Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

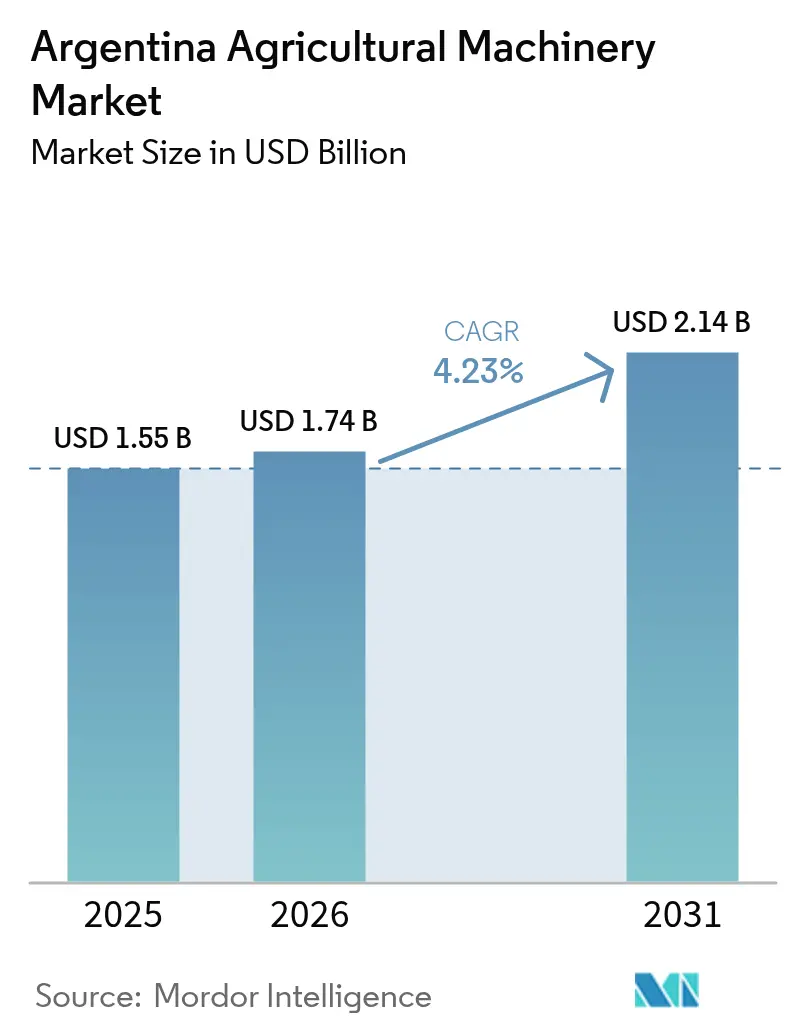

| Base Year Market Size (2025) | USD 1.55 Billion |

| Market Size (2026) | USD 1.74 Billion |

| Market Size (2031) | USD 2.14 Billion |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

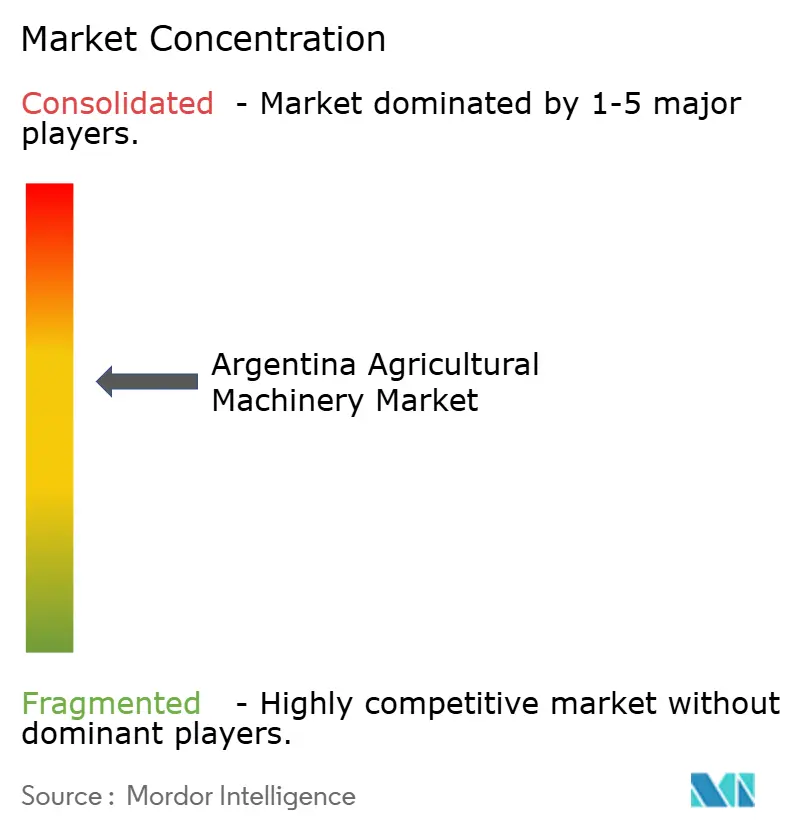

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Agricultural Machinery Market Analysis by Mordor Intelligence

The Argentina agricultural machinery market size is projected to grow from USD 1.55 billion in 2025 to USD 1.74 billion in 2026 and is forecast to reach USD 2.14 billion by 2031 at a 4.23% CAGR over 2026-2031. The rebound follows the severe 2023-2024 drought that cut farm output and drove machinery sales into steep decline, but sweeping tariff reductions on both exports and imported capital goods are now stimulating purchasing cycles. According to the Foreign Agricultural Service (FAS) of the US Department of Agriculture, record grain and oilseed harvests in 2025, led by 27.5 million metric tons of wheat and a projected 58 million metric tons of corn, have restored producer liquidity and sparked a rush to replace aging fleets with precision-ready tractors, combines, and planters [1]Source: Foreign Agricultural Service, “Argentina – Grain and Feed Annual,” fas.usda.gov. Chinese low-cost tractors have entered through non-traditional channels, pressuring prices and accelerating technology bundling by long-time leaders. Meanwhile, climate-finance inflows and carbon-credit programs are making sensor-rich implements and low-tillage equipment affordable in water-stressed regions, adding structural demand to the Argentina agricultural machinery market.

Key Report Takeaways

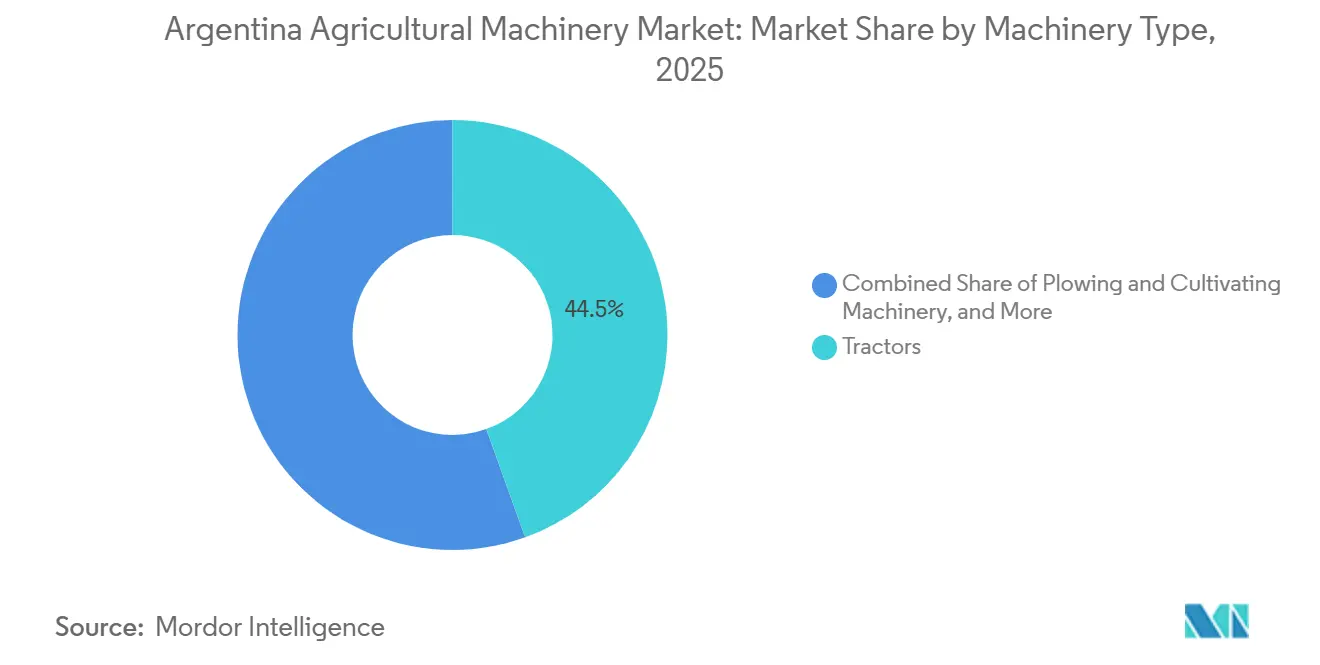

- By machinery type, tractors led with 44.5% of the Argentina agricultural machinery market share in 2025, and irrigation machinery is forecast to expand at a 5.4% CAGR through 2031, the fastest pace among all product segments, reflecting chronic water scarcity in Cuyo and the Northwest.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Agricultural Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor-cost inflation accelerates mechanization uptake | +0.8% | National, concentrated in Pampa Húmeda grain belt | Medium term (2-4 years) |

| Access to multilateral climate-finance for ag-tech upgrades | +0.6% | National, priority in drought-prone Cuyo and Northwest | Medium term (2-4 years) |

| 5G connectivity unlocking real-time machine-to-machine farming | +0.5% | Buenos Aires, Córdoba, and Santa Fe fringe zones | Long term (≥ 4 years) |

| Carbon-credit premiums for low-tillage machinery | +0.6% | National, leveraging 90% no-till adoption | Medium term (2-4 years) |

| On-farm data monetization spurring sensor-rich implements | +0.4% | Estates above 1,000 hectares in Pampa Húmeda | Long term (≥ 4 years) |

| Electrification of specialty orchard and vineyard tractors | +0.2% | Mendoza wine region and Patagonia orchards | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labor-Cost Inflation Accelerates Mechanization Uptake

Agricultural wages increased in peso terms during 2024, but the concurrent currency depreciation raised dollar-denominated labor costs, driving up daily harvest expenses. Declining rural labor availability is prompting grain producers in Buenos Aires and Córdoba to adopt autonomous sprayers and GPS-guided planters, which can achieve a return on investment within three crop cycles. These technologies not only address labor shortages but also enhance operational efficiency and precision in farming practices. The tariff reductions implemented in July 2025 lowered the landed cost of precision equipment, making replacements more accessible even for mid-sized farms. This policy change has encouraged farmers to upgrade their machinery, further boosting productivity. A single autonomous tractor can replace four to six seasonal workers on a 500-hectare farm, while variable-rate applicators help minimize fertilizer waste by applying inputs more accurately. These combined factors are driving increased demand for agricultural machinery in the Argentine market, as farmers seek to optimize costs and improve yields.

Access to Multilateral Climate-Finance for Ag-Tech Upgrades

The World Bank, the Inter-American Development Bank, and the Development Bank of Latin America and the Caribbean have collectively pledged to support climate-smart farming technologies. These funds are offered at significantly lower interest rates than local peso loan rates [2]Source: World Bank, “Argentina Overview,” worldbank.org. The financing is directed toward initiatives such as drip irrigation systems and low-tillage planters in regions like Mendoza and the semi-arid Northwest, where only a limited portion of farmland is irrigated. Producers can combine concessional loans with proceeds from carbon credits, effectively subsidizing the cost of machinery. This combination of affordable financing and additional revenue streams is driving increased adoption among cooperatives and smallholders, contributing to steady growth in the Argentina agricultural machinery market.

5G Connectivity Unlocking Real-Time Machine-to-Machine Farming

Argentina's commercial 5G deployment began in 2024, and by late 2025, operators had activated rural towers. However, coverage remains limited, falling short of the nation's cropland. Sub-50-millisecond latency enables autonomous tractors to adjust seeding or spraying rates in real time, improving yields in pilot projects. This technology has the potential to revolutionize farming practices by enabling more precise and efficient operations, reducing waste, and optimizing resource use. Satellite loans aim to extend broadband access to rural homes by 2028. Until then, many farms rely on offline precision machinery that uploads data later, limiting immediate benefits. Nevertheless, long-term advancements in connectivity are projected to drive digital integration, significantly impacting the agricultural machinery market in Argentina. These improvements are anticipated to enhance productivity, reduce operational costs, and support sustainable farming practices in the region.

Electrification of Specialty Orchard and Vineyard Tractors

Electric tractors currently account for a very small portion of Argentina's specialty-crop fleet. However, pilot programs in Mendoza and Patagonia have demonstrated significantly lower operating energy costs and the elimination of tailpipe emissions. These features are particularly valued by exporters targeting European Union retailers, which enforce strict carbon and residue standards. Despite upfront costs being considerably higher than diesel counterparts and the limited availability of rural charging infrastructure, declining battery prices and climate-focused loans are projected to enhance the economic viability of electric tractors in the long term. As vineyards and fruit orchards increasingly adopt these units, a niche yet rapidly growing segment is anticipated to develop within Argentina's agricultural machinery market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency-linked credit risk for farm equipment loans | −0.8% | National, acute in smaller-farm provinces | Short term (≤ 2 years) |

| Cyber-vulnerability in autonomous equipment controls | −0.5% | Zones more than 200 km from urban cores | Medium term (2-4 years) |

| Shortage of rural ultra-fast broadband backhaul | −0.4% | Northwest and Patagonia | Long term (≥ 4 years) |

| Scarcity of certified technicians for advanced powertrains | −0.3% | Estates deploying autonomous fleets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Rural Ultra-Fast Broadband Backhaul

The limited availability of ultra-fast broadband backhaul in rural areas poses a significant challenge to the adoption of modern, data-intensive agricultural machinery. As farming increasingly relies on precision agriculture enabled by real-time data from autonomous or smart tractors, IoT sensors, and drones, the lack of high-speed, reliable, and cost-effective internet connectivity in these regions hampers modernization, productivity, and sustainability efforts. High deployment costs in low-density regions, coupled with currency fluctuations, pose significant investment barriers, limiting connectivity primarily to urban centers. Very few croplands receive 25 megabits per second service, so many growers cannot take advantage of the real-time telematics required for autonomous operation [3]Source: National Communications Entity, “Conectividad Rural,” enacom.gob.ar. Although satellite initiatives are projected to improve coverage, the persistent issue of high latency continues to impede sub-field logistics. The fiber expansion under Santa Fe’s More Connected program holds significant promise but is not projected to be finalized for several years, leaving connectivity as an ongoing medium-term obstacle to the adoption of smart agricultural machinery in Argentina.

Cyber-Vulnerability in Autonomous Equipment Controls

GPS spoofing and ransomware incidents in other countries underscore the risks associated with Argentina's expanding fleet of smart machinery. These incidents highlight vulnerabilities in connected systems, which could lead to operational disruptions and financial losses. While standards such as ISO 15998 are available to mitigate such risks, their adoption remains voluntary, and only a limited number of dealers have implemented network segmentation or intrusion-detection protocols. The lack of widespread implementation of these measures leaves the smart machinery network exposed to potential cyber threats. Insurance products addressing cyber disruptions are still in their early stages, which is contributing to investor hesitancy about fully autonomous deployments in the Argentina agricultural machinery market. This cautious approach reflects concerns about the market's readiness to address cybersecurity challenges effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Tractors Anchor Market Value Amid Precision Upgrades

Tractors are the largest machinery segment and commanded 44.5% of the Argentina agricultural machinery market share in 2025, underpinned by their essential role in tillage, planting, and logistics across grain land. Units between 40 and 99 horsepower make up roughly 55% of registrations, serving the typical 500-to-2,000-hectare farm. Between January and September 2025, Deere & Company accounted for 38.5% of all tractor registrations, representing 1,561 units. This performance occurred in a market totaling 4,057 units, reflecting an 8.2% increase compared to the same period in the previous year. According to the National Institute of Statistics and Censuses (INDEC), in 2024, the total number of machines sold was 16.103, a 4% drop from the previous year and a 17% drop from the average of the last five years. Despite a dip in overall machinery, including tractor registrations, during the 2024 credit crunch, the 2025 export-tax cuts triggered a forecast 20% rebound in orders, reinforcing tractors as the linchpin of the Argentina agricultural machinery market.

Irrigation systems represent a smaller base today but are the fastest-growing segment and are forecast to expand at a 5.4% CAGR through 2031 in the Argentina agricultural machinery market. Valmont Industries, Inc. and Lindsay Corporation dominate center-pivot projects for large grain farms, while Netafim Limited excels in drip technology for vineyards and orchards. Multilateral climate funds for precision irrigation, creating blended finance packages that bring system paybacks within seven years, even at current water tariffs. Carbon-credit revenue from reduced pumping emissions sweetens returns and encourages smaller growers to adopt. The Argentina agricultural machinery market size for irrigation is forecast to grow, highlighting a structural shift toward climate resilience.

Geography Analysis

The Pampa Húmeda provinces of Buenos Aires, Córdoba, Santa Fe, and Entre Ríos account for a significant share of Argentina's national grain production and agricultural equipment spending, making the region the economic center of the country's agricultural machinery market. Buenos Aires leads in tractor and combine registrations due to the prevalence of larger holdings, which justify the use of autonomous fleets. Córdoba benefits from its proximity to CNH Industrial N.V.’s manufacturing facility and its skilled dealers, which drive the adoption of advanced guidance systems. Santa Fe's "More Connected" fiber program is reducing the digital divide, enabling real-time fleet management. In contrast, Entre Ríos, characterized by smaller average farm sizes, focuses on mid-range horsepower equipment with lower levels of automation.

Outside the grain belt, the Cuyo region, comprising Mendoza, San Juan, and La Rioja, contributes significantly to Argentina's agricultural machinery market value. Persistent drought conditions and the expansion of vineyards have led to increased demand for drip irrigation systems and compact specialty tractors. In the Northwest provinces of Salta, Tucumán, and Jujuy, spending is focused on sugarcane, citrus, and tobacco harvesters, driven by rising labor costs that encourage mechanization. Although Patagonia accounts for only a small portion of national sales, it is emerging as a testing ground for electric tractors, aimed at meeting stringent European retailer standards for fruit exports.

Geographic disparities in access to credit, broadband, and technical support influence future developments. Córdoba offers equipment tax rebates linked to precision features, while Santa Fe provides subsidies for fiber backhaul supporting cloud-based platforms. Buenos Aires lags in rural broadband, limiting live data sharing beyond a 100-kilometer radius from the capital. Remote Northwest and Patagonia face 500-kilometer journeys to service centers, lengthening downtime and weakening the business case for complex electronics. These divergences suggest that the Argentina agricultural machinery market will see faster growth in water-scarce regions and technologically proactive provinces, while equipment penetration in fringe zones hinges on concurrent improvements in credit and connectivity.

Competitive Landscape

Argentina’s agricultural machinery arena shows moderate concentration. Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, and Mahindra & Mahindra Limited accounted for significant market revenue in 2025. Deere & Company sustains a significant tractor and combine share by bundling its Operations Center data platform with hardware and embedding subscription revenue into every deal. CNH Industrial N.V. capitalizes on domestic assembly in Córdoba to quote in pesos and shorten delivery, an edge during currency swings. AGCO Corporation pushes its premium Fendt line for estates that already profit from carbon credits and need autonomy-ready powertrains, yet high pricing limits mid-tier uptake in the Argentina agricultural machinery market.

Disruption is brewing. About 4,000 Chinese tractors entered via informal importers in 2024, undercutting prices by as much as 40% yet offering limited precision features. Domestic implement specialists like Crucianelli and Metalfor exploit this middle space with lower-cost, locally serviced equipment tailored to 500-to-1,000-hectare farms overlooked by global giants. Precision-irrigation leaders Netafim Limited, Lindsay Corporation, and Valmont Industries, Inc. compete largely outside the tractor majors’ core skill sets, capturing a segment growing faster than tillage machinery. Technology stakes are high: AGCO Corporation’s USD 2.0 billion buyout of the PTx Trimble joint venture in April 2024 underscores the race to own data ecosystems and analytics margins that may exceed iron margins after 2028.

Policy changes influence market competition. The absence of clear cybersecurity or data-sovereignty regulations benefits established players with the resources to draft indemnities and maintain in-house legal teams. Leading companies address this by offering integrated solutions that combine machinery, software, financing, and agronomic consulting, thereby increasing customer dependency but also raising capital requirements. As a result, the agricultural machinery market in Argentina is becoming segmented. Precision-focused fleets are prevalent in the Pampa Húmeda region, while cost-sensitive buyers in peripheral areas prefer domestic equipment and gray-market imports.

Argentina Agricultural Machinery Industry Leaders

Deere & Company

CNH Industrial N.V.

AGCO Corporation

Kubota Corporation

Mahindra & Mahindra Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Fendt, a premium agricultural machinery brand under AGCO Corporation, has entered the Argentine market, further expanding its presence in South America beyond Brazil and Paraguay. The brand plans to introduce its Fendt Gold Star program in Argentina, which includes a three-year factory warranty and remote performance monitoring.

- November 2025: Crucianelli, an Argentina-based leader in agricultural machinery, has implemented the Siemens Xcelerator business platform to enhance its product development and manufacturing processes. The Dómina seeder, a new piece of machinery, was fully designed using Siemens software to help farmers optimize yield per hectare.

- March 2025: Captain Tractors has entered the Argentine market through a strategic partnership with VIALCAM S.A. (GROSSPAL), an agricultural manufacturer based in Las Varillas, to commence sales operations.

Argentina Agricultural Machinery Market Report Scope

Agricultural machinery refers to mechanical equipment and tools used to perform farm operations such as plowing, planting, irrigation, harvesting, and post-harvest processing, aimed at improving efficiency and productivity in agriculture.

The Argentina agricultural machinery market report is segmented by machinery type, including tractors, plowing and cultivating machinery, planting machinery, harvesting machinery, haying and forage machinery, irrigation machinery, and other machinery types. The market forecasts are provided in terms of value in USD.

By Machinery Type

| Tractors | Less than 40 HP |

| 40-99 HP | |

| Greater than 100 HP | |

| Plowing and Cultivating Machinery | Ploughs |

| Harrows | |

| Cultivators and Tillers | |

| Other Plowing and Cultivating Machinery | |

| Planting Machinery | Seed Drills |

| Planters | |

| Spreaders | |

| Other Planting Machinery | |

| Harvesting Machinery | Combine Harvesters |

| Forage Harvesters | |

| Other Harvesting Machinery | |

| Haying and Forage Machinery | Mowers |

| Balers | |

| Other Haying and Forage Machinery | |

| Irrigation Machinery | Sprinkler Irrigation |

| Drip Irrigation | |

| Other Irrigation Machinery | |

| Other Machinery Types |

| By Machinery Type | Tractors | Less than 40 HP |

| 40-99 HP | ||

| Greater than 100 HP | ||

| Plowing and Cultivating Machinery | Ploughs | |

| Harrows | ||

| Cultivators and Tillers | ||

| Other Plowing and Cultivating Machinery | ||

| Planting Machinery | Seed Drills | |

| Planters | ||

| Spreaders | ||

| Other Planting Machinery | ||

| Harvesting Machinery | Combine Harvesters | |

| Forage Harvesters | ||

| Other Harvesting Machinery | ||

| Haying and Forage Machinery | Mowers | |

| Balers | ||

| Other Haying and Forage Machinery | ||

| Irrigation Machinery | Sprinkler Irrigation | |

| Drip Irrigation | ||

| Other Irrigation Machinery | ||

| Other Machinery Types | ||

Key Questions Answered in the Report

What is the projected value of the Argentina agricultural machinery market in 2031?

It is forecast to reach USD 2.14 billion by 2031, growing at 4.23% CAGR from 2026.

Which equipment category currently holds the largest share of sales?

Tractors account for 44.5% of 2025 market value, the biggest slice of spending.

Why is irrigation machinery the fastest-growing segment?

Chronic drought in Cuyo and the Northwest plus concessional climate finance push system adoption at 5.4% CAGR through 2031.

How are carbon credits influencing machinery purchases?

No-till farms can earn USD 15-USD 25 per metric ton of carbon dioxide equivalent, offsetting 30%-40% of equipment costs over five years.

Page last updated on: