Structural Adhesives Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

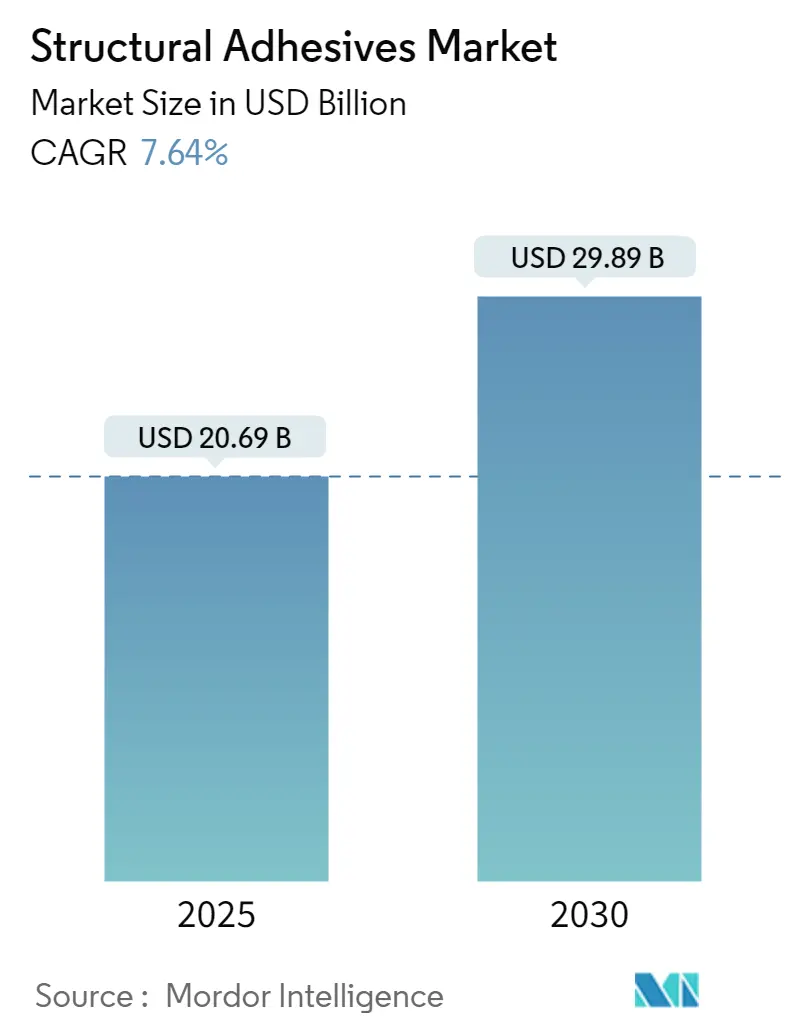

| Market Size (2025) | USD 20.69 Billion |

| Market Size (2030) | USD 29.89 Billion |

| Growth Rate (2025 - 2030) | 7.64% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

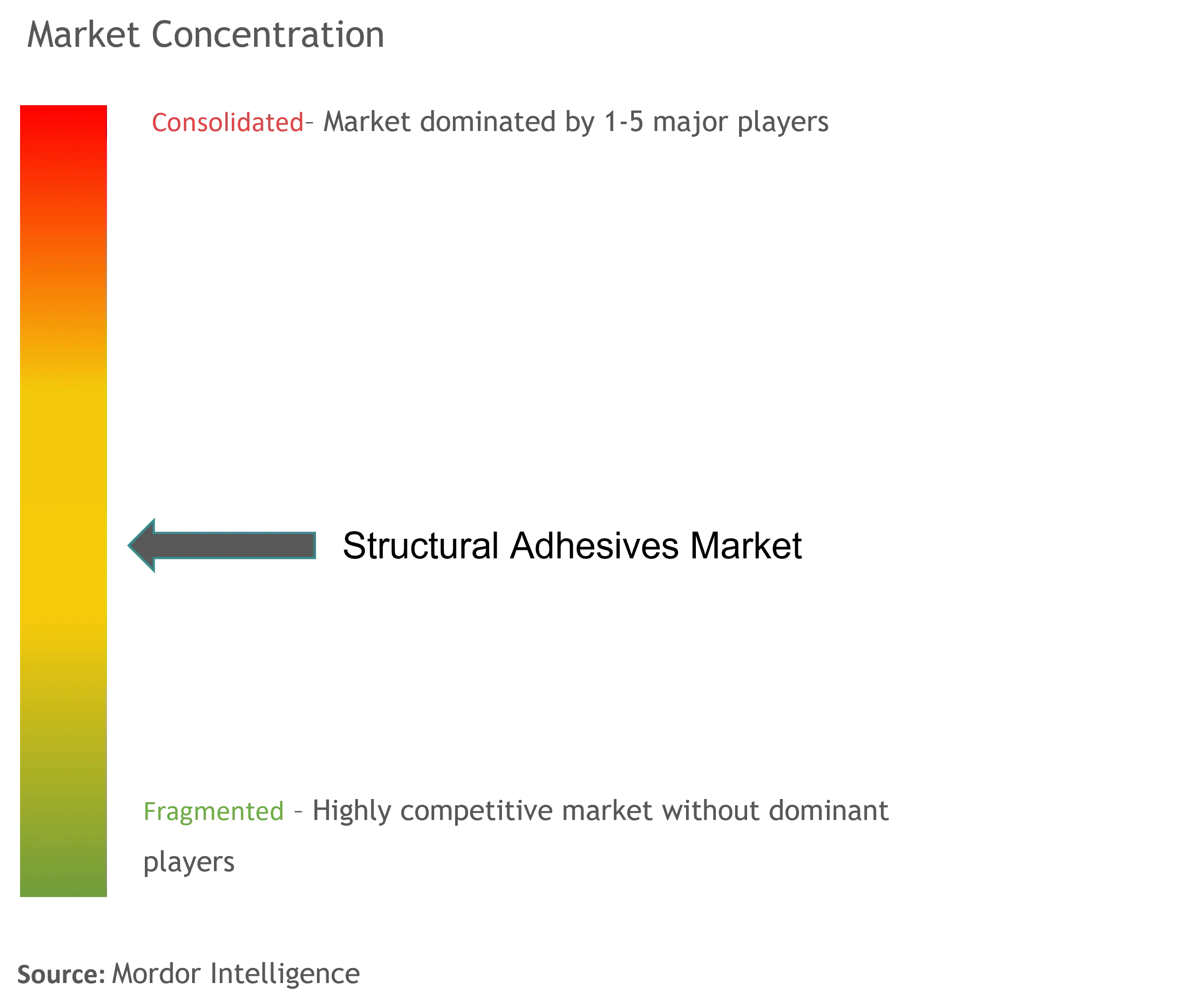

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Structural Adhesives Market Analysis by Mordor Intelligence

The Structural Adhesives Market size is estimated at USD 20.69 billion in 2025, and is expected to reach USD 29.89 billion by 2030, at a CAGR of 7.64% during the forecast period (2025-2030).

The structural adhesives industry continues to evolve with technological advancements in bonding solutions, particularly in response to the growing demand for lightweight materials across industries. Manufacturers are increasingly focusing on developing innovative advanced adhesives formulations that offer improved strength, durability, and processing characteristics. The integration of smart adhesive technologies, including self-healing properties and enhanced thermal resistance, has become a significant trend in the industry. These developments are particularly crucial as industries seek solutions that can withstand extreme conditions while maintaining structural integrity.

The aerospace and wind energy sectors have emerged as significant growth drivers for structural adhesives. According to Boeing Commercial Outlook 2022-2041, the global forecast for commercial aviation services is expected to reach USD 3,615 billion by 2041, driving demand for high-performance adhesive solutions. The wind energy sector has also demonstrated substantial growth, with the industry adding 93.6 GW of new wind energy installations globally in 2021, comprising 72.5 GW onshore and 21.1 GW offshore installations, creating increased demand for specialized adhesive solutions for turbine assembly and maintenance.

Environmental sustainability has become a central focus in the structural adhesives industry, with manufacturers investing in eco-friendly formulations and production processes. Companies are developing bio-based adhesives and implementing stricter environmental compliance measures in their manufacturing processes. The industry is witnessing a shift towards water-based and solvent-free formulations, responding to increasing regulatory pressure and consumer demand for sustainable products. These developments are reshaping product development strategies and manufacturing processes across the industry.

Supply chain optimization and digital transformation are revolutionizing the industrial adhesives manufacturing landscape. Companies are implementing advanced manufacturing technologies and automation solutions to improve production efficiency and product consistency. The integration of Industry 4.0 technologies, including artificial intelligence and machine learning, is enabling better quality control and predictive maintenance in adhesive manufacturing facilities. These technological advancements are helping manufacturers optimize their operations while maintaining high product quality standards and meeting increasing market demands.

Global Structural Adhesives Market Trends and Insights

Increase in Investments in Developing Economies in Asia-Pacific

The strong inflow of foreign direct investment (FDI) into the Asia-Pacific region has become a major driver for structural adhesives market demand across various industrial applications. Despite global economic challenges, FDI flows to Asian developing countries increased by 19% to reach an all-time high of USD 619 billion in 2021, with China, Hong Kong, Singapore, India, and Indonesia attracting over 80% of these investments. International project finance values in sectors critical to achieving UN Sustainable Development Goals increased significantly by 74% to USD 121 billion, primarily driven by increased interest in renewable energy projects that require substantial use of construction adhesives.

The manufacturing sector has witnessed particularly strong investment growth, exemplified by major projects like GlobalFoundries' USD 4 billion chipmaking plant in Singapore and significant semiconductor investments in Malaysia, including Risen Solar Technology's USD 10 billion, Intel's USD 7 billion, and AT&S's USD 2.1 billion projects. In India, substantial manufacturing investments include ArcelorMittal Nippon Steel's USD 13.5 billion steel and cement plant and Suzuki Motor's USD 2.4 billion car manufacturing facility. These large-scale manufacturing projects require extensive use of metal bonding adhesives in various applications, from equipment installation to final product assembly, driving sustained demand growth in the region.

Increasing Demand from the Global Construction and Automotive Sectors

The construction industry's robust growth has emerged as a key driver for construction adhesives demand, with the global construction market reaching a valuation of USD 7.2 trillion in 2021 and projected to grow at 3.6% in 2022. Construction adhesives have become increasingly critical in modern construction practices, offering advantages such as reduced material costs, enhanced productivity, and superior bonding strength. For instance, a four-foot-by-four-foot shear wall assembly that traditionally requires 45 minutes and approximately 300 collated screws can now be completed in just 5 minutes using adhesives and 75 pneumatic pins, resulting in an 85% reduction in construction time while maintaining structural integrity.

The automotive sector's evolution, particularly the transition toward electric vehicles, has created substantial demand for automotive adhesives. Global electric vehicle sales reached 6.75 million units in 2021, registering a remarkable growth rate of 108% compared to the previous year. Automotive adhesives play a crucial role in electric vehicle manufacturing, particularly in battery assembly and lightweight construction. The global automotive industry's production reached 80.15 million vehicles in 2021, with a growing emphasis on lightweight materials and alternative joining methods to improve fuel efficiency and reduce emissions. Structural adhesives are increasingly replacing traditional welding and mechanical fastening methods, as they can reduce vehicle weight while maintaining or improving structural integrity - an essential factor in modern automotive design and manufacturing.

Segment Analysis: Resin Type

Epoxy Segment in Structural Adhesives Market

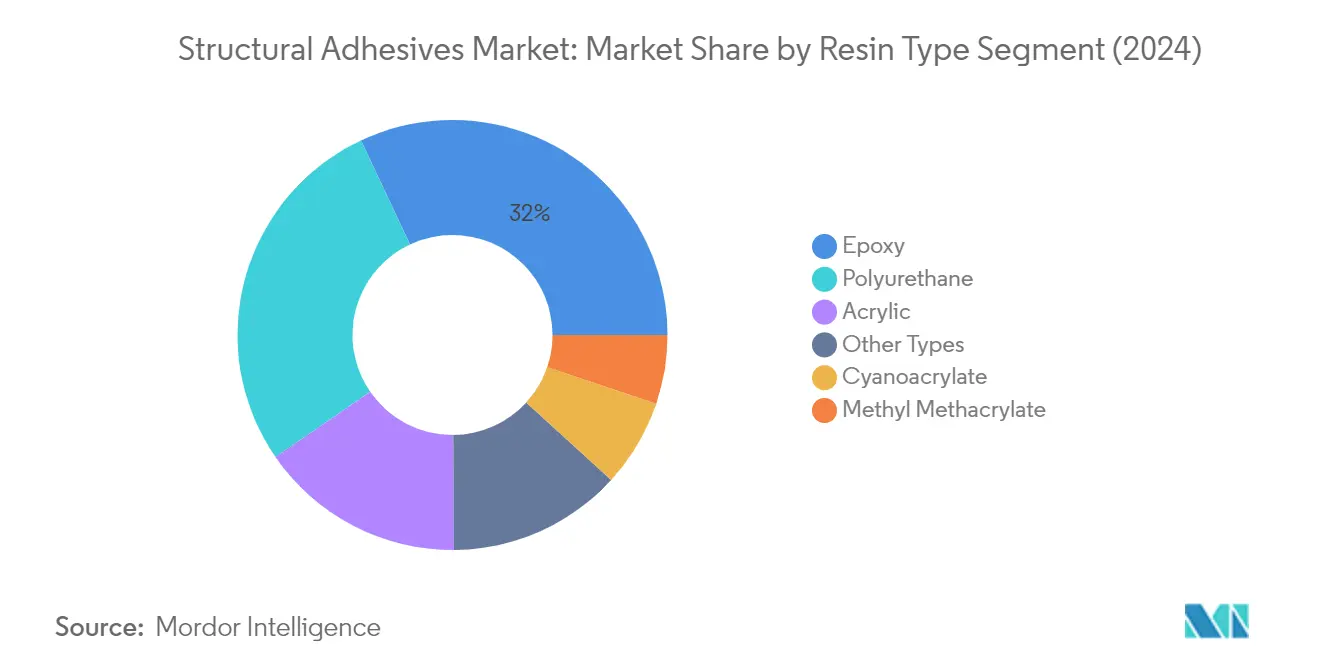

The epoxy adhesives segment dominates the structural adhesives market, commanding approximately 32% of the total market share in 2024. Epoxy adhesives have emerged as the preferred choice across various industries due to their superior bonding properties and versatility. These adhesives demonstrate exceptional performance in high-stress applications, particularly in the automotive, aerospace, and construction sectors. The segment is experiencing robust growth, projected to expand at around 7% from 2024 to 2029, driven by increasing demand in emerging economies and growing adoption in electric vehicle manufacturing. Epoxy adhesives offer crucial advantages including high mechanical strength, excellent chemical resistance, minimal shrinkage, and strong adhesion to a wide variety of substrates. Their widespread use in metal-to-metal bonding, composite materials assembly, and structural applications in building and construction continues to fuel their market dominance.

Remaining Segments in Resin Type

The structural adhesives market encompasses several other significant resin types, including polyurethane adhesives, acrylic adhesives, cyanoacrylate, and methyl methacrylate adhesives. Polyurethane adhesives have established a strong presence due to their flexibility and excellent durability in outdoor applications. Acrylic adhesives are valued for their fast curing properties and ability to bond dissimilar materials. Cyanoacrylate adhesives, known for their instant bonding capabilities, serve crucial roles in assembly operations and quick repairs. Methyl methacrylate adhesives have gained traction in high-performance applications requiring superior impact resistance. Each of these segments contributes uniquely to the market, serving specific application requirements across various industries and complementing the overall growth of the structural adhesives market.

Segment Analysis: End-User Industry

Construction Segment in Structural Adhesives Market

The construction segment dominates the structural adhesives market, commanding approximately 41% of the market share in 2024. This significant market position is driven by the extensive use of structural adhesives in various construction applications, including concrete-to-concrete bonding, ceramic tile-to-concrete bonding, masonry, construction panels, outside doors, sealing metal parts into concrete, civil engineering, and composite bonding. The segment's dominance is further strengthened by the growing trend of using structural adhesives to reduce construction time and materials, with studies showing up to an 85% reduction in assembly time compared to traditional fastening methods. Additionally, the implementation of major infrastructure projects across Asia-Pacific, North America, and Europe, coupled with increasing investments in residential and commercial construction activities, continues to drive the demand for structural adhesives in the construction sector.

Wind Energy Segment in Structural Adhesives Market

The wind energy segment is emerging as the fastest-growing segment in the structural adhesives market for the period 2024-2029. This remarkable growth is primarily driven by aggressive renewable energy targets set by various countries and substantial investments in wind power projects globally. The segment's growth is supported by the critical role of structural adhesives in wind turbine manufacturing, particularly in blade assembly, void filling, bolt fixing, metal-insert fixing, and panel and stringer structural bonding. The expansion is further accelerated by major wind energy projects in key markets like China, which currently operates almost half of the world's installed offshore wind capacity, and the European Union's ambitious wind energy expansion plans. The increasing focus on offshore wind installations and the development of larger, more efficient wind turbines is creating additional demand for high-performance structural adhesives in this sector.

Remaining Segments in End-User Industry

The automotive and aerospace adhesives segments, along with other industrial applications, constitute significant portions of the structural adhesives market. The automotive sector continues to be a crucial end-user, particularly with the increasing adoption of electric vehicles and lightweight materials in vehicle manufacturing. The aerospace segment, though smaller in market share, maintains steady demand due to the critical role of structural adhesives in aircraft manufacturing and maintenance. Other industrial applications span across electronics, marine adhesives, and medical devices sectors, each contributing to the market's diversity. These segments are characterized by their specific requirements for high-performance adhesives, ranging from temperature resistance in automotive applications to precision bonding in aerospace components.

Structural Adhesives Market Geography Segment Analysis

Structural Adhesives Market in Asia-Pacific

The Asia-Pacific region maintains its position as the dominant force in the global structural adhesives market, driven by robust manufacturing activities across various end-user industries. Countries like China, India, Japan, and South Korea form the backbone of this market, each contributing significantly through their respective industrial strengths. The region's growth is primarily fueled by increasing investments in construction, automotive manufacturing, and renewable energy sectors, particularly wind energy installations. The presence of major automotive manufacturers, a growing aerospace industry, and rapid industrialization continue to create substantial demand for structural adhesives across these economies.

Structural Adhesives Market in China

China stands as the powerhouse of the Asia-Pacific structural adhesives market, commanding approximately 72% of the regional market share in 2024. The country's dominance is reinforced by its position as the world's largest automotive manufacturer and construction market. China's structural adhesives industry benefits from the country's robust manufacturing sector, particularly in electric vehicle production and renewable energy installations. The government's focus on infrastructure development, including the construction of new megacities and the expansion of wind energy capacity, continues to drive demand. The country's aerospace and defense sectors also contribute significantly to market growth, supported by increasing investments in domestic aircraft manufacturing capabilities.

Structural Adhesives Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 7% during 2024-2029. The country's structural adhesives market is experiencing rapid expansion driven by ambitious infrastructure development plans and growing automotive manufacturing capabilities. India's position as the world's third-largest construction market by 2024 creates substantial opportunities for structural adhesives in various applications. The government's push towards electric vehicle manufacturing, coupled with initiatives like "Make in India" and "Aatma Nirbhar Bharat," further accelerates market growth. The country's expanding aerospace sector and growing wind energy installations also contribute to the increasing demand for structural adhesives.

Structural Adhesives Market in North America

North America represents a mature yet dynamic market for structural adhesives, characterized by advanced manufacturing capabilities and innovative applications across various industries. The region's market is primarily driven by the United States, Canada, and Mexico, each contributing uniquely through their industrial strengths. The region demonstrates strong demand from automotive manufacturing, particularly in electric vehicles, aerospace applications, and construction activities. The presence of major manufacturers and continuous technological advancements in adhesive formulations further strengthens the market position.

Structural Adhesives Market in United States

The United States dominates the North American structural adhesives market, holding approximately 79% of the regional market share in 2024. The country's market leadership is supported by its robust aerospace industry, extensive automotive manufacturing capabilities, and substantial construction activities. The nation's focus on electric vehicle production and renewable energy installations creates significant demand for structural adhesives. The presence of major adhesive manufacturers and continuous research and development activities in the country further reinforces its market position. The growing adoption of lightweight materials in various industries drives the demand for innovative structural adhesive solutions.

Structural Adhesives Market in Mexico

Mexico emerges as the fastest-growing market in North America, with an expected growth rate of approximately 7% during 2024-2029. The country's structural adhesives market benefits from increasing foreign investments in manufacturing facilities, particularly in the automotive sector. Mexico's strategic position as a manufacturing hub for North America, coupled with growing aerospace industry investments, drives market expansion. The country's construction sector development and increasing focus on renewable energy installations further contribute to market growth. The government's initiatives to attract manufacturing investments and develop industrial infrastructure support the growing demand for structural adhesives.

Structural Adhesives Market in Europe

Europe maintains its position as a significant market for structural adhesives, driven by its strong industrial base and technological advancement. The region's market is characterized by the presence of major economies including Germany, United Kingdom, Italy, and France, each contributing substantially to market growth. The region's focus on sustainable manufacturing practices and increasing adoption of electric vehicles creates new opportunities for structural adhesive applications. The strong presence of aerospace manufacturing and wind energy installations further drives market development across the region.

Structural Adhesives Market in Germany

Germany leads the European structural adhesives market through its advanced manufacturing capabilities and strong industrial base. The country's dominance is particularly evident in its automotive sector, where structural adhesives play a crucial role in electric vehicle manufacturing and lightweight construction. Germany's leadership in wind energy installations and aerospace manufacturing further strengthens its market position. The country's focus on research and development in adhesive technologies, coupled with the presence of major manufacturers, continues to drive innovation in the sector.

Structural Adhesives Market in United Kingdom

The United Kingdom demonstrates the fastest growth potential in the European structural adhesives market, driven by increasing investments in sustainable manufacturing and infrastructure development. The country's aerospace sector, being the second-largest in Europe, creates substantial demand for high-performance structural adhesives. The UK's commitment to electric vehicle manufacturing and offshore wind energy development further accelerates market growth. The government's focus on infrastructure development and construction activities supports the expanding application of structural adhesives.

Structural Adhesives Market in South America

The South American structural adhesives market shows promising growth potential, with Brazil emerging as both the largest and fastest-growing market in the region. Argentina also contributes significantly to regional market development. The market benefits from increasing investments in automotive manufacturing, construction activities, and renewable energy installations across these countries. Brazil's leadership is particularly evident in its robust automotive sector and growing aerospace industry, while Argentina's market is driven by infrastructure development and industrial growth. The region's focus on sustainable development and increasing industrial activities continues to create new opportunities for structural adhesive applications.

Structural Adhesives Market in Middle East and Africa

The Middle East and Africa region presents significant growth opportunities in the structural adhesives market, with Saudi Arabia emerging as the largest market and South Africa showing the fastest growth potential. The region's market is driven by increasing investments in construction activities, particularly in Saudi Arabia's ambitious infrastructure projects. The growing focus on renewable energy installations, especially wind energy projects, creates additional demand for structural adhesives. The automotive sector's development in South Africa and increasing aerospace activities across the region further contribute to market growth. The region's ongoing industrial diversification efforts and infrastructure development projects continue to expand the application scope for structural adhesives.

Competitive Landscape

Top Companies in Structural Adhesives Market

The structural adhesives market features prominent players like Henkel AG & Co. KGaA, Sika, 3M, H.B. Fuller, and Arkema, leading the industry through continuous innovation and strategic expansion. Companies are focusing on developing next-generation adhesive solutions with enhanced performance characteristics, particularly for automotive and aerospace applications. The industry witnesses regular product launches targeting specific end-user requirements, such as lightweight bonding solutions for electric vehicles and eco-friendly formulations for construction applications. Market leaders are strengthening their positions through strategic acquisitions and partnerships, exemplified by moves like Arkema's acquisition of Ashland's Performance Adhesive business and Sika's acquisition of Hamatite. Operational excellence is being achieved through investments in manufacturing facilities, R&D centers, and distribution networks across key regions, particularly in Asia-Pacific, where market growth potential remains substantial.

Consolidating Market with Strong Global Players

The structural adhesives market exhibits a partially fragmented structure, with the top five to six players commanding a significant share of the global market. These leading companies are typically large chemical conglomerates with diverse product portfolios, substantial R&D capabilities, and extensive global manufacturing footprints. The market is characterized by a mix of multinational corporations and regional specialists, with the former dominating due to their integrated operations and comprehensive distribution networks. The presence of vertically integrated players who manufacture both raw materials and final products adds another layer of complexity to the competitive landscape.

The industry is gradually moving toward consolidation through strategic mergers and acquisitions, as evidenced by recent high-profile transactions. Major players are actively pursuing acquisition opportunities to expand their geographic presence, enhance their technology portfolios, and strengthen their market positions in specific end-user segments. This consolidation trend is particularly pronounced in mature markets like Europe and North America, where companies are seeking to achieve economies of scale and broaden their product offerings through strategic combinations.

Innovation and Sustainability Drive Future Success

For established players to maintain and expand their market share, a focus on technological innovation and sustainability has become paramount. Companies are investing heavily in developing environmentally friendly adhesive solutions that meet increasingly stringent regulations while maintaining high-performance standards. The ability to offer comprehensive solutions across multiple end-user industries, combined with strong technical support and customer service capabilities, has become crucial for market leadership. Successful incumbents are also strengthening their positions through strategic partnerships with key customers in high-growth sectors like electric vehicles and renewable energy.

New entrants and smaller players can gain ground by focusing on specialized market segments and developing innovative solutions for specific applications. Success factors include building strong relationships with regional distributors, offering customized products for local market needs, and maintaining agility in responding to changing customer requirements. The relatively low threat of substitution for structural adhesives in many applications provides opportunities for growth, though companies must navigate challenges such as raw material price volatility and increasing environmental regulations. The concentration of end-users in sectors like automotive and aerospace makes strong industry relationships and technical expertise critical success factors.

Structural Adhesives Industry Leaders

3M

Henkel AG

Sika AG

H.B. Fuller Company

Arkema

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2022: Arkema finalized the acquisition of the Performance Adhesives business of Ashland. The products offered under this division include structural adhesives. The value of the transaction was USD 1.65 billion. The acquisition helped strengthen Arkema's Adhesive Solutions segment and aligned with the company's strategy to become a pure specialty material player by 2024.

- February 2022: H.B. Fuller Company announced that it had finalized its purchase of Apollo, a manufacturer of liquid adhesives, coatings, and primers for the roofing, industrial and construction markets. It is expected that Apollo will strengthen H.B. Fuller's position in important high-value, high-margin areas in the United Kingdom and Europe. Apollo will operate inside H.B. Fuller's current Construction Adhesives and Engineering Adhesives business units.

Global Structural Adhesives Market Report Scope

An adhesive that hardens or cures into a material that can hold two or more substrates together while withstanding the forces involved in the product's lifespan is referred to as a structural adhesive. It is also referred to as a "load-bearing" adhesive. Epoxies, methacrylates, polyurethanes, and cyanoacrylate adhesives are the types of adhesives that can hold things together.

The structural adhesives market is segmented by resin type, end-user industry, and geography. By resin type, the market is segmented into epoxy, polyurethane, acrylic, cyanoacrylate, methyl methacrylate, and other resin types. By end-user industry, the market is segmented into construction, automotive, aerospace, wind energy, and other end-user industries. The report covers the sizes and forecasts for the structural adhesives market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done based on value (USD million).

| Epoxy |

| Polyurethane |

| Acrylic |

| Cyanoacrylate |

| Methyl Methacrylate |

| Other Resin Types |

| Construction |

| Automotive |

| Aerospace |

| Wind Energy |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Resin Type | Epoxy | |

| Polyurethane | ||

| Acrylic | ||

| Cyanoacrylate | ||

| Methyl Methacrylate | ||

| Other Resin Types | ||

| By End-user Industry | Construction | |

| Automotive | ||

| Aerospace | ||

| Wind Energy | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Structural Adhesives Market?

The Structural Adhesives Market size is expected to reach USD 20.69 billion in 2025 and grow at a CAGR of 7.64% to reach USD 29.89 billion by 2030.

What is the current Structural Adhesives Market size?

In 2025, the Structural Adhesives Market size is expected to reach USD 20.69 billion.

Who are the key players in Structural Adhesives Market?

3M, Henkel AG, Sika AG, H.B. Fuller Company and Arkema are the major companies operating in the Structural Adhesives Market.

Which is the fastest growing region in Structural Adhesives Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Structural Adhesives Market?

In 2025, the Asia-Pacific accounts for the largest market share in Structural Adhesives Market.

What years does this Structural Adhesives Market cover, and what was the market size in 2024?

In 2024, the Structural Adhesives Market size was estimated at USD 19.11 billion. The report covers the Structural Adhesives Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Structural Adhesives Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: