Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

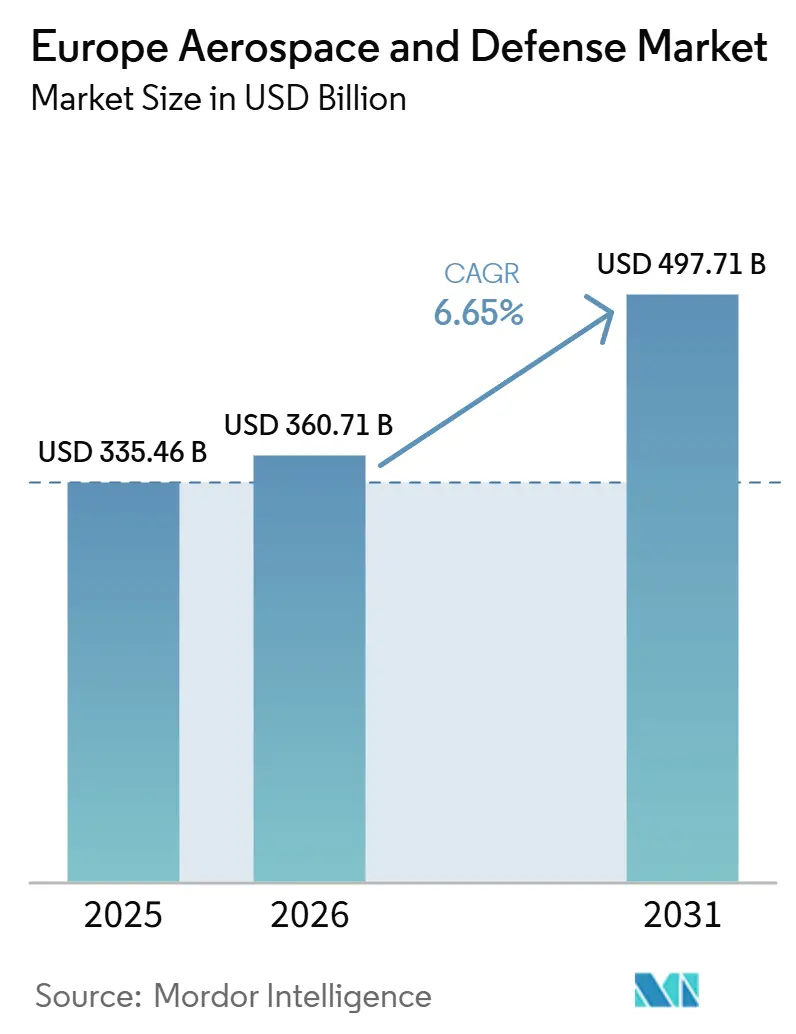

| Base Year Market Size (2025) | USD 335.46 Billion |

| Market Size (2026) | USD 360.71 Billion |

| Market Size (2031) | USD 497.71 Billion |

| Growth Rate (2026 - 2031) | 6.65% CAGR |

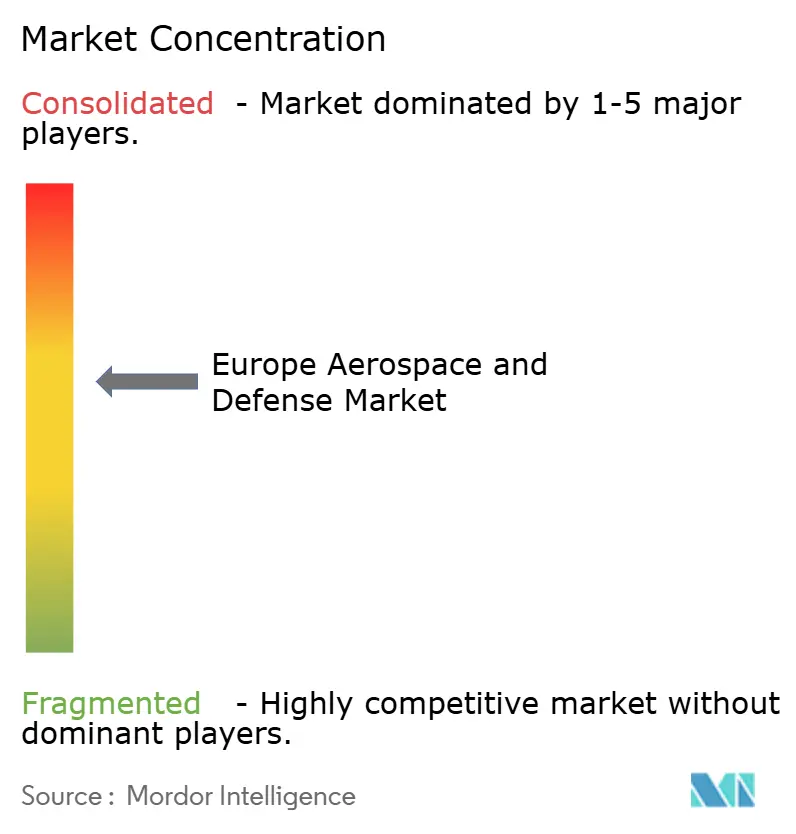

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Aerospace and Defense Market Analysis by Mordor Intelligence

The Europe aerospace and defense market size is expected to grow from USD 335.46 billion in 2025 to USD 360.71 billion in 2026 and is forecasted to reach USD 497.71 billion by 2031 at a 4.90% CAGR over 2026-2031. Multiple forces are converging to lift demand. Renewed security threats after Russia’s full-scale invasion of Ukraine pushed nearly every North Atlantic Treaty Organization (NATO) government to meet or exceed the 2% of GDP defense spending floor, unlocking significant procurement backlogs. Concurrently, the ReFuelEU Aviation mandate requires all EU airports to blend sustainable aviation fuel (SAF), thereby accelerating research and development expenditures on hydrogen propulsion, open-rotor engines, and power-to-liquid facilities. Intensifying competition, often from software-native entrants, is rewriting long-standing go-to-market models and sharpening the need for resilient titanium and rare-earth supply chains as sanctions, trade frictions, and labor shortages destabilize production schedules. Supply sovereignty initiatives and digital engineering adoption are therefore rising in tandem, redefining the structure and cadence of investment across the Europe aerospace and defense market.

Key Report Takeaways

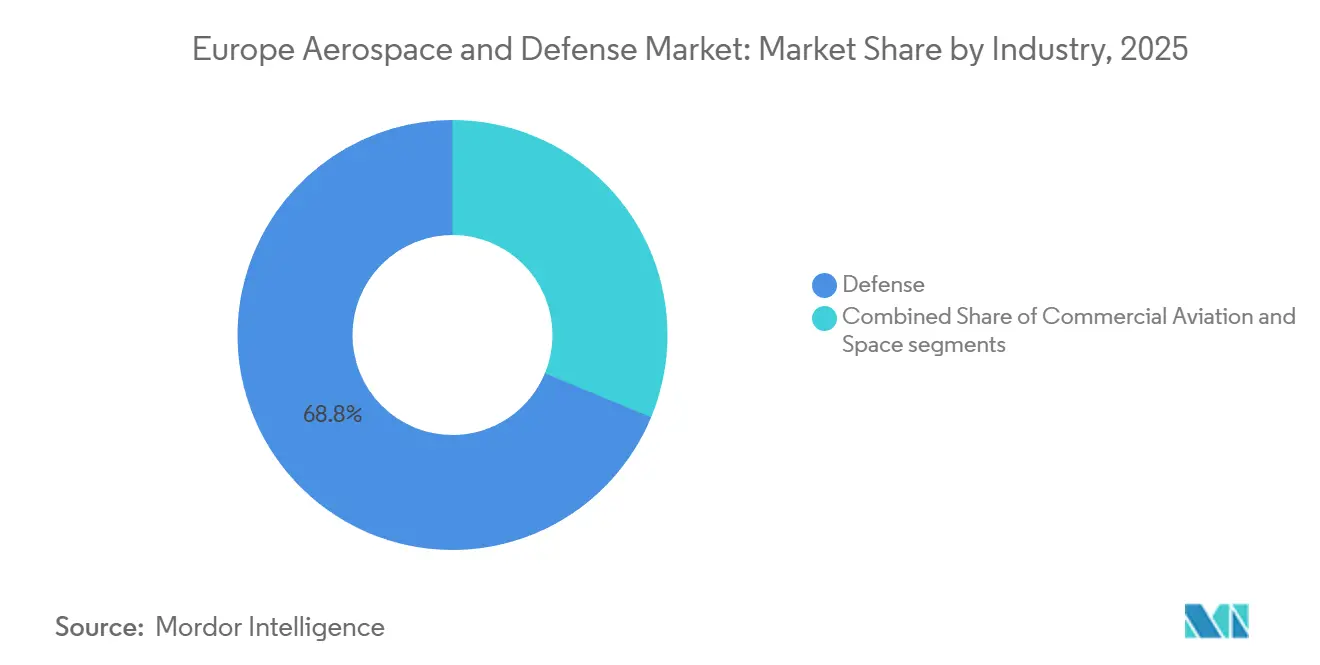

- By industry vertical, defense accounted for 68.75% of 2025 revenue, while the space segment is forecast to grow at an 8.19% CAGR through 2031.

- By type, platform sales led with a 62.37% revenue share in 2025; systems are forecast to grow at a 7.22% CAGR through 2031.

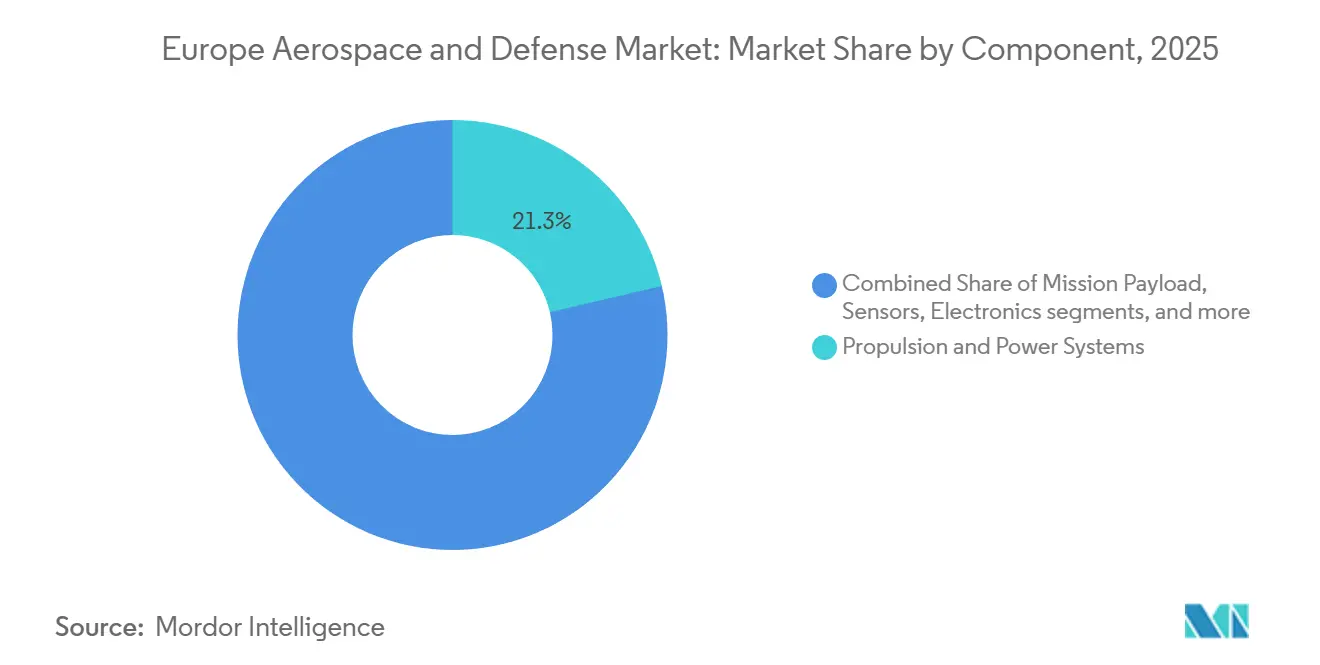

- By component, propulsion and power systems accounted for 21.34% of the Europe aerospace and defense market share in 2025, whereas software and digital systems are forecast to grow at a 7.51% CAGR through 2031.

- By point of sale, OEM accounted for 74.45% of 2025 turnover; retrofit/upgrade pathways are projected to grow at a 7.41% CAGR through 2031.

- By geography, Russia retained 16.87% revenue share in 2025; Spain is forecast to grow at a 7.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Aerospace and Defense Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased EU defense fund and strategic compass budget allocations | +1.2% | France, Germany, Italy, Spain | Medium term (2–4 years) |

| Climate-neutral aviation and SAF mandates driving aerospace R&D investments | +0.9% | EU-27, United Kingdom, Norway, Switzerland | Long term (≥ 4 years) |

| Ukraine conflict accelerating demand for munitions and land-based defense systems | +1.5% | Poland, Baltics, Germany, France, United Kingdom | Short term (≤ 2 years) |

| Expansion of Europe’s commercial small-launch and mini-launcher ecosystem | +0.7% | France, Germany, Spain, Norway | Medium term (2–4 years) |

| Adoption of digital engineering and MBSE to reduce program life-cycle costs | +0.8% | United Kingdom, France, Germany, Italy | Medium term (2–4 years) |

| Urban air mobility corridor pilot programs advancing next-generation air transport | +0.5% | France, Germany, United Kingdom, Italy | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased EU Defense Fund and Strategic Compass Budget Allocations

The European Defence Fund (EDF) disbursed EUR 1.5 billion (USD 1.75 billion) in 2025, representing a 15% year-on-year increase, which financed 61 cross-border projects covering next-generation tanks, hypersonic interceptors, and secure satellite communications. The Strategic Compass initiative, approved in 2022, calls for a 5,000-troop Rapid Deployment Capacity by 2025, requiring interoperable Command and Control (C2) networks that legacy national architectures cannot deliver. Multinational teaming has therefore accelerated; KNDS, a Franco-German joint venture, secured funds to prototype the Main Ground Combat System, satisfying funding rules that privilege collaborative bids. Dual-use prioritization is also driving the development of AI-enabled target recognition and autonomous logistics, thereby narrowing Europe’s historical gap with US primes. The Europe aerospace and defense market benefits directly as advanced capability programs transition from concept to funded development, securing multi-year pipeline visibility.

Climate-Neutral Aviation and SAF Mandates Driving Aerospace R&D Investments

ReFuelEU Aviation requires a 6% SAF blend by 2030, escalating to 70% by 2050, and imposes financial penalties on suppliers that fail to comply with this requirement. Airbus has earmarked research on hydrogen propulsion through 2035 and is retrofitting its Toulouse final-assembly lines to handle cryogenic tanks.[1]Airbus, “Zero-Emission Hydrogen,” airbus.com Safran is validating its open-rotor RISE engine, which promises 20% lower fuel burn and full SAF compatibility, with ground tests expected to be completed in 2025. A joint Shell-TotalEnergies power-to-liquid plant slated for Rotterdam will produce 200,000 tons of e-kerosene annually by 2028, ensuring feedstock availability. These mandates shift R&D risk profiles, pulling alternative-propellant programs into the mainstream and creating long-run upside for the Europe aerospace and defense market as civil and military fleets converge on low-carbon technologies.

Ukraine Conflict Accelerating Demand for Munitions and Land-Based Defense Systems

Daily artillery expenditure in Ukraine peaked at 10,000 shells during 2024, rapidly depleting NATO stockpiles. The Act in Support of Ammunition Production allocated EUR 500 million (USD 584.44 million) in 2024 to expand European shell production lines. Rheinmetall responded by opening a new Unterlüß plant, which increases the 155 mm capacity from 70,000 to 200,000 rounds annually. Orders for counter-drone jammers and passive radars tripled, underscoring a pivot toward layered air-defense architectures. The Europe aerospace and defense market, therefore, captures both elevated platform demand and rapid-fire replenishment contracts that shorten revenue recognition cycles.

Expansion of Europe’s Commercial Small-Launch Ecosystem

Ariane 6 is expected to restore European heavy-lift autonomy in 2024, but venture-backed micro-launchers are pushing the cost curve lower. Isar Aerospace raised USD 165 million in 2023 to finish its Spectrum pad at Norway’s Andøya Spaceport, targeting 12 flights per year by 2028. Spain’s PLD Space plans an orbital Miura 5 debut in 2026 after a successful Miura 1 sub-orbital flight. As the launch cadence increases, per-kilogram costs for sun-synchronous rideshares have decreased by 37% since 2023, stimulating new earth observation and communications constellations that expand the addressable Europe aerospace and defense market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply chain vulnerabilities in titanium and rare earth materials | -0.8% | Germany, France, Italy, United Kingdom | Short term (≤ 2 years) |

| Persistent skills shortages in avionics and propulsion engineering | -0.6% | Germany, France, Netherlands, Sweden | Medium term (2–4 years) |

| Stringent noise and emissions regulations extending civil certification timelines | -0.7% | All EASA member states | Medium term (2–4 years) |

| Fragmented export-control frameworks constraining multinational programs | -0.5% | France, Germany, Italy, Spain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Vulnerabilities in Titanium and Rare-Earth Materials

Russia supplied 30% of European aerospace-grade titanium before sanctions took hold, and stockpiles are forecast to run dry by mid-2026. Substitution contracts with Japanese mills closed some gaps, but prices climbed 40% between 2024 and 2025, eroding margins on fixed-price airframe deals. Parallel exposure exists in rare-earth magnets, where China controls 85% of global refining capacity and tightened export quotas in 2025. A Thales-Safran recycling venture aims to recover 15% of annual neodymium demand by 2028, yet no domestic extraction projects have broken ground.[2]Thales Group, “Rare-Earth Recycling Initiative,” thalesgroup.com The Europe aerospace and defense market, therefore, carries raw material cost volatility that could dilute program profitability and stretch delivery schedules.

Persistent Skills Shortages in Avionics and Propulsion Engineering

The region faces a shortfall of roughly 20,000 specialized engineers, a gap that pandemic-related hiring freezes and accelerated retirements have widened. MTU Aero Engines disclosed a six-month delay in geared-turbofan certification due to staffing gaps. Retraining initiatives such as Saab’s internal academy and Rolls-Royce’s postgraduate partnership mitigate the risk, but demographic trends suggest the deficit will persist through 2031. Software-centric avionics compounds the problem because legacy curricula emphasize hardware design. Talent scarcity, therefore, constrains throughput in the Europe aerospace and defense market and may force primes to offshore specific digital-engineering tasks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Industry: Defense Dominates While Space Surges

Defense accounted for 68.75% of 2025 revenue as governments replenished inventories and elevated readiness. Space captures a smaller baseline but is advancing at an 8.19% CAGR on the strength of IRIS² and commercial Earth-observation constellations. The dual-use nature of surveillance satellites attracts both civil and military budgets, further enlarging the Europe aerospace and defense market. Commercial aviation is recovering from pandemic-era troughs; Airbus delivered 793 jets in 2025, yet a backlog of over 8,600 aircraft highlights ongoing supply chain bottlenecks.[3]Airbus, “2025 Deliveries,” airbus.com

Space momentum is reinforced by the proliferation of mini-launchers and growing demand for low-Earth-orbit broadband, adding durable upside for sensor payloads, ground-segment software, and frequency-allocation services. Defense growth, though strong, may moderate after initial restocking peaks unless export pipelines offset plateauing domestic spend post-2031. Commercial aviation will hinge on the availability and certification timelines of SAF, which could either compress or stretch the trajectory of the Europe aerospace and defense market size.

By Type: Platform Revenue Leads, Systems Capture Faster Growth

Platforms delivered 62.37% of turnover in 2025, driven by fighter aircraft, upgraded frigates, and satellite buses. Systems, however, are projected to expand at a 7.22% CAGR as militaries retrofit digital backbones onto legacy fleets. MBDA’s missile order from Poland, Germany, and Italy typifies the shift toward networked effectors. Platform demand remains healthy for unmanned aerial vehicles; Airbus’s Zephyr achieved a 64-day stratospheric flight, showcasing long-endurance surveillance at a fractional cost.

Growth in systems reflects the adoption of open architecture, allowing for incremental capability insertions without requiring wholesale fleet replacement. Over the forecast horizon, budget holders favor software-defined radios, AESA radars, and cyber-warfare modules that integrate swiftly and elevate operational readiness, further tilting the share toward systems within the Europe aerospace and defense market.

By Component: Propulsion Leads, Software and Digital Systems Scale Quickly

Propulsion and power systems accounted for 21.34% of the revenue share in 2025, making them the largest component category. The Europe aerospace and defense market share for propulsion is underwritten by fleet re-engining cycles and emerging hydrogen demonstrators, such as Rolls-Royce’s UltraFan, which achieved a 10% efficiency gain on 100% SAF. Software and digital systems, though smaller at present, are forecasted to rise at a 7.51% CAGR. MBSE platforms and open-standards avionics cut integration timelines and unlock rapid spiral upgrades, driving sustained double-digit growth in digital-twin services.

Sensors and electronics also register solid demand as counter-drone and electronic-warfare needs spike. In 2025, HENSOLDT’s Twinvis passive radar secured contracts to detect low-observable aircraft without revealing emitter location. Yet titanium inflation squeezes margins in structures and materials, pressing primes to automate composite lay-up and source alternative alloys.

By Point of Sale: OEM Channel Dominance Persists as Retrofit Growth Accelerates

OEM sales accounted for 74.45% of 2025 revenue, as new-build platforms incur high bill-of-materials costs and require multi-year payment milestones. Retrofit and upgrade demand is nevertheless climbing at 7.41% CAGR, aided by open-architecture avionics that de-risk mid-life insertions. Germany’s Typhoon radar upgrade illustrates the cost-effectiveness of capability renewal over all-new orders. Obsolescence management also propels the retrofit cycle as 1990s-era line-replaceable units reach the end of life.

Over time, digital-twin analytics will enable predictive maintenance that prolongs airframe lives, shifting more value into services contracts. Thus, while OEM deliveries remain the revenue cornerstone, the retrofit channel will steadily widen its contribution to the overall Europe aerospace and defense market.

Geography Analysis

Russia retained a 16.87% revenue share in 2025, buoyed by domestic procurement of Su-57 fighters and S-400 air defense units, despite export and civil aerospace sanctions. Civil programs collapsed as Superjet and MC-21 production stalled due to the lack of Western engines and avionics, and Roscosmos recorded its lowest launch tally since 1961. The defense-only skew highlights the geopolitical bifurcation shaping the Europe aerospace and defense market.

Spain is the fastest-growing geography at a 7.75% CAGR. Participation in the Future Combat Air System (FCAS) program and an F-110 frigate order have increased the country’s defense budget by 18% for 2025. Navantia’s frigate program and Indra’s data-fusion workshare strengthen Spain’s industrial base and spill over into advanced composites and embedded-software clusters, amplifying national share inside the Europe aerospace and defense market.

Germany crossed the 2% GDP defense spending line in 2025 and is implementing a modernization fund, resulting in orders for Puma IFVs, IRIS-T missiles, and HENSOLDT radars.[4]German Federal Ministry of Defence, “Budget Information,” bmvg.de France maintains consistent outlays anchored by the Scorpion vehicle suite and Rafale exports, while the UK advances Tempest and Dreadnought programs on a GBP 57 billion (USD 76.74 billion) budget. The rest of Europe markets, led by Poland’s USD 20 billion armored-vehicle spree, deliver 6.80% CAGR growth through 2031. Collectively, these dynamics ensure geographic diversification across the Europe aerospace and defense market, mitigating over-reliance on any single country.

Competitive Landscape

The Europe aerospace and defense market is moderately concentrated. Airbus, BAE Systems plc, Leonardo S.p.A., Thales Group, and Safran SA collectively hold a significant market share. Incumbents are pursuing vertical integration of software to protect their margins. Airbus purchased Polish avionics specialist Infotron in 2025 to internalize DO-178C talent. BAE Systems has converted its Typhoon sustainment contract to a performance-based logistics model that rewards aircraft availability, aligning incentives with those of the Royal Air Force.

Venture-funded disruptors are simultaneously unbundling value chains. Volocopter’s Series E round advances a distributed electric-propulsion eVTOL that bypasses turbine-engine certification and reduces development cycles to four years. Isar Aerospace offers launch services at half the cost of Ariane 6 per kilogram, pressuring incumbent economics. Competition is also intensifying in counter-small-UAS solutions, sovereign satellite constellations, and hydrogen infrastructure, each representing new battlefields for share capture within the Europe aerospace and defense market.

Supply chain resiliency and talent acquisition have become differentiators. Safran’s rare-earth recycling initiative and Rolls-Royce’s graduate pipeline tackle structural constraints that could impair delivery schedules. With no single firm able to dominate the sprawling civil, military, and space domains, strategic partnerships and open standards ecosystems will define competitive advantage across the Europe aerospace and defense market through 2031.

Europe Aerospace and Defense Industry Leaders

BAE Systems plc

Leonardo S.p.A.

Thales Group

Safran SA

Airbus SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: The UK MoD awarded Thales an initial contract worth GBP 10 million (approximately USD 13.47 million) to provide AI-enabled remote command centers for the Royal Navy's mine countermeasures (MCM) operations.

- August 2025: Elbit Systems, Ltd. signed a USD 1.6 billion, five-year contract to provide a European customer with advanced defense systems. The agreement includes long-range precision artillery, rocket systems, and unmanned aerial platforms equipped with embedded AI technologies.

- February 2024: France's Defense Procurement Agency announced the procurement of self-propelled howitzers, armored vehicles, and helicopters, valued at more than USD 1.2 billion, as part of the nation's military modernization initiative, which will continue until 2030.

Europe Aerospace and Defense Market Report Scope

The Europe aerospace and defense market encompasses the design, manufacture, and operation of commercial aircraft, military land vehicles, military aircraft, naval vessels, rockets, missiles, and spacecraft in space. Defense equipment refers to weapons, arms, and equipment used for military purposes. The study conducted in this report provides an in-depth analysis of the European aerospace and defense market.

The Europe aerospace and defense market is segmented by industry, type, component, point of sale, and geography. By industry, the market is segmented into commercial aviation, defense, and space. By type, the market is segmented into platform, systems, and MRO. By component, the market is segmented into structures and materials; propulsion and power systems; mission payload; sensors; electronics; communications; cyber warfare; software and digital systems; and services and sustainment. By point of sale, the market is segmented into original equipment manufacturer (OEM) and retrofit/upgrade. The report also offers the market sizes and forecasts for six countries across the region. For each segment, the report offers market sizing and forecasts in terms of value (USD).

By Industry

| Commercial Aviation |

| Defense |

| Space |

By Type

| Platform | Commercial Aviation |

| General Aviation | |

| Military Land Vehicles | |

| Military Aircraft | |

| Military Naval Vessels | |

| Unmanned Systems | |

| Satellites | |

| Systems | Weapons and Munitions |

| Sensors | |

| C4ISR and Tactical Communications | |

| Electronic and Cyber Warfare Systems | |

| Air and Missile Defense | |

| Soldier Systems | |

| Military Infrastructure | |

| Training and Simulation | |

| MRO | Military MRO |

| Commercial aviation MRO | |

| General Aviation MRO |

By Component

| Structures and Materials |

| Propulsion and Power Systems |

| Mission Payload |

| Sensors |

| Electronics |

| Communications |

| Cyber Warfare |

| Software and Digital Systems |

| Services and Sustainment |

By Point of Sale

| Original Equipment Manufacturer (OEM) |

| Retrofit/Upgrade |

By Geography

| United Kingdom |

| France |

| Germany |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By Industry | Commercial Aviation | |

| Defense | ||

| Space | ||

| By Type | Platform | Commercial Aviation |

| General Aviation | ||

| Military Land Vehicles | ||

| Military Aircraft | ||

| Military Naval Vessels | ||

| Unmanned Systems | ||

| Satellites | ||

| Systems | Weapons and Munitions | |

| Sensors | ||

| C4ISR and Tactical Communications | ||

| Electronic and Cyber Warfare Systems | ||

| Air and Missile Defense | ||

| Soldier Systems | ||

| Military Infrastructure | ||

| Training and Simulation | ||

| MRO | Military MRO | |

| Commercial aviation MRO | ||

| General Aviation MRO | ||

| By Component | Structures and Materials | |

| Propulsion and Power Systems | ||

| Mission Payload | ||

| Sensors | ||

| Electronics | ||

| Communications | ||

| Cyber Warfare | ||

| Software and Digital Systems | ||

| Services and Sustainment | ||

| By Point of Sale | Original Equipment Manufacturer (OEM) | |

| Retrofit/Upgrade | ||

| By Geography | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the projected value of the Europe aerospace and defense market in 2031?

The Europe aerospace and defense market is forecasted to reach USD 497.71 billion by 2031 on a 6.65% CAGR.

Which segment is growing fastest within the market?

The space segment rises at 8.19% CAGR, outpacing all other industry verticals.

Why is Spain the quickest-expanding geography?

Spain’s participation in the Future Combat Air System (FCAS) and new F-110 frigate orders push a 7.75% CAGR, the region’s highest.

How do SAF mandates influence aerospace investment?

ReFuelEU Aviation’s SAF quotas are directing multi-billion-euro R&D into hydrogen propulsion and open-rotor engines, shifting program priorities.

What supply chain risks threaten delivery schedules?

Titanium dependence on sanctioned Russia and rare-earth reliance on China introduce price spikes and potential shortages through 2028.

Page last updated on: