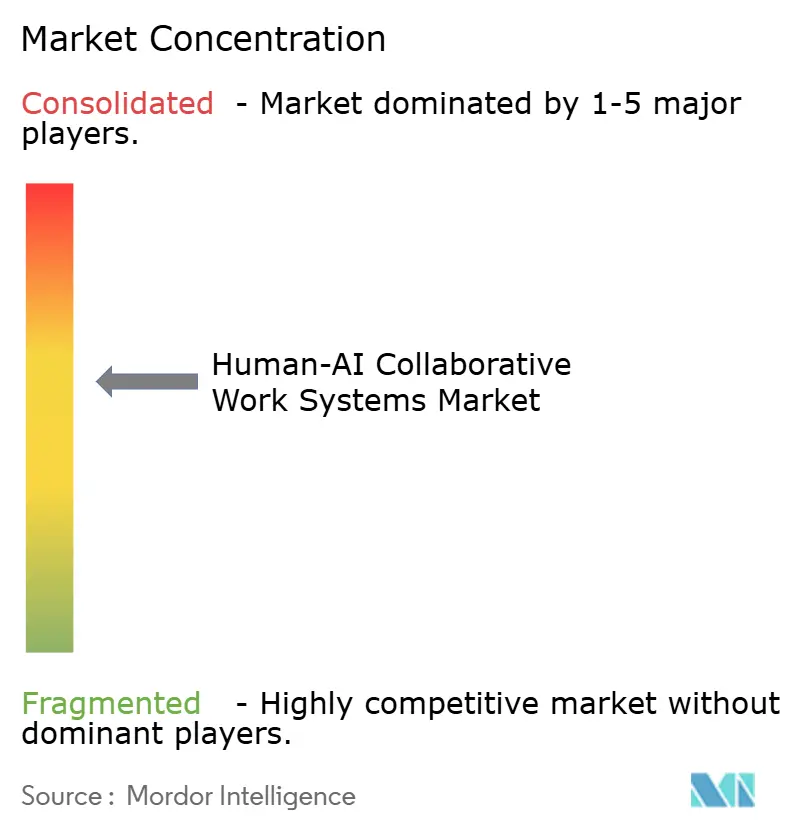

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Human-AI Collaborative Work Systems Market Analysis by Mordor Intelligence

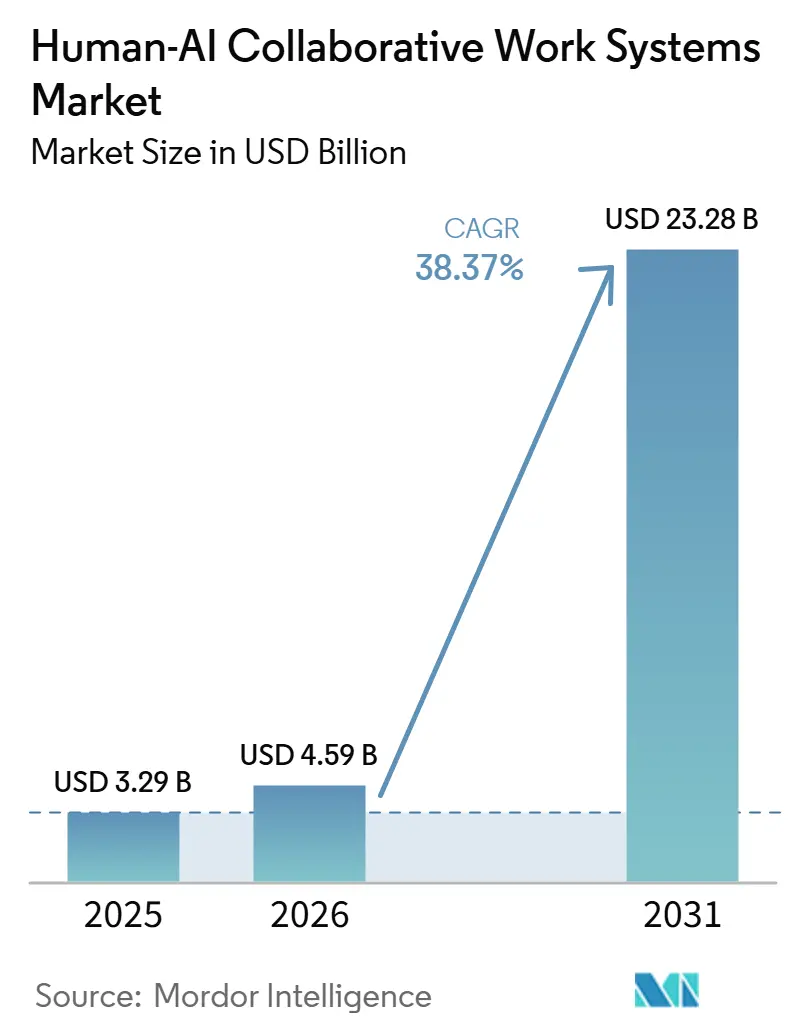

The human-AI collaborative work systems market size is projected to be USD 3.29 billion in 2025, USD 4.59 billion in 2026, and reach USD 23.28 billion by 2031, growing at a CAGR of 38.37% from 2026 to 2031. Accelerated enterprise adoption of agentic generative AI, hybrid-work normalization, and expanding low-code tools are shortening proof-of-concept cycles and moving pilots into production at scale. Early rollouts by Microsoft, IBM, and Salesforce have demonstrated measurable productivity gains, though penetration remains low relative to their total installed bases. Vendors are now prioritizing multimodal model capabilities, edge inference, and industry-specific governance toolkits to address organizations’ latency, compliance, and explainability requirements. Competition is intensifying as hyperscalers embed AI into productivity suites, while robotic process automation specialists converge toward conversational interfaces to protect their share against workflow incumbents.

Key Report Takeaways

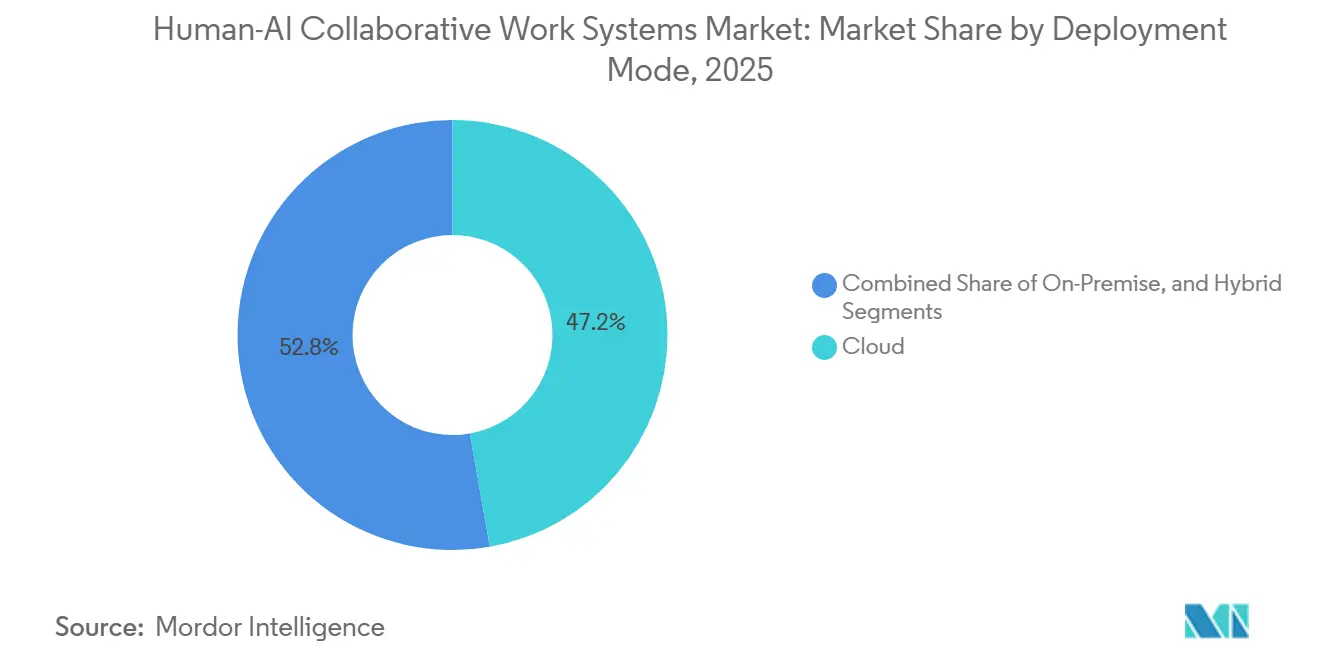

- By deployment mode, cloud configurations led with 47.22% revenue share in 2025; hybrid architectures are forecast to expand at a 38.97% CAGR through 2031.

- By organization size, large enterprises accounted for 58.19% of the human-AI collaborative work systems market share in 2025, while small and medium enterprises are projected to grow at 38.77% CAGR over 2026-2031.

- By component, software held 63.49% share of the human-AI collaborative work systems market size in 2025, and services are advancing at a 40.37% CAGR through 2031.

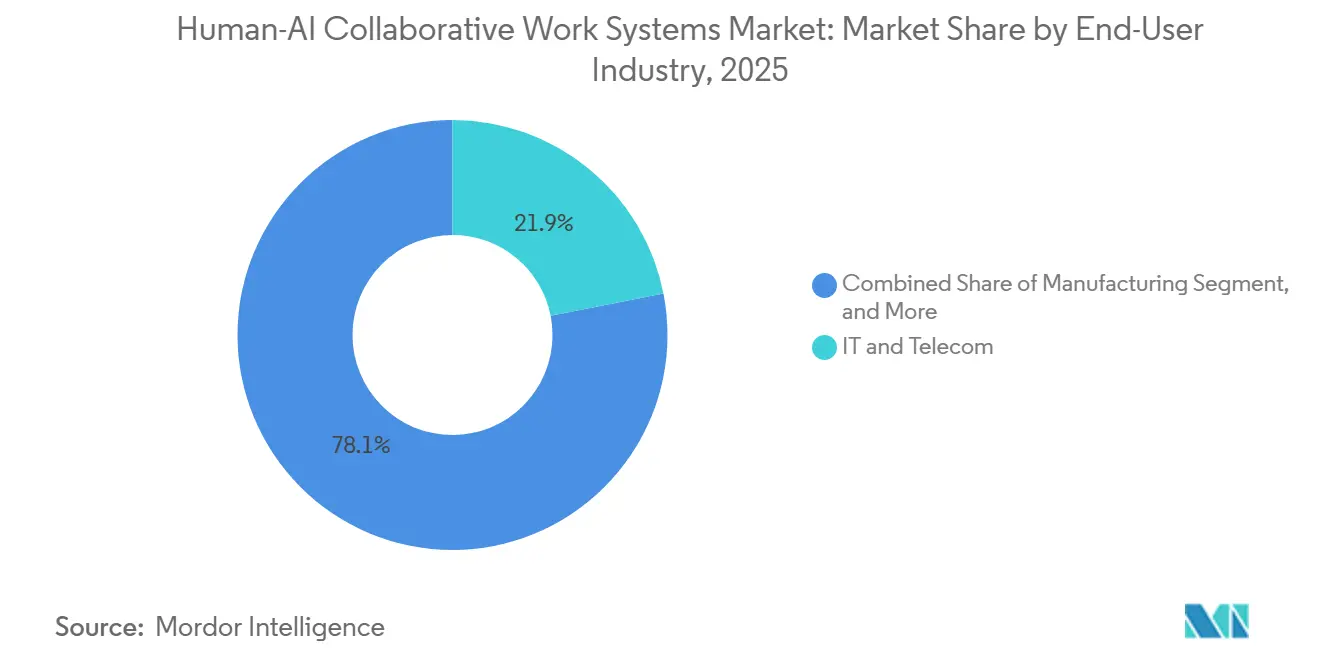

- By end-user industry, IT and telecom captured 21.91% spending in 2025; healthcare and life sciences is poised to grow at a 38.91% CAGR to 2031.

- By geography, North America commanded 34.57% of revenue in 2025, whereas Asia-Pacific is slated to register the fastest 39.57% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Human-AI Collaborative Work Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Enterprise Adoption Of Generative AI Assistants | +12.5% | Global, early concentration in North America and Western Europe | Short term (≤ 2 years) |

| Advances In Multimodal Large Language Models Enhancing Collaboration | +9.8% | Global, R&D leadership in United States, China, United Kingdom | Medium term (2-4 years) |

| Rising Demand For Hybrid-Work Orchestration Platforms | +7.2% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Integration Of RPA Bots With Conversational Agents | +6.4% | Global, manufacturing in Asia-Pacific and Europe | Medium term (2-4 years) |

| Availability Of Low-Code And No-Code AI Development Tools | +5.9% | Global, SME adoption strong in North America and Europe | Short term (≤ 2 years) |

| Growing Compliance Mandates For AI Auditability And Transparency | +4.1% | Europe, United States, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Enterprise Adoption of Generative AI Assistants

Organizations are embedding assistants directly into decision workflows rather than treating them as separate productivity add-ons. Microsoft disclosed that more than 65,000 enterprises consumed Azure OpenAI Service by late 2025, almost quadrupling its early-2024 count, while Copilot for Microsoft 365 surpassed 15 million paid seats, yet still touched less than 4% of the Office installed base, showing substantial headroom. Salesforce customers using Agentforce reported 30-50% reductions in case-resolution time after its late-2025 launch. IBM’s internal roll-out of watsonx across 270,000 employees targets USD 4.5 billion in cumulative productivity gains by 2027, reinforcing the ROI narrative. These examples underscore how early adopters validate economic impact before extending deployment across all knowledge workers.

Advances in Multimodal Large Language Models Enhancing Collaboration

Multimodal models that understand text, images, audio, and video are opening new collaboration frontiers in design, clinical diagnostics, and industrial maintenance. Google’s Gemini hit 750 million monthly active users in December 2025, with many regulated-industry customers opting for on-premises deployments to comply with data-residency rules. Adobe embedded Firefly into Creative Cloud, enabling marketers to generate personalized visual assets without hiring extra designers. In healthcare, the FDA approved more than 950 AI-enabled medical devices through 2024, many of which are powered by vision-language models that streamline radiology reads.[1]U.S. Food and Drug Administration, “AI/ML-Enabled Medical Devices,” fda.gov The move toward edge inference addresses low-latency requirements in retail checkout and autonomous robotics scenarios.

Rising Demand for Hybrid-Work Orchestration Platforms

Permanent hybrid-work policies spur the need for platforms that stitch together asynchronous tasks and surface contextual knowledge. Atlassian’s Rovo, launched in October 2025, indexes Confluence, Jira, Slack, and third-party repositories so staff can retrieve insights via natural language. Zoom’s AI Companion expanded in mid-2025 to extract action items and sentiment, helping firms cut post-meeting admin by about 25% ZOOM.US. Microsoft Teams integrated Copilot for live note-taking and follow-up drafting, turning the application into a central nervous system for distributed teams. Adoption remains uneven across the Asia-Pacific outside Japan and South Korea due to slower cultural shifts away from office-centric routines.

Integration of RPA Bots With Conversational Agents

Robotic process automation suppliers now overlay large language models to handle judgment-intensive steps that were previously excluded from rule-based flows. UiPath’s Autopilot lets workers describe tasks in plain English and watches Clipboard AI automatically assemble the workflow, attracting more than 1.7 million developers by early 2026. Automation Anywhere customers recorded 60% productivity gains in back-office processes during 2025 rollouts. ServiceNow’s Now Assist surpassed USD 1.5 billion in ARR, serving 8,800 clients that embed agents into HR and procurement flows. Yet integrating legacy ERPs, RPA platforms, and model APIs often demands custom middleware, driving services revenue as organizations seek end-to-end governance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevanc | Impact Timeline |

|---|---|---|---|

| Lack Of Standardized Human-AI Interaction Protocols | -3.8% | Global, cross-vendor integrations | Medium term (2-4 years) |

| Data-Privacy Concerns Limiting Cross-Team Data Sharing | -3.2% | Europe, United States, China | Short term (≤ 2 years) |

| High Upfront Integration And Training Costs | -2.7% | Global, SME impact in emerging markets | Short term (≤ 2 years) |

| Workforce Resistance From Job-Displacement Anxiety | -2.1% | Global, manufacturing and back-office functions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of Standardized Human-AI Interaction Protocols

No common protocol governs how agents receive instructions, ask clarifying questions, or escalate to humans. ISO/IEC 42001 outlines management systems but leaves technical hand-off details undefined. IEEE’s P7001 transparency standard remains voluntary and will not be finalized until 2027. Enterprises report that close to 40% of integration time is spent harmonizing authentication schemes, feedback loops, and audit logs across vendors. This fragmentation slows multi-agent adoption and increases switching costs, particularly inside regulated finance and healthcare environments that must document every decision path.

Data-Privacy Concerns Limiting Cross-Team Data Sharing

Strict regulations tighten controls on personal and commercially sensitive information that AI systems crave for nuanced recommendations. The EU AI Act demands comprehensive documentation of training data and will enforce transparency for high-risk systems starting August 2026.[2]European Data Protection Board, “GDPR Enforcement Tracker 2025,” edpb.europa.eu GDPR fines topped EUR 2.5 billion (USD 2.7 billion approximately) in 2025 for improper sharing with AI vendors. HIPAA and GLBA similarly constrain U.S. healthcare and banking datasets, while China’s Personal Information Protection Law requires local storage and government approvals for cross-border transfers, complicating global model versioning. Privacy-preserving techniques such as federated learning lessen compliance risk but can reduce model accuracy and increase latency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Hybrid Architectures Bridge Compliance and Latency Needs

Hybrid models are forecast to lead growth, advancing at a 38.97% CAGR from 2026-2031, as heavily regulated sectors process sensitive data on-premise while offloading non-critical inference to the cloud. Financial institutions using Azure Stack or Google Distributed Cloud keep customer PII within local jurisdiction while still using the latest transformer models for risk scoring. In manufacturing plants, edge nodes execute low-latency quality inspections while centralized servers refine models, demonstrating how a hybrid architecture solves both data sovereignty and millisecond response constraints.

Cloud deployments nonetheless sustained the largest 47.22% share of the human-AI collaborative work systems market in 2025 because pure SaaS minimizes upfront capital outlays and accelerates proof of value. On-premises remains relevant for defense and public-sector agencies that require air-gapped security. Vendors now bundle a single control plane spanning environments, easing observability and cost governance. The architectural flexibility widens the market for human-AI collaborative work systems, as late-majority adopters demand compliance without sacrificing performance.

By Component: Services Revenue Outpaces Software Licensing

While software captured 63.49% revenue in 2025, services will expand more quickly at a 40.37% CAGR as enterprises seek integration, custom workflow design, and periodic model re-tuning. Continuous audit obligations outlined in the EU AI Act and sectoral U.S. rules oblige organizations to refresh fairness and bias reports for each model iteration, a task often outsourced to systems integrators. By early 2026, Accenture had trained more than 40,000 consultants in generative AI to meet surging demand.

The human-AI collaborative work systems market for managed services is growing fastest among small and medium enterprises that lack in-house data scientists. Turnkey subscription bundles from monday.com or ClickUp wrap platform access with support, lowering entry barriers. Some vendors tie professional services to outcome-based pricing, aligning incentives around productivity lifts rather than hourly billing, a trend expected to reshape contracting norms across the human-AI collaborative work systems industry.

By End-User Industry: Healthcare Emerges as Fastest-Growing Vertical

IT and telecom dominated early spending with a 21.91% share in 2025, reflecting large installed software budgets and early experimentation with chat-based support tools. Yet clearer FDA guidance on AI-enabled devices propels healthcare to the highest 38.91% CAGR outlook. By end-2024, more than 950 approved algorithms will underpin use cases ranging from radiology triage to ambient clinical documentation. Google’s Med-PaLM 2 pilots achieved physician-level question-answering performance, prompting hospital administrators to invest in scribe agents that reduce burnout.

Manufacturers employ vision-language models for predictive maintenance, especially in automotive lines needing uninterrupted uptime. BFSI firms deploy conversational underwriting under strict explainability rules, whereas retail and e-commerce players embed large language models into demand forecasting engines to reduce stockouts. Education, government, and public sector trail due to budget and procurement complexity, but represent latent pools that could unlock new demand waves for the human-AI collaborative work systems market.

By Organization Size: Low-Code Tooling Unlocks SME Opportunities

Large enterprises are projected to retain 58.19% control of the human-AI collaborative work systems market share in 2025. This dominance is attributed to their substantial capital resources and extensive IT capabilities, which allow them to adopt and integrate advanced technologies seamlessly. However, small and medium-sized enterprises (SMEs) are expected to significantly narrow this gap. SMEs are expected to grow at a compound annual growth rate (CAGR) of 38.77%, nearly as fast as the overall market. This growth is driven by the adoption of visual builders that eliminate the need for extensive coding expertise, thereby lowering entry barriers for smaller firms. For instance, UiPath’s Clipboard AI facilitates automation by automatically generating workflows based on observed user actions. Similarly, Zoho’s Zia offers prompts in local languages, which helps reduce translation overheads, particularly benefiting businesses in emerging markets.

Despite this progress, SMEs face challenges such as data fragmentation and a lack of governance skills, which hinder their ability to fully leverage human-AI collaborative systems. To address these issues, governments are stepping in with supportive initiatives. For example, India has launched the USD 1.25 billion IndiaAI Mission, aimed at subsidizing infrastructure development and workforce skilling to accelerate AI adoption. In response to these challenges and opportunities, vendors are adapting their strategies. They are introducing consumption-based pricing models that minimize financial risks for SMEs and offering template libraries tailored to specific industry workflows. These measures are making the human-AI collaborative work systems industry more accessible to firms with limited technical expertise, enabling broader participation and fostering growth across the market.

Geography Analysis

North America retained 34.57% revenue in 2025, anchored by hyperscaler capex and early experimentation across software, telecom, and professional services. Microsoft invested USD 37.5 billion in AI-optimized data centers that now underpin Azure OpenAI Service, while Salesforce saw 70% of Agentforce pilots originate from U.S. customers, reflecting a culture of rapid technology trials. Nonetheless, litigation under HIPAA and GLBA prolongs deployment timelines in healthcare and banking as risk officers scrutinize data flow.

Asia-Pacific is projected to be the most dynamic region, registering a 39.57% CAGR. China’s CNY 1 trillion (USD 138.9 billion approximately) national AI program funds domestic model development by Baidu, Alibaba, and Tencent, emphasizing Mandarin fluency and local domain adaptation. India’s thriving IT services sector embeds AI to raise billable efficiency, supported by government subsidies and a vast English-speaking talent pool.[3]Government of India, “Press Release on IndiaAI Mission,” pib.gov.in Japan and South Korea focus on manufacturing and semiconductor design to offset aging demographics and global supply-chain shifts. However, stringent data-sovereignty laws force multinational companies to maintain parallel instances, inflating operating costs.

Europe balances innovation with strict compliance. The EU AI Act’s transparency mandates lengthen procurement cycles yet create opportunities for governance specialists. Germany leads industrial adoption, particularly in automotive predictive maintenance, whereas the United Kingdom leverages its AI Safety Institute for pre-deployment testing that reassures corporate boards. Cloud region build-outs in Brazil, the United Arab Emirates, and South Africa are gradually pulling Latin America and the Middle East, and Africa into the human-AI collaborative work systems market, though spending remains concentrated in multinational subsidiaries.

Competitive Landscape

The human-AI collaborative work systems market is moderately fragmented, with key players leveraging their existing strengths to maintain a competitive edge. Hyperscalers such as Microsoft, Google, and IBM integrate generative AI capabilities into their productivity and cloud subscription offerings, capitalizing on their extensive distribution networks to secure market dominance. For instance, Microsoft Copilot, with its 15 million seats, provides a significant opportunity for upselling once integration challenges are reduced to acceptable levels. Similarly, Salesforce differentiates itself by offering customer and procurement agents that deliver measurable return-on-investment metrics, such as reducing case or sourcing cycle times by up to 50%. These strategies highlight the competitive dynamics within the market as companies strive to enhance their value propositions.

Robotic process automation (RPA) leaders like UiPath and Automation Anywhere are shifting their focus toward natural-language orchestration to address increasing platform overlap from competitors such as ServiceNow and Atlassian. UiPath’s robust developer ecosystem, comprising 1.7 million developers, plays a critical role in fostering community-built templates that accelerate time-to-production, creating a strong competitive advantage in the human-AI collaborative work systems market.[4]UiPath Inc., “Annual Report 2025,” uipath.com Meanwhile, Adobe leverages its dominance in the Creative Cloud space to integrate Firefly into creative workflows, effectively capturing marketing budgets that are being reallocated from traditional agencies. These moves underscore the importance of innovation and ecosystem development in maintaining relevance and driving growth in this evolving market.

Compliance tools are emerging as a key differentiator in the market, particularly for vendors targeting highly regulated industries such as finance and life sciences. Companies that can bundle ISO/IEC 42001-aligned management dashboards and EU AI Act audit reports are more likely to win procurement contracts in these sectors. Additionally, new entrants are focusing on niche areas such as domain-specific knowledge graphs, agent safety checkers, and lightweight on-device models designed for frontline workers. However, these newcomers face significant challenges, including building trust and overcoming integration barriers, which remain critical hurdles to their success. As the market continues to evolve, the ability to address these challenges while meeting the specific needs of target industries will determine the long-term viability of these players.

Human-AI Collaborative Work Systems Industry Leaders

Microsoft Corporation

Google LLC

IBM Corporation

Salesforce, Inc.

OpenAI, L.L.C

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Microsoft reported that Azure OpenAI Service surpassed 70,000 enterprise customers and Copilot for Microsoft 365 hit 15 million paid seats, up 25% quarter-on-quarter.

- February 2026: Salesforce added autonomous procurement agents to Agentforce, with pilots citing 40-60% shorter sourcing cycles.

- January 2026: UiPath launched Autopilot for Testing, automating test-case generation and defect triage for faster software releases.

- December 2025: Google confirmed Gemini reached 750 million monthly active users, with regulated-industry clients adopting on-premises versions.

Global Human-AI Collaborative Work Systems Market Report Scope

The Human-AI Collaborative Work Systems Market refers to the global ecosystem of technologies, platforms, and services designed to enable joint task execution, decision-making, and workflow optimization between human workers and artificial intelligence (AI) systems. These systems are built on the principle of augmentation, where AI enhances human capabilities rather than replacing them, by combining human judgment, creativity, and contextual understanding with AI-driven data processing, automation, and predictive analytics.

The Human-AI Collaborative Work Systems Market Report is Segmented by Deployment Mode (On-Premise, Cloud, and Hybrid), Component (Software, and Services), End-User Industry (IT and Telecom, Healthcare and Life Sciences, Manufacturing, BFSI, Retail and E-commerce, Education, Government and Public Sector, and Other End-user Industries), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| On-Premise |

| Cloud |

| Hybrid |

| Software |

| Services |

| IT and Telecom |

| Healthcare and Life Sciences |

| Manufacturing |

| BFSI |

| Retail and E-commerce |

| Education |

| Government and Public Sector |

| Other End-user Industries |

| Large Enterprises |

| Small and Medium Enterprises |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Deployment Mode | On-Premise | ||

| Cloud | |||

| Hybrid | |||

| By Component | Software | ||

| Services | |||

| By End-User Industry | IT and Telecom | ||

| Healthcare and Life Sciences | |||

| Manufacturing | |||

| BFSI | |||

| Retail and E-commerce | |||

| Education | |||

| Government and Public Sector | |||

| Other End-user Industries | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the human-AI collaborative work systems market by 2031?

It is expected to reach USD 23.28 billion, expanding from USD 4.59 billion in 2026 at a 38.37% CAGR.

Which deployment mode is growing fastest?

Hybrid architectures show the quickest rise, forecast to grow at 38.97% CAGR as firms balance compliance with real-time AI inference.

Why is healthcare the fastest-growing vertical?

FDA guidance on AI medical devices and rising clinician-burnout mitigation efforts are driving a 38.91% CAGR for healthcare and life sciences.

How are small and medium enterprises adopting these systems?

Low-code and no-code tools, subscription bundles, and government incentives allow SMEs to integrate AI agents without large data-science teams, supporting a 38.77% CAGR.

What are the main barriers to adoption?

Lack of standardized interaction protocols and stringent data-privacy laws increase integration effort and slow cross-team data sharing.

Which region will lead growth through 2031?

Asia-Pacific is projected to post the highest 39.57% CAGR, buoyed by large-scale national AI investments in China, India, Japan, and South Korea.

Page last updated on: