Adhesive Films Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 39.92 Billion |

| Market Size (2031) | USD 50.78 Billion |

| Growth Rate (2026 - 2031) | 4.93% CAGR |

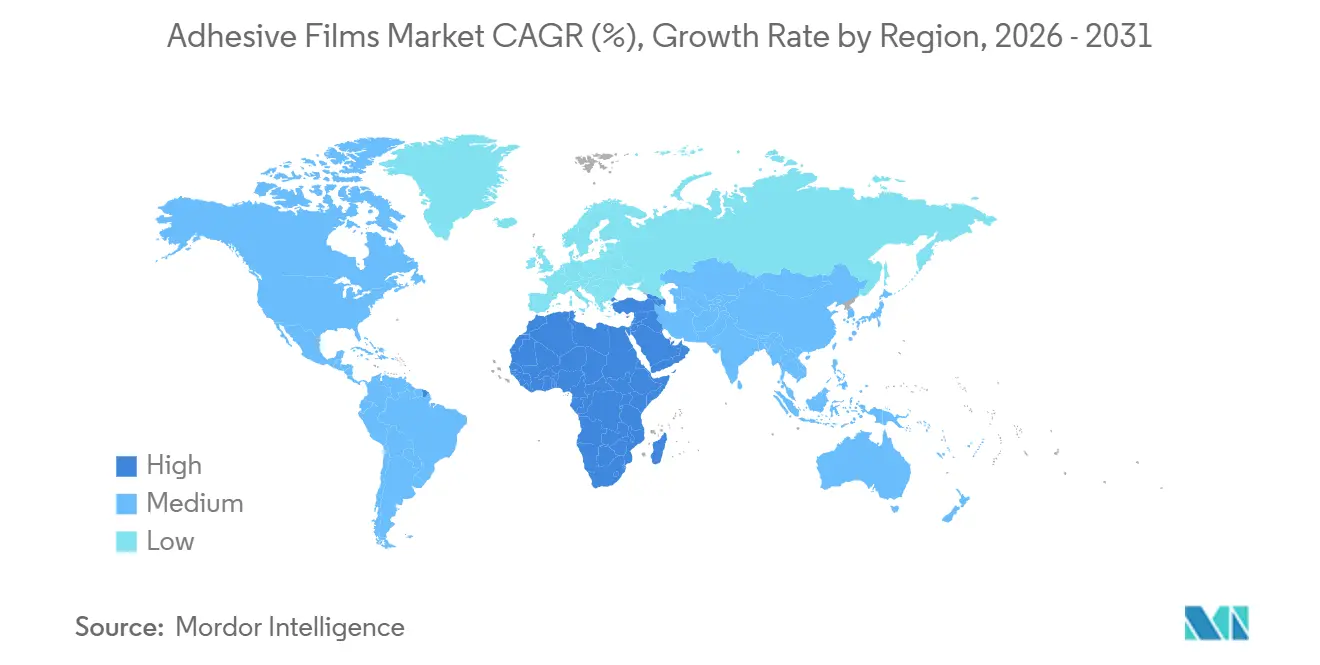

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

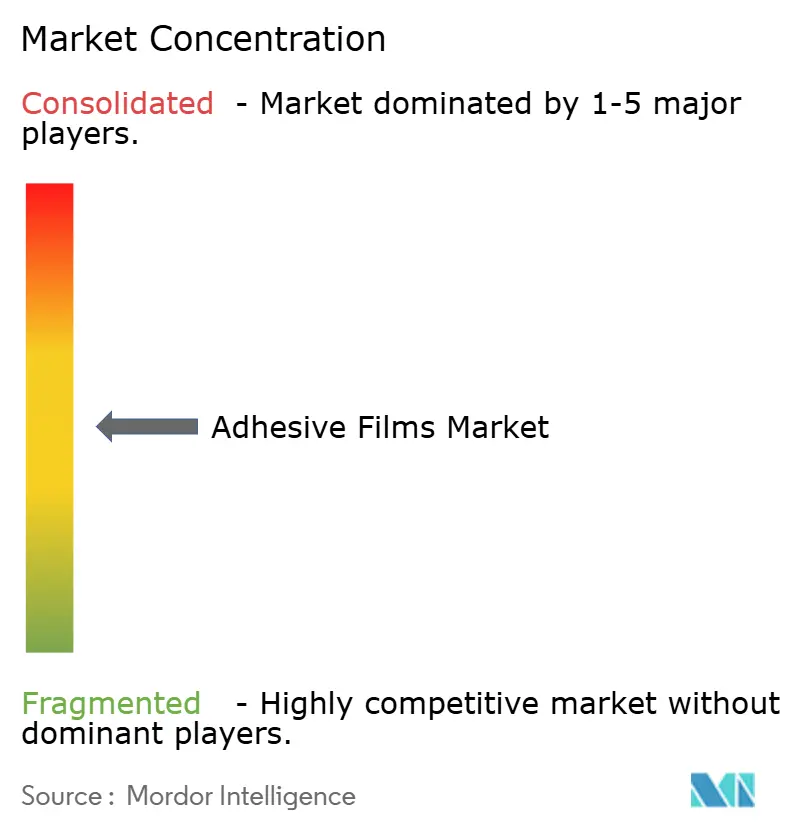

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Adhesive Films Market Analysis by Mordor Intelligence

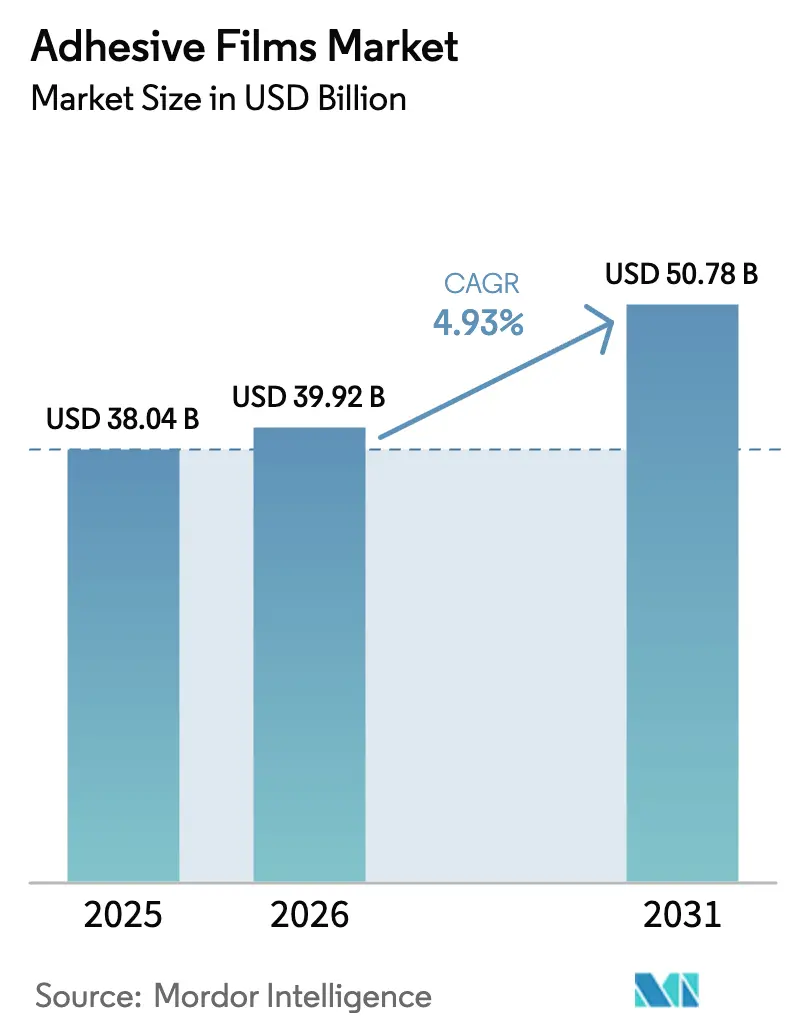

The Adhesive Films Market size is expected to grow from USD 38.04 billion in 2025 to USD 39.92 billion in 2026 and is forecast to reach USD 50.78 billion by 2031 at 4.93% CAGR over 2026-2031. Current growth rests on three pillars: surging electric-vehicle battery builds that demand sub-50-micron bonding layers, accelerating e-commerce parcel volumes that favor lighter yet tougher packaging films, and quickening product-design cycles in flexible electronics that reward ultra-thin optically clear adhesives. Competitive dynamics now hinge on precision-coating capabilities, sustainability credentials, and responsiveness to resin-price swings, all of which shape procurement decisions across automotive, electronics, and packaging supply chains. Market leaders continue to widen the technology gap through investments in water-based chemistries, ultraviolet curing, and high-filler thermally conductive films, while regional specialists leverage fast prototyping and short-run service levels to win niche projects.

Key Report Takeaways

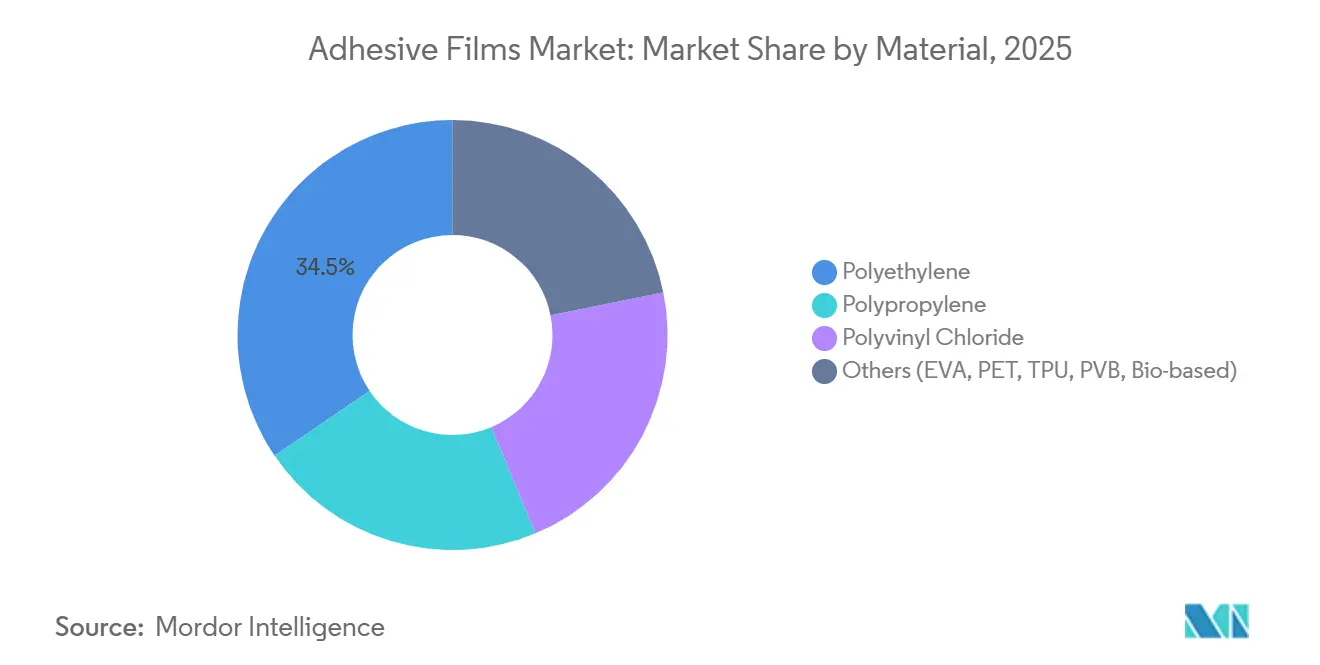

- By material, polyethylene captured 34.47% of adhesive films market share in 2025. Bio-based and specialty polymer blends are projected to expand at a 6.31% CAGR through 2031.

- Pressure-sensitive technology held 46.38% revenue share in 2025. Radiation and ultraviolet-cured films are forecast to be the fastest-growing technology at a 6.42% CAGR to 2031.

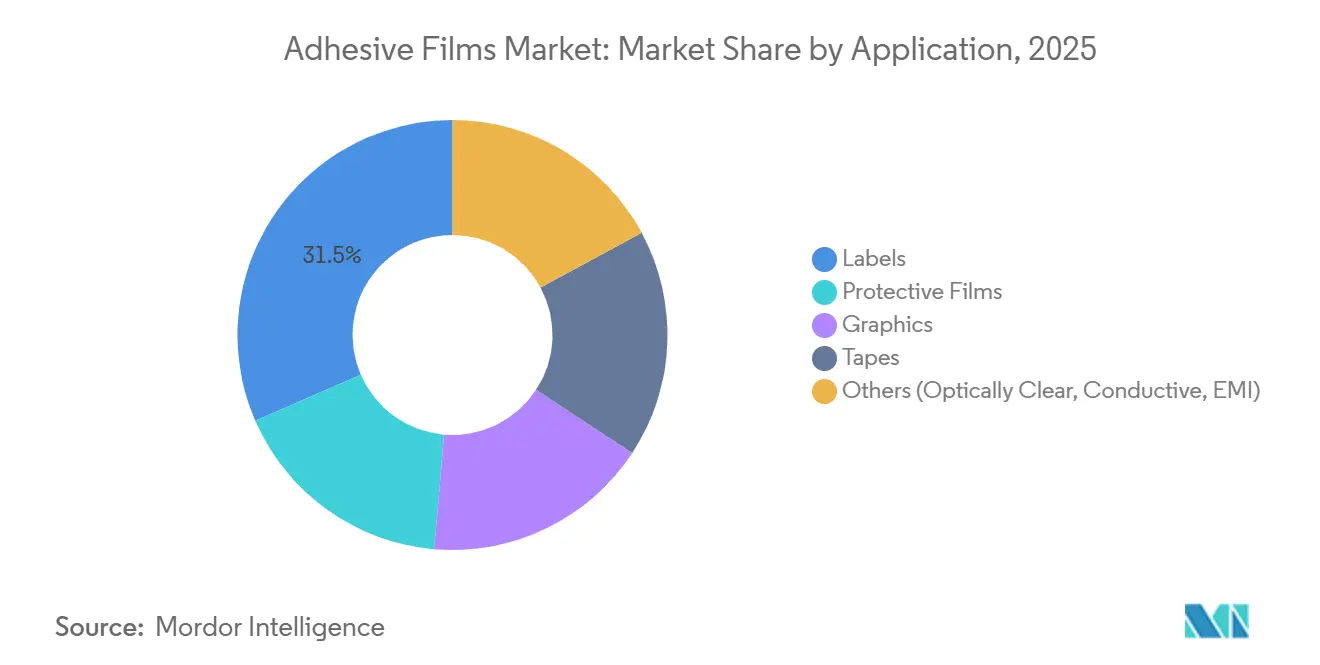

- Labels accounted for 31.52% of application revenue in 2025. Optically clear, conductive, and electromagnetic-interference-shielding films are set to advance at a 6.27% CAGR through 2031.

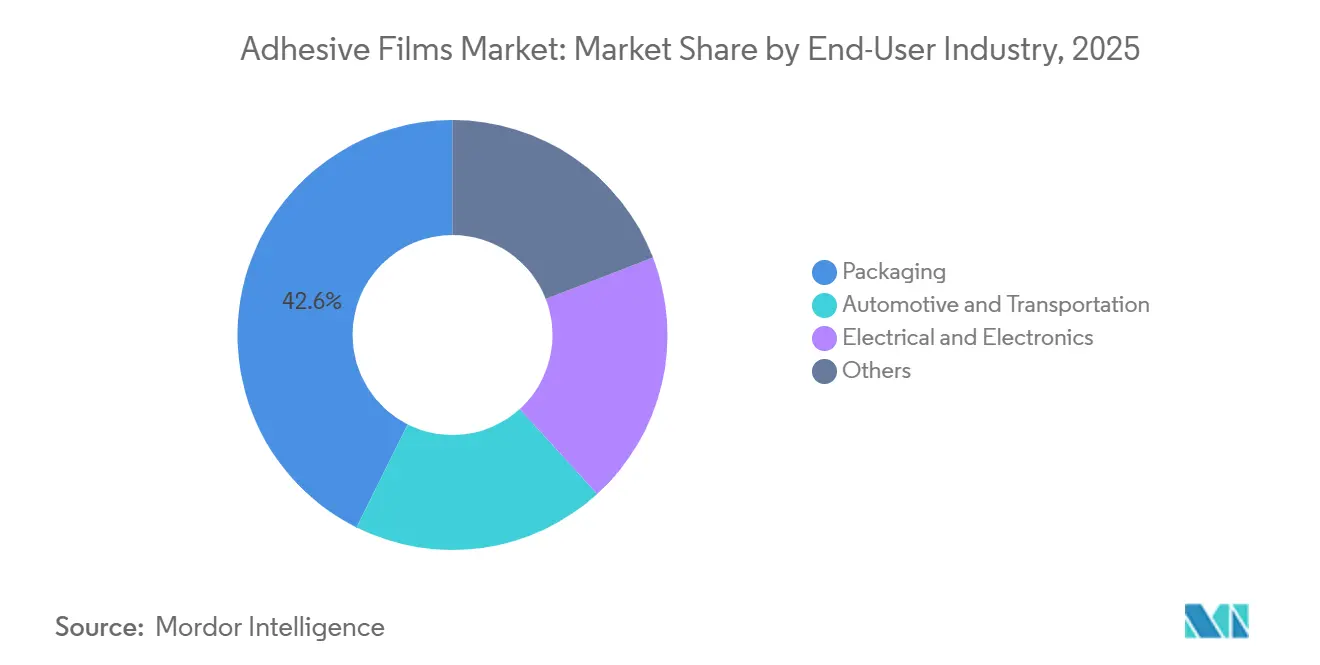

- Packaging represented 42.63% of demand in 2025. Electrical and electronics end-users are expected to grow at a 6.24% CAGR through 2031.

- Asia-Pacific contributed 48.36% of global revenue in 2025. The Middle East and Africa are projected to deliver the fastest regional CAGR at 5.93% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Adhesive Films Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV/Battery Thermal-Management Demand | +0.8% | China, EU, North America | Medium term (2-4 years) |

| E-commerce Packaging Boom | +0.6% | APAC, North America | Short term (≤ 2 years) |

| Miniaturization in Flexible and Wearable Electronics | +0.7% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Shift to Water-based/Solvent-free Chemistries | +0.5% | North America, EU | Long term (≥ 4 years) |

| Infrastructure Spend on Smart Construction Facades | +0.4% | Middle East, China, select EU markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV/Battery Thermal-Management Demand

Vehicle manufacturers moving from module-to-pack to cell-to-pack architectures need films that deliver both electrical isolation and thermal conductivity above 3 W/m-K. Henkel posted an 18% jump in revenue from thermally conductive adhesive films during 2024, aided by solutions that replace gap pads and eliminate one-third of assembly steps. H.B. Fuller’s EV THERM series, launched in 2024, laminates in a single pass and carries ceramic filler loadings above 70 wt%. Patent applications for adhesive-based runaway barriers rose 22% year on year in 2024, underscoring the strategic importance of fire-mitigation films. Lithium-iron-phosphate packs require more cells per vehicle, lifting film consumption by roughly 25-35% per car. New standards such as UL 2580 now call for 1,000-hour thermal-aging tests at 85 °C, accelerating the shift from acrylic to silicone or polyurethane chemistries.

E-commerce Packaging Boom

Parcel throughput per square meter jumped 15% versus 2024, compelling fulfillment operators to specify thinner gauges-now 35 microns instead of 50 microns-while still passing 1.2-meter drop tests. The EU Packaging and Packaging Waste Regulation demands 70% recyclability by 2030, encouraging mono-material polyethylene constructions bonded with water-based adhesives[1]Nature Communications, “Low-Haze Optically Clear Adhesives for Foldable OLEDs,” nature.com. H.B. Fuller reported double-digit growth in water-based packaging adhesives in 2024 as brand owners chased volatile-organic-compound limits below 250 g/L. Rising product return rates sustain demand for re-sealable adhesive films that maintain tack after multiple openings. Meanwhile, the average parcel weight fell from 2.8 kg in 2020 to 2.3 kg in 2025, magnifying cost savings from lightweight films.

Miniaturization in Flexible and Wearable Electronics

Printed-sensor production is on track to top USD 15.3 billion by 2030, with adhesive films acting as both substrate and encapsulant. Samsung Display and LG Display now employ optically clear films under 25 microns that must match panel refractive index within 0.02 and stay below 1% haze[2]ChannelNews, “Samsung & LG Are Joining Forces on Power Efficient OLED Panels,” channelnews.com.au. LINTEC’s 2024 dicing tapes enable 10-micron die separation without chipping, a prerequisite for chiplet packaging. Wearable health monitors integrate conductive adhesive films that double as electrodes, trimming component count and bill-of-materials cost by USD 0.40-0.60 per unit. Compliance with IEC 62368-1 drives uptake of halogen-free flame retardants, lifting raw-material spend by 8-12% yet unlocking premium OEM demand.

Shift to Water-based/Solvent-free Chemistries

U.S. EPA rules cap volatile-organic-compound content at 250 g/L for flexible-packaging adhesives, a limit that solvent-based systems overshoot by up to 50%. Henkel earmarked EUR 150 million in 2024 to enlarge water-based output in Düsseldorf and Bridgewater. Europe’s planned PFAS ban will outlaw fluorinated release liners by 2026, stoking reformulation toward silicone-based alternatives that still lag on release-force consistency. Water-based pressure-sensitives need 20-30% longer drying time, slowing uptake among label press lines running 200 m/min. Hot-melt faces open-time limits, but their zero-VOC profile secures a share in carton and case sealing.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-Material Price Volatility | -0.6% | North America, Europe | Short term (≤ 2 years) |

| Complex End-of-life Recycling of Multi-layer Films | -0.4% | EU, North America | Medium term (2-4 years) |

| Stricter PFAS and VOC Regulations | -0.5% | North America, EU, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

Polyethylene resin added 8 cents/lb during the first two months of 2025, while polypropylene climbed 4 cents/lb, slicing 200-300 basis points off converter margin. The U.S. Producer Price Index for plastic resins hit 275.323 in March 2025, up 2.5% quarter on quarter. Smaller converters lacking hedging tools face a 6-9-month delay before passing costs to customers, pushing many sub-USD 50 million firms toward consolidation. Structural oversupply keeps global cracker utilization near 80%, yet unplanned outages and geopolitical shocks still jolt spot prices.

Stricter PFAS and VOC Regulations

The EU Packaging and Packaging Waste Regulation compels 70% recyclability by 2030, threatening 15-20% of current multilayer film capacity. Proposed REACH Annex XV PFAS limits will remove fluorinated release liners that account for about half of silicone-free liner stocks. U.S. EPA formaldehyde limits below 0.09 ppm for composite wood products also affect laminating adhesives in furniture supply chains. Only 14% of plastic packaging is collected for recycling worldwide, and the rate falls below 5% for multilayer flexible films, reflecting delamination challenges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Bio-based Blends Narrow Cost Gap

Polyethylene delivered 34.47% of 2025 revenue thanks to its cost advantage at USD 1.20-1.40 per kg and compatibility with widespread blown-film assets. Specialty and bio-based polymers are forecast to post a 6.31% CAGR, topping the overall adhesive films market by 140 basis points as automotive and electronics buyers embed carbon-reduction targets in supplier contracts. Polypropylene ranks second by volume on the strength of its clarity and moisture barrier, but its 4.5% growth trails specialty blends that promise better heat stability.

In niche arenas, thermoplastic polyurethane commands USD 8-12 per kg, justified by elasticity and abrasion resistance valued in paint-protection and wound-care films. Polyvinyl butyral is spreading from windshield interlayers to smart-glass façades, a segment that could reach 20 million m² annually by 2030. Compostable options such as polylactic acid remain under 2% share because heat-deflection temperatures below 60 °C prevent use in most hot-melt or thermal-lamination lines.

By Adhesive Technology: UV-Cured Films Gain Momentum

Radiation and ultraviolet-cured products are projected to grow at 6.42% CAGR, the fastest within the adhesive films market, spurred by electronics assemblers that cannot afford 10-15 second dwell times typical of hot-melts. Pressure-sensitives retained 46.38% share in 2025 owing to their plug-and-play integration on high-speed labelers. However, water-based versions require longer oven zones, posing a hurdle for converters running at 300 m/min.

Hot-melts have won incremental packaging share because they emit zero VOCs, yet their short open window restricts intricate pouch assembly. Solvent systems are tethered to sub-3% growth as EPA’s 250 g/L cap sparks migration to water-based formulations. Ultraviolet-cured pressure-sensitives now offer instant tack and 24-hour post-cure strength, but USD 200,000-plus lamp lines deter smaller shops.

By Application: Specialty Films Move Up the Value Ladder

Optically clear, conductive, and electromagnetic-interference-shielding films are forecast to climb at a 6.27% CAGR, outperforming labels, which still held 31.52% of 2025 revenue. Automotive paint-protection demand lifted protective films in line with the overall adhesive films market, thanks to XPEL’s direct-to-installer model that expands aftermarket reach.

Graphics films face substitution pressure from direct-to-substrate digital printing, causing flat growth at Avery Dennison’s graphic division. Conductive adhesive films, priced as high as USD 100 per m², enable touch sensors and shield 5G handsets from interference, trading at 10-20 times the value of commodity tapes. Optically clear adhesive output is dominated by a handful of Japanese and Korean firms that consistently meet haze below 1% and refractive-index tolerance within 0.02.

By End-User Industry: Electronics Accelerates

Packaging absorbed 42.63% of demand in 2025, yet electronics is set to register the quickest 6.24% CAGR as films migrate from passive covers to functional layers such as antennas and heat spreaders. Automotive builds continue to consume large square meterage for battery thermal interfaces, interior trim, and noise-damping, rising 5.8% in 2024 on 14 million electric-vehicle units.

Mono-material polyethylene pouches bonded with water-based adhesives are winning in e-commerce, while multilayer barrier films for shelf-stable food face recyclability headwinds. Electronics demand is heavily Asia-Pacific-centric, challenging North American and European suppliers to shorten lead times or invest in local compounding. Construction and medical applications offer steady volume but remain fragmented across small job sizes.

Geography Analysis

Asia-Pacific generated 48.36% of global revenue in 2025 and should extend at a 5.1% CAGR through 2031, propelled by its 60% share of semiconductor packaging capacity and dominance in smartphone assembly. China exported USD 1.75 billion of self-adhesive tape in 2023, confirming its price-setting status. Japan and South Korea stay at the innovation frontier for foldable OLED bonding films, while Southeast Asia attracts incremental lines as supply chains diversify.

North America and Europe together controlled a significant revenue share but will trail the Asia-Pacific by nearly 1 percentage point in CAGR. Resin price oscillations of 5-8 cents/lb in early 2025 squeezed margins and forced consolidation among mid-tier extruders. The EU’s recyclability mandate is triggering fresh capital for mono-material lines, including Henkel’s EUR 150 million water-based expansion. The United States remains the largest country market, supported by e-commerce parcel growth of 12% in 2024 and persistent automotive demand of roughly 225 million m² annually.

Middle East and Africa, though smaller, is forecast to grow fastest at 5.93% CAGR, helped by Saudi Arabia’s USD 1.1 trillion Vision 2030 build-out. Egypt’s flexible-packaging plants feed North African food brands, while United Arab Emirates construction projects lift demand for façade and interior laminate films. South America lags, with Brazil and Argentina constrained by import tariffs and limited domestic capacity for high-performance bases, keeping the region focused on commodity tapes and labels.

Competitive Landscape

The global adhesive films market is moderately consolidated. Competitive fronts are split between scale-driven commodity labels and science-intensive specialty films. Patent filings for lithium-ion cell encapsulation rose 22% in 2024, spotlighting a scramble for intellectual property that will define battery assembly standards through the decade. Emerging leaders in the market are exploiting white spaces by combining die-cut customization with sub-24-hour delivery for order sizes below 10,000 m², service levels that global conglomerates struggle to match. Leading groups defend legacy labels while investing in optically clear and thermally conductive lines whose unit economics yield three to five times the gross profit of commodity packaging films. Technological thrusts include ultraviolet-cured tackifiers that cut ovens, digital presses that run adhesive-backed media on demand, and hyperspectral inspection that detects defects under 10 microns, outperforming manual checks.

Adhesive Films Industry Leaders

3M

Avery Dennison Corporation

Henkel AG & Co. KGaA

Nitto Denko Corporation

LINTEC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: H.B. Fuller rolled out EV THERM thermally conductive pressure-sensitive films enabling one-pass lamination of battery cold plates, slashing assembly time by 30% .

- July 2024: Eastman Chemical expanded molecular recycling capacity targeting multilayer adhesive films, aiming for 200 million lb of recycled feedstock by 2027.

- June 2024: Henkel allocated EUR 150 million to enlarge water-based adhesive capability in Germany and the United States to help converters meet VOC and PFAS curbs.

Global Adhesive Films Market Report Scope

Adhesive films are thin layers of material coated with an adhesive that bonds surfaces together when applied. They are commonly used in packaging, electronics, automotive, aerospace, and construction industries. These films can be pressure-sensitive, heat-activated, or UV-cured.

The adhesive films market is segmented on the basis of material, adhesive technology, application, end-user industry, and geography. On the basis of material, the market is segmented into polyethylene, polypropylene, polyvinyl chloride, and others. By adhesive technology, the market is segmented into pressure-sensitive (PSA), hot-melt, water-based, solvent-based, and radiation/UV-cured. By application, the market is segmented into protective films, graphics, labels, tapes, and others. On the basis of end-user industry, the market is segmented into packaging, automotive and transportation, electrical and electronics, and others. The report also covers the market size and forecasts for the adhesive films market in 26 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Polyethylene |

| Polypropylene |

| Polyvinyl Chloride |

| Others (EVA, PET, TPU, PVB, Bio-based) |

| Pressure-Sensitive (PSA) |

| Hot-Melt |

| Water-based |

| Solvent-based |

| Radiation/UV-cured |

| Protective Films |

| Graphics |

| Labels |

| Tapes |

| Others (Optically Clear, Conductive, EMI) |

| Packaging |

| Automotive and Transportation |

| Electrical and Electronics |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material | Polyethylene | |

| Polypropylene | ||

| Polyvinyl Chloride | ||

| Others (EVA, PET, TPU, PVB, Bio-based) | ||

| By Adhesive Technology | Pressure-Sensitive (PSA) | |

| Hot-Melt | ||

| Water-based | ||

| Solvent-based | ||

| Radiation/UV-cured | ||

| By Application | Protective Films | |

| Graphics | ||

| Labels | ||

| Tapes | ||

| Others (Optically Clear, Conductive, EMI) | ||

| By End-User Industry | Packaging | |

| Automotive and Transportation | ||

| Electrical and Electronics | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| Qatar | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the adhesive films market?

The adhesive films market size stood at USD 39.92 billion in 2026 and is projected to reach USD 50.78 billion by 2031.

Which material leads demand in adhesive film production?

Polyethylene leads, accounting for 34.47% of global revenue in 2025 due to its low cost and broad processing compatibility.

Which application segment is expected to grow fastest?

Optically clear, conductive, and electromagnetic-interference-shielding films are forecast to advance at a 6.27% CAGR through 2031.

Why are ultraviolet-cured adhesive films gaining traction?

UV-cured films offer instant bonding without lengthy oven cycles, aligning with high-speed electronics lines and zero-VOC sustainability targets.

Which region will register the highest growth rate to 2031?

Middle East and Africa should post the quickest regional CAGR at 5.93%, buoyed by Saudi Vision 2030 infrastructure spending and packaging expansion in Egypt.

Page last updated on: