Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

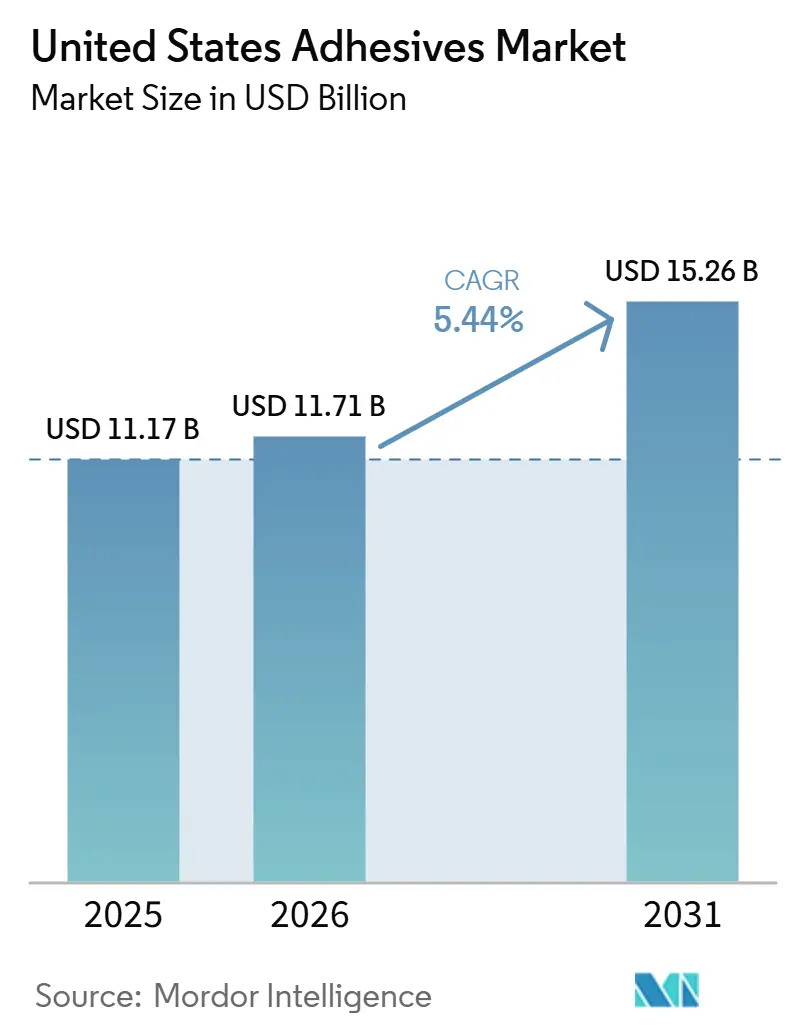

| Base Year Market Size (2025) | USD 11.17 Billion |

| Market Size (2026) | USD 11.71 Billion |

| Market Size (2031) | USD 15.26 Billion |

| Growth Rate (2026 - 2031) | 5.44% CAGR |

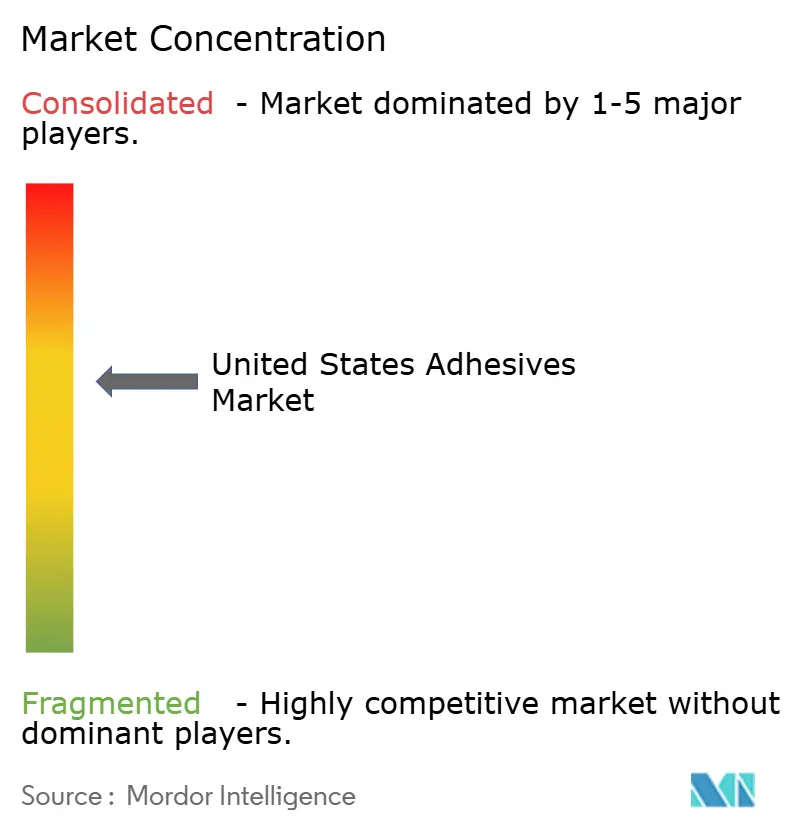

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Adhesives Market Analysis by Mordor Intelligence

The United States Adhesives Market size is expected to increase from USD 11.17 billion in 2025 to USD 11.71 billion in 2026 and reach USD 15.26 billion by 2031, growing at a CAGR of 5.44% over 2026-2031. Federal “Buy Clean” procurement mandates, surging electric-vehicle (EV) output, robust e-commerce logistics, and rising residential construction underpin steady demand. Large producers are accelerating the shift to bio-based resins to lock in eligibility for federally funded infrastructure projects, a move reinforced by the Inflation Reduction Act (IRA) incentives that reward low-carbon formulations. Automotive original equipment manufacturers (OEMs) are standardizing structural adhesives for aluminum closures and battery-pack enclosures to trim curb weight and extend driving range, thereby capturing Corporate Average Fuel Economy (CAFE) credits. In packaging, corrugated converters demand faster-curing, lower-volatile organic compound (VOC) chemistries that can sustain line speeds above 300 meters per minute, a prerequisite for meeting e-commerce fulfillment throughput. Simultaneously, furniture and electronics producers are migrating toward light-emitting diode-initiated ultraviolet-cure systems that slash energy consumption by 40% versus thermal ovens while eradicating thermal distortion in engineered-wood substrates.

Key Report Takeaways

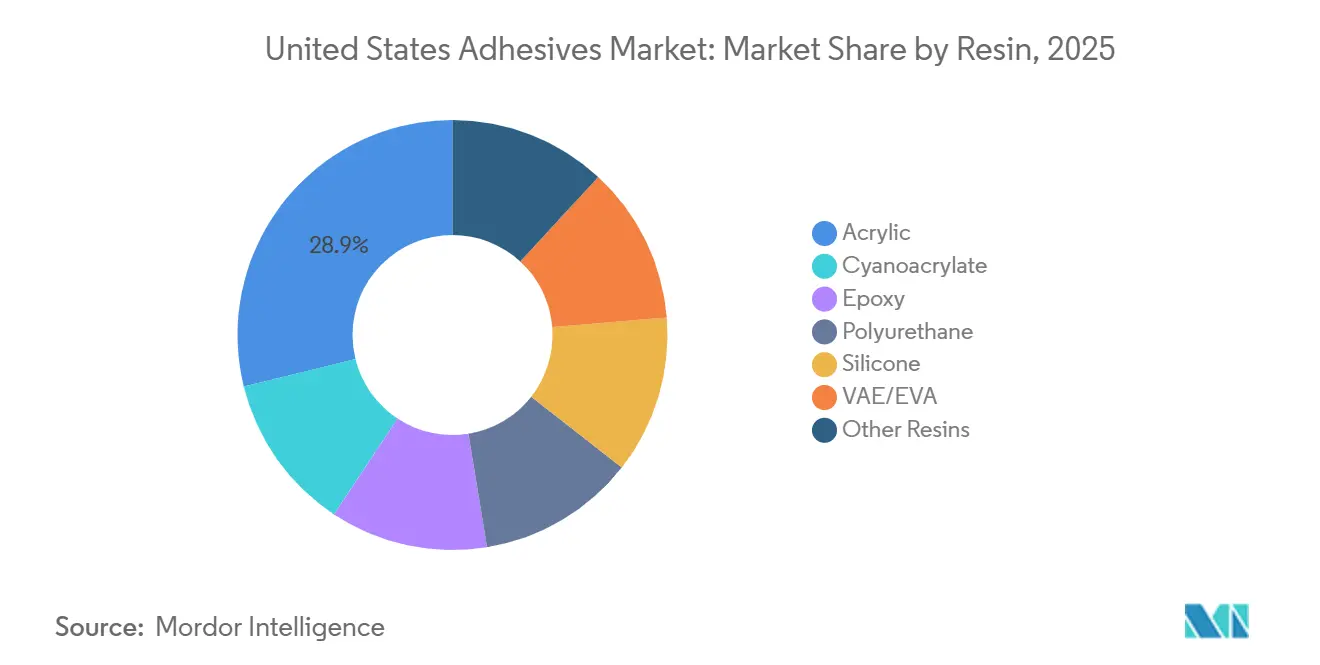

- By resin type, acrylic maintained the revenue lead with 28.85% of the United States adhesives market share in 2025, while silicone is projected to expand at a 6.45% CAGR between 2026 and 2031.

- By technology, water-borne systems held 38.50% share of the United States adhesives market size in 2025, whereas ultraviolet-cured variants are forecast to grow at a 6.98% CAGR between 2026 and 2031.

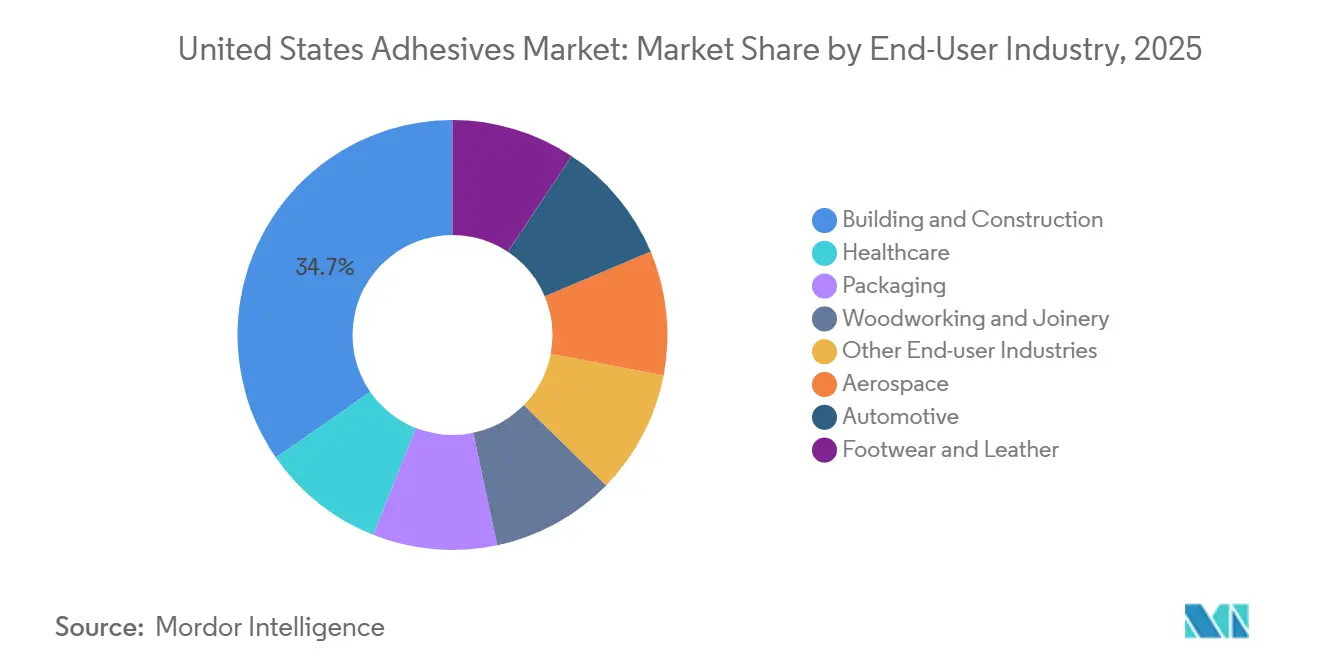

- By end-user industry, building and construction commanded 34.65% of 2025 volume, yet healthcare is set to record the fastest 6.74% CAGR across 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in lightweighting demand in automotive manufacturing | +1.20% | National, concentrated in Michigan, Ohio, and Tennessee automotive corridors | Medium term (2-4 years) |

| Continued growth in e-commerce is boosting packaging adhesives | +0.90% | National, with the highest intensity in logistics hubs (Texas, California, Pennsylvania) | Short term (≤ 2 years) |

| Rising U.S. residential construction and housing starts | +0.80% | National, led by Sun Belt markets (Texas, Florida, Arizona, North Carolina) | Medium term (2-4 years) |

| Adoption of hybrid bonding for mass-timber construction | +0.60% | National, early adoption in the Pacific Northwest and Northeast urban centers | Long term (≥ 4 years) |

| Federal "Buy Clean" incentives for low-VOC bio-based chemistries | +0.50% | National, prioritizing federal procurement and infrastructure projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Lightweighting Demand in Automotive Manufacturing

Automotive original equipment manufacturers (OEMs) now specify epoxy and polyurethane structural adhesives that can shave 10%-15% from body-in-white mass, translating directly into longer electric vehicle range and compliance with the latest Corporate Average Fuel Economy (CAFE) targets. General Motors’ Ultium platform deploys thermally conductive epoxy lines below 0.3 Watts per meter-Kelvin (W/(m·K)) to curb cell-to-cell heat propagation, while maintaining electrical isolation over 3 kilovolts. The lengthy 18-24 month qualification window for new chemistries shields incumbents but opens niches for silicone specialists able to pair dielectric strength with electromagnetically dissipative additives that protect 800-volt architectures. Regional Tier-1 suppliers in Michigan and Ohio have already booked multi-year contracts for gap-filler silicones rated to 200°C, signaling a sustained pull through 2029.

Continued Growth in E-Commerce Boosting Packaging Adhesives

With e-commerce accounting for a significant share of United States retail sales, corrugators demand hot-melt and water-borne adhesives that cure fast without sacrificing green strength at speeds topping 300 meters per minute. Amazon’s pledge to replace plastic air pillows with paper filler has driven uptake of starch- and vinyl-acetate-ethylene (VAE) emulsions compatible with mono-material recycling streams. These VAE systems command 20%-25% price premiums but ensure polyethylene reclaim purity[1]Amazon, “Amazon to Replace Plastic Air Pillows with Paper Filler in North America,” aboutamazon.com . Meanwhile, carton producers are thinning board calipers to 180 g/m², forcing rheology upgrades so adhesive lay-down remains consistent despite reduced substrate porosity. Logistics hubs in Texas and Pennsylvania report double-shift plant utilization to meet peak fulfillment seasons, underscoring the secular momentum behind packaging grades.

Rising U.S. Residential Construction and Housing Starts

In December 2025, housing starts reached an annualized rate indicative of strong demand for polyurethane adhesives used in subflooring and panel lamination. Builders across Florida, Texas, and Arizona are turning to hybrid-polymer bond-lines, designed to stay flexible against hurricane-force winds and seismic shifts. With the 2024 update to the International Residential Code now requiring adhesive-bonded subfloor assemblies in specific seismic zones, the potential market footprint has expanded. Engineered-wood beams treated with moisture-curing polyurethanes demonstrate significantly higher shear capacity compared to those using mechanical fasteners, paving the way for lighter joist designs and quicker installations.

Adoption of Hybrid Bonding for Mass-Timber Construction

Developers pursuing Leadership in Energy and Environmental Design (LEED) Platinum mid-rise towers in the Pacific Northwest are capitalizing on cross-laminated timber (CLT) panels bonded with formaldehyde-free polyurethane systems certified to ICC-ES AC478. Hybrid combinations of dowel connections and structural adhesive interfaces satisfy International Building Code (IBC) Chapter 23 fire and seismic criteria, delivering two-hour fire ratings without intumescent coatings. Supply, however, remains constrained: only 14 domestic Cross-Laminated Timber (CLT) mills operate, keeping capacity tight and premiums elevated. Training contractors to maintain substrate moisture below 12% before adhesive application remains a bottleneck, spurring suppliers to bundle technical services with product sales.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petro-feedstock price volatility | -0.70% | National, with acute exposure in Gulf Coast production clusters | Short term (≤ 2 years) |

| Stringent VOC emission limits on solvent-borne systems | -0.60% | National, most stringent in California, the Northeast Ozone Transport Commission (OTC) states | Medium term (2-4 years) |

| Skilled-labor shortage for precision adhesive application | -0.40% | National, concentrated in aerospace and automotive assembly regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Petro-Feedstock Price Volatility

Early 2026 propylene prices dipped from mid-2024 peaks but remain highly sensitive to Gulf Coast cracker outages and geopolitical events [2]Dow. "Dow Expands Low-VOC Adhesive Portfolio with New Acrylic Emulsions." Accessed March 23, 2026. . Contract structures seldom hedge quarterly swings, exposing converters to margin squeezes before downstream price adjustments can take effect. Although bio-attributed resins offer a diversification hedge, they import exposure to crop-price cycles and renewable-credit markets, offsetting some stability gains. Adhesive buyers, therefore, demand flexible-formulation clauses allowing filler substitutions, complicating inventory planning and formulation consistency.

Stringent VOC Emission Limits on Solvent-Borne Systems

Environmental Protection Agency risk evaluation of 1,3-butadiene and California Air Resources Board (CARB) rules cap volatile organic compound (VOC) content below 250 grams per liter (g/L) for contact adhesives, accelerating the pivot to water-borne and ultraviolet-cured chemistries. Firms must re-validate performance under American Society for Testing and Materials D3654 peel and American Society for Testing and Materials D905 shear benchmarks, a costly endeavor that drains Research and Development bandwidth. Furniture makers switching to water-borne lines report throughput dips of 5%-8% until process parameters are optimized, illustrating the operational drag associated with compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin: Silicone Gains on High-Temperature Demands

Acrylics retained 28.85% of 2025 revenue, but commoditization pressures margins, especially in pressure-sensitive tapes. Epoxies remain indispensable for aerospace primary structures, commanding premium prices for Tg values exceeding 180°C. Polyurethanes dominate flexible packaging and panel lamination, prized for impact resilience, whereas cyanoacrylates serve niche rapid-bonding roles in electronics and surgical closures. VAE/EVA copolymers supply cost-effective hot-melts in packaging, though limited heat resistance curtails automotive uptake. Specialty phenolic, polyimide, and anaerobic resins occupy small but lucrative segments demanding extreme chemical or thermal stability. Silicone grades are forecast to grow at a 6.45% CAGR from 2026 to 2031, on the back of high-temperature electric vehicle (EV) drivetrains and wearable-healthcare use cases. Battery-pack designers specify gap-filler silicones that withstand 150-200°C without embrittlement, delivering dielectric insulation above 3 kilovolts while dissipating heat. Medical device firms value silicone pressure-sensitives for 14-day glucose-monitor adhesion, ensuring International Organization for Standardization (ISO) 10993 biocompatibility.

By Technology: UV-Cured Systems Lead Innovation

The United States adhesives market share for water-borne systems stood at 38.50% in 2025, buoyed by volatile organic compound (VOC) regulations. Hot-melts deliver zero- volatile organic compound (VOC) compliance and rapid set, but face heat-resistance improvements to survive 80°C cabin temperatures. Reactive systems, epoxy, polyurethane, and acrylic, offer structural strength but incur longer cure cycles. Solvent-borne volumes continue a managed decline confined to specialty niches. UV-cured adhesives will accelerate at a 6.98% CAGR from 2026 to 2031 as furniture, electronics, and medical disposables embrace light-emitting diode curing. Cabinet makers report 30% cycle-time reductions and 40% energy savings after shifting from water-borne lines, a boon for just-in-time production. Smartphone assemblers adopt optically clear ultraviolet adhesives for bezel-less displays, leveraging instant cure to eliminate bottlenecks. Shadow-cure limitations persist, prompting dual-cure hybrids combining ultraviolet initiation with moisture or thermal cross-linking.

By End-User Industry: Healthcare Outpaces Traditional Sectors

Building and construction retained 34.65% of 2025 revenue, supported by polyurethane subfloor bonding and exterior insulation systems. Packaging enjoys strong volumes but faces margin pressure as converters request cost-downs to offset pulp inflation. Automotive adoption of multi-material structures elevates structural epoxy and polyurethane consumption, displacing spot welds. Woodworking hinges on California Air Resources Board (CARB) Phase 2-compliant Polyvinyl Acetate (PVA) and polyurethane glues, while aerospace and footwear remain specialized yet lucrative niches. Healthcare adhesives will rise at 6.74% CAGR from 2026 to 2031, the swiftest among end users. Food and Drug Administration (FDA) clearances for extended-wear transdermal patches and minimally invasive surgical adhesives propel volume gains. Wearable sensors demand skin-friendly silicone and acrylic pressure-sensitives that maintain adhesion under perspiration and variable humidity, validated through International Organization for Standardization (ISO) 10993-10 irritation testing.

Geography Analysis

Manufacturing corridors and population growth centers drive domestic demand. In the Midwest, automotive hubs in Michigan and Ohio anchor the uptake of silicone and structural epoxy for electric vehicle assemblies. Meanwhile, in the Sun Belt, states like Texas, Florida, and Arizona are witnessing a surge in construction-grade polyurethane volumes, fueled by booming housing starts and a climate that favors engineered wood. In the Pacific Northwest, cities like Seattle and Portland are at the forefront of mass-timber trials, leading to a localized uptick in ICC-certified polyurethane consumption. Additionally, logistics hubs such as Dallas-Fort Worth, Los Angeles-Inland Empire, and Pennsylvania’s Lehigh Valley are home to high-speed corrugated plants, which consume significant amounts of hot-melt and water-borne packaging adhesives.

States under the Northeast Ozone Transport Commission (OTC) and California are enforcing stringent caps on volatile organic compounds (VOCs). This push has accelerated the industry's shift towards water-borne and UV-cured systems. Producers with formulation labs in Delaware and New Jersey benefit from their closeness to regulatory agencies and rebate programs, which financially support solvent-free research and development. While Gulf Coast cities like Houston and Baton Rouge enjoy advantages as feedstock hubs for petrochemical derivatives, they grapple with supply disruptions caused by hurricanes, underscoring the need for robust business continuity planning.

Rural areas in the Carolinas and Tennessee, home to a dense furniture manufacturing base, heavily rely on polyvinyl acetate (PVA) wood glues and hot-melt edge-banders. Though the United States adhesives market size for this furniture cluster is modest in absolute terms, its strategic importance is undeniable. Early adopters of LED-UV technology in cabinetry often set specification standards that ripple upstream into national retail programs. This regional diversification provides a buffer against singular economic shocks for the United States adhesives market. However, the regulatory inconsistencies between states pose challenges for nationwide product rollouts.

Competitive Landscape

The United States Adhesives Market is moderately consolidated. Mid-tier specialists such as Jowat and Franklin International carve out defensible niches in woodworking and paper converting by offering rapid-customization services and localized technical training. Start-ups commercializing lignin-based tackifiers and bio-succinic-acid feedstocks attract venture funding owing to cradle-to-gate emissions savings past 30%, yet still navigate multi-year original equipment manufacturers (OEMs) qualification hurdles.

United States Adhesives Industry Leaders

-

3M

-

H.B. Fuller Company

-

Henkel AG & Co. KGaA

-

Sika AG

-

Arkema

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Henkel announced a USD 70 million Consumer Brands research and development Center in Trumbull, Connecticut, strengthening the United States adhesives market through innovation, collaboration, and advanced product development.

- March 2026: Forza Inc. expanded its HyPer Polymer formulations in the United States Adhesives Market, enhancing advanced polymer adhesive adoption and strengthening high-performance bonding technologies across industries.

United States Adhesives Market Report Scope

Adhesives, including glue and paste, bond two surfaces together, preventing their separation. Available in forms like liquid, paste, or tape, these substances are defined by their stickiness, allowing them to adhere to materials such as wood, metal, or skin.

The United States Adhesives Market is segmented by resin, technology, and end-user industry. By resin, the market is segmented into acrylic, cyanoacrylate, epoxy, polyurethane, silicone, VAE/EVA, and other resins. By technology, the market is segmented into hot-melt, reactive, solvent-borne, UV-Cured, and water-borne. By end-user industry, the market is segmented into aerospace, automotive, building and construction, footwear and leather, healthcare, packaging, woodworking and joinery, and other end-user industries. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Resin

| Acrylic |

| Cyanoacrylate |

| Epoxy |

| Polyurethane |

| Silicone |

| VAE/EVA |

| Other Resins |

By Technology

| Hot-Melt |

| Reactive |

| Solvent-borne |

| UV-Cured |

| Water-borne |

By End-User Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Footwear and Leather |

| Healthcare |

| Packaging |

| Woodworking and Joinery |

| Other End-user Industries |

| By Resin | Acrylic |

| Cyanoacrylate | |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| VAE/EVA | |

| Other Resins | |

| By Technology | Hot-Melt |

| Reactive | |

| Solvent-borne | |

| UV-Cured | |

| Water-borne | |

| By End-User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Footwear and Leather | |

| Healthcare | |

| Packaging | |

| Woodworking and Joinery | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the adhesives market.

- Product - All adhesive products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, and Silicone are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms