Agentic Enterprise Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

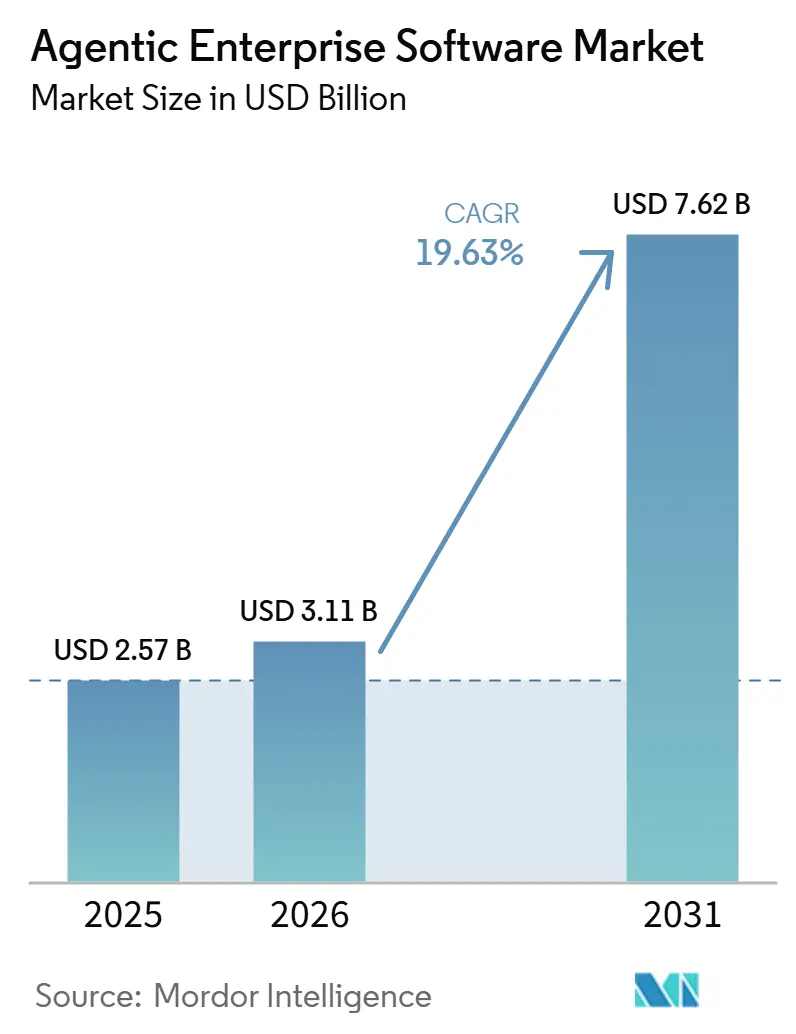

| Market Size (2026) | USD 3.11 Billion |

| Market Size (2031) | USD 7.62 Billion |

| Growth Rate (2026 - 2031) | 19.63% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agentic Enterprise Software Market Analysis by Mordor Intelligence

The agentic enterprise software market size is expected to grow from USD 2.57 billion in 2025 to USD 3.11 billion in 2026 and is forecast to reach USD 7.62 billion by 2031 at a 19.63% CAGR over 2026-2031. Sustained momentum reflects a structural pivot from brittle, rule-based scripts to adaptive agents that interpret natural language, reason across context, and trigger downstream applications with minimal human supervision. Lower per-token inference costs, the arrival of outcome-based pricing, and expanding reference architectures are shortening payback periods, which encourages even risk-averse sectors to accelerate deployments. North American financial institutions continue to anchor early adoption, yet Asia-Pacific policy mandates that favor sovereign data processing are redrawing the competitive map. Simultaneously, standards-setting bodies are clarifying authentication, audit, and interoperability protocols, reducing procurement friction and unlocking multi-vendor rollouts.

Key Report Takeaways

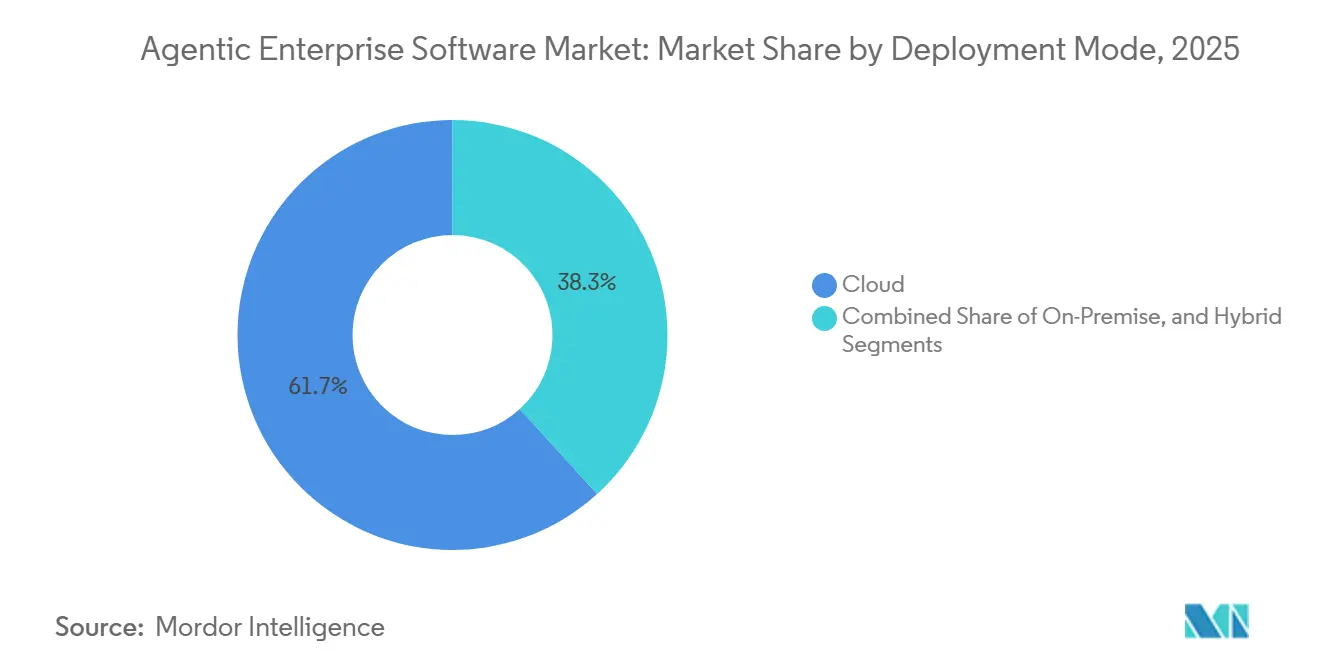

- By deployment mode, cloud-based platforms led with 61.74% revenue share in 2025, while hybrid architectures are projected to expand at a 20.23% CAGR through 2031.

- By component, software licenses accounted for 58.42% of spending in 2025, whereas services are forecast to grow at a 20.03% CAGR through 2031.

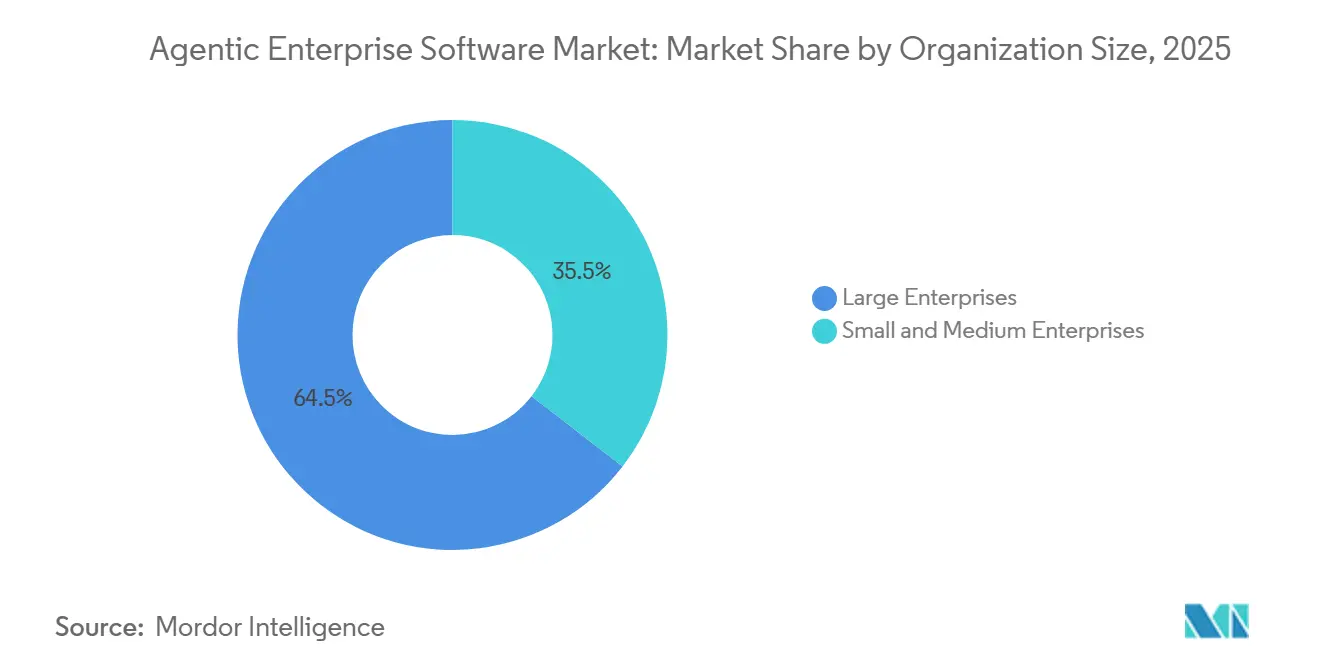

- By organization size, large enterprises held 64.52% share in 2025, yet small and medium enterprises are advancing at a 20.36% CAGR through 2031.

- By industry vertical, banking, financial services, and insurance accounted for 19.11% of 2025 revenue, while healthcare and life sciences are set to climb at a 20.43% CAGR to 2031.

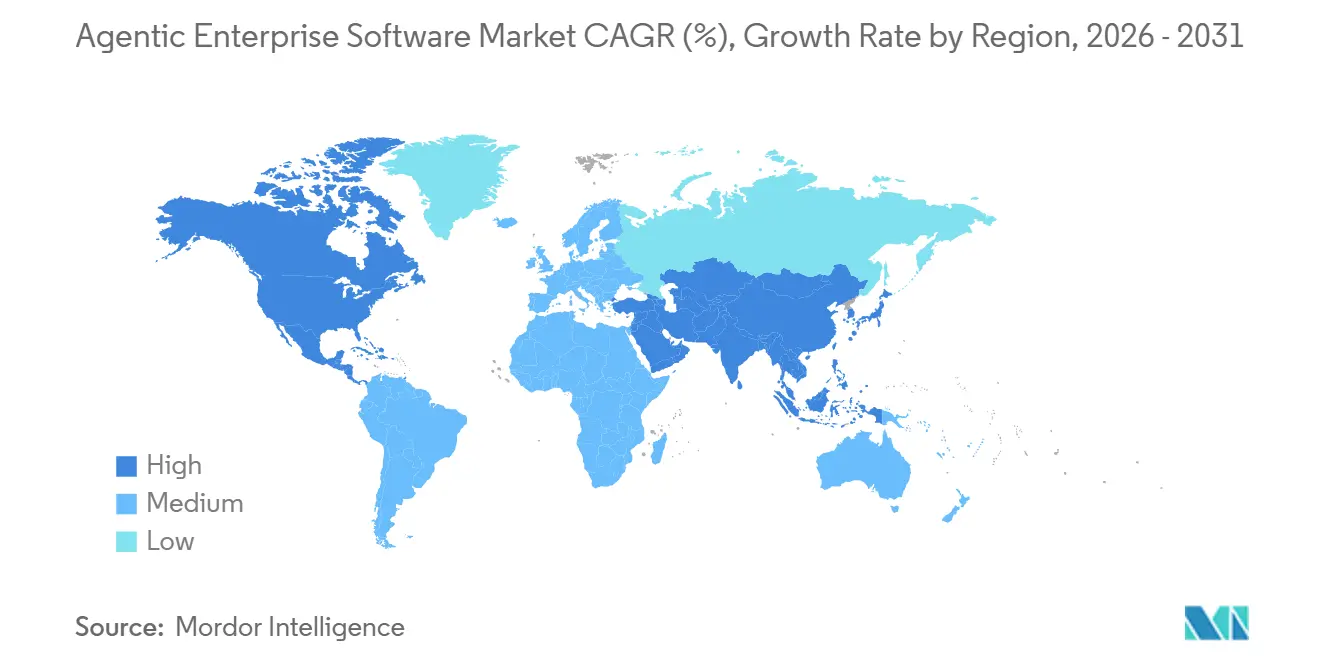

- By geography, North America commanded 39.68% revenue share in 2025, and Asia-Pacific is projected to register a 20.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agentic Enterprise Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise Demand for Hyper-Automation and Cost Efficiency | +5.2% | Global, with early concentration in North America and Western Europe | Short term (≤ 2 years) |

| Rapid Advances in Large Language Models and Tool-Orchestration Frameworks | +4.8% | Global, led by United States, China, and United Kingdom | Medium term (2-4 years) |

| Cloud Infrastructure Expansion and Lower Inference Costs | +3.9% | Global, with accelerated adoption in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Emergence of Multi-Agent Governance Standards Enabling Cross-Vendor Interoperability | +2.7% | North America and Europe, with spillover to Asia-Pacific | Long term (≥ 4 years) |

| Sector-Specific Responsible AI Frameworks Unlocking Regulated Industry Adoption | +2.1% | Global, concentrated in BFSI and healthcare sectors | Long term (≥ 4 years) |

| Availability of Outcome-Based Pricing Models Accelerating Mid-Market Uptake | +1.8% | Global, with strongest traction in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Enterprise Demand for Hyper-Automation and Cost Efficiency

Organizations are consolidating scattered point tools into unified agent stacks that compress cycle times and shrink payroll outlays, especially in finance, human resources, and procurement. Agents remain resilient when user interfaces or data schemas shift, which avoids the costly re-scripting that undermined earlier robotic process automation efforts. In high-wage regions, deployments now attain payback in under one year, strengthening board-level sponsorship. Banking compliance teams, for example, deploy agents that monitor transactions in real time, achieving double-digit reductions in false positives while maintaining regulatory audit trails. Rising labor costs and persistent skills gaps further magnify the appeal of digital labor, ensuring that demand for hyper-automation will stay elevated across both mature and emerging economies.

Rapid Advances in Large Language Models and Tool-Orchestration Frameworks

Frameworks such as LangGraph, AutoGen, and CrewAI allow developers to chain specialized agents for data retrieval, code execution, and reasoning into cohesive workflows that approximate human analyst performance. OpenAI’s Frontier platform introduced out-of-the-box templates for contract reviews, customer support triage, and supply chain diagnostics, cutting deployment cycles from quarters to weeks. Context windows have leapt from 32,000 tokens in early 2025 to more than 200,000, enabling agents to process entire code bases or multi-year ledgers in a single pass, a capability prized for root-cause investigations in manufacturing. Vertically tuned models backed by safety guardrails are addressing concerns about hallucinations, which is widening adoption in regulated fields that require deterministic rollback and comprehensive audit trails.

Cloud Infrastructure Expansion and Lower Inference Costs

Purpose-built accelerators such as NVIDIA’s H200 and AMD’s MI300X, alongside optimized inference engines, have lowered per-token costs by about 40% between early and late 2025, making always-on agents affordable for high-frequency workloads. Amazon Web Services, for instance, offers batch inference that can trim expenses by up to 50% for non-latency-sensitive processing. Yet agentic workflows can multiply token traffic by up to 30-fold compared with single-shot completions, so operators mitigate spend through reserved capacity, spot instances, and regional data centers that minimize egress charges and latency. As clouds extend into Malaysia, Thailand, and Saudi Arabia, real-time retail and telemedicine agents can maintain sub-second responses, which are essential for a positive user experience.

Emergence of Multi-Agent Governance Standards Enabling Cross-Vendor Interoperability

The National Institute of Standards and Technology launched the AI Agent Standards Initiative in February 2026, catalyzing work on shared schemas for authentication, task delegation, and audit logging.[1]National Institute of Standards and Technology, “NIST Launches AI Agent Standards Initiative,” nist.gov Early specifications, such as the Model Context Protocol, let a Salesforce agent trigger a ServiceNow workflow or query an SAP table without bespoke middleware. ISO/IEC 42001:2023 provides a management blueprint that enterprises now embed into vendor contracts, demanding third-party reviews of training data provenance and model update cadence. Although fewer than one-fifth of commercial platforms fully comply today, convergence around common interfaces is expected to lower switching costs and speed multi-vendor rollouts over the next four years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation Costs and Legacy Integration Challenges | -3.4% | Global, with acute impact in Europe and North America due to older enterprise systems | Short term (≤ 2 years) |

| Data Privacy and Regulatory Uncertainty | -2.8% | Europe and North America, with spillover to Asia-Pacific as regulations tighten | Medium term (2-4 years) |

| Scarcity of Safety-Alignment Engineering Talent | -1.9% | Global, most severe in North America and Europe | Medium term (2-4 years) |

| Absence of Enterprise-Grade Agent Reliability Benchmarks | -1.6% | Global, with heightened concern in regulated industries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Implementation Costs and Legacy Integration Challenges

Embedding agents into decades-old enterprise resource planning and customer management platforms demands custom connectors, data harmonization, and exhaustive regression testing. Mainframe environments that still power banking and insurance add another layer of complexity because COBOL interfaces lack modern APIs, which increases latency and failure risk. On-premise rollouts also require specialized GPU clusters, which entail capital expenditures ranging from USD 0.5 million to USD 2 million for mid-sized estates. While outcome-based pricing shifts some risk to vendors, it compresses their margins and restricts the pool of capable integrators. These factors prolong project timelines and temper near-term adoption despite compelling total cost-of-ownership calculations.

Data Privacy and Regulatory Uncertainty

The European Union’s AI Act, in a phased enforcement approach, classifies credit scoring, hiring, and clinical decision support as high-risk systems, mandating transparency reports, human oversight, and third-party conformity assessments before production use.[2]European Commission, “Artificial Intelligence Act – Key Provisions,” ec.europa.eu Cross-border deployments must also comply with the General Data Protection Regulation, China’s Personal Information Protection Law, and California’s Consumer Privacy Act, each of which imposes divergent storage, deletion, and consent requirements. Unclear liability for agent errors adds further hesitation, especially in the pharmaceutical and aerospace industries. Although regulatory sandboxes in the United Kingdom and Singapore provide controlled test beds, they serve only a fraction of the enterprises seeking guidance, leaving most firms to chart compliance paths without clear precedent.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Hybrid Architectures Reconcile Sovereignty and Scale

Hybrid deployments are expanding at a 20.23% annual clip through 2031 as firms route sensitive inference workloads, such as patient records or credit-risk models, to on-premise nodes while leveraging cloud elasticity for batch analytics and public-facing chatbots. Cloud offerings accounted for 61.74% of 2025 revenue due to rapid provisioning and vendor-maintained updates, yet data residency statutes in Germany and Switzerland limit pure-cloud penetration. Microsoft Azure Stack, AWS Outposts, and similar solutions replicate cloud control planes on local hardware, enabling developers to invoke identical APIs regardless of location. The agentic enterprise software market size for hybrid solutions is forecast to accelerate as emerging interoperability protocols reduce configuration overhead and as edge use cases, from robotics to retail kiosks, demand sub-100-millisecond response times.

Regulators are nudging adoption toward hybrid models by requiring that high-risk inference logs remain within sovereign borders, thereby guarding against vendor lock-in by keeping mission-critical data onsite. Enterprises cut egress bills by keeping latency-sensitive tokens local while bursting non-critical jobs to spot instances priced up to 80% below on-demand rates. As multi-cloud governance matures, agents will increasingly orchestrate tasks across AWS, Azure, and Google Cloud within a single workflow, thereby diversifying runtime risk and amplifying resilience.

By Component: Services Surge as Integration Complexity Outpaces Licensing

Software accounted for 58.42% of 2025 spending, yet the agentic enterprise software market share mix is shifting as services register a 20.03% CAGR, mirroring the difficulty of stitching agents into heterogeneous estates. Data engineering, schema mapping, and safety testing can swallow 30% to 50% of first-year budgets, while hourly rates for specialized engineers reach USD 300 in major hubs. Outcome-based managed services that commit to definitive performance benchmarks are attracting mid-market buyers that lack in-house machine-learning talent.

OpenAI’s Frontier Alliances with global consultancies formalize this ecosystem by pooling model expertise with change-management playbooks, shrinking pilot timelines in heavily regulated verticals.[3]OpenAI, “Frontier Alliances With Global Consultancies,” openai.com Training programs from hyperscalers certify thousands of practitioners in prompt engineering and red-teaming, further fueling services growth. The agentic enterprise software market size for managed offerings is set to expand as vendors assume operational risk, though margin pressures may induce consolidation among undercapitalized startups.

By Organization Size: Outcome-Based Models Unlock Small and Medium Enterprise Adoption

Large enterprises accounted for 64.52% of 2025 revenue, underscoring their significant influence in the market. However, the small and medium enterprise (SME) segment is experiencing faster growth, with a compound annual growth rate (CAGR) of 20.36% projected through 2031. This accelerated growth can be attributed to the adoption of consumption-based pricing models, which eliminate the upfront licensing costs that often act as barriers for smaller firms. For instance, UiPath’s Autopilot offers a pricing structure starting at USD 500 per month, with additional fees based on transaction volumes rather than the number of seats. This approach significantly lowers the entry threshold for companies with fewer than 500 employees, enabling them to adopt advanced automation solutions more easily.

Outcome-based contracts are gaining traction as they ensure measurable results within a specified timeframe, thereby guaranteeing time-to-value for clients. However, these contracts also shift the integration risk to suppliers, who must deliver quantifiable improvements, such as a 25% reduction in invoice cycle time, within the agreed-upon period. Strategic partnerships are also evolving to better align vendor and client incentives. A notable example is the USD 200 million Snowflake-OpenAI collaboration, which ties revenue sharing to customer consumption, creating a mutually beneficial model.[4]Snowflake, “Snowflake–OpenAI Strategic Partnership,” snowflake.com Additionally, advancements in no-code agent builders are empowering business analysts to design and configure workflows without coding expertise. Despite these advancements, complex edge cases still require developers to address intricate requirements.

By Industry Vertical: Healthcare Acceleration Driven by Administrative Burden Relief

Banking, financial services, and insurance captured 19.11% of 2025 revenue by deploying agents that flag suspicious transactions and streamline regulatory filings. However, healthcare and life sciences are expected to log the fastest growth, at a 20.43% CAGR through 2031, as clinical documentation agents reduce physician paperwork and free capacity for patient care. In manufacturing, predictive-maintenance agents ingest sensor telemetry to forecast part failures 48-72 hours ahead, reducing unplanned downtime by up to one-third.

Retail and e-commerce lean on agents for personalized offers and dynamic pricing, yielding double-digit conversion lifts during pilot programs. Telecommunications carriers automate tier-1 troubleshooting, slicing average handle time by roughly one-quarter. Government use remains exploratory because procurement and security reviews lengthen timelines, yet early tax administration pilots show 30%-plus throughput gains. Across verticals, the agentic enterprise software industry is converging on multi-modal reasoning that fuses text, images, and tabular data into unified decision engines, reducing hallucination rates in domain-specific contexts.

Geography Analysis

North America accounted for 39.68% of 2025 revenue, driven by the presence of established technology incumbents and a favorable regulatory environment. The region's market stronghold is attributed to its early adoption of advanced technologies and significant investments in innovation. However, the Asia-Pacific is expected to achieve the highest regional CAGR of 20.63% through 2031. Countries such as China, Japan, India, and South Korea are heavily investing in indigenous model training and local inference clusters to ensure data sovereignty. This focus has led to increased demand for on-premise accelerators and open-source tools, positioning the region as a key growth driver in the market. Meanwhile, Europe faces slower rollouts due to its stringent privacy regulations, but this approach fosters long-term trust, which could serve as a competitive advantage for vendors in the region.

The Middle East and Africa are channeling oil windfall revenues into the development of AI hubs, though current use remains concentrated in sectors such as energy and public services. These investments aim to diversify regional economies and enhance technological capabilities. In Latin America, growth is primarily centered around Brazil and Argentina, where digital banking and retail pilots are successfully demonstrating the value of AI in fraud detection and personalized merchandising. These advancements highlight the region's potential for AI adoption, despite challenges such as economic instability and infrastructure limitations.

Hyperscaler region build-outs in countries like Malaysia, Thailand, and Saudi Arabia are reducing latency for edge-heavy workloads, further enabling the adoption of advanced technologies. These developments are complemented by the World Economic Forum's governance framework, which provides a standardized vocabulary for enterprises to harmonize multi-jurisdiction deployments. This framework is particularly beneficial for organizations operating across diverse regulatory environments, ensuring smoother integration and compliance. Collectively, these regional dynamics underscore the global momentum toward AI adoption, with varying growth trajectories influenced by local policies, investments, and technological readiness.

Competitive Landscape

The agentic enterprise software market remains moderately concentrated as cloud hyperscalers embed agents across existing productivity and infrastructure suites, while focused startups differentiate on safety and domain specificity. Microsoft integrates Copilot across Azure and Office 365, creating a seamless upgrade path for its installed base and reinforcing ecosystem stickiness. Salesforce’s Agentforce extends dominant customer-relationship capabilities into autonomous lead qualification and case resolution, reinforcing subscription revenue without requiring customers to leave the familiar interface.

OpenAI, Anthropic, Cohere, and Adept compete on model alignment and privacy commitments. Anthropic’s Constitutional AI training framework attracts risk-averse banks and hospitals that demand transparent safeguards. Cohere’s policy of excluding customer data from training further resonates with confidentiality-driven sectors. Standards work led by NIST is diminishing vendor lock-in by enabling cross-platform messaging, disrupting single-vendor moats while enlarging the total addressable market as integration overhead falls.

Reliability metrics, such as mean time between agent failures, latency at the 95th percentile, and hallucination incidence, are emerging as key selling points, but the lack of accepted yardsticks forces enterprises to run bespoke evaluations that favor deep-pocketed suppliers able to subsidize exhaustive pilots. Strategic alliances with global systems integrators accelerate go-to-market velocity by pairing models with industry change-management muscle, a bundling tactic that smaller vendors struggle to match.

Agentic Enterprise Software Industry Leaders

Microsoft Corporation

Amazon Web Services, Inc.

Alphabet Inc.

IBM Corporation

NVIDIA Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Anthropic unveiled the Claude Partner Network with USD 100 million in committed funding to co-develop vertical agents and provide implementation services across financial services, healthcare, and manufacturing.

- February 2026: NIST initiated the AI Agent Standards Initiative to draft baseline protocols for authentication, delegation, and audit logging, with final specifications expected in 2027.

- February 2026: Snowflake and OpenAI formed a USD 200 million partnership to embed natural-language, agentic analytics within Snowflake’s data cloud, cutting time-to-insight for business analysts by 40%.

- February 2026: Cognigy released version 2026.3 of its platform, adding multi-agent orchestration, reducing voice bot latency, and expanding ERP integrations.

Global Agentic Enterprise Software Market Report Scope

The Agentic Enterprise Software Market refers to the market for advanced enterprise software solutions that leverage autonomous AI agents to perform tasks, make decisions, and orchestrate complex business processes with minimal human intervention. These systems utilize technologies such as artificial intelligence, machine learning, natural language processing, and multi-agent architectures to enable real-time decision-making, workflow automation, and adaptive optimization across enterprise functions.

The Agentic Enterprise Software Market Report is Segmented by Deployment Mode (Cloud, On-Premise, and Hybrid), Component (Software, and Services), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (BFSI, Healthcare and Life Sciences, Manufacturing, Retail and E-Commerce, IT and Telecom, and Government and Public Sector), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Based |

| On-Premise |

| Hybrid |

| Software |

| Services |

| Large Enterprises |

| Small and Medium Enterprises |

| Banking Financial Services and Insurance BFSI |

| Healthcare and Life Sciences |

| Manufacturing |

| Retail and E-Commerce |

| Information Technology and Telecom |

| Government and Public Sector |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Deployment Mode | Cloud-Based | ||

| On-Premise | |||

| Hybrid | |||

| By Component | Software | ||

| Services | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Industry Vertical | Banking Financial Services and Insurance BFSI | ||

| Healthcare and Life Sciences | |||

| Manufacturing | |||

| Retail and E-Commerce | |||

| Information Technology and Telecom | |||

| Government and Public Sector | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the agentic enterprise software market by 2031?

The market is forecast to reach USD 7.62 billion by 2031 Which deployment mode is growing the fastest Hybrid architectures are expanding at a 20.23% CAGR as firms balance sovereignty and cloud scale.

Which industry vertical is expected to see the highest growth?

Healthcare and life sciences driven by administrative-task automation is projected to grow at a 20.43% CAGR.

Why are small and medium enterprises adopting agents more rapidly?

Outcome-based pricing removes upfront costs and aligns fees with measurable improvements enabling faster payback.

How are interoperability standards influencing vendor selection?

Emerging NIST and ISO protocols reduce lock-in by allowing agents from different vendors to communicate over shared schemas.

What regions present the greatest future growth potential?

Asia-Pacific leads with a projected 20.63% CAGR boosted by sovereign data mandates and large-scale AI infrastructure investment.

Page last updated on: