Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.46 Billion |

| Market Size (2026) | USD 3.69 Billion |

| Market Size (2031) | USD 5.06 Billion |

| Growth Rate (2026 - 2031) | 6.52% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Adhesives And Sealants Market Analysis by Mordor Intelligence

The India Adhesives and Sealants Market size is expected to grow from USD 3.46 billion in 2025 to USD 3.69 billion in 2026 and is forecast to reach USD 5.06 billion by 2031 at 6.52% CAGR over 2026-2031. This growth reflects a decisive shift from commodity‐grade bonding agents toward engineered solutions driven by performance specifications and regulatory compliance. Construction spending under the National Infrastructure Pipeline, fast-rising e-commerce packaging volumes, and expanding automotive and aerospace assembly lines are lifting demand for high-strength, low-emission formulations. Domestic chemical capacity upgrades shorten supply chains for key resins, while government incentives for local manufacturing favor producers with Indian production footprints. Technology adoption trends show hot-melt, water-borne, and reactive chemistries steadily replacing solvent-borne legacy products as environmental rules tighten[1]Press Information Bureau, “National Infrastructure Pipeline—Sectoral Allocation Update,” pib.gov.in .

Key Report Takeaways

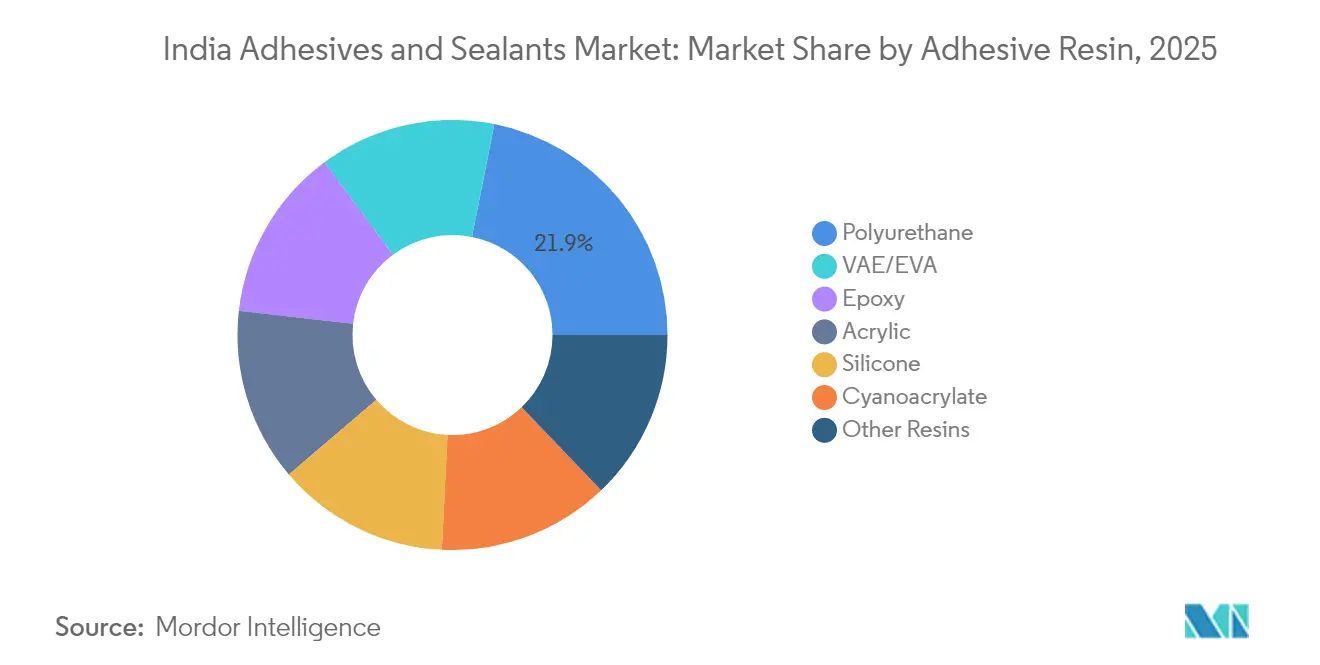

- By adhesive resin, polyurethane led with 21.88% of the India adhesives and sealants market share in 2025; VAE/EVA is projected to grow at a 7.42% CAGR to 2031.

- By adhesive technology, hot-melt captured 36.62% of the India adhesives and sealants market size in 2025 and is forecast to expand at a 6.88% CAGR through 2031.

- By sealant resin, silicone held 44.96% revenue share in 2025, while polyurethane sealants are expected to advance at a 6.63% CAGR by 2031.

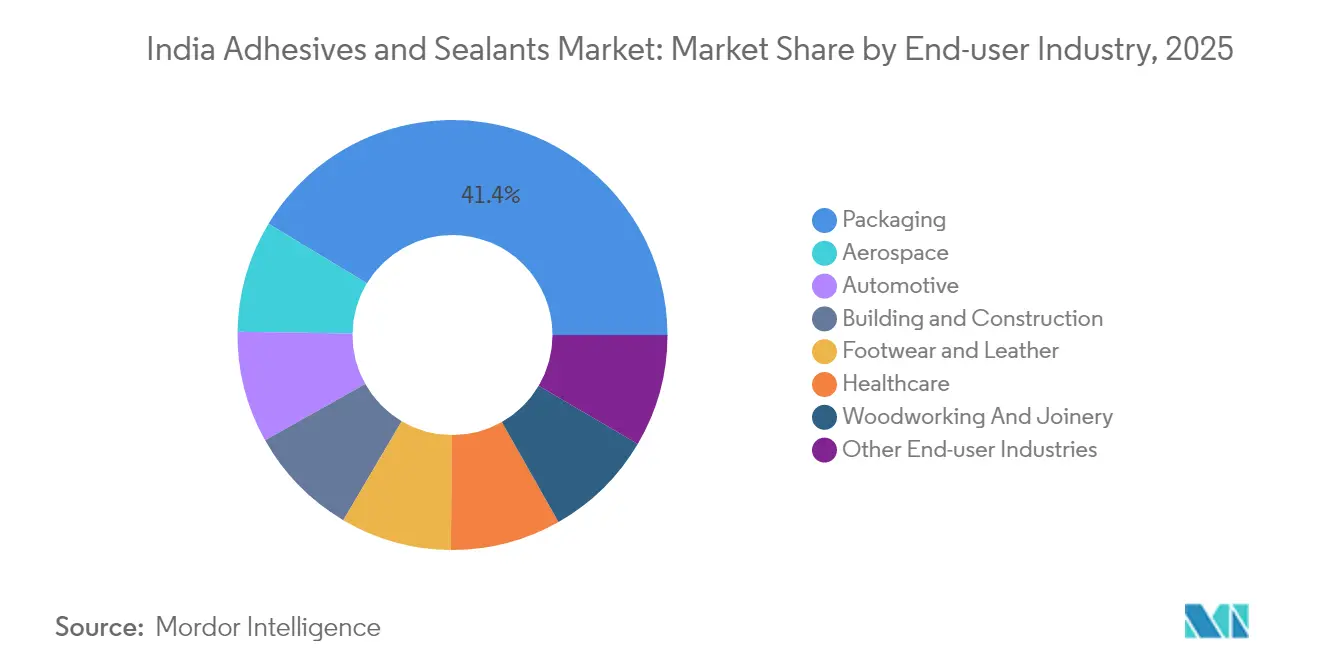

- By end-user industry, packaging accounted for 41.35% share of the India adhesives and sealants market size in 2025; aerospace applications are set to post a 7.01% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Adhesives And Sealants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising residential and infrastructure construction demand | +2.1% | National, with concentration in tier-1 and tier-2 cities | Medium term (2-4 years) |

| Booming e-commerce-led packaging requirements | +1.8% | National, with early gains in Mumbai, Delhi, Bangalore | Short term (≤ 2 years) |

| Automotive lightweighting and localisation push | +1.4% | Western and Southern India manufacturing hubs | Medium term (2-4 years) |

| Woodworking and modular furniture uptake | +0.9% | National, with concentration in Punjab, Karnataka, Tamil Nadu | Long term (≥ 4 years) |

| Make-in-India defence/aerospace offsets fuel high-spec bonding | +0.7% | Bangalore, Hyderabad, Pune aerospace corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Residential and Infrastructure Construction Demand

Infrastructure programs worth USD 120 billion allocated to housing and urban development in 2024 are triggering a spike in construction chemical usage, including structural adhesives, sealants for façade glazing, and energy-efficient building envelope solutions. Modular and prefabricated techniques that rely on factory-applied bonding are gaining favor because they slash on-site labor and accelerate project schedules. Builders also face stricter Bureau of Indian Standards (BIS) requirements, which encourage the adoption of certified, low-VOC bonding systems. Manufacturers with BIS-compliant polyurethane and silicone lines win share by offering on-site technical audits and training services. Demand is particularly strong for weather-resistant sealants that tolerate India’s temperature swings, pushing suppliers to expand research and development centers near major construction hubs in Delhi-NCR and Hyderabad.

Booming E-Commerce-Led Packaging Requirements

Double-digit online retail growth has changed packaging from a cost-center to a brand-protection tool requiring tamper evidence, heat resistance, and recyclability. Flexible packaging converters are scaling up water-borne and solvent-free laminating adhesives, such as UFlex’s pigmented white and wet-lamination systems, to service monthly order runs exceeding 5,000 tonnes. Food-grade migration limits and Extended Producer Responsibility rules favor low-VOC chemistries validated under global food-contact tests. Cold-chain expansion drives the need for sealants that maintain bond strength from –20 °C to 50 °C, while direct-to-consumer shipments fuel the uptake of fast-setting hot-melts that keep corrugated boxes intact over last-mile cycles. Suppliers winning in this space bundle online viscosity monitoring and adhesive usage analytics that cut waste by 8-10%.

Automotive Lightweighting and Localisation Push

Production-Linked Incentive schemes and the Automotive Mission Plan 2047 are localizing electric-vehicle and component lines, spurring demand for structural bonding agents that can join aluminum, magnesium, and carbon-fiber parts without adding weld weight. Henkel’s development of CO₂-based polyurethane polyols shows how sustainability and performance are converging in under-hood and battery applications. Tier-1 suppliers now source silicone gap-fillers and thermally conductive epoxies locally to ensure just-in-time delivery; this trend supports regional adhesive plants in Pune and Chennai. Vehicle makers also specify crash-durable adhesives to meet Bharat NCAP safety targets, raising the bar on shear strength and fatigue life. The India adhesives and sealants market benefits from rising domestic sourcing ratios as OEMs shift from imported to locally certified chemistries.

Woodworking and Modular Furniture Uptake

Urban consumers favor flat-pack and modular furniture that must withstand humidity swings from 30% to 90% without joint failure. BIS emission standards, in force since February 2025, limit formaldehyde release and push plywood and MDF factories to adopt water-borne or hybrid polyurethane dispersions approved for E0 and E1 ratings. Regional clusters in Punjab, Karnataka, and Tamil Nadu provide scale efficiencies, allowing adhesive vendors to run application labs that test bond strength on indigenous hardwood veneers. Export-focused furniture makers demand bio-based additives that help them qualify for eco-label programs in the European Union, creating a premium segment that grows at nearly twice the overall India adhesives and sealants market rate. Suppliers counter price sensitivity by offering bulk-pack hot-melts that cut per-unit cost 12% while reducing downtime.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC and EHS regulations | -1.2% | National, with stricter enforcement in metropolitan areas | Short term (≤ 2 years) |

| Petro-feedstock price volatility | -0.8% | National, affecting all manufacturers | Short term (≤ 2 years) |

| Import-dependency for specialty monomers | -0.6% | National, with higher impact on specialty adhesive manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent VOC and EHS Regulations

The Central Pollution Control Board has lowered allowable VOC thresholds, compelling producers to retrofit lines with regenerative thermal oxidizers and to shift portfolio mix toward water-borne and hot-melt grades. Capital outlays for small firms can reach USD 1 million, reducing operating margins in the near term. Aerospace formulations containing methylene chloride are under global phase-out, creating requalification costs and temporary shortages. Plants in Mumbai and Bangalore have introduced closed-loop solvent recovery to stay compliant, but the added complexity favors multinationals with established environmental engineering teams. End-users meanwhile insist on Safety Data Sheets aligned with GHS version 8, adding further documentation overhead.

Petro-Feedstock Price Volatility

Quarterly swings of 15–20% in isocyanate and acrylic monomer prices undermine cost forecasts and weaken bargaining power with downstream customers. While large producers hedge with long-term naphtha contracts and currency swaps, many mid-tier firms maintain 60-day inventory coverage, tying up working capital and warehouse space. H.B. Fuller noted double-digit raw-material inflation during its 2025 earnings call, leading to price‐rise notifications across multiple adhesive families. Volatility also impacts freight as bunker surcharges pass through to imported feedstocks, widening landed-cost differences between domestic and overseas alternatives. Consequently, procurement teams are collaborating more closely with research and development to design formulations that can tolerate wider feedstock substitutions without performance loss.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Adhesive Resin: Polyurethane Leadership Faces Bio-Based Disruption

Polyurethane accounted for 21.88% of India's adhesives and sealants market share in 2025, underpinned by its ability to bond dissimilar substrates and resist chemicals in construction and automotive joints. Epoxy and acrylic systems follow for applications that demand high-temperature endurance or UV stability. VAE/EVA, though smaller in base, is registering the fastest 7.42% CAGR through 2031 as flexible packaging converters switch to recyclable mono-material films. Market leaders are improving green credentials by incorporating CO₂-captured polyols and plant-oil intermediates, moves that align with brand-owner sustainability scorecards.

Over the forecast window, India's adhesives and sealants market demand shifts toward hybrid polyurethane-silicone blends that combine paintability with weatherability, especially in high-rise glazing. Cyanoacrylates retain niches in electronics, fast repair, and consumer DIY kits owing to instant bonding speeds. Suppliers scaling bio-based feedstocks compete on total cost of ownership by highlighting lower hazardous-waste fees and possible carbon-credit offsets. Formulators that earn BIS certification for their new chemistries are expected to gain quicker specification approvals from real estate and automotive OEMs.

By Adhesive Technology: Hot-Melt Dominance Reflects Sustainability Shift

Hot-melt held 36.62% of India adhesives and sealants market size in 2025 and continues to outpace other platforms with a 6.88% CAGR through 2031. Zero-solvent content, fast set times, and low energy curing make hot-melts ideal for corrugated packaging and hygiene disposables processed at up to 600 units-per-minute. Water-borne emulsions stand second as formulators tune particle size and surfactant systems to approach solvent-borne tack while remaining under 5 g/L VOC.

Solvent-borne volumes decline annually as metro governments tighten plant-air permits, yet remain relevant for leather bonding and certain metal pretreatments requiring deep substrate penetration. Reactive polyurethanes gain traction in windshield bonding, where open time and cure-on-demand deliver assembly flexibility. UV-curable acrylates capture more electronics lines as mini-LED and OLED display makers prioritize precision bonding. Equipment manufacturers responding toIndia'sa adhesives and sealants market trends now bundle melter systems with Industry 4.0 sensors that feed viscosity and temperature data to cloud dashboards, cutting glue consumption 8–12% per shift.

By Sealant Resin: Silicone Supremacy Challenged by Polyurethane Growth

Silicone maintained 44.96% share in 2025 because its weather-proof elasticity protects curtain-wall facades across humid coastal and arid inland climates. New low-modulus formulations reduce stress on laminated glass edges, extending façade life cycles well beyond 25 years. Polyurethane sealants, projected at a 6.63% CAGR, appeal to contractors seeking paintable seams for expansion joints and precast panels. Acrylic latex lines serve interior drywall joints where cost and paintability override extreme weather resistance.

Hybrid silyl-terminated polyether (STP) systems are emerging in the India adhesives and sealants market as they merge silicone elasticity with polyurethane adhesion, eliminating the need for primers on porous concrete. Epoxy-based sealants hold niche usage in chemical bund linings where contact with aggressive solvents is likely. BIS-driven durability tests are elevating minimum performance benchmarks, prompting regional formulators to license European and Japanese hybrid technologies to meet 25% movement capability without losing adhesion under cyclic thermal loads.

By End-User Industry: Packaging Dominance Amid Aerospace Acceleration

Packaging represented 41.35% of India adhesives and sealants market demand in 2025, spanning laminates, carton closing, labels, and specialty flexible pouches. Growth stems from consumer-goods manufacturing clusters in Gujarat and Uttar Pradesh that need FDA-compliant, migration-safe chemistries for food contact. Automated filling lines running 24/7 rely on hot-melts with open times below 1 second, reducing machine stoppages.

Aerospace registers the highest 7.01% CAGR through 2031 as Make-in-India offsets push local assembly of nacelles, radomes, and interiors. Epoxy film adhesives qualified to MIL-specs secure structural panels, while silicone potting compounds insulate avionics. Construction, the second-largest volume user, absorbs moisture-curing polyurethane sealants for joint filling and hybrid adhesives for AAC block installation. Healthcare and hygiene adopters demand low-odor chemistries that clear ISO 10993 cytotoxicity tests, whereas woodworking upgrades to no added formaldehyde adhesives to meet European import rules.

Geography Analysis

Western states led the India adhesives and sealants market in 2024 due to integrated petrochemical complexes in Gujarat and the automotive cluster surrounding Pune. Ready access to isocyanates, acrylics, and silicones shortens supply chains and trims landed costs by about 5% compared with inland regions. Maharashtra’s highway expansion pipeline boosts consumption of pavement joint sealants, while port logistics in Kandla and Mundra ease bulk import of specialty monomers.

Southern India is buoyed by aerospace corridors in Bangalore and Hyderabad that require film and paste adhesives validated to global aviation standards. Electronics exporters in Tamil Nadu raise demand for UV-curable coatings used on printed-circuit boards. Furniture factories in Mysuru and Tiruchirappalli purchase water-borne PVAc at container-load scale, pulling distributors to set up just-in-time depots. The India-UK Free Trade Agreement, ratified in May 2025, reduces tariffs on adhesive products, encouraging producers in Andhra Pradesh’s SEZs to target the UK for private-label hot-melts.

Northern and eastern zones exhibit growth as smart-city and mass-housing schemes take shape in Lucknow, Patna, and Bhubaneswar. Cold-chain warehouses under the PM GatiShakti plan spawn localized demand for polyurethane foam sealants that minimize thermal leakage. Inland players face higher freight on bulk chemicals, yet compensate through lower labor costs and state tax incentives that can trim capital expenditure by 10-12%.

Competitive Landscape

The India adhesives and sealants market is moderately fragmented. Pidilite remains the domestic frontrunner by leveraging a 680,000-outlet dealer network and multi-tier branding that ranges from Fevicol for carpentry to Roff for tile installation. Sika invests in new polyurethane and acrylic sealant lines attached to its Jhagadia complex to serve modular construction clients switching from imported mastics. Competitive strategies center on sustainability, technical service, and digital engagement. Firms publish carbon footprints and offer bio-based options to win OEM scorecard points. Application labs in Mumbai and Bangalore test bond performance on customer substrates within 72 hours, speeding design-in.

India Adhesives And Sealants Industry Leaders

3M

H.B. Fuller Company

Henkel AG & Co. KGaA

Pidilite Industries Ltd.

Sika AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Henkel unveiled a new Application Engineering Center in Chennai, Tamil Nadu, bolstering its Adhesive Technologies division's leadership in the electronics arena.

- July 2024: Henkel inaugurated an Industry 4.0-enabled Loctite adhesives plant expansion in Kurkumbh, Maharashtra, raising domestic output of high-performance grades and attaining LEED Gold certification.

India Adhesives And Sealants Market Report Scope

The India adhesives and sealants market is segmented by adhesive by resins, adhesives by technology, sealants by resin, and the end-user industry. On the basis of Adhesive by Resin, the market is segmented into Polyurethane, Epoxy, Acrylic, Silicone, Cyanoacrylate, VAE/EVA, and Other Resins. By Adhesives by Technology, the market is segmented into Solvent-Borne, Reactive, Hot Melt, and UV Cured Adhesives. By Sealants by Resin, the market is segmented by Polyurethane, Epoxy, Acrylic, Silicone, and Other Resins, and by End-User Industries, the market is segmented into Aerospace, Automotive, Building and Construction, Footwear and Leather, Healthcare, Packaging, Woodworking and Joinery, and Other End-user Industries. The report offers the market sizes and forecasts in revenue (USD million) and in volume (kilotons) for all the above segments. The report offers the market sizes and forecasts in terms of revenue (USD million) and volume (kilotons) for all the above segments.

By Adhesives Resin

| Polyurethane |

| Epoxy |

| Acrylic |

| Silicone |

| Cyanoacrylate |

| VAE / EVA |

| Other Resins |

By Adhesives Technology

| Water-borne |

| Solvent-borne |

| Reactive |

| Hot-Melt |

| UV Cured |

By Sealants Resin

| Silicone |

| Polyurethane |

| Acrylic |

| Epoxy |

| Other Resins |

By End-user Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Footwear and Leather |

| Healthcare |

| Packaging |

| Woodworking And Joinery |

| Other End-user Industries |

| By Adhesives Resin | Polyurethane |

| Epoxy | |

| Acrylic | |

| Silicone | |

| Cyanoacrylate | |

| VAE / EVA | |

| Other Resins | |

| By Adhesives Technology | Water-borne |

| Solvent-borne | |

| Reactive | |

| Hot-Melt | |

| UV Cured | |

| By Sealants Resin | Silicone |

| Polyurethane | |

| Acrylic | |

| Epoxy | |

| Other Resins | |

| By End-user Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Footwear and Leather | |

| Healthcare | |

| Packaging | |

| Woodworking And Joinery | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the expected value of the India adhesives and sealants market in 2031?

It is forecast to reach USD 5.06 billion by 2031.

Which resin type currently leads demand?

Polyurethane holds the top spot with a 21.88% share in 2025.

Which technology shows the fastest growth?

Hot-melt adhesives are projected to grow at a 6.88% CAGR through 2031.

How will packaging demand influence the sector?

Packaging remains the largest end-user, representing 41.35% of 2025 demand and expanding with e-commerce logistics.

What is a key restraint facing producers?

Stricter VOC regulations that push manufacturers toward water-borne and hot-melt solutions.

Where are most new adhesive plants being built?

Western and Southern India attract the bulk of recent capacity additions, particularly around Pune and Bangalore.

Page last updated on: