Agentic AI In HCM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.56 Billion |

| Market Size (2031) | USD 13.48 Billion |

| Growth Rate (2026 - 2031) | 24.21% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agentic AI In HCM Market Analysis by Mordor Intelligence

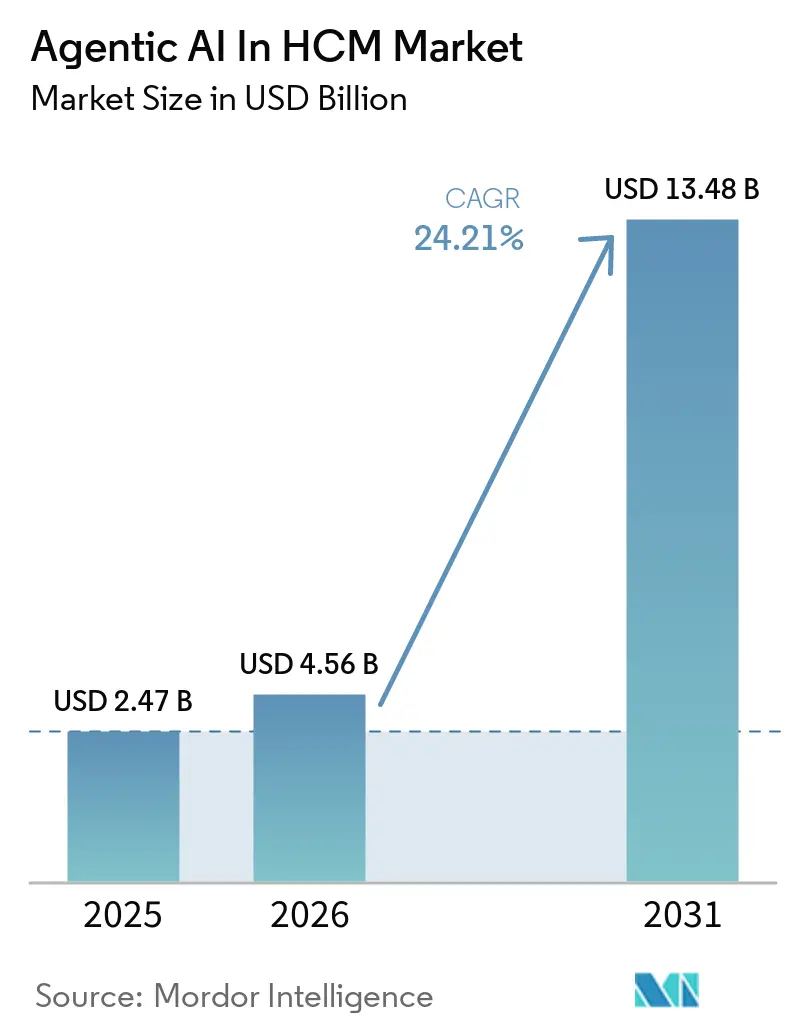

The agentic AI in the HCM market size is expected to grow from USD 2.47 billion in 2025 to USD 4.56 billion in 2026 and is forecast to reach USD 13.48 billion by 2031 at 24.21% CAGR over 2026-2031. This rapid expansion reflects a clear shift from limited copilots to agent networks that can manage connected HR tasks across sourcing, service delivery, payroll review, and mobility decisions. Enterprise buyers are treating these systems as operating infrastructure because labor scarcity, productivity pressure, and rising service expectations now affect both hiring and ongoing workforce administration. Adoption is also being shaped by the need to connect fragmented ATS, HRIS, payroll, helpdesk, and collaboration systems so that HR workflows can move with less manual intervention. At the same time, platform vendors are accelerating native product releases, while specialized providers are competing through deeper use case coverage and integration flexibility. The main constraint remains compliance complexity, since organizations must balance automation gains with tighter rules on privacy, oversight, explainability, and cross-border data handling.

Key Report Takeaways

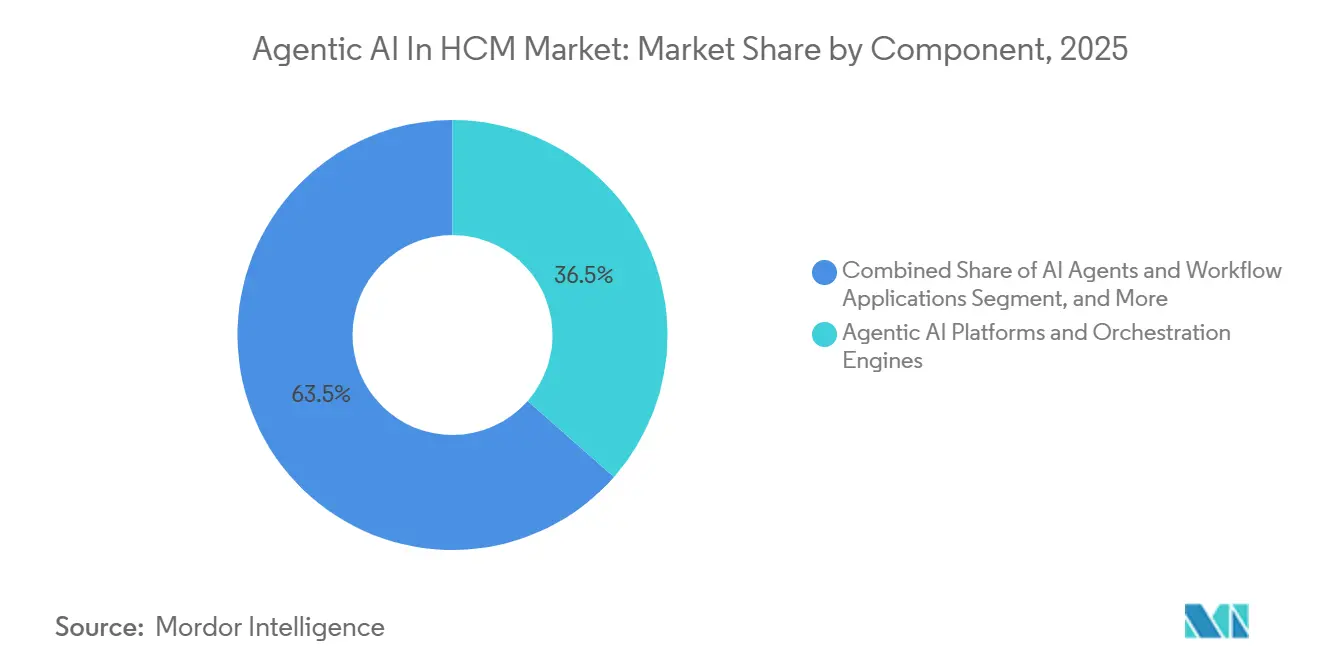

- By component, agentic AI platforms and orchestration engines led with a 36.47% share in Agentic AI in the HCM Market in 2025, while AI agents and workflow applications are projected to expand at a 27.39% CAGR through 2031.

- By function, workforce planning and analytics accounted for 22.83% of the share in 2025, while talent management and internal mobility are projected to advance at a 25.41% CAGR through 2031.

- By deployment model, cloud-based deployment held 71.29% of the agentic AI market share in HCM in 2025, while hybrid deployment is projected to grow at a 26.17% CAGR through 2031.

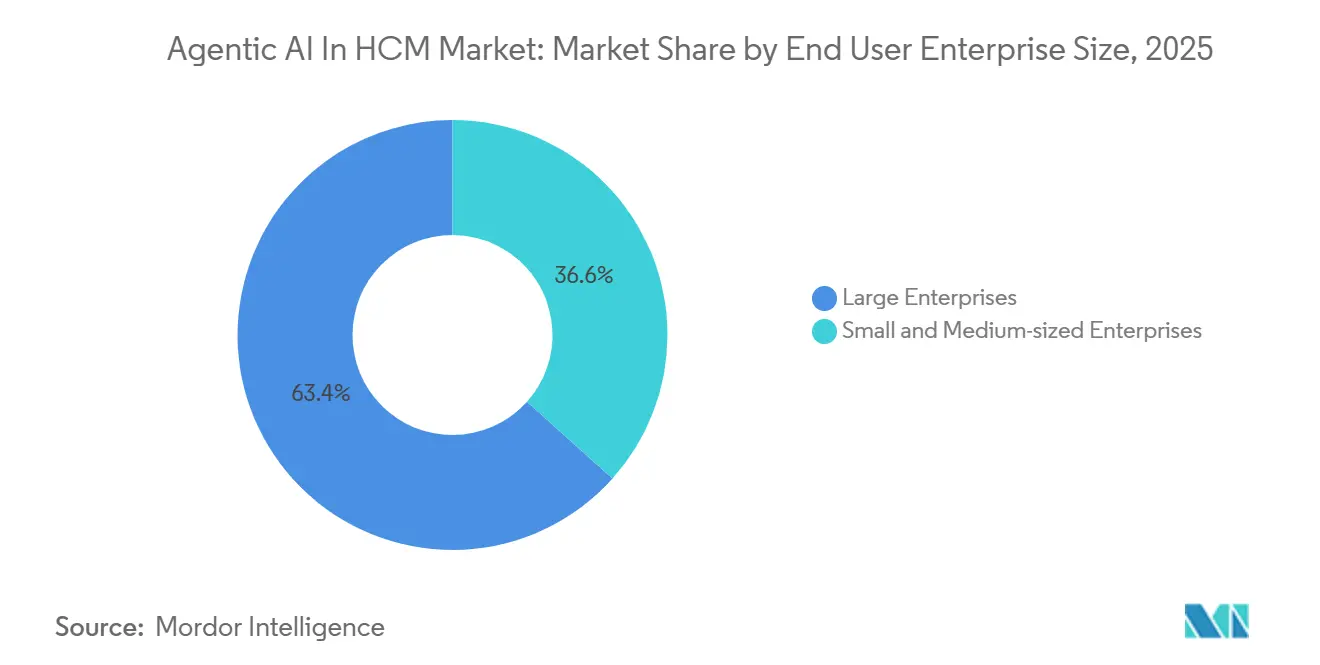

- By end-user enterprise size, large enterprises held 63.37% of the agentic AI market share in HCM in 2025, while SMEs are projected to expand at a 28.43% CAGR through 2031.

- By end user industry, information technology and telecom held 24.91% share in 2025, while healthcare and life sciences are projected to grow at 26.89% CAGR through 2031

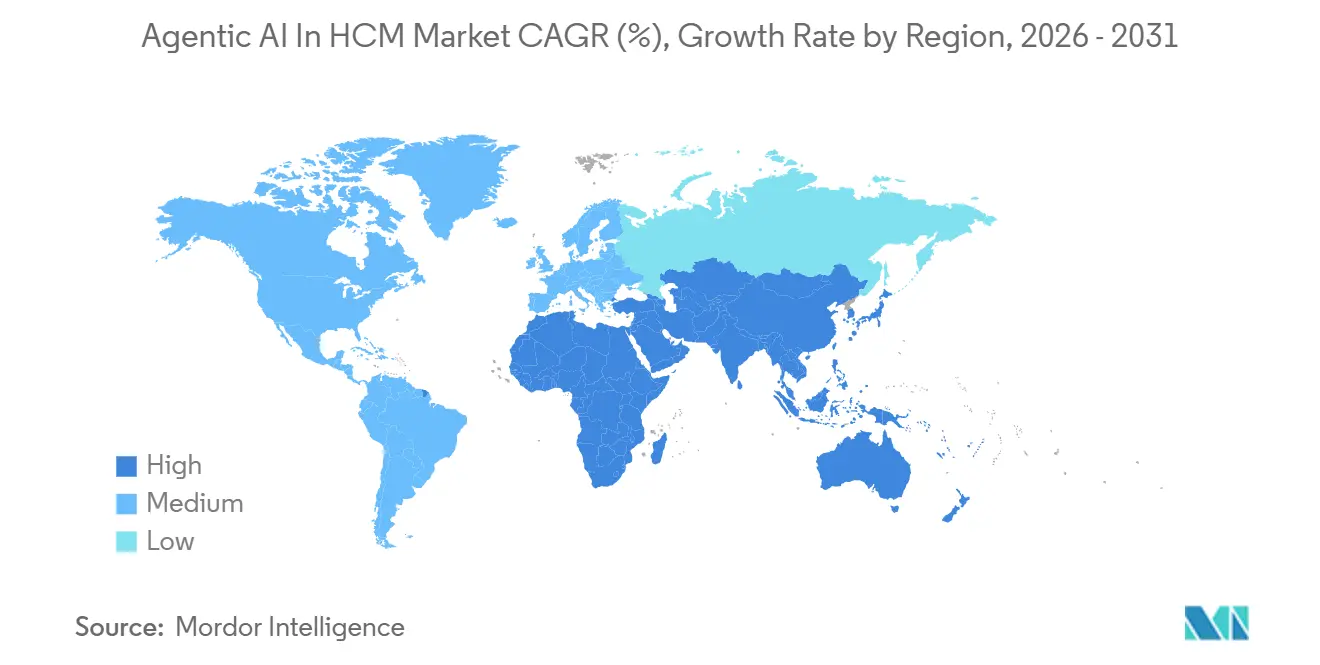

- By geography, North America held 39.73% of the global agentic AI in the HCM market in 2025, while Asia-Pacific is projected to expand at 29.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agentic AI In HCM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Labor Scarcity in High-Skill and Frontline Hiring | 5.8% | Global, most acute in North America and Western Europe | Short term (= 2 years) |

| Enterprise Pressure to Lift Recruiter and Manager Productivity Without Adding Headcount | 4.9% | North America and Europe | Short term (= 2 years) |

| Demand for Always-on Employee Self-service and HR Case Deflection | 4.2% | Global | Medium term (2-4 years) |

| Shift Toward Skills-Based Talent Decisions and Internal Mobility | 3.7% | North America, Europe, and Australia | Medium term (2-4 years) |

| Need to Orchestrate Work Across Fragmented ATS, HRIS, Helpdesk, and Collaboration Stacks | 2.8% | Global, strongest in large enterprises across APAC and North America | Medium term (2-4 years) |

| Emergence of Agent Governance Layers That Make Multi-agent HR Automation Auditable | 2.1% | North America and Europe | Long term (= 4 years) |

| Source: Mordor Intelligence | |||

Rising Labor Scarcity in High-Skill and Frontline Hiring

Persistent labor scarcity is pushing the agentic AI in the HCM market toward faster adoption because manual recruiting teams cannot keep pace with the volume and speed now required across frontline and specialized roles. U.S. JOLTS data showed 7.4 million job openings in December 2025, with openings-to-hire ratios in healthcare, manufacturing, and logistics still above pre-pandemic norms, signaling sustained hiring pressure rather than a short-term disruption.[1]Nick Bunker, “December 2025 JOLTS Report: Balance or Breaking Point?,” Indeed Hiring Lab, hiringlab.org Companies also reported that unfilled U.S. vacancies stood at 4.5% of total labor demand in February 2025, while the hiring rate fell to a decade-low of 3.3% in December 2025, pointing to a structural mismatch in labor supply. This pressure matters because frontline employees account for a large share of the global workforce, and replacement costs per worker still range from USD 3,000 to USD 5,000 before productivity losses are counted. iCIMS reported in March 2026 that customers using Frontline AI achieved up to 75% lower time-to-fill and up to 10 times more hires per recruiter, which strengthens the business case for conversational sourcing agents in high-volume roles. The longer-term pull on the agentic AI in the HCM market is reinforced by demographic decline in working-age populations across mature economies, which makes faster hiring capacity more important to workforce continuity.

Enterprise Pressure to Lift Recruiter and Manager Productivity Without Adding Headcount

The agentic AI in the HCM market is also being driven by tighter cost discipline, since HR teams are being asked to improve output without expanding headcount. BCG reported in February 2026 that organizations applying AI in targeted HR workflows recorded 20-30% efficiency gains, and a GPT-based manager review tool cut review-writing time by 45% while improving review quality by 22% with 90% user satisfaction. Payroll administration places the same pressure on finances, with research indicating that employers lose 2-4% of total labor spend to payroll leakage, and that even a 1% loss can equal USD 15 million annually for a large employer. IBM’s AskHR program showed that when agentic support is built on standardized workflows, HR teams can centralize service through a single entry point while reaching a 94% containment rate and cutting HR operating costs by 40% over 4 years. That model matters because McKinsey found in 2025 that only 18% of organizations with more than 1,000 employees used specialized HR shared services centers, leaving a significant process gap for software-led productivity gains. As a result, the agentic AI in the HCM market is increasingly tied to measurable labor efficiency rather than experimental automation budgets.

Demand for Always-on Employee Self-service and HR Case Deflection

The agentic AI in the HCM market is benefiting from a shift in employee expectations, as workers now expect HR support to be available at the same speed and with the same continuity they see in consumer software. SAP cited research in May 2026 showing that 62% of C-suite leaders were dissatisfied with how people data connected to business performance, which supports the demand for agents who can resolve requests while leveraging broader organizational context.[2]Dan Beck, “SAP SuccessFactors Innovations Define a New Era of Autonomous HCM,” SAP News Center, news.sap.com Salesforce reported that employee interactions with AI agents increased by an average of 65% per month in the first half of 2025, while agent actions generated from those conversations rose 76% per month across early enterprise deployments.[3]Salesforce, “Salesforce Shares Agentic Enterprise Index Insights for H1 2025,” Salesforce, salesforce.com These usage trends support greater spending on agentic AI in the HCM market, as self-service can absorb routine demand that would otherwise require growing case management teams. At the same time, quality control still matters because poor process design can scale incorrect resolutions in areas such as leave, benefits, and policy interpretation. Oracle addressed that concern in April 2026 by embedding My Help Workspace for Employees within its Fusion environment so that agents can operate closer to transactional records, policies, and approval paths.

Shift Toward Skills-Based Talent Decisions and Internal Mobility

The agentic AI in HCM market is being strengthened by the move from credential-led hiring to skills-led workforce decisions, especially where companies need to redeploy talent faster than they can recruit externally. Demand for AI fluency in U.S. job postings grew nearly 7 times in 2 years through mid-2025, while demand for AI-related skills rose from 2.2 million to 7.5 million occupied roles between 2023 and 2025. This supports broader use of matching, career pathing, and skills inference tools inside the agentic AI in HCM market because companies need better visibility into workforce capabilities than static job titles can provide. In June 2025, Merck KGaA’s AI-enabled internal mobility program led 41,000 of 63,000 employees to create accounts on its talent marketplace, cut average interview scheduling time by 70%, and reduced sourcing time for hired candidates by more than 4 days. These results are helping position the agentic AI in HCM market as a tool for workforce allocation and retention, not only for candidate acquisition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy, Cross-border Data Transfer, and AI Governance Burden | -3.2% | Global, most pronounced in the EU and APAC | Long term (= 4 years) |

| Integration Complexity Across Legacy HCM, Payroll, and Identity Systems | -2.6% | Global | Medium term (2-4 years) |

| Works Council and Employee Relations Pushback Against Autonomous HR Decisions | -1.8% | Europe, particularly Germany and France | Medium term (2-4 years) |

| Weak Process Standardization That Limits Agent Reliability in Mid-market Deployments | -1.4% | Global, disproportionate in South America and Africa | Long term (= 4 years) |

| Source: Mordor Intelligence | |||

Data Privacy, Cross-Border Data Transfer, And AI Governance Burden

Compliance remains the clearest drag on the agentic AI in the HCM market because HR decisions touch highly sensitive data and often fall into higher-risk regulatory categories. The EU AI Act, Regulation (EU) 2024/1689, entered into force on August 1, 2024, and classified recruitment screening, candidate ranking, performance monitoring, and task allocation systems as high risk under Annex III.[4]European Parliament and Council of the European Union, “Regulation (EU) 2024/1689 of the European Parliament and of the Council of 13 June 2024 Laying Down Harmonised Rules on Artificial Intelligence,” Publications Office of the European Union, europa.eu The framework requires conformity assessments, use-log retention, impact reviews, and worker-representative consultation, which increase costs and slow deployment of agentic AI in the HCM market. In the United Kingdom, the Information Commissioner’s Office said in March 2026 that AI hiring tools without genuine human review can breach legal standards, and it warned that simple rubber-stamping does not qualify as meaningful oversight. Research in January 2026 showed that 77% of U.S. leaders cited data privacy as a top enterprise risk in the fourth quarter of 2025, up from 53% at the start of the year, which shows how governance concerns now shape buying criteria as much as functionality. This means the agentic AI in the HCM market will continue to expand, but vendors will need stronger localization, auditability, and oversight features to convert demand into deployed revenue.

Integration Complexity Across Legacy HCM, Payroll, And Identity Systems

Integration complexity is another major restraint, as the agentic AI in the HCM market depends on clean, continuous data across systems that were often built in different eras and by different vendors. Organizations with clear job architecture, stronger skills data, and standardized workflows achieve better outcomes when deploying AI agents than those that implement automation on top of unstable foundations. Only about 30% of enterprises had integrated skills data into workforce planning in 2025, which shows that many still lack the structure needed for reliable agent decisions. Release cycles from major vendors have acknowledged that semantic search and advanced HR data connectivity require a strong engineering discipline and ongoing monitoring, which entail costs and technical effort that many mid-market buyers may underestimate. Expanding partner and external agent access around standardized business-process controls shows that platform interoperability is becoming a central design issue rather than a secondary integration task. Until more organizations modernize payroll, identity, and workforce data layers, the agentic AI in the HCM market will continue to face slower deployment cycles in complex installed bases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Orchestration Engines Anchor The Foundation And AI Agents Define The Growth Layer

Agentic AI platforms and orchestration engines accounted for 36.47% of the component segment in 2025, making them the largest component category in the agentic AI in HCM market. This leadership reflected the enterprise's preference to secure governance, routing, policy control, and escalation logic before expanding the number of live agents. These platforms gave buyers a way to manage task decomposition, human checkpoints, and identity control across recruiting, HR service, payroll, and mobility workflows. That foundation mattered because many deployments in 2025 and 2026 focused first on reducing execution risk rather than maximizing agent volume. The component mix, therefore, showed that infrastructure confidence came before broader expansion of use cases in the agentic AI market in the HCM market.

AI agents and workflow applications are projected to grow at a 27.39% CAGR from 2026 to 2031, making them the fastest-growing component segment. This phase marks the next step for agentic AI in the HCM market, where enterprises that built orchestration capacity in 2024 and 2025 are now filling it with task-specific agents for interviewing, policy navigation, payroll exception review, and internal mobility. Research in February 2026 showed that staffing firms using AI were 4 times more likely to outperform peers, while 55% said AI screening improved KPIs by more than 25%, and 46% achieved a 50% or greater reduction in screening time. Services remain relevant because large, multi-system deployments still require implementation support, workflow redesign, and ongoing tuning. Managed AI services are also gaining traction, as buyers want the benefits of agentic AI in the HCM industry without building deep internal AI operations teams. This leaves the component structure with a clear pattern where platforms establish control, applications drive scaling, and services support long-tail deployment complexity.

By Function: Analytics Anchors Spend While Talent Mobility Drives The Next Phase

Workforce planning and analytics accounted for 22.83% of the market in 2025, making it the largest functional segment in the agentic AI HCM market. That position reflected the need for real-time labor allocation, budget visibility, and scenario planning amid tight hiring conditions and changing skill demand. The agentic AI in the HCM market size in this function benefited from executive demand for tools that connect workforce decisions more directly to financial outcomes. Only 12% of U.S. HR leaders engaged in workforce planning with a 3-year or longer horizon, while 73% remained focused solely on operational planning. AI-driven workforce planning launched in 2026 to link headcount and labor decisions to ERP and contingent workforce data, supporting stronger demand for analytics-centered automation. In practice, this function became the control room for the agentic AI in the HCM market rather than a reporting add-on.

Talent management and internal mobility are projected to expand at 25.41% CAGR from 2026 to 2031, making it the fastest-growing function. This rise shows that the agentic AI in the HCM market is moving closer to workforce redeployment and retention goals, rather than just external hiring efficiency. Recruiting and candidate sourcing still account for a large share of the deployment volume, especially in frontline roles where speed and application completion matter. Conversational ATS deployments delivered a 72% average application completion rate, 3.5-day average time-to-hire, and 95% candidate satisfaction rating in 2025. Employee service and HR operations are also improving through higher case containment, while payroll and time administration remain more tightly controlled due to a low tolerance for error. Across the agentic AI in the HCM industry, the function mix shows that buyers are broadening spend from efficiency-led workflows toward workforce value creation.

By Deployment Model: Cloud Commands Share While Hybrid Gains Relevance In Regulated Environments

Cloud-based deployment retained a 71.29% share in 2025, making it the dominant deployment model in the agentic AI HCM market. This was supported by the API-led structure of newer platforms and by subscription models that allow enterprises to scale use more flexibly across business units and workflows. The cloud model also aligns with the fast release cycles vendors used in 2025 and 2026 to add new agents, copilots, and orchestration features. Research in September 2025 showed that 88% of organizations had increased generative AI investment over the prior 12 months and that 12% of total IT budgets were dedicated to generative AI, supporting the wider shift toward cloud-hosted AI infrastructure. In this setting, cloud remained the default operating model for the agentic AI in the HCM market because it reduced deployment friction and aligned with vendor commercial strategies.

Hybrid deployment is projected to grow at a 26.17% CAGR from 2026 to 2031, making it the fastest-growing model. That growth reflects a more selective architecture in the agentic AI in the HCM market, especially where organizations want cloud reasoning layers but must keep payroll, identity, or employee records closer to sovereign or on-premises environments. Financial services, healthcare, and public sector buyers are central to this shift because regulatory and resilience obligations remain stricter in those settings. In May 2025, a proprietary Model Context Protocol server was launched to enable compatible agents to interact securely with HR workflows across connected enterprise systems. On-premises models still retain a role in industrial and government environments with long modernization cycles. The result is a more layered deployment pattern where cloud leads in scale, but hybrid is becoming the architecture of choice, with compliance and system control carrying more weight.

By End User Enterprise Size: Large Enterprises Lead Current Spend While SMEs Set The Growth Pace

Large enterprises held a 63.37% share in 2025, giving them a commanding role in the agentic AI market for HCM. Their lead came from the very complexity that creates value for orchestration, including multi-country payroll, multiple HR platforms, layered approval paths, and large internal service volumes. Half of executives at organizations with annual revenue of more than USD 1 billion planned to allocate USD 10-50 million in 2026 toward agentic architectures, data lineage, and model governance. Large enterprises also faced greater pressure to standardize governance because a single weak decision path can affect thousands of employees or candidates. This made them the earliest buyers of broader orchestration and policy-control layers in the agentic AI market for HCM

SMEs are projected to grow at a 28.43% CAGR from 2026 to 2031, making them the fastest-growing segment of the enterprise market. This shows that the agentic AI in the HCM market is beginning to move beyond global enterprises into more accessible cloud packages and preconfigured workflows. In 2026, Canadian SMEs were using AI for hiring at rates comparable with peers in Japan and the United Kingdom, and the tools reduced hiring timelines by an average of 10 days without requiring dedicated HR technology teams. Growth in this segment is supported by vendors that package agentic capabilities inside unified platforms rather than requiring buyers to assemble multi-vendor stacks. It is also helped by lower implementation requirements than in older HCM transformation projects. Even so, the agentic AI in the HCM industry will still see slower SME penetration, as process discipline, data quality, and compliance readiness remain weak.

By End User Industry: IT And Telecom Sets The Benchmark While Healthcare And Life Sciences Accelerates

Information technology and telecom held a 24.91% share in 2025, making it the largest industry segment in the agentic AI in the HCM market. The sector benefited from richer workforce data, better-established skills taxonomies, and stronger tolerance for algorithm-assisted talent decisions. Many of its use cases already matched the strengths of agentic systems, including skills-based sourcing, project staffing, coding assessment, and internal redeployment. This gave the sector a quality advantage because cleaner data improves model reliability and lowers deployment friction. As a result, IT and telecom became the main benchmarks for how agentic AI in the HCM market can scale in structured talent environments.

The healthcare and life sciences industry is projected to grow at a 26.89% CAGR from 2026 to 2031, making it the fastest-growing industry segment. Estimates in 2025 suggested that the global clinical workforce shortage would reach at least 10 million workers by 2030, which gives the sector a strong need for faster and more auditable hiring and staffing decisions. Workforce planning analysis also identified healthcare as a major use area for staff certification management and real-time staffing decisions linked to patient load variables. Retail and e-commerce remain important for high-volume frontline recruitment, while BFSI places stronger weight on explainability and decision logging. The government and public sector are earlier in deployment, but readiness is improving, with security and compliance certifications reducing adoption barriers. This means the agentic AI in the HCM market is expanding across industries at different speeds, with data quality, labor pressure, and regulatory intensity shaping the order of adoption.

Geography Analysis

North America held a 39.73% share of the global agentic AI market in the HCM market in 2025, making it the leading regional cluster. The United States anchored this position through a mature HCM software ecosystem, deep enterprise cloud adoption, and a stronger willingness to fund AI programs at scale. Unfilled U.S. job vacancies stood at 4.5% of total labor demand in February 2025, which continued to put pressure on hiring efficiency and supported demand for AI-led sourcing and screening. In January 2026, 64% of U.S. organizations had changed their approach to entry-level hiring due to AI agent influence, up from 18% in the prior quarter, signaling rapid normalization of AI-assisted recruiting practices. The region is also defining procurement standards because buyers now evaluate governance, explainability, and ROI together rather than treating compliance as a later-stage issue.

Visible enterprise commitments support the North American lead. In March 2026, Adecco Group signed an unlimited, multi-year Agentforce 360 agreement with Salesforce to power more than 50% of revenues with agentic AI across 27,000 recruiters in more than 60 countries by the end of 2026. Early United Kingdom pilots had already produced 15% time savings. At the same time, state-level employment AI rules in the United States are expanding, which means the agentic AI in the HCM market share gained in North America will increasingly depend on vendor readiness for notification, impact review, and anti-discrimination controls. Canada remains smaller in scale, but it is moving steadily as SME hiring adoption improves. Mexico is also part of the broader regional opportunity, though enterprise depth remains lower than in the United States.

Europe remained the second-largest region in the agentic AI in the HCM market, but it operates under the most demanding governance conditions. The EU AI Act has raised the compliance floor across recruitment, performance, and workforce allocation systems, meaning deployment speed is often slower, but governance quality is higher. The United Kingdom is moving on its own track, and in March 2026, the Information Commissioner’s Office said that AI-supported hiring decisions still require genuine human oversight rather than formal approval without the authority to intervene. Europe also shows a significant skills gap, with only 21% of European employees having received generative AI training, compared with 45% in the United States, underscoring the need for continued investment in productivity-oriented HR AI tools. Asia-Pacific is projected to grow at a 29.11% CAGR from 2026 to 2031, making it the fastest-growing regional segment of the agentic AI in the HCM market. Southeast Asia is strengthening through higher HR AI usage and budget intent, while India, Japan, and China each add demand through different combinations of labor pressure, technology investment, and enterprise modernization. South America, the Middle East, and Africa remain early-stage opportunities, but large enterprise bases, cloud HCM modernization, and national digital programs are gradually expanding the addressable base for agentic AI in the HCM market.

Competitive Landscape

The agentic AI in the HCM market is structured into 2 broad competitive groups: established HCM suite providers that are embedding agents into existing platforms, and specialist vendors that are building deeper use-case coverage on top of talent intelligence or workflow automation. In 2026, incumbent providers strengthened their position by launching large-scale agentic initiatives across payroll, recruiting, onboarding, and HR service management. These moves matter because incumbent vendors already control core records, workflows, and security models, which gives them a natural path to embed agentic functionality inside trusted environments. That advantage helps explain why the agentic AI in the HCM market is not developing as a standalone software layer in every case.

Specialists are responding by focusing on depth, interoperability, and workflow precision. Several acquisitions in 2026 expanded coverage across psychometrics, cognitive assessment, and applied hiring intelligence. New platforms were introduced to enable enterprises to build custom HR software on top of talent intelligence and agentic workflow foundations, paired with readiness tools to monitor real-time AI adoption across the workforce. Integration-first approaches also emerged, extending agentic HR platforms into productivity suites such as Microsoft 365 and Teams, enabling deployment across existing HCM environments rather than requiring replacement. This creates a market split in which some vendors compete through platform control, while others compete through cross-platform relevance. In the agentic AI market for HCM, that split is likely to persist because many buyers want new capabilities without reopening full-platform replacement decisions.

Another feature of the agentic AI in the HCM market is that the commercial and technical architectures are changing together. Vendors are moving away from purely seat-based pricing and are placing more weight on usage, orchestration, and embedded workflow value, which changes how buyers assess total cost over time. Governance is also becoming a competitive feature rather than a background requirement, especially in sectors where audit trails, human oversight, and secure data flow influence vendor selection. This favors providers that can combine automation with clear control points and established enterprise integrations. It also leaves room for newer entrants in mid-market and multi-vendor settings where a large suite transformation is too costly or too slow. Overall, the agentic AI in the HCM market remains competitive and fragmented, with no evidence in the supplied material that a single vendor or small group has already secured dominant control across the full value chain.

Agentic AI In HCM Industry Leaders

Phenom People, Inc.

Eightfold AI Inc.

iCIMS, Inc.

Paradox, Inc.

Beamery Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Eightfold AI launched TalentForge for custom HR software, a Workforce Readiness Platform to track AI adoption, and a 360 Interview combining multiple assessments on a certified framework.

- May 2026: SAP SuccessFactors rolled out Autonomous HCM with Joule Assistants and AI workforce planning, naming Anthropic as a partner in its largest AI launch.

- May 2026: UKG introduced UKG Pro Pay with Workforce AI to cut payroll time and address leakage, reporting USD 4.31 Billion revenue and serving 80K+ organizations.

- May 2026: Eightfold AI embedded Agentic Interviewing into Oracle Fusion Recruiting to scale candidate assessment and speed hiring.

Global Agentic AI In HCM Market Report Scope

The agentic AI in the HCM market refers to advanced platforms and services that leverage autonomous AI agents and orchestration engines to transform HR operations and workforce management. These solutions automate recruiting, employee services, talent mobility, learning, workforce planning, payroll, and compliance by embedding intelligent workflows across enterprise systems. Offered through cloud, on-premises, and hybrid models, agentic AI in HCM serves both large enterprises and SMEs across industries such as BFSI, healthcare, IT and telecom, retail, manufacturing, government, and others. The market’s core purpose is to enable organizations to optimize employee experience, productivity, and strategic HR decision-making by integrating adaptive, AI-driven intelligence into the full employee lifecycle.

The agentic AI in HCM market report is segmented by Component (Agentic AI Platforms and Orchestration Engines, AI Agents and Workflow Applications, Professional Services, and Managed AI Services), Function (Recruiting and Candidate Sourcing, Employee Service and HR Operations, Talent Management and Internal Mobility, Learning and Development, Workforce Planning and Analytics, Payroll and Time Administration), Deployment Model (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises and Small and Medium-sized Enterprises), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, and Government and Public Sector), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Agentic AI Platforms and Orchestration Engines |

| AI Agents and Workflow Applications |

| Professional Services |

| Managed AI Services |

| Recruiting and Candidate Sourcing |

| Employee Service and HR Operations |

| Talent Management and Internal Mobility |

| Learning and Development |

| Workforce Planning and Analytics |

| Payroll and Time Administration |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Agentic AI Platforms and Orchestration Engines | |

| AI Agents and Workflow Applications | ||

| Professional Services | ||

| Managed AI Services | ||

| By Function | Recruiting and Candidate Sourcing | |

| Employee Service and HR Operations | ||

| Talent Management and Internal Mobility | ||

| Learning and Development | ||

| Workforce Planning and Analytics | ||

| Payroll and Time Administration | ||

| By Deployment Model | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By End User Enterprise Size | Large Enterprises | |

| Small and Medium-sized Enterprises | ||

| By End User Industry | BFSI | |

| Healthcare and Life Sciences | ||

| Information Technology and Telecom | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the size outlook for agentic AI in HCM market through 2031?

The agentic AI in HCM market was valued at USD 2.47 billion in 2025, rose to USD 4.56 billion in 2026, and is forecast to reach USD 13.48 billion by 2031 at a 24.21% CAGR.

Which region leads adoption and which region is growing the fastest?

North America led with 39.73% share in 2025, while Asia-Pacific is projected to record the fastest growth at 29.11% CAGR through 2031.

Which component category currently leads spending?

Agentic AI platforms and orchestration engines held the largest component share at 36.47% in 2025 because enterprises first prioritized governance, routing, and control layers.

Which HR function is expanding the fastest?

Talent management and internal mobility is projected to grow at 25.41% CAGR through 2031, while workforce planning and analytics remained the largest function in 2025 with 22.83% share.

Why are enterprises investing in these tools now?

Labor scarcity, recruiter productivity pressure, demand for always-on employee self-service, and stronger interest in skills-based hiring and internal mobility are the main demand drivers.

What is the biggest risk to wider rollout?

Compliance and integration remain the main barriers, especially around privacy, cross-border data rules, AI governance, and the technical challenge of connecting legacy HCM, payroll, and identity systems.

Page last updated on: