Market Overview

| Study Period | 2020 - 2031 |

|---|---|

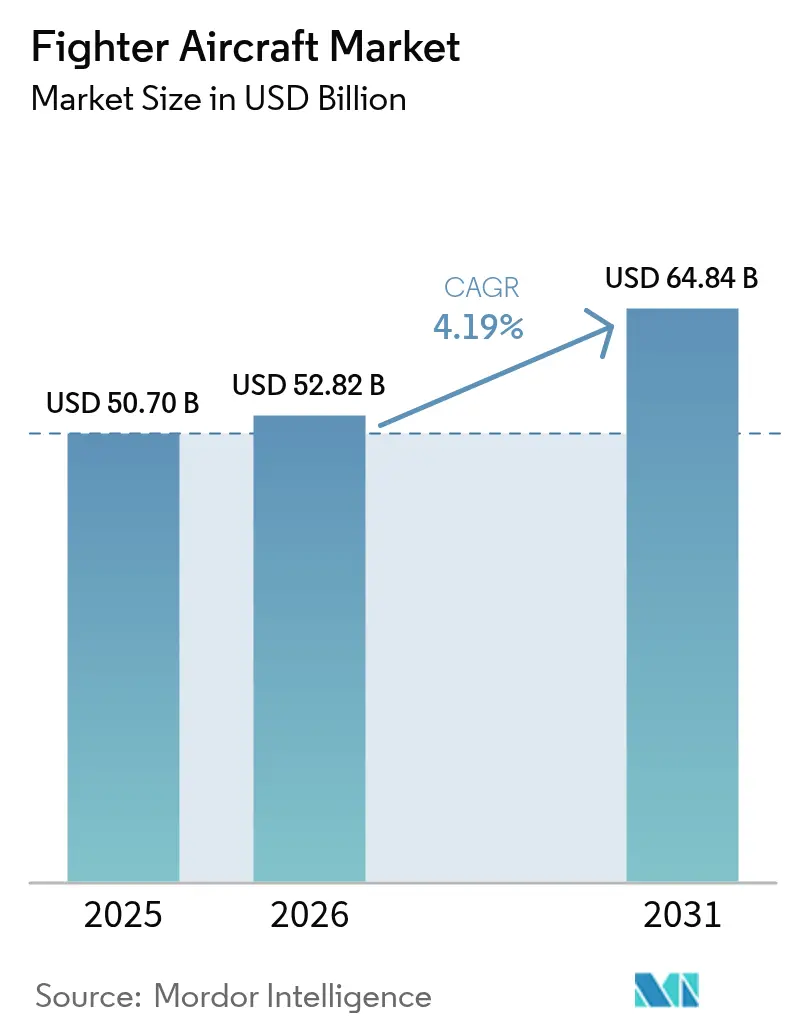

| Market Size (2026) | USD 52.82 Billion |

| Market Size (2031) | USD 64.84 Billion |

| Growth Rate (2026 - 2031) | 4.19% CAGR |

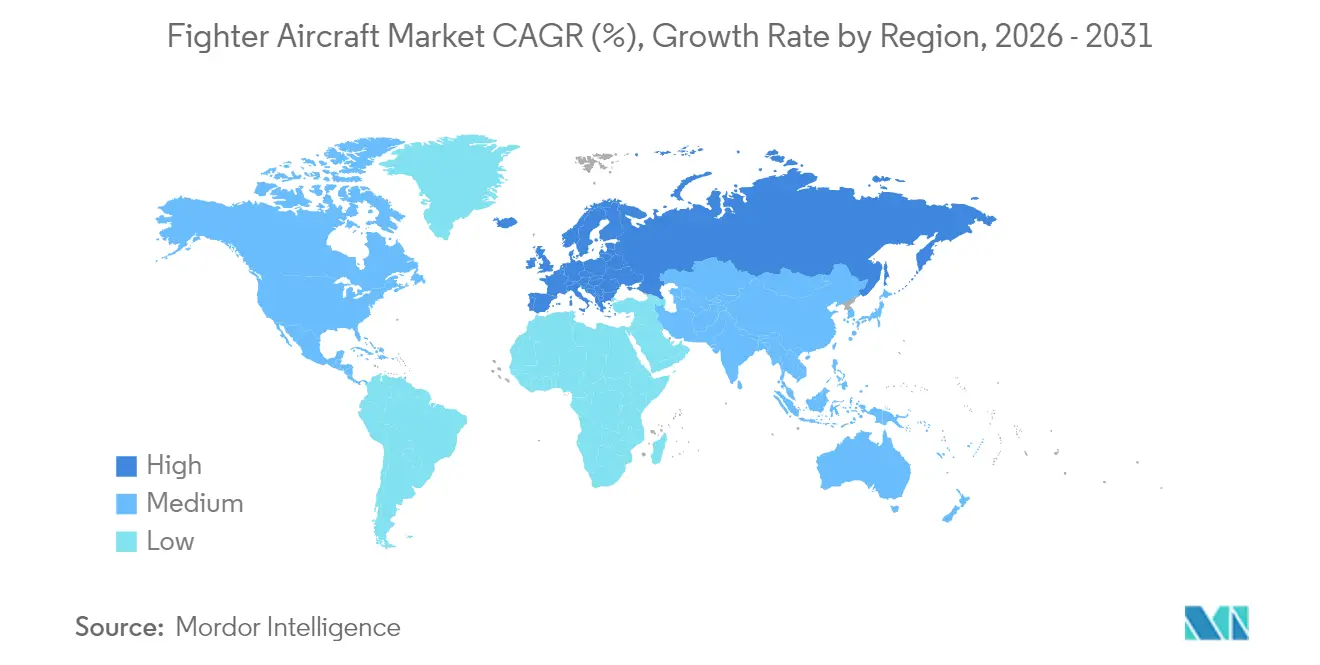

| Fastest Growing Market | Europe |

| Largest Market | North America |

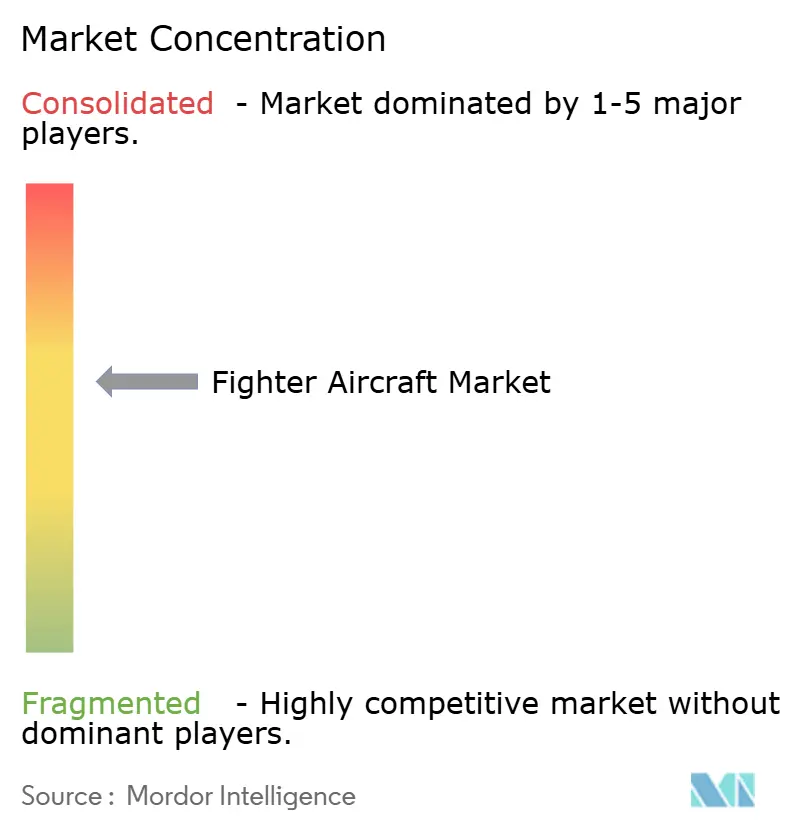

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fighter Aircraft Market Analysis by Mordor Intelligence

The fighter aircraft market size was valued at USD 50.70 billion in 2025 and estimated to grow from USD 52.82 billion in 2026 to reach USD 64.84 billion by 2031, at a CAGR of 4.19% during the forecast period (2026-2031). Surging defense budgets in the Indo-Pacific, accelerated fleet recapitalization across NATO, and the emergence of 6th-generation air-dominance concepts are steering steady expansion, although program delays and rising pilot-training costs temper momentum. Sustained procurement appetite is visible in the shift from 4.5th-generation toward manned-unmanned teaming, the growing influence of naval aviation requirements, and intensified investment in indigenous design programs that promise strategic sovereignty for host nations. Competitive dynamics are transitioning from platform-centric to software-defined offerings, rewarding suppliers that master digital-twin workflows, open architectures, and AI-enabled autonomy. Meanwhile, environmental regulations on engine emissions, looming talent shortages, and ITAR compliance hurdles continue to pose structural challenges for OEMs and operators alike.

Key Report Takeaways

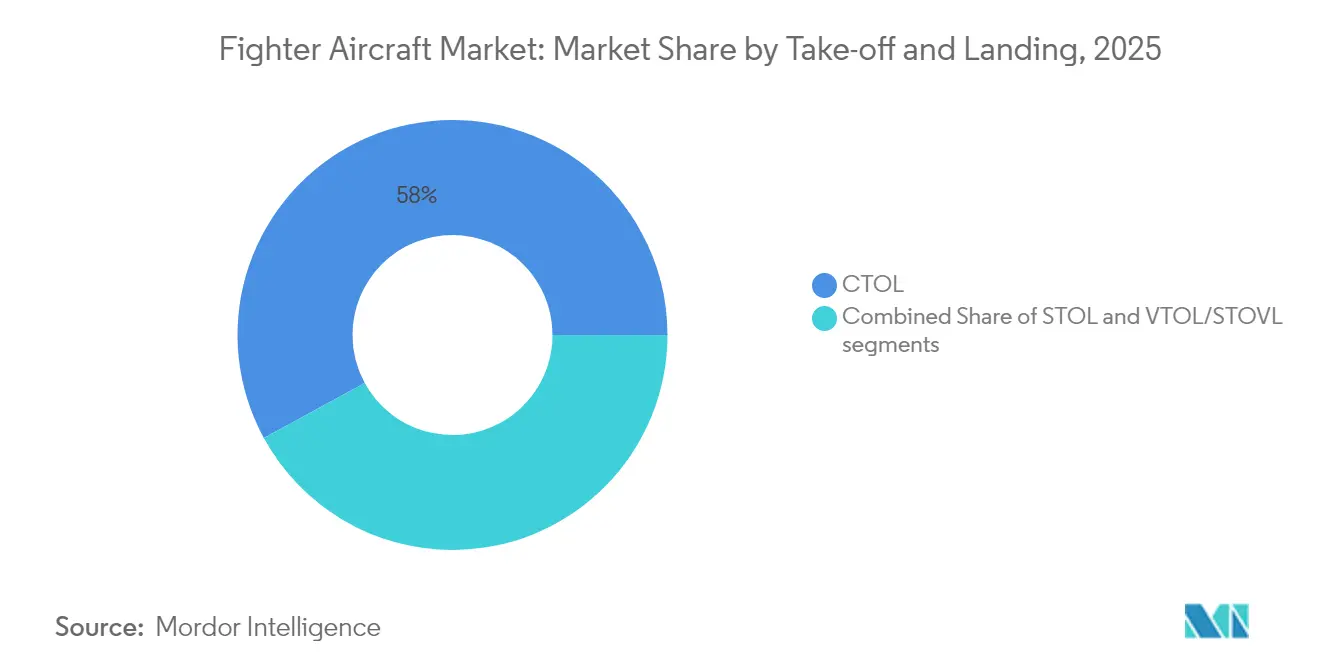

- By take-off and landing, CTOL platforms commanded 57.96% of the fighter aircraft market share in 2025, while VTOL/STOVL platforms are projected to expand at a 6.27% CAGR through 2031.

- By end user, naval aviation is advancing at a 7.72% CAGR to 2031, outpacing the Air Force segment, which held a 52.41% share of the fighter aircraft market in 2025.

- By fighter generation, 4.5th-generation platforms captured 41.37% of the fighter aircraft market share in 2025; 6th-generation systems are forecasted to grow at 8.16% CAGR between 2026 and 2031.

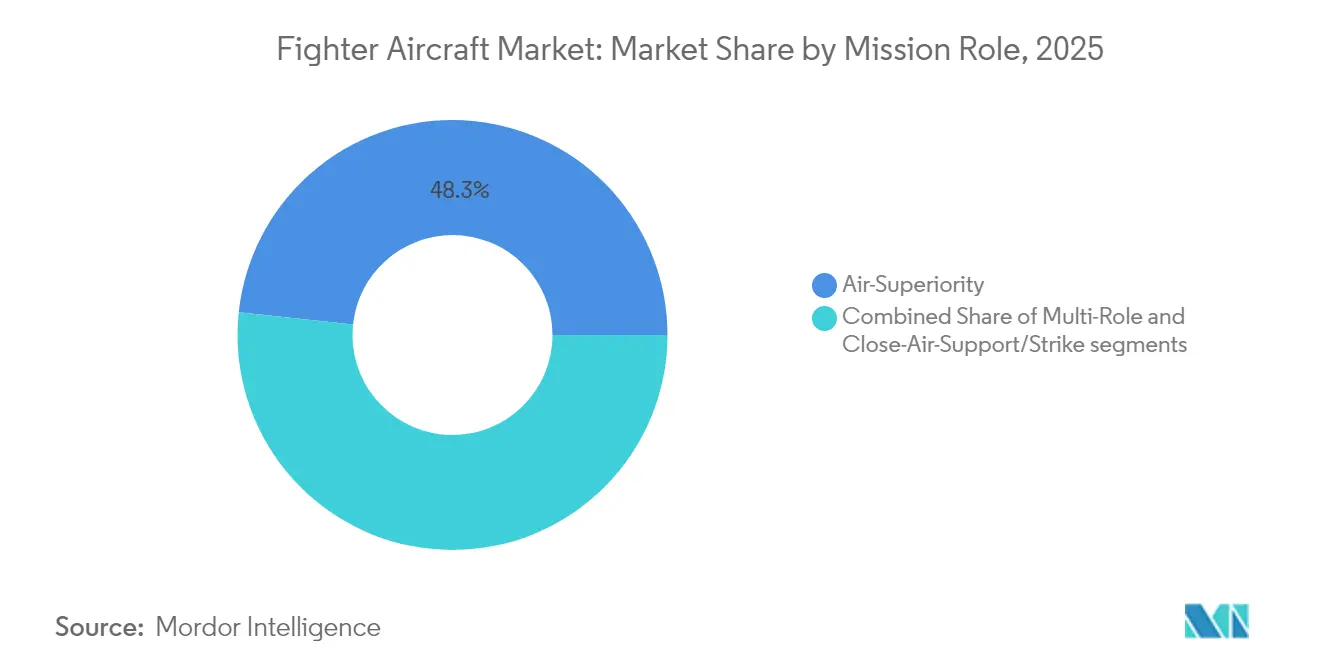

- By mission role, air-superiority platforms accounted for 48.31% of the market in 2025, and the multi-role segment is set to grow by a 6.25% CAGR from 2026 to 2031.

- By engine configuration, single-engine models accounted for 51.88% of the fighter aircraft market size in 2025, whereas twin-engine platforms are set to grow at a 5.18% CAGR over the forecast window.

- By geography, North America retained 36.62% fighter aircraft market share in 2025, while Europe is projected to post the fastest 6.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fighter Aircraft Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing defense budgets in emerging APAC economies | +1.20% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Recapitalization of aging 4th-gen fleets with 5th-gen aircraft | +0.90% | North America, Europe | Long term (≥4 years) |

| Advanced avionics enabling multi-domain operations | +0.70% | Global | Medium term (2-4 years) |

| Indigenous fighter programs for strategic sovereignty | +0.80% | APAC, Europe, Middle East | Long term (≥4 years) |

| Rapid prototyping and digital-twin design workflows | +0.40% | Global | Short term (≤2 years) |

| Export-credit and G-to-G financing packages | +0.30% | Global | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Increasing Defense Budgets in Emerging APAC Economies

East Asian military spending rose to USD 411 billion in 2023, marking 6.2% annual growth that eclipsed the global average.[1]Gregory Allen & Isaac Goldston, “CCA Signals a New Era in AI-Driven Air Combat,” csis.org India allocated USD 75 billion for defense in FY 2024-25, funneling roughly 30% of that toward capital projects such as the AMCA program. South Korea boosted its 2024 budget to USD 44.2 billion, prioritizing KF-21 production and F-35A expansion to deter regional threats. These sustained outlays underpin multi-year procurement pipelines for indigenous fighters and foreign military sales (FMS). Local production offsets, meanwhile, are catalyzing new joint-venture assembly lines and increasing long-term MRO workloads in the fighter aircraft market.

Recapitalization of Aging 4th-Generation Fleets with 5th-Generation Aircraft*

The US Air National Guard secured approval in 2025 to swap 54 F-15C/D jets for 42 F-35As and 21 F-15EXs, underscoring the urgency to retire maintenance-intensive airframes.[2]Department of the Air Force, “Record of Decision—F-15EX and F-35A Operational Beddowns,” federalregister.gov Similar patterns prevail in Europe, where Spain ordered 25 additional Typhoons in 2024 and Finland’s 64-unit F-35A program stays on track for 2030 completion. Escalating sustainment costs for legacy fighters—often aggravated by component cannibalization—are accelerating replacement schedules despite budget pressure. Operators also seek step-change stealth, sensor fusion, and electronic warfare (EW) performance unattainable via incremental upgrades. These tendencies anchor a stable demand baseline for 5th-generation jets through the decade.

Advanced Avionics Enabling Multi-Domain Operations

An F-35 recently commanded autonomous drones in flight through AI-enabled links, illustrating how sensor fusion converts fighters into network nodes rather than isolated shooters.[3]Lockheed Martin, “F-35 Demonstrates Autonomous Control of Drone,” lockheedmartin.com Pilots can offload surveillance, electronic attack, and decoy tasks to unmanned wingmen, freeing bandwidth for strategic decision-making. Air forces now draft requirements around open architectures and rapid software drops rather than solely thrust-to-weight ratios. This pivot fuels lucrative upgrade cycles for mission computers, data links, and cyber-hardened operating systems. Vendors that master secure DevSecOps pipelines quickly gain a competitive advantage in the fighter aircraft market.

Indigenous Fighter Programs for Strategic Sovereignty

India’s USD 15 billion AMCA and Turkey’s KAAN—fresh off a February 2024 first flight—exemplify a global quest for defense autonomy. These projects cultivate domestic supply chains, build aerospace talent pools, and promise export leverage once maturity is reached. Europe is pursuing the tri-national GCAP and the Franco-German-Spanish FCAS with aggregate commitments exceeding USD 100 billion through 2040. Such programs often include generous R&D tax credits and public-private consortia that de-risk early-stage technology work. For global suppliers, aligning with local tier-2 manufacturers is essential to remain present in future tenders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long development lead-times and cost overruns | −0.8% | Global | Long term (≥4 years) |

| High pilot-training and retention costs | −0.6% | Global | Medium term (2-4 years) |

| Environmental/noise-emission regulations at airbases | −0.3% | Europe, North America | Medium term (2-4 years) |

| Geopolitical export and ITAR compliance hurdles | −0.5% | Global | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Long Development Lead-Times and Cost Overruns

Weapons integration averages 38 months per store-aircraft combo, driving cumulative delays that balloon life-cycle cost projections.[4]Defense Acquisition University, “Accelerating Weapons Integration for Fighter and Bomber Aircraft,” dau.edu Europe’s FCAS struggles to reconcile capability ambition with affordability, pushing milestone dates to the right. NGAD faces similar headwinds, with a unit-cost whisper number near USD 300 million sparking calls for program rescope. Prolonged design phases also risk obsolescence as threat envelopes evolve faster than certification queues. Customers, therefore, hedge with mixed fleets of proven 4.5th-generation platforms while monitoring next-gen maturation.

High Pilot-Training and Retention Costs

The US Air Force’s 1,142-fighter-pilot deficit in 2024 forced pipeline changes that diverted trainees to mobility aircraft, slowing fighter-unit manning. Bonuses and improved quality-of-life initiatives have yielded marginal gains but have not closed the gap. European and Asia-Pacific air arms face similar churn as commercial airlines rebound and entice aviators with higher pay. Unmanned wingman programs promise workload relief but introduce new training syllabi and simulator requirements. Ultimately, elevated personnel costs eat into procurement budgets, tempering fleet-expansion aspirations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Take-off and Landing: Carrier Operations Drive VTOL Innovation

Conventional CTOL aircraft generated 57.96% of the 2025 fighter aircraft market size, reflecting broad runway infrastructure and proven logistics chains. VTOL fighters, led by the F-35B, are rising at a 6.27% CAGR as European navies and the Indo-Pacific seek deck-launched capabilities for dispersed operations.

VTOL demand is further boosted by Agile Combat Employment doctrines that require flexibility under runway-denied conditions. STOL platforms remain niche but could see uplift as dispersed basing gains traction. These trends reshape OEM R&D budgets toward compact propulsion and thrust-vectoring modules to secure future fighter aircraft market share in carrier and expeditionary roles.

By Fighter Generation: 6th-Generation Emergence Accelerates

4.5th-generation designs controlled 41.37% of the fighter aircraft market share in 2025 amid ongoing upgrades to Typhoon, Rafale, and Super Hornet. Yet 6th-generation programs post an 8.16% CAGR, fueled by NGAD and GCAP roadmaps that feature adaptive engines, collaborative combat aircraft, and AI-enabled sensor fusion.

Producers of legacy 4th-generation fleets face dwindling order books as sustainment costs climb, pushing them toward service-life extensions and export financing solutions. In contrast, 5th-generation backlogs remain robust but are constrained by production chokepoints, keeping delivery slots full through 2030 even as 6th-generation demonstrators mature.

By Engine Configuration: Twin-Engine Growth Reflects Mission Complexity

Single-engine fighters—primarily the F-35A and F-16—held 51.88% of the fighter aircraft market in 2025, favored by lower life-cycle costs and simpler maintenance footprints. Twin-engine platforms will grow 5.18% CAGR as extended-range strike missions, high electrical loads, and survivability imperatives gain prominence.

Air forces valuing deep-strike capacity or heavy electronic-warfare payloads increasingly gravitate toward twin-engine options such as the F-15EX, Rafale, and Typhoon. The consensus among emerging 6th-generation designs is that a twin-engine baseline ensures ample power and thermal margins for directed-energy weapons and broadband sensors.

By Mission Role: Multi-Role Platforms Dominate Procurement

Air-superiority variants held 48.31% of the fighter aircraft market share in 2025; however, multi-role aircraft are expanding at a 6.25% CAGR as budget-constrained operators demand swing-role flexibility.

Sensor fusion and precision-guided munitions equip multi-role fighters to suppress air defenses, execute close-air support, and gather ISR in one sortie. Dedicated CAS or strike airframes continue to fade as generational upgrades integrate advanced weapons and data links, boosting demand elasticity for multi-role offerings within the fighter aircraft market.

By End User: Naval Aviation Drives Market Expansion

Air Force operators retained a 52.41% share in 2025 but face the slowest growth. Naval aviation traffic—buoyed by Indo-Pacific carrier investments—will outpace all other segments at 7.72% CAGR through 2031.

India’s USD 7.5 billion Rafale Marine acquisition and France’s continued Rafale-M buys reinforce blue-water strike ambitions. Marine and Army aviation upgrades center on vertical-lift concepts, but naval air wings stand out as prime adopters of collaborative combat aircraft, enlarging addressable opportunities for mission-system suppliers.

Geography Analysis

North America generated 36.62% of the global fighter aircraft market revenue in 2025, anchored by F-35A, F-15EX, and forthcoming CCA orders. The region’s share is stable, yet growth moderates as production ramps plateau and governmental focus tilts toward sustainability efficiencies.

Europe’s fighter aircraft market size is forecasted to rise at a 6.43% CAGR. Russia’s invasion of Ukraine catalyzed defense-spending uplifts exceeding NATO’s 2% GDP pledge across multiple member states. FCAS and GCAP consortia inject substantial R&D outlays, while short-run deliveries of Typhoon Tranche 4 and Rafale F4 support immediate readiness.

Asia-Pacific exhibits bifurcated trajectories: US allies continue F-35 adoption, whereas China advances J-20 and J-31 production. India and South Korea pursue indigenous programs that stretch beyond 2030 but redirect local value addition upwards of 60%. Middle East operators prioritize turnkey capability, sustaining repeat F-15SA, F-35I, and Rafale contracts despite fiscal volatility linked to oil prices.

Competitive Landscape

The fighter aircraft industry remains moderately consolidated. Five incumbents—Lockheed Martin Corporation, The Boeing Company, Airbus SE, Dassault Aviation SA, and BAE Systems plc—accounted for a major share of new-build deliveries in 2024. Second-tier challengers like Saab, KAI, HAL, and Turkish Aerospace capture niche orders tied to sovereign-capability agendas.

Competitive focus is shifting from airframe performance to software and mission-systems agility. In 2025, the US Air Force selected General Atomics and Anduril as CCA finalists, signaling openness to non-traditional primes that excel in autonomy and rapid prototyping. Partnerships across cybersecurity, AI, and edge-cloud computing proliferate as OEMs seek digital supremacy.

Sustainability also shapes differentiation. In 2025, Lockheed Martin approved 50% synthetic-fuel blends for the F-35 fleet, and Airbus is exploring SAF compatibility for FCAS demonstrators. Suppliers able to certify low-carbon operations gain ESG credibility, which increasingly influences procurement scoring in Europe.

Fighter Aircraft Industry Leaders

Lockheed Martin Corporation

The Boeing Company

Airbus SE

Dassault Aviation SA

BAE Systems plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: The US Air Force revealed that the first F-47 6th-generation aircraft will fly in 2028.

- June 2025: Australia’s MQ-28 Ghost Bat demonstrated two-aircraft control by a single E-7A operator.

- April 2025: India finalized USD 7.5 billion deal for 26 Rafale Marine fighters.

Global Fighter Aircraft Market Report Scope

A fighter aircraft can be termed a high-speed fixed-wing military aircraft that can carry out air-to-air combat missions. High speed, ease of maneuvering, and relatively smaller size are the hallmarks of fighter aircraft. These aircraft can also carry heavy payloads and perform electronic warfare, ground attacks, and air-to-air combat.

The fighter aircraft market is segmented by take-off and landing, type, and geography. By take-off and landing, the market has been segmented into conventional take-off and landing, short take-off and landing, and vertical take-off and landing. By type, the market has been segmented into light attack, electronic warfare, multi-role fighter, trainers, and others. By geography, the market has been segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Take-off and Landing

| Conventional Take-off and Landing (CTOL) |

| Short Take-off and Landing (STOL) |

| Vertical Take-off and Landing (VTOL/STOVL) |

By Fighter Generation

| 4th Generation |

| 4.5th Generation |

| 5th Generation |

| 6th Generation/NGAD |

By Engine Configuration

| Single-Engine |

| Twin-Engine |

By Mission Role

| Air-Superiority |

| Multi-Role |

| Close-Air-Support/Strike |

By End User

| Air Force |

| Naval Aviation |

| Marine/Army Aviation |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Take-off and Landing | Conventional Take-off and Landing (CTOL) | ||

| Short Take-off and Landing (STOL) | |||

| Vertical Take-off and Landing (VTOL/STOVL) | |||

| By Fighter Generation | 4th Generation | ||

| 4.5th Generation | |||

| 5th Generation | |||

| 6th Generation/NGAD | |||

| By Engine Configuration | Single-Engine | ||

| Twin-Engine | |||

| By Mission Role | Air-Superiority | ||

| Multi-Role | |||

| Close-Air-Support/Strike | |||

| By End User | Air Force | ||

| Naval Aviation | |||

| Marine/Army Aviation | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the fighter aircraft market in 2026?

The fighter aircraft market size was USD 52.82 billion in 2026 and is projected to reach USD 64.84 billion by 2031.

Which segment is growing fastest through 2031?

Naval aviation demand leads with a 7.72% CAGR, driven by Indo-Pacific carrier acquisitions and blue-water strategies.

What share do 4.5th-generation platforms hold today?

5th-generation fighters accounted for 41.37% of fighter aircraft market share in 2025.

Which companies dominate current deliveries?

Lockheed Martin Corporation, The Boeing Company, Airbus SE, Dassault Aviation SA, and BAE Systems plc collectively shipped more than 65% of new fighters in 2024.

How are pilot shortages affecting procurement?

Persistent pilot deficits are accelerating investment in autonomous loyal-wingman systems to sustain sortie rates without proportional increases in trained pilots.

What environmental measures impact future fighters?

New particulate-matter limits and synthetic-fuel requirements in the US and Europe compel OEMs to certify engines for lower emissions and higher SAF blends.

Page last updated on: