Agentic AI For Sustainability Operations Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

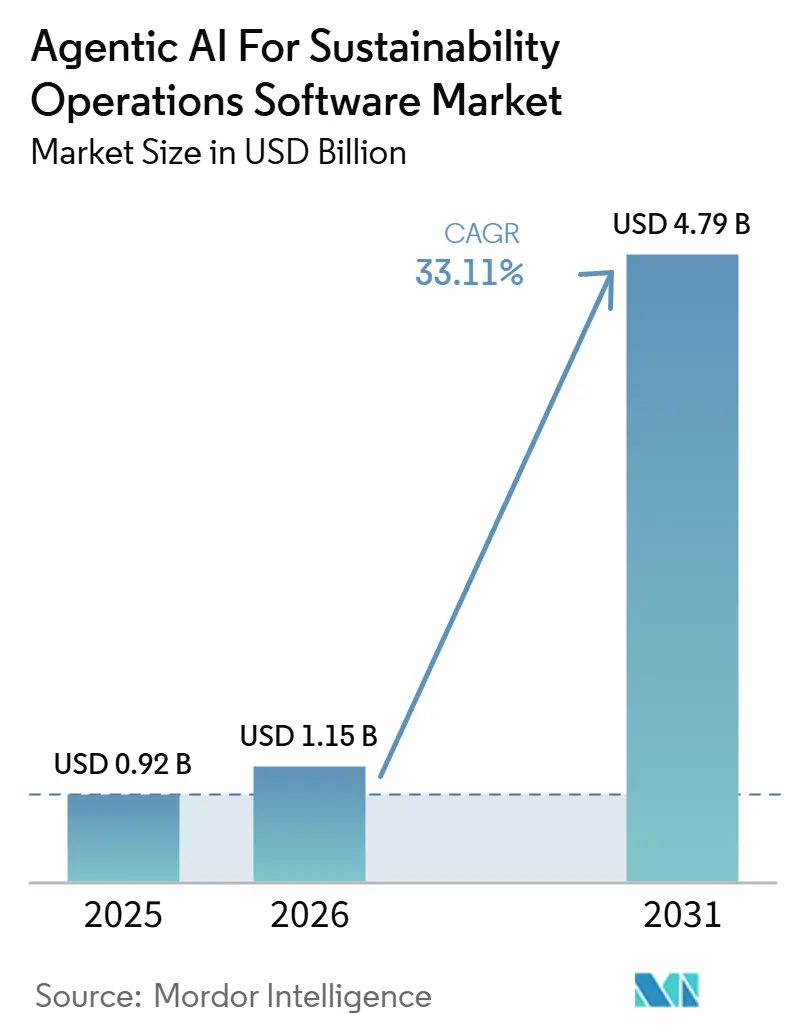

| Market Size (2026) | USD 1.15 Billion |

| Market Size (2031) | USD 4.79 Billion |

| Growth Rate (2026 - 2031) | 33.11% CAGR |

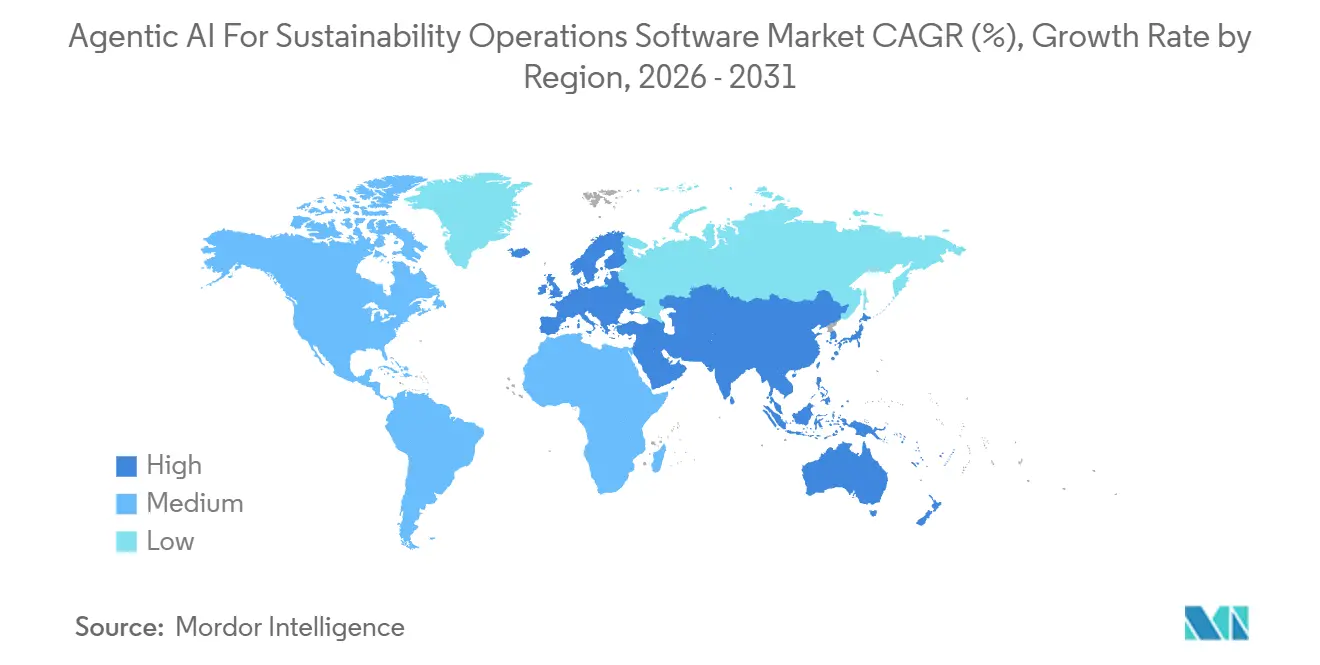

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agentic AI For Sustainability Operations Software Market Analysis by Mordor Intelligence

The agentic AI for sustainability operations software market size is expected to grow from USD 0.92 billion in 2025 to USD 1.15 billion in 2026 and is forecast to reach USD 4.79 billion by 2031 at 33.11% CAGR over 2026-2031. The agentic AI for sustainability operations software market is expanding because sustainability disclosure has shifted from a voluntary governance task to a formal reporting obligation in major economies. Reporting frameworks have multiplied faster than internal systems, data structures, and team capacity, which is pushing enterprises toward software that can manage recurring workflows instead of one-time reporting tasks. Buyers are also moving toward platforms that can sit inside ERP, finance, procurement, and CRM environments, because those connections determine whether data can be collected, checked, and reused at scale. The competitive field is being shaped by a clear split between large enterprise software vendors that bring broad system access and specialist vendors that bring deeper methodology, assurance readiness, and framework coverage. As integration costs rise and buyers push to reduce the number of vendor relationships they manage, the agentic AI for sustainability operations software market is opening the strongest opportunities for vendors that combine automation, traceability, and workflow depth inside core enterprise systems.

Key Report Takeaways

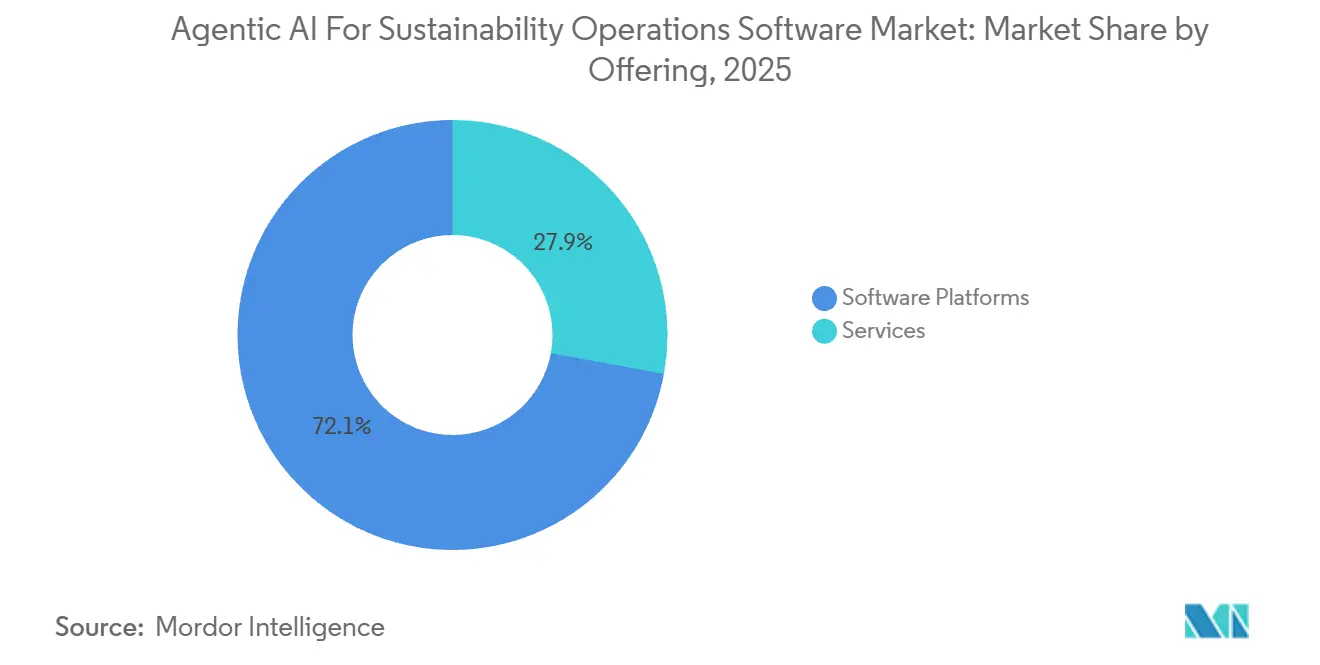

- By offering, software platforms held 72.10% of the agentic AI for sustainability operations software market share in 2025, while services are projected to expand at a 34.16% CAGR through 2031.

- By deployment mode, cloud accounted for 71.40% of the market in 2025 and is also expected to record the highest CAGR at 35.00% through 2031.

- By application, ESG data collection and orchestration led with a 29.40% share in 2025, while carbon accounting and Scope 3 management is projected to grow at a 36.00% CAGR through 2031.

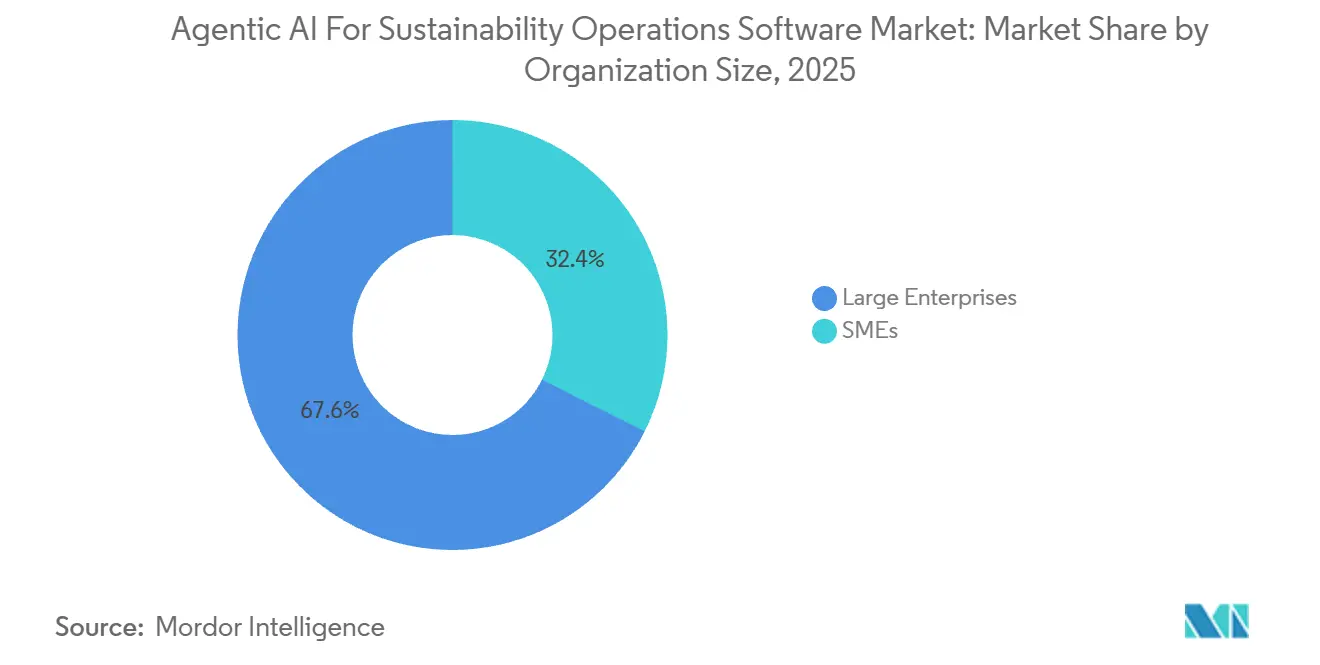

- By organization size, large enterprises represented 67.60% of the market in 2025, while SMEs are expected to expand at a 36.09% CAGR through 2031.

- By end user, industrial and manufacturing held 26.19% of the market in 2025, while BFSI is projected to advance at a 35.70% CAGR through 2031.

- By geography, North America held 32.90% share of the agentic AI for sustainability operations software market in 2025, while Asia-Pacific is expected to grow at a 35.00% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agentic AI For Sustainability Operations Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Deadlines Force Workflow-Level AI Adoption | +4.2% | Global, with peak intensity in Europe, Japan, and the U.S. West Coast | Short term (≤ 2 years) |

| Need For Audit-Ready Scope 3 Automation | +3.8% | Global, with acute demand in supply-chain-intensive economies such as Europe, China, and Japan | Short term (≤ 2 years) |

| Demand for Hyper-Automation Across ESG Workflows | +3.2% | North America and Europe core, with Asia-Pacific growing | Medium term (2-4 years) |

| Sustainability Teams Are Understaffed | +2.9% | Global, with the greatest strain in mid-market enterprises | Medium term (2-4 years) |

| Agentic AI Improves Cross-Functional Data Orchestration | +2.4% | North America and Europe | Medium term (2-4 years) |

| Sustainability Data Integration with ERP And Finance Systems | +2.1% | Global, with highest relevance in SAP and Oracle ERP-heavy markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Deadlines are Forcing Workflow-Level AI Adoption

The agentic AI for sustainability operations software market is moving from pilot activity to full enterprise deployment because disclosure obligations now demand repeatable and reviewable workflows. European, Japanese, and U.S. regulatory pressure is making sustainability reporting look more like financial reporting, where documentation, traceability, and assurance standards matter from the first filing cycle. That shift is pushing buyers away from dashboards and toward platforms that can map requirements to data fields, maintain records, and generate defensible audit trails across multiple business functions. In Japan, NEC reported that its AI-supported climate disclosure process reduced workload by 93% against manual preparation, which shows why regulated companies are treating automation as an operating requirement rather than a future option.[1]NEC Corporation, “NEC Uses AI to Improve Climate Disclosure Process for Securities Reports,” NEC Press Release, jpn.nec.com The same pressure is lifting demand in the agentic AI for sustainability operations software market for systems that can align disclosure tasks with securities filings, internal controls, and board-level review cycles. As rulebooks stabilize and filing timetables tighten, software that can convert legal obligations into structured workflows will remain central to adoption in the agentic AI for sustainability operations software market.

Rising Need for Audit-Ready Scope 3 Automation

The agentic AI for sustainability operations software market is gaining momentum because Scope 3 data remains the largest unresolved reporting problem for most enterprises. Companies can often measure direct operations with reasonable control, but supply-chain emissions still depend on fragmented supplier inputs, procurement records, and inconsistent factor libraries. Meta showed that AI applied to component-level hardware procurement data improved Scope 3 data quality and coverage compared with spend-based methods, which supports the case for deeper transaction-level automation. Watershed stated that its agents cut data cleaning time by 80%, and one test customer reduced a five-hour project to 20 minutes, while SAP said its Footprint Optimization Agent reduced scenario simulation time from 1 day to 20 minutes. These examples matter because the agentic AI for sustainability operations software market is no longer selling convenience alone; it is selling the ability to replace estimates with more auditable activity data. Vendors with stronger ERP and procurement connections will keep a structural advantage in the agentic AI for sustainability operations software market because better access to source transactions improves both data quality and assurance readiness.

Enterprise Demand for Hyper-Automation Across ESG Workflows

The agentic AI for sustainability operations software market is benefiting from a wider enterprise shift toward AI systems that handle complete workflows instead of isolated tasks. Sustainability teams do not need text generation by itself; they need software that can ingest energy and procurement data, classify records, route exceptions, prepare disclosures, and document each step for review. That requirement is favoring platforms that combine data automation, controls, and workflow logic across finance, risk, and reporting functions. Workiva’s Intelligent Sustainability release embedded agentic capabilities into sustainability, finance, and governance workflows, and Cognizant reported a 40% time saving on strategic sustainability governance tasks using those capabilities. The agentic AI for sustainability operations software market is therefore expanding not only because regulations are rising, but also because enterprises want to reduce manual handoffs across systems that already contain the underlying data. As those workflow links improve, the agentic AI for sustainability operations software market will keep moving toward continuous operating processes instead of periodic reporting exercises.

Sustainability Teams are Understaffed Relative to Reporting Burden

The agentic AI for sustainability operations software market is also being lifted by a basic capacity problem within reporting organizations. The number of required disclosure tasks has expanded faster than most sustainability teams, internal audit groups, and finance support functions can absorb with manual processes. This gap is especially visible in first-time filers and mid-market companies, where compliance expectations are rising even when specialist headcount remains limited. In practice, the agentic AI for sustainability operations software market is addressing that imbalance by automating repetitive work such as data gathering, rule mapping, draft preparation, exception checks, and coordination across business units. That value proposition matters because enterprises are not simply looking for labor reduction; they are looking for a way to sustain filing quality when obligations recur every year and across more jurisdictions. Vendors that can prove low-friction deployment, clear controls, and faster time to usable output will continue to gain ground in the agentic AI for sustainability operations software market as reporting workloads widen.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Quality Gaps in Scope 1, 2, And 3 Inputs | -3.5% | Global, with the greatest severity in supply-chain-heavy sectors and emerging markets | Medium term (2-4 years) |

| Trust, Explainability, and Governance Concerns | -2.8% | North America and Europe, where assurance and fiduciary obligations are highest | Medium term (2-4 years) |

| High Integration Cost with Legacy Enterprise Systems | -2.4% | Global, with the greatest strain in manufacturing, industrials, and mid-market companies | Long term (≥ 4 years) |

| Fragmented Standards Across Jurisdictions | -1.9% | Global, with the highest friction in multinational companies operating across Europe, the United States, and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Quality Gaps in Scope 1, 2, And 3 Inputs

The agentic AI for sustainability operations software market still faces a major limit because AI systems cannot produce reliable output from weak source data. Enterprise sustainability data usually sits across utility bills, ERP procurement records, supplier questionnaires, operational systems, and external factor libraries, which means there is rarely one clean system of record. When those inputs are incomplete or inconsistent, emissions factors can be misapplied, anomaly flags can become false positives, and audit trails can lose their link to the original source document. IBM’s Envizi Emissions API includes a library of more than 140,000 globally recognized emission datasets, which shows how vendors are trying to standardize factor selection and improve consistency before downstream analysis begins.[2]IBM Corporation, “IBM Envizi Emissions Calculations in Excel, Now Live on Microsoft AppSource,” IBM Community Blog, community.ibm.com Watershed’s launch also emphasized data cleaning before analysis, which reflects the simple fact that preprocessing remains essential even in more automated environments. The agentic AI for sustainability operations software market will continue to grow, but vendors that cannot improve data readiness at the ingestion stage will struggle to convert automation into trusted reporting outcomes.

Trust, Explainability, and Governance Concerns

The agentic AI for sustainability operations software market also faces a credibility challenge because buyers still need to understand how AI-generated outputs were produced. Sustainability filings are moving closer to financial-reporting discipline, so enterprises want every material metric to be supported by traceable logic, source references, and human review points. Salesforce said that 85% of investors are wary of greenwashing, which reinforces why disclosure teams want proof of provenance and not just faster narrative generation. SAP has also argued that sustainability AI without governance, auditability, and control can be more harmful than helpful, which explains why many buyers still keep human review at the final output stage. These concerns do not stop adoption in the agentic AI for sustainability operations software market, but they do favor vendors that can document calculations, preserve review logs, and fit within existing governance and compliance structures. As a result, the strongest providers in the agentic AI for sustainability operations software market are likely to be those that combine automation speed with transparent and reviewable decision paths.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Platform Demand is Centered on Durable Reporting Infrastructure

Software platforms held 72.10% of the market in 2025, which shows that buyers preferred standing infrastructure over one-off service engagement models. Within the agentic AI for sustainability operations software market, that lead reflects demand for systems that can preserve historical records, manage version control, and maintain audit-ready workflows year after year. Enterprises facing recurring disclosure obligations generally need connected software environments, not isolated projects, because continuity matters when filings are reviewed across multiple reporting cycles. The platform-heavy structure also raises switching costs early in the customer relationship, which is why the agentic AI for sustainability operations software market is already seeing intense competition to secure long-term enterprise accounts before consolidation becomes more visible. This preference for platforms is also tied to the way sustainability work is spreading across finance, procurement, operations, legal, and internal audit functions.

Services held the remaining share and are projected to expand at a 34.16% CAGR through 2031, which keeps them relevant in the agentic AI for sustainability operations software market even as platforms dominate. Services remain necessary because implementation, regulatory readiness, workflow redesign, data validation, and output review still require specialist judgment in many enterprise environments. As agentic capabilities improve, service work is shifting away from manual spreadsheet preparation and toward advisory services around controls, methodology choices, and deployment design. That transition matters because clients increasingly want a single accountable partner for both software and operating model support. The agentic AI for sustainability operations software industry is therefore not moving toward a simple software-only future, because the hardest problems often involve process change across functions rather than coding alone.

By Deployment Mode: Cloud Leads Because Connectivity Determines Usability

Cloud held 71.40% of the market in 2025, and cloud is also projected to grow at a 35.00% CAGR through 2031. In the agentic AI for sustainability operations software market size mix, that lead reflects the need for constant API connectivity across ERP systems, utility feeds, supplier networks, and disclosure workflows. Cloud architecture supports faster integration, more regular updates, and broader access to the data sources that agentic systems need in order to function well. Buyers are therefore choosing cloud not as a branding preference, but because the reporting workflow itself depends on connected data movement across many internal and external systems. Microsoft’s 2025 Wave 2 release for Sustainability Manager added product carbon footprint calculation and sustainability data allocation capabilities inside the Microsoft cloud environment, which shows how hyperscaler ecosystems are deepening their value in this category.[3]Microsoft Corporation, “Overview of Microsoft Sustainability Manager 2025 Release Wave 2,” Microsoft Learn, learn.microsoft.com

On-premises deployment still retains a practical role in the agentic AI for sustainability operations software market, where sovereignty rules, strict residency needs, or plant-level operational systems limit cloud adoption. Defense programs, sensitive public-sector environments, and some financial or industrial deployments continue to value tighter local control over data movement and system access. Large manufacturers also have operational technology environments that sit close to emissions-generating assets, which can make local deployment more workable for real-time industrial data capture. Even so, on-premises deployments are likely to remain a niche revenue stream because the broader market continues to favor faster connectivity and lower integration effort. The main strategic question is not whether on-premises disappears, but whether vendors can support hybrid models without creating inconsistent controls or duplicate data logic. In the agentic AI for sustainability operations software industry, vendors that handle both architectures well will have an edge with regulated and asset-heavy buyers.

By Application: Foundational Data Work Leads Revenue, Scope 3 Work Leads Growth

ESG data collection and orchestration held the largest application share at 29.40% in 2025, because all downstream workflows depend on clean and structured source data. In the agentic AI for sustainability operations software market, applications that sit closest to ingestion and normalization naturally lead revenue because they determine whether later calculations, disclosures, and analytics can be trusted. Enterprises often start here because a weak data structure undermines every later step, including reporting, scenario analysis, and supplier engagement. That pattern also explains why platforms with stronger data management layers have been able to secure more strategic customer positions than products built only for isolated reporting outputs. Buyers tend to view this application layer as core operating infrastructure rather than a narrow compliance feature. Once the data backbone is stable, additional modules become easier to adopt because the same records can be reused across multiple reporting and planning tasks. This dynamic keeps the first wave of spending focused on systems that can ingest, classify, and route information across business functions. It also gives foundational applications an anchoring role in the agentic AI for sustainability operations software market.

Carbon accounting and Scope 3 management is projected to grow at a 36.00% CAGR through 2031, which makes it the strongest growth engine across the application set. This rise reflects the widening accountability gap between Scope 1 and 2 processes, which are more mature, and Scope 3 supply-chain work, which still relies heavily on estimates in many organizations. SAP stated that its Footprint Optimization Agent can simulate reduction levers across products, plants, and supply chains in 20 minutes, while Watershed highlighted a broad adoption gap in AI use among sustainability practitioners. Regulatory reporting and disclosure automation is also scaling because enterprises need structured outputs that can be checked and reused, while sustainability analytics and scenario planning are gaining ground as buyers move beyond reactive compliance. Supplier and value-chain engagement remains smaller, but it has strategic value because much of the remaining data quality gap sits outside the enterprise boundary.

By Organization Size: Large Enterprises Still Anchor Revenue, While SMEs Create the Next Adoption Wave

Large enterprises held 67.60% of the market in 2025, which reflects the fact that early mandatory reporting pressure fell first on large corporations with more mature ERP and governance environments. In the agentic AI for sustainability operations software market, those organizations had the budgets, internal controls, and IT support required to deploy enterprise-grade platforms across multiple business units and geographies. They were also more likely to face direct regulatory scrutiny, complex supply chains, and assurance expectations that made manual processes difficult to sustain. This has given large enterprises a continuing lead in revenue because they can commit to fuller suites, deeper integration work, and broader internal rollouts than smaller peers. Their adoption pattern also shapes competition because major vendors often build features first for the needs of these larger accounts. Once those features become standardized, they can then be adapted downward for smaller customers. That sequence keeps large enterprises at the center of platform economics even while the next wave of demand broadens. It is one reason the agentic AI for sustainability operations software market continues to show early concentration around large corporate deployments.

SMEs are projected to grow at a 36.09% CAGR through 2031, which means the next expansion cycle will come from companies that are often pulled into reporting through customer pressure rather than direct regulatory choice. Large buyers increasingly need supplier-specific emissions data, and many of those suppliers are smaller firms that must now provide verified activity data instead of generalized estimates. This creates a compliance-led adoption path for SMEs, where software becomes necessary because customer relationships depend on disclosure readiness. In the agentic AI for sustainability operations software market, that dynamic favors lower-cost platforms with faster onboarding, prebuilt templates, and simple data collection workflows that do not require large specialist teams. It also opens room for vendors that can package implementation support, lightweight controls, and practical reporting guidance into a manageable subscription model. The agentic AI for sustainability operations software industry will therefore see volume growth from smaller enterprises even if absolute contract values remain lower than those of global corporations. What matters is that SMEs are no longer outside the reporting chain once large enterprise Scope 3 obligations begin to flow upstream. That change will widen the customer base of the agentic AI for sustainability operations software market during the forecast period.

By End User: Industrial Buyers Lead Current Spend, BFSI Lead Expansion

Industrial and manufacturing held 26.19% of the market in 2025, giving them the largest end-user share. In the agentic AI for sustainability operations software market, that lead reflects emissions-intensive operations, complex facility networks, and direct exposure to policies and customer demands tied to carbon measurement and reporting. These companies were also early users of energy management and environmental software, so many are now extending existing systems into more automated sustainability workflows. Their use cases often require frequent operational data capture, plant-level visibility, and stronger links between procurement, production, and compliance functions. Because of that, industrial buyers remain especially important to vendors that can connect sustainability controls to asset-heavy operating environments. The current share profile also indicates that measurable emissions exposure still matters in deciding which sectors buy first. In that sense, industrial demand provides the revenue base that supports broader category development in the agentic AI for sustainability operations software market. It remains one of the clearest examples of reporting needs being tied directly to operational complexity.

BFSI is projected to grow at a 35.70% CAGR through 2031, which makes them the fastest-growing end-user group in the category. Their challenge is different because material emissions often sit in financed portfolios rather than in direct operations, which makes manual analysis especially difficult at scale. Banks, insurers, and asset managers need systems that can process large counterparty sets, align calculations to financed-emissions methodologies, and maintain evidence quality for internal and external review. That need makes workflow automation highly valuable, because the volume and granularity of portfolio-level analysis are difficult to sustain through manual methods. The agentic AI for sustainability operations software market is therefore widening beyond physical operations into capital allocation, portfolio governance, and disclosure obligations linked to financial exposure. Consumer goods and retail companies are also using these tools for supplier engagement and product footprint labeling, but the strongest growth signal sits with institutions that must evaluate financed emissions across large books of business. This shift broadens the category’s relevance and reduces its dependence on only industrial use cases. It also confirms that the agentic AI for sustainability operations software market is becoming important wherever material sustainability exposure must be translated into structured and reviewable reporting.

Geography Analysis

North America held 32.90% of the agentic AI for sustainability operations software market share in 2025, making it the largest regional market. The region benefits from a high concentration of early technology adopters, large multinational enterprises, and corporate environments that already operate complex ERP and cloud estates. Demand has also been supported by state-level climate disclosure requirements in the United States, especially where companies must align internal reporting with formal governance and investor expectations. Canada adds depth through ISSB-aligned disclosure activity, while South America remains smaller but strategically important because Brazil’s role around COP30 in 2026 is increasing attention on corporate climate disclosure and supply-chain readiness. Argentina’s investment climate remains less stable, but export-oriented firms still face pressure when global customers ask for verified reporting inputs. Taken together, the Americas show how the agentic AI for sustainability operations software market can be led by large enterprise demand in the north while still opening selective opportunities further south through trade-linked disclosure pressure.

Europe remains one of the strongest demand centers in the agentic AI for sustainability operations software market because formal disclosure requirements continue to shape enterprise buying decisions. Even with narrower scope in the revised European framework, the remaining in-scope companies are large enterprises that are most likely to deploy full-suite platforms with deeper controls and integration needs. Germany’s industrial base, the United Kingdom’s financial sector, and France’s reporting environment each create distinct demand patterns, which keeps the region broad in both use case and buyer profile. The region also supports specialist providers that focus on local compliance interpretation, which adds another layer of competition alongside global software vendors. This matters because the agentic AI for sustainability operations software market in Europe is not driven by one uniform buying pattern, but by several overlapping needs across manufacturing, finance, and supply-chain compliance. Large multinational filers in the region are likely to keep favoring platforms that can handle cross-border reporting logic, assurance preparation, and integration with existing enterprise systems.

Asia-Pacific is projected to grow at a 35.00% CAGR through 2031, which makes it the fastest-growing geography in the agentic AI for sustainability operations software market size outlook. Japan is an especially important driver because disclosure obligations tied to securities reporting are raising the value of workflow automation for listed companies. NEC said its AI-supported climate disclosure process cut workload by 93%, while Fujitsu launched a commercial AI-powered non-financial disclosure analysis service in May 2026, which shows that practical enterprise deployment is already moving ahead in Japan. China, India, and South Korea also add demand through green finance, business responsibility, and ESG disclosure frameworks that increase reporting complexity across large listed companies and supply chains. Middle East markets, particularly the United Arab Emirates and Saudi Arabia, are investing in sustainability software as part of broader decarbonization and portfolio-governance agendas. Africa remains nascent, with South Africa and Egypt serving as early anchors, but adoption will depend more heavily on infrastructure readiness and enterprise software maturity. The regional picture shows that the agentic AI for sustainability operations software market is broadening fastest, where regulation, export exposure, and enterprise digitization are moving together.

Competitive Landscape

The agentic AI for sustainability operations software market is moderately fragmented, with large platform vendors and pure-play specialists competing from different starting advantages. SAP SE, Microsoft Corporation, IBM Corporation, and Salesforce, Inc. use their existing ERP, cloud, and CRM footprints to make deployment easier for enterprises that already rely on those systems. Their main advantage is breadth, because sustainability functions can be connected to the data environments where procurement, finance, operations, and customer workflows already sit. SAP strengthened that position in May 2026 by announcing 5 sustainability AI agents, including tools for regulatory readiness, footprint optimization, packaging compliance, classification, and workplace safety. Salesforce also launched Agentforce for Net Zero Cloud in June 2025, linking agentic AI with Data Cloud to support disclosure responses, insight generation, and real-time data gap identification.[4]Salesforce, Inc., “Salesforce Launches Agentforce for Net Zero Cloud,” Salesforce News, salesforce.com

Specialists compete differently in the agentic AI for sustainability operations software market, usually emphasizing methodological depth, assurance readiness, and more focused workflow design. Watershed, Persefoni AI, Workiva, Sweep, Greenly, Plan A, and Normative are examples of vendors that have built their products around domain-specific reporting problems rather than around broad horizontal suites. Workiva’s Intelligent Sustainability launch showed how a specialist can tie sustainability functions more closely to finance, controls, and governance workflows while still preserving a focused product identity. Watershed’s April 2026 release of new agents and its related fellowship program also illustrates how specialists are trying to win through operational depth and customer enablement rather than system breadth alone. The competitive tension is therefore clear, because large vendors bring installed base and data access, while specialists bring narrower but often deeper workflow execution.

White space in the agentic AI for sustainability operations software market remains visible in financed-emissions automation, supplier engagement across fragmented industrial networks, and reporting that can adapt across several disclosure frameworks without extensive rework. IBM’s launch of Envizi Emissions Calculations in Excel on Microsoft AppSource shows how incumbents are also trying to serve users who still rely on familiar spreadsheet workflows while gradually moving them toward more connected systems. Microsoft’s continued expansion of Sustainability Manager shows a similar effort to deepen native capability rather than leave sustainability as a separate point tool. At the same time, smaller companies are applying pressure where local regulation, faster onboarding, or stronger methodology support matters more than global scale. Buyers are responding by evaluating not only feature lists, but also the vendor’s ability to support evidence quality, governance needs, and long-term integration into enterprise workflows.

Agentic AI For Sustainability Operations Software Industry Leaders

Sweep

SAP SE

3E Company Environmental, Ecological and Engineering, LLC

Zycus Inc.

Persefoni AI, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SAP SE announced 5 sustainability AI agents at SAP Sapphire 2026, currently in beta and scheduled for general availability by the end of 2026. Agents span regulatory readiness, Scope 3 footprint optimization, packaging compliance, GHS classification, and workplace safety. The Footprint Optimization Agent reduces scenario simulation time from approximately one day to 20 minutes, and the Packaging Compliance Agent cuts manual compliance review hours by more than 50%, directly addressing the enterprise gap between reporting volume and sustainability team capacity.

- May 2026: Fujitsu launched a commercial AI-powered non-financial information disclosure analysis service in Japan, providing companies with AI-generated analysis of their own and competitors' ESG disclosure status against major rating agency criteria, and supporting strategic improvement in non-financial disclosures toward securities report requirements.

- April 2026: Watershed Technology launched Watershed Agents at San Francisco Climate Week, including data cleaning and analysis agents that cut time to actionable sustainability data by 80%. The platform also launched the Watershed AI Fellowship, an eight-week accelerator program for enterprise sustainability teams to deepen AI deployment expertise. Across test customers, one company reduced a five-hour data cleaning project to 20 minutes, a 93% time reduction.

- April 2026: NEC Corporation (Japan) completed development of an AI-supported climate disclosure process for securities reports, demonstrating a 93% workload reduction in internal trials. NEC plans to commercialize the climate disclosure support service in fiscal year 2026.

Global Agentic AI For Sustainability Operations Software Market Report Scope

The agentic AI for sustainability operations software market comprises software platforms that leverage autonomous and goal-oriented artificial intelligence (AI) agents to automate, orchestrate, and optimize sustainability and environmental, social, and governance (ESG) operations across enterprise workflows. These solutions enable organizations to collect, validate, analyze, and manage sustainability data, automate carbon accounting and greenhouse gas (GHG) emissions calculations (including Scope 1, Scope 2, and Scope 3 emissions), generate regulatory disclosures, monitor sustainability performance, and support decision-making through intelligent recommendations and workflow execution with minimal human intervention.

The Agentic AI for Sustainability Operations Software Market Report is segmented by Offering (Software Platform, and Services), Deployment Mode (Cloud, and On-Premises), Application (ESG Data Collection and Orchestration, Carbon Accounting and Scope 3 Management, Regulatory Reporting and Disclosure Automation, Sustainability Analytics and Scenario Planning, and Supplier and Value Chain Engagement), Organization Size (Large Enterprises, and SMEs), End User (BFSI, Industrial and Manufacturing, Consumer Goods and Retail, Energy and Utilities, IT and Telecom, Healthcare and Life Sciences, and Other End Users), and Geography (North America, Europe , Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software Platform |

| Services |

| Cloud |

| On-Premises |

| ESG Data Collection and Orchestration |

| Carbon Accounting and Scope 3 Management |

| Regulatory Reporting and Disclosure Automation |

| Sustainability Analytics and Scenario Planning |

| Supplier and Value Chain Engagement |

| Large Enterprises |

| SMEs |

| BFSI |

| Industrial and Manufacturing |

| Consumer Goods and Retail |

| Energy and utilities |

| IT and Telecom |

| Healthcare and life sciences |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Offering | Software Platform | |

| Services | ||

| By Deployment Mode | Cloud | |

| On-Premises | ||

| By Application | ESG Data Collection and Orchestration | |

| Carbon Accounting and Scope 3 Management | ||

| Regulatory Reporting and Disclosure Automation | ||

| Sustainability Analytics and Scenario Planning | ||

| Supplier and Value Chain Engagement | ||

| By Organization Size | Large Enterprises | |

| SMEs | ||

| By End User | BFSI | |

| Industrial and Manufacturing | ||

| Consumer Goods and Retail | ||

| Energy and utilities | ||

| IT and Telecom | ||

| Healthcare and life sciences | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the agentic AI for sustainability operations software market?

The agentic AI for sustainability operations software market size stands at USD 0.92 billion in 2025, rises to USD 1.15 billion in 2026, and is forecast to reach USD 4.79 billion by 2031 at a 33.11% CAGR.

What is driving demand for agentic AI in sustainability operations?

Demand is being driven by mandatory disclosure rules, the need for audit-ready Scope 3 workflows, rising reporting complexity, and pressure to automate cross-functional sustainability tasks inside enterprise systems.

Which deployment model leads adoption in sustainability operations software?

Cloud leads adoption with 71.40% share in 2025 and is also the fastest-growing deployment model at a 35.00% CAGR through 2031 because connected data flows are essential to this category.

Which application area is growing the fastest?

Carbon accounting and Scope 3 management is the fastest-growing application, with a 36.00% CAGR through 2031, as enterprises move beyond direct emissions tracking and focus on supply-chain evidence quality.

Which region is expanding the fastest for agentic AI sustainability software?

Asia-Pacific is the fastest-growing region at a 35.00% CAGR through 2031, supported by disclosure developments in Japan, China, India, and South Korea.

Which end users are creating the strongest growth opportunity?

Industrial and manufacturing currently lead with 26.19% share in 2025, while BFSI is the fastest-growing end users at a 35.70% CAGR because financed-emissions workflows are difficult to manage manually.

Page last updated on: