Agent-Oriented Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

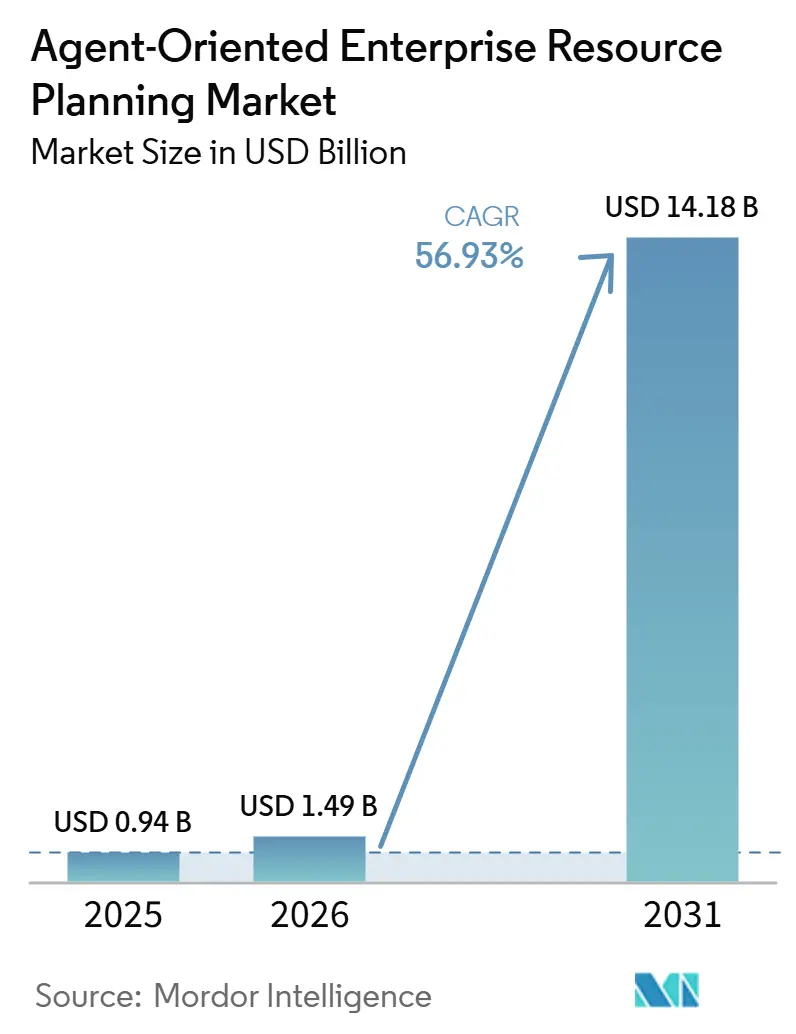

| Market Size (2026) | USD 1.49 Billion |

| Market Size (2031) | USD 14.18 Billion |

| Growth Rate (2026 - 2031) | 56.93% CAGR |

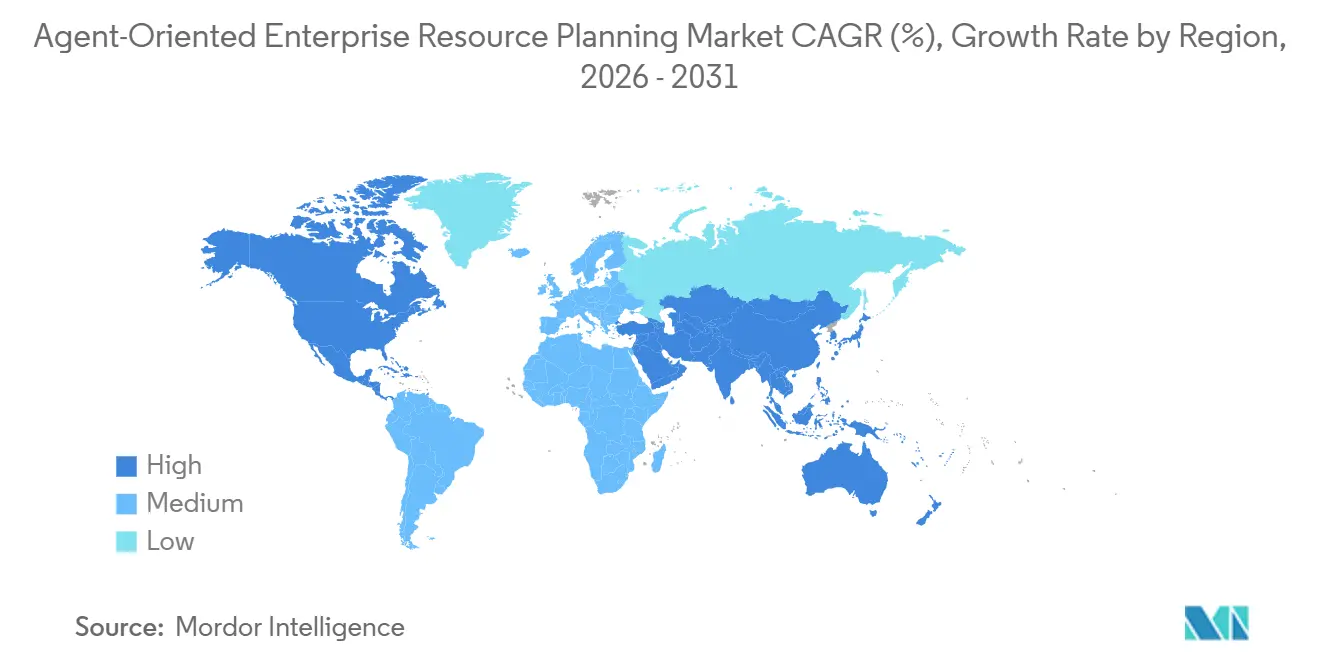

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agent-Oriented Enterprise Resource Planning Market Analysis by Mordor Intelligence

The agent-oriented enterprise resource planning market size is expected to grow from USD 0.94 billion in 2025 to USD 1.49 billion in 2026 and is forecast to reach USD 14.18 billion by 2031 at 56.93% CAGR over 2026-2031. Demand is shifting from static diagram repositories to autonomous, goal-driven agent systems that orchestrate workloads, rebalance clusters, and trigger rollbacks in real time. Enterprises are compressing infrastructure decision cycles from weeks to minutes, which transforms platform selection into an operating-model choice. Modeling tools are being retrofitted with agent semantics, while hyperscalers embed agent fabrics directly into cloud platforms. Governance requirements for explainability, auditability, and data residency are shaping deployment choices and accelerating interest in hybrid and sovereign cloud architectures.

Key Report Takeaways

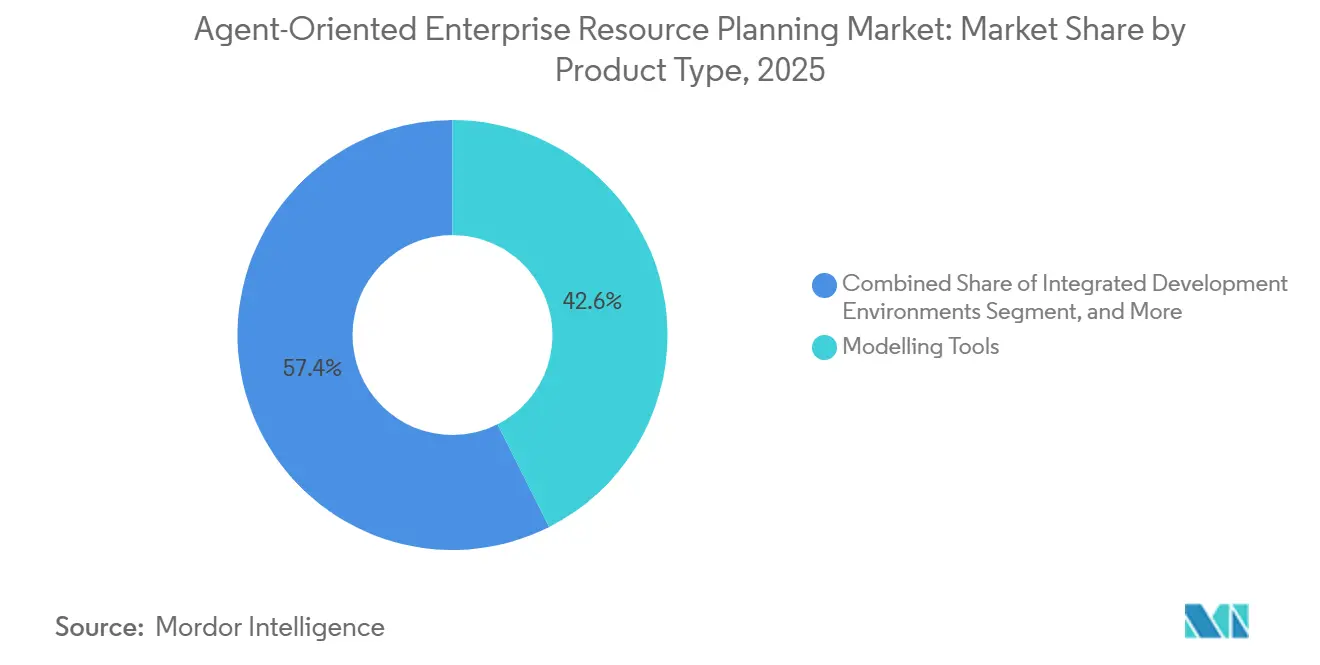

- By product type, modeling tools led with 42.57% of the agent-oriented enterprise resource planning market share in 2025, while agent-based simulation platforms are advancing at a 57.93% CAGR through 2031.

- By deployment mode, cloud-controlled accounted for 55.32% of revenue in 2025, whereas hybrid is projected to expand at a 57.53% CAGR between 2026 and 2031.

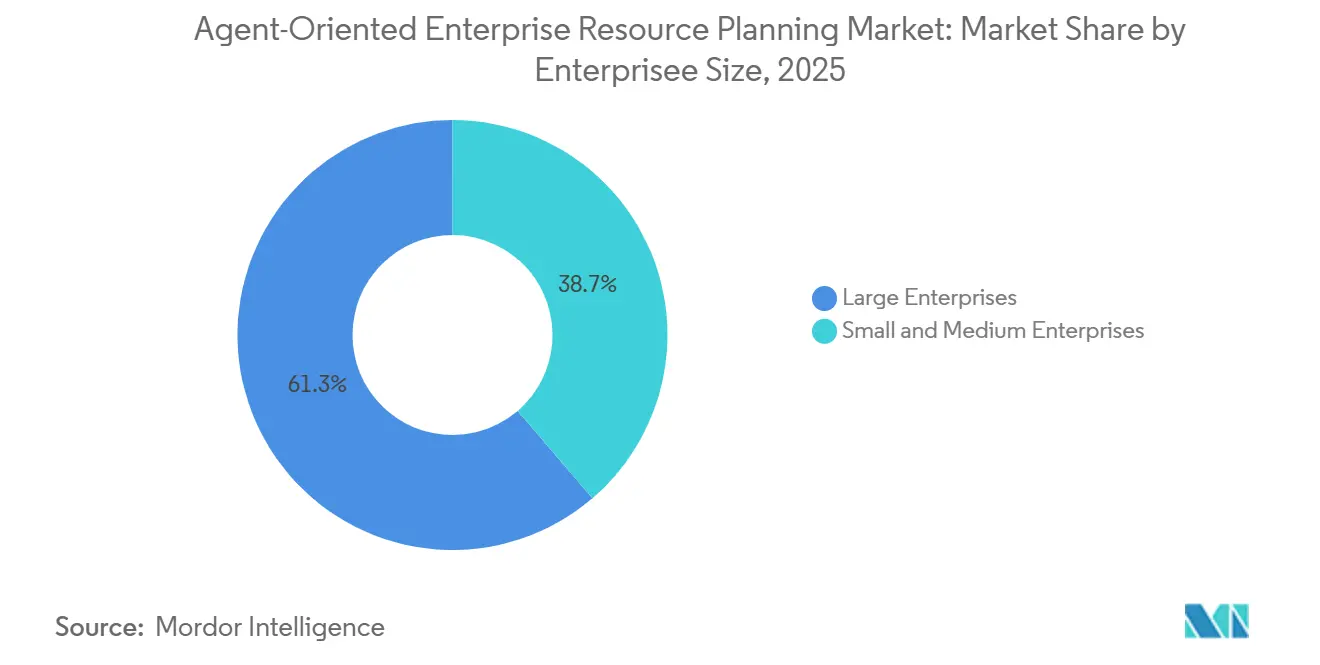

- By enterprise size, large enterprises accounted for 61.29% of spending in 2025, while small and medium enterprises are growing at a 58.73% annual rate.

- By end-user industry, IT and telecom held 26.79% share in 2025, and healthcare and life sciences are registering the fastest 57.33% CAGR to 2031.

- By geography, North America commanded 37.48% revenue in 2025, while Asia-Pacific is set to record a 57.37% CAGR across the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agent-Oriented Enterprise Resource Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Adoption of Autonomous Business Processes | +10.1% | Global with early focus in North America financial services and Asia-Pacific manufacturing | Medium term (2-4 years) |

| Shift Toward Composable Agent-Based Digital Platforms | +9.2% | Global with spill-over from North America and Europe hyperscalers to emerging markets | Medium term (2-4 years) |

| Surge in Edge-to-Cloud Workload Orchestration Demands | +8.8% | Asia-Pacific core, Middle East smart-city programs, North America and Europe industrial IoT | Long term (≥ 4 years) |

| Rising Complexity of Heterogeneous IT Environments | +8.5% | Global, acute in large enterprises that run multi-cloud with legacy systems | Short term (≤ 2 years) |

| Rapid Uptake of Digital Twin-Driven Enterprise Modeling | +8.3% | Europe manufacturing, North America aerospace and defense, Asia-Pacific smart factories | Long term (≥ 4 years) |

| Growing Regulatory Pressure for Explainable AI Governance | +7.9% | European Union, North America sectoral rules, Asia-Pacific mixed regimes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Adoption of Autonomous Business Processes

Enterprises now embed agents that execute end-to-end workflows such as compliance validation, scheduling, and cross-system updates without human initiation, which lowers coordination friction and improves cycle times. A global bank shortened loan processing by integrating agentic orchestration across underwriting and customer-relationship platforms, realizing gains by eliminating manual handoffs rather than workforce cuts. Agents differ from robotic process automation because they plan multi-step actions, self-correct when exceptions arise, and escalate only when confidence falls below policy thresholds. Gulf financial institutions deploy multi-agent orchestration for anti-money-laundering, reducing false positives while retaining human review for high-risk alerts. The resulting productivity gains are pushing boards to formalize AI operating models that define which decisions agents can execute autonomously.

Shift Toward Composable Agent-Based Digital Platforms

Chief information officers consolidate investments around integrated superplatforms that merge applications, data foundations, orchestration layers, and cloud infrastructure for scalable, governed agent deployment. Integrated control planes offering deterministic policy enforcement, audit trails, and cost governance now represent a key differentiator. Enterprises running on unified platforms report 20-30% faster AI outcomes due to reduced integration friction. SAP and Amazon Web Services launched an AI Co-Innovation Program that enables partners to build domain agents for supply-chain optimization and anomaly detection.[1]Herzig, Philipp, “Business AI Innovation Unveiled at SAP TechEd,” SAP News Center, news.sap.com Accenture delivers resiliency agents for utilities while Deloitte builds finance agents for healthcare on the same stack.

Surge in Edge-to-Cloud Workload Orchestration Demands

The spread of industrial IoT sensors requires orchestration across the edge, data centers, and public clouds, requiring agents that weigh latency, bandwidth costs, sovereignty, and compute availability in real time. Chinese manufacturers deploy agents that monitor supplier and port data and then propose rerouting to keep just-in-time schedules. Middleware that supports the Model Context Protocol abstracts API complexity, enabling agents to interact with systems without embedding endpoint logic. SAP is piloting Joule Agents with autonomous robots for field services and warehouse operations, partnering with industrial firms such as Bitzer. Utilities use carbon-aware scheduling agents to shift compute to regions with high renewable energy mix, aligning with sustainability targets.

Rapid Uptake of Digital Twin-Driven Enterprise Modeling

Digital twins now integrate agent reasoning to enable predictive maintenance and scenario modeling. SAP HANA Cloud added Model Context Protocol support so agents can access relational, spatial, and vector data in a single in-memory engine, and will launch an automated knowledge graph engine in 2026 that converts metadata into graphs within minutes. Manufacturers deploy digital twins of production lines, where agents monitor telemetry and trigger parameter adjustments or part orders before faults occur. Aerospace contractors test agent behavior under adversarial conditions in virtual environments to ensure safety before field deployment. Enterprise-architecture vendors now model agent semantics and visualize data flow across these autonomous systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Agent-Oriented Design Skill Sets | -4.1% | Global with higher impact in emerging markets and mid-sized enterprises | Short term (≤ 2 years) |

| Fragmentation of Interoperability Standards | -3.2% | Global with severe friction in multi-vendor projects | Medium term (2-4 years) |

| High Integration Cost with Legacy EA Tooling | -2.8% | North America and Europe large enterprises that hold decades of technical debt | Short term (≤ 2 years) |

| Perceived Security Risks in Distributed Agent Systems | -2.5% | Global, especially BFSI, healthcare, and government | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Agent-Oriented Design Skill Sets

Enterprises struggle to find architects fluent in multi-agent systems, communication protocols, and AI governance, which slows deployment and increases reliance on vendors.[2]TheBlue.ai Team, “Multi-Agent Systems 2026,” theblue.ai ISO 42001 and new job roles, such as Enterprise Agent Architect, require skills not taught in traditional curricula. Emerging markets face brain drain and limited training pipelines, intensifying competition for talent. Vendors answer with low-code tools like SAP Journey Studio, but architectural judgment on escalation policies and risk alignment still requires expert input. Without rapid upskilling, project timelines extend, and governance gaps widen.

Fragmentation of Interoperability Standards

The lack of universally adopted protocols for agent communication and capability discovery raises integration cost and vendor lock-in risk. Model Context Protocol promises unification, but adoption is uneven, leaving enterprises to juggle LangGraph, CrewAI, and vendor-specific frameworks. SAP is collaborating with Amazon Web Services, Google, Microsoft, and ServiceNow on protocol compatibility with full rollout slated for late 2026. IBM positions watsonx Orchestrate as a semantic control plane that bridges diverse agent frameworks, yet competing standards still complicate multi-vendor ecosystems. Until global bodies finalize trustworthy agent standards, enterprises must fund custom adapters and version management, which slows scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type - Simulation Platforms Capture Complex Workflow Modeling Demand

Simulation platforms are the fastest-growing category, expanding at a 57.93% CAGR as organizations stress-test multi-agent behavior before production deployment, while modeling tools retained 42.57% of the agent-oriented enterprise resource planning market share in 2025. The agent-oriented enterprise resource planning market size for simulation platforms is projected to outpace other product types, driven by firms that must validate decision logic against adversarial scenarios. Integrated development environments now ship with pro-code studios and notebooks that connect to LangGraph and CrewAI, allowing developers to configure tool usage and memory scopes. Middleware abstracts REST and GraphQL endpoints, so agents can tap enterprise resource planning and customer relationship management systems without embedded credentials.

A second growth vector is the conversion of traditional diagrams into structured repositories. SAP LeanIX uses computer vision to parse images and populate inventory with applications, data objects, and their dependencies, enabling rapid impact analysis.[3]Sheppard, Neil, “Diagram to Data,” SAP LeanIX Blog, leanix.net Ardoq’s Model Context Protocol server lets agents query live architecture repositories in natural language and retrieve structured answers, which blurs lines between modeling and orchestration. Services revenue is also rising as consulting firms design governance frameworks and integrate agents with legacy systems.

By Deployment Mode - Hybrid Architectures Balance Innovation and Sovereignty

Cloud deployment accounted for 55.32% of revenue in 2025, yet hybrid approaches are forecast to grow at a 57.53% CAGR, as enterprises balance innovation speed with data residency and cost optimization. The agent-oriented enterprise resource planning market size for hybrid environments will expand as the European Union Data Act forces portability and exit strategies. Microsoft Azure supports SAP’s 99.95% service-level agreement, enabling RISE with SAP customers to enhance recovery while maintaining sovereignty. Sovereign cloud spending is set to reach USD 80 billion in 2026, with 20% of workloads shifting to local providers.

On-premises remains essential for classified workloads, particularly in industries such as defense, healthcare, and financial services, where data security and compliance are critical. IBM offers Power Virtual Server for clients that need air-gapped SAP landscapes, ensuring secure environments with migration windows under 90 days. Enterprises increasingly view hybrid models as the default choice for managing regulated data, handling burst compute requirements, and executing cost-controlled batch jobs. This growing reliance on hybrid architectures has led to a rising demand for advanced orchestration layers. These layers enable seamless movement of agents and data across diverse environments while ensuring adherence to governance policies and regulatory standards, thereby addressing the complex needs of modern enterprises.

By Enterprise Size - SMEs Leverage No-Code Builders for Rapid Adoption

Large enterprises accounted for 61.29% of spending in 2025 because they can fund multi-year programs and staff AI operations teams, while small and medium enterprises are expanding at a 58.73% growth rate through 2031. Low-code builders and consumption-based pricing reduce the barrier to entry, enabling SMEs to deploy agents for sales, customer support, and finance without owning AI infrastructure. The agent-oriented enterprise resource planning market share captured by SMEs is growing, as visual authoring in SAP Joule Studio enables business specialists to extend pre-built agents with custom fields and tool calls.

Japanese mid-market firms have reported a significant increase in operational efficiency after adopting agentic AI. Meeting volumes per sales representative have tripled, and support tickets are now resolved within 30 seconds. However, talent scarcity continues to pose a challenge for these firms. To address this issue, vendors are offering bundled solutions that include governance blueprints and role-based access control templates, helping smaller teams mitigate risks effectively. As more success stories emerge from these implementations, investor confidence in the adoption of agentic AI by SMEs is steadily growing, further driving market expansion.

By End-User Industry - Healthcare Agents Accelerate Clinical and Operational Workflows

IT and telecom led with 26.79% share in 2025, driven by advancements in network optimization and autonomous code generation. However, healthcare and life sciences are anticipated to grow at a remarkable 57.33% CAGR through 2031. The increasing adoption of agent-oriented enterprise resource planning in healthcare is driven by its ability to streamline processes such as scheduling, billing, and documentation while ensuring human oversight in critical clinical operations. Deloitte, for instance, utilizes finance agents built on Amazon Bedrock to enhance product mix strategies and improve forecast accuracy for life-science firms, showcasing the potential of such technologies in the sector.

Banks in the Gulf region are implementing multi-agent frameworks to enhance liquidity monitoring and fraud detection processes, significantly reducing false positives. Similarly, manufacturing enterprises are leveraging agents to assess supplier risks and monitor commodity price volatility, enabling them to maintain efficient just-in-time inventory systems. In the energy and utilities sector, carbon-aware scheduling agents are being employed to help organizations meet their sustainability targets effectively. Meanwhile, government agencies are adopting air-gapped agent systems to manage mission-critical workloads securely, adhering to stringent compliance standards such as FedRAMP High and other similar regulatory frameworks.

Geography Analysis

North America accounted for 37.48% of revenue in 2025, driven by mature cloud ecosystems and hyperscaler investments. Enterprises in the United States navigate decades of technical debt, integrating agents with mainframes and on-premises data centers, while embedding explainability and audit controls to meet regulatory scrutiny. SAP and Microsoft launched the Business Suite Acceleration Program that integrates Joule Copilot with Microsoft 365 Copilot, initially in the United States and expanding globally. IBM migrated global quote-to-cash and manufacturing processes to SAP S/4HANA Cloud Private, achieving a 30% reduction in infrastructure costs with 100% availability.

Asia-Pacific is forecast to grow at 57.37% over 2026-2031, propelled by national AI strategies in China, India, Japan, and South Korea.[4]Salesforce, “Great Asia AI Summit 2026,” salesforce.com The Great Asia AI Summit in February 2026 underscored the shift from pilots to scaled, governed agentic models. Japanese startups in Shibuya build multi-agent software-as-a-service, while integrators in Shinagawa cut release cycles from weeks to hours. Manufacturing clusters deploy agents that monitor commodity and port data to adapt sourcing. India and Singapore accelerate adoption across financial services and the public sector by using cloud-native stacks.

Europe follows a governance-first path shaped by the EU AI Act and Data Act, which mandate portability, documentation, and sovereign cloud. Enterprises demand vendor-agnostic orchestration frameworks that embed compliance. SAP Business Data Cloud went live on Microsoft Azure in Switzerland in March 2026, giving customers EU Access and data sovereignty. SAP is expanding European data center capacity by 40% and forming sovereign cloud ventures such as Bleu in France. The Middle East is accelerating agent adoption within national AI strategies focused on smart government and utility optimization. South America and Africa are smaller today, but benefit from vendor programs that target mid-market clients with cloud-native offerings

Competitive Landscape

The agent-oriented enterprise resource planning market remains moderately fragmented. Established vendors like SAP, IBM, Microsoft, and Salesforce bundle orchestration layers deep inside systems of record, which anchor workloads to their ecosystems. Specialist firms, including LeanIX, Ardoq, Avolution, and BiZZdesign, extend modeling tools with AI that convert diagrams to structured data and support conversational queries. Competitive advantage is shifting toward platforms that can ground agents natively in enterprise resource planning, customer relationship management, and IT service management while providing deterministic governance.

Innovation clusters around observability, cost control, and interoperability. IBM claims watsonx Orchestrate supports 80 enterprise systems and 150 pre-built agents across multiple foundation models, positioning it as a semantic control plane for heterogeneous environments. Vendors that embrace open standards such as Model Context Protocol gain favor among buyers wary of lock-in. SAP announced agent-to-agent protocol compatibility with Amazon Web Services, Google, Microsoft, and ServiceNow, which strengthens its role as a cross-vendor orchestrator.

Strategic moves since 2025 include hyperscaler-software alliances, niche orchestrator acquisitions, and developer community incentives. SAP released 40 Joule Agents and 2,100 Joule Skills, while Microsoft and SAP provide a joint 99.95% service-level agreement for SAP Cloud ERP Private on Azure. Start-ups target white spaces in regulatory-heavy sectors like healthcare and energy, offering compliance-by-design agents that integrate legacy data silos. As buyers prioritize augmentation coherence over raw model quality, platforms that orchestrate humans, agents, applications, and data on a single, trusted plane are gaining momentum.

Agent-Oriented Enterprise Resource Planning Industry Leaders

Sparx Systems Pty Ltd.

BiZZdesign B.V.

Avolution Pty Ltd.

Orbus Software Ltd.

BOC Group OOD

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: SAP Business Data Cloud launched on Microsoft Azure in Switzerland, giving customers EU Access with sovereignty and compliance guarantees.

- February 2026: Salesforce hosted the Great Asia AI Summit, highlighting scalable, governed agentic operating models across South Asia and Southeast Asia.

- November 2025: SAP unveiled 40 Joule Agents, Joule Studio, and agent-to-agent protocol compatibility with major cloud vendors at TechEd.

- May 2025: IBM introduced watsonx Orchestrate, supporting 150 pre-built agents and multiple foundation models with an open protocol stance.

Global Agent-Oriented Enterprise Resource Planning Market Report Scope

The Agent-Oriented Enterprise Resource Planning (AOEA) Market refers to the ecosystem of tools, platforms, and services that enable organizations to design, model, simulate, integrate, and manage enterprise architectures based on agent-oriented principles, where autonomous software agents represent business processes, systems, and decision-making entities.

The Agent-Oriented Enterprise Resource Planning Market Report is Segmented by Product Type (Modeling Tools, Integrated Development Environments, Agent-Based Simulation Platforms, Middleware and Integration Software, and Services), Deployment Mode (On-Premises, Cloud, and Hybrid), Enterprise Size (Large Enterprises, Small and Medium Enterprises), End-User Industry (BFSI, Government and Defense, Healthcare and Life Sciences, Manufacturing, IT and Telecom, Energy and Utilities, Retail and e-Commerce, Transportation and Logistics, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Modelling Tools |

| Integrated Development Environments |

| Agent-Based Simulation Platforms |

| Middleware and Integration Software |

| Services |

| On-Premises |

| Cloud |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| Government and Defense |

| Healthcare and Life Sciences |

| Manufacturing |

| IT and Telecom |

| Energy and Utilities |

| Retail and e-Commerce |

| Transportation and Logistics |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Modelling Tools | ||

| Integrated Development Environments | |||

| Agent-Based Simulation Platforms | |||

| Middleware and Integration Software | |||

| Services | |||

| By Deployment Mode | On-Premises | ||

| Cloud | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-user Industry | BFSI | ||

| Government and Defense | |||

| Healthcare and Life Sciences | |||

| Manufacturing | |||

| IT and Telecom | |||

| Energy and Utilities | |||

| Retail and e-Commerce | |||

| Transportation and Logistics | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What growth rate is projected for the agent-oriented enterprise resource planning market between 2026-2031?

The market is forecast to grow at 56.93% CAGR from 2026 to 2031.

Which product category is expanding the fastest through 2031?

Agent-based simulation platforms are advancing at a 57.93% CAGR.

Why are hybrid deployments gaining traction after 2025?

Hybrid balances innovation speed with data residency and cost control, leading to a 57.53% CAGR for the mode.

Which region will be the fastest growing during the forecast period?

Asia-Pacific is set to register a 57.37% CAGR due to national AI strategies and cloud-native adoption.

How are small and medium enterprises adopting agentic architectures?

SMEs use low-code builders and SaaS orchestration layers, driving a 58.73% growth rate in their spending share.

What is the main challenge slowing multi-agent deployments today?

A shortage of skilled professionals in agent-oriented design and governance is the most immediate restraint.

Page last updated on: