Chemicals & Materials

7th MayStrategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

The Plastic Adhesives Market Report is Segmented by Resin Type (Epoxy, Cyanoacrylate, Urethane, Silicones, Other Resin Types), Technology (Solvent-Based, Water-Based), End-User Industry (Automotive, Building and Construction, Electrical and Electronics, Medical, Packaging, Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

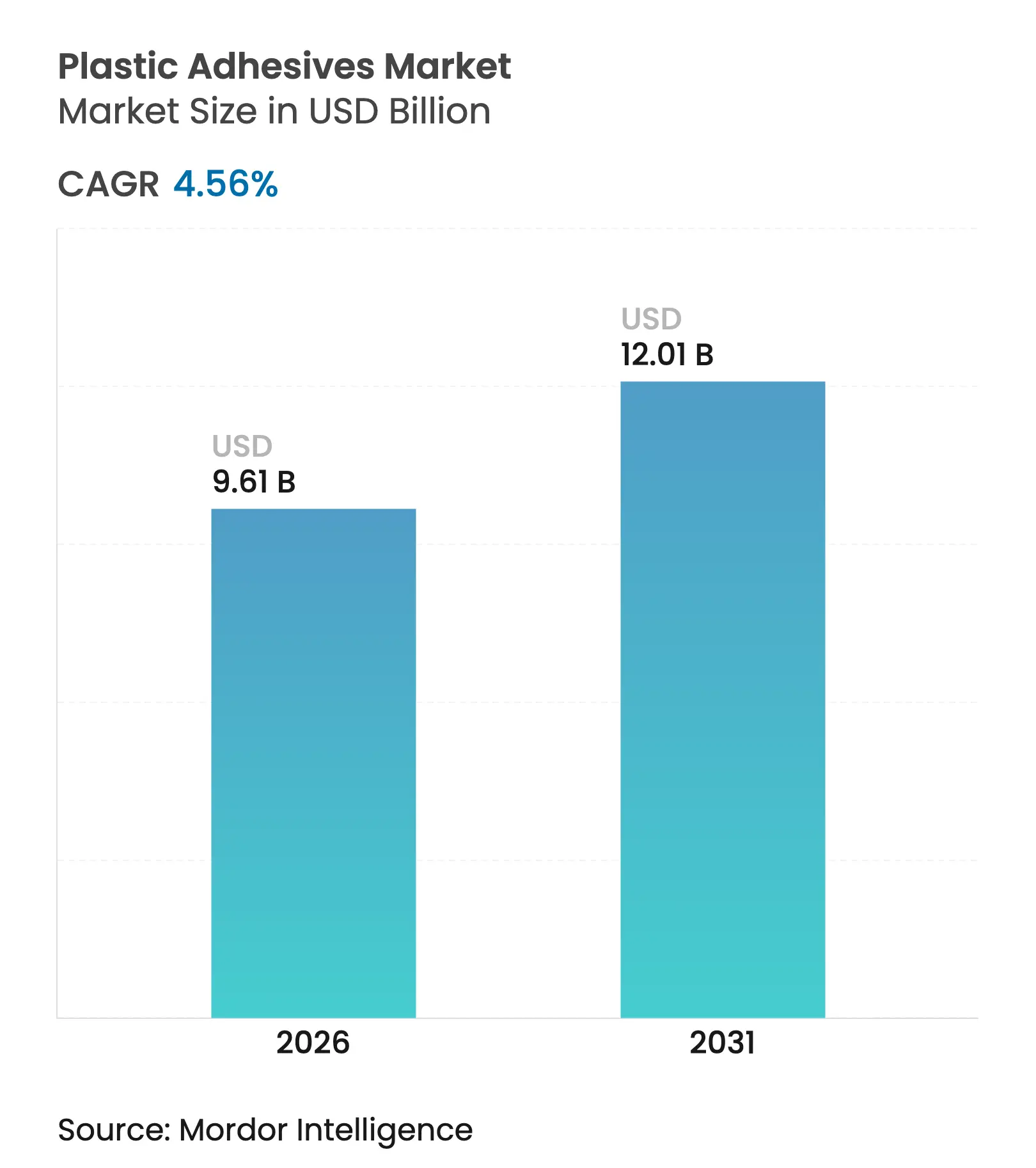

| Market Size (2026) | USD 9.61 Billion |

| Market Size (2031) | USD 12.01 Billion |

| Growth Rate (2026 - 2031) | 4.56 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Plastic Adhesives Market size was valued at USD 9.19 billion in 2025 and estimated to grow from USD 9.61 billion in 2026 to reach USD 12.01 billion by 2031, at a CAGR of 4.56% during the forecast period (2026-2031). The plastic adhesives market is transitioning from general-purpose bonding agents toward specialized chemistries that address electric-vehicle battery packs, medical wearables, and next-generation construction panels. Rising demand for lightweight vehicles, the shift to bio-based polyurethane films in healthcare, and stricter VOC legislation are widening application scopes across automotive, medical, and building sectors. Producers are releasing water-based and bio-derived grades that comply with evolving emission ceilings in China, the European Union, and the United States, enabling the plastic adhesives market to capture opportunities created by sustainability mandates. Competitive dynamics remain fluid as manufacturers adopt targeted M&A and joint-development agreements to close technology gaps, balance feedstock cost risks, and reach new geographic pockets.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Lightweight-vehicle push in automotive industry

Lightweight-vehicle push in automotive industry

| +1.2% | Global, with concentration in North America, Europe, and China | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Global, with concentration in North America, Europe, and

China

|

Impact Timeline

:

Medium term (2-4 years)

|

Construction shift to high-performance plastics

Construction shift to high-performance plastics

| +0.8% | Global, with early adoption in developed markets | Long term (≥ 4 years) | |||

Increasing demand from packaging and e-commerce industry

Increasing demand from packaging and e-commerce industry

| +0.9% | Global, with APAC leading growth | Short term (≤ 2 years) | |||

Bio-based polyurethane films for medical wearables

Bio-based polyurethane films for medical wearables

| +0.4% | North America and Europe, expanding to APAC | Medium term (2-4 years) | |||

Thermal-management adhesives for modular electric vehicle

battery packs

Thermal-management adhesives for modular electric vehicle

battery packs

| +0.7% | Global, with early adoption in China and Europe | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Lightweight-vehicle push in automotive industry

Automakers are replacing mechanical fasteners with structural adhesives to eliminate excessive weight and strengthen mixed-material designs. A typical 2025 electric SUV now integrates more than 400 linear feet of adhesive compared with fewer than 30 feet two decades ago, illustrating the structural role adhesives play in joining aluminum, carbon fiber, and engineering plastics[1]3M, “Structural Bonding Solutions for Multi-Material Vehicles,” 3m.com. Impact-toughened elastomer–epoxy hybrids developed at Nagoya University deliver 22-times higher impact strength than legacy epoxies, which allows thinner panels and energy-absorbing crash structures while maintaining crashworthiness[2]Nagoya University, “Impact-Resistant Elastomer-Modified Epoxy Adhesives,” nagoya-u.ac.jp. With most OEMs committing to lighter bodies for range extension, the plastic adhesives market expects automotive consumption to climb at double-digit annual rates through 2030.

Construction shift to high-performance plastics

Facade and glazing systems are moving toward lightweight composite panels that demand long-life, high-modulus bonding agents. Sika’s protective glazing adhesive family can absorb seismic loads yet retain rigidity for hurricane-rated curtain walls. High-rise retrofits in developed economies and green-field megaprojects in Asia require plastic adhesives that balance fire resistance, UV durability, and fast installation. Fast-cure PVC TrimWelder products reach 80% handling strength in 30 minutes, enabling contractors to accelerate project cycles without sacrificing code compliance.

Increasing demand from packaging and e-commerce industry

E-commerce shipping windows shortened to 24–48 hours in many cities, exposing parcels to more sorting hubs and vibration. Brand owners therefore source recyclable water-based tear tapes and barrier coatings that withstand multi-modal transport yet delaminate cleanly in fiber recovery streams, supporting Extended Producer Responsibility rules in the EU and several US states. APAC fulfillment centers propel incremental adhesive volumes as regional online spending expands, reinforcing the plastic adhesives market trajectory in packaging.

Bio-based polyurethane films for medical wearables

Wearable trackers require adhesives that remain gentle on skin during week-long monitoring. Formulators now employ bio-engineered mussel proteins that switch from strong underwater adhesion to easy peel-off when exposed to alkaline saline, reducing irritation for elderly patients. University of California researchers synthesized aromatic diisocyanates from D-galactose, eliminating toxic phosgene and achieving 100% bio-based polyurethane chains. These breakthroughs widen the plastic adhesives market in healthcare.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Petro-feedstock price volatility

Petro-feedstock price volatility

| -0.7% | Global, with higher impact in import-dependent regions | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-0.7%

|

Geographic Relevance

:

Global, with higher impact in import-dependent regions

|

Impact Timeline

:

Short term (≤ 2 years)

|

Tightening global VOC and hazard regulations

Tightening global VOC and hazard regulations

| -0.5% | Global, with stricter enforcement in developed markets | Medium term (2-4 years) | |||

Fire-safety code upgrades for façade panels

Fire-safety code upgrades for façade panels

| -0.3% | Primarily Europe and North America, expanding globally | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Petro-feedstock price volatility

Epoxy and polyurethane base-resin costs fluctuate with crude oil and propylene trends. German liquid epoxy prices rose 1.73% in January 2025 amid thin inventories, while Asian contracts slipped 1.4% later that month as sellers cleared surplus ahead of the Spring Festival. Polyethylene spikes of 5 ¢/lb in the United States further lifted packaging-grade adhesive inputs. Covestro signed a certified mass-balance supply agreement with H.B. Fuller to mitigate fossil feedstock swings through ISCC-PLUS-accredited bio-naphtha streams.

Tightening global VOC and hazard regulations

The European Union now restricts industrial diisocyanate use above 0.1% without licensed worker training, accelerating the switch to water-based polyurethane dispersions. Canada enforced category-specific VOC ceilings across 130 consumer-product classes in January 2024, covering contact adhesives and sealants. California will list vinyl acetate as a Prop 65 carcinogen by December 2025, compelling manufacturers to evaluate warnings or reformulate. Compliance costs add headwinds for the plastic adhesives market, yet they also trigger innovation in safer chemistries.

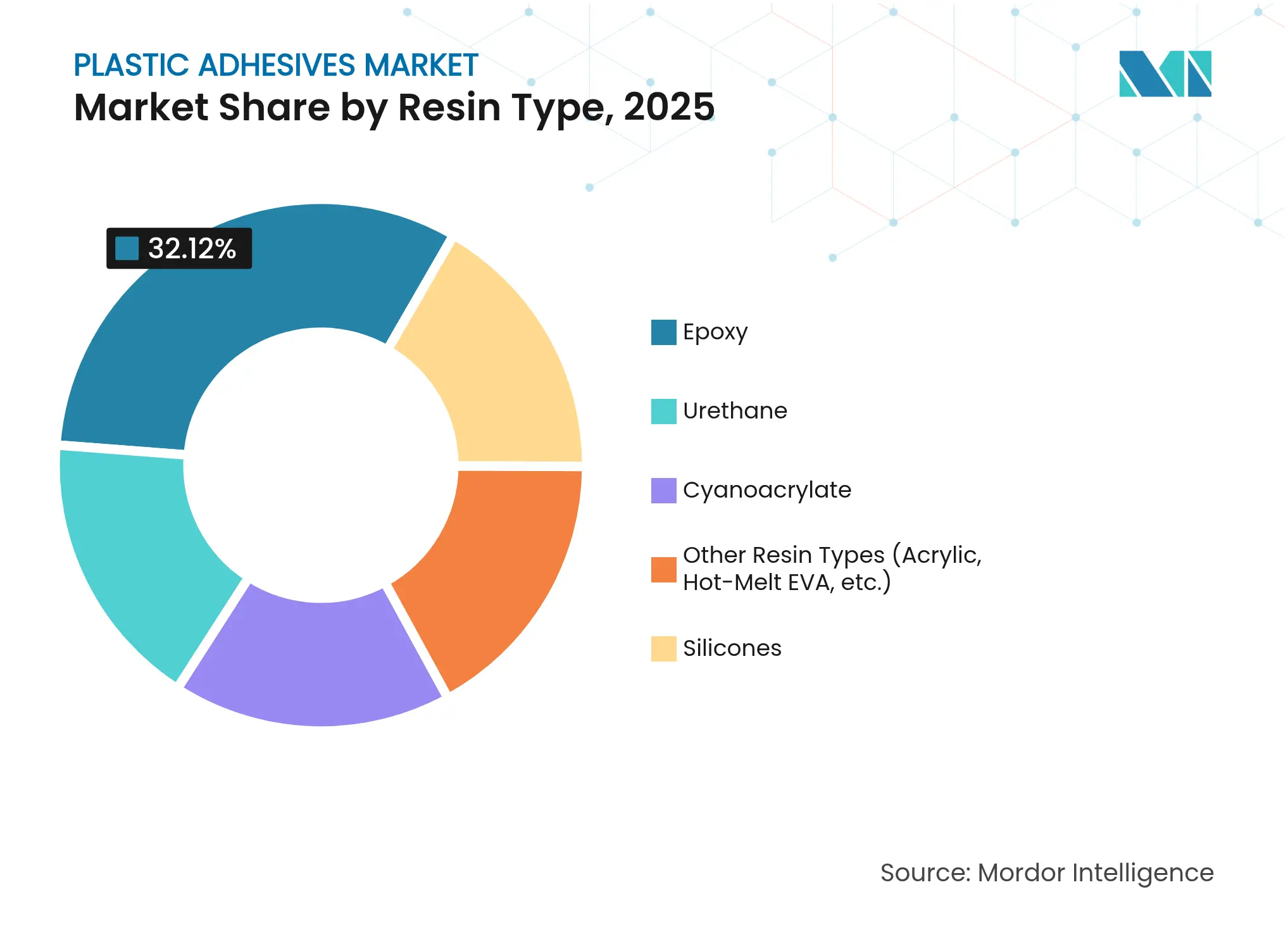

By Resin Type: Epoxy dominance faces specialty growth

Epoxy grades accounted for 32.12% of the plastic adhesives market size in 2025, underpinning structural joints in automotive body-in-white assemblies and steel-reinforced concrete panels. The high glass-transition temperature and chemical resistance keep epoxies relevant where shear loads and temperature spikes converge. Specialty cyanoacrylates, acrylics, and hybrid urethanes, however, exhibit the fastest 5.03% CAGR, as OEMs pursue rapid bonding in miniature electronics and need cold-cure alternatives for heat-sensitive substrates. The plastic adhesives market therefore balances epoxy’s entrenched share with emergent niche chemistries that emphasize speed and flexibility. Cyanoacrylate packages such as H.B. Fuller’s Cyberbond line allow viscosity tailoring for medical device micro-dosing while meeting ISO 10993 cytotoxicity requirements. Non-isocyanate polyurethanes made from bio-derived cyclic carbonates are scaling pilot lines, signalling a broader pivot toward sustainable resins inside the plastic adhesives market.

Manufacturers layer R&D to optimise adhesion promoters that interface with low-surface-energy polyolefins, aiming to unlock higher peel strengths without primers. Silicone-epoxy hybrids maintain hermetic seals in high-temperature electronics modules, giving formulators another route to differentiate. As environmental bans curb bisphenol-A derivatives, epoxy suppliers accelerate the launch of bis-F and novolac alternatives, guarding their sizeable plastic adhesives market share while aligning with upcoming endocrine-disruptor reviews in the EU.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Water-based solutions lead environmental transition

Water-based chemistries commanded 56.15% of the plastic adhesives market share in 2025 and are forecast to widen the gap with a 5.32% CAGR. Continuous polymer-dispersion advances now deliver bond strengths equal to solvent systems at lower coat weights, which is critical for label, paperboard, and hygiene applications. Henkel launched multiple compostable hot-melt dispersion grades compatible with corrugated recycling streams, reflecting the plastic adhesives market trend toward circular-economy materials. Solvent-based systems remain indispensable in high-gloss automotive interiors and high-frequency electronics where immediate green strength is non-negotiable, yet their share erodes each year as environmental taxes expand.

Emerging UV-curable waterborne platforms shorten line-tack times from minutes to seconds, enabling converters to reduce oven residence and energy draw. For flexible-packaging laminates, Dow and Kraton co-developed a bio-based acrylic dispersion that cuts carbon footprints 25% while passing food-contact norms. As brands publish scope 3 emission targets, purchasers give preference to water-based grades with ready life-cycle assessments, steering volume toward the greener quadrant of the plastic adhesives market.

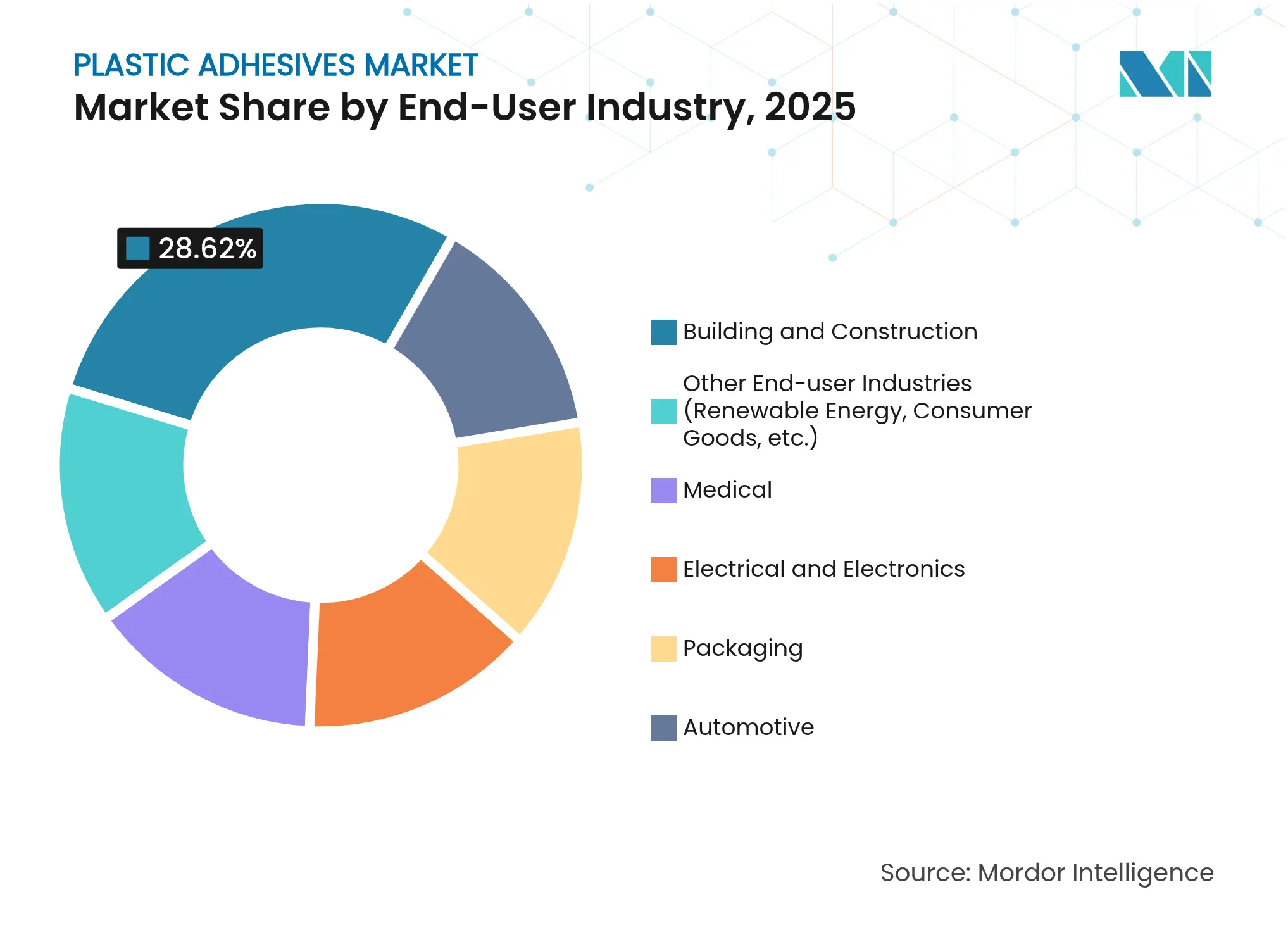

By End-User Industry: Construction leadership meets medical innovation

Building and construction captured 28.62% of the plastic adhesives market size in 2025, buoyed by urban renovation across North America and ambitious transit corridors in Asia. High-modulus structural silicones, fire-retardant polyurethanes, and moisture-cure polyether systems collectively anchor curtain walls, roofing membranes, and composite decking installations. Infrastructure projects such as metro-rail extensions and data-center campuses specify low-VOC, non-shrink bonding agents, reinforcing construction’s anchor role inside the plastic adhesives market.

The medical segment is set to expand at 5.55% CAGR through 2031, reflecting growth in wearable biosensors, transdermal patches, and rapid-cure wound closure films. Acquisition activity underscores the pivot: H.B. Fuller purchased GEM S.r.l. to gain cyanoacrylate tissue-adhesive technology that complements its hydrocolloid ostomy portfolio. As hospital procurement teams prioritise skin-safe, solvent-free options, suppliers with ISO 13485 facilities and proven biological-evaluation dossiers secure advance contracts, helping the plastic adhesives market diversify beyond traditional industrial channels.

Note: Segment shares of all individual segments available upon report purchase

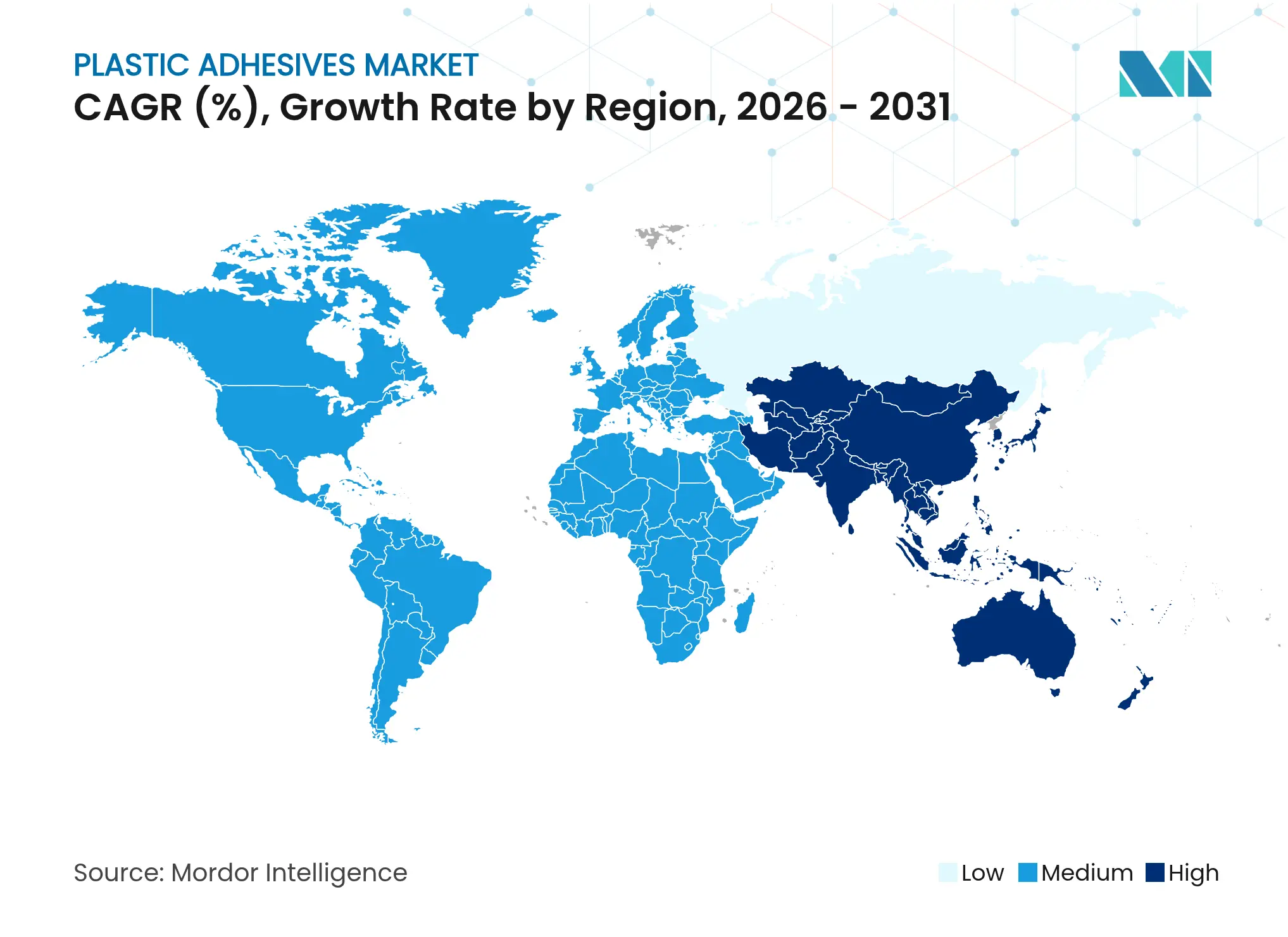

Asia-Pacific remains the principal manufacturing hub for engineering plastics, electronics, and footwear, positioning the region as the largest revenue contributor to the plastic adhesives market. China’s EV output, India’s highway and housing programs, and ASEAN’s packaging plants collectively amplify consumption. Government initiatives such as India’s Smart City Mission continue to stimulate public-works spending that relies on polymer-bonded panels and pipes.

North America, while mature, registers steady gains through stringent fuel-economy and building-energy codes that promote lightweight composites and air-tight building envelopes. The United States Environmental Protection Agency’s push toward low-GWP construction materials accelerates demand for low-smog adhesives in roofing and insulation boards. The plastic adhesives market also benefits from the United States-Mexico-Canada Agreement, which incentivises regional sourcing of automotive adhesives to qualify for tariff exemptions.

Europe leverages its Green Deal framework to catalyse recyclable adhesive innovation. Producers adapt formulas to disassemble end-of-life consumer goods and enable closed-loop plastic flows. Stricter EN 16603-20-01 outgassing criteria in aerospace applications pressurise suppliers to certify space-grade adhesives, opening a niche yet valuable tier within the plastic adhesives market.

The Middle East and Africa host expansion projects in desalination, solar infrastructure, and high-rise hospitality. Premium hotel builds specify silicone weather-seals rated for desert temperatures, supporting incremental growth. Latin America’s construction rebound and on-shore electronics assembly in Mexico and Brazil add diverse demand layers, albeit from a smaller base than the three dominant regions.

Market Concentration

The plastic adhesives market exhibits moderate fragmentation, with global leaders sharing space with regional specialists. Henkel’s Adhesive Technologies division generated EUR 10.97 billion sales in 2024 and posted a 16.6% adjusted EBIT margin by focusing on automotive electronics thermal-management tapes and medical device potting compounds. Saint-Gobain completed a USD 1.025 billion acquisition of FOSROC to reinforce its construction chemicals vertical, expanding epoxy-anchoring and waterproofing lines that intertwine with facade adhesive systems.

Dow divested its flexible-packaging laminating-adhesives operation to Arkema for USD 150 million, redeploying capital to high-value silicone thermally conductive pastes critical for EV modules. DELO Industrial Adhesives invests 15% of revenue in R&D—more than double the sector norm—and reported 12% sales growth in 2023 as its low-temperature curing epoxies gained design-wins in medical catheter assemblies. Kraton, and Eastman co-developed low-VOC tackifiers from pine-based feedstocks, illustrating cross-value-chain collaborations that characterize competition in the plastic adhesives market.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities and Future Outlook

The plastic adhesives market report includes:

Strategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

Unlocking Saudi Arabia’s Regional Tourism Growth Potential

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.