Flock Adhesives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

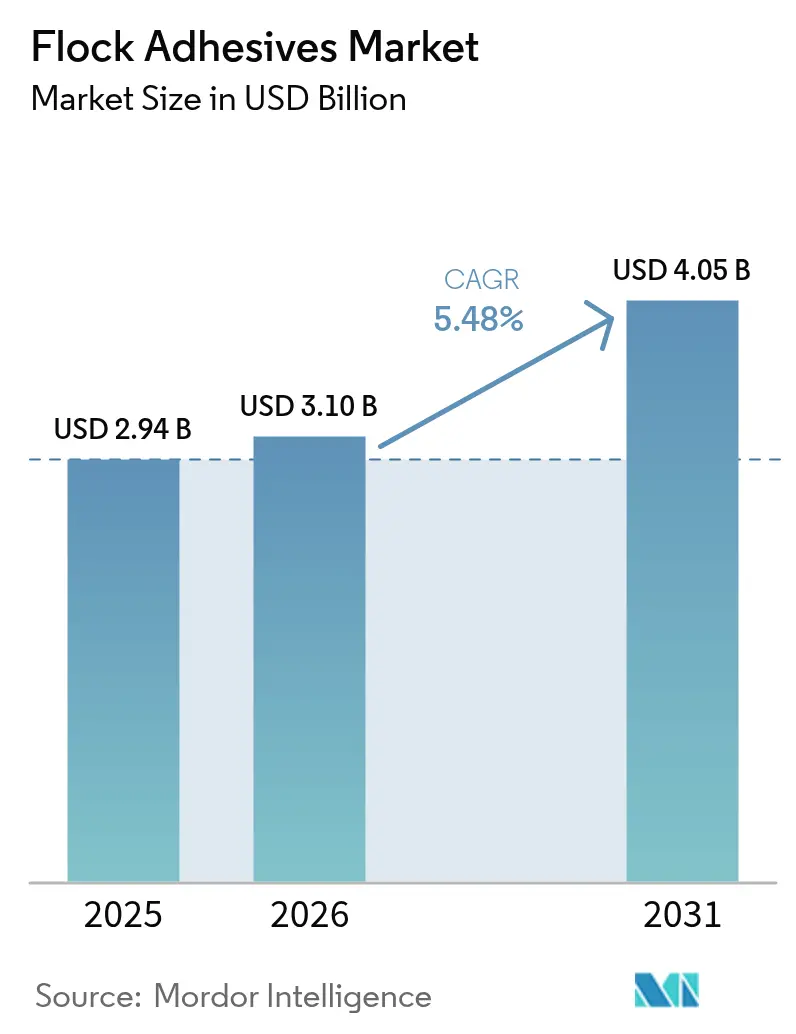

| Market Size (2026) | USD 3.1 Billion |

| Market Size (2031) | USD 4.05 Billion |

| Growth Rate (2026 - 2031) | 5.48% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flock Adhesives Market Analysis by Mordor Intelligence

The Flock Adhesives Market size was valued at USD 2.94 billion in 2025 and estimated to grow from USD 3.1 billion in 2026 to reach USD 4.05 billion by 2031, at a CAGR of 5.48% during the forecast period (2026-2031). Growth is anchored in automotive interior demand, accelerated by rising electric-vehicle (EV) production, and reinforced by premium packaging requirements that emphasize soft-touch aesthetics and thermal functionality. Regulatory shifts toward water-based and VOC-free chemistries are prompting rapid product reformulation, especially as the European Union restricts diisocyanates and China tightens interior-emission limits. Automotive applications command the largest slice of the flock adhesives market at 42.56% in 2024 and also expand the fastest at 6.42% CAGR, underscoring the segment’s dual role as volume base and innovation engine. Asia-Pacific retains geographic leadership with 51.84% share in 2024 and a 6.19% CAGR outlook through 2030, benefiting from concentrated automotive manufacturing footprints and expanding EV battery capacity. Meanwhile, polyurethane resin systems dominate with 38.19% share, yet “other” chemistries display the strongest 6.65% CAGR as formulators pivot toward acrylic, epoxy and non-isocyanate alternatives to stay ahead of incoming regulation.

Key Report Takeaways

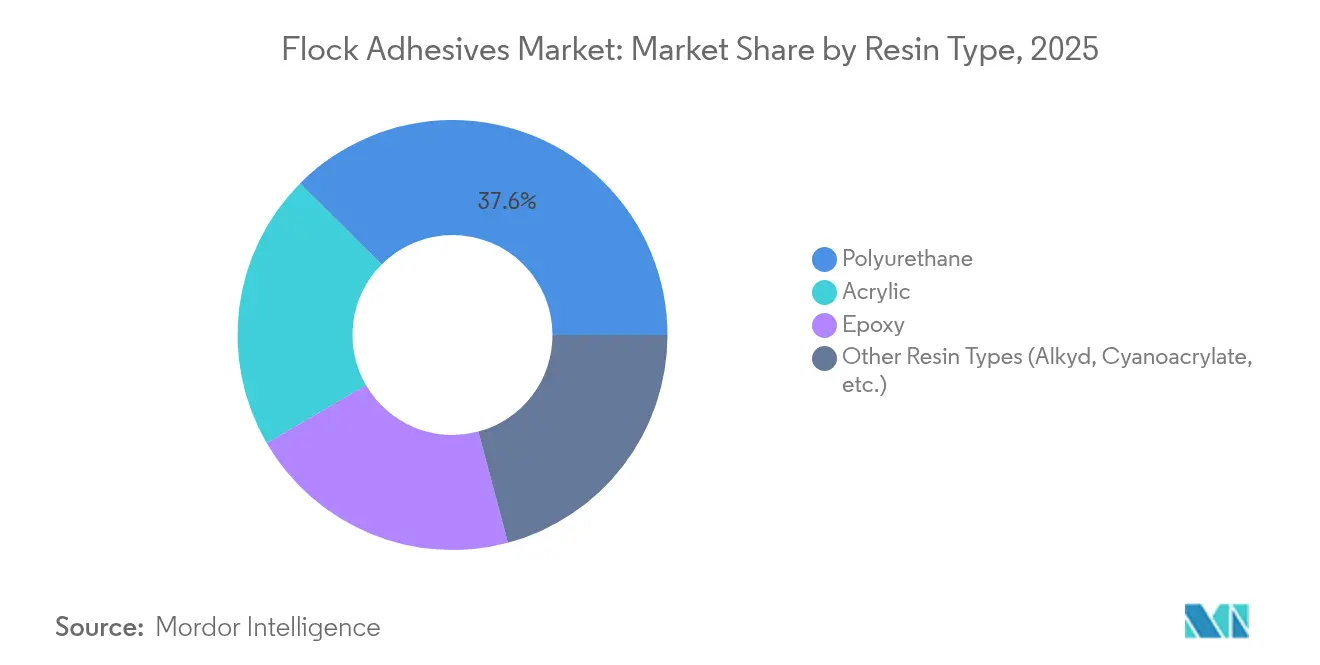

- By resin type, polyurethane led with 37.55% of flock adhesives market share in 2025, whereas other resin types are projected to post the highest 6.53% CAGR through 2031.

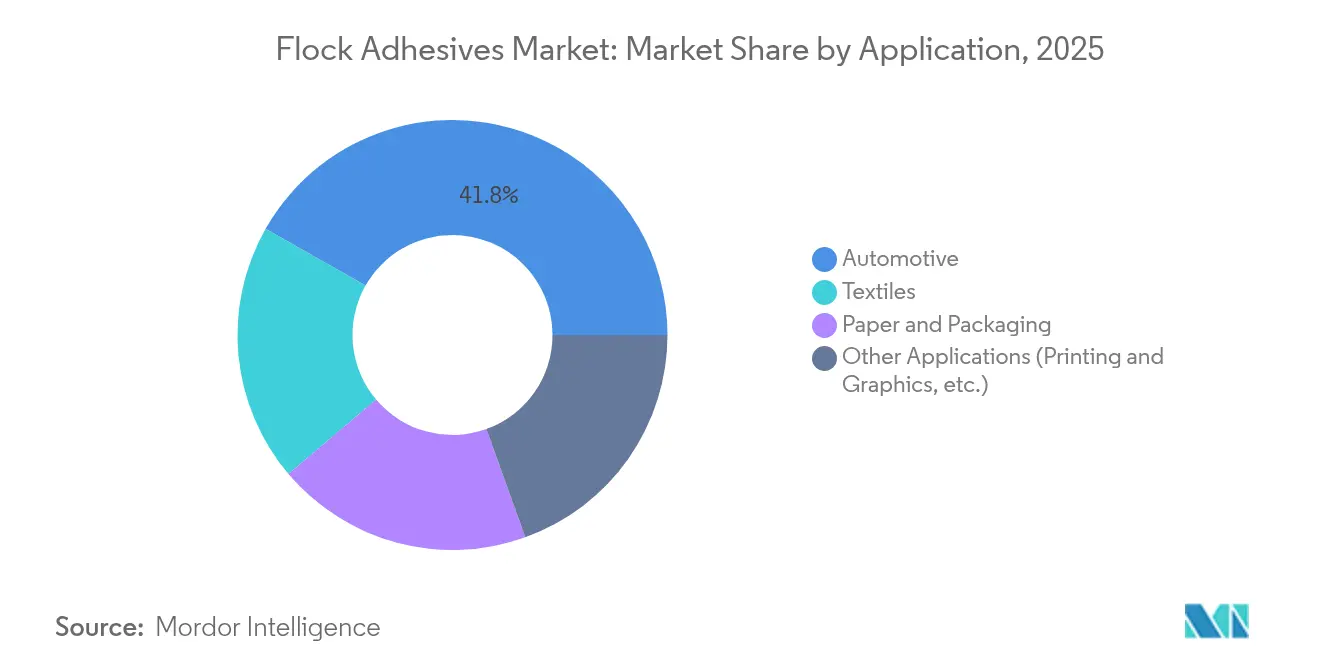

- By application, the automotive segment captured 41.78% share of the flock adhesives market size in 2025 and is projected to advance at a 6.18% CAGR between 2026-2031.

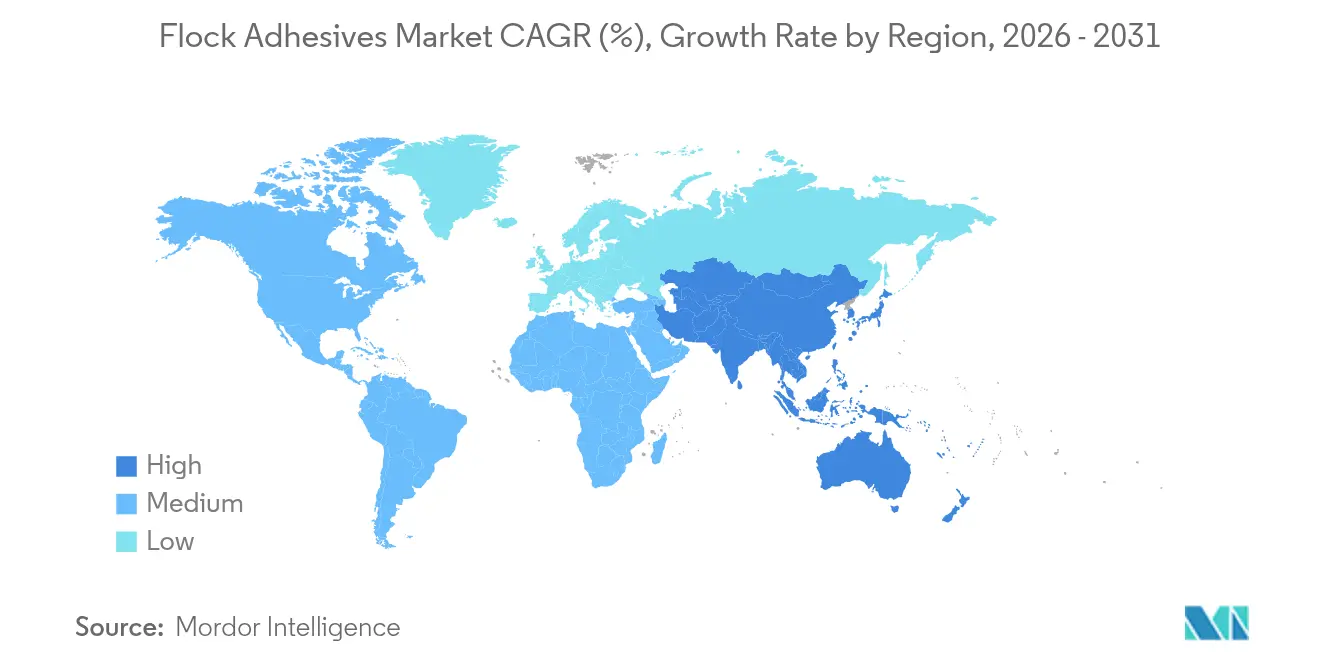

- By geography, Asia-Pacific accounted for 51.20% of the flock adhesives market share in 2025 while the same region is set to expand at a 6.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flock Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for coated fabrics and luxury finish products | +1.2% | Global, with premium segments in North America & Europe | Medium term (2-4 years) |

| Lightweight, low-carbon vehicle interior parts push adoption | +1.8% | APAC core, spill-over to North America & Europe | Long term (≥ 4 years) |

| Regulatory shift toward water-based / VOC-free chemistries | +1.1% | Global, led by EU & China regulations | Short term (≤ 2 years) |

| Flocked thermal-management liners in electric vehicles battery packs | +0.9% | APAC & North America EV manufacturing hubs | Medium term (2-4 years) |

| Premium unboxing aesthetics in consumer-electronics packaging | +0.4% | Global, concentrated in consumer electronics markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Coated Fabrics and Luxury Finish Products

Automotive and luxury-goods producers are stepping up use of flocked materials to signal elevated quality. Cabin parts such as dashboards, pillars and storage trays gain a plush feel that improves grip and cuts rattling noise. Premium packaging makers adopt the same technology so that jewelry boxes or smartphone cases feel exclusive from first touch. The tactile upgrade supports higher retail prices and strengthens brand differentiation. Together these factors translate into a wider, more stable demand base for flock adhesives[1]Henkel AG & Co. KGaA, “Soft-Touch Interior Trends,” henkel.com.

Lightweight, Low-Carbon Vehicle Interior Parts Push Adoption

Car makers are substituting heavy fasteners with adhesive-bonded composite panels to shave grams from every model. Flock adhesives secure thin plastics and fabric laminates while meeting crash, vibration and durability tests. Mass reductions directly extend EV driving range, a metric closely watched by consumers and regulators. Assembly lines also benefit because fewer clips and screws cut cycle times and simplify recycling. As electrification spreads, the weight-saving argument keeps flock solutions on engineering shortlists.

Regulatory Shift Toward Water-Based / VOC-Free Chemistries

The European Union now restricts diisocyanate levels and mandates extra worker training above 0.1% content, while China enforces lower interior-emission caps. These policies push formulators toward acrylic dispersions, non-isocyanate polyurethanes and other low-solvent systems. Brands that redesign early gain a compliance edge in global sourcing bids. End-users benefit from safer workplaces and greener product labels. The rule changes therefore act as a growth catalyst for next-generation flock adhesives.

Flocked Thermal-Management Liners in Electric Vehicles Battery Packs

Battery modules run hot and require barriers that spread heat yet block electrical shorts. Short fibers anchored by specialty adhesives create an insulating but conductive layer on cell housings. The material must also survive fire-safety tests and long vibration cycles. Because performance stakes are high, automakers pay premium prices for proven formulations. Each new EV launch, therefore, lifts the value pool for flock suppliers focused on thermal applications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile isocyanate and acrylate feedstock prices | -0.8% | Global, with acute impact in regions dependent on imports | Short term (≤ 2 years) |

| Tightening solvent-emission regulations | -0.6% | EU & North America regulatory jurisdictions | Medium term (2-4 years) |

| Competition from laser-texturing and alternative finishes | -0.4% | Premium automotive segments globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Isocyanate and Acrylate Feedstock Prices

Adhesive makers rely on petrochemical derivatives whose costs whipsaw with oil and supply-chain shocks. Recent methacrylic-acid oversupply drove a 12% price drop, only for resin producers to impose sharp increases weeks later. Long fixed-price contracts with automotive OEMs limit the ability to pass surcharges through. Smaller formulators are especially exposed because they lack hedging scale and diversified portfolios. Margin uncertainty discourages bold capacity investments during turbulent periods.

Tightening Solvent-Emission Regulations

The EU will cap formaldehyde at 0.062 mg/m³ inside vehicles from August 2026, forcing extensive lab tests and documentation. Reformulating away from high-VOC solvents can alter adhesion strength, aging resistance and cure speed. Additional R&D outlays hit profitability even before new grades reach the market. Delays in regulatory approval may create supply gaps that end-users must bridge with substitutes. Consequently, the rulebook imposes both direct expense and sales-cycle friction on the industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Polyurethane Dominance Faces Regulatory Pressure

Polyurethane captured 37.55% of flock adhesives market share in 2025, buoyed by broad compatibility with automotive substrates and strong thermal resilience. Yet regulatory scrutiny of isocyanates is shifting demand, evidenced by the 6.53% CAGR projected for “other” resin types. The flock adhesives market size for non-isocyanate chemistries is expected to outpace incumbents as acrylic and epoxy alternatives gain traction, driven by inherently lower VOCs and simplified handling. Henkel’s bio-based polyurethane containing 71% renewable content demonstrates a 60% CO₂ reduction versus standard formulas, signaling how sustainability narratives translate into purchasing criteria.

Regulators require worker training and stricter labelling for diisocyanate products, prompting OEMs to request compliant substitutes. Formulators respond by scaling acrylic dispersions and non-isocyanate polyurethane (NIPU) chemistries that meet adhesion, flexibility and heat-cycling needs without surpassing 0.1% diisocyanate thresholds. Suppliers able to balance compliance, performance and cost will command premium margins as legacy options face phased restriction.

By Application: Automotive Sector Drives Both Scale and Innovation

Automotive interiors dominated 2025 with 41.78% flock adhesives market share and will expand at 6.18% CAGR, propelled by demand for tactile dashboards, door trims and battery-pack liners. The flock adhesives market size allocated to automotive electronics alone rises as wire harnesses, seat sensors and infotainment modules require soft, abrasion-resistant housing. EV development accelerates this trend, because flocked interfaces dissipate heat and reduce noise within compact battery compartments.

Beyond vehicles, textiles and luxury packaging remain important but slower-growing outlets. Technical fabrics use flock to improve grip and insulation in sportswear and medical garments, while high-end consumer-electronics brands rely on flocked inserts for premium unboxing experiences. Printing and graphics gradually lose share to digital methods that need fewer specialty coatings, yet still absorb niche demand for tactile marketing materials. Automotive’s innovation pull therefore reverberates across all segments, as FMVSS 302 burn-rate limits enforce stringent flame-spread criteria on every flock adhesive entering the vehicle cabin.

Geography Analysis

Asia-Pacific held 51.20% flock adhesives market share in 2025 and is set to grow at 6.05% CAGR through 2031. China anchors regional demand as domestic brands and export-oriented assemblers adopt flocked interiors to elevate perceived quality and meet low-VOC mandates. Sika’s new Liaoning and Singapore plants illustrate local capacity investments aimed at shortening lead times and tailoring chemistries for emerging battery-thermal needs. Japan and South Korea complement volume with materials science leadership, scaling epoxy-based and low-formal-emission systems for electronics as well as autos.

North America follows with mature but technologically demanding consumption. OEMs enforce strict sourcing criteria on sustainability and supply-chain transparency, incentivizing rapid adoption of water dispersions and bio-based content. Public infrastructure and military procurement channels support niche flocked applications in rail interiors and aerospace cabin fittings, keeping baseline demand intact despite plateaued vehicle output.

Europe blends tight regulation with innovation leadership. The continent’s Circular Economy Action Plan requires removable batteries in devices by 2027, spawning new debondable-adhesive niches where flock must cleanly separate at end-of-life. Companies like Power Adhesives recently introduced certified biodegradable hot-melt systems containing 44% bio-based content, a template likely to spread into flock formulations.

South America, the Middle East and Africa collectively represent modest volumes but rising importance as supply chains diversify. Brazil expands automotive assembly capacity that relies on locally sourced flocked trims, while petrochemical integration in the Gulf provides competitive resin feedstock. African markets remain early-stage yet draw investment from consumer-electronics packagers seeking proximity to high-growth urban centers.

Competitive Landscape

The flock adhesives industry is moderately fragmented. 3M, Henkel and Sika constitute the global tier, differentiated by broad portfolios, multi-region production and heavy R&D spend. DELO commits 15% of annual revenue to research, far exceeding industry norms, which supports novel chemistries for battery thermal applications. Strategy centers on value, not price cutting, because flocking often appears in safety-critical or premium tactile roles where performance premiums are acceptable.

Technology partnerships accelerate sustainability pivots. Henkel collaborates with Celanese on CO₂-captured feedstocks, while Sika engineers dispersions for ultra-low-VOC dashboards. Regional specialists such as SwissFlock AG and Nyatex command niche shares by offering custom rheology and fiber-anchor solutions to mid-tier OEMs that global giants overlook.

Threats arise from laser-texturing, plasma coating and micro-molding processes that minimize materials and streamline recycling. KEYENCE’s laser structuring can etch tactile micro-patterns directly onto substrates, eliminating adhesive layers and fibers while reducing energy usage. Incumbents counter with value propositions around superior soft-touch, grip and acoustic dampening that purely textured plastics still struggle to match. Feedstock volatility complicates margin management, pressing producers to hedge raw materials and explore bio-based or waste-stream feedstocks that decouple pricing from petrochemicals.

Flock Adhesives Industry Leaders

H.B. Fuller Company

Henkel AG & Co. KGaA

Sika AG

Arkema

Dow

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Sika has opened a new technology center and manufacturing plant in Pune, Maharashtra, India. This modern facility is designed to produce high-quality adhesives and sealants, including flock adhesives. With its R&D labs and production units, the plant is set to meet the growing needs of the Indian market.

- July 2024: Henkel Adhesives Technologies India Private Limited (Henkel India) announced the completion of Phase III of its manufacturing facility in Kurkumbh, near Pune, Maharashtra. The Kurkumbh site is focused on supporting the increasing demand from Indian industries by providing high-performance adhesive solutions, including flock adhesives.

Global Flock Adhesives Market Report Scope

Flock adhesives are friction-resistant and durable and offer various properties, including easy washable, storable, and health & cold-resistant. The flock adhesives are generally applied to glass, textiles, paper, metal, plastics, and paper.

The flock adhesives market is segmented by resin type, application, and geography. Based on resin type, the market is segmented into acrylic, polyurethane, epoxy, and other resin types (alkyd, Cyanoacrylate, etc.). Based on application, the market is segmented into automotive, textiles, paper and packaging, and other applications (printing, footwear, etc.).

The report also covers the market size and forecasts for extrusion coatings in 15 countries across major regions. Each segment's market sizing and forecasts are based on value (USD).

| Acrylic |

| Polyurethane |

| Epoxy |

| Other Resin Types (Alkyd, Cyanoacrylate, etc.) |

| Automotive |

| Textiles |

| Paper and Packaging |

| Other Applications (Printing and Graphics, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Resin Type | Acrylic | |

| Polyurethane | ||

| Epoxy | ||

| Other Resin Types (Alkyd, Cyanoacrylate, etc.) | ||

| By Application | Automotive | |

| Textiles | ||

| Paper and Packaging | ||

| Other Applications (Printing and Graphics, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the flock adhesives market?

The flock adhesives market size stands at USD 3.1 billion in 2026.

How fast is the flock adhesives market expected to grow?

The market is projected to expand at a 5.48% CAGR between 2026 and 2031.

Which application segment leads the flock adhesives market?

Automotive interiors held 41.78% share in 2025 and will remain the largest and fastest‐growing segment through 2031.

Why are water-based flock adhesives gaining traction?

EU and Chinese regulations restricting VOCs and diisocyanates are prompting manufacturers to adopt water-based and solvent-free chemistries.

Page last updated on: