AI-Enabled NDT Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 2.37 Billion |

| Market Size (2030) | USD 6.73 Billion |

| Growth Rate (2025 - 2030) | 23.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-Enabled NDT Market Analysis by Mordor Intelligence

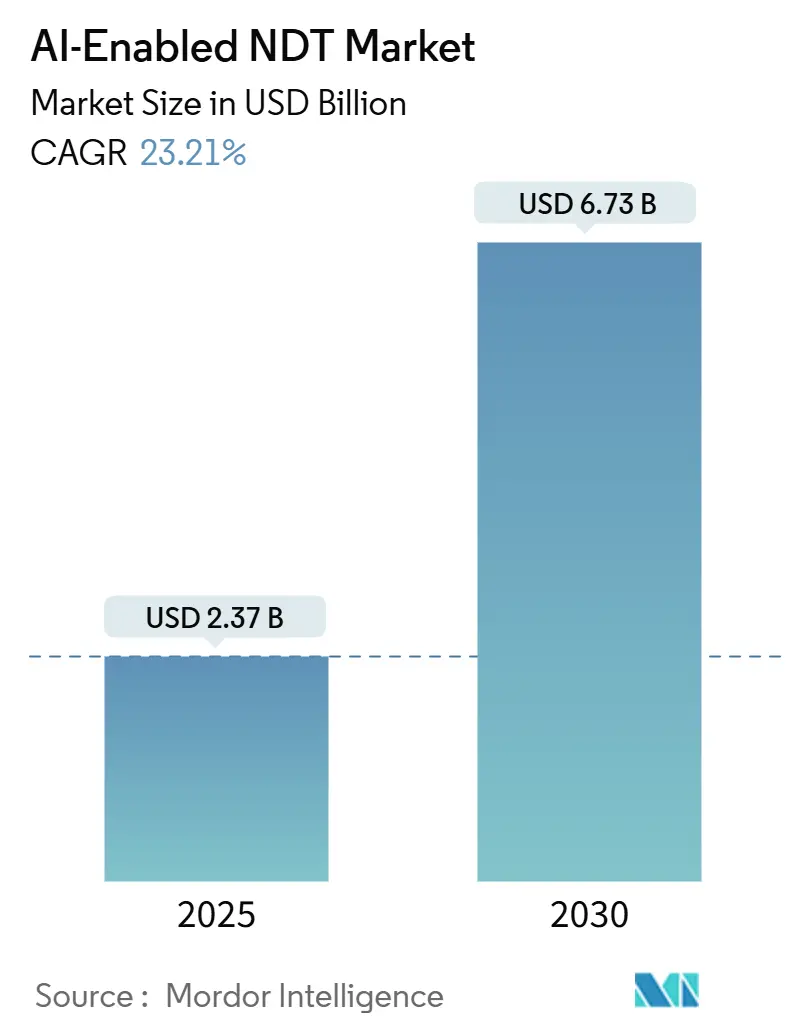

The AI-enabled NDT market size was USD 2.37 billion in 2025 and is projected to reach USD 6.73 billion by 2030, growing at a 23.21% CAGR from 2025 to 2030. Robust CAPEX programs in oil and gas, electric-vehicle-led shifts in automotive manufacturing, and computer-vision breakthroughs that compress inspection cycles are expanding the addressable customer base for AI inspection platforms. Faster defect detection reduces shutdown days, while cloud and edge compute options provide asset owners with elastic processing choices that lower the total cost of ownership. Vendors that bundle explainable AI toolkits with robotics now win multi-site contracts, and regulatory bodies are gradually codifying guidance that legitimizes algorithm-assisted calls. Persistent cybersecurity threats, however, oblige operators to isolate critical inspection networks and favor suppliers offering verifiable encryption.

Key Report Takeaways

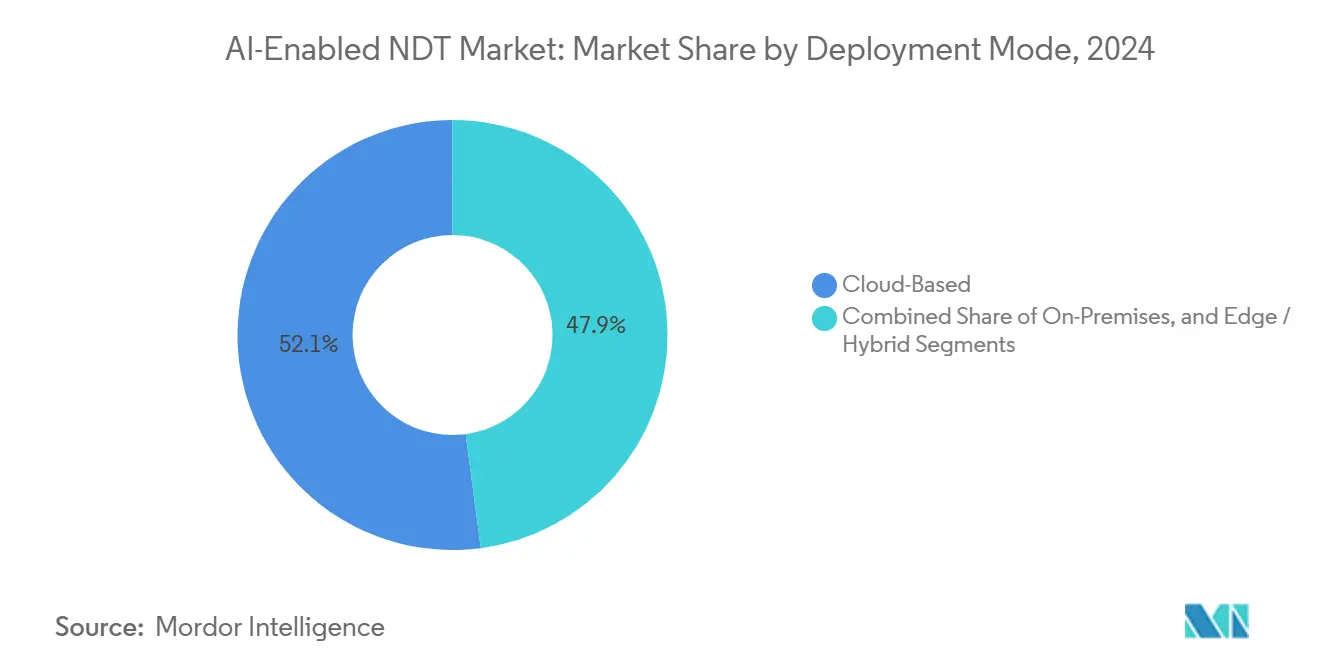

- By deployment mode, cloud services led with 52.1% revenue share in 2024, while edge and hybrid architectures are projected to post a 28.3% CAGR to 2030.

- By component, services held 78.7% of the AI-enabled NDT market share in 2024; software is forecast to expand at 30.5% through 2030.

- By testing method, ultrasonic testing captured 28.4% of the AI-enabled NDT market size in 2024; eddy-current testing is projected to advance at a 26.4% CAGR through 2030.

- By end-user, the oil and gas sector dominated with a 24.8% revenue share in 2024, whereas the automotive and transportation sector is set to accelerate at a 29.7% CAGR between 2025 and 2030.

- By geography, North America accounted for 36.4% of the AI-enabled NDT market in 2024, and the Asia-Pacific region is predicted to grow at a 25.3% CAGR through 2030.

Global AI-Enabled NDT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancing computer-vision algorithms cuts inspection time | +4.2% | Global, with early adoption in North America and Europe | Short term (≤ 2 years) |

| Growing demand for predictive maintenance in process industries | +3.8% | Global, strongest in oil and gas regions (Middle East, North America) | Medium term (2-4 years) |

| Integration of AI with robotics for hazardous-area inspection | +3.1% | North America, Europe, Asia-Pacific industrial corridors | Medium term (2-4 years) |

| Shift toward asset-integrity management standards | +2.9% | Global, regulatory-driven in developed markets | Long term (≥ 4 years) |

| Emergence of physics-informed neural networks for defect characterization | +2.7% | Advanced manufacturing regions (Germany, Japan, South Korea) | Long term (≥ 4 years) |

| Proliferation of digital twins enabling closed-loop NDT analytics | +2.4% | Industry 4.0 leaders (Germany, the United States, and China) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advancing Computer-Vision Algorithms Cut Inspection Time

Convolutional neural networks can now detect surface discontinuities as small as 1 mm in seconds, surpassing human repeatability and freeing inspectors for higher-order tasks.[1]IEEE Editorial Board, “Computer Vision for Automated Defect Detection,” ieeexplore.ieee.org Transformer models handle 4K radiographic images in near real time, removing production bottlenecks in aerospace forging lines. Classification accuracy routinely reaches 95%, a 10-15 percentage-point gain over manual interpretation, which underpins the 40% reduction in average cycle time reported by turbine blade producers. Standards bodies, such as ASME Section V, are drafting annexes that define acceptable automated call validation, signaling broader acceptance while retaining human sign-off for critical welds.

Growing Demand for Predictive Maintenance in Process Industries

Oil refineries and petrochemical crackers are abandoning calendar-based shutdowns in favor of condition-based windows orchestrated by AI-enabled NDT alerts, which lowers unplanned downtime by up to 50% and saves USD 1-5 million per avoided outage.[2]Shell Technology Center, “Predictive Maintenance Case Studies,” shell.com Ultrasonic thickness readings, vibration spectra, and IR thermograms are integrated into cloud dashboards that forecast wall loss or bearing failure weeks in advance. ERP integration automatically queues spare-part requisitions, and finance teams link risk probabilities to cash-flow models, turning inspection data into strategic budget levers.

Integration of AI with Robotics for Hazardous-Area Inspection

Drones, pipe crawlers, and magnetic-wheeled robots equipped with AI inspection heads now deliver 24/7 coverage in explosive or radioactive zones, eliminating the need for confined-space entry permits and reducing insurance premiums. Edge compute packs on these machines pre-process sensor streams so only flagged anomalies hit the cloud, slashing bandwidth costs and enabling real-time decision loops that direct robots to rescan suspect areas autonomously. Case studies on offshore platforms demonstrate a 2-fold increase in inspected weld length per shift with zero human exposure.

Shift Toward Asset-Integrity Management Standards

Regulations such as API 580 mandate quantified risk frameworks that depend on continuous inspection feedback. AI platforms surface probability-of-failure curves tied to operating pressure, corrosion rate, and historical anomalies, giving operators a defensible basis to defer or expedite turnarounds.[3]American Petroleum Institute, “API 580 Risk-Based Inspection,” api.org Auditors now request machine-generated evidence trails, pushing suppliers to embed explainability modules that record feature-weight contributions behind every call.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of labeled flaw datasets for algorithm training | -2.8% | Global, particularly acute in specialized industries | Medium term (2-4 years) |

| High upfront cost of AI-ready NDT equipment | -2.1% | Cost-sensitive markets (emerging economies, SMEs) | Short term (≤ 2 years) |

| Cybersecurity concerns in connected inspection platforms | -1.9% | Global, heightened in critical infrastructure sectors | Medium term (2-4 years) |

| Regulatory uncertainty on AI model explainability | -1.6% | Developed markets with strict compliance requirements | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Labeled Flaw Datasets for Algorithm Training

Supervised learning relies on curated flaw libraries with dimensional truth; however, proprietary concerns and the limited capture of rare crack morphologies leave many verticals data-starved. Development cycles stretch 12-18 months as vendors stage synthetic flaw campaigns or negotiate anonymized data pools.[4]National Institute of Standards and Technology, “Industrial AI Dataset Challenges,” nist.gov Until federated-learning initiatives scale, model generalization across alloys and component geometries will lag, slowing adoption in nuclear and medical device applications where defect tolerance is unforgiving.

High Upfront Cost of AI-Ready NDT Equipment

Facility retrofits often exceed USD 500,000, encompassing phased-array probes, GPU edge servers, and annual cloud subscriptions that account for 20-30% of the original spend. Budget-restricted SMEs defer purchases despite attractive ROI projections, thereby elongating replacement cycles for analog equipment that lacks streaming and computing capabilities. Leasing models and inspection-as-a-service offerings are emerging stop-gaps but have yet to penetrate price-sensitive emerging markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode – Cloud Dominance Persists While Edge Gains Momentum

Cloud platforms owned 52.1% of the AI-enabled NDT market in 2024, supplying elastic GPU farms that accelerate model training and coordinate multi-site updates. Many global majors now route terabytes of ultrasonic capture to regionally compliant data centers, achieving algorithm parity across refinery networks. The AI-enabled NDT market size attributed to cloud deployments is projected to reach USD 3.4 billion by 2030 as SaaS billing aligns with OPEX budgets. Edge and hybrid topologies, however, register a brisk 28.3% CAGR, shipping hardened inference boxes that slash round-trip latency below 50 milliseconds for autonomous drone inspections. Vendors bundle self-healing software that syncs with the cloud during connectivity windows, ensuring version integrity and reducing IT overhead. Hybrid models split preprocessing on-premise and advanced analytics off-site, balancing confidentiality and compute economics in nuclear, defense, and offshore facilities.

Second-generation edge chipsets compress transformer networks into 15-W power envelopes, enabling battery-powered crawlers to run eight-hour missions without requiring swaps. This architectural flexibility eliminates bandwidth bottlenecks in remote mines, where satellite links cost USD 8 per GB, sparking pilot programs that are forecast to increase the AI-enabled NDT market share for the edge to 19% by 2030.

By Component – Services Lead but Software Becomes the Fastest Engine

Services retained a commanding 78.7% revenue footprint in 2024 because custom model tuning, standards compliance, and Level III sign-off remain labor-intensive. Inspection houses bundle algorithm validation, technician upskilling, and cyber-hardening under multi-year managed service contracts. With the pipeline of new hires thin, suppliers are investing in e-learning modules that reduce certification time by 30%. Software, meanwhile, shows a 30.5% CAGR as low-code platforms enable integrators to drag-and-drop inspection workflows and call pre-trained flaw libraries. Subscription licenses scale down to line-item plant budgets, accelerating penetration into discrete manufacturing. As OEMs embed AI accelerators inside probes and cameras, equipment sales hold steady yet cede value-add to firmware updates and analytics add-ons. Consumables—such as wedges, couplants, and calibration blocks—track installed-base growth but are often commoditized.

By Testing Method – Eddy Current Surges With Real-Time AI Synergy

Ultrasonic testing still commanded 28.4% of 2024 revenue, its lead underpinned by half-century code endorsements and phased-array innovations. AI modules now automatically optimize beam steering to compensate for anisotropic weld microstructures, elevating volumetric coverage to 98% and reducing wall-thickness sensitivity in sour-gas pipelines. The AI-enabled NDT market size for ultrasonic platforms is set to surpass USD 2 billion by 2030 as mainstream pressure-equipment codes widen AI annexes.

Eddy-current, lifted by a 26.4% CAGR, aligns neatly with convolutional filters that parse high-frequency impedance signatures to single out hairline surface cracks in aerospace rivet holes. GPU-accelerated inversion shrinks post-scan crunching from 5 minutes to 15 seconds. Emerging workflows combine pulsed eddy-current with thermal imaging, synthesizing multimodal datasets that enhance confidence scores. The radiographic, magnetic particle, and thermography segments integrate object-detection stacks that auto-flag porosity clusters or delaminations; however, their growth trails due to higher safety protocols or limited high-volume applications.

By End-User Industry – Automotive and Transportation Drives Next-Wave Uptake

Oil and gas owners controlled 24.8% of the AI-enabled NDT market share in 2024, as operators digitized their pipeline and upstream assets to meet methane-leak mitigation pledges. Robust budgets and decades of NDT culture have catalyzed the adoption of deep-learning crack classifiers and corrosion-growth predictors. Automotive and transportation, however, is the fastest riser, with a 29.7% CAGR. Gigafactories utilize inline eddy-current coils and IR cameras, which are connected to transformer models, to inspect battery tabs and laser welds at a conveyor speed of 1 meter per second. Lightweight aluminum chassis require high-frequency ultrasonic arrays, and OEMs demand statistical proof of zero-defect rates before scale-up.

Power generation utilities integrate AI into turbine blade scans and thermographic boiler monitoring, preventing forced outages that can cost USD 500,000 daily. Aerospace primes qualify physics-informed neural nets that simulate ultrasound propagation through composite lay-ups, halving the re-work loop. Electronics fabs are an emerging niche focused on sub-micron crack detection in micro-vias, aligning with AI optics optimized for semiconductor geometries.

Geography Analysis

North America retained 36.4% of 2024 revenue owing to USD 200 billion in annual plant maintenance outlays that finance advanced inspection pilots. Flagship users such as Boeing cut fuselage radiography turnarounds by 25% using cloud-hosted classifiers, while midstream pipeline majors leverage real-time inline analytics to schedule digs only when anomaly scores exceed risk thresholds. Federal agencies, such as PHMSA, are developing data-submission portals that accept AI-derived wall-loss estimates, thereby legitimizing the deployment of algorithms.

Asia-Pacific is the high-velocity region, advancing at a 25.3% CAGR as China, Japan, and South Korea embed AI inspection nodes into USD 4.2 trillion worth of manufacturing output. Government infrastructure megaprojects drive demand for inspections across rail, bridge, and LNG terminal builds. Local robotics startups partner with cloud hyperscalers to ship vertically integrated platforms packaged for export across ASEAN, boosting regional talent density and encouraging indigenous algorithm R&D.

Europe is following a steady path, fueled by Industry 4.0 subsidies that reimburse SMEs for their digitalization investments. German auto-makers tie ultrasonic phased-array data streams into MES to flag weld failures within 120 seconds, trimming scrap. Regulations, such as the EU Machinery Directive revisions, reference AI risk tiers, encouraging suppliers to maintain transparent decision logs. The Middle East and Africa rely heavily on oil and gas, but are also witnessing a nascent uptake in petrochemicals and renewables; meanwhile, cybersecurity mandates require on-premise inference nodes. South America shows pilot projects in mining haul-truck inspection, with adoption gated by currency volatility.

Competitive Landscape

Market consolidation remains moderate. Baker Hughes integrated AI toolkit suppliers to incorporate Cordant Edge analytics into its legacy inspection fleets, providing single-pane dashboards for pipeline clients. Waygate Technologies invested USD 50 million in a Munich lab that crafts physics-informed networks tailored to aerospace composites. MISTRAS Group acquired InspectionAI to enhance computer-vision coverage of civil infrastructure, signaling a horizontal expansion beyond the oil and gas sector.

Differentiation circles explainable AI modules. Zetec codes eddy-current-specific convolution layers that output saliency maps, while Evident Corporation integrates beam-forming visualizers into OmniScan X3 64, enabling auditors to trace the origins of amplitude. Startups focus on narrow verticals, such as additive manufacturing or microelectronics, where incumbents lack domain expertise. Cloud alliances with hyperscalers grant scalable compute; however, data sovereignty rules in defense and energy constrain lift-and-shift architectures, favoring hybrid stacks. The top five vendors account for roughly 45% of 2024 revenue, reflecting a mildly concentrated field where niche experts still carve out footholds.

AI-Enabled NDT Industry Leaders

Baker Hughes Company

Waygate Technologies GmbH

Eddyfi NDT Inc

MISTRAS Group Inc

Evident Corporation (Olympus)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Baker Hughes rolled out Cordant Edge for real-time pipeline analytics, pairing inline inspection with cloud dashboards that rank repair urgency.

- December 2024: Waygate Technologies earmarked USD 50 million to open a Munich AI center for physics-informed inspection research.

- November 2024: MISTRAS Group acquired InspectionAI for USD 35 million to infuse computer-vision into structural health monitoring.

- October 2024: Evident Corporation launched OmniScan X3 64 with embedded AI phased-array processing.

Global AI-Enabled NDT Market Report Scope

| Cloud-Based |

| On-Premises |

| Edge / Hybrid |

| Equipment |

| Software |

| Services |

| Consumables |

| Ultrasonic Testing |

| Radiographic Testing |

| Magnetic Particle Testing |

| Liquid Penetrant Testing |

| Visual Inspection Testing |

| Eddy-Current Testing |

| Acoustic Emission Testing |

| Thermography / Infrared Testing |

| Computed Tomography Testing |

| Oil and Gas |

| Power Generation |

| Aerospace |

| Defense |

| Automotive and Transportation |

| Manufacturing and Heavy Engineering |

| Construction and Infrastructure |

| Chemical and Petrochemical |

| Marine and Ship Building |

| Electronics and semiconductor |

| Mining |

| Medical Devices |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Deployment Mode | Cloud-Based | ||

| On-Premises | |||

| Edge / Hybrid | |||

| By Component | Equipment | ||

| Software | |||

| Services | |||

| Consumables | |||

| By Testing Method | Ultrasonic Testing | ||

| Radiographic Testing | |||

| Magnetic Particle Testing | |||

| Liquid Penetrant Testing | |||

| Visual Inspection Testing | |||

| Eddy-Current Testing | |||

| Acoustic Emission Testing | |||

| Thermography / Infrared Testing | |||

| Computed Tomography Testing | |||

| By End-user Industry | Oil and Gas | ||

| Power Generation | |||

| Aerospace | |||

| Defense | |||

| Automotive and Transportation | |||

| Manufacturing and Heavy Engineering | |||

| Construction and Infrastructure | |||

| Chemical and Petrochemical | |||

| Marine and Ship Building | |||

| Electronics and semiconductor | |||

| Mining | |||

| Medical Devices | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the AI-enabled NDT market expected to grow through 2030?

The AI-enabled NDT market is forecast to expand from USD 2.37 billion in 2025 to USD 6.73 billion by 2030, translating into a 23.21% CAGR.

Which deployment model is gaining momentum alongside cloud solutions?

Edge and hybrid architectures are the fastest-growing, with a projected 28.3% CAGR, as latency-sensitive inspections shift processing closer to assets.

What drives the rapid adoption of AI-enabled NDT in automotive production?

Electric-vehicle plants require real-time inspection of battery welds and lightweight materials, driving the automotive and transportation sectors to a 29.7% CAGR.

Why are labeled flaw datasets critical for AI model accuracy?

High-quality, ground-truth defect libraries enable supervised learning; however, their scarcity delays the generalization of algorithms across industries.

Which region will add the most new spending on AI-enabled inspection tools?

The Asia-Pacific region, advancing at a 25.3% CAGR, is expected to outpace other regions due to large-scale manufacturing digitization and infrastructure development programs.

Page last updated on: