Chemicals & Materials

7th MayStrategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

The Metal Bonding Adhesives Market Report is Segmented by Resin Type (Acrylic, Epoxy, Polyurethane, Silicone, and Other Resin Types), Application (Automotive and Transportation, Aerospace and Defense, Electrical and Electronics, Industrial Assembly, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East & Africa). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

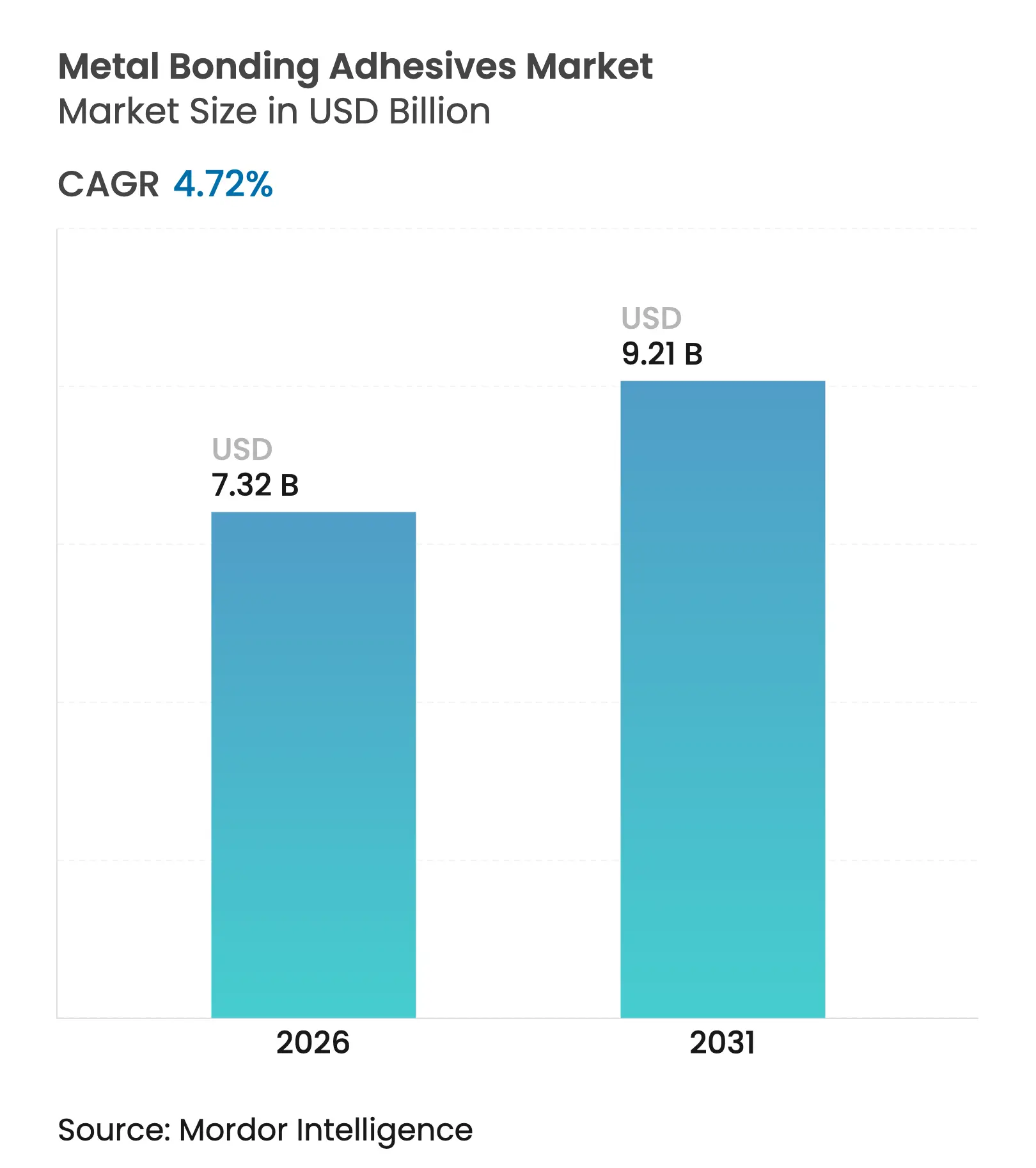

| Market Size (2026) | USD 7.32 Billion |

| Market Size (2031) | USD 9.21 Billion |

| Growth Rate (2026 - 2031) | 4.72 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Metal Bonding Adhesives Market size was valued at USD 6.99 billion in 2025 and estimated to grow from USD 7.32 billion in 2026 to reach USD 9.21 billion by 2031, at a CAGR of 4.72% during the forecast period (2026-2031). The shift from mechanical fastening to high-performance bonding solutions drives adoption across automotive, aerospace, electronics, and infrastructure projects. Weight-reduction programs in transport, rising composite–metal hybrid structures, and a broad push for sustainability underpin demand. Manufacturers that offer low-VOC (Volatile Organic Compound), bio-based, or recyclable chemistries gain an edge as global emission rules tighten. Competitive intensity remains moderate because leading suppliers control critical research and development (R&D) pipelines and global service networks, yet niche innovators are carving space in thermal-management, conductive, and debond-on-demand technologies to meet next-generation application needs.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Lightweighting Push in Automotive and Rail Lightweighting Push in Automotive and Rail | +1.2% | Global, APAC & Europe | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Global, APAC & Europe

|

Impact Timeline

:

Medium term (2-4 years)

|

Growing Adoption in Aerospace Composite-metal Joints Growing Adoption in Aerospace Composite-metal Joints | +0.8% | North America & Europe | Long term (≥ 4 years) | |||

Infrastructure Refurbishments using Adhesive-bonded Steel Infrastructure Refurbishments using Adhesive-bonded Steel | +0.9% | Developed markets | Medium term (2-4 years) | |||

Miniaturised Electronics Requiring Conductive Metal Adhesives Miniaturised Electronics Requiring Conductive Metal Adhesives | +1.1% | APAC core, North America | Short term (≤ 2 years) | |||

Wind-turbine Blade Metal Insert Repairs Wind-turbine Blade Metal Insert Repairs | +0.6% | Europe & North America | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Lightweighting Push in Automotive and Rail

The automotive industry's aggressive pursuit of weight reduction to meet stringent fuel efficiency standards drives unprecedented demand for metal bonding adhesives as alternatives to traditional mechanical fasteners. Automotive Original Equipment Manufacturers (OEMs) now specify structural adhesives as primary joining methods to meet fleet-average CO₂ limits and crash-energy targets. Henkel opened a battery test center in 2024 to validate adhesive designs that cut component weight by up to 50% while boosting impact absorption[1]Henkel Automotive Solutions, “Lightweight Structural Adhesives Portfolio,” henkel.com. Rail car builders follow suit, citing vibration-damping and corrosion-resistance gains over rivets or welds. As regulatory targets tighten, the metal bonding adhesives market embeds itself deeper into multi-material vehicle platforms, expanding content per unit and pulling regional suppliers into global programs.

Growing Adoption in Aerospace Composite-metal Joints

Aerospace manufacturers increasingly turn to metal bonding adhesives to address the complex challenges of joining composite materials to metallic structures, driven by the industry's relentless pursuit of fuel efficiency and performance optimization. Hybrid fuselage and wing designs bond carbon-fiber panels to titanium or aluminum frames, demanding adhesives that survive cryogenic to 400°F cycles. Master Bond’s Supreme 10HT series underpins such joints, offering fuel and hydraulic-fluid resistance. Plasma-activation and etched-primer routines now extend bond life past 60,000 flight hours. Unmanned aerial vehicles, satellites and emerging air-mobility craft widen the addressable domain for specialty grades, sustaining premium pricing within the metal bonding adhesives market.

Infrastructure Refurbishments using Adhesive-bonded Steel

Aging infrastructure across developed economies creates substantial opportunities for metal bonding adhesives in structural rehabilitation projects, where traditional repair methods often prove inadequate or prohibitively expensive. Bridge operators adopt structural epoxies as “cold-applied steel grout” to arrest crevice corrosion without heat-affected zones. The Virginia Department of Transportation demonstrated full-scale success, eliminating lane-closure welding work and lowering lifecycle cost. Rapid-cure chemistries curb downtime on occupied assets, while formulated thixotropy eases overhead application. Stimulus-backed repair budgets in the United States, Canada, Germany, and Japan translate into recurring orders that lift the metal bonding adhesives market beyond new-build reliance.

Miniaturised Electronics Requiring Conductive Metal Adhesives

System-in-package architectures and 3D integrated circuits (ICs) need silver-filled pastes and sintering films that operate at lower reflow windows. MacDermid Alpha’s die-attach materials address these constraints, handling aggressive thermal cycling in AI accelerators and 5G base-stations. Flexible wearables require adhesives that maintain conductivity under bending, propelling R&D into stretchable resin backbones. The electronics segment’s momentum lifts unit volumes at a pace eclipsing mature transport end-markets, diversifying revenue for metal bonding adhesives market participants.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Epoxy and Isocyanate Raw Material Price Volatility Epoxy and Isocyanate Raw Material Price Volatility | -1.4% | Global, acute in APAC | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-1.4%

|

Geographic Relevance

:

Global, acute in APAC

|

Impact Timeline

:

Short term (≤ 2 years)

|

Stricter Global and Regional VOC/emission Limits Stricter Global and Regional VOC/emission Limits | -0.9% | Europe & North America | Medium term (2-4 years) | |||

Low Recyclability of Adhesive-bonded Metal Assemblies Low Recyclability of Adhesive-bonded Metal Assemblies | -0.7% | Europe & North America | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Epoxy and Isocyanate Raw-Material Price Volatility

Raw material price instability significantly constrains metal bonding adhesive market growth, with epoxy resin costs experiencing dramatic fluctuations due to supply chain disruptions and feedstock availability challenges. Feedstock disruptions in 2025 swung epoxy costs up 1.73% in Germany while inventories pushed Asian prices down 1.4% later that month, stalling discretionary projects. European Union (EU) REACH (Registration, Evaluation, Authorization and Restriction of Chemicals) rules on diisocyanates compel costly reformulation or worker-training rollouts. Suppliers hedge volatility by locking multi-year phenol and propylene oxide contracts or integrating upstream, strategies inaccessible to smaller converters. Elevated input risk suppresses short-term order visibility, tempering the metal bonding adhesives market growth outlook.

Stricter Global and Regional VOC / Emission Limits

Increasingly stringent volatile organic compound regulations across major markets create substantial compliance costs and formulation challenges for metal bonding adhesive manufacturers. Canada capped VOC concentrations for 130 adhesive classes in January 2024, mirroring EU ceilings and pending per- and polyfluoroalkyl substances (PFAS) curbs. Reformulation to water-borne or UV-curable systems can lower shear strength or extend cycle time, raising application costs for end-users. Capital-constrained SMEs delay switching, softening near-term uptake. Global convergence of emission rules forecloses compliance arbitrage, compelling a broad pivot that marginally drags the metal bonding adhesives market until next-generation chemistries close the performance gap.

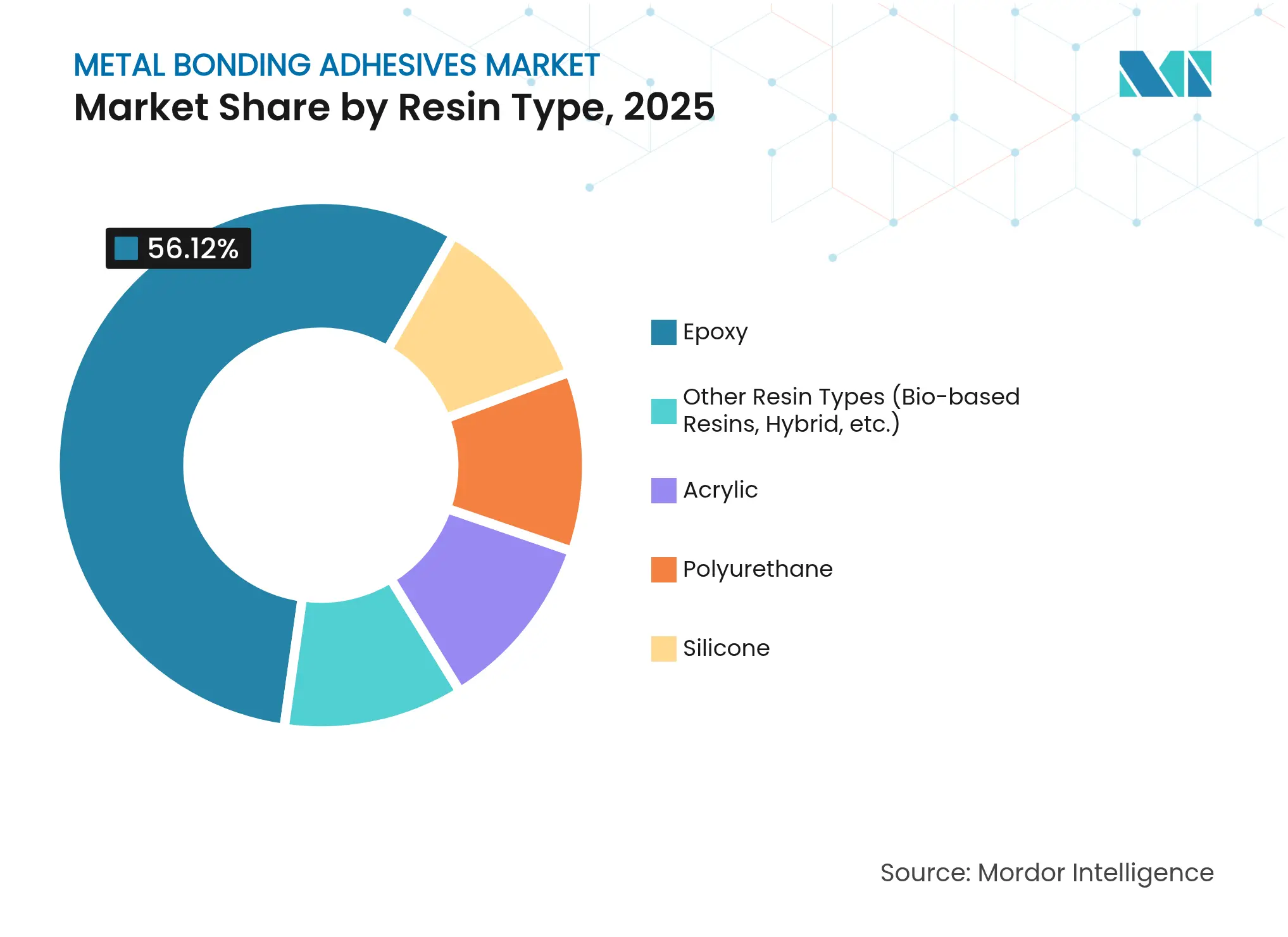

By Resin Type: Epoxy Dominance Faces Sustainable Challenges

Epoxy products delivered 56.12% of the Metal Bonding Adhesives market in 2025, anchored by unrivaled strength, chemical resistance and dimensional stability in aerospace skins, electronics die-attach and structural automotive joints. Polyurethane grades top growth charts at 5.24% CAGR to 2031 thanks to impact tolerance and flexibility demanded in mixed-material car body structures. The metal bonding adhesives market size for epoxy joint solutions is poised to climb steadily, yet pressure mounts as Europe’s diisocyanate curbs trigger migration toward micro-emission polyurethane and bio-based hybrids. Acrylic and silicone chemistries retain niche relevance where fast fixturing or extreme temperature resistance is mandatory. Light-triggered debonding epoxies under incubator trials could unlock closed-loop recyclability, reshaping share allocation beyond 2030.

Polyurethane suppliers bridge sustainability and performance by introducing 60% bio-content products that cut cradle-to-gate CO₂ by the same margin without sacrificing peel strength. Acrylics benefit from solvent-free two-component systems that minimize VOC compliance burdens for prefabricated building producers. Across all chemistries, fillers enabling thermal conductivity and electrical isolation blur traditional segment boundaries, underpinning higher value per kilogram across the metal bonding adhesives market.

Note: Segment shares of all individual segments available upon report purchase

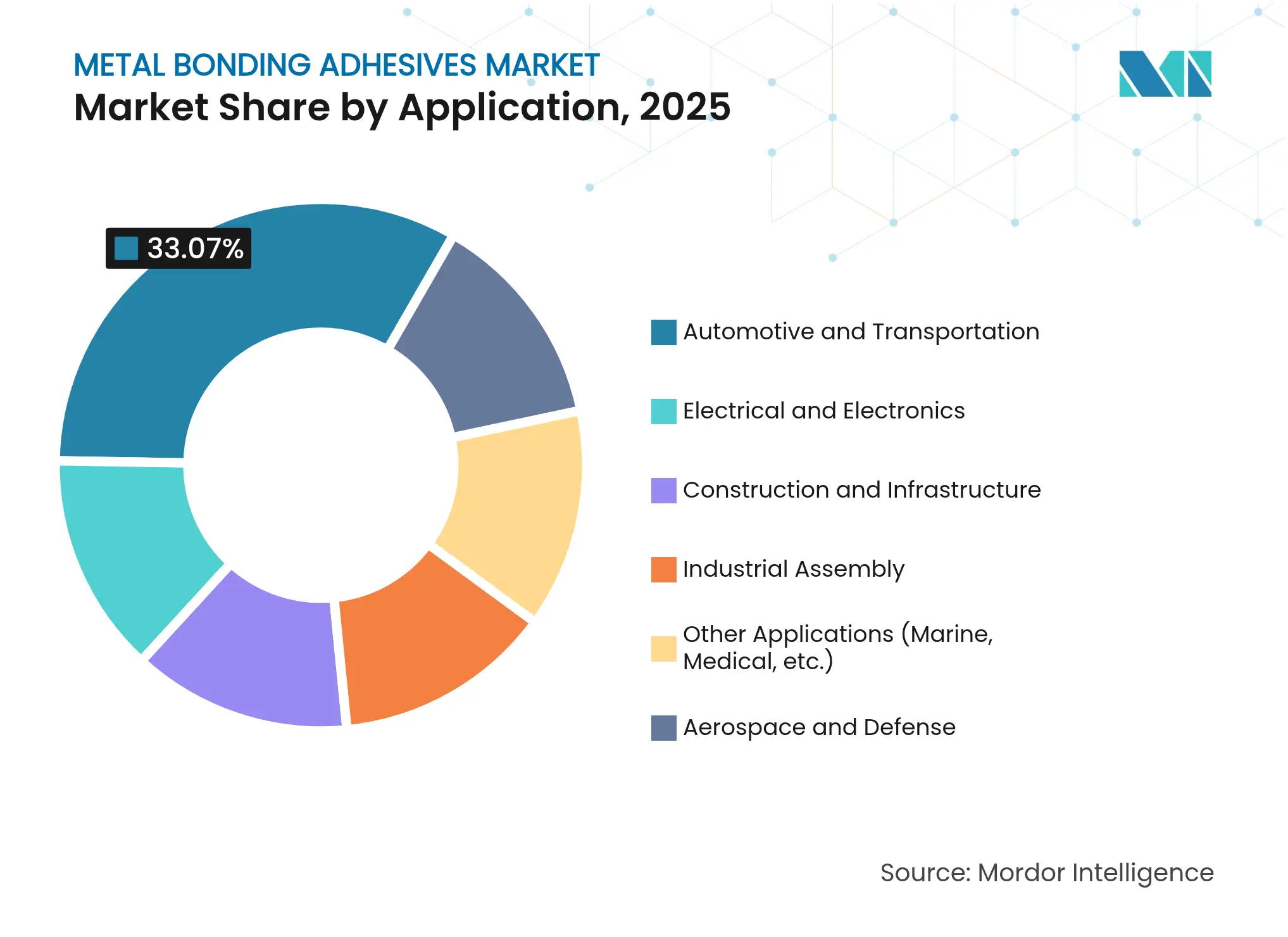

By Application: Electronics Surge Challenges Automotive Leadership

Automotive and transportation still anchors 33.07% of 2025 revenues, yet electrification shifts value pools toward battery-module potting, cell-to-pack gap fillers, and bus-bar bonding. Electronics revenue is rising at 5.52% CAGR, narrowing the gap as smartphones, 5G routers, and artificial intelligence (AI) accelerators require conductive films and underfill adhesives with sub-3 ppm (parts per million) moisture uptake. If adoption curves persist, the metal bonding adhesives market share leader may tilt toward electronics in the next planning cycle.

Industrial assembly, construction, and infrastructure segments leverage structural bonding to replace labor-intensive welding during plant retrofits and building façade upgrades, ensuring a stable baseline for producers. Upside potential resides in aerospace, where twin-aisle backlog and defense programs introduce larger bonded-panel volumes per unit. Medical and marine niches secure premium margins due to regulatory hurdles and harsh environments, albeit contributing modest tonnage to the metal bonding adhesives market size. Cross-learning between EV power-train thermal interfaces and data-center liquid-cooling plates accelerates recipe diversification, fostering incremental sales across multiple verticals.

Note: Segment shares of all individual segments available upon report purchase

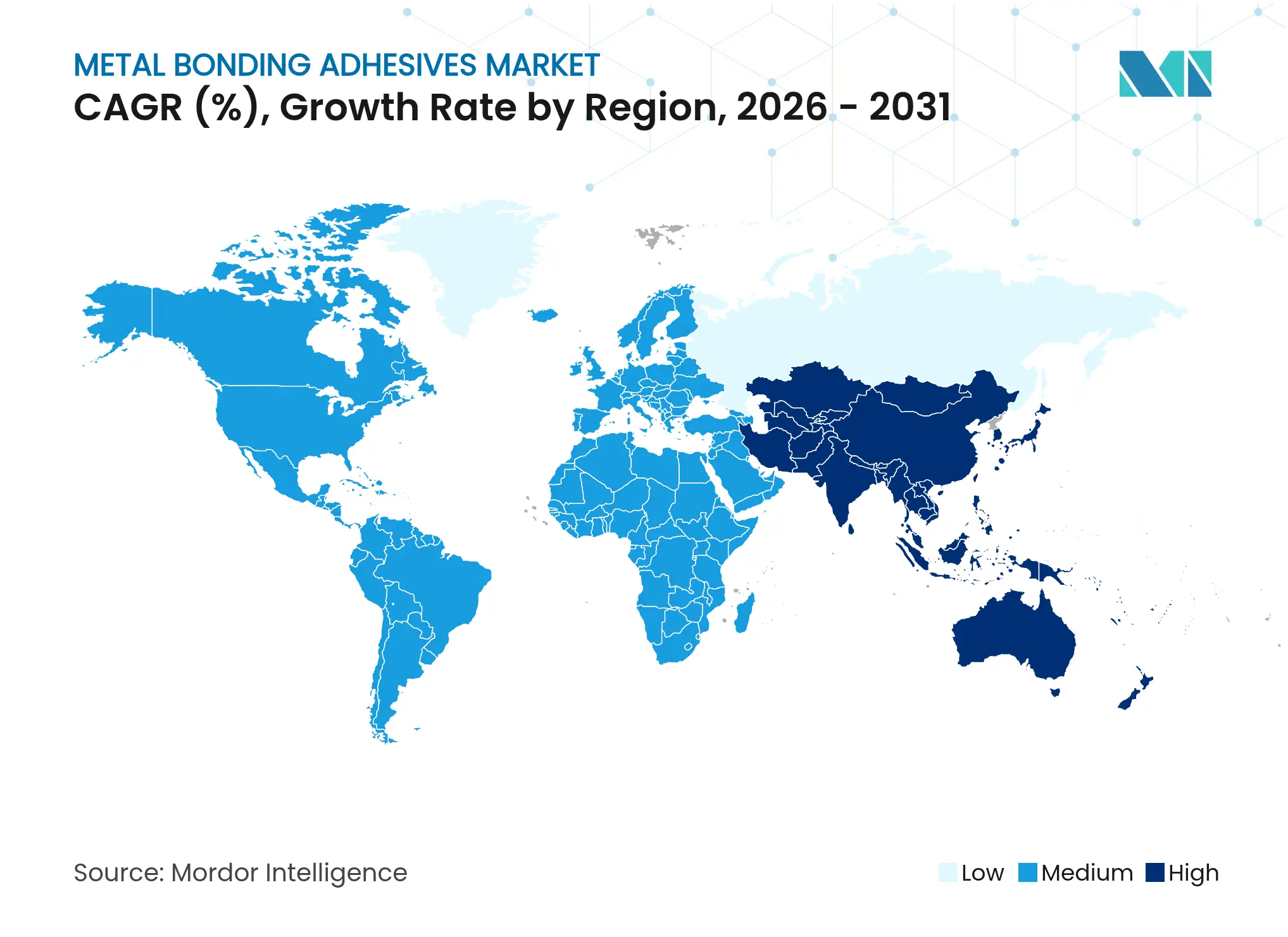

Asia-Pacific commanded 46.31% of global demand in 2025 and is expanding at a 5.63% CAGR as China and India deepen auto production, electronics assembly, and infrastructure modernization. Henkel’s new Loctite complex in Maharashtra and Tesa’s Mumbai and Bengaluru offices shorten lead times and tailor specs for local OEMs. Japan and South Korea sustain high-value electronics uses, paying premiums for ultra-clean, low-outgas grades. Composite aircraft sub-contracting in Malaysia and Thailand builds an additional consumption layer that secures the region’s primacy within the metal bonding adhesives market.

North America follows as a mature yet innovation-driven arena. Aerospace primes specify cryogenic-to (-400)°F epoxies, while EV startups in the United States accelerate trials of fire-retardant battery gap fillers. Canada’s 2024 VOC regulations are spurring early adoption of water-borne chemistries that later percolate into export markets. Federal bridge-rehab grants channel epoxy steel-plate bonding demand, sustaining the metal bonding adhesives market even during automotive model-change pauses.

Europe focuses on sustainability and recyclability. Wind-energy OEMs adopt debond-on-command resins to ease blade-end-of-life processing, reinforcing the region’s leadership in circular economy solutions. Micro-emission polyurethane rollouts comply with post-2023 diisocyanate restrictions, allowing continuous application without costly on-site training programs. Automotive lightweighting and packaging houses demanding PFAS-free electronics grades underpin resilient volumes despite overall regional GDP softness. The confluence of strict regulation and advanced R&D shapes Europe into a bellwether for next-generation trends within the metal bonding adhesives market.

Market Concentration

The Metal Bonding Adhesives market has a moderate concentration, with the presence of Henkel AG & Co. KGaA, 3M, H.B. Fuller Company, Sika AG, and Dow. Henkel, 3M, and Sika harness global technical centers and multi-channel distribution to defend their share. Their vertical integration into key resin precursors insulates margin against volatile phenol, epichlorohydrin, and Methylene Diphenyl Diisocyanate (MDI) streams, while internal incubators fast-track bio-based and debondable platforms. 3M pilots copper-to-copper bonding films for semiconductor mini-LED backplanes, while Sika widens its wind-energy repair toolbox with UV-cure chemistries to trim turbine downtime. Mid-tier rivals pursue specialization. H.B. Fuller broadened medical-device reach via Medifill Ltd. and GEM S.r.l. buys, accessing cyanoacrylate and epoxy syringe systems for catheter and surgical instrument assembly.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts (Value)

6. Competitive Landscape

7. Market Opportunities & Future Outlook

Metal bonding adhesives are high-performance adhesives or chemicals used to join or connect two or more metal surfaces together with a bond that is strong and flexible enough to resist separation when subjected to movements, stress, high temperatures, and other adverse conditions.

The metal bonding adhesives market is segmented by resin type, application, and geography. By resin type, the market is segmented into acrylic, epoxy, polyurethane, silicone, and other resin types (bio-based resins, hybrid, etc.). By application, the market is segmented into automotive and transportation, aerospace and defense, electrical and electronics, industrial assembly, construction and infrastructure, and other applications (marine, medical, etc.). The report also covers the market size and forecasts for the metal bonding adhesives market in 27 countries across major regions.

For each segment, the market sizing and forecasts have been done based on value (USD).

Strategic Expansion of Floor Coatings in the MEIA Region

4 Min Read

Unlocking Supplier Partnerships in the Africa Lubricants Market

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.