Vietnam Tire Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

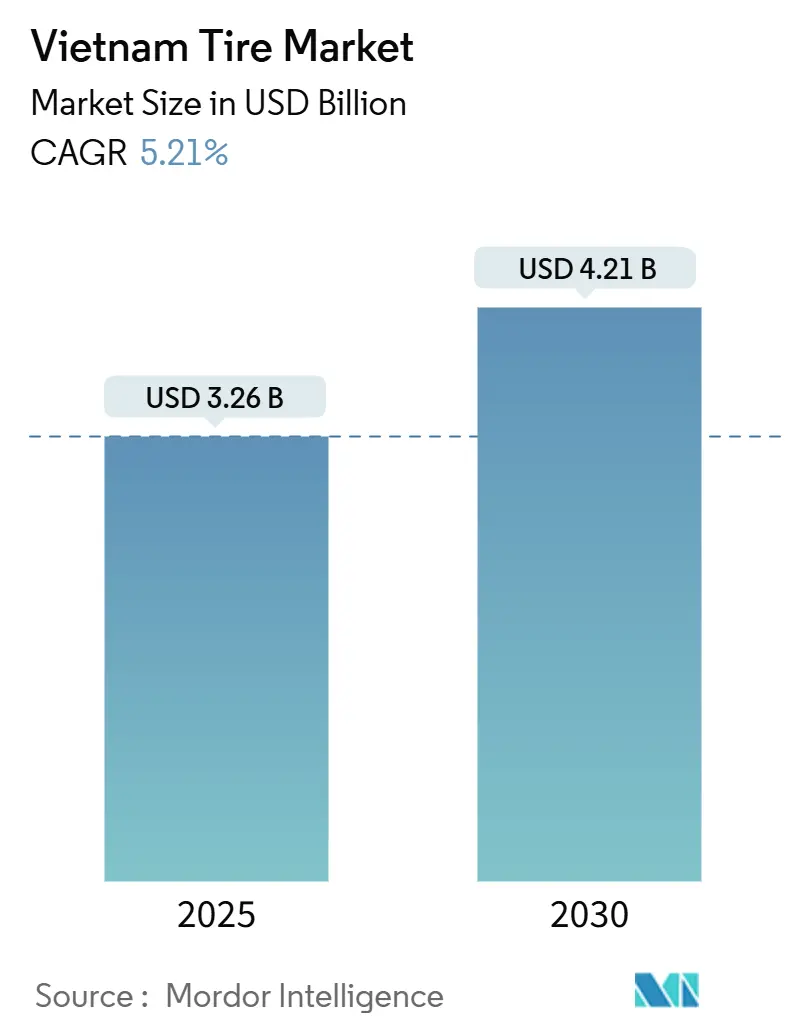

| Market Size (2025) | USD 3.26 Billion |

| Market Size (2030) | USD 4.21 Billion |

| Growth Rate (2025 - 2030) | 5.21% CAGR |

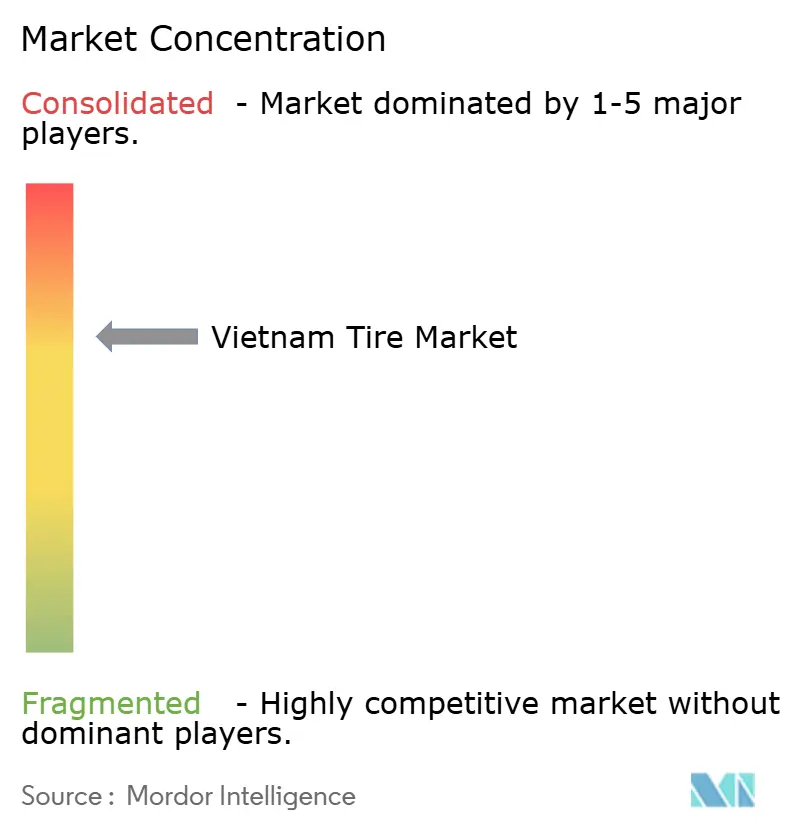

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Tire Market Analysis by Mordor Intelligence

The Vietnam Tire Market size is estimated at USD 3.26 billion in 2025, and is expected to reach USD 4.21 billion by 2030, at a CAGR of 5.21% during the forecast period (2025-2030). Robust domestic demand, natural-rubber availability, and sustained foreign direct investment define the market’s expansion path. Tariff headwinds from key export partners are prompting capacity localization for U.S.-bound product lines, while urbanization propels passenger-car ownership and fuels aftermarket replacement cycles. Government tax holidays for automotive supporting industries through 2027 and industrial-park infrastructure continue to attract Chinese, Korean, and Japanese tire majors. Electrification of two-wheelers and public procurement of low-emission fleets are widening the addressable base for specialized radial and low-rolling-resistance products. Rising e-commerce logistics volumes further lift medium- and heavy-commercial-vehicle fitments, reinforcing radialization momentum across haulage corridors.

Key Report Takeaways

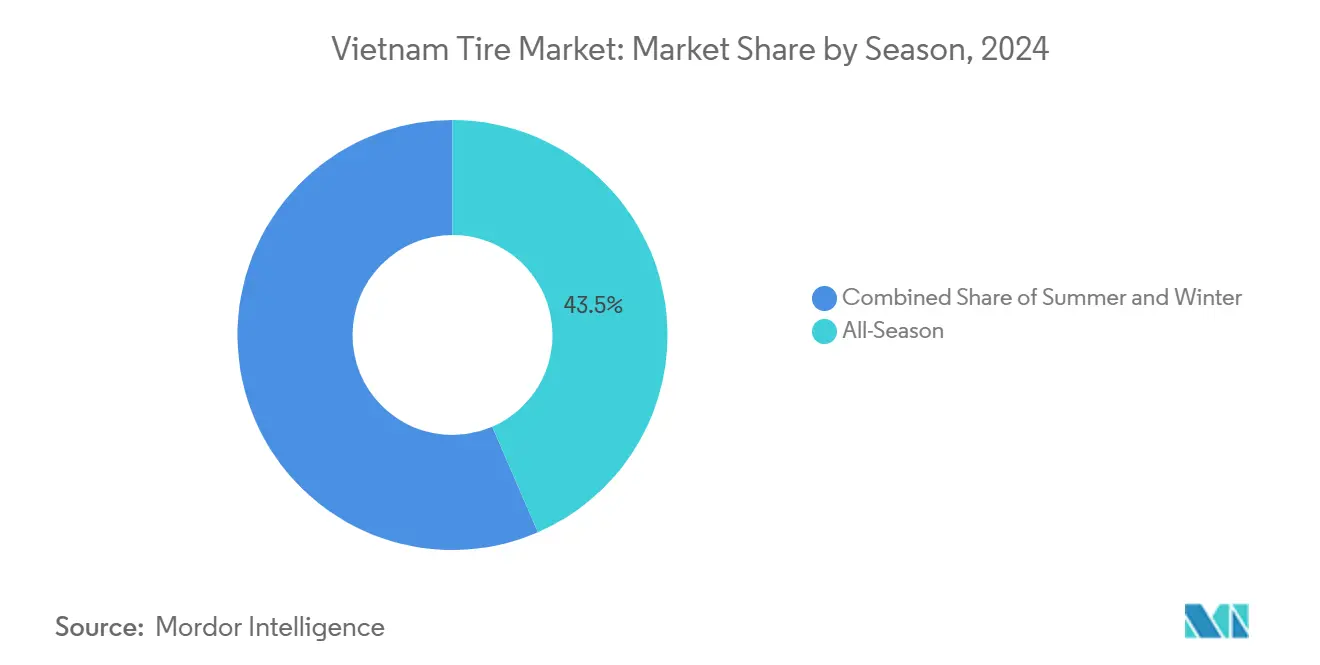

- By season, all-season tires led with 43.47% of Vietnam's market share in 2024, while summer tires are forecast to advance at a 5.23% CAGR through 2030.

- By tire design, radial construction commanded 89.73% of the Vietnam tire market size in 2024 and is set to grow at a 5.32% CAGR to 2030.

- By vehicle type, two-wheelers held 43.35% of the Vietnam tire market share in 2024, while passenger cars recorded the fastest CAGR at 5.27% through 2030.

- By application, on-road tires accounted for 83.12% of the Vietnam tire market size in 2024; off-road fitments are projected to grow at a 5.26% CAGR between 2025 and 2030.

- By end user, the aftermarket contributed 65.51% of the Vietnam tire market size in 2024, whereas OEM channels are projected to post a 5.24% CAGR through 2030.

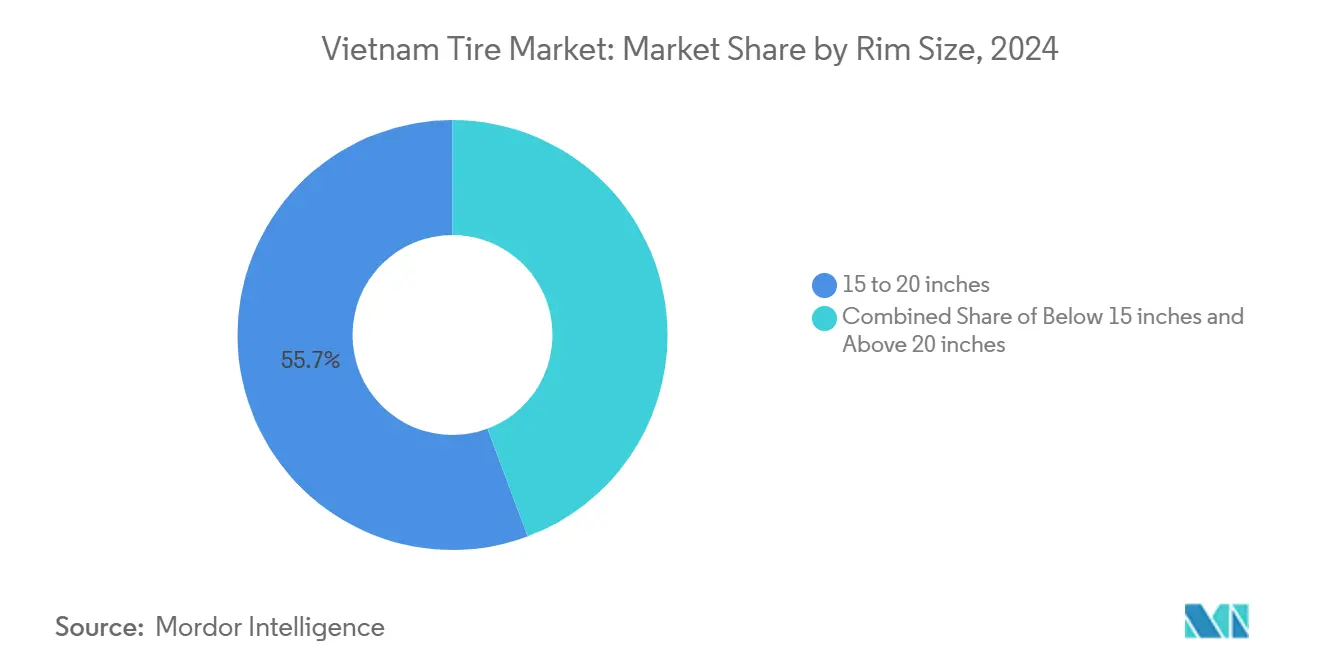

- By rim size, the 15-20-inch segment captured a 55.67% share of the Vietnam tire market in 2024; the above-20-inch category is forecast to expand at a 5.35% CAGR between 2025 and 2030.

- By propulsion, Internal-combustion vehicles had an 87.43% of the Vietnam tire market size in 2024, yet battery-electric fitments will register the highest growth at a 5.28% CAGR through 2030.

Vietnam Tire Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Vehicle PARC | +1.2% | National, concentrated in urban centers | Medium term (2-4 years) |

| Logistics & E-Commerce Boom | +0.9% | National, strongest in Mekong Delta and Red River Delta | Short term (≤ 2 years) |

| Government Incentives | +0.8% | National, focused on industrial zones | Long term (≥ 4 years) |

| Rapid Electrification Of Two-Wheelers | +0.6% | Urban centers, expanding to rural areas | Medium term (2-4 years) |

| Green Public-Sector Procurement Targets | +0.4% | National, government fleet focus | Long term (≥ 4 years) |

| Truck & Bus Radialization Push | +0.3% | National highway corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle PARC & Disposable Income Growth

Vehicle registrations climbed exponentially in 2024, anchoring a growing installed base of multiple units that sustains a steady aftermarket pull. Annual GDP expansion of nearly one-tenth is lifting household purchasing power and shortening replacement intervals, especially for premium branded tires in Hanoi and Ho Chi Minh City. Motorcycles remain the modal choice for new entrants into personal mobility, but passenger-car uptake is accelerating as financing access improves and urban road networks expand. Higher utilization intensifies tread wear, translating into predictable demand for quality replacements across dealer and quick-fit outlets[1]“Vehicle Registration Data 2024,” General Statistics Office, gso.gov.vn.

Logistics & E-Commerce Boom Increasing CV Tire Demand

The gross merchandise value of Vietnamese e-commerce has surged, producing dense urban last-mile fleets and longer intra-regional trunk routes. Each parcel van or refrigerated truck covers dense daily mileage, consuming tires at a faster clip than private cars. Road-building in the North–South Expressway and ongoing highway links to border gates add radially friendly pavement where operators pursue fuel savings. Specialized cold-chain vehicles for seafood exports adopt high-load, low-temperature tread compounds that command premium pricing.

Government Incentives for Domestic Tire Manufacturing

Preferential corporate-income-tax rates and import tariff exemptions on machinery until December 2027 underpin Chinese and Korean capital influxes. Guizhou Tyre’s semi-steel radial facility in Tien Giang and Kumho Tire’s capacity upgrade epitomize the strategy to build Vietnam as a low-cost export springboard amid escalating U.S.–China trade friction[2]“FDI in Automotive Supporting Zones,” Ministry of Planning & Investment, mpi.gov.vn. Streamlined permitting inside Long Hau, Phuoc Dong, and VSIP industrial parks cuts lead times for greenfield plants, while vocational-training grants ensure a skilled operator pool.

Rapid Electrification of Two-Wheelers

Subsidized registration fees and battery-swap infrastructure stimulate the adoption of electric scooters, led by VinFast’s Klara and Feliz models. Instant torque subjects rear tires to elevated wear, while regenerative braking alters contact-patch dynamics, spurring OEM requests for bespoke silica-laden low-rolling-resistance compounds. Ride-hailing and delivery fleets electrify to meet corporate ESG pledges, translating into fleet-level bulk ordering cycles that benefit vendors with tailored service programs[3]“Electric Scooter Portfolio and Battery Swap Network,” VinFast, vinfastauto.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Natural Rubber Price Volatility | -0.7% | National, affecting all manufacturers | Short term (≤ 2 years) |

| Price Competition From Low-Cost Chinese Imports | -0.5% | National, concentrated in price-sensitive segments | Medium term (2-4 years) |

| Extended Producer Responsibility (EPR) Compliance Costs | -0.4% | National, with higher impact on smaller manufacturers | Medium term (2-4 years) |

| Rural Infrastructure Gaps Limiting Off-Take | -0.3% | Rural and remote areas, affecting distribution reach | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Natural Rubber Price Volatility

Despite ranking among the top globally, Vietnam faces plantation aging and erratic rainfall that tightened supply in 2024. The Vietnam Rubber Group’s estate cannot buffer global pricing swings, compelling tire firms to hedge or diversify synthetic-rubber inputs. Sharp raw-material spikes prompt deferred consumer purchases, especially in rural motorcycle segments where price elasticity remains high.

Price Competition from Low-Cost Chinese Imports

Chinese brands leverage vertical integration, lower labor costs, and export-rebate structures to undercut local rivals, particularly in bias-ply truck and budget passenger tiers. Sailun Vietnam already controls two-fifths of export shipments, while Jinyu Vietnam holds one-fifth, squeezing margins for domestic independents. Continuous capacity ramp-ups inside Vietnamese industrial parks blur origin labeling, making price the chief buying criterion among fleet owners.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Season: All-Season Dominance Reflects Climate Pragmatism

All-season tires accounted for 43.47% of the Vietnam tire market share in 2024, whereas summer tires will grow steadily in line with the 5.23% CAGR. Single-pattern convenience aligns with the country’s relatively uniform temperature profile, minimizing storage or changeover costs for motorists. Winter designs remain relegated, addressing mountain-pass buses and cold-storage forklifts where sub-10 °C conditions occasionally occur. For manufacturers, the climate homogeneity simplifies compound portfolios and streamlines distribution inventory.

Consumer education campaigns by premium brands highlight hydroplaning resistance and braking advantages of purpose-engineered summer patterns, nudging gradual substitution away from entry-level all-season SKUs. Da Nang and Can Tho retailers report upselling opportunities tied to monsoon-season safety messaging. The rising car-rental sector prefers higher-speed-rated summer lines to satisfy corporate fleet insurers, introducing new B2B channels with predictable ordering calendars.

By Tire Design: Radial Technology Achieves Near-Universal Adoption

Radials comprised 89.73% of the Vietnam tire market share in 2024 and are on track to grow at a 5.32% CAGR by 2030, due to the mandating of low-emission truck standards. Fleet cost accounting underscores longer retread cycles and lower fuel use, justifying the premium over bias alternatives. OEM fitments have been exclusively radial since 2023, accelerating aftermarket conversion when factory warranties lapse.

Non-pneumatic prototypes showcased by leading brands target urban last-mile vans where puncture downtime proves costly, yet commercial viability remains several years away. Meanwhile, Chinese entrants deploy advanced belt-package radials with graphene or recycled rubber content, adding sustainability credentials that resonate with EPR compliance pressures. Such moves raise the technology bar for domestic second-tier producers aiming to share in budget motorcycle niches.

By Vehicle Type: Two-Wheeler Legacy Meets Passenger-Car Ascendancy

Two-wheelers held 43.35% of the Vietnam tire market share in 2024, whereas passenger cars, contributing with a 5.27% CAGR, underpinned by aggressive dealer finance packages and widening model offerings by VinFast, Hyundai, and Toyota. Vietnam's tire market share for passenger cars will breach two-fifths by 2030 as multi-car households proliferate in second-tier cities.

Light commercial vans and pickups sustain the e-commerce engine, recording almost one-fifth of 2024 sales and tilting toward all-terrain radial designs that tolerate mixed-road conditions. Heavy trucks and buses gain from BRI-linked infrastructure, yet axle-load restrictions cap the proliferation of ultra-heavy-spec vehicles. Specialty off-the-road segments, such as mining trucks and combine harvesters, grow off a small base, presenting higher-margin opportunities for domestic makers that leverage short supply chains to supply plantation clients rapidly.

By Application: On-Road Supremacy with Off-Road Opportunities

On-road fitments contributed 83.12% of the Vietnam tire market share in 2024, aligned with urban commuting and inter-provincial haulage patterns. Continuous lane additions on the Ho Chi Minh City–Long Thanh–Dau Giay route stimulate demand for high-speed highway tread designs featuring low-noise patterning. Though smaller, off-road applications are projected to outpace at a 5.26% CAGR underpinned by mining concessions in Quang Ninh and construction megaprojects like Long Thanh International Airport. Mechanization in rice cultivation, coupled with palm and rubber plantation expansion in the Central Highlands, spreads demand for flotation and paddy-friendly patterns that resist stubble damage.

Tire makers bundling telematics sensors for quarry dumpers report higher uptake as mining contractors strive to curb downtime. Civil-engineering contractors also embrace radial OTR products with cut-resistant compounds to navigate lateritic soils prevalent in infrastructure cut-and-fill operations, widening value streams for suppliers prepared to offer field-side service trucks.

By End User: Aftermarket Strength Signals Mature Replacement Cycles

Aftermarket channels took 65.51% of the Vietnam tire market share in 2024, reflecting the vast installed motorbike and aging truck base that requires recurrent servicing. Independent tire retailers dominate the urban aftermarket, stocking imported Chinese and Thai budget lines alongside premium Japanese and European SKUs. Retail consolidation remains limited, giving wholesalers leverage in price negotiations. OEM share, while smaller, is set for a 5.24% CAGR as localized vehicle assembly gains ground under tariff-reduction schedules of ASEAN trade pacts. Factory-approved tire kits bundled into new-vehicle sales offer makers captive volume, especially as VinFast scales its sedan and SUV output.

EPR obligations push OEM and replacement players to coordinate collection logistics, fostering joint-venture recycling hubs. Brands offering take-back credits or free fitment win consumer goodwill and repeat purchases, reinforcing brand stickiness in premium segments.

By Rim Size: Mid-Range Dominance with Premium Growth

Rims between 15 and 20 inches accounted for 55.67% of the Vietnam tire market share in 2024, corresponding to B-segment sedans, C-segment SUVs, and LCVs. Segment growth mirrors passenger-car sales, keeping pace with the broader CAGR. Above-20-inch tires, despite minimal revenue, are tracking the fastest 5.35% CAGR as affluent consumers purchase imported luxury SUVs and pickups that demand 21 to 24-inch sizes. The sub-15-inch bracket remains relevant mainly to 150cc motorcycles and mini-cars, but will slowly decline as consumers upsize vehicles.

Premium rims necessitate low-profile UHP tires featuring reinforced bead packs and noise-reduction ridges. This opens margin-rich niches for global majors, who can import specialized molds. Domestic producers keen to capture luxury demand invest in multi-cavity presses to support smaller batch runs without sacrificing throughput.

By Propulsion: ICE Dominance Faces Electric Disruption

Internal combustion engine vehicles delivered 87.43% of Vietnam's tire market share in 2024 but will taper to four-fifths by 2030 as electric alternatives scale. Battery-electric vehicles boast the highest 5.28% CAGR, catalyzed by duty exemptions on imported EV parts and state-utility charging-station partnerships. Tire developers respond with extra-load ratings to accommodate battery mass and foam-inlay technology to mitigate drivetrain noise. Hybrid sales, though modest, provide transition volumes that familiarize consumers with low-rolling-resistance tires.

Hydrogen fuel-cell prototypes for intercity buses remain experimental, yet early trials in Hai Phong port corridors hint at future adoption where long range and quick refueling are critical. Manufacturers engaging early in hydrogen-ready tire testing will secure engine-OEM approvals before commercialization.

Geography Analysis

The Vietnam tire market derives significant revenue from the southeast and Red River Delta economic zones, which have dense populations and extensive road networks. Ho Chi Minh City leads retail sales owing to the largest registered vehicle parc, while Hanoi follows closely with rising premium-SUV penetration. Central coastal provinces, benefiting from tourism and industrial parks, inject incremental demand through airport transfers and construction fleets. The Mekong Delta, Vietnam’s rice bowl, necessitates unique rice-harvester flotation tires alongside rising LCV fitments that shuttle produce to river ports.

Mountainous northern provinces remain underserved due to sparse dealership coverage; however, government investments under the National Target Program for Socio-Economic Development of Ethnic Minorities are upgrading road access, unlocking latent replacement sales. Cross-border trucking via Lang Son and Lao Cai contributes continuous wear-and-tear demand on long-haul radials, and customs-bonded zones host transshipment fleets that consume international-spec tires.

Natural-rubber plantations cluster in Binh Phuoc and Tay Ninh, granting proximal supply advantages to nearby plants, yet exposing production to localized droughts. Flood mitigation projects along the Mekong promise improved all-season roadability, favoring journey-time-sensitive logistics operators who prioritize premium radials. Export-oriented factories along the south-central coast leverage seaport proximity at Cai Mep-Thi Vai to dispatch containers to North America. However, almost half of the U.S. antidumping duties instituted in April 2025 compel strategic shipping route adjustments to Europe or ASEAN neighbors.

Competitive Landscape

The Vietnam tire market exhibits a moderate concentration, with the top five exporters holding significant outbound volume. Sailun Vietnam leads in export share, leveraging economies of scale and an integrated synthetic rubber line. Jinyu Vietnam and Bridgestone Vietnam follow just behind, specializing in premium radial truck and passenger categories. Kumho’s expansion reinforces the Korean presence and provides original-equipment supply to Hyundai and Kia assembly plants.

Domestic brands capitalize on proximity to latex feedstock and lower logistics costs to defend motorcycle and agricultural niches. Casumina and DRC Tire allocate R&D budgets toward retreadable truck casings and specialty OTR compounds, differentiating on adaptability to Vietnamese road and climate idiosyncrasies. Strategic clustering within Dong Nai and Hai Duong industrial zones facilitates supplier collabs, while EPR compliance sharing reduces collection overheads for smaller players.

Innovative footholds emerge in sustainable materials. Bridgestone Vietnam pilots recycled carbon-black integration, and Sailun tests liquid-phase mixing of silica that reduces energy consumption by two-fifths. Partners such as VinES battery unit explore joint ventures to co-develop low-rolling-resistance compounds tailored for VinFast EV chassis. As tariff regimes shift, firms diversify export portfolios toward Canada, the EU, and the Middle East to mitigate U.S. risk exposure.

Vietnam Tire Industry Leaders

Bridgestone Corporation

Michelin SCA

Goodyear Tire & Rubber Company

Continental AG

Yokohama Rubber Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: Vietnam enacted Extended Producer Responsibility rules mandating a 5% tire-recovery rate, compelling manufacturers to finance collection and recycling systems.

- March 2024: Via Advance Tyre Vietnam, Guizhou Tire invested USD 227.8 million in a Tien Giang plant, targeting the export of 6 million semi-steel radials annually.

- March 2024: Sumitomo Corporation signed an MoU with Green and Smart Mobility Joint Stock Company to co-develop electric-mobility services and infrastructure in Vietnam.

Vietnam Tire Market Report Scope

| Summer |

| Winter |

| All-Season |

| Radial |

| Bias |

| Non-pneumatic / Airless |

| Two-Wheelers |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Trucks & Buses |

| Off-the-Road & Specialty (OTR, Agriculture, Mining, Racing) |

| On-Road |

| Off-Road |

| OEM |

| Aftermarket |

| Below 15 inches |

| 15 – 20 inches |

| Above 20 inches |

| Internal-Combustion Vehicles |

| Battery-Electric Vehicles |

| Hybrid & Fuel-Cell Vehicles |

| By Season | Summer |

| Winter | |

| All-Season | |

| By Tire Design | Radial |

| Bias | |

| Non-pneumatic / Airless | |

| By Vehicle Type | Two-Wheelers |

| Passenger Cars | |

| Light Commercial Vehicles | |

| Heavy Commercial Trucks & Buses | |

| Off-the-Road & Specialty (OTR, Agriculture, Mining, Racing) | |

| By Application | On-Road |

| Off-Road | |

| By End User | OEM |

| Aftermarket | |

| By Rim Size | Below 15 inches |

| 15 – 20 inches | |

| Above 20 inches | |

| By Propulsion | Internal-Combustion Vehicles |

| Battery-Electric Vehicles | |

| Hybrid & Fuel-Cell Vehicles |

Key Questions Answered in the Report

How large is the Vietnamese tire market in 2025?

Vietnam's tire market reached USD 3.26 billion in 2025 and is projected to grow at a 5.21% CAGR by 2030.

Which vehicle segment is expanding faster due to tire demand?

Passenger-car fitments are rising at a 5.27% CAGR through 2030, the quickest among all vehicle types.

What share do radial tires hold in Vietnam?

Radial construction accounted for 89.73% of the Vietnam tire market share in 2024 and continues to edge higher as bias-ply replacement accelerates.

How do new EPR regulations affect manufacturers?

From January 2024, producers must recycle at least 5% of annual volumes, adding collection and processing costs but opening circular-economy business avenues.

Which region contributes the most to tire demand?

Southeast economic zones anchored by Ho Chi Minh City generate the highest sales, driven by the largest vehicle parc and dense logistics traffic.

What is driving growth in above 20-inch rim sizes?

Rising premium-SUV and luxury-pickup ownership among affluent households propels the above-20-inch category at a 5.35% CAGR.

Page last updated on: