Poland Pet Veterinary Diets Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

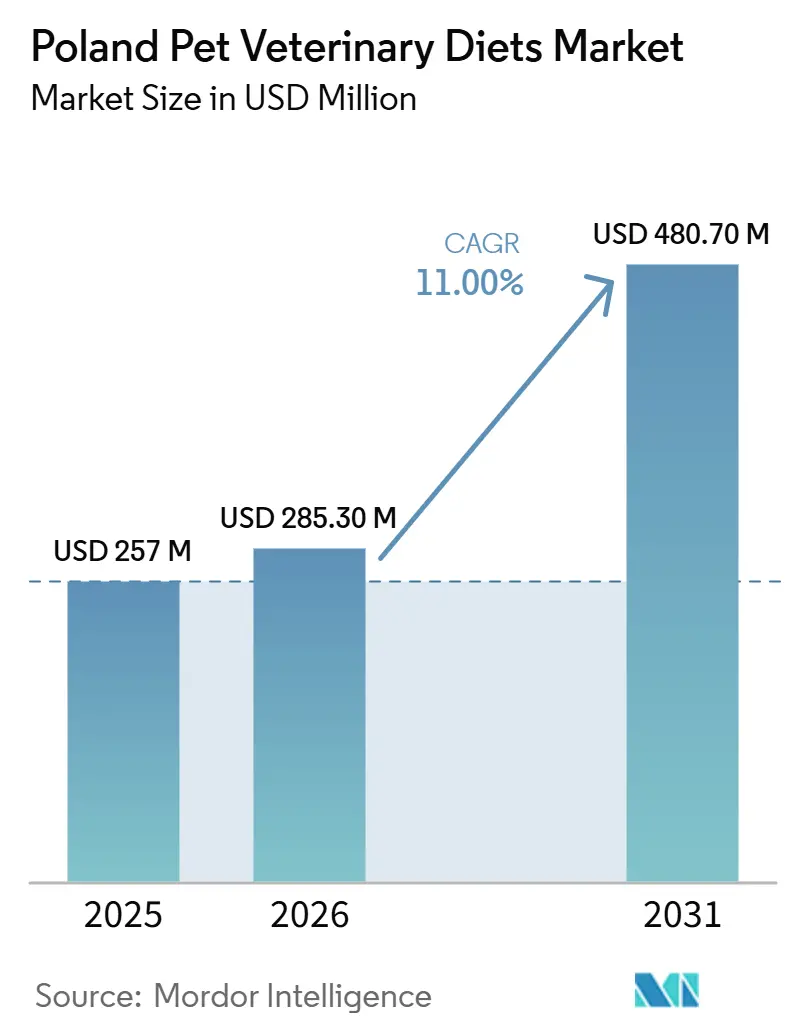

| Base Year Market Size (2025) | USD 257 Million |

| Market Size (2026) | USD 285.30 Million |

| Market Size (2031) | USD 480.70 Million |

| Growth Rate (2026 - 2031) | 11.00% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Pet Veterinary Diets Market Analysis by Mordor Intelligence

The Poland Pet Veterinary Diets Market size was valued at USD 257 million in 2025 and is estimated to grow from USD 285.30 million in 2026 to reach USD 480.70 million by 2031, at a CAGR of 11% during the forecast period (2026-2031). The Poland pet veterinary diets market is growing due to a substantial pet population, increased clinical involvement, and a shift toward condition-specific nutrition integrated into pet care rather than being viewed as a discretionary purchase. The pet food market in Poland provides a solid foundation, and domestic production increased by 21% during 2024, supporting product availability, manufacturing confidence, and distribution depth. In 2024, Poland had over 8.4 million dogs and more than 7.5 million cats, offering a significant base for long-term therapeutic feeding as diagnosis rates improve[1]Source: European Pet Food Industry Federation, “European Pet Food Industry Facts and Figures 2024,” FEDIAF, fediaf.org. Market leaders are driving growth through product innovation, veterinary education, and local investments. However, challenges such as price sensitivity, inconsistent adherence outside major urban areas, and slower adoption of newer ingredient systems continue to moderate the pace of expansion.

Key Report Takeaways

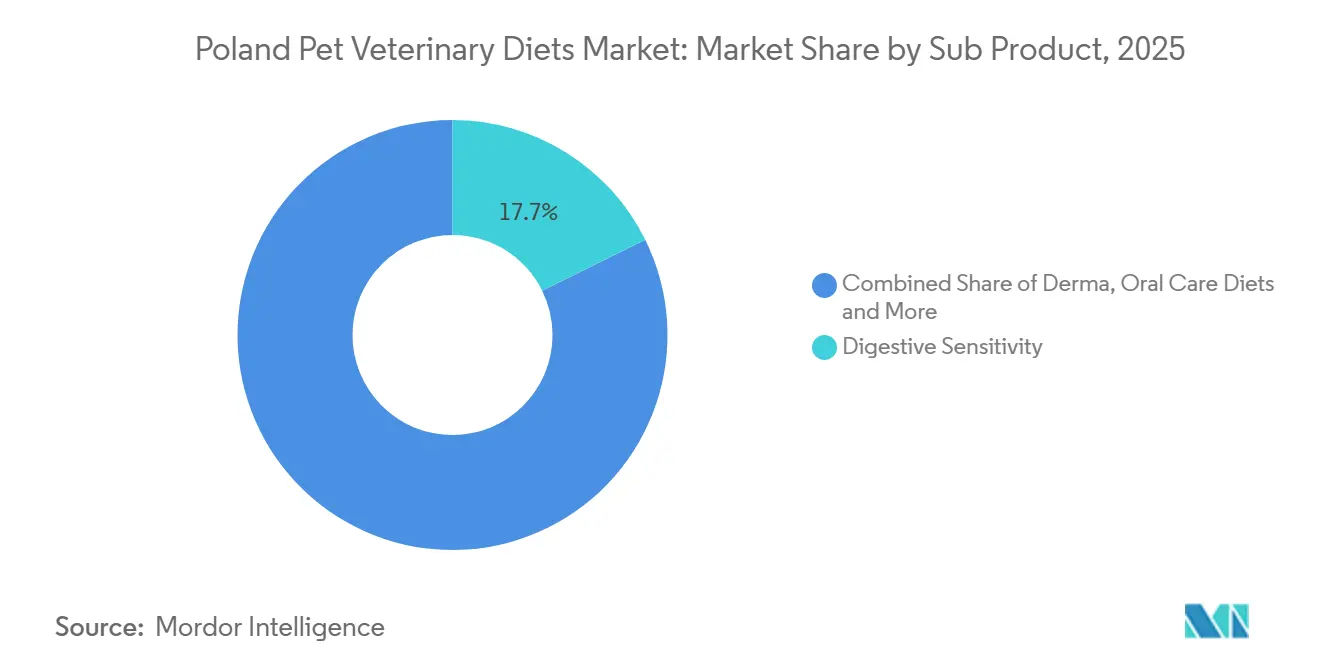

- By sub product, digestive sensitivity led with 17.7% revenue share in 2025, while oral care diets are projected to grow at a 9.0% CAGR through 2031.

- By pets, dogs held 53.2% of the Poland pet veterinary diets market share in 2025, while dogs recorded the highest projected CAGR at 9.7% through 2031.

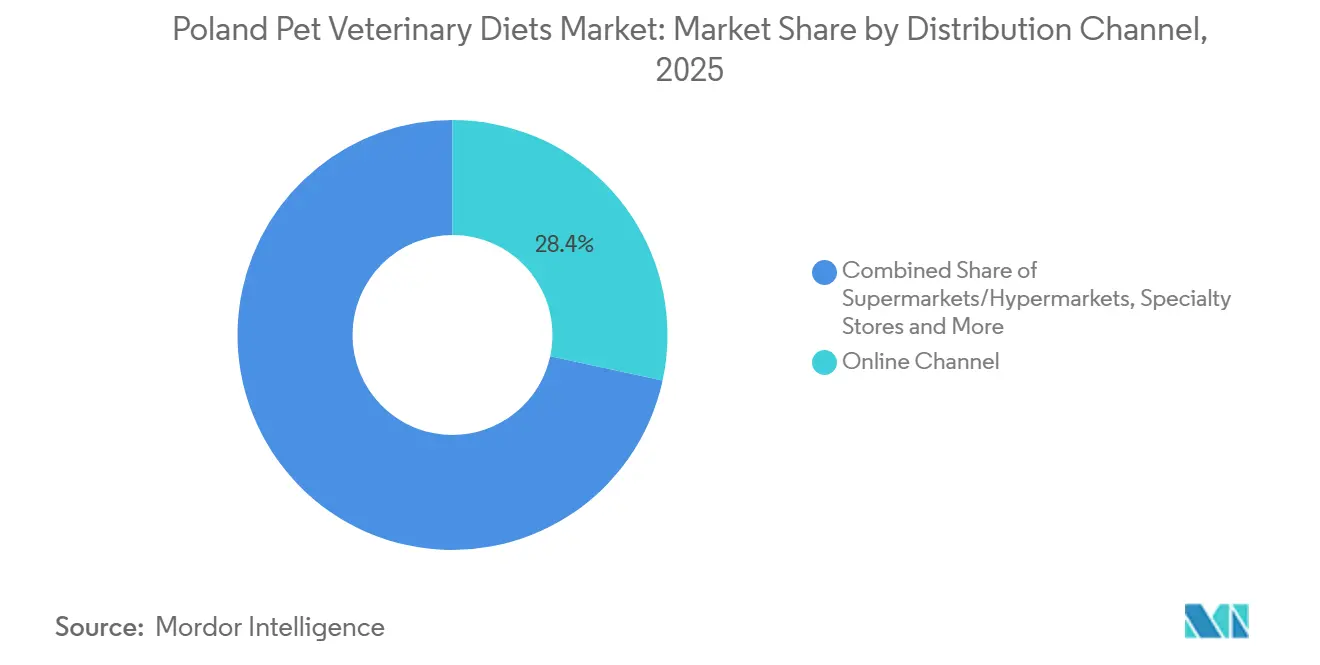

- By distribution channel, the online channel accounted for 28.4% share of the Poland pet veterinary diets market size in 2025 and is advancing at a 10.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Poland Pet Veterinary Diets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Premiumization and Veterinary Grade Product Preference | +2.8% | National, with strongest concentration in Warsaw, Kraków, Wrocław, and the Tri-City area | Medium term (2-4 years) |

| Expansion of Clinic Driven Functional Nutrition Recommendations | +2.5% | National, with higher intensity in urban areas where clinic density is greatest | Short term (≤ 2 years) |

| Growth of Online Refill and Subscription Purchases | +2.1% | National, with highest penetration in large cities and digitally active households | Short term (≤ 2 years) |

| Higher Diagnosis Rates for Chronic Pet Conditions | +1.8% | National, expanding into secondary cities as diagnostics improve | Medium term (2-4 years) |

| Wider Retail Visibility for Specialized Diets | +1.4% | National, led by major urban retail corridors | Medium term (2-4 years) |

| Early Adoption of Sustainable Novel Proteins in Therapeutic Diets | +0.7% | National, initially concentrated in specialty and online channels | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Premiumization and Veterinary Grade Product Preference

The Poland pet veterinary diets market is experiencing growth due to a shift toward products associated with measurable health outcomes. Pet owners are increasingly adopting therapeutic feeding as part of treatment plans for chronic conditions. This shift positions these products as less comparable to mainstream pet food and more aligned with clinical needs. For example, Royal Canin’s VMX 2026 therapeutic nutrition initiative demonstrated how suppliers are focusing on structured care and post-diagnosis support. Similarly, Hill's Pet Nutrition Inc. expanded its prescription product portfolio with new condition-specific launches, emphasizing higher-value formulations with a clear medical focus. This trend benefits the Poland pet veterinary diets market by fostering more resilient repeat purchase decisions, as diets linked to disease management hold greater importance than standard premium feeding. Additionally, it enables leading brands to maintain pricing levels, as owners prioritize continuity of care over ingredient quality alone.

Expansion of Clinic Driven Functional Nutrition Recommendations

The Poland pet veterinary diets market continues to rely significantly on veterinarians to translate diagnoses into long-term dietary solutions. When a clinician recommends a specific therapeutic formula, pet owners are generally less inclined to switch diets without further professional advice. According to the updated ACVIM consensus on canine chronic inflammatory enteropathy, in 2024, 38% of affected dogs respond positively to dietary adjustments, underscoring the importance of therapeutic diets in managing digestive health[2]Source: American College of Veterinary Internal Medicine, “Updated Consensus on Canine Chronic Inflammatory Enteropathy,” ACVIM, acvim.org. Digestive conditions remain one of the most common clinical reasons for diet-based interventions. For instance, Farmina Pet Foods' distribution agreement with MWI Animal Health, announced in July 2025, highlights how suppliers are prioritizing clinical channels for therapeutic diet distribution over standard retail strategies. Similarly, VAFO Group strengthened its focus on this approach by organizing the first Brit Nutrition Conference in Poland, which brought together veterinarians, technicians, and students for a structured clinical nutrition forum. The market benefits from this strategy, as trust in veterinary recommendations fosters stronger product adherence than mass advertising.

Growth of Online Refill and Subscription Purchases

The Poland pet veterinary diets market is growing due to improved access to refills, which have become more reliable and convenient. Pets with chronic conditions often require consistent formulations over extended periods, making uninterrupted resupply nearly as important as the initial prescription. Digital ordering minimizes the risk of owners discontinuing purchases due to local unavailability or limited stock at the clinics. In 2024, Nestlé Purina made its entire Pro Plan Veterinary Diets portfolio available on Amazon, reflecting a broader shift toward direct and repeat online access for prescription nutrition. Similarly, Farmina Pet Foods supported home-delivery options to facilitate the replenishment of therapeutic diets following diagnosis. These developments benefit the Poland pet veterinary diets market by leveraging digital convenience to extend diet adherence and improve household retention. Additionally, they help reduce disparities in access between urban and non-urban areas, although regional differences in counseling quality persist.

Higher Diagnosis Rates for Chronic Pet Conditions

The Poland pet veterinary diets market is benefiting from an increasing number of diagnosed cases across conditions such as digestive, renal, urinary, endocrine, dental, and obesity-related issues. Improved veterinary practices, including enhanced routine screening and diagnostic procedures, are enabling earlier treatment initiation and prolonged management programs for pets. The ENOVAT guidance published in 2024 discouraged the routine use of antibiotics for canine acute diarrhea, emphasizing dietary management as the primary intervention. This development underscores the growing importance of therapeutic nutrition in gastrointestinal care. Early diagnosis is particularly significant as it fosters long-term dietary management rather than short-term acute treatment. Poland's substantial pet population further supports this trend, with over 8.4 million dogs and more than 7.5 million cats reported in 2024. Additionally, the launch of Vikaly by Virbac in Europe in 2025 highlights the growing specialization in diet therapy and prescription treatments, particularly in feline renal care. Consequently, the Poland pet veterinary diets market is driven not only by the growth in pet ownership but also by a rising diagnosis rate per animal.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium Price Sensitivity in Mass Market Households | -2.4% | National, with strongest drag in rural areas and lower-income urban districts | Short term (≤ 2 years) |

| Limited Veterinary Prescription Compliance in Non-Urban Areas | -1.8% | Rural Poland and smaller secondary cities with lower clinic density | Long term (≥ 4 years) |

| Home Prepared Diet Substitution Among Cost Conscious Owners | -1.0% | National, with highest incidence in households managing large breeds with chronic conditions | Medium term (2-4 years) |

| Uncertainty Around Novel Ingredient Acceptance and Labeling | -0.6% | National, affecting new therapeutic formulations entering specialty and online channels | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium Price Sensitivity in Mass Market Households

The clearest restraint on the Poland pet veterinary diets market is the price gap between therapeutic products and standard pet food. Chronic-condition diets can remain outside the comfort range of many mass-market households, especially when the feeding plan must continue for months or years. The issue is not that owners reject the medical logic of therapeutic nutrition. The problem is that cost pressure returns after the first purchase and often after the first visible health improvement. This can lead to partial compliance, delayed repeat orders, or full return to cheaper mainstream alternatives. The Poland pet veterinary diets market is exposed because its strongest value lies in sustained use and not in one-time trial. The same pressure is likely to be more visible outside premium urban clusters, where household budgets are tighter and clinic reinforcement is weaker. Until affordability improves through pack architecture, clearer value communication, or stronger follow-up support, price sensitivity will remain a structural drag on market expansion.

Limited Veterinary Prescription Compliance in Non-Urban Areas

The Poland pet veterinary diets market faces challenges related to geographic disparities outside major cities. Smaller towns and rural areas often have lower clinic density, limited access to specialty care, and less consistent nutritional follow-up after initial diagnoses. This can result in pet owners accepting prescribed diets at clinics but failing to maintain long-term adherence to the recommended products. This issue is particularly significant in conditions such as renal, digestive, and urinary disorders, as well as in obesity management, where consistent dietary compliance is essential for achieving desired outcomes. While online ordering has improved physical access to these products, it cannot fully substitute for ongoing professional guidance. Consequently, the market is more developed in metropolitan areas, where diagnosis, education, and refill support are more effectively integrated. Until support systems in non-urban areas become more robust, compliance challenges in these regions will continue to limit the market's overall growth at the national level.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Product: Digestive Health Higher Share of the Market While Oral Care Grows Fastest

Digestive sensitivity accounted for 17.7% of the Poland pet veterinary diets market size in 2025, making it the largest sub-product segment. This dominance is attributed to the high prevalence of gastrointestinal disorders and the critical role of diet in first-line management. According to the ACVIM consensus, in 2024, 38% of dogs with chronic inflammatory enteropathy respond positively to food-based treatments, underscoring the clinical importance of digestive therapeutic diets. In 2024, Royal Canin strengthened this segment by introducing five new gastrointestinal diets, including a Hydrolyzed Protein Feline formula designed for long-term management.

Renal diets continue to be a significant segment in the Poland pet veterinary diets market due to the high incidence of chronic kidney disease in senior cats, which necessitates consistent long-term feeding solutions. Meanwhile, oral care diets are projected to grow at a CAGR of 9.0% through 2031, making them the fastest-growing sub-product category. Virbac’s 2024 reformulation of Veterinary HPM Small and Toy introduced an oral health component targeting plaque, tartar, and gum inflammation, supporting the category’s evolution toward specialized dental care[3]Source: Virbac, “Virbac Reformulates Veterinary HPM Small and Toy with Oral Health Ingredients,” Virbac, virbac.com.

Companies such as Hill's Pet Nutrition Inc. and Mars Incorporated are driving a shift toward multi-condition therapeutic diets, as evidenced by recent product launches addressing kidney, dermatological, gastrointestinal, diabetes, and weight-management care. This trend reflects the Poland pet veterinary diets market's transition from a narrow focus on staple conditions to a more comprehensive clinical portfolio with precise applications.

By Pets: Dogs Drive Volume While Cats Hold High-Value Clinical Niches

Dogs accounted for 53.2% of the Poland pet veterinary diets market share in 2025, driven by their larger population and higher treatment volumes for long-term conditions. Poland had over 8.4 million dogs in 2024, underscoring the centrality of canine therapeutic care to overall demand. Additionally, dogs are projected to grow at a 9.7% CAGR through 2031, supporting continued investment in diet lines targeting digestive, obesity, musculoskeletal, endocrine, and renal conditions. In 2026, Mars Incorporated emphasized the clinical importance of weight management by renewing its partnership with the University of Tennessee Veterinary Obesity Center.

Cats remain critical to driving demand for renal and urinary diets. Their significance in the Poland pet veterinary diets market is particularly notable in managing chronic kidney disease, diabetes, and multi-condition treatments that require precise formulations and long-term adherence. Virbac’s 2025 launch of Vikaly marked a significant advancement in feline therapeutic care by integrating a renal diet with an active pharmaceutical ingredient under EU Regulation 2019/4. Royal Canin and Purina further enhanced their relevance in feline care by introducing new products targeting diabetes, gastrointestinal, dermatological, and staged renal conditions. While other pets represent a smaller segment of the Poland pet veterinary diets market, the category is gradually expanding as veterinary guidance increasingly extends beyond dogs and cats.

By Distribution Channel: Online Leads Scale While Specialty Stores Retain Guidance

The online channel accounted for a 28.4% share of the Poland pet veterinary diets market size in 2025 and is projected to grow at a CAGR of 10.6% through 2031. This combination of current market share and anticipated growth highlights the importance of digital access for long-term compliance. The Poland pet veterinary diets market benefits from the need for chronic-condition pets to have consistent access to specific formulas, with online channels reducing barriers to refills. Purina’s complete Pro Plan Veterinary Diets listing on Amazon in 2024 exemplifies this broader shift toward reliable and repeatable digital supply through platforms.

Specialty stores remain significant as many pet owners seek guidance and reassurance when transitioning to a prescribed feeding program. This is particularly relevant in the Poland pet veterinary diets market, where products addressing digestive, renal, urinary, and multi-condition needs often require more detailed discussion compared to mainstream pet food options. While supermarkets and hypermarkets raise awareness of premium products, they play a less critical role in therapeutic conversions than digital and specialty channels. Convenience stores and other outlets primarily serve as supplementary points for top-up purchases rather than structured disease-management solutions. As a result, the category is increasingly shifting toward digital channels, while specialty stores continue to provide essential support for first-time purchases and product understanding.

Geography Analysis

The country has significant potential, as its broader pet food market is already growing on a robust foundation. According to the Polish Ministry of Economic Development and Technology, Poland's pet food market reached nearly PLN 5 billion (approximately USD 1.27 billion) in 2024, supported by a 21% increase in domestic production. The Ministry, based on data from Statistics Poland (GUS), also reported that dog and cat food exports totaled PLN 9.6 billion (approximately USD 2.44 billion) in 2024, reinforcing Poland's position as one of Europe's leading pet food manufacturing and export hubs. This production capacity supports the Poland pet veterinary diets market by enhancing supply flexibility and encouraging local investment.

Urban concentration remains the most prominent structural driver of demand in the Poland pet veterinary diets market. Cities such as Warsaw, Kraków, Wrocław, Poznań, and the Tri-City area benefit from higher purchasing power, greater clinic density, and stronger engagement with premium pet care. As a result, therapeutic adoption is more advanced in these metropolitan areas compared to smaller towns. VAFO Group’s veterinary conference initiatives in Poland and its investments in wet food manufacturing underscore the importance of bolstering clinical and production infrastructure near these high-demand urban corridors. This urban dominance is anticipated to continue throughout the forecast period.

Rural areas and smaller secondary cities in Poland still present the largest structural challenges. While product access is improving through e-commerce, clinic follow-up and nutrition counseling remain inconsistent outside major urban centers. This limits adherence and makes the Poland pet veterinary diets market more reliant on digital refill systems in non-urban regions. Although penetration is estimated to improve gradually, it is likely to remain below the levels seen in large cities, where diagnosis, product availability, and premium product acceptance are already more established.

Competitive Landscape

The Poland pet veterinary diets market is moderately concentrated, with the top five players being Mars, Incorporated, Nestlé S.A. (Purina), Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), VAFO Group, and Farmina Pet Foods. These companies compete by leveraging veterinary trust, clinical evidence, broad condition coverage, and robust compliance support across digital and clinic channels. Hill’s strengthened its position in 2026 with the introduction of k/d + Derm Complete and k/d + z/d Hydrolyzed, expanding its multi-condition prescription offerings. Mars Incorporated enhanced its therapeutic standing through scientific contributions, with Mars Veterinary Health citing over 500 peer-reviewed publications in its 2025 science impact report. Purina continued to build its position with new launches focused on digestive and senior support, alongside ongoing research into microbiome-linked veterinary nutrition.

Regional challengers maintain relevance by focusing on specific areas rather than offering a broad product range. VAFO Group is bolstering its position through veterinary engagement, product range expansion, and investments in local production. Farmina Pet Foods enhanced its clinical profile by expanding distribution and introducing digital adherence tools such as Genius AI. Virbac occupies a unique position, as its Vikaly brand operates in the space between therapeutic nutrition and prescription medicine.

Barriers to entry in the Poland pet veterinary diets market remain high due to the need for clinical credibility, strong veterinary relationships, and a reliable refill strategy. Leading companies do not compete solely on product formulations but they also invest in education, manufacturing capabilities, and compliance support systems. This approach keeps the market dynamic and innovative but favors established participants with existing evidence, scale, and professional trust.

Poland Pet Veterinary Diets Industry Leaders

Mars Incorporated

Nestle S.A. (Purina)

Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

VAFO Group

Farmina Pet Foods

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Colgate-Palmolive Company (Hill's Pet Nutrition Inc.) launched k/d + Derm Complete and k/d + z/d Hydrolyzed prescription diets for dogs and cats, combining kidney management with ActivBiome+ Kidney Defense technology and either dermatological or gastrointestinal support, the first dual-indication therapeutic formulations of this type in the company's product history

- April 2026: Nestlé Purina PetCare launched Pro Plan AdvantEDGE, a probiotic-supported line including Adult Digestive Support+ and Senior Support+ for dogs and cats, targeting the gut health segment with a clinically validated microbial strain approach.

- April 2026: Colgate-Palmolive Company (Hill's Pet Nutrition Inc.) launched Prescription Diet Metabolic + j/d for cats, addressing simultaneous weight management and joint mobility in a single therapeutic formulation and reducing the number of separate dietary interventions an owner must manage for a multi-condition patient

Poland Pet Veterinary Diets Market Report Scope

Pet veterinary diets (also known as therapeutic or prescription diets) are specialized, scientifically formulated pet foods designed to treat, prevent, or manage specific medical conditions.

The Poland pet veterinary diets market report is segmented by sub product (Diabetes, Renal, Urinary Tract Disease, Digestive Sensitivity, Oral Care Diets, Derma Diets, Obesity Diets, and Others), by pets (Cats, Dogs, and Other Pets), by distribution channel (Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets, and others). The market forecasts are provided in terms of value (USD) and volume (metric tons).

| Milk Bioactives |

| Omega-3 Fatty Acids |

| Probiotics |

| Proteins and Peptides |

| Vitamins and Minerals |

| Other Pet Nutraceuticals |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| By Sub Product | Milk Bioactives |

| Omega-3 Fatty Acids | |

| Probiotics | |

| Proteins and Peptides | |

| Vitamins and Minerals | |

| Other Pet Nutraceuticals | |

| By Pets | Cats |

| Dogs | |

| Other Pets | |

| By Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

Key Questions Answered in the Report

What is the projected value of pet veterinary diets in Poland by 2031?

The market is forecasted to reach USD 480.7 million by 2031.

Which sub product leads demand in Poland?

Digestive sensitivity led with 17.7% of revenue in 2025, supported by the strong role of gastrointestinal disorders in clinical nutrition demand.

Which pet type contributes the most revenue?

Dogs led with 53.2% share in 2025 due to its large pet population in the country and higher awareness for prevention of diseases.

What is slowing broader therapeutic diet adoption across Poland?

The main limits are premium price sensitivity, weaker non-urban compliance, home-prepared substitution, and slower acceptance of novel ingredient systems.

Why is online distribution important for therapeutic diets?

Online channels improve refill continuity, widen access, and support longer compliance for pets on chronic-condition feeding plans.

Page last updated on: