Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

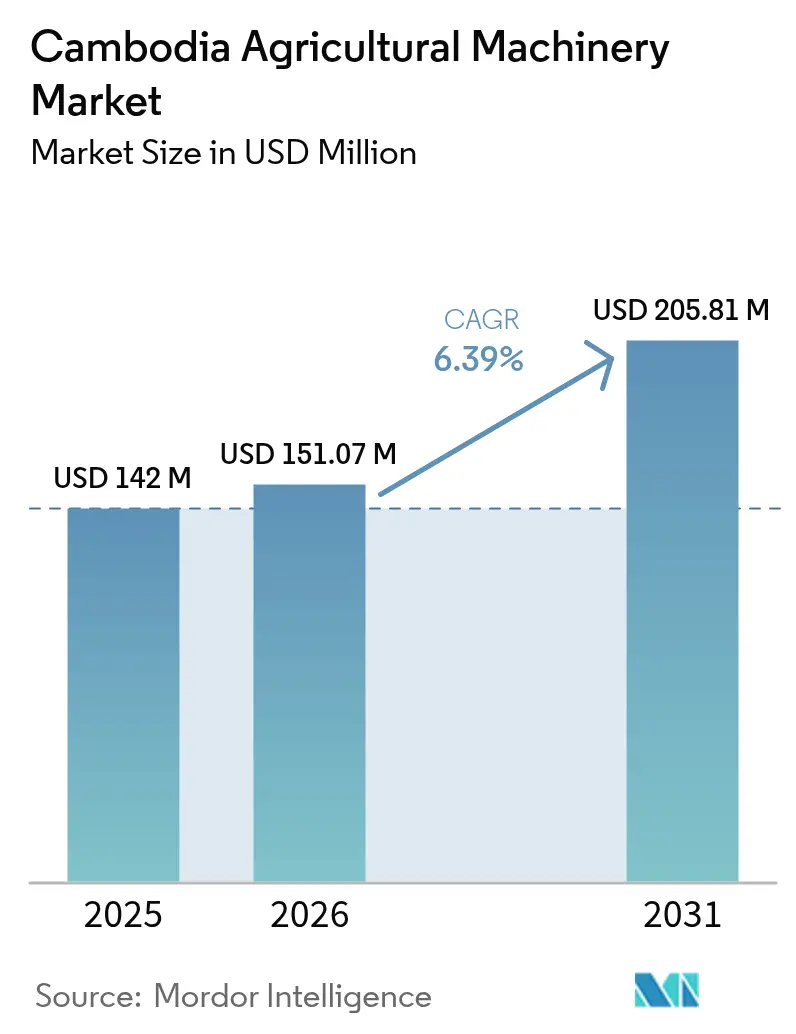

| Base Year Market Size (2025) | USD 142.0 Million |

| Market Size (2026) | USD 151.07 Million |

| Market Size (2031) | USD 205.81 Million |

| Growth Rate (2026 - 2031) | 6.39% CAGR |

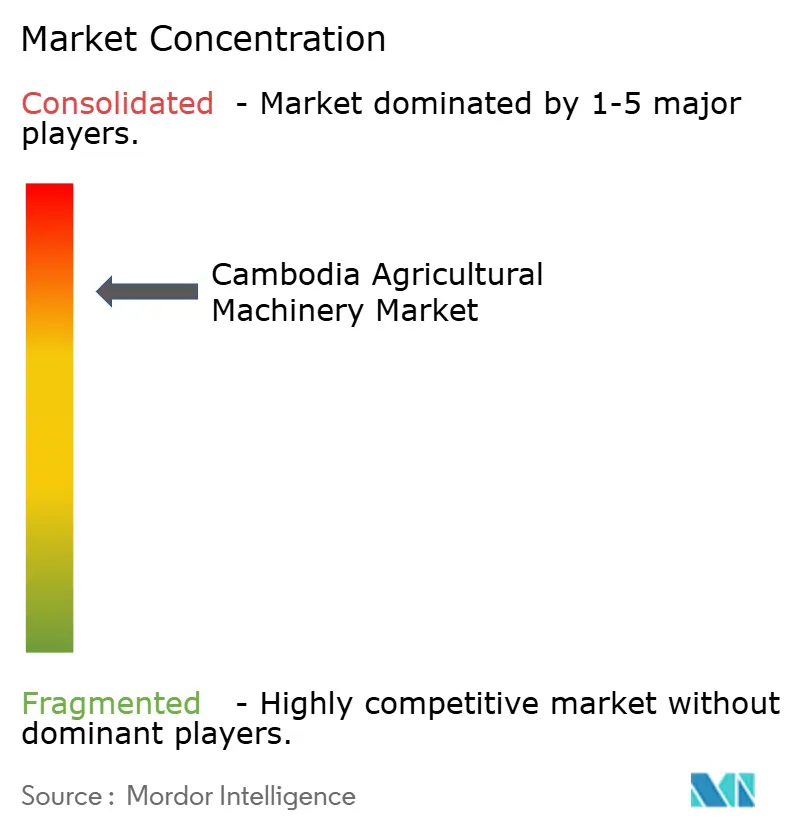

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cambodia Agricultural Machinery Market Analysis by Mordor Intelligence

Cambodia agricultural machinery market size in 2026 is estimated at USD 151.07 million, growing from 2025 value of USD 142.0 million with 2031 projections showing USD 205.81 million, growing at 6.39% CAGR over 2026-2031. This growth trajectory reflects the country's strategic pivot toward agricultural modernization as it aims to become one of the world's top 10 agricultural producers by 2030. Rising rice export targets, pressure to curb post-harvest losses, and foreign investment in large plantations shape a market environment where tractors remain dominant, but precision technologies, such as laser land leveling and combine harvesters, gain ground. Custom-hire service models lower capital barriers for smallholders, while public-private partnerships accelerate rural access to equipment. The sector’s progress is tempered by patchy after-sales networks, high repair costs, and persistent reliance on draught animals in remote provinces.

Key Report Takeaways

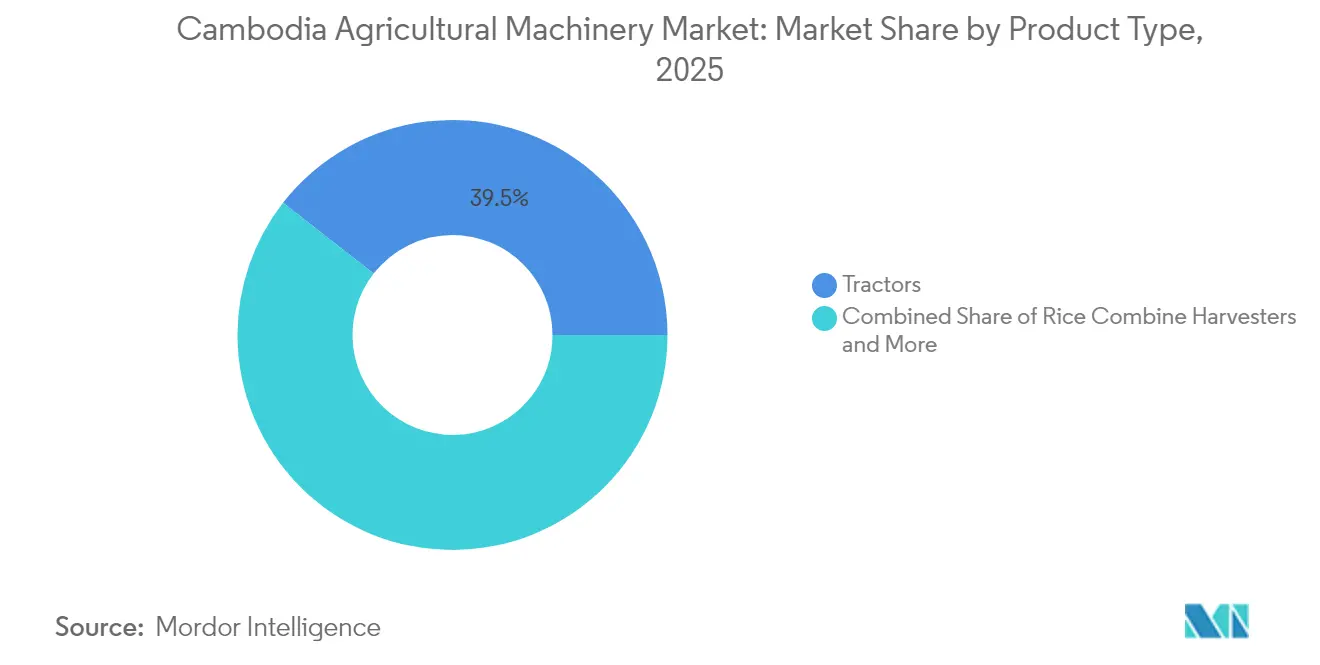

- By product type, the tractors segment held a 39.45% of the Cambodia agricultural machinery market share in 2025, while rice combine harvesters are advancing at a 9.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Cambodia Agricultural Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government subsidy scheme for two-wheel tractors | +1.2% | National, rice provinces | Medium term (2-4 years) |

| Increasing focus on sustainable agricultural mechanization | +0.9% | National, early adoption on plantations | Long term (≥ 4 years) |

| Rising public-private partnerships for custom-hire centers | +1.1% | Battambang, Siem Reap, Kampong Thom | Medium term (2-4 years) |

| Improved micro-finance access for machinery purchases | +0.8% | Rural smallholder zones | Short term (≤ 2 years) |

| Expansion of contract-farming by rice millers | +1.0% | Mekong Delta border areas | Medium term (2-4 years) |

| Adoption of laser land-leveling to conserve water | +0.7% | Irrigated, drought-prone provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Subsidy Scheme for Two-Wheel Tractors

The national subsidy program allocates a portion of the USD 100 million modernization fund to small two-wheel tractors that match the average farm size of 1.2 hectares prevalent among Cambodia’s 2.1 million smallholder households. Implemented through provincial agriculture departments, the scheme lowers upfront costs by pairing tax incentives with microloans, encouraging local dealers to stock parts and provide basic servicing. Differentiating from neighboring Vietnam’s preference for larger four-wheel units, Cambodia is cultivating a unique compact-tractor niche that fits narrow field layouts and minimizes soil compaction.

Increasing Focus on Sustainable Agricultural Mechanization

Laser land-leveling delivers twin benefits of 24% higher paddy yields and up to 47% lower irrigation water use, which aligns with Cambodia’s Paris Agreement commitments and unlocks eligibility for climate finance facilities.[1]Source: International Rice Research Institute, “GHG Mitigation in Rice – Laser land leveling,” irri.org Commercial estates have begun bundling the technology with alternate wetting and drying irrigation promoted in regional demonstration plots by Kubota Corporation, pointing toward a future where precision farming becomes integral to greenhouse-gas mitigation strategies.

Improved Micro-Finance Access for Machinery Purchases

Eighty-one licensed microfinance institutions now offer equipment loans averaging USD 4,200, a size that suits two-wheel tractors and low-horsepower power tillers. Bundling credit with contract-farming agreements reduces default risk and helps prevent distress land sales that were previously linked to collateralized loans. The state-owned Agriculture and Rural Development Bank steers concessional lines to lenders that meet rural outreach targets.

Expansion of Contract Farming by Rice Millers

Amru Rice Co., Ltd., producer and exporter of Cambodian rice, has expanded its contract farming network from 3,600 growers in 2022 to over 15,000 by 2025, reflecting a strategic push toward inclusive and sustainable rice production in Cambodia. The company ensures guaranteed paddy off-take and delivers technical guidance to farmers, including mechanization standards aligned with Sustainable Rice Platform (SRP) certification. This approach not only improves productivity and environmental compliance but also strengthens farmer resilience on agricultural machinery. These investments enhance grain quality, promote machinery upgrades across farming clusters, and support market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heavy reliance on conventional farming practices | -1.4% | Remote traditional areas | Long term (≥ 4 years) |

| Higher repair and maintenance costs of farm machinery | -1.1% | Provinces with poor service access | Medium term (2-4 years) |

| Shortage of skilled machinery operators | -0.9% | National, especially new mechanization zones | Short term (≤ 2 years) |

| Fragmented after-sales service network | -0.8% | Outside major commercial centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heavy Reliance on Conventional Farming Practices

Fuel cost spikes that doubled diesel prices to a high rate in 2024 prompted many smallholders to revert to draught animals, illustrating how economic shocks can derail machinery adoption. Cultural preference for familiar ox-based methods persists in isolated villages, where generational knowledge transfer underpins risk-averse attitudes toward new technology. Integration programs that pair mechanical weeders with the System of Rice Intensification demonstrate a hybrid path that respects tradition while introducing labor-saving devices.

Shortage of Skilled Machinery Operators

Vocational curricula lag behind the complexity of modern combine harvesters and precision implements. Research indicates limited availability of operators trained in GPS guidance and digital farm management, particularly in newly mechanized provinces. Short-duration courses offered through the UN Economic and Social Commission for Asia-Pacific help fill some gaps, yet coverage remains limited relative to the growing number of machine populations.[2]Source: United Nations ESCAP, “Regional UN training promotes conservation agriculture,” unescap.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Compact Tractors Dominate While Harvesters Accelerate

Tractors held a 39.45% market share of the Cambodian agricultural machinery market in 2025, with the sub-40-horsepower category reflecting the widespread use of one-hectare farm sizes. The Cambodia agricultural machinery market size allocated to tractors is projected to grow steadily as government subsidies favor compact, fuel-efficient models suited to narrow paddies. Combine harvesters, although accounting for a smaller revenue base, are expanding at a 9.41% CAGR because they reduce 15-20% of post-harvest losses associated with manual cutting and beating. Power tillers and diesel engines with a power output of below 10 horsepower remain staples for land preparation and irrigation pumping, respectively, providing smallholders with modular mechanization pathways.

Kubota Corporation’s GPS-ready mini tractors and Yanmar Holdings Co., Ltd.’s ergonomic SM series exemplify how precision features trickle down to lower-horsepower classes. While tractors with engines exceeding 100 horsepower see limited adoption due to land fragmentation, plantation investments indicate a higher demand for larger engines in rubber, cassava, and industrial rice estates. Forward-looking vendors are positioning mid-range 70-90 horsepower units that can double as haulage tractors, anticipating gradual farm consolidation.

Geography Analysis

Rice powerhouse provinces in the Mekong corridor, Battambang, Kampong Cham, and Prey Veng, generate roughly 60% of Cambodia agricultural machinery market demand, combining broad paddies with better road access that favors large machine transport. Border provinces benefit from their proximity to established machinery markets in Thailand and Vietnam, enabling farmers to access equipment and services across national boundaries. However, regulatory compliance and warranty considerations can complicate cross-border transactions.

Central plains such as Kampong Thom benefit from ongoing irrigation reconstruction projects, including the USD 31 million Damnak Chheukrom mega system that improves field accessibility for tractors and harvesters. Northern frontier provinces Ratanakiri, Mondulkiri, and Kratie present high potential yet face sparse dealer coverage and weaker logistics. A special investment promotion program running from 2025 to 2028 offers tax holidays and infrastructure grants to entice agro-processing and mechanization firms to the region.

Rubber and cassava estates backed by Vietnamese investors are early adopters of mid-range tractors and self-propelled sprayers, anchoring future sales channels. Coastal zones around Kampot and Preah Sihanouk show modest uptake focused on salt and pepper cultivation that requires niche implements, while Phnom Penh serves as the hub for equipment warehousing, parts importation, and high-end service facilities.

Competitive Landscape

Market leadership is held by five global manufacturers. Kubota Corporation, Yanmar Holdings Co., Ltd., Mahindra and Mahindra Ltd., Tractors and Farm Equipment Limited, and Deere & Company shared the majority of share of 2024 revenue. Kubota Corporation’s crawler combine harvesters tailored for paddy fields and Yanmar Holdings Co., Ltd.’s compact diesel engines strengthen their positions.

Local affiliates focus on product localization, modifying tire widths, and adding canopy frames to suit Cambodia’s high humidity and intense UV exposure. Mahindra and Mahindra Ltd. accelerates entry by partnering with Phnom Penh-based distributors that bundle spare parts financing. Custom-hire businesses create indirect competition by pooling branded fleets, allowing growers to experience machines from multiple manufacturers before purchase. Technology is an emerging battlefield where GPS steering, yield monitors, and remote diagnostics differentiate higher-margin units.

Yanmar Holdings Co., Ltd. is piloting battery-powered diesel hybrids, while Kubota Corporation is testing methane-reducing paddy management systems that may be bundled with its tractors. Regulatory compliance capability is now a competitive resource because import approval hinges on meeting the Institute of Standards of Cambodia requirements for emissions and safety. Looking ahead, vendor success hinges on scaling rural service footprints and forging finance partnerships that bring mid-range equipment within reach of consolidating farm enterprises.

Cambodia Agricultural Machinery Industry Leaders

Kubota Corporation

Yanmar Holdings Co., Ltd.

Mahindra and Mahindra Ltd

Tractors and Farm Equipment Limited

Deere & Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Vietnamese conglomerate THACO Group invested USD 1 billion in Cambodia's agriculture sector, aiming to achieve USD 800 million in annual revenue by 2028. The investment focuses on agricultural mechanization, infrastructure development, and agro-processing, encompassing tractors, harvesters, and specialized agricultural machinery for Cambodian crops such as bananas, cassava, and durian.

- September 2024: RMA Cambodia's Agricultural Equipment Division has unveiled two new Deere & Company tractor models the 6195M, boasting 195 hp, and the 8RT370, a powerful 370 hp model with tracked wheels. This launch underscores RMA's ambition to cement its position as a leading agricultural entity in the Kingdom.

Cambodia Agricultural Machinery Market Report Scope

Agricultural machinery encompasses all machines and tools used in the production, harvesting, and care of farm products, as well as trailers used to transport agricultural produce. For this report, the tractor and other machinery used in agricultural operations have been taken into consideration. The tractor used for industrial and construction purposes is excluded from the study. The Cambodia Agricultural Machinery Market is Segmented by Product Type (Tractors, Rice Combine Harvesters, Power Tillers, and Diesel Engine Units). The report provides market size and forecasts in terms of sales in units and value in USD for all the aforementioned segments.

By Product Type

| Tractors | Below 40 HP |

| 40 to 100 HP | |

| Above 100 HP | |

| Rice Combine Harvesters | |

| Power Tillers | Below 10 HP |

| 10 to 15 HP | |

| Diesel Engine Units | Below 10 HP |

| 10 to 15 HP |

| By Product Type | Tractors | Below 40 HP |

| 40 to 100 HP | ||

| Above 100 HP | ||

| Rice Combine Harvesters | ||

| Power Tillers | Below 10 HP | |

| 10 to 15 HP | ||

| Diesel Engine Units | Below 10 HP | |

| 10 to 15 HP | ||

Key Questions Answered in the Report

What is the current value of the Cambodia agricultural machinery market?

It is valued at USD 151.07 million in 2026 with a projected rise to USD 205.81 million by 2031.

Which product category leads sales in Cambodia?

Tractors hold the largest share at 39.45% of 2025 revenue, driven by demand for sub-40 horsepower units.

What restrains faster mechanization uptake?

High repair costs, limited service networks, operator skill shortages, and cultural preference for draught animals slow adoption.

How important are combine harvesters to the rice sector?

Combine harvesters grow at a 9.41% CAGR because they cut 15-20% post-harvest losses and address labor shortages.

Page last updated on: