Market Overview

| Study Period | 2018 - 2031 |

|---|---|

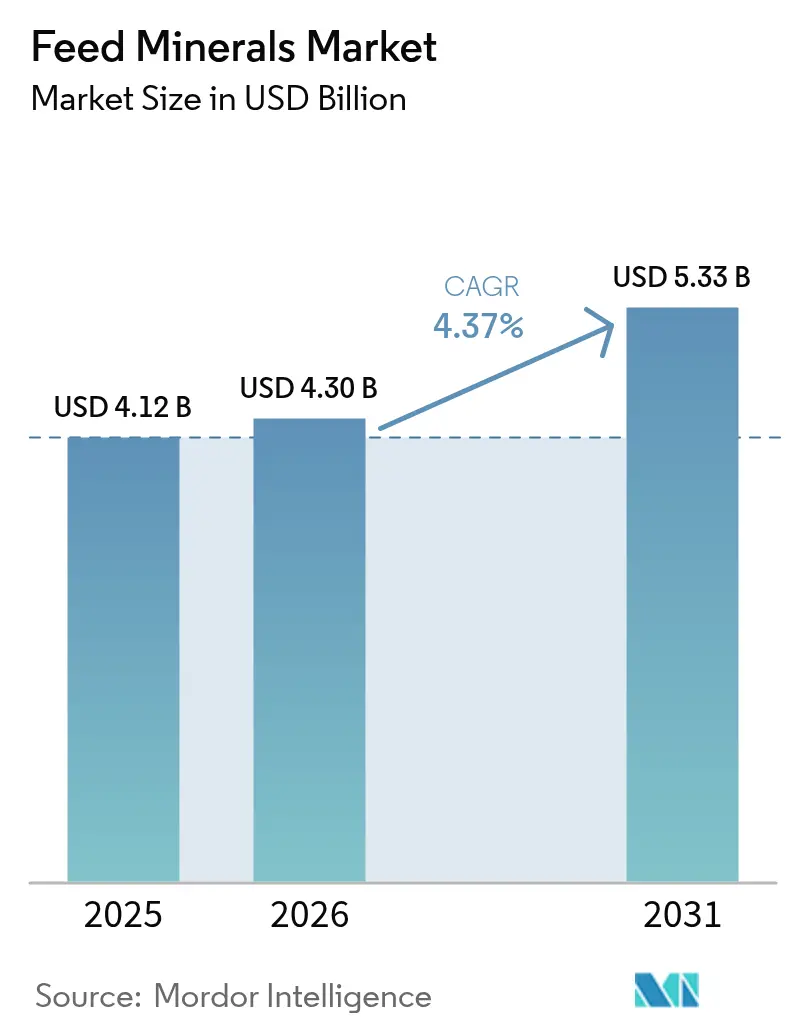

| Market Size (2026) | USD 4.3 Billion |

| Market Size (2031) | USD 5.33 Billion |

| Growth Rate (2026 - 2031) | 4.37% CAGR |

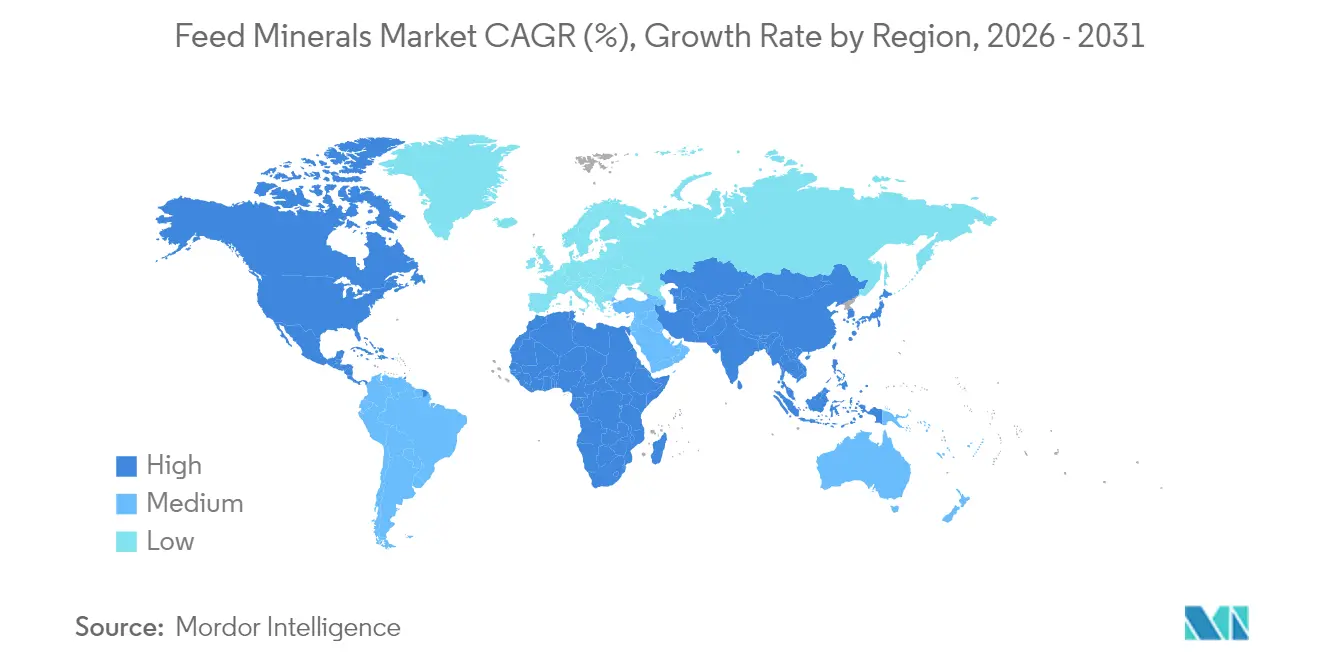

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Feed Minerals Market Analysis by Mordor Intelligence

The feed minerals market size was valued at USD 4.12 billion in 2025 and estimated to grow from USD 4.3 billion in 2026 to reach USD 5.33 billion by 2031, at a CAGR of 4.37% during the forecast period (2026-2031). Rising demand for precision animal nutrition, tighter regulatory oversight on trace-element inclusion, and broadening protein consumption in emerging economies continue to propel market growth.[1]Source: FDA Center for Veterinary Medicine, “Animal Food Labeling Guide,” U.S. Food and Drug Administration, fda.gov Increased adoption of chelated organic minerals that improve bioavailability, alongside investments in microencapsulation to protect mineral integrity during pelleting, have reshaped competitive strategies. Higher disposable incomes in Asia-Pacific, a pivot toward nutrient-dense poultry and dairy diets, and expanding industrial livestock operations sustain steady volume uptake. Meanwhile, sustainability pressures encourage innovations such as insect-frass recycling and IoT-based micro-dosing systems that curb mineral losses while easing environmental compliance costs.[2]Source: Environmental Protection Agency, “Animal Feeding Operations,” epa.gov

Key Report Takeaways

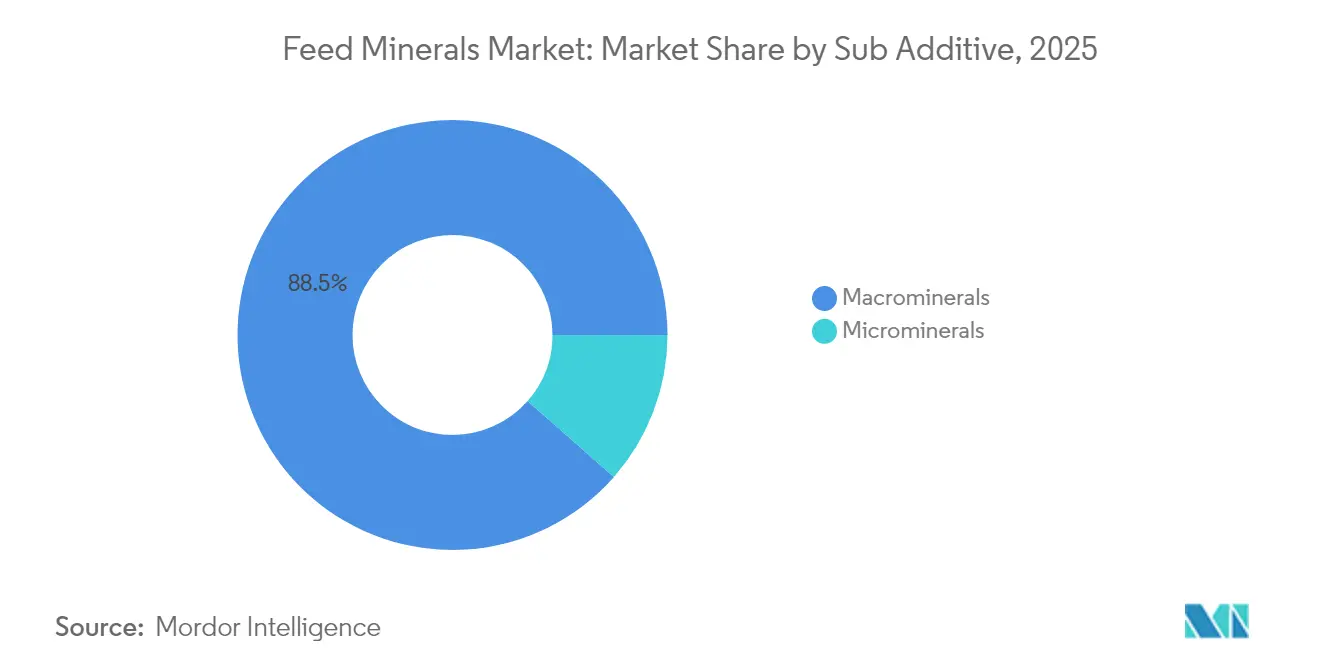

- By sub-additive, macrominerals captured 88.52% of the feed minerals market share in 2025 and are anticipated to grow at a CAGR of 4.39% through 2031.

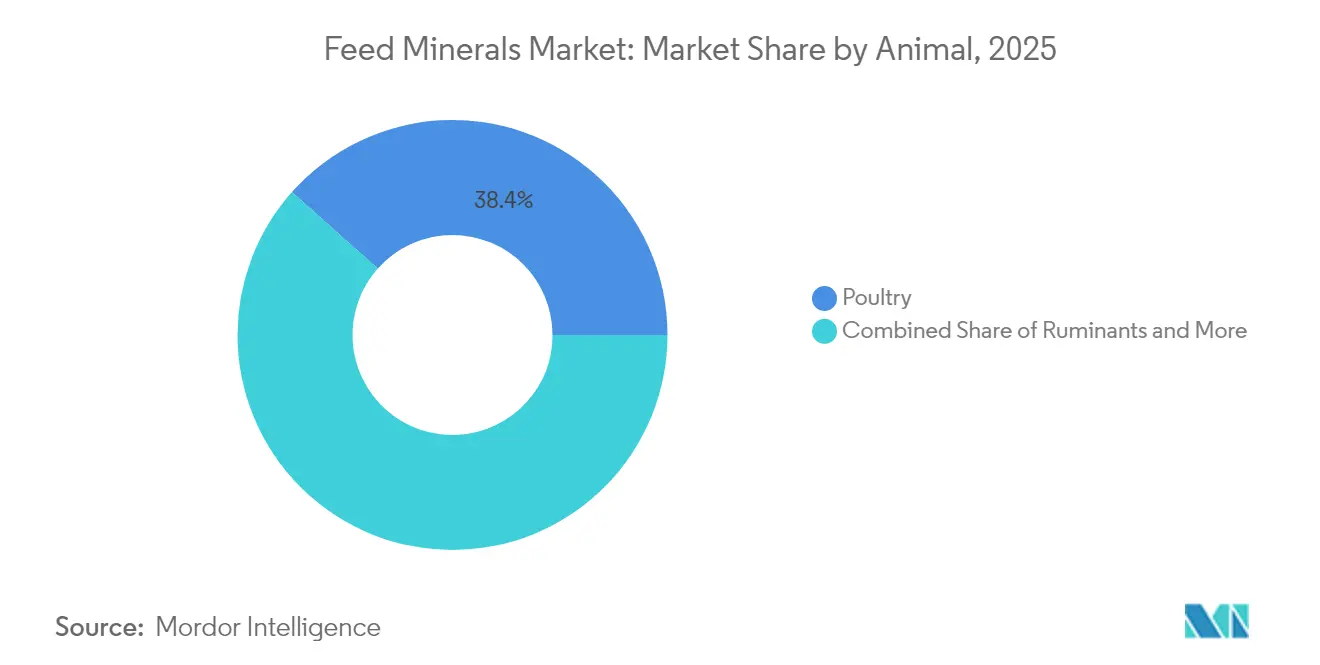

- By animal type, poultry led with a 38.42% revenue share in 2025, while ruminants are advancing at the fastest rate, with a 4.68% CAGR through 2031.

- By geography, the Asia–Pacific region dominated with a 30.12% share in 2025, while North America recorded the fastest 5.26% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Feed Minerals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nutrient-dense poultry diets driving mineral premix demand | +0.8% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Industrial livestock expansion in emerging economies | +1.2% | Asia-Pacific core, spill-over to South America and Africa | Long term (≥ 4 years) |

| Regulatory mandates on trace-mineral inclusion levels | +0.6% | North America and EU, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Shift toward chelated organic minerals for higher bioavailability | +0.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| IoT-based precision feeding enabling micro-dosing of minerals | +0.5% | North America and Europe, early adoption in developed markets | Long term (≥ 4 years) |

| Circular sourcing: insect-frass recycling for mineral content | +0.3% | Europe and North America, pilot programs in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nutrient-dense poultry diets driving mineral premix demand

Global poultry producers increasingly deploy precise mineral premixes to sustain rapid broiler growth and shell quality in layers. Modern broiler diets incorporate 40-100 ppm zinc and 60-120 ppm manganese, while layer rations require 3.5-4.2 % calcium for shell integrity. Antibiotic-free production intensifies the need for zinc and copper to support gut health and immunity, prompting suppliers to launch species-specific premixes that combine organic and inorganic sources. Microencapsulation techniques now deliver targeted intestinal release, improving absorption efficiency by up to 25% over conventional sulfate forms. European Union (EU) standardization of copper and zinc limits ensures consistent demand for compliant formulations.

Industrial livestock expansion in emerging economies

Modernization of livestock in China, India, Brazil, and Vietnam fuels substantial growth in the feed minerals market. China’s swine sector rebound, backed by the Ministry of Agriculture trace-element mandates, drives volume demand for standardized copper and zinc additives.[3]Source: Ministry of Agriculture and Rural Affairs of China, “Agricultural Policies,” agri.gov.cn India’s dairy push relies on chelated zinc and manganese to raise reproductive efficiency, while Brazil’s poultry and swine integrators adopt EU-style organic minerals to lower environmental excretion. Precision feeding systems enable cost-efficient micro-dosing, widening uptake among price-sensitive producers.

Regulatory mandates on trace-mineral inclusion levels

Authorities in North America and Europe prescribe tight inclusion ceilings to prevent soil and water contamination. The Food and Drug Administration (FDA) caps copper at 125 ppm in swine diets and zinc at 150 ppm in poultry diets, compelling premix manufacturers to adopt high-bioavailability organic forms. EU regulations enforce similar ceilings, bolstering demand for precision formulation software that assures compliance. Association of American Feed Control Officials (AAFCO) nutrient revisions have extended such mandates to companion animals, adding incremental growth pockets.

Shift toward chelated organic minerals for higher bioavailability

Chelated zinc methionine offers 40-60% superior uptake compared with zinc sulfate, allowing feed formulators to cut inclusion rates without performance loss. Improved uptake lowers heavy-metal excretion, aligning with environmental targets and justifying premium pricing. Dairy operations report 8-12% fertility gains when chelated copper and zinc replace inorganic forms, and poultry growers observe firmer bones and improved feathering as side benefits, reinforcing the switch to organics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw-mineral prices and supply risk | -0.7% | Global, with acute impact in import-dependent regions | Short term (≤ 2 years) |

| Phosphorus and heavy-metal discharge regulations | -0.5% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Functional additives replacing high mineral doses | -0.4% | Global, led by developed markets | Long term (≥ 4 years) |

| Mineral antagonism concerns lowering inclusion rates | -0.3% | Global, with focus on precision nutrition markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Raw-Mineral Prices and Supply Risk

Copper, zinc, and manganese markets experienced significant price fluctuations throughout 2024, with zinc prices showing notable volatility during the period. Concentration of output in South Africa and China exposes buyers to geopolitical disruptions, forcing higher inventory buffers that raise working-capital needs by about 10%. Long-term supply contracts mitigate some risk but embed premium costs, pressuring margins across premix supply chains.

Phosphorus and heavy-metal discharge regulations

The Environmental Protection Agency (EPA) nutrient-management permits cap phosphorus runoff from concentrated animal feeding operations, driving adoption of highly available mineral sources and complementary phytase enzymes. EU nitrates limits impose similar curbs, adding compliance monitoring and manure handling expenses. The trend pushes formulators toward lower-dosage organic minerals and feed additives that boost retention efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Additive: Macrominerals anchor essential metabolic functions

Macrominerals commanded 88.52% of the feed minerals market share in 2025 and are anticipated to grow at a CAGR of 4.39% through 2031, underscoring their indispensable role in skeletal growth, electrolyte balance, and metabolic regulation across all livestock classes. Dairy herds require specific calcium and phosphorus levels in their dry-matter intake to maintain milk production, while broilers need balanced ratios of these minerals for bone strength. The macrominerals segment continues to grow as industrial farms expand their operations and focus on increasing productivity. Specialized salt blends enriched with electrolytes now counter heat stress in tropical operations, broadening product depth.

Microminerals represent a stronger value proposition owing to higher per-kilogram pricing for chelated zinc, copper, selenium, and chromium. Chelated zinc commands significant premiums over sulfate forms while delivering greater tissue deposition and reduced fecal loss. Copper inclusion varies based on swine growth phases and remains pivotal for immune and pigment functions. Precision micro-dosing helps restrain iron levels to prevent antagonism with zinc and copper. Selenium-enriched yeast, newly approved in the EU, supports antioxidant systems and fertility, lifting adoption in organic herds.

By Animal: Poultry leadership amid intensive production systems

Poultry retained a 38.42% share of the feed minerals market in 2025 as global diets shifted toward economical lean meat and eggs. Modern broiler genetics drive accelerated growth rates, increasing the importance of zinc and manganese supplementation to prevent skeletal issues. Layer operations require consistent calcium levels throughout extended production cycles to maintain eggshell integrity. Advanced housing systems and automated feeding technologies enable standardized mineral premix delivery, improving cost efficiency and supporting increased production volumes.

Ruminants show the highest growth at 4.68% CAGR through 2031, driven by expanding dairy operations in India and reproductive-efficiency programs worldwide. Early-lactation diets now include elevated organic zinc and copper to bolster immunity during negative energy balance. Beef-feedlot operators adopt chelated minerals for carcass-quality boosts, while grass-fed niches use organics to meet label requirements. Swine and aquaculture continue to diversify mineral portfolios: high selenium and iodine diets support marine species osmoregulation, and modern finishing barns rely on copper to enhance growth and lean yield.

Geography Analysis

Asia–Pacific accounted for 30.12% of the feed minerals market share in 2025 and remains the epicenter of demand with sustained investment in commercial poultry complexes, pig mega-farms, and integrated aqua hubs. China’s pork recovery alone necessitates continuous imports of chelated copper and zinc, given local mining shortfalls, while India’s dairy cooperatives buy macromineral blocks in bulk to support smallholder networks. Oceania, though smaller, sets benchmarks in organic mineral adoption among pasture-based systems.

North America posts the fastest 5.26% CAGR as precision feeding and regulatory compliance converge. U.S. dairies link milk-component software with mineral feeders to fine-tune copper and selenium inputs, cutting excess excretion. Large feedlots deploy micro-bin blenders that automate 110 metric ton-per-hour rations with ±1 % accuracy, fostering steady feed minerals market growth. Mexico’s integrated pork processors align with U.S. standards, enabling cross-border mineral formulations.

Europe intensifies its environmental agenda. German poultry integrators use phytase and chelated minerals to stay within phosphorus quotas, while French dairy groups test insect-frass blends for organic herds. Scandinavian salmon farms innovate seawater-specific mineral mixes high in iodine and selenium for improved smolt survival. Eastern Europe, though cost-sensitive, imports low-dose organics that reduce heavy-metal surcharges on manure land-application permits.

Competitive Landscape

The top five players, like ADM, Yara International, Solvay, Cargill, and Nutreco, collectively hold the low share of the global feed minerals market, leaving room for regional specialists. Competitive intensity centers on bioavailability technologies. ADM’s amino-acid chelation patents, Solvay’s mineral microcapsules, and Yara’s digital nutrient platforms all aim to lock in premium margins. Firms with end-to-end supply chains manage mining risk and regulatory complexity better, raising barriers for smaller entrants.

Strategic alliances dominate recent moves. Cargill’s partnership with an insect farm commercializes frass minerals for circular economy-minded customers, while Solvay integrates IoT dosing units to bundle hardware and consumables. Yara’s South American acquisition boosts local production of chelated copper and zinc, leveraging its fertilizer logistics for cross-selling.

Sustainability credentials increasingly steer purchase decisions. Nutreco’s selenium-yeast approval positions it for premium dairy clients. Balchem, Zinpro, and Alltech invest in on-farm diagnostics that assess mineral status via hair or serum, shifting value from products to services. Chinese providers scale low-cost chelated lines, yet regulatory hurdles and traceability concerns temper global expansion.

Feed Minerals Industry Leaders

Yara International ASA

ADM

Solvay SA

Cargill, Incorporated.

Nutreco (SHV Holdings)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: ADM and Alltech established a joint venture in North America, combining 49 feed mills to improve animal nutrition capabilities. The partnership integrates ADM's premix expertise with Alltech's specialty trace minerals to enhance feed mineral production and distribution.

- July 2025: Cargill's acquisition of Brazil-based Mig-Plus expanded its feed premix and mineral production capabilities, particularly in swine and ruminant segments. The acquisition strengthened Cargill's regional supply chain and complemented its previous mineral-focused acquisitions of Integral and Anhambi.

Global Feed Minerals Market Report Scope

Macrominerals, Microminerals are covered as segments by Sub Additive. Aquaculture, Poultry, Ruminants, Swine are covered as segments by Animal. Africa, Asia-Pacific, Europe, Middle East, North America, South America are covered as segments by Region.By Sub Additive

| Macrominerals |

| Microminerals |

By Animal

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Swine | |

| Other Animals |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Italy | |

| Netherlands | |

| Russia | |

| Spain | |

| Turkey | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Indonesia | |

| Japan | |

| Philippines | |

| South Korea | |

| Thailand | |

| Vietnam | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Iran | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Sub Additive | Macrominerals | |

| Microminerals | ||

| By Animal | Aquaculture | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | Broiler | |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Spain | ||

| Turkey | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Indonesia | ||

| Japan | ||

| Philippines | ||

| South Korea | ||

| Thailand | ||

| Vietnam | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Iran | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Market Definition

- FUNCTIONS - For the study, feed additives are considered to be commercially manufactured products that are used to enhance characteristics such as weight gain, feed conversion ratio, and feed intake when fed in appropriate proportions.

- RESELLERS - Companies engaged in reselling feed additives without value addition have been excluded from the market scope, to avoid double counting.

- END CONSUMERS - Compound feed manufacturers are considered to be end-consumers in the market studied. The scope excludes farmers buying feed additives to be used directly as supplements or premixes.

- INTERNAL COMPANY CONSUMPTION - Companies engaged in the production of compound feed as well as the manufacturing of feed additives are part of the study. However, while estimating the market sizes, the internal consumption of feed additives by such companies has been excluded.

| Keyword | Definition |

|---|---|

| Feed additives | Feed additives are products used in animal nutrition for purposes of improving the quality of feed and the quality of food from animal origin, or to improve the animals’ performance and health. |

| Probiotics | Probiotics are microorganisms introduced into the body for their beneficial qualities. (It maintains or restores beneficial bacteria to the gut). |

| Antibiotics | Antibiotic is a drug that is specifically used to inhibit the growth of bacteria. |

| Prebiotics | A non-digestible food ingredient that promotes the growth of beneficial microorganisms in the intestines. |

| Antioxidants | Antioxidants are compounds that inhibit oxidation, a chemical reaction that produces free radicals. |

| Phytogenics | Phytogenics are a group of natural and non-antibiotic growth promoters derived from herbs, spices, essential oils, and oleoresins. |

| Vitamins | Vitamins are organic compounds, which are required for normal growth and maintenance of the body. |

| Metabolism | A chemical process that occurs within a living organism in order to maintain life. |

| Amino acids | Amino acids are the building blocks of proteins and play an important role in metabolic pathways. |

| Enzymes | Enzyme is a substance that acts as a catalyst to bring about a specific biochemical reaction. |

| Anti-microbial resistance | The ability of a microorganism to resist the effects of an antimicrobial agent. |

| Anti-microbial | Destroying or inhibiting the growth of microorganisms. |

| Osmotic balance | It is a process of maintaining salt and water balance across membranes within the body's fluids. |

| Bacteriocin | Bacteriocins are the toxins produced by bacteria to inhibit the growth of similar or closely related bacterial strains. |

| Biohydrogenation | It is a process that occurs in the rumen of an animal in which bacteria convert unsaturated fatty acids (USFA) to saturated fatty acids (SFA). |

| Oxidative rancidity | It is a reaction of fatty acids with oxygen, which generally causes unpleasant odors in animals. To prevent these, antioxidants were added. |

| Mycotoxicosis | Any condition or disease caused by fungal toxins, mainly due to contamination of animal feed with mycotoxins. |

| Mycotoxins | Mycotoxins are toxin compounds that are naturally produced by certain types of molds (fungi). |

| Feed Probiotics | Microbial feed supplements positively affect gastrointestinal microbial balance. |

| Probiotic yeast | Feed yeast (single-cell fungi) and other fungi used as probiotics. |

| Feed enzymes | They are used to supplement digestive enzymes in an animal’s stomach to break down food. Enzymes also ensure that meat and egg production is improved. |

| Mycotoxin detoxifiers | They are used to prevent fungal growth and to stop any harmful mold from being absorbed in the gut and blood. |

| Feed antibiotics | They are used both for the prevention and treatment of diseases but also for rapid growth and development. |

| Feed antioxidants | They are used to protect the deterioration of other feed nutrients in the feed such as fats, vitamins, pigments, and flavoring agents, thus providing nutrient security to the animals. |

| Feed phytogenics | Phytogenics are natural substances, added to livestock feed to promote growth, aid in digestion, and act as anti-microbial agents. |

| Feed vitamins | They are used to maintain the normal physiological function and normal growth and development of animals. |

| Feed flavors and sweetners | These flavors and sweeteners help to mask tastes and odors during changes in additives or medications and make them ideal for animal diets undergoing transition. |

| Feed acidifiers | Animal feed acidifiers are organic acids incorporated into the feed for nutritional or preservative purposes. Acidifiers enhance congestion and microbiological balance in the alimentary and digestive tracts of livestock. |

| Feed minerals | Feed minerals play an important role in the regular dietary requirements of animal feed. |

| Feed binders | Feed binders are the binding agents used in the manufacture of safe animal feed products. It enhances the taste of food and prolongs the storage period of the feed. |

| Key Terms | Abbreviation |

| LSDV | Lumpy Skin Disease Virus |

| ASF | African Swine Fever |

| GPA | Growth Promoter Antibiotics |

| NSP | Non-Starch Polysaccharides |

| PUFA | Polyunsaturated Fatty Acid |

| Afs | Aflatoxins |

| AGP | Antibiotic Growth Promoters |

| FAO | The Food And Agriculture Organization of the United Nations |

| USDA | The United States Department of Agriculture |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms