Indonesia Pet Veterinary Diets Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

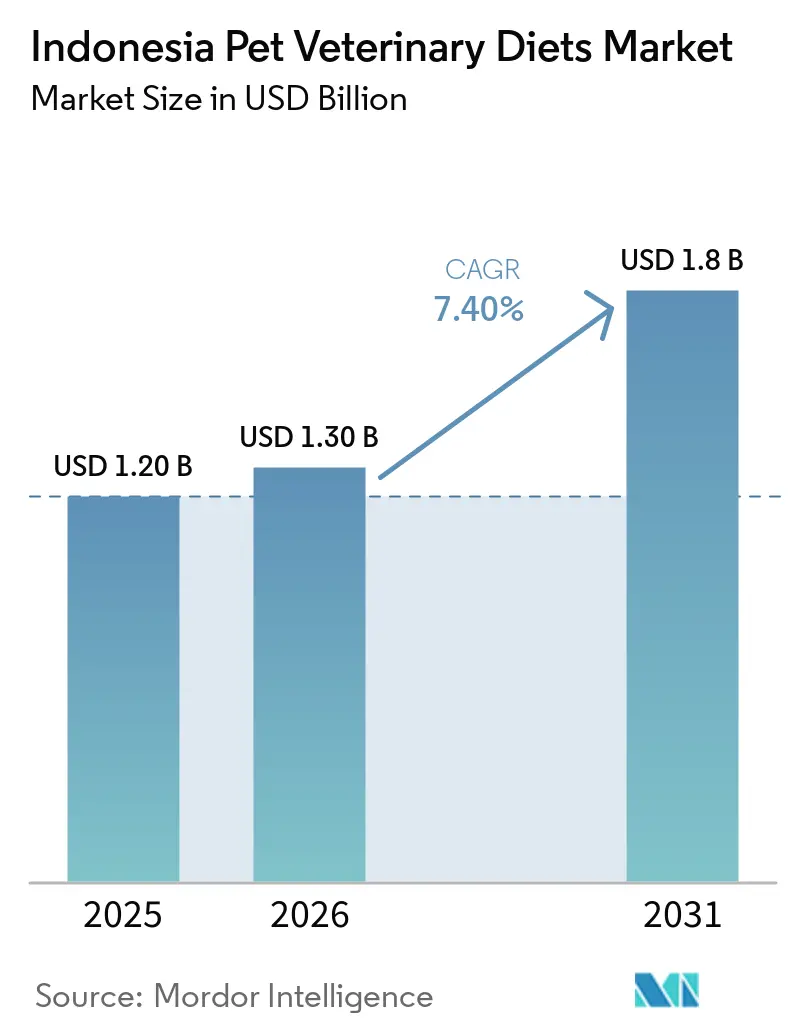

| Base Year Market Size (2025) | USD 1.20 Billion |

| Market Size (2026) | USD 1.30 Billion |

| Market Size (2031) | USD 1.8 Billion |

| Growth Rate (2026 - 2031) | 7.40% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Pet Veterinary Diets Market Analysis by Mordor Intelligence

The Indonesia pet veterinary diets market was anticipated to increase from USD 1.20 billion in 2025 to USD 1.30 billion in 2026 and reach USD 1.80 billion by 2031, growing at a CAGR of 7.40% over 2026-2031. The Indonesia pet veterinary diet market is expanding as therapeutic nutrition moves beyond a narrow, clinic-led purchase and becomes part of broader pet health spending in urban households. Veterinary endorsement still shapes buying decisions, which gives established brands an advantage in cities where diagnosis, follow-up care, and product availability are closely linked. Online purchasing is widening access and is starting to reduce the older dependence on specialist stores and clinic counters, even though trust and product guidance still matter in this category. The tighter import approval rules under Permendag 18/2025 are increasing the importance of local sourcing, labeling readiness, and supply chain control for companies active in the Indonesia pet veterinary diets market[1]Source: Department of Foreign Affairs and Trade, “Complying With Indonesian Halal Requirements,” Australian Government, dfat.gov.au. Competitive conditions remain fragmented, so growth is likely to favor companies that pair clinical credibility with broad distribution, compliant sourcing, and a price ladder that reaches both premium and mass-affluent households.

Key Report Takeaways

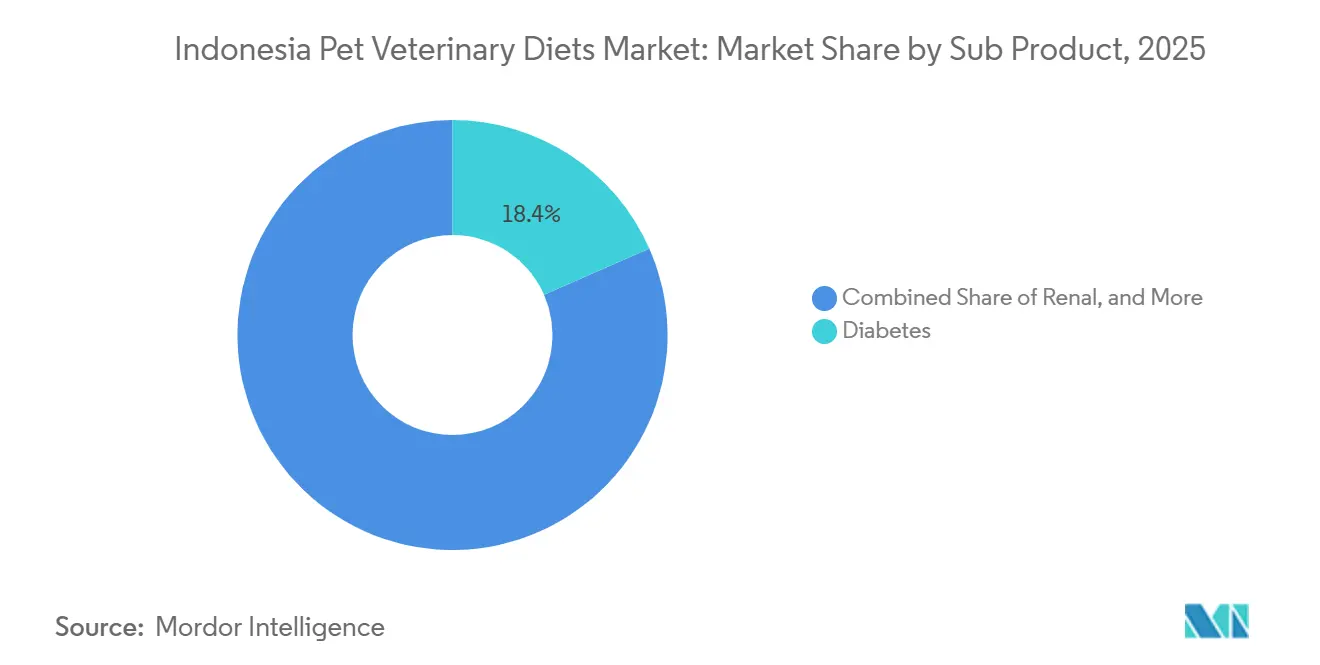

- By sub product, diabetes led the Indonesia pet veterinary diets market in 2025, accounting for 18.4% of the market share, and is the fastest-growing, forecast to expand at a 11.2% CAGR through 2026 to 2031.

- By pet type, cats lead the Indonesia pet veterinary diets market size in 2025, accounting for 65.1%, and also recorded the fastest growth, with a projected CAGR of 8.6% through 2026 to 2031.

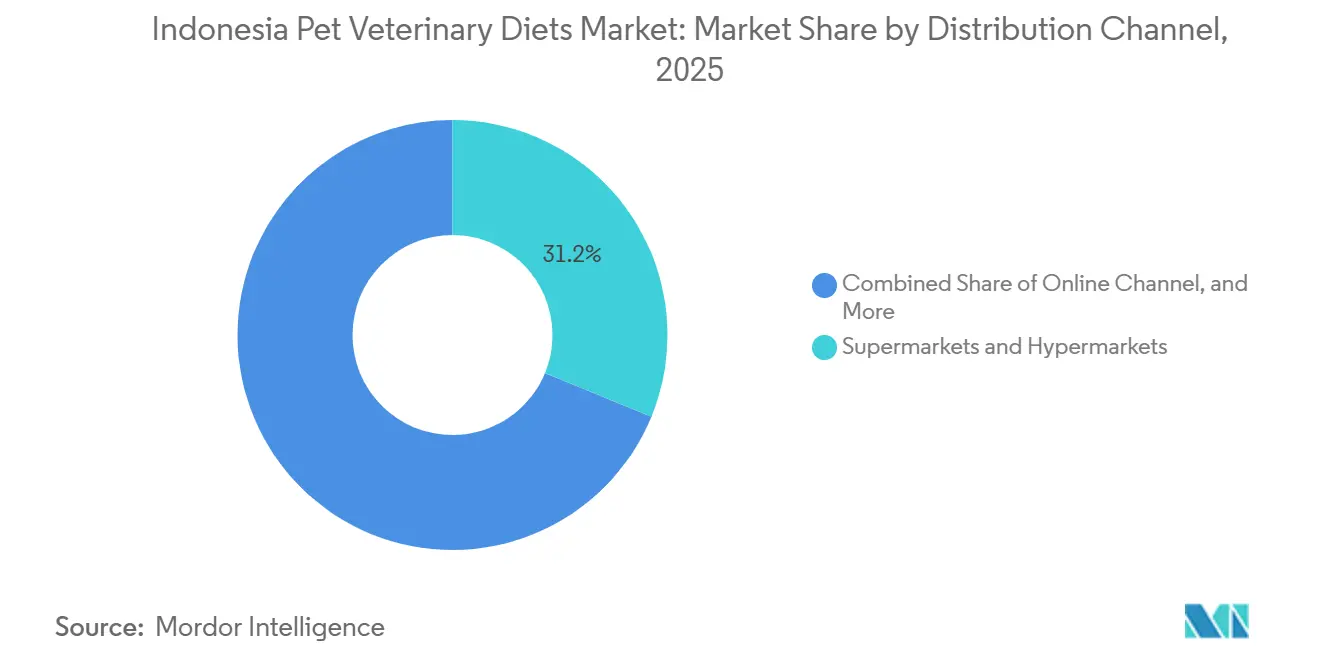

- By distribution channel, supermarkets and hypermarkets hold the largest share, accounting for 31.2% of the Indonesia pet veterinary diets market in 2025, while online distribution channels are the fastest-growing, forecast to expand at a 9.1% CAGR through 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Indonesia Pet Veterinary Diets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Pet Humanization and Preventive Care Spending | +1.8% | Greater Jakarta, Surabaya, and Bandung | Long term (≥ 4 years) |

| Veterinarian-Endorsed Nutrition for Chronic Pet Conditions | +1.5% | Urban clinic networks nationwide | Medium term (2-4 years) |

| Expansion of E-Commerce and Modern Retail Access | +1.3% | Java and major metropolitan corridors | Short term (≤ 2 years) |

| Premiumization of Therapeutic Pet Diets | +1.0% | High-income urban households | Medium term (2-4 years) |

| Higher Awareness of Breed-Specific and Condition-Specific Diets | +0.7% | Tier 1 and tier 2 cities | Long term (≥ 4 years) |

| Halal Compliance and Ingredient Transparency | +0.6% | National, strongest in urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Pet Humanization and Preventive Care Spending

The Indonesia pet veterinary diets market is benefiting from a clear shift in how urban households view companion animal care. Therapeutic diets are no longer treated solely as emergency purchases after a diagnosis. They are increasingly part of routine spending tied to digestive stability, weight management, renal support, and urinary health. This is most visible in Greater Jakarta, Surabaya, and Bandung, where pet owners are more willing to pay for products that appear aligned with long-term wellness. The result is a stronger demand for nutritionally positioned products and a greater willingness to follow a prescribed feeding plan once a veterinarian or trusted retailer introduces the product.

Veterinarian-Endorsed Nutrition for Chronic Pet Conditions

The Indonesia pet veterinary diet market still relies heavily on veterinary recommendations, especially for chronic conditions that require ongoing feeding discipline. Renal, urinary, and digestive conditions remain the strongest triggers for a therapeutic diet purchase because owners are more likely to accept a premium when the product is tied to a diagnosed need. Nestlé Purina’s expansion of Pro Plan Veterinary Diets for digestive and urinary conditions at Indonesia International Pet Expo (IIPE) 2025 showed that manufacturers continue to treat the clinic-linked channel as a serious growth route in Indonesia[2]Source: Royal Canin Indonesia, “Royal Canin Hadir Di IIPE 2024 Tekankan Nutrisi Tepat Untuk Anabul,” PKM Mengkubang, pkm-mengkubang.beltim.go.id. Adoption will remain uneven across the country because urban markets have denser care networks and stronger follow-up behavior than smaller cities. That pattern keeps Java ahead in early therapeutic diet uptake and gives companies a reason to keep investing in clinician education, sampling, and clinic-facing product portfolios.

Expansion of E-Commerce and Modern Retail Access

The Indonesia pet veterinary diet market is benefiting from a distribution model that is becoming broader and easier to access. Supermarkets and hypermarkets remain the largest physical channel, but online retail is becoming the fastest-growing channel for product discovery, repeat purchases, and delivery. This matters because therapeutic diets often need steady replenishment, and digital platforms make it easier for owners to continue a regimen after an initial recommendation. Modern retail also helps brands present multiple price tiers in one place, supporting trial without forcing owners to visit a specialist store on their first purchase. Over time, better digital search behavior, home delivery, and subscription-style replenishment will help the Indonesia pet veterinary diets market reach consumers who previously had limited access to specialized nutrition.

Premiumization of Therapeutic Pet Diets

The Indonesia pet veterinary diets market is also moving through a premiumization phase, but that shift is not limited to the highest-priced imported formulas. International brands still hold an advantage in clinically validated prescription-style products. At the same time, more accessible therapeutic-adjacent products are widening the addressable base and giving owners a step-up option between standard pet food and premium clinical nutrition. PT Perfect Companion Indonesia’s February 2025 launched of SmartHeart Gold Veterinary Diet in Gastrointestinal and Weight Management variants demonstrated that mid-priced offerings can capture health-focused demand without relying on the highest price point. This is making category growth broader, but it is also narrowing the pricing cushion that premium incumbents once enjoyed in the Indonesia pet veterinary diets market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Sensitivity Among Mass-Market Pet Owners | -1.2% | Outside premium urban clusters | Long term (≥ 4 years) |

| Limited Availability of Specialized Veterinary Diets Outside Major Cities | -0.9% | Sumatra, Kalimantan, Sulawesi, and eastern Indonesia | Medium term (2-4 years) |

| Limited Veterinary Prescription Culture for Companion Animals | -0.8% | Non-urban markets | Long term (≥ 4 years) |

| Higher Product Compliance and Import Dependence Costs | -0.7% | National, strongest for import-led brands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity Among Mass-Market Pet Owners

The Indonesia pet veterinary diets market still faces a real affordability ceiling outside premium urban clusters. Many households continue to compare therapeutic diets against standard commercial food and may not see enough immediate value to justify the higher spend. This is especially relevant in tier 2 and tier 3 cities, where price discipline tends to be stronger, and replacement with lower-cost alternatives is easier. Premiumization is present, but it is not uniform across income groups or regions. Companies that fail to offer smaller packs, clearer clinical value, or more accessible entry points may find that demand in the Indonesia pet veterinary diets market grows more slowly than anticipated.

Limited Availability of Specialized Veterinary Diets Outside Major Cities

The Indonesia pet veterinary diet market is constrained by uneven access to diagnostics, limited product availability, and a lack of modern retail infrastructure outside the largest urban areas. Therapeutic diets depend on a chain that starts with clinical recognition and ends with consistent product access, and both are weaker in outer-island markets. Sumatra, Kalimantan, Sulawesi, Maluku, and Papua lag behind Java in specialist access and depth of assortment. Import-related friction under Permendag 18/2025 can add more time and cost to already stretched supply lines, especially for companies that depend on imported inputs or finished products[3]Source: CNBC Indonesia, “Importir Wajib Baca! Ini Syarat Baru Impor Produk Pertanian-Peternakan,” CNBC Indonesia, cnbcindonesia.com. This leaves dry formats in a stronger position than wet therapeutic diets in many non-Java markets, as shelf stability is easier to manage than cold-chain logistics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Product: Diabetes Dominate the Market

Diabetes dominated the Indonesia pet veterinary diets market in 2025, accounting for 18.4% of the market share. It is also the fastest-growing segment, projected to expand at a CAGR of 11.2% from 2026 to 2031. This dominance is primarily due to the increasing prevalence of diabetes and obesity-related metabolic disorders among companion animals, particularly dogs and cats. Factors such as changing lifestyles, reduced physical activity, and rising pet obesity rates contribute to this trend. Additionally, growing awareness among pet owners about the importance of disease-specific nutritional management has driven demand for specialized diabetic veterinary diets. These diets are designed to regulate blood glucose levels, support weight management, and enhance overall health outcomes in diabetic pets.

The sub-product view of the Indonesia pet veterinary diets market shows the greatest maturity in renal and urinary formulations, while digestive sensitivity remains a practical entry category. These segments are well aligned with conditions that owners and veterinarians are more likely to recognize and manage through daily feeding. Digestive sensitivity products are also important because digestive complaints often prompt owners to seek specialized feeding earlier than other health concerns. That makes digestive care a useful bridge between routine nutrition and prescription-style diets.

By Pet Type: Cats Lead Volume and Growth

Cats held the largest pet type, 65.1% of the Indonesia pet veterinary diets market share in 2025, and the segment is also projected to advance at an 8.6% CAGR through 2026 to 2031. This leading position reflects the central role of cats in Indonesia’s companion animal base and the strong fit between feline health needs and therapeutic feeding. Cats often require more specialized management for urinary and renal issues, which supports repeat demand once a condition is identified. The practical feeding pattern also supports this segment, as cat diets are easier to position as single-animal, condition-specific solutions in urban homes. As a result, cats remain the clearest growth anchor in the Indonesia pet veterinary diet market.

Dogs are a smaller segment by volume, but they remain important because they carry a stronger per-unit value in several therapeutic categories. Larger breeds need greater food volume and may require formulas for mobility, obesity, or joint support, which increases the ticket size per purchase. Royal Canin’s emphasis on breed-focused nutrition at the Indonesia International Pet Expo (IIPE) 2024 and IIPE 2025 showed that premium brands continue to use an education-led positioning to capture value in the dog segment. Other pets remain a very small part of the therapeutic category because commercial formulations for rabbits, birds, and ornamental fish are still underdeveloped in this context. This leaves cats as the clearest source of both scale and growth in the Indonesia pet veterinary diets industry.

By Distribution Channel: Online Reorders Are Reshaping Access

Supermarkets and hypermarkets lead the market, accounted for 31.2% of the Indonesia pet veterinary diets market size in 2025, while the online channel is forecast to expand at a 9.1% CAGR through 2026 to 2031. Large-format retail still matters because it gives owners broad access, visible shelf comparison, and exposure to multiple brands in one trip. That makes it the primary physical gateway for therapeutic-adjacent products and for first-time buyers trading up from standard food. The scale of this channel also supports assortment by price tier, which is important in a category that serves both premium and more value-conscious households. Even so, the growth path clearly favors online access in the Indonesia pet veterinary diets market.

Online distribution is changing how owners search, compare, and repurchase therapeutic nutrition after an initial recommendation. It supports convenience, refill behavior, and better reach into neighborhoods where specialist physical access is limited. Specialty stores still matter because some owners want staff guidance and reassurance when choosing a condition-specific formula. Convenience stores and other channels remain secondary because they are less suited to a category that depends on education, trust, and ongoing adherence. Over time, the balance inside the Indonesia pet veterinary diets market will shift further toward digital fulfillment, while physical retail will remain important for discovery, reassurance, and broader visibility.

Geography Analysis

Java held the leading position in the Indonesia pet veterinary diets market in 2025 because it combines the strongest urban spending base with the deepest veterinary and retail infrastructure. Greater Jakarta, Surabaya, and Bandung remain the core demand centers where therapeutic nutrition fits more naturally into routine companion animal care. These cities also support the highest product visibility across hypermarkets, specialty pet stores, and major e-commerce fulfillment networks. Java’s lead is therefore tied not only to population but also to the density of care pathways that facilitate therapeutic diet adoption.

Sumatra stands as the next important growth corridor as the urban middle class expands in cities such as Medan, Palembang, and Pekanbaru. Kalimantan is also becoming more relevant as professional households are rising alongside broader development activity, including the new national capital project in East Kalimantan. Sulawesi has a growing urban consumer base around Makassar, but product access remains narrower than in Java. In these regions, halal credentials can matter more directly at the point of purchase because Muslim-majority communities often weigh certification in brand selection. Import compliance under Permendag 18/2025 can further slow product introduction outside Java because supply chains are less established and distribution depth is weaker.

Bali and Nusa Tenggara form a distinct pocket where expatriate demand and tourism-linked purchasing support interest in international premium brands. Bali can justify a stronger imported assortment than its scale alone would suggest because buyer preferences are different from those in most other islands. Nusa Tenggara remains much more price sensitive and access constrained, which limits broad therapeutic adoption. Maluku and Papua remain the least developed parts of the Indonesia pet veterinary diets market because clinic density, cold-chain capacity, and formal companion animal care are all lower. These geographies may improve over the long run as infrastructure develops, but near-term demand will remain concentrated in a small set of urban centers.

Competitive Landscape

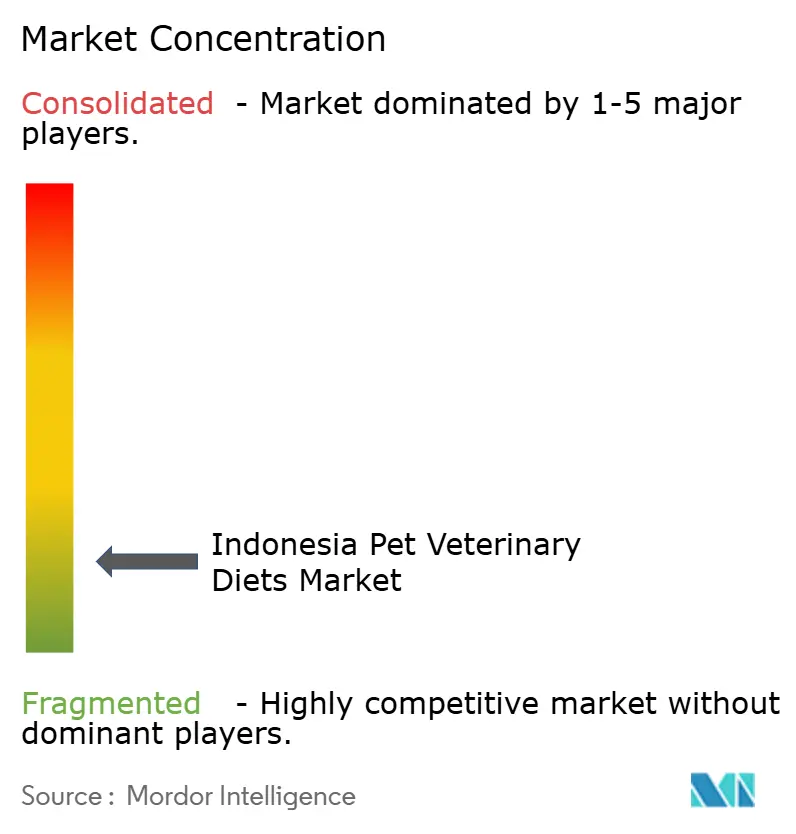

The Indonesia pet veterinary diet market remains fragmented, with players such as Mars, Incorporated, Nestle S.A.Colgate-Palmolive, Inc., PT Central Proteina Prima Tbk, and EBOS Group Limited. This means no company has enough scale to control the category through distribution reach alone. Instead, competition depends on veterinary trust, clear health positioning, and the ability to stay visible across both clinics and consumer retail. The Indonesia pet veterinary diet market, therefore, rewards companies that can defend a premium image while still adjusting to local pricing and regulatory realities.

The next layer of competition will be shaped by compliance and distribution execution as much as by brand strength. Halal certification deadlines and stricter import procedures increase the value of local sourcing options, reliable registration timing, and clean documentation. Outer-island coverage also remains underdeveloped, so there is still room for companies that can pair affordable dry therapeutic products with better national fulfillment. The Indonesia pet veterinary diets market is unlikely to consolidate quickly because domestic and regional participants still have room to compete through pricing, localized portfolios, and channel focus.

The increasing digitalization of pet healthcare and purchasing behavior is significantly influencing competitive dynamics. Pet owners are turning to online platforms for veterinary advice, exploring therapeutic nutrition options through digital channels, and purchasing prescription and specialized diets via e-commerce. This shift presents opportunities for both multinational and regional companies to enhance customer engagement through educational content, teleconsultation partnerships, and direct-to-consumer strategies. Companies that effectively integrate veterinarian recommendations with a robust online presence, product accessibility, and pet owner education are likely to achieve a competitive edge. With growing awareness of preventive pet healthcare in Indonesia, brands that focus on omnichannel distribution and evidence-based nutritional solutions are better positioned to increase market share and foster long-term customer loyalty.

Indonesia Pet Veterinary Diets Industry Leaders

PT Central Proteina Prima Tbk

EBOS Group Limited

Mars, Incorporated

Colgate-Palmolive (The Hill's Pet Nutrition)

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Nestle Purina Pro Plan launched new Pro Plan Veterinary Diets for digestive and urinary conditions in dogs and cats at IIPE 2025 (October 31 to November 2, ICE BSD City, Tangerang), deepening its therapeutic nutrition portfolio in Indonesia with lines spanning Urinary Tract Health, Sensitive Skin and Stomach, Hairball Control, Weight Loss, and Sterilized variants.

- February 2025: PT Perfect Companion Indonesia launched SmartHeart Gold Veterinary Diet in two new clinical variants, Gastrointestinal and Weight Management, at a Jakarta event attended by representatives of Perhimpunan Dokter Hewan Indonesia (PDHI). The launch expanded an existing lineup of Renal, Recovery, and Urinary variants distributed through veterinary clinics at an accessible price point.

- September 2024: Royal Canin participated in Indonesia International Pet Expo (IIPE) (September 6-8, ICE BSD Tangerang) under its 2024 campaign "Health is Worth It," promoting precision therapeutic nutrition from the Start of Life stage as a preventive care investment for cats and dogs in Indonesia.

Indonesia Pet Veterinary Diets Market Report Scope

Pet veterinary diets are specialized pet foods formulated to manage, support, or treat specific medical conditions in companion animals, as recommended by a veterinarian. Indonesia pet veterinary diet market report is segmented by sub-product (diabetes, digestive sensitivity, oral care diets, renal, urinary tract disease, derma diets, obesity diets, and other veterinary diets), by pets (cats, dogs, and other pets), and by distribution channel (convenience stores, online channel, specialty stores, supermarkets and hypermarkets, and other channels). The market forecasts are provided in terms of Value (USD) and Volume (Metric Tons).

| Diabetes |

| Renal |

| Urinary Tract Disease |

| Digestive Sensitivity |

| Oral Care Diets |

| Derma Diets |

| Obesity Diets |

| Other Veterinary Diets |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets and Hypermarkets |

| Other Channels |

| By Sub Product | Diabetes |

| Renal | |

| Urinary Tract Disease | |

| Digestive Sensitivity | |

| Oral Care Diets | |

| Derma Diets | |

| Obesity Diets | |

| Other Veterinary Diets | |

| By Pet Type | Cats |

| Dogs | |

| Other Pets | |

| By Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets and Hypermarkets | |

| Other Channels |

Key Questions Answered in the Report

How large is Indonesia pet veterinary diets space in 2026?

Indonesia pet veterinary diets market is estimated at USD 1.30 billion in 2026

Which pet category drives the strongest demand in Indonesia?

Cats led with 65.1% of revenue in 2025 and are also projected to grow the fastest at an 8.6% CAGR through 2031.

Which sales channel is expanding the fastest for therapeutic pet nutrition in Indonesia?

The online channel is projected to expand at a 9.1% CAGR through 2031, ahead of all other distribution channels.

Why is halal certification important for veterinary diet suppliers in Indonesia?

The October 17, 2026 deadline for imported food and beverage products raises the need for compliant sourcing, labeling, and process control.

Page last updated on: