Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

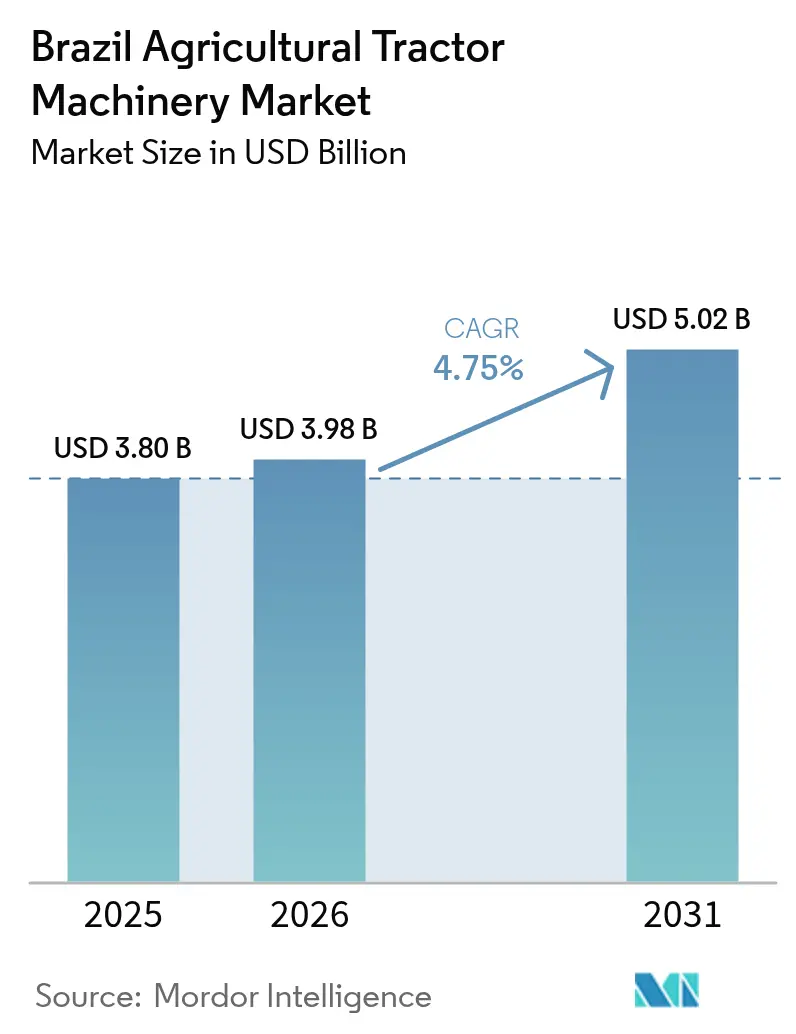

| Base Year Market Size (2025) | USD 3.80 Billion |

| Market Size (2026) | USD 3.98 Billion |

| Market Size (2031) | USD 5.02 Billion |

| Growth Rate (2026 - 2031) | 4.75% CAGR |

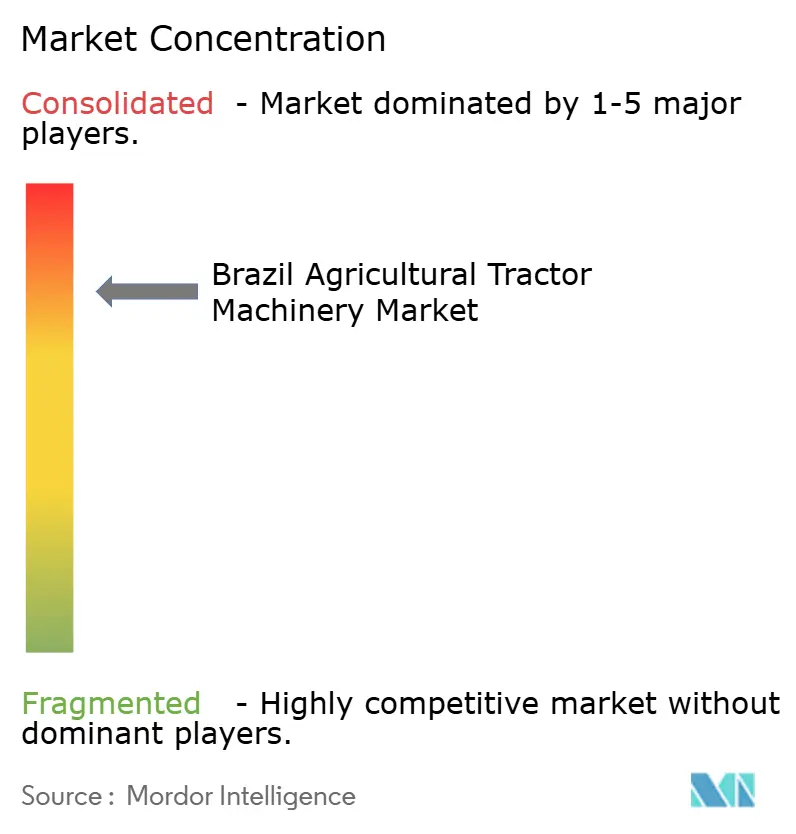

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Agricultural Tractor Machinery Market Analysis by Mordor Intelligence

The Brazil agricultural tractor machinery market size is expected to grow from USD 3.80 billion in 2025 to USD 3.98 billion in 2026 and is forecast to reach USD 5.02 billion by 2031 at 4.75% CAGR over 2026-2031. Robust rural credit subsidies, a rebound in commodity prices, and greater adoption of precision-ready implements are anticipated to keep the Brazil agricultural tractor machinery market on a steady expansion path. Producer demand is recovering after a slide in 2024 unit sales that stemmed from high interest rates and weak soybean prices. Government programs such as Moderfrota and the National Development Bank’s (BNDES) equalized credit lines continue to anchor equipment financing at rates 200–300 basis points below commercial benchmarks, allowing dealers to stretch payment terms and smooth seasonal spikes[1]Source: BNDES, “Financing for Capital Goods,” bndes.gov.br. Original equipment manufacturer (OEM) strategies now center on autonomous-ready platforms, quick-attach retrofit kits, and satellite connectivity, all of which align with Brazil’s large, geographically dispersed farm operations. Competitive intensity remains high as multinationals invest in domestic production while local implement specialists undercut imports through shorter supply chains and subsidized dealer financing.

Key Report Takeaways

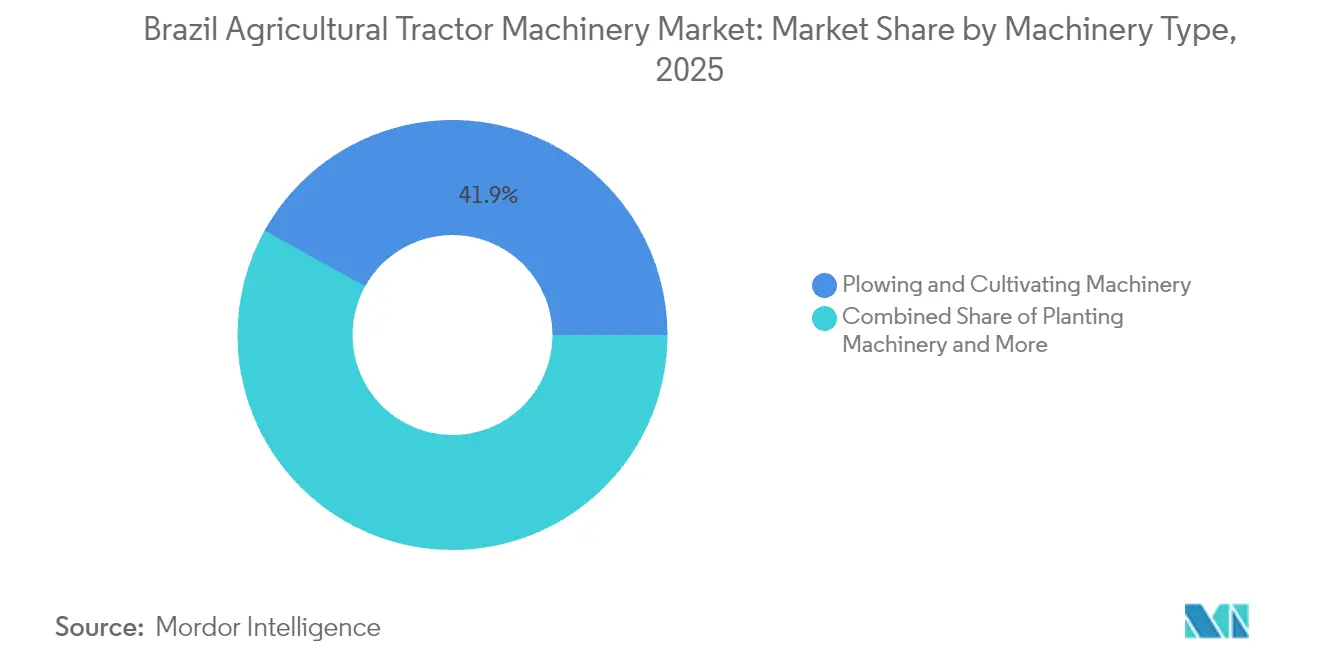

- By machinery type, plowing and cultivating machinery led the Brazil agricultural tractor machinery market with a 41.92% revenue share in 2025. In contrast, planting machinery is forecast to expand at a 8.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Agricultural Tractor Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream Credit-Financed Mechanization Boom | +1.2% | National, strongest in Mato Grosso, Paraná, and Goiás | Medium term (2–4 years) |

| Commodity-price-linked Capex Cycles | +0.8% | Soybean and corn belts | Short term (≤2 years) |

| Domestic OEM Remanufacturing Push | +0.6% | São Paulo, Paraná, and Rio Grande do Sul | Long term (≥4 years) |

| Government Moderfrota Subsidy Extension | +1.0% | Nationwide small and medium farms | Medium term (2–4 years) |

| Precision-ready Quick-Attach Retrofit Upsurge | +0.7% | Large estates in Mato Grosso, Goiás | Short term (≤2 years) |

| Emergence of Carbon-Smart Tillage Practices | +0.5% | Cerrado and Amazon transition zones | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Mainstream Credit-Financed Mechanization Boom

BNDES disbursed funds for machinery in 2024, reflecting a notable increase that allowed dealers to extend payment terms significantly. Moderfrota contributed to the addition of a substantial number of tractors to the national fleet over a decade, highlighting the important role of subsidized loans. The February 2025 tranche of funding supports lending activities during critical planting months. These initiatives collectively reduce growers’ cost of capital compared to commercial rates and encourage consistent equipment replacement.

Commodity-price-linked Capex Cycles

Soybean futures experienced significant declines, reducing farm margins and delaying tractor purchases for several months. Historically, an increase in soybean prices has been linked to a notable rise in equipment orders within a short period, highlighting the strong connection between revenue and spending. Coffee provided some stability as Arabica prices supported ongoing mechanization efforts in key agricultural regions. These price fluctuations create immediate impacts that either encourage or hinder capital investments.

Domestic OEM Remanufacturing Push

Jacto and Stara now refurbish key driveline parts locally, reducing overall ownership costs compared with imports. AGCO’s Canoas remanufacturing plant extends tractor life significantly, appealing to a large portion of Brazil’s aging fleet. Shorter supply chains also mitigate currency fluctuations and improve parts delivery times. These benefits are gradually shifting buyer preferences toward domestically produced or remanufactured components.

Government Moderfrota Subsidy Extension

Moderfrota rates remain well below the national benchmark interest rate, making it an attractive option for financing. The program allocates a significant portion of its packages to small and medium growers, expanding mechanization beyond traditional agricultural hubs. Equalized credit ensures predictable monthly payments despite increasing interest burdens. Its continuation remains crucial for maintaining stability in equipment sales.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Import Tariffs on Precision Components | −0.9% | Nationwide import-dependent users | Medium term (2–4 years) |

| Double-digit Interest Rates on Working Capital | −1.3% | Dealers and small farms | Short term (≤2 years) |

| Seasonal Logistics Bottlenecks | −0.6% | Mato Grosso and southern ports | Short term (≤2 years) |

| Fragmented Rural Financing Access | −0.7% | Semi-arid Northeast, Amazon fringes | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Import Tariffs on Precision Components

Capital-goods duties are significant and increase further when local service taxes are included, making advanced sensors and controllers expensive for growers. The expiration of the ex-tarifário waiver creates uncertainty and leads to forward-buying activity[2]Source: World Trade Organization, “Trade Policy Review Brazil 2024,” wto.org. Importers also face extended approval timelines due to recent regulatory changes. High costs hinder the adoption of precision-agriculture technologies, particularly for smaller operations.

Seasonal Logistics Bottlenecks

Brazil faces a significant storage shortfall, forcing immediate grain sales at harvest discounts[3]Source: Embrapa, “Grain Storage Deficit Reaches 120 Million Tons,” embrapa.br. Port queues at Arco Norte can experience lengthy delays, impacting the timely arrival of machinery during peak demand. Road congestion on key routes further extends transit times for tractors shipped from southern factories. Limited cash flow and delayed deliveries together hinder timely equipment upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Plowing and Cultivating Machinery Dominates While Planting Machinery Accelerates

Plowing and cultivating machinery accounted for 41.92% of 2025 revenue, reflecting the extensive use of no-till practices that necessitate investments in specialized double-disc openers and shanks. Planting machinery gear is the fastest-growing segment of the Brazilian agricultural tractors market, advancing 8.83% per year as cotton, corn, and specialty-grain growers adopt zero-damage seed placement. The Brazil agricultural tractor machinery market size for sowing solutions is forecast to rise from USD 0.85 billion in 2025 to USD 1.42 billion in 2031. Domestic players such as Stara and Jacto offer pneumatic meters and variable-rate controllers that cut seed waste by 4% and reduce overlaps by up to 8%. Harvesting implements grow moderately because sugarcane mechanization already exceeds 90%. Fertilizer and pest-control sprayers gain momentum from precision-agriculture retrofits that trim input costs 10–15%.

Precision-ready implements feed a broader ecosystem shift. Jacto’s Lumina planter integrates cloud-based telemetry, allowing agronomists to adjust seeding depth in real-time. Kuhn’s VBP 3260 baler supports integrated crop-livestock systems that store higher-protein feed. Such innovations raise implement prices by 15–20% yet shorten payback through reduced inputs and higher yields, supporting the long-term growth of the Brazilian agricultural tractors machinery market.

Geography Analysis

Dealer and service networks remain concentrated in Brazil’s South and Southeast, even as production shifts northward. São Paulo hosts a significant number of dealerships, reflecting its OEM manufacturing base. Minas Gerais and Paraná follow closely, benefiting from coffee and grain demand. Rio Grande do Sul is emerging as a production node thanks to Mahindra’s assembly plant.

Mato Grosso accounts for a substantial portion of soybean production yet has a limited number of dealerships, creating after-sales gaps that lengthen downtime and restrict credit. Goiás gains from significant investments in ethanol that raise demand for sugarcane harvesters. The frontier Matopiba region produces a large share of combined soybean and corn output but commands a small percentage of dealerships, spotlighting white-space for distributors.

The Arco Norte corridor, ports of Itaqui, Barcarena, and Santarém, has seen considerable growth, shortening machinery transit times to northern states. John Deere’s Starlink roll-out, starting in Horizontina and Catalão factories, addresses connectivity gaps across a majority of farm areas, enabling remote diagnostics that reduce service trips significantly.

Competitive Landscape

The Brazil agricultural tractor machinery market is highly concentrated, Deere and Company, CNH Industrial, AGCO Corporation, Bucher Industries, and Stara together control maximum percentage of the 2025 revenue. Multinationals channel capital into autonomy, connectivity, and local production. John Deere invested BRL 3 billion (USD 600 million) in three factories plus a BRL 180 million (USD 36 million) tropical-agriculture technology center. CNH launched a fully Brazilian-built Axial-Flow 160 combine after a BRL 100 million (USD 20 million) upgrade to its Sorocaba plant.

Domestic champions leverage home-field advantages. Jacto’s partnership with DJI extends to agricultural drones, while Stara’s Zero Crop Damage planter claims 4% seed savings. Financing remains a key differentiator: Jacto and Stara offer annual rates of 6.99–9.99%, undercutting dealer financing tied to the Selic rate. Mahindra and Yanmar pursue the aged-fleet replacement cycle by adding 18 dealerships in 2024 alone and scaling local assembly capacity.

Importers face headwinds. Bucher Industries reported a significant drop in revenue in Brazil for 2024, as interest-rate spikes forced inventory write-downs. The ex-tarifário duty holiday, in effect through December 2025, provides temporary relief, domestic content rules and longer approval timelines weigh on new entrants.

Brazil Agricultural Tractor Machinery Industry Leaders

Deere & Company

AGCO Corporation

CNH Industrial N.V.

Bucher Industries AG

Stara S/A

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Case IH has initiated field testing of an ethanol-powered Puma 230 tractor in Brazil, in collaboration with São Martinho. This initiative aims to support agricultural decarbonization by utilizing renewable fuel to lower emissions while maintaining operational efficiency.

- August 2025: Yanmar announced an investment of BRL 280 million (USD 55 million) to establish a new tractor factory in Indaiatuba, Brazil. This initiative aims to increase production capacity and enhance Yanmar's presence in Brazil's agricultural machinery market.

- July 2025: Brazil has increased interest rates on farm equipment financing, potentially hindering the recovery of tractor sales. Higher borrowing costs are deterring farmers from purchasing new machinery, thereby slowing growth in the agricultural sector.

Brazil Agricultural Tractor Machinery Market Report Scope

A tractor is an industrial vehicle usually used to move the attached implement, which does the work of plowing the field or performing other activities. For this report, the tractors used in agricultural operations have been considered. The tractors used for industrial and construction purposes are also excluded from the scope of the study. The Brazilian agricultural tractors market is segmented by engine power into less than 80 HP, 81 to 130 HP, and above 130 HP. By application, it is segmented into row crop tractors, orchard tractors, and other applications. The report offers the market size and forecasts for volume (units) and value (USD) for all the above segments.

By Machinery Type

| Plowing and Cultivating Machinery | Plows |

| Harrows | |

| Rotovators and Cultivators | |

| Other Plowing and Cultivating Machinery | |

| Planting Machinery | Seed Drills |

| Planters | |

| Spreaders | |

| Other Planting Machinery | |

| Haying and Forage Machinery | Mowers and Conditioners |

| Balers | |

| Other Haying and Forage Machinery | |

| Sprayers | |

| Other Types |

| By Machinery Type | Plowing and Cultivating Machinery | Plows |

| Harrows | ||

| Rotovators and Cultivators | ||

| Other Plowing and Cultivating Machinery | ||

| Planting Machinery | Seed Drills | |

| Planters | ||

| Spreaders | ||

| Other Planting Machinery | ||

| Haying and Forage Machinery | Mowers and Conditioners | |

| Balers | ||

| Other Haying and Forage Machinery | ||

| Sprayers | ||

| Other Types | ||

Key Questions Answered in the Report

What is the current size of the Brazil agricultural tractor machinery market?

The Brazil agricultural tractor machinery market size stands at USD 3.98 billion in 2026.

How fast is the market anticipated to grow?

It is forecast to post a 4.75% CAGR and reach USD 5.02 billion by 2031.

Which implement type is growing the quickest?

Planting machinery are projected to grow at a 8.83% CAGR through 2031.

Why are high-horsepower tractors gaining traction?

Large estates are adopting above-130 horsepower autonomous-ready platforms to cover 5,000 to 10,000 hectares efficiently.

Page last updated on: