Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

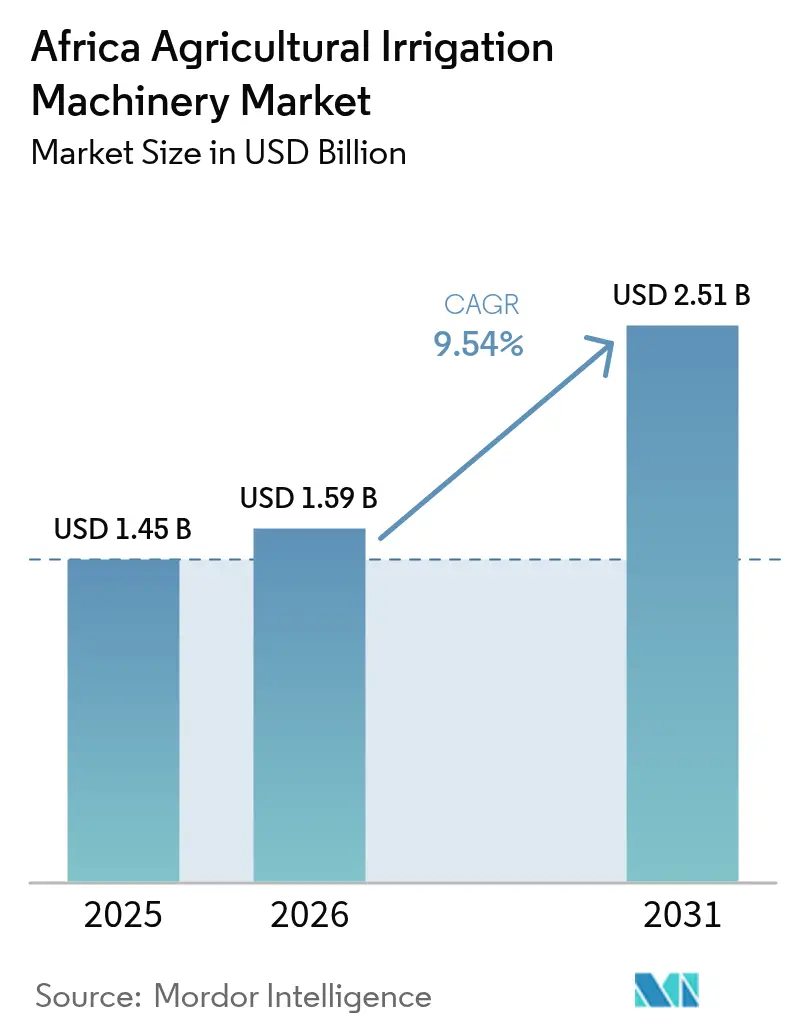

| Base Year Market Size (2025) | USD 1.45 Billion |

| Market Size (2026) | USD 1.59 Billion |

| Market Size (2031) | USD 2.51 Billion |

| Growth Rate (2026 - 2031) | 9.54% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Agricultural Irrigation Machinery Market Analysis by Mordor Intelligence

The Africa agricultural irrigation machinery market size was valued at USD 1.45 billion in 2025 and estimated to grow from USD 1.59 billion in 2026 to reach USD 2.51 billion by 2031, at a CAGR of 9.54% during the forecast period (2026-2031). Acute water stress, recurring droughts, and tightening water-use regulations are compelling growers to swap flood irrigation for precision systems that cut consumption by 30%–50%[1]Source: Food and Agriculture Organization, “AQUASTAT Global Water and Agriculture Data,” fao.org. South Africa’s Western Cape estates are driving large retrofits of center pivots and subsurface drip lines, while Egypt’s New Delta and Toshka mega-projects underpin double-digit growth in drip installations[2]Source: World Bank, “Agriculture Finance and Insurance,” worldbank.org. Government micro-irrigation subsidies, the rise of solar-powered pumps in off-grid zones, and rising climate-finance flows are expanding addressable demand faster than farm incomes, but currency volatility, high upfront capital expenditure, and skills shortages still moderate near-term uptake[3]Source: African Development Bank, “Sahel Irrigation Initiative,” afdb.org. Competitive intensity is increasing as agritech firms launch pay-per-use platforms that lower entry costs for fragmented smallholders, challenging incumbents that dominate large-estate sales.

Key Report Takeaways

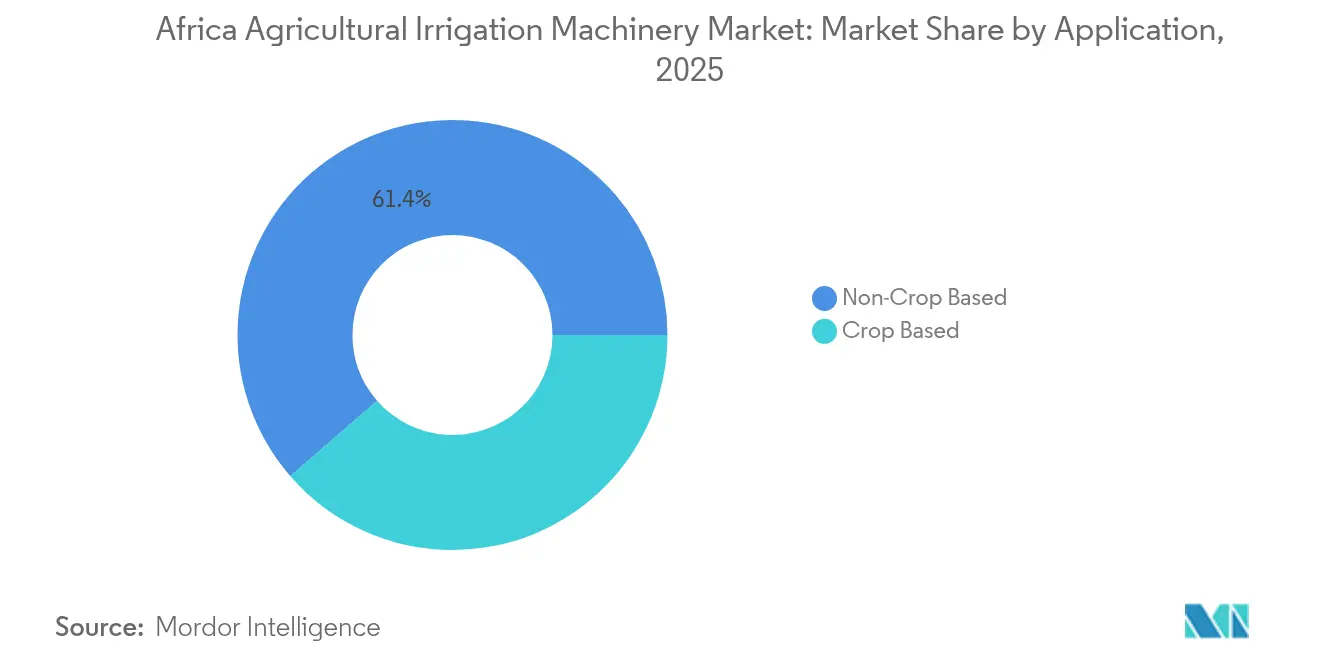

- By application, crop-based uses held a 38.60% Africa agricultural irrigation machinery market share in 2025; non-crop segments are forecast to expand at a 12.17% CAGR through 2031.

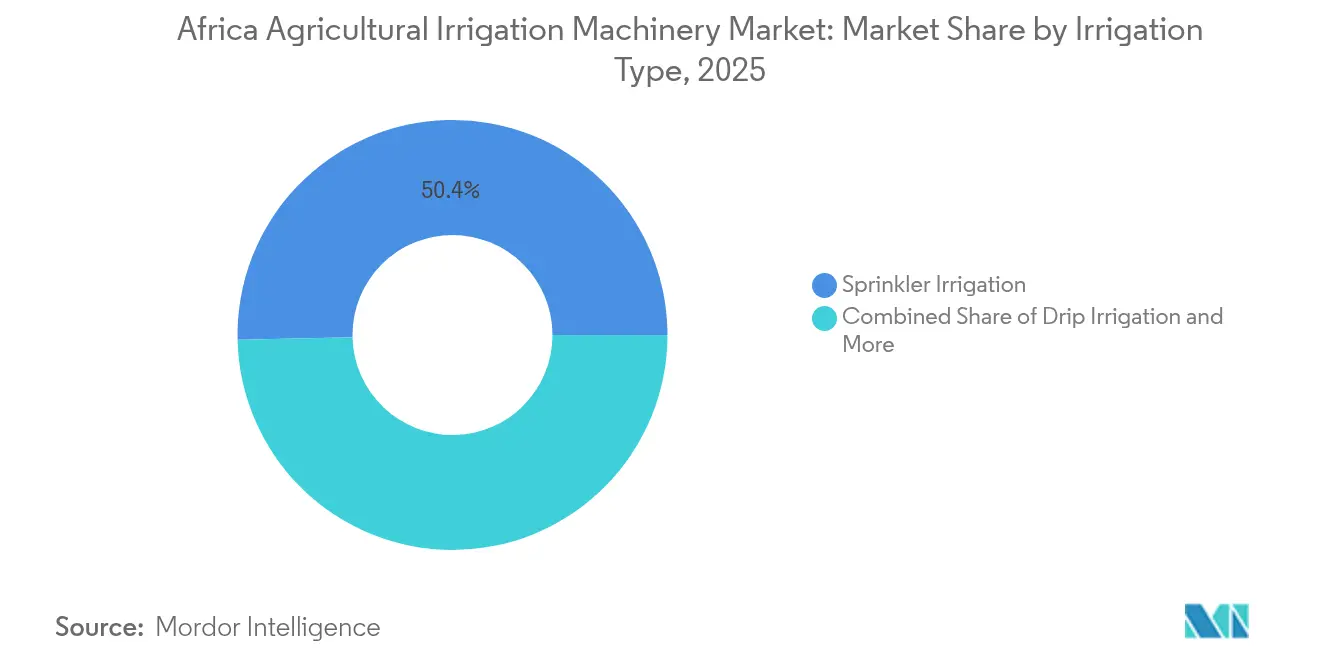

- By irrigation type, sprinklers led with 50.35% revenue share in 2025; drip systems are projected to register a 13.86% CAGR through 2031.

- By geography, South Africa accounted for 33.25% of 2025 revenue; Egypt is set to grow at an 10.74% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Agricultural Irrigation Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying water scarcity and food-security mandates | +2.5% | Global, acute in Sahel, Southern Africa, and North Africa | Medium term (2-4 years) |

| Expansion of government micro-irrigation subsidy schemes | +2.2% | Egypt, Morocco, South Africa, and Kenya | Short term (≤ 2 years) |

| Rapid pivot toward climate-smart agriculture financing | +1.8% | Global, concentrated in East Africa and Southern Africa | Medium term (2-4 years) |

| Mainstream adoption of center-pivot retrofits on large estates | +1.5% | South Africa, Kenya, Zambia, and Zimbabwe | Short term (≤ 2 years) |

| Underground drip systems for high-value horticulture niches | +1.2% | South Africa (Western Cape), Egypt (Nile Delta), Morocco | Medium term (2-4 years) |

| Agritech-enabled pay-per-use irrigation-as-a-service models | +0.9% | Kenya, Nigeria, Ghana, Rwanda, early gains in Ethiopia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Water Scarcity and Food Security Mandates

Only a small percentage of Africa's cultivated land is irrigated compared to a significantly higher proportion in Asia, even as the continent's population is anticipated to grow substantially, doubling food demand. Consecutive below-average rainy seasons in the Sahel have led to emergency drip-irrigation programs for rice and vegetable plots in countries such as Burkina Faso, Niger, and Mali. Southern Africa recently faced its most severe drought in decades, prompting efforts to retrofit precision irrigation systems on maize and soybean farmland. Water allocations from the Nile to Egypt have decreased, resulting in mandatory use of drip or sprinkler irrigation systems for new agricultural projects of a certain size. Projections indicate that water availability in North Africa will decline further, highlighting the importance of improving irrigation efficiency to ensure food security.

Expansion of Government Micro-Irrigation Subsidy Schemes

Egypt’s National Program for Lining Canals and Conversion to Modern Irrigation focuses on subsidizing a significant portion of equipment costs for small farms. Morocco’s Green Generation 2020–2030 program supports smallholder farmers by covering a large share of drip irrigation costs, with plans to expand micro-irrigation across a substantial area. In South Africa, efforts are underway to upgrade smallholder schemes with solar-powered drip irrigation kits. Kenya’s Galana-Kulalu project is expanding its coverage, integrating pivots and drip lines under a financial arrangement that includes a grant component. These initiatives significantly lower the capital expenditure for farmers, making modern irrigation systems more affordable.

Rapid Pivot toward Climate-Smart Agriculture Financing

Climate finance directed towards African agriculture has seen significant growth, with a substantial portion allocated to irrigation and other water-related projects. The Green Climate Fund has supported initiatives aimed at installing solar-powered drip irrigation systems across countries in the Sahel region. Similarly, the Adaptation Fund has introduced programs to co-finance precision irrigation in select Southern African nations, offering substantial subsidies. Investments have also been directed towards irrigation-as-a-service ventures, with returns linked to verified water savings. Additionally, regional policy alignment under the African Union’s resilience strategy requires member states to dedicate a portion of agricultural budgets to climate adaptation efforts, including the modernization of irrigation systems.

Mainstream Adoption of Center-Pivot Retrofits on Large Estates

In 2024, South Africa retrofitted a significant area of commercial maize and soybean farmland with new center pivots to comply with water-license caps limiting abstraction to a percentage of historical levels. Valmont Industries and Lindsay Corporation supplied pivots to Kenyan grain estates, incorporating variable-rate technology that improved water efficiency and boosted yields. In Zambia, the Agri-Kulima cooperative financed pivots across thousands of hectares through a loan from the Development Bank of Southern Africa, tied to water-efficiency benchmarks. Zimbabwe implemented a pilot project with solar-hybrid pivots, eliminating diesel costs and reducing CO₂ emissions annually. Compliance with ISO 11545 standards and national water-license audits is driving increased demand for retrofitting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capex versus traditional flood irrigation | -1.8% | Global, most acute in West Africa and smallholder zones | Short term (≤ 2 years) |

| Limited technical skills for precision-system maintenance | -1.3% | Sub-Saharan Africa, rural areas with low extension coverage | Medium term (2-4 years) |

| Foreign-exchange volatility affecting imported components | -1.1% | Egypt, Nigeria, Ghana, and Kenya | Short term (≤ 2 years) |

| Fragmented land holdings limiting economies of scale | -0.9% | West Africa, East Africa smallholder belts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex versus Traditional Flood Irrigation

Precision irrigation systems are significantly more expensive for smallholders compared to furrow infrastructure, making them inaccessible for the majority of growers. High interest rates for loans in Nigeria extend the payback period for drip irrigation systems, even though they result in notable yield improvements. In Ghana, the lack of formal land titles among many farmers limits their access to adequate microfinance loans, which are insufficient for implementing drip irrigation on typical farm sizes. In Tanzania, most smallholder irrigation schemes continue to rely on gravity-fed systems, as the upfront costs remain a major obstacle despite subsidies. Furthermore, dependence on imported parts increases costs due to regional tariff duties.

Limited Technical Skills for Precision-System Maintenance

Sub-Saharan Africa faces a significant shortage of trained irrigation technicians, with extension services reaching only a fraction of smallholder farmers. In Kenya, many drip irrigation kits fail within a few years due to issues such as clogged emitters and inadequate flushing protocols. An evaluation of Nigeria’s Fadama III project highlighted that a considerable number of drip installations were non-operational, caused by regulator faults and damaged laterals. In South Africa, irrigation schemes frequently experience downtime during breakdowns, resulting in reduced yields. Furthermore, low literacy levels among farmers in the region limit the adoption of digital monitoring tools that could automate maintenance alerts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Non-Crop Segments Gain as Urbanization Accelerates

Crop-based uses generated 38.60% of 2025 revenue in the African agricultural irrigation machinery market, led by maize, wheat, and soybean production on 280,000 hectares of center-pivot and drip-equipped estates in South Africa’s Free State and Mpumalanga regions. Non-crop segments turf, ornamental, and nursery irrigation are set to outpace with a 12.17% CAGR as urban landscaping proliferates in Lagos, Nairobi, and Johannesburg, and export floriculture expands in Kenya and Ethiopia. Turf applications logged a 14% year-on-year rise in 2024, due to weather-based sprinkler controllers that cut water use by 35% on golf courses, aligning with municipal restrictions.

The fruits and vegetables sub-segment is the fastest-growing within crop-based uses, driven by Egypt’s 85,000-hectare drip expansion for tomatoes, peppers, and citrus between 2024 and 2025. Africa agricultural irrigation machinery market size for fruits and vegetables is projected to advance at a 12.04% CAGR through 2031, aided by subsidies that defray up to 60% of drip costs. Oilseeds use pivots on 95,000 hectares yet lag due to lower per-hectare returns, while nursery crops now cover 12,000 hectares under micro-sprinklers that satisfy GlobalGAP water-efficiency rules for exports. Regulatory audits under Kenya’s Water Act 2016 further propel precision adoption across both crop and non-crop categories.

By Irrigation Type: Drip Systems Overtake Sprinklers in High-Value Crops

Sprinklers retained a 50.35% share of the Africa agricultural irrigation machinery market in 2025 after decades of dominance on large grain estates across South Africa, Kenya, and Zambia. Drip systems, are expanding at a 13.86% CAGR and already serve 310,000 hectares, spurred by subsidy coverage and a 12% drop in component prices as Chinese and Indian plants scale output. Pivot irrigation, a sprinkler subset, grew 9.8% in 2024 with 1,200 new units financed through blended loans tied to water-efficiency KPIs.

Africa agricultural irrigation machinery market size for drip lines in Egypt is increasing, reflecting the mandatory conversion of farms larger than 10 feddans. Africa's agricultural irrigation machinery market share for pivots is anticipated to decline marginally as variable-rate technology pushes efficiency but faces power-cost headwinds. Micro-sprinklers hold an 8.05% slice, favored by small vegetable plots in Nigeria and Ghana, where line pressure is low. Standards such as ISO 9260 for emitter performance now guide public procurement across Egypt, South Africa, and Kenya, steering the mix toward certified high-uniformity systems.

Geography Analysis

South Africa retained a 33.25% revenue share in the Africa agricultural irrigation machinery market during 2025, supported by 380,000 hectares of irrigated commercial farmland equipped with pivots for cereals and subsurface drip for citrus and vineyards. Mandatory water-use licences cap abstraction at 60% of historical allocations, compelling farmers to show 30%–40% savings before receiving new permits. Underground drip on citrus orchards now achieves over 85% application efficiency, meeting GlobalGAP export compliance.

Egypt is the fastest-growing geography at an 10.74% CAGR, underpinned by the reclamation in the New Delta and Toshka projects, where drip systems are obligatory to counter shrinking Nile flows. The canal-lining initiative subsidizes a significant portion of equipment costs for small farms and has already facilitated the adoption of drip irrigation systems on a large scale. Table-grape and citrus exporters have implemented precision drip irrigation, utilizing mobile app-based scheduling, achieving notable water savings compared to traditional furrow irrigation systems.

The Rest of Africa, including countries such as Kenya, Nigeria, Morocco, and Ethiopia, made a significant contribution to the revenue in 2025 and is anticipated to experience steady growth through 2031. In Kenya, advanced drip and sprinkler systems were implemented under the Galana-Kulalu project. Additionally, floriculture investors installed climate-controlled drip irrigation systems, boosting export revenue. Morocco expanded its micro-irrigation coverage, supported by a subsidy program, which facilitated the adoption of subsurface drip irrigation in olive and almond orchards.

Competitive Landscape

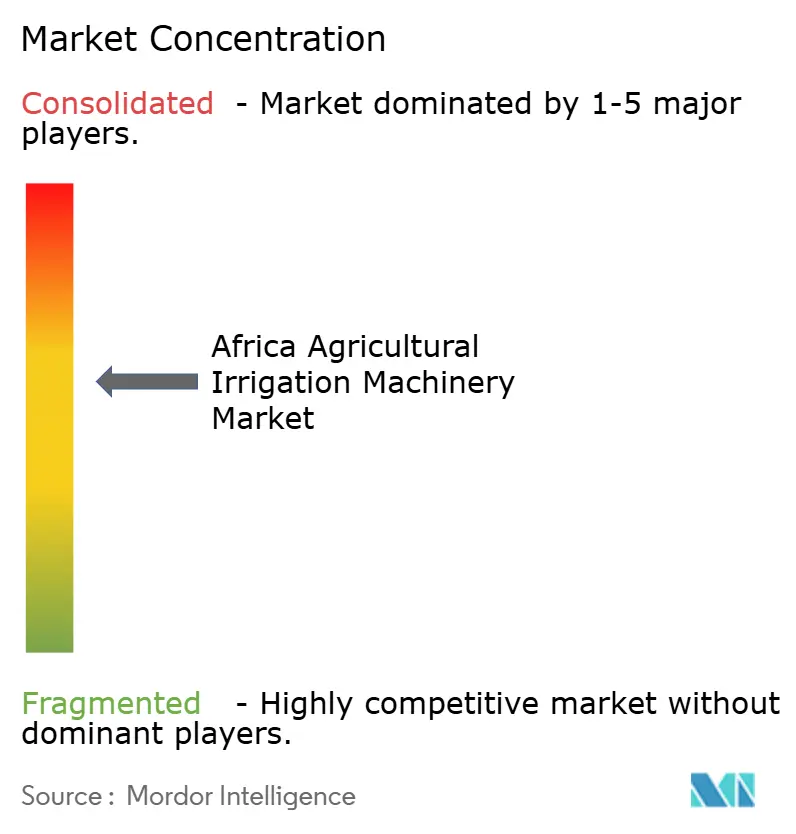

The Africa agricultural irrigation machinery market is moderately concentrated, with a few key players dominating the market. Companies like Netafim, Valmont, Lindsay, Rain Bird, and Rivulis are prominent, competing on aspects such as product durability, after-sales service, and financing partnerships with multilateral banks. Netafim has expanded its platform to cover significant agricultural areas in Kenya and South Africa. This platform integrates advanced technologies like sensors, satellite imagery, and automated fertigation, leading to notable improvements in labor efficiency and crop yields.

Valmont and Lindsay focus on providing pivot retrofits tailored for large agricultural estates. Recent developments have seen the addition of advanced pivots with variable-rate controllers to enhance grain farming operations in South Africa. Rivulis has introduced innovative pressure-compensating emitters with anti-siphon technology, designed for underground installations. This technology has gained traction in the subsurface drip irrigation segment across Egypt and South Africa.

Emerging agritech companies are driving disruption in the market by offering bundled solutions that combine hardware, agronomy services, and micro-financing through mobile-money platforms. These solutions are particularly beneficial for smallholders with limited landholdings. Additionally, companies like Hunter Industries and Rain Bird are addressing the growing demand in the commercial landscaping and turf segments. These segments are expanding rapidly due to urban water-efficiency mandates, with weather-based controllers and telemetry systems offering automated reporting to meet stricter government audit requirements.

Africa Agricultural Irrigation Machinery Industry Leaders

Netafim Limited (Orbia Advance Corporation)

Valmont Industries

Lindsay Corporation

Rain Bird Corporation

Rivulis (Temasek Holdings)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Netafim is transforming farming in Kenya with precision drip irrigation systems that optimize water use and boost yields. This initiative strengthens the Africa irrigation machinery market, driving sustainable and technology-driven agricultural practices.

- September 2025: KickStart International has entered Senegal with low-cost irrigation tools aimed at empowering smallholder farmers. This initiative expands access to the Africa irrigation machinery market, promoting affordable mechanisation and improved water management.

- October 2024: Netafim, under Orbia Precision Agriculture, unveiled groundbreaking precision irrigation innovations at EIMA 2024 in Italy. These solutions reinforce its leadership in the global irrigation machinery market, focusing on sustainability and smart water management.

Africa Agricultural Irrigation Machinery Market Report Scope

Agricultural irrigation machinery refers to equipment used to supply water to farmland and crops, promoting hydration and growth. This report provides a comprehensive analysis of Africa's agricultural irrigation machinery market size. The market is segmented by irrigation type (sprinkler irrigation, drip irrigation, pivot irrigation, and other irrigation types), application type (crop and non-crop), and geography (South Africa, Egypt, and the rest of Africa). The report offers market size and forecasts in terms of value (USD) for all the above segments.

By Application

| Food Crop Based | Cereals and Grains |

| Oilseeds | |

| Fruits and Vegetables | |

| Non-Food Crop Based | Turf and Ornamental |

| Nursery Crops |

By Irrigation Type

| Sprinkler Irrigation |

| Drip Irrigation |

| Pivot Irrigation |

| Other Irrigation Types |

By Geography

| South Africa |

| Egypt |

| Rest of Africa |

| By Application | Food Crop Based | Cereals and Grains |

| Oilseeds | ||

| Fruits and Vegetables | ||

| Non-Food Crop Based | Turf and Ornamental | |

| Nursery Crops | ||

| By Irrigation Type | Sprinkler Irrigation | |

| Drip Irrigation | ||

| Pivot Irrigation | ||

| Other Irrigation Types | ||

| By Geography | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the Africa agricultural irrigation machinery market?

The market reached USD 1.59 billion in 2026 and is projected to hit USD 2.51 billion by 2031.

Which irrigation type is growing fastest across Africa?

Drip systems are advancing at a 13.86% CAGR, propelled by subsidies and water-efficiency mandates.

Why is Egypt the fastest-growing geography for irrigation machinery?

Large-scale land reclamation and a 60% subsidy on micro-irrigation hardware are driving an 10.74% CAGR through 2031.

How are smallholders overcoming high upfront costs?

Pay-per-use platforms bundle solar pumps, drip lines, agronomy advice, and mobile-money payments.

Page last updated on: