Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.07 Billion |

| Market Size (2031) | USD 10.69 Billion |

| Growth Rate (2026 - 2031) | 8.63% CAGR |

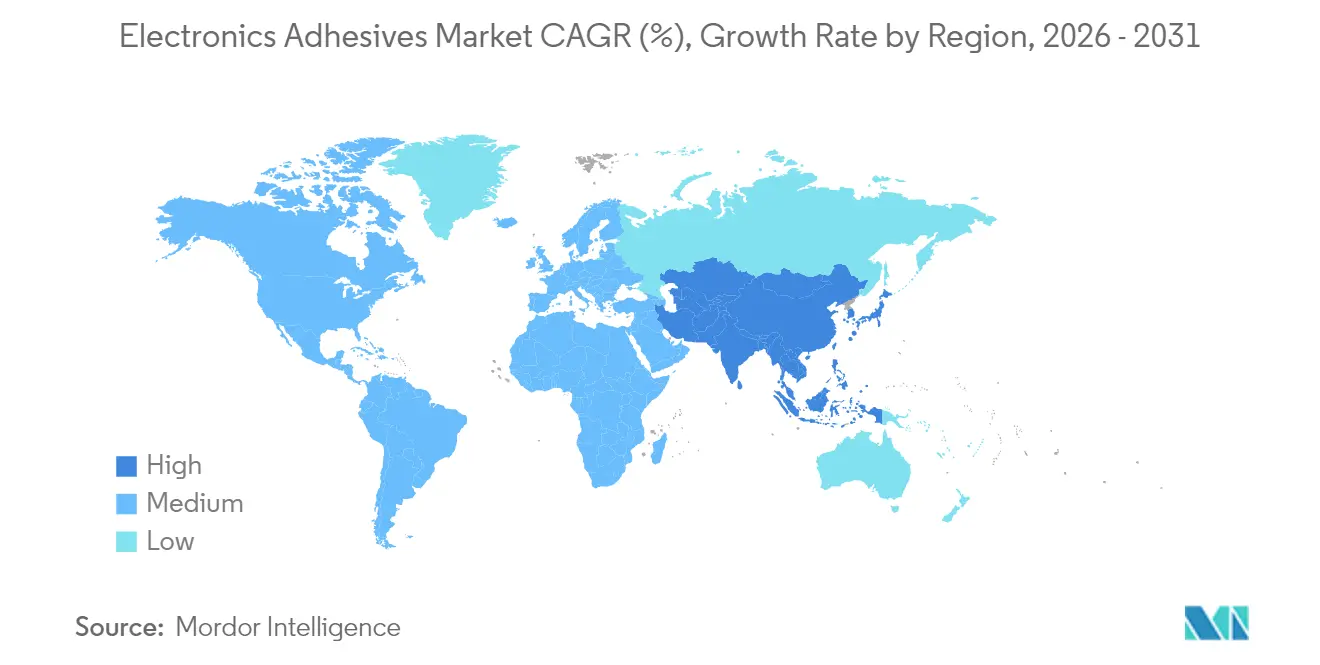

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

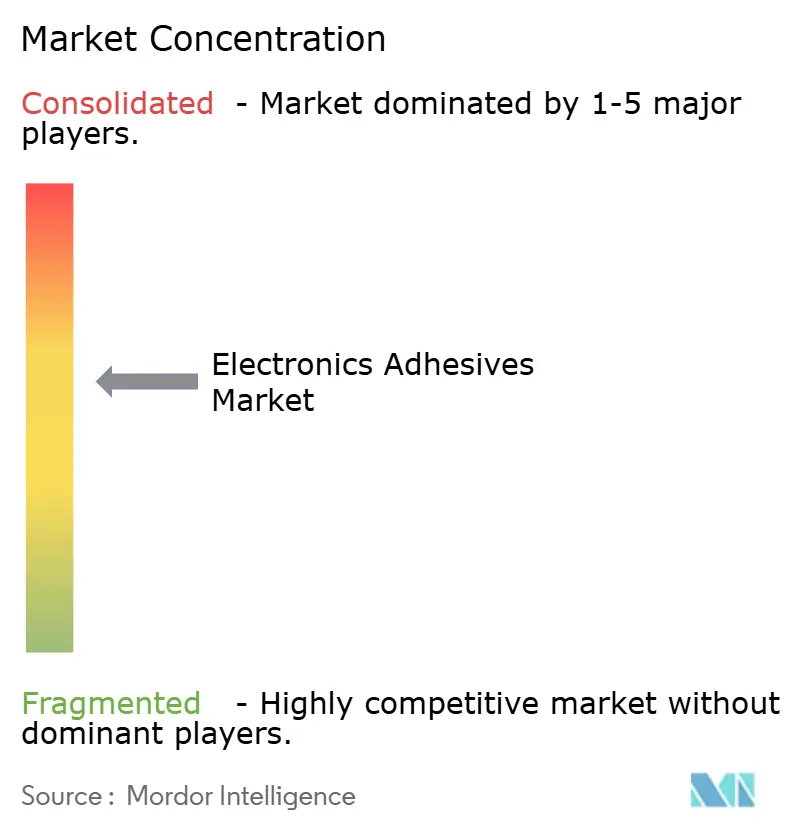

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electronics Adhesives Market Analysis by Mordor Intelligence

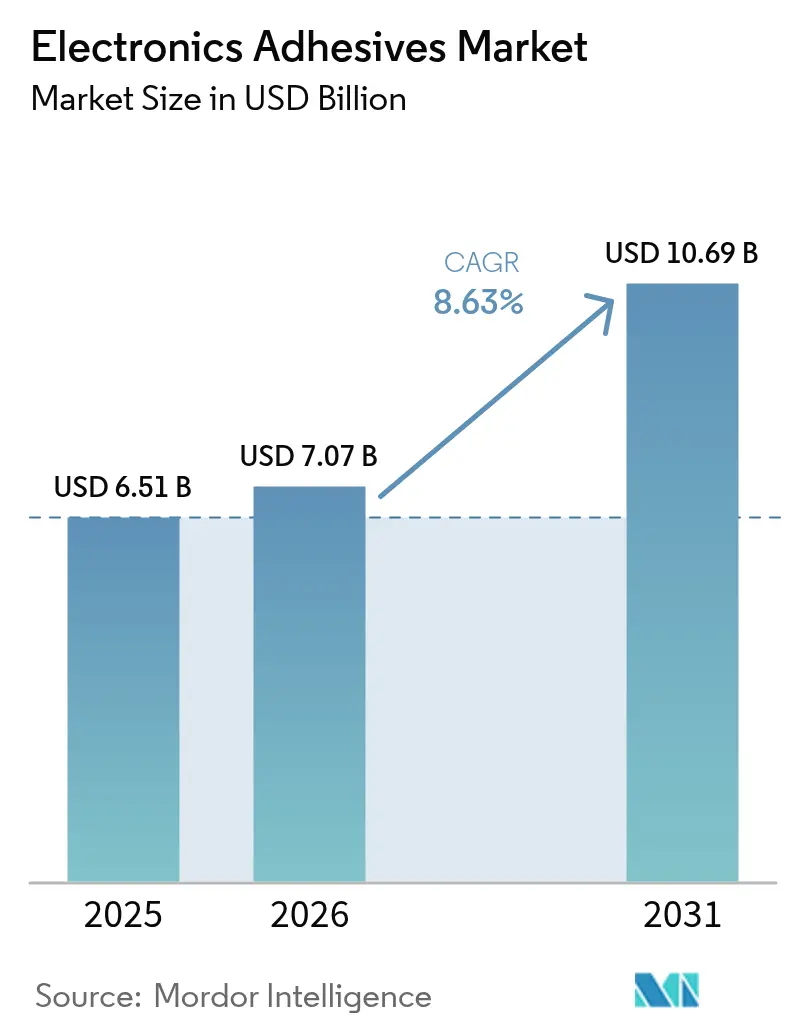

The Electronics Adhesives market size is expected to grow from USD 6.51 billion in 2025 to USD 7.07 billion in 2026 and is forecast to reach USD 10.69 billion by 2031 at 8.63% CAGR over 2026-2031. Rising component miniaturization, wider surface-mount technology (SMT) penetration, and rapid adoption of advanced displays are the primary forces guiding this progress. Demand momentum is reinforced by high-density packaging that increases interconnect counts while amplifying thermal loads, positioning adhesives as indispensable thermal and mechanical buffers between ever-smaller device features. Manufacturers are also prioritizing fast-curing chemistries that cut cycle times in high-volume lines, especially across Asian contract manufacturing hubs. At the same time, sustainability regulations are prompting shifts toward PFAS-free, bio-based, and low-VOC formulations that do not compromise long-term reliability. Taken together, these themes illustrate an electronics adhesives market whose growth is both volume-driven and value-driven, with innovative products commanding share premiums in applications requiring elevated heat resistance and optical purity.

Key Report Takeaways

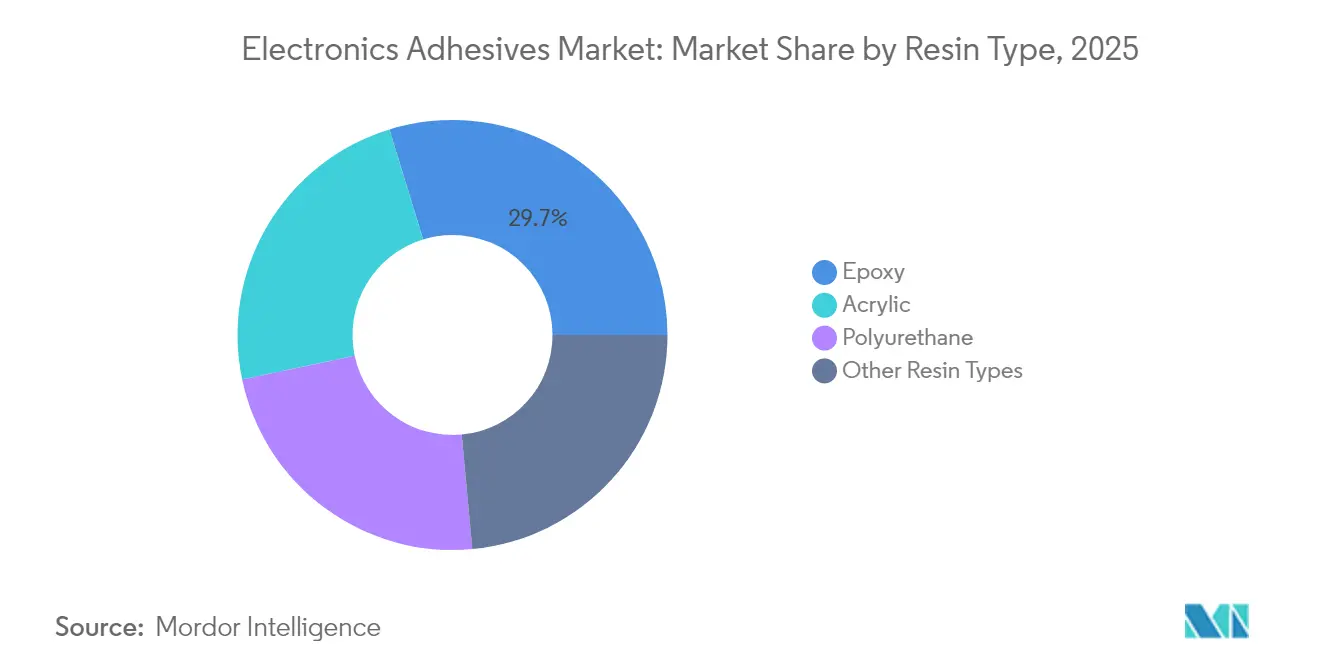

- By resin type, epoxy commanded 29.74% of the electronics adhesives market share in 2025, while acrylic formulations are forecast to expand at an 10.78% CAGR through 2031.

- By product type, electrically conductive grades led with 43.25% revenue contribution in 2025; UV-curing variants are projected to post the fastest 11.42% CAGR to 2031.

- By application, surface mounting captured 39.78% of the electronics adhesives market size in 2025 and is set to advance at an 11.21% CAGR over the outlook period.

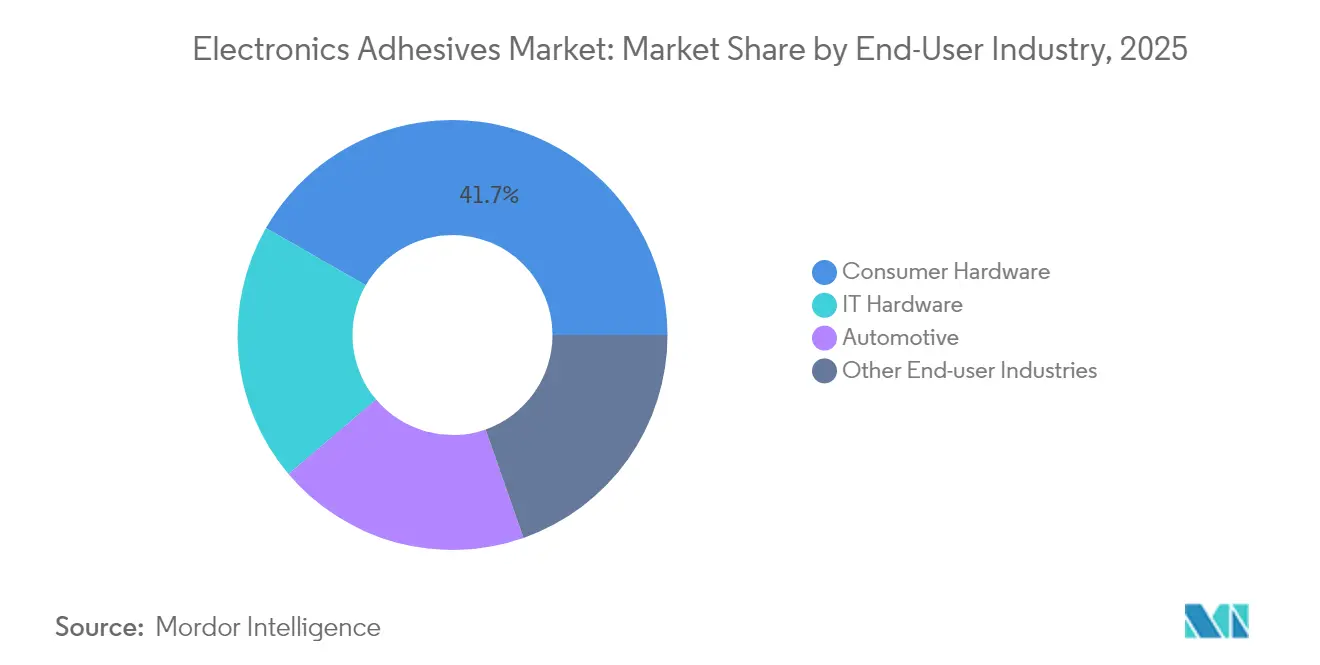

- By end-user industry, consumer hardware held 41.72% share in 2025; other industries, including automotive and industrial automation, are forecast to accelerate at an 10.74% CAGR.

- By geography, Asia-Pacific dominated with a 58.21% share of the electronics adhesives market in 2025 and shows the strongest 10.31% CAGR potential to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electronics Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in high-density packaging | +2.1% | Global, with APAC leading adoption | Medium term (2-4 years) |

| Increase in demand for surface mount technology requiring adhesives | +1.8% | Global, concentrated in electronics manufacturing hubs | Short term (≤ 2 years) |

| Increasing Mini-LED and micro-LED backlighting adoption | +1.5% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Growing technological advancements in electronic adhesives | +1.3% | Global, with R&D centers in developed markets | Long term (≥ 4 years) |

| Expansion of consumer electronics production | +1.2% | APAC dominance, emerging in Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in High-Density Packaging

High-density packaging pushes bond lines toward micron-level tolerances, demanding adhesives with tight-viscosity windows, controlled outgassing, and elastic moduli that absorb differential expansion among stacked die. Wafer-level packaging (WLP) and 3D integration expose joints to reflow excursions that peak near 260 °C, a threshold met by newly formulated epoxy-siloxane hybrids. DELO’s latest wafer-level range sustains that temperature while maintaining flow behavior suitable for precision jetting heads. Robust materials have broadened beyond smartphones into advanced driver-assistance systems (ADAS) control units and compact industrial sensors, both of which mirror consumer device space constraints.

Increase in Demand for Surface-Mount Technology Requiring Adhesives

SMT once filled cost-reduction roles but now enables ultra-fine-pitch assembly where component clearances fall below solder paste tolerances. Underfill adhesives redistribute thermo-mechanical stress in flip-chip packages and arrest tin-whisker propagation, cutting field-failure rates in wearable electronics. Automotive infotainment boards add further requirements for vibration damping and 1,000-hour thermal-cycling durability, elevating demand for specialty epoxy-polyimide blends. Equipment makers respond with high-throughput jet dispensers and dual-stage thermal/UV curing stations that shrink in-line takt times by up to 40%, reinforcing adhesive uptake throughout the electronics adhesives market.

Increasing Mini-LED and Micro-LED Backlighting Adoption

Mini-LED backlights integrate thousands of dies per panel, driving adhesive volumes despite thinning bondlines. Materials must remain optically clear across the visible spectrum and conduct heat away from densely packed emitters. Early adopters in premium televisions report lifetime improvements above 25,000 hours when thermally conductive clear adhesives replace traditional silicone pads. Automotive display suppliers are specifying operating windows from -40 °C to 125 °C, compelling adhesive suppliers to validate cyclical humidity resistance without haze formation.

Growing Technological Advancements in Electronic Adhesives

Debond-on-demand chemistries that release under targeted light or magnetic fields promise modular repair and easier recyclability, aligning with circular-economy frameworks. Hebrew University research teams demonstrated UV-triggered bonds that liquefy under 2.45 GHz microwave exposure, recovering pristine substrates within seconds. Parallel development of bio-based polyhydroxybutyrate (P3HB) adhesives shows tensile strengths above 35 MPa while achieving full biodegradation under industrial composting. Artificial-intelligence modeling shortens formulation cycles, allowing suppliers to screen thousands of monomer combinations virtually before lab scale-up.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in epoxy and acrylate feedstock prices | -1.4% | Global, with acute impact in price-sensitive markets | Short term (≤ 2 years) |

| Stringent VOC and RoHS/REACH compliance costs | -0.9% | Europe and North America primarily | Medium term (2-4 years) |

| Thermal-mismatch failures in ultra-thin flexible substrates | -0.7% | APAC manufacturing centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Epoxy and Acrylate Feedstock Prices

Epichlorohydrin supply disruptions and freight surcharges pushed spot epoxy prices to multi-year highs, crimping gross margins for small formulators. The U.S. International Trade Commission’s ruling against certain Asian epoxy imports introduced additional tariffs that filtered into contract renegotiations within weeks[1]U.S. Federal Register, “Epoxy Resin Tariff Determination,” federalregister.gov. Composite-grade resin producers responded with EUR 150–200 per-ton price hikes, directly raising adhesive cost bases. While top-tier vendors hedge via multi-year supply deals, regional specialists face working-capital strain that may curb innovation pace.

Stringent VOC and RoHS/REACH Compliance Costs

The 2025 REACH update added branched nonylphenyl phosphite to the SVHC list, triggering immediate reformulation work across several legacy product lines. Parallel PFAS legislation in Maine extends broad prohibitions to 2032 yet imposes near-term reporting and labeling duties on electronics sold nationally. European diisocyanate restrictions now require mandatory worker training for handlers of chemistries above 0.1% content, raising compliance overhead on shop-floor operations. Collectively, regulatory shifts divert 5–10% of adhesive R&D budgets toward documentation, toxicology tests, and alternate raw-material screening.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Epoxy Dominance Faces Acrylic Innovation

Epoxy resins remained paramount, accounting for 29.74% of 2025 revenue within the electronics adhesives market. Their high cohesive strength, dielectric stability, and resistance to harsh fluids keep them entrenched in under-the-hood automotive modules and industrial drives. Meanwhile, acrylic chemistries, expanding at an 10.78% CAGR, offer faster light-plus-heat curing and greater substrate flexibility, features prized by smartphone lens-stack bonding. Bio-based epoxy initiatives, leveraging lignin and vegetable-oil derivatives, aim to cut carbon footprints without sacrificing 260 °C peak-temperature capability. Across specialty assembly houses, hybrid epoxy-acrylate blends are gaining traction where manufacturers need snap-cure attributes in a single formulation. This interplay of legacy robustness and emerging agility underscores the diverse formulation roadmap powering the electronics adhesives market.

Second-tier polyurethane systems address vibration-rich settings such as battery modules that face road-surface shocks, whereas silicone and cyanoacrylate niches persist for high-temperature power devices and rapid fixturing. Regulatory attention on bisphenol-A diglycidyl ether is nudging epoxy suppliers toward alternative monomers, yet long-term demand fundamentals remain intact. Manufacturers continue to differentiate through proprietary toughening agents that widen operating windows from -55 °C to 175 °C, thereby cementing epoxy’s leadership even as acrylic volumes accelerate.

By Product Type: Conductive Leadership Meets UV Innovation

Electrically conductive grades delivered 43.25% of 2025 sales, proving indispensable wherever solder voids threaten circuit continuity. Silver-flake epoxies dominate flip-chip die-attach, while nickel-loaded versions offer cost-effective EMI shielding for 5G antennas. UV-curing adhesives, scaling at a 11.42% CAGR, compress line tact times to seconds and enable in-situ optical inspection, elevating first-pass yields in camera module factories. Thermally conductive variants, infused with aluminum nitride or boron nitride fillers, dissipate up to 5 W/mK, extending LED lumen maintenance and inverter uptime.

Non-conductive structural epoxies sustain demand where isolation from high-voltage traces is non-negotiable, notably in traction inverters and data-center power supplies. Hybrid dual-cure products that combine UV pre-gelling with thermal post-cure are emerging as the go-to option for complex three-dimensional assemblies. The breadth of performance profiles available today strengthens the electronics adhesives market, giving designers latitude to optimize electrical, thermal, and optical parameters simultaneously.

By Application: Surface-Mounting’s Dual Dominance

Surface mounting occupied 39.78% of revenue in 2025 and leads growth at 11.21% CAGR, reinforcing its role as both volume anchor and innovation frontier within the electronics adhesives market. Fine-pitch board layouts reaching 01005 passives leave negligible real estate for mechanical standoffs, magnifying adhesive reliance for component retention prior to reflow. Automotive radar units and wearable health trackers share this density mandate, but impose tougher vibration and sweat-resistance specs, directing formulators to elevate cross-link densities and ionic purity.

Conformal coatings follow as the second-largest application class, safeguarding PCBs against condensation and corrosive gases encountered in e-mobility charging stations and offshore wind converters. Encapsulation materials shield power semiconductors from particle ingress, while wire-tacking adhesives simplify harness management in 800 V battery packs. Underfill volumes rise in tandem with flip-chip adoption, delivering uniform stress distribution beneath copper pillar interconnects. Altogether, these varied uses keep the electronics adhesives market closely aligned with advances in electronic assembly methodologies.

By End-User Industry: Consumer Hardware Maturity Meets Industrial Growth

Consumer hardware generated 41.72% of 2025 demand, underscored by annual smartphone refresh cycles that enforce stringent throughput and optical-clarity benchmarks. Tablet cameras, augmented-reality headsets, and wireless earbuds each add micro-bonding challenges that propel premium high-thixotropy adhesives. Nevertheless, automotive, industrial, and medical sectors are expanding faster—collectively grouped under “other industries” and charting an 10.74% CAGR—as they electrify fleets, automate factories, and miniaturize diagnostic sensors.

IT hardware boards for cloud servers employ long-life epoxies capable of 10-year service at 55 °C continuous temperature, supporting data-center uptime commitments. Industrial drives and solar inverters integrate silicone-modified adhesives to endure daily thermal swings while minimizing outgassing that might degrade optical encoders. Medical wearables adopt skin-friendly UV-flexible grades that maintain tack through perspiration cycles. This widening application lattice cements a multi-sector growth flywheel, encouraging suppliers to broaden portfolios and entrench the electronics adhesives market across adjacent value pools.

Geography Analysis

Asia-Pacific contributed 58.21% of 2025 revenue, making it the single largest regional pillar of the electronics adhesives market. Mainland China raised electronics output by 11.3% in 2024 through state grants for advanced packaging lines and local wafer-level underfill capacity expansions. Thailand and Vietnam absorbed fresh foreign direct investment after the United States granted selected tariff exemptions on electronics imports from April 2025, redirecting assembly programs into ASEAN clusters. The region’s integrated supply base—from resin reactors to fully automated SMT lines—compresses lead times and reinforces its cost leadership.

North America’s reshoring narrative gained momentum via the CHIPS and Science Act, which allocates USD 52 billion toward domestic wafer fabrication. This upstream capital outlay is stimulating downstream adhesive demand for clean-room-grade underfills and liquid thermal interface materials. Canada’s Quebec corridor likewise hosts new printed-electronics pilot plants that prioritize bio-based chemistries, mirroring sustainability pushes seen in Europe.

Europe is charting an electronics adhesives market size rebound as its own EU Chips Act strengthens local microelectronic value chains. Environmental regulations, including progressive PFAS limitations, are galvanizing R&D into fluorine-free lubricious fillers. Germany’s automotive Tier 1s are qualifying debondable grades for dashboard displays, while Scandinavian EMS providers emphasize low-temperature curing to shrink energy footprints.

South America and the Middle East and Africa represent emerging frontiers. Brazil’s Manaus free-trade zone is broadening consumer-electronic assembly, opening opportunities for mid-viscosity acrylics tailored to tropical humidity. The United Arab Emirates is positioning itself as a regional logistics hub, pairing free-zone incentives with AI-centered R&D parks that could seed localized adhesive blending plants. Though smaller today, these geographies add diversification prospects for firms eager to de-risk concentration within traditional production centers.

Competitive Landscape

The electronics adhesives industry displays moderate consolidation, with the top five suppliers holding just under 50% of global revenue. Henkel, 3M, and DELO lean on deep application engineering staffs and regional production footprints to sustain incumbency. DELO sets itself apart by channeling 15% of yearly sales into R&D, well above peer averages, and unveiling light-curable epoxies certified for 260 °C peak reflow. Henkel’s “Kunpeng” plant in China, operational from 2025, adds over 100,000 tons of annual output capacity oriented toward electronics, automotive, and aerospace demand[2]European Coatings, “Henkel ‘Kunpeng’ Plant Announcement,” european-coatings.com.

Strategic mergers continue to reshape share positions. Saint-Gobain’s USD 1.025 billion acquisition of FOSROC strengthened its construction chemicals reach but also broadened epoxy synthesis expertise relevant to electronics encapsulants. H.B. Fuller’s Medifill purchase unlocked medical-grade adhesive IP that can be cross-leveraged into wearable biosensor substrates. Patent filings remain brisk; July 2024 saw grants covering aqueous adhesives for inorganic surfaces, epoxy adducts that improve fracture toughness, and graphene-oxide-reinforced two-part cyanoacrylates.

White-space innovation targets debond-on-demand solutions enabling easier product refurbishment. Tesa alone logged more than 50 global applications for magnetic-field-triggered release layers, responding to OEM repairability pledges. Smaller disruptors emerging from academia experiment with electromagnetic adhesives and fully recyclable polymer matrices; many pursue joint-development deals with tier-one suppliers to shortcut commercialization. Region-specific preferences further fragment the playing field: Asian entrants prioritize cost-per-gram competitiveness, whereas European buyers weigh carbon footprints and VOC profiles heavily. This nuanced competitive matrix underscores electronics adhesives market dynamism and the possibility for share shifts when breakthrough chemistries align with tightening sustainability regulations.

Electronics Adhesives Industry Leaders

Henkel AG & Co. KGaA

3M Company

H.B. Fuller Company

Dow Inc.

Sika AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Researchers at Hebrew University developed adhesives that activate through light exposure, requiring only seconds to cure. These adhesives can be broken down using microwave energy, enabling efficient device repair and material recycling processes.

- June 2023: Henkel invested EUR 120 million to construct a new adhesive manufacturing facility in China to increase production capacity for electronics, automotive, and aerospace customers

Global Electronics Adhesives Market Report Scope

Resins such as epoxy, acrylics are used as adhesives in the manufacturing of PCBs and surface mounting of motherboards. Electronics adhesives are widely used in the manufacturing and assembling of electronic circuits and products. They help in the miniaturization of electronic components, and the longstanding trend of reducing the size of electronics is driving the market. The market is segmented by resin type, application, end-user industry, and geography. By resin type, the market is segmented into Epoxy, Acrylics, Polyurethane, and Other Resin Types. By Application, the market is segmented into Conformal Coatings, Surface Mounting, Encapsulation, Wire Tacking, and Other Applications. By end-user industry, the market is segmented into Consumer Hardware, IT Hardware, Automotive, and Other End-user Industries. The report also covers the market size and forecasts for the Electronic Adhesives Market in 16 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of Revenue (USD million).

By Resin Type

| Epoxy |

| Acrylic |

| Polyurethane |

| Other Resin Types (Silicone, Cyanoacrylate, etc.) |

By Product Type

| Electrically Conductive |

| Thermally Conductive |

| UV Curing |

| Other Product Types (Non-conductive, etc.) |

By Application

| Conformal Coating |

| Surface Mounting |

| Encapsulation |

| Wire Tacking |

| Other Applications (Underfill, Die-Attach) |

By End-user Industry

| Consumer Hardware |

| IT Hardware |

| Automotive |

| Other End-user Industries (Industrial and Power Electronics, etc.) |

By Geography

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Resin Type | Epoxy | |

| Acrylic | ||

| Polyurethane | ||

| Other Resin Types (Silicone, Cyanoacrylate, etc.) | ||

| By Product Type | Electrically Conductive | |

| Thermally Conductive | ||

| UV Curing | ||

| Other Product Types (Non-conductive, etc.) | ||

| By Application | Conformal Coating | |

| Surface Mounting | ||

| Encapsulation | ||

| Wire Tacking | ||

| Other Applications (Underfill, Die-Attach) | ||

| By End-user Industry | Consumer Hardware | |

| IT Hardware | ||

| Automotive | ||

| Other End-user Industries (Industrial and Power Electronics, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the electronics adhesives market?

The electronics adhesives market size reached USD 7.07 billion in 2026 and is forecast to climb to USD 10.69 billion by 2031.

How fast is the electronics adhesives market expected to grow?

The market is projected to expand at a robust 8.63% CAGR between 2026 and 2031.

Which region leads the electronics adhesives market and why?

Asia-Pacific commands 58.21% share and shows the fastest 10.31% CAGR, supported by high-volume semiconductor assembly and strong government incentives.

Which resin types dominate and which are growing the quickest?

Epoxy resins held 29.74% share in 2025, while acrylic formulations are expanding fastest at an 10.78% CAGR through 2031.

Why is surface-mount technology crucial for electronics adhesives demand?

Surface-mounting captured 39.78% market share in 2025 and leads growth at an 11.21% CAGR because fine-pitch components and flip-chip designs rely on advanced underfill and bonding chemistries.

Page last updated on: